Financial Analysis of ASX Listed Organisation: QMS Media Report

VerifiedAdded on 2021/06/17

|14

|2276

|24

Report

AI Summary

This report conducts a financial evaluation of QMS Media Limited, an ASX-listed company providing out-of-home advertising and media services. The analysis assesses the company's financial statements over two years, focusing on key financial ratios such as current ratio, quick ratio, gross profit margin, return on equity, and return on assets. The study benchmarks QMS Media against its main competitors, Ooh Media Limited and APN Outdoor Group Limited, to provide a comparative performance analysis. The report indicates that APN Outdoor Group demonstrated superior financial performance. While QMS Media Limited presents potential investment opportunities, the report suggests that future returns might be limited. The analysis includes limitations related to the scope of the financial ratios and external economic factors. The report uses financial data from 2016 and 2017 to analyze the liquidity, profitability, and efficiency of QMS Media Limited and its competitors within the Australian market.

Running head: ACCOUNTING FOR BUSINESS

Accounting for Business

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Accounting for Business

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1ACCOUNTING FOR BUSINESS

Executive Summary:

The purpose of the report is to conduct financial evaluation of an ASX listed

organisation by assessing its financial statements for the previous two years. In this paper,

QMS Media Limited is chosen as the firm that provides out-of-home advertising and media

services in Australia and other global nations. In order to widen the scope of the report, the

financial condition of QMS Media Limited is compared with its two main rivals, Ooh Media

Limited and APN Outdoor Group Limited. It could be inferred that APN Outdoor Group is

the best performing company among the three organisations, as evaluated from the financial

analysis. Even though the investors could earn positive return on investment by investing in

the shares of QMS Media Limited, the returns might be minimised in future.

Executive Summary:

The purpose of the report is to conduct financial evaluation of an ASX listed

organisation by assessing its financial statements for the previous two years. In this paper,

QMS Media Limited is chosen as the firm that provides out-of-home advertising and media

services in Australia and other global nations. In order to widen the scope of the report, the

financial condition of QMS Media Limited is compared with its two main rivals, Ooh Media

Limited and APN Outdoor Group Limited. It could be inferred that APN Outdoor Group is

the best performing company among the three organisations, as evaluated from the financial

analysis. Even though the investors could earn positive return on investment by investing in

the shares of QMS Media Limited, the returns might be minimised in future.

2ACCOUNTING FOR BUSINESS

Table of Contents

1.0 Introduction:.........................................................................................................................3

1.1 Purpose:............................................................................................................................3

1.2 Scope:...............................................................................................................................3

1.3 Limitations:......................................................................................................................3

2.0 Company overview of QMS Media Limited:......................................................................3

3.0 Ratio analysis:......................................................................................................................4

3.1 Current ratio:....................................................................................................................4

3.2 Quick ratio:.......................................................................................................................5

3.3 Gross profit margin:.........................................................................................................6

3.4 Return on equity:..............................................................................................................7

3.5 Return on assets:..............................................................................................................8

4.0 Analysis and comparison of QMS Media Limited with Ooh Media Limited and APN

Outdoor Group:..........................................................................................................................9

References:...............................................................................................................................13

Table of Contents

1.0 Introduction:.........................................................................................................................3

1.1 Purpose:............................................................................................................................3

1.2 Scope:...............................................................................................................................3

1.3 Limitations:......................................................................................................................3

2.0 Company overview of QMS Media Limited:......................................................................3

3.0 Ratio analysis:......................................................................................................................4

3.1 Current ratio:....................................................................................................................4

3.2 Quick ratio:.......................................................................................................................5

3.3 Gross profit margin:.........................................................................................................6

3.4 Return on equity:..............................................................................................................7

3.5 Return on assets:..............................................................................................................8

4.0 Analysis and comparison of QMS Media Limited with Ooh Media Limited and APN

Outdoor Group:..........................................................................................................................9

References:...............................................................................................................................13

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3ACCOUNTING FOR BUSINESS

1.0 Introduction:

1.1 Purpose:

The purpose of the report is to conduct financial evaluation of an ASX listed

organisation by assessing its financial statements for the previous two years. In this paper,

QMS Media Limited is chosen as the firm that provides out-of-home advertising and media

services in Australia and other global nations. The financial evaluation is carried out by

computing five various financial ratios for obtaining an overview of the present standing of

the firm in the operating market of Australia.

1.2 Scope:

In order to widen the scope of the report, the financial condition of QMS Media

Limited is compared with its two main rivals, Ooh Media Limited and APN Outdoor Group

Limited. Three ratios from the above five ratios are used for ascertaining the best performing

company in the market.

1.3 Limitations:

Since this report contains only analysis of certain financial ratios computed, such

ratios could only tell the past performance of the organisation. It would be difficult to predict

the future growth through these ratios, since they ignore the recessionary effects on the global

economy, variations in industrial trends and customer preferences. Moreover, the ratios

computed are for the past two years only, while consideration of another past three additional

years could have improved the analysis further.

2.0 Company overview of QMS Media Limited:

QMS Media Limited is one of the leading outdoor media companies in Australia and

New Zealand. It specialises in providing its clients and agency partners with new and

innovative advertising solutions throughout its premium outdoor media network

(Qmsmedia.com 2018). By using its portfolio of outstanding conventional and digital

billboards in large formats, offerings of exclusive street furniture along with opportunities of

ambient media, it is committed to provide its clients with flexible and tailored outdoor

solutions for delivering solutions. Thus, it provides its clients with engaging and inspiring

campaigns for their target audiences.

1.0 Introduction:

1.1 Purpose:

The purpose of the report is to conduct financial evaluation of an ASX listed

organisation by assessing its financial statements for the previous two years. In this paper,

QMS Media Limited is chosen as the firm that provides out-of-home advertising and media

services in Australia and other global nations. The financial evaluation is carried out by

computing five various financial ratios for obtaining an overview of the present standing of

the firm in the operating market of Australia.

1.2 Scope:

In order to widen the scope of the report, the financial condition of QMS Media

Limited is compared with its two main rivals, Ooh Media Limited and APN Outdoor Group

Limited. Three ratios from the above five ratios are used for ascertaining the best performing

company in the market.

1.3 Limitations:

Since this report contains only analysis of certain financial ratios computed, such

ratios could only tell the past performance of the organisation. It would be difficult to predict

the future growth through these ratios, since they ignore the recessionary effects on the global

economy, variations in industrial trends and customer preferences. Moreover, the ratios

computed are for the past two years only, while consideration of another past three additional

years could have improved the analysis further.

2.0 Company overview of QMS Media Limited:

QMS Media Limited is one of the leading outdoor media companies in Australia and

New Zealand. It specialises in providing its clients and agency partners with new and

innovative advertising solutions throughout its premium outdoor media network

(Qmsmedia.com 2018). By using its portfolio of outstanding conventional and digital

billboards in large formats, offerings of exclusive street furniture along with opportunities of

ambient media, it is committed to provide its clients with flexible and tailored outdoor

solutions for delivering solutions. Thus, it provides its clients with engaging and inspiring

campaigns for their target audiences.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4ACCOUNTING FOR BUSINESS

3.0 Ratio analysis:

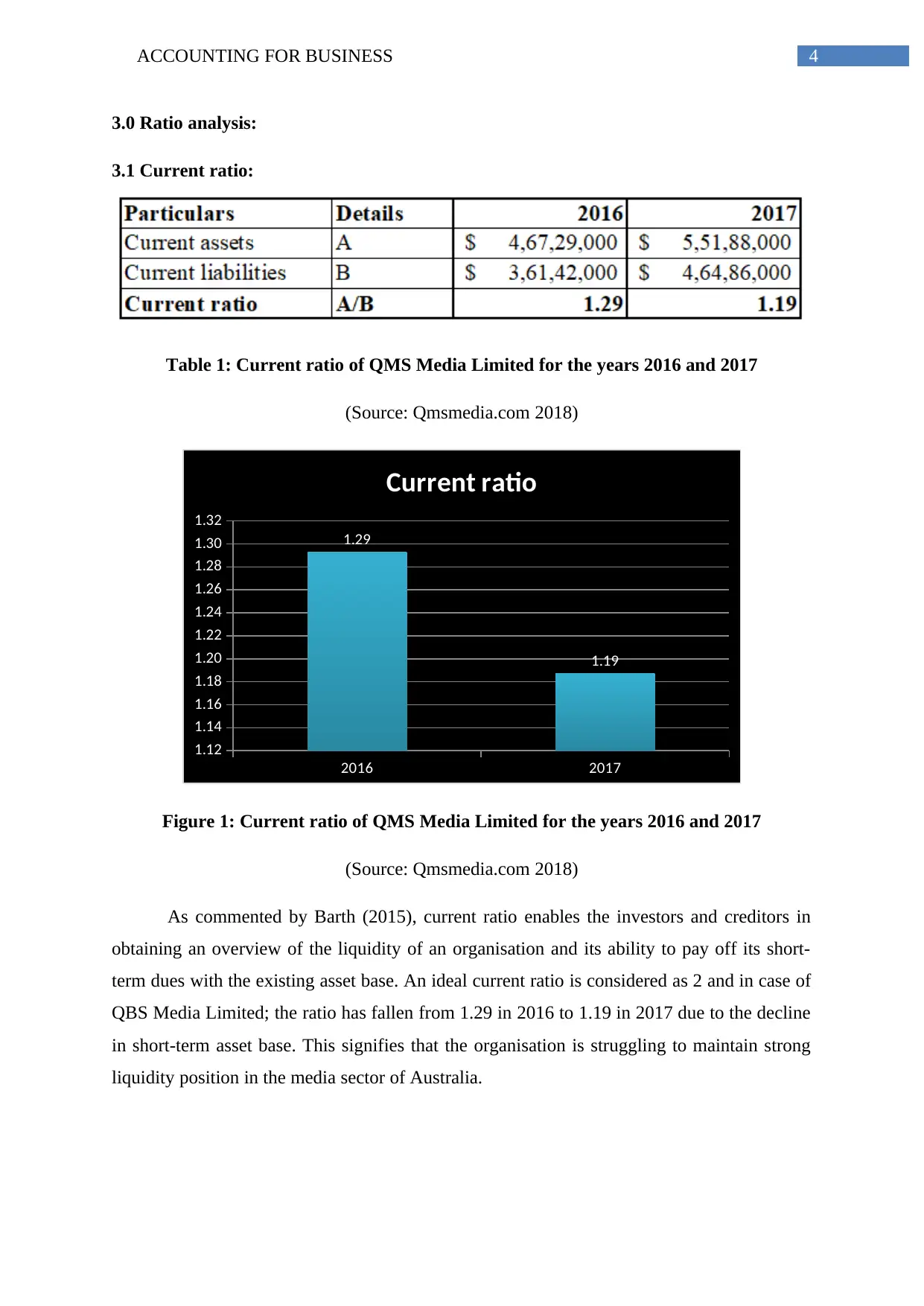

3.1 Current ratio:

Table 1: Current ratio of QMS Media Limited for the years 2016 and 2017

(Source: Qmsmedia.com 2018)

2016 2017

1.12

1.14

1.16

1.18

1.20

1.22

1.24

1.26

1.28

1.30

1.32

1.29

1.19

Current ratio

Figure 1: Current ratio of QMS Media Limited for the years 2016 and 2017

(Source: Qmsmedia.com 2018)

As commented by Barth (2015), current ratio enables the investors and creditors in

obtaining an overview of the liquidity of an organisation and its ability to pay off its short-

term dues with the existing asset base. An ideal current ratio is considered as 2 and in case of

QBS Media Limited; the ratio has fallen from 1.29 in 2016 to 1.19 in 2017 due to the decline

in short-term asset base. This signifies that the organisation is struggling to maintain strong

liquidity position in the media sector of Australia.

3.0 Ratio analysis:

3.1 Current ratio:

Table 1: Current ratio of QMS Media Limited for the years 2016 and 2017

(Source: Qmsmedia.com 2018)

2016 2017

1.12

1.14

1.16

1.18

1.20

1.22

1.24

1.26

1.28

1.30

1.32

1.29

1.19

Current ratio

Figure 1: Current ratio of QMS Media Limited for the years 2016 and 2017

(Source: Qmsmedia.com 2018)

As commented by Barth (2015), current ratio enables the investors and creditors in

obtaining an overview of the liquidity of an organisation and its ability to pay off its short-

term dues with the existing asset base. An ideal current ratio is considered as 2 and in case of

QBS Media Limited; the ratio has fallen from 1.29 in 2016 to 1.19 in 2017 due to the decline

in short-term asset base. This signifies that the organisation is struggling to maintain strong

liquidity position in the media sector of Australia.

5ACCOUNTING FOR BUSINESS

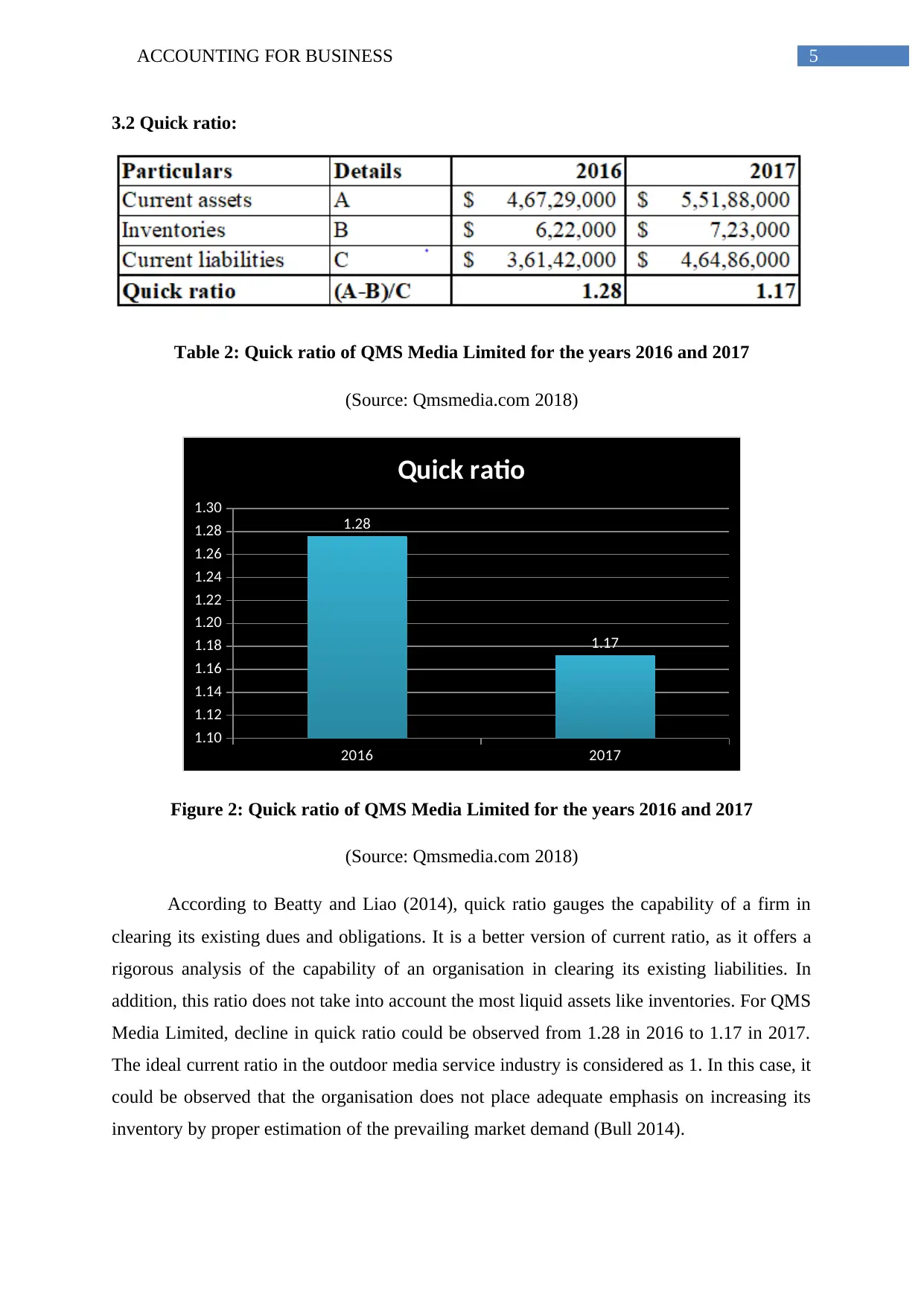

3.2 Quick ratio:

Table 2: Quick ratio of QMS Media Limited for the years 2016 and 2017

(Source: Qmsmedia.com 2018)

2016 2017

1.10

1.12

1.14

1.16

1.18

1.20

1.22

1.24

1.26

1.28

1.30

1.28

1.17

Quick ratio

Figure 2: Quick ratio of QMS Media Limited for the years 2016 and 2017

(Source: Qmsmedia.com 2018)

According to Beatty and Liao (2014), quick ratio gauges the capability of a firm in

clearing its existing dues and obligations. It is a better version of current ratio, as it offers a

rigorous analysis of the capability of an organisation in clearing its existing liabilities. In

addition, this ratio does not take into account the most liquid assets like inventories. For QMS

Media Limited, decline in quick ratio could be observed from 1.28 in 2016 to 1.17 in 2017.

The ideal current ratio in the outdoor media service industry is considered as 1. In this case, it

could be observed that the organisation does not place adequate emphasis on increasing its

inventory by proper estimation of the prevailing market demand (Bull 2014).

3.2 Quick ratio:

Table 2: Quick ratio of QMS Media Limited for the years 2016 and 2017

(Source: Qmsmedia.com 2018)

2016 2017

1.10

1.12

1.14

1.16

1.18

1.20

1.22

1.24

1.26

1.28

1.30

1.28

1.17

Quick ratio

Figure 2: Quick ratio of QMS Media Limited for the years 2016 and 2017

(Source: Qmsmedia.com 2018)

According to Beatty and Liao (2014), quick ratio gauges the capability of a firm in

clearing its existing dues and obligations. It is a better version of current ratio, as it offers a

rigorous analysis of the capability of an organisation in clearing its existing liabilities. In

addition, this ratio does not take into account the most liquid assets like inventories. For QMS

Media Limited, decline in quick ratio could be observed from 1.28 in 2016 to 1.17 in 2017.

The ideal current ratio in the outdoor media service industry is considered as 1. In this case, it

could be observed that the organisation does not place adequate emphasis on increasing its

inventory by proper estimation of the prevailing market demand (Bull 2014).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6ACCOUNTING FOR BUSINESS

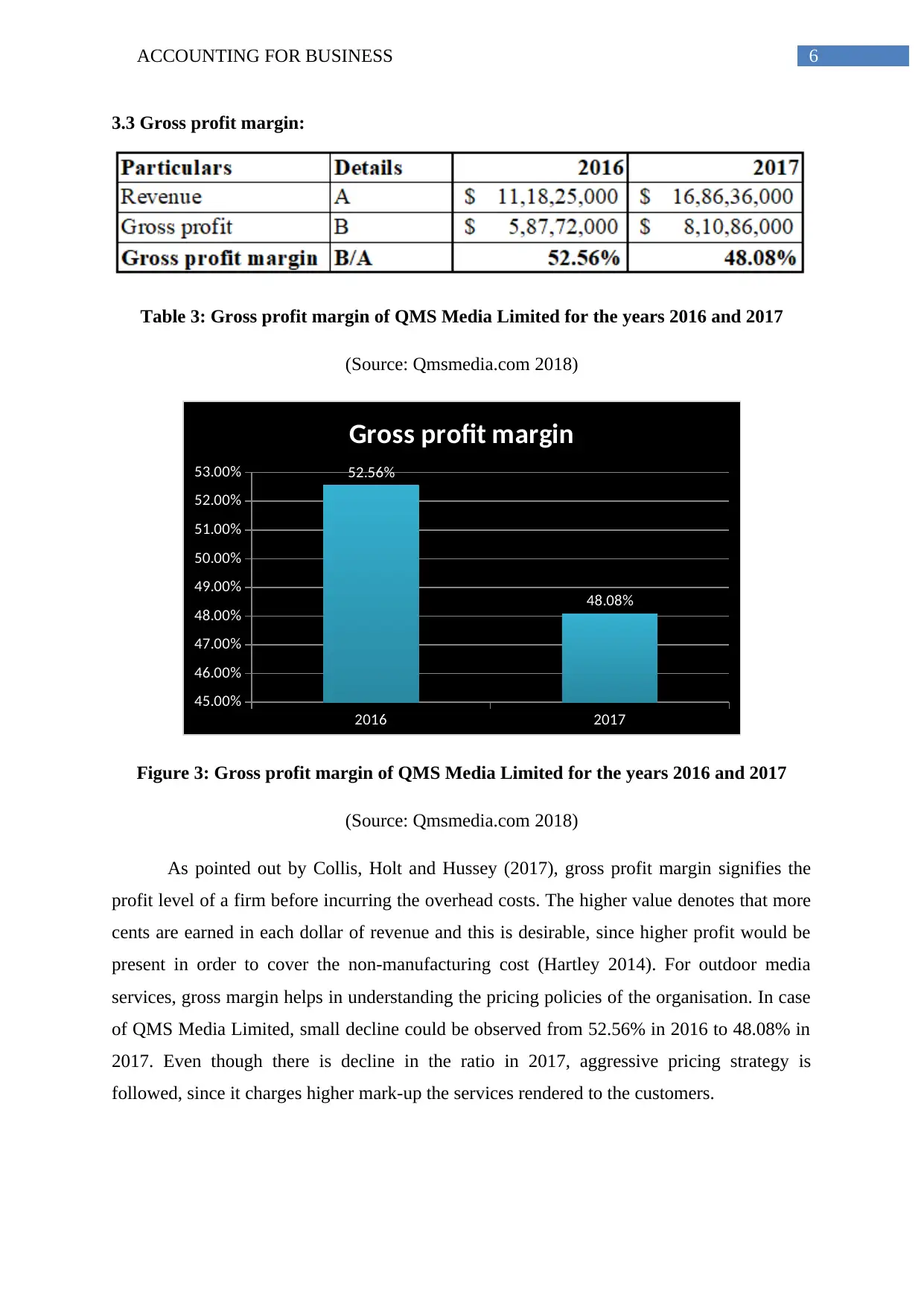

3.3 Gross profit margin:

Table 3: Gross profit margin of QMS Media Limited for the years 2016 and 2017

(Source: Qmsmedia.com 2018)

2016 2017

45.00%

46.00%

47.00%

48.00%

49.00%

50.00%

51.00%

52.00%

53.00% 52.56%

48.08%

Gross profit margin

Figure 3: Gross profit margin of QMS Media Limited for the years 2016 and 2017

(Source: Qmsmedia.com 2018)

As pointed out by Collis, Holt and Hussey (2017), gross profit margin signifies the

profit level of a firm before incurring the overhead costs. The higher value denotes that more

cents are earned in each dollar of revenue and this is desirable, since higher profit would be

present in order to cover the non-manufacturing cost (Hartley 2014). For outdoor media

services, gross margin helps in understanding the pricing policies of the organisation. In case

of QMS Media Limited, small decline could be observed from 52.56% in 2016 to 48.08% in

2017. Even though there is decline in the ratio in 2017, aggressive pricing strategy is

followed, since it charges higher mark-up the services rendered to the customers.

3.3 Gross profit margin:

Table 3: Gross profit margin of QMS Media Limited for the years 2016 and 2017

(Source: Qmsmedia.com 2018)

2016 2017

45.00%

46.00%

47.00%

48.00%

49.00%

50.00%

51.00%

52.00%

53.00% 52.56%

48.08%

Gross profit margin

Figure 3: Gross profit margin of QMS Media Limited for the years 2016 and 2017

(Source: Qmsmedia.com 2018)

As pointed out by Collis, Holt and Hussey (2017), gross profit margin signifies the

profit level of a firm before incurring the overhead costs. The higher value denotes that more

cents are earned in each dollar of revenue and this is desirable, since higher profit would be

present in order to cover the non-manufacturing cost (Hartley 2014). For outdoor media

services, gross margin helps in understanding the pricing policies of the organisation. In case

of QMS Media Limited, small decline could be observed from 52.56% in 2016 to 48.08% in

2017. Even though there is decline in the ratio in 2017, aggressive pricing strategy is

followed, since it charges higher mark-up the services rendered to the customers.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7ACCOUNTING FOR BUSINESS

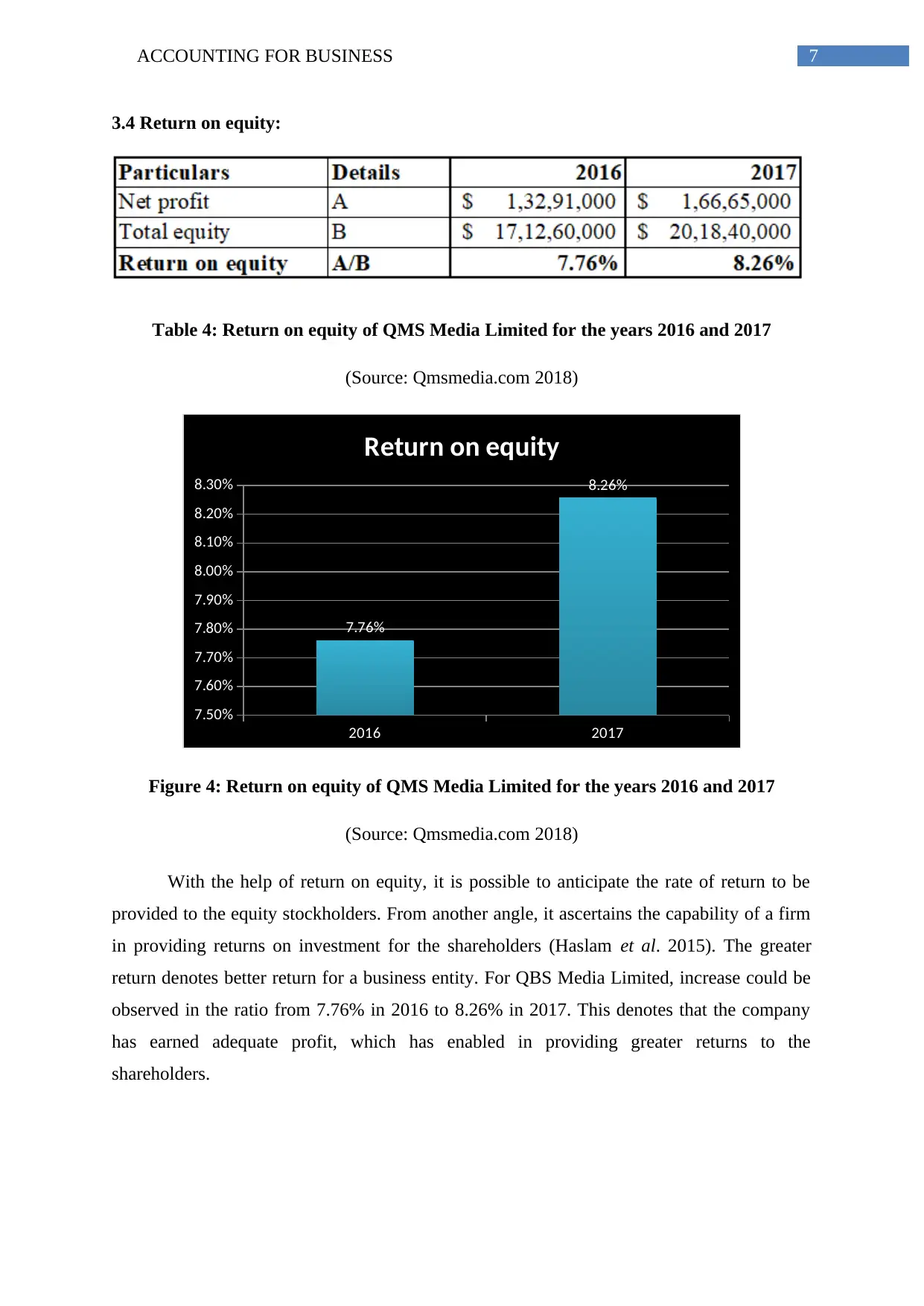

3.4 Return on equity:

Table 4: Return on equity of QMS Media Limited for the years 2016 and 2017

(Source: Qmsmedia.com 2018)

2016 2017

7.50%

7.60%

7.70%

7.80%

7.90%

8.00%

8.10%

8.20%

8.30%

7.76%

8.26%

Return on equity

Figure 4: Return on equity of QMS Media Limited for the years 2016 and 2017

(Source: Qmsmedia.com 2018)

With the help of return on equity, it is possible to anticipate the rate of return to be

provided to the equity stockholders. From another angle, it ascertains the capability of a firm

in providing returns on investment for the shareholders (Haslam et al. 2015). The greater

return denotes better return for a business entity. For QBS Media Limited, increase could be

observed in the ratio from 7.76% in 2016 to 8.26% in 2017. This denotes that the company

has earned adequate profit, which has enabled in providing greater returns to the

shareholders.

3.4 Return on equity:

Table 4: Return on equity of QMS Media Limited for the years 2016 and 2017

(Source: Qmsmedia.com 2018)

2016 2017

7.50%

7.60%

7.70%

7.80%

7.90%

8.00%

8.10%

8.20%

8.30%

7.76%

8.26%

Return on equity

Figure 4: Return on equity of QMS Media Limited for the years 2016 and 2017

(Source: Qmsmedia.com 2018)

With the help of return on equity, it is possible to anticipate the rate of return to be

provided to the equity stockholders. From another angle, it ascertains the capability of a firm

in providing returns on investment for the shareholders (Haslam et al. 2015). The greater

return denotes better return for a business entity. For QBS Media Limited, increase could be

observed in the ratio from 7.76% in 2016 to 8.26% in 2017. This denotes that the company

has earned adequate profit, which has enabled in providing greater returns to the

shareholders.

8ACCOUNTING FOR BUSINESS

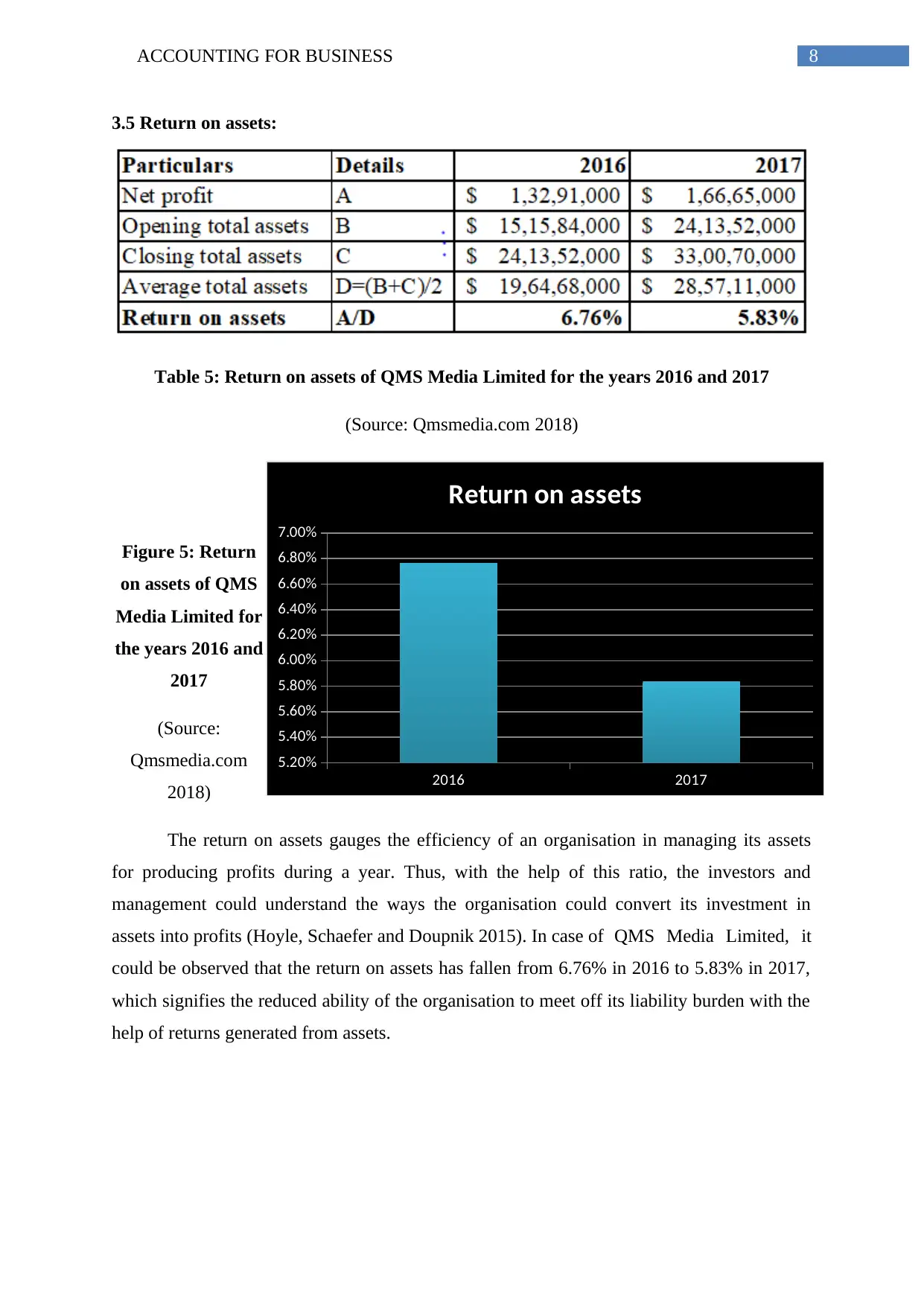

3.5 Return on assets:

Table 5: Return on assets of QMS Media Limited for the years 2016 and 2017

(Source: Qmsmedia.com 2018)

Figure 5: Return

on assets of QMS

Media Limited for

the years 2016 and

2017

(Source:

Qmsmedia.com

2018)

The return on assets gauges the efficiency of an organisation in managing its assets

for producing profits during a year. Thus, with the help of this ratio, the investors and

management could understand the ways the organisation could convert its investment in

assets into profits (Hoyle, Schaefer and Doupnik 2015). In case of QMS Media Limited, it

could be observed that the return on assets has fallen from 6.76% in 2016 to 5.83% in 2017,

which signifies the reduced ability of the organisation to meet off its liability burden with the

help of returns generated from assets.

2016 2017

5.20%

5.40%

5.60%

5.80%

6.00%

6.20%

6.40%

6.60%

6.80%

7.00%

6.76%

5.83%

Return on assets

3.5 Return on assets:

Table 5: Return on assets of QMS Media Limited for the years 2016 and 2017

(Source: Qmsmedia.com 2018)

Figure 5: Return

on assets of QMS

Media Limited for

the years 2016 and

2017

(Source:

Qmsmedia.com

2018)

The return on assets gauges the efficiency of an organisation in managing its assets

for producing profits during a year. Thus, with the help of this ratio, the investors and

management could understand the ways the organisation could convert its investment in

assets into profits (Hoyle, Schaefer and Doupnik 2015). In case of QMS Media Limited, it

could be observed that the return on assets has fallen from 6.76% in 2016 to 5.83% in 2017,

which signifies the reduced ability of the organisation to meet off its liability burden with the

help of returns generated from assets.

2016 2017

5.20%

5.40%

5.60%

5.80%

6.00%

6.20%

6.40%

6.60%

6.80%

7.00%

6.76%

5.83%

Return on assets

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9ACCOUNTING FOR BUSINESS

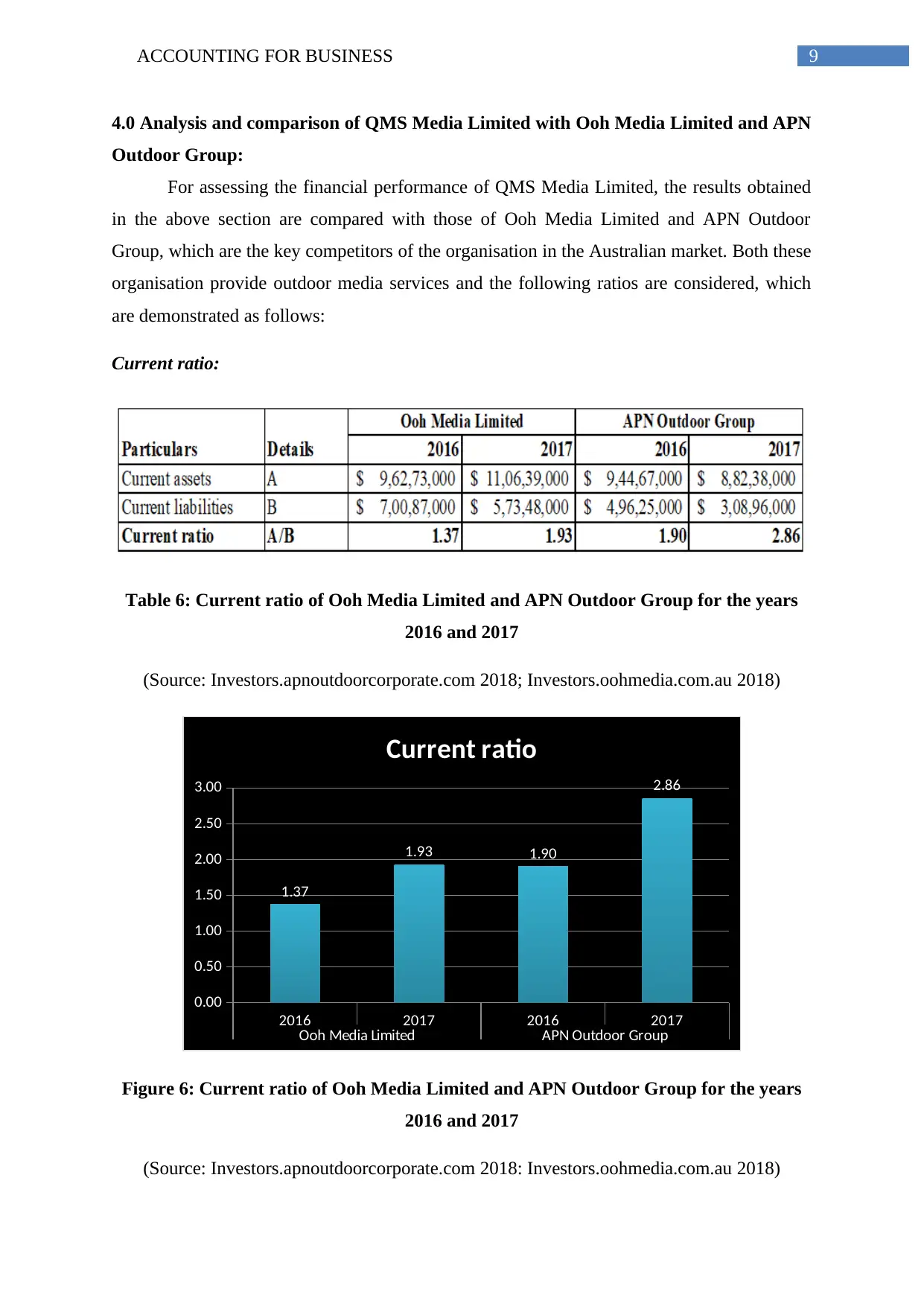

4.0 Analysis and comparison of QMS Media Limited with Ooh Media Limited and APN

Outdoor Group:

For assessing the financial performance of QMS Media Limited, the results obtained

in the above section are compared with those of Ooh Media Limited and APN Outdoor

Group, which are the key competitors of the organisation in the Australian market. Both these

organisation provide outdoor media services and the following ratios are considered, which

are demonstrated as follows:

Current ratio:

Table 6: Current ratio of Ooh Media Limited and APN Outdoor Group for the years

2016 and 2017

(Source: Investors.apnoutdoorcorporate.com 2018; Investors.oohmedia.com.au 2018)

2016 2017 2016 2017

Ooh Media Limited APN Outdoor Group

0.00

0.50

1.00

1.50

2.00

2.50

3.00

1.37

1.93 1.90

2.86

Current ratio

Figure 6: Current ratio of Ooh Media Limited and APN Outdoor Group for the years

2016 and 2017

(Source: Investors.apnoutdoorcorporate.com 2018: Investors.oohmedia.com.au 2018)

4.0 Analysis and comparison of QMS Media Limited with Ooh Media Limited and APN

Outdoor Group:

For assessing the financial performance of QMS Media Limited, the results obtained

in the above section are compared with those of Ooh Media Limited and APN Outdoor

Group, which are the key competitors of the organisation in the Australian market. Both these

organisation provide outdoor media services and the following ratios are considered, which

are demonstrated as follows:

Current ratio:

Table 6: Current ratio of Ooh Media Limited and APN Outdoor Group for the years

2016 and 2017

(Source: Investors.apnoutdoorcorporate.com 2018; Investors.oohmedia.com.au 2018)

2016 2017 2016 2017

Ooh Media Limited APN Outdoor Group

0.00

0.50

1.00

1.50

2.00

2.50

3.00

1.37

1.93 1.90

2.86

Current ratio

Figure 6: Current ratio of Ooh Media Limited and APN Outdoor Group for the years

2016 and 2017

(Source: Investors.apnoutdoorcorporate.com 2018: Investors.oohmedia.com.au 2018)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10ACCOUNTING FOR BUSINESS

The above figure clearly inherits the fact that the current ratio for both the

organisations have increased significantly for both the organisations A higher ratio above 2

indicates that there is adequate amount of idle working capital and in case of APN Outdoor

Group, it has restricted its ability to reinvest in business operations or expansion of capital

projects., while Ooh Media Limited is enjoying better position in the market (Warren and

Jones 2018).

Gross profit margin:

Table 7: Gross profit margin of Ooh Media Limited and APN Outdoor Group for the

years 2016 and 2017

(Source: Investors.apnoutdoorcorporate.com 2018; Investors.oohmedia.com.au 2018)

2016 2017 2016 2017

Ooh Media Limited APN Outdoor Group

0.00%

20.00%

40.00%

60.00%

80.00%

100.00%

120.00%

43.12% 46.16%

97.83% 97.85%

Gross profit margin

Figure 7: Gross profit margin of Ooh Media Limited and APN Outdoor Group for the

years 2016 and 2017

(Source: Investors.apnoutdoorcorporate.com 2018; Investors.oohmedia.com.au 2018)

The above figure clearly states that APN Outdoor Group has the highest profit margin

compared to the other two companies due to the adoption of lower pricing strategy and cost

The above figure clearly inherits the fact that the current ratio for both the

organisations have increased significantly for both the organisations A higher ratio above 2

indicates that there is adequate amount of idle working capital and in case of APN Outdoor

Group, it has restricted its ability to reinvest in business operations or expansion of capital

projects., while Ooh Media Limited is enjoying better position in the market (Warren and

Jones 2018).

Gross profit margin:

Table 7: Gross profit margin of Ooh Media Limited and APN Outdoor Group for the

years 2016 and 2017

(Source: Investors.apnoutdoorcorporate.com 2018; Investors.oohmedia.com.au 2018)

2016 2017 2016 2017

Ooh Media Limited APN Outdoor Group

0.00%

20.00%

40.00%

60.00%

80.00%

100.00%

120.00%

43.12% 46.16%

97.83% 97.85%

Gross profit margin

Figure 7: Gross profit margin of Ooh Media Limited and APN Outdoor Group for the

years 2016 and 2017

(Source: Investors.apnoutdoorcorporate.com 2018; Investors.oohmedia.com.au 2018)

The above figure clearly states that APN Outdoor Group has the highest profit margin

compared to the other two companies due to the adoption of lower pricing strategy and cost

11ACCOUNTING FOR BUSINESS

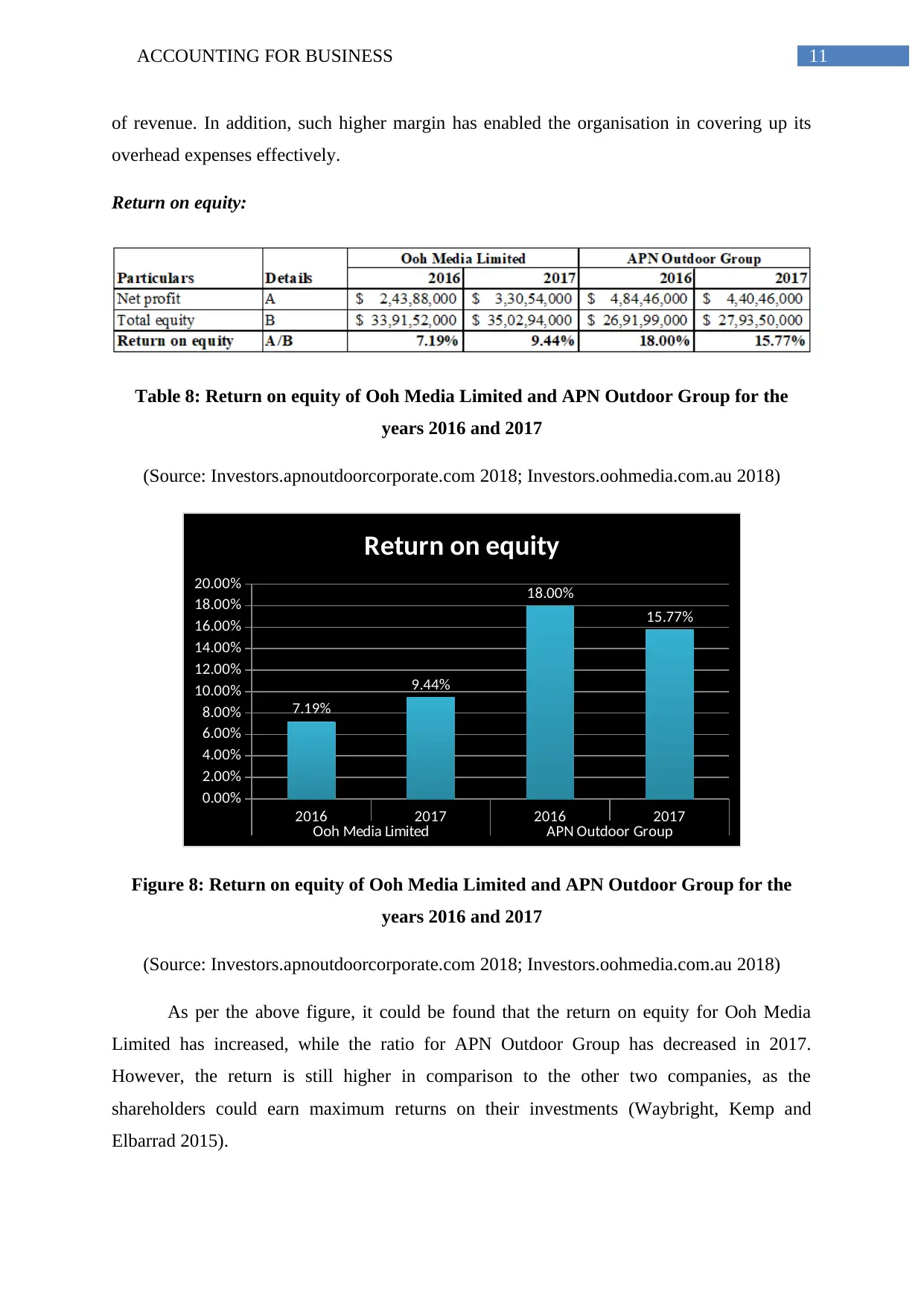

of revenue. In addition, such higher margin has enabled the organisation in covering up its

overhead expenses effectively.

Return on equity:

Table 8: Return on equity of Ooh Media Limited and APN Outdoor Group for the

years 2016 and 2017

(Source: Investors.apnoutdoorcorporate.com 2018; Investors.oohmedia.com.au 2018)

2016 2017 2016 2017

Ooh Media Limited APN Outdoor Group

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

12.00%

14.00%

16.00%

18.00%

20.00%

7.19%

9.44%

18.00%

15.77%

Return on equity

Figure 8: Return on equity of Ooh Media Limited and APN Outdoor Group for the

years 2016 and 2017

(Source: Investors.apnoutdoorcorporate.com 2018; Investors.oohmedia.com.au 2018)

As per the above figure, it could be found that the return on equity for Ooh Media

Limited has increased, while the ratio for APN Outdoor Group has decreased in 2017.

However, the return is still higher in comparison to the other two companies, as the

shareholders could earn maximum returns on their investments (Waybright, Kemp and

Elbarrad 2015).

of revenue. In addition, such higher margin has enabled the organisation in covering up its

overhead expenses effectively.

Return on equity:

Table 8: Return on equity of Ooh Media Limited and APN Outdoor Group for the

years 2016 and 2017

(Source: Investors.apnoutdoorcorporate.com 2018; Investors.oohmedia.com.au 2018)

2016 2017 2016 2017

Ooh Media Limited APN Outdoor Group

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

12.00%

14.00%

16.00%

18.00%

20.00%

7.19%

9.44%

18.00%

15.77%

Return on equity

Figure 8: Return on equity of Ooh Media Limited and APN Outdoor Group for the

years 2016 and 2017

(Source: Investors.apnoutdoorcorporate.com 2018; Investors.oohmedia.com.au 2018)

As per the above figure, it could be found that the return on equity for Ooh Media

Limited has increased, while the ratio for APN Outdoor Group has decreased in 2017.

However, the return is still higher in comparison to the other two companies, as the

shareholders could earn maximum returns on their investments (Waybright, Kemp and

Elbarrad 2015).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.