ACC00712: Qualitative Characteristics of Accounting Information

VerifiedAdded on 2022/11/25

|8

|2517

|188

Essay

AI Summary

This essay delves into the qualitative characteristics of accounting information, using the Reject Shop company as a case study. It examines the application of the Australian Conceptual Framework, focusing on elements like understandability, relevance, reliability, faithful representation, and comparability. The analysis includes the implications of revaluation on asset values, the significance of prudence in accounting practices, and the impact of financial reporting on market reactions and investor decisions. The essay references key concepts and principles in business accounting and provides comments on a statement regarding the revaluation of land, linking this to the qualitative characteristic of faithful presentation, and discussing how the company's financial statements demonstrate the application of these principles in their annual reports, as well as the importance of relevance and reliability to investors. It also explores the roles of Australian conceptual framework and its influence on accounting standards. References from established authors are cited to support each claim.

QUALITATIVE CHARACTERISTICS OF ACCOUNTING INFORMATION 1

STUDENT NAME

STUDENT ID NO.:

UNIT NAME:

UNIT CODE:

TUTOR’S NAME:

ASSIGNMENT

NO.:

ASSIGNMENT

TITLE:

DUE DATE:

DATE

SUBMITTED:

STUDENT NAME

STUDENT ID NO.:

UNIT NAME:

UNIT CODE:

TUTOR’S NAME:

ASSIGNMENT

NO.:

ASSIGNMENT

TITLE:

DUE DATE:

DATE

SUBMITTED:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

QUALITATIVE CHARACTERISTICS OF ACCOUNTING INFORMATION 2

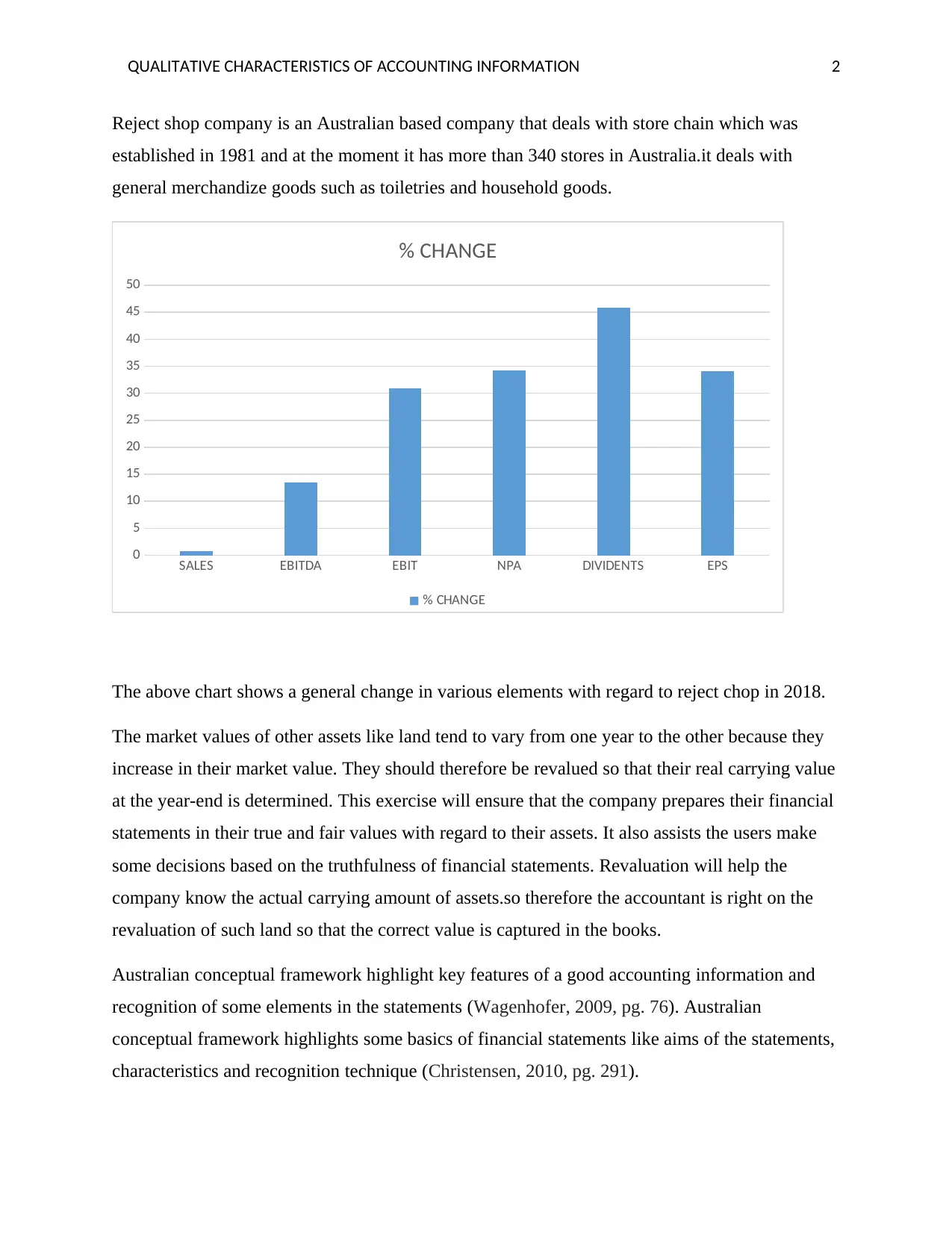

Reject shop company is an Australian based company that deals with store chain which was

established in 1981 and at the moment it has more than 340 stores in Australia.it deals with

general merchandize goods such as toiletries and household goods.

SALES EBITDA EBIT NPA DIVIDENTS EPS

0

5

10

15

20

25

30

35

40

45

50

% CHANGE

% CHANGE

The above chart shows a general change in various elements with regard to reject chop in 2018.

The market values of other assets like land tend to vary from one year to the other because they

increase in their market value. They should therefore be revalued so that their real carrying value

at the year-end is determined. This exercise will ensure that the company prepares their financial

statements in their true and fair values with regard to their assets. It also assists the users make

some decisions based on the truthfulness of financial statements. Revaluation will help the

company know the actual carrying amount of assets.so therefore the accountant is right on the

revaluation of such land so that the correct value is captured in the books.

Australian conceptual framework highlight key features of a good accounting information and

recognition of some elements in the statements (Wagenhofer, 2009, pg. 76). Australian

conceptual framework highlights some basics of financial statements like aims of the statements,

characteristics and recognition technique (Christensen, 2010, pg. 291).

Reject shop company is an Australian based company that deals with store chain which was

established in 1981 and at the moment it has more than 340 stores in Australia.it deals with

general merchandize goods such as toiletries and household goods.

SALES EBITDA EBIT NPA DIVIDENTS EPS

0

5

10

15

20

25

30

35

40

45

50

% CHANGE

% CHANGE

The above chart shows a general change in various elements with regard to reject chop in 2018.

The market values of other assets like land tend to vary from one year to the other because they

increase in their market value. They should therefore be revalued so that their real carrying value

at the year-end is determined. This exercise will ensure that the company prepares their financial

statements in their true and fair values with regard to their assets. It also assists the users make

some decisions based on the truthfulness of financial statements. Revaluation will help the

company know the actual carrying amount of assets.so therefore the accountant is right on the

revaluation of such land so that the correct value is captured in the books.

Australian conceptual framework highlight key features of a good accounting information and

recognition of some elements in the statements (Wagenhofer, 2009, pg. 76). Australian

conceptual framework highlights some basics of financial statements like aims of the statements,

characteristics and recognition technique (Christensen, 2010, pg. 291).

QUALITATIVE CHARACTERISTICS OF ACCOUNTING INFORMATION 3

prefix “Aus” is inserted to show the difference from IFRS.

Roles of the Australian conceptual framework.

Helps Australian accounting standards board in the amendments of different accounting

standards to enhance quality of accounting information.

Brings out harmonization in different rules and regulations that guides the presentation of

accounting information.

It assists various accountants in utilization of various standards such as Australian

accounting standards in the preparation and presentation of accounting information.

It helps auditors in the generation of judgements relating to the preparation and

presentation of financial statements and if such statements have been prepared in line

with relevant standards.

It simplifies the interpretation of accounting information since it presents it in a uniform

way making it easier to be interpreted.

Understandability means that the information presented should be in a form that can be easily

understood by a common user. It should be free from ambiguity and complex figures that are not

understandable by the users.

Relevance means that the financial statements must be useful to the need of the user for

purposes of decision making (Karğın, 2013, pg.73). It helps in predicting future structures and

arrangements of the company based on past performance. Therefore, presentation of elements

like dividend payout, salary payment and prices of shares should be well highlighted so that it

can be relevant to investors (Nobes &Stadler, 2015, Pg. 591).

Comparability simply implies that the information presented are easy to compare for instance

previous, current and future results regarding a particular item (Yip &Young, 2012, pg.1770).

financial information therefore should refer to the same period of time to be comparable for

instance 2nd July of 2017 and 2018.companies in the same industry should present information in

a comparable format for users to easily make comparison.

Reliability means information is free from errors and possible misstatement of facts. Relevance

of information does not necessarily mean it is reliable. This could be due to the recognition

method used which could be misleading. A good example is the amount of damages regarding a

prefix “Aus” is inserted to show the difference from IFRS.

Roles of the Australian conceptual framework.

Helps Australian accounting standards board in the amendments of different accounting

standards to enhance quality of accounting information.

Brings out harmonization in different rules and regulations that guides the presentation of

accounting information.

It assists various accountants in utilization of various standards such as Australian

accounting standards in the preparation and presentation of accounting information.

It helps auditors in the generation of judgements relating to the preparation and

presentation of financial statements and if such statements have been prepared in line

with relevant standards.

It simplifies the interpretation of accounting information since it presents it in a uniform

way making it easier to be interpreted.

Understandability means that the information presented should be in a form that can be easily

understood by a common user. It should be free from ambiguity and complex figures that are not

understandable by the users.

Relevance means that the financial statements must be useful to the need of the user for

purposes of decision making (Karğın, 2013, pg.73). It helps in predicting future structures and

arrangements of the company based on past performance. Therefore, presentation of elements

like dividend payout, salary payment and prices of shares should be well highlighted so that it

can be relevant to investors (Nobes &Stadler, 2015, Pg. 591).

Comparability simply implies that the information presented are easy to compare for instance

previous, current and future results regarding a particular item (Yip &Young, 2012, pg.1770).

financial information therefore should refer to the same period of time to be comparable for

instance 2nd July of 2017 and 2018.companies in the same industry should present information in

a comparable format for users to easily make comparison.

Reliability means information is free from errors and possible misstatement of facts. Relevance

of information does not necessarily mean it is reliable. This could be due to the recognition

method used which could be misleading. A good example is the amount of damages regarding a

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

QUALITATIVE CHARACTERISTICS OF ACCOUNTING INFORMATION 4

pending case. This value must not be recorded in full since it will show a wrong image regarding

the earnings of the company. Users might not draw relevant information from this reports.

Faithfull representation means that truth should prevail with regard to preparation of financial

statements. Assumptions and accounting estimates used should be well disclosed. Presentation of

items like assets, equities and liabilities must be presented in a truthful manner and recognition

method should be understandable and acceptable. Untruthful presentation might arise because of

wrong measurement criteria and recognition. Where there is difficulty regarding recognition and

measurement, relevant disclosures of possible errors should be provided (Macintosh, 2009, pg.

150).

Prudence concept. according to the concept, revenues of the company should not be

overestimated and also expenses should not be underestimated. This concept requires that

revenue recognition only happen when you are certain of their inflows (Barker, 2015, pg. 515).

recognition of sales revenue and other revenues in pg.37 of the annual reports clearly shows that

the accountants have utilized the concept of prudence. Sales revenue of 2018 and 2017 differ

with a slight amount of $ 6286 million, this shows a fair figure. Expenses have been also listed

properly and with minimal differences (Kirschenheiter &Ramakrishna, 2010). A specific element

resulting from expenditure is not clearly shown but a prudent accountant provides a reasonable

amount for such in expectation for such. Accountants should therefore be familiar with uncertain

economic conditions they operate in such as probability of collecting debts and life expectancy

of assets. This will therefore involve application of their judgement and experience in the field.

Understandability characteristics is clearly shown since various elements in the statements are

accompanied with notes which shows underlying assumption, workings and any other relevant

information. For instance, under note 19. Regarding contingent liabilities, it is clearly stated that

the company has no contingent liabilities as at 1st July 2018., note 25 highlight key issues relating

to dividends. These accompanying notes therefore brings the feature of understandability into

play.net income after tax is also shown clearly to be $16.5 and 12.3 in 2018 and 2017, this is

easy to understand by common user.

Comparability quality is shown in the half year financial report pg.2 where it is stated that Sales

grew by 1.1% from $432.9m to $437.6m against the prior corresponding period. the term

‘corresponding’ means the statements are comparable from the previous period. This shows that

pending case. This value must not be recorded in full since it will show a wrong image regarding

the earnings of the company. Users might not draw relevant information from this reports.

Faithfull representation means that truth should prevail with regard to preparation of financial

statements. Assumptions and accounting estimates used should be well disclosed. Presentation of

items like assets, equities and liabilities must be presented in a truthful manner and recognition

method should be understandable and acceptable. Untruthful presentation might arise because of

wrong measurement criteria and recognition. Where there is difficulty regarding recognition and

measurement, relevant disclosures of possible errors should be provided (Macintosh, 2009, pg.

150).

Prudence concept. according to the concept, revenues of the company should not be

overestimated and also expenses should not be underestimated. This concept requires that

revenue recognition only happen when you are certain of their inflows (Barker, 2015, pg. 515).

recognition of sales revenue and other revenues in pg.37 of the annual reports clearly shows that

the accountants have utilized the concept of prudence. Sales revenue of 2018 and 2017 differ

with a slight amount of $ 6286 million, this shows a fair figure. Expenses have been also listed

properly and with minimal differences (Kirschenheiter &Ramakrishna, 2010). A specific element

resulting from expenditure is not clearly shown but a prudent accountant provides a reasonable

amount for such in expectation for such. Accountants should therefore be familiar with uncertain

economic conditions they operate in such as probability of collecting debts and life expectancy

of assets. This will therefore involve application of their judgement and experience in the field.

Understandability characteristics is clearly shown since various elements in the statements are

accompanied with notes which shows underlying assumption, workings and any other relevant

information. For instance, under note 19. Regarding contingent liabilities, it is clearly stated that

the company has no contingent liabilities as at 1st July 2018., note 25 highlight key issues relating

to dividends. These accompanying notes therefore brings the feature of understandability into

play.net income after tax is also shown clearly to be $16.5 and 12.3 in 2018 and 2017, this is

easy to understand by common user.

Comparability quality is shown in the half year financial report pg.2 where it is stated that Sales

grew by 1.1% from $432.9m to $437.6m against the prior corresponding period. the term

‘corresponding’ means the statements are comparable from the previous period. This shows that

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

QUALITATIVE CHARACTERISTICS OF ACCOUNTING INFORMATION 5

reject shop limited prepares its reports in line with good features set. This will enhance the

comparability of different items in the statement which relate to same reporting time. Financial

statement of reject company shows some net earnings after tax of $16.5 and $12.3 million in

2018 and 2017 consecutively. This profits relates to the same period which enhances

comparison. Users can therefore compare this earnings and carry draw relevant decision out of it

(Cascino & Gassen, 2010).

faithful representation is portrayed in the statements of Reject shop where they have shown how

they have arrived at various accounting judgements.it has been disclosed in pg.42 of 2018 annual

report that financial report has been prepared using the historical cost method. This is a key

disclosure necessary to make key decision by the user.it is further indicated that judgement

regarding some estimates has been utilized with regard to useful life of assets. Further they have

disclosed that depreciation is to be calculated using straight line method.

Prudence is an important concept in accounting that implies use of judgement regarding

treatment of some accounting estimates. Reject shop has adhered to this concept as shown in the

way they have arrived at the useful life of computers, vehicles, fixtures with useful life

expectancy of 3,3-5 and 5-12 respectively. This is shown in pg.43 of 2018 annual report.

(Yurisandi & Puspitasari, 2015, pg. 645). judgement is arrived at using capitalization rates.

Provisions under note.12 of liabilities with a figure of $ 10,564,000 and $ 9,757,000 in 2018 and

2017 utilized the concept of prudence. (Shortridge & Smith, 2009, pg. 11).

Reject shop company has shown clearly every element regarding their obligations like

borrowings of $ 13000,000 in 2017 and 0 in 2018.this shows that the statements are very reliable

to the user and give every aspect of information it requires. It further lists net assets of the

company of $ 150,986,000 and $ 135,153,000 in 2018 and 2017 respectively. This reliability of

the statement will aid the user make relevant investment decision. (Lim, Lee, Kausar & Walker,

2014, pg. 270).

Relevance is portrayed since the company prepares and present their annual reports yearly with

their financial period ending 2nd July each year. This indicates that the statement is prepared with

the interests of the user in mind. This presentation will aid the user anticipate the declaration of

the performance of the company at a particular time. Under note.17 of 2018 annual reports,

dividends paid are presented to be $6926000 and $12409000 in 2018 and 2017 respectively. This

reject shop limited prepares its reports in line with good features set. This will enhance the

comparability of different items in the statement which relate to same reporting time. Financial

statement of reject company shows some net earnings after tax of $16.5 and $12.3 million in

2018 and 2017 consecutively. This profits relates to the same period which enhances

comparison. Users can therefore compare this earnings and carry draw relevant decision out of it

(Cascino & Gassen, 2010).

faithful representation is portrayed in the statements of Reject shop where they have shown how

they have arrived at various accounting judgements.it has been disclosed in pg.42 of 2018 annual

report that financial report has been prepared using the historical cost method. This is a key

disclosure necessary to make key decision by the user.it is further indicated that judgement

regarding some estimates has been utilized with regard to useful life of assets. Further they have

disclosed that depreciation is to be calculated using straight line method.

Prudence is an important concept in accounting that implies use of judgement regarding

treatment of some accounting estimates. Reject shop has adhered to this concept as shown in the

way they have arrived at the useful life of computers, vehicles, fixtures with useful life

expectancy of 3,3-5 and 5-12 respectively. This is shown in pg.43 of 2018 annual report.

(Yurisandi & Puspitasari, 2015, pg. 645). judgement is arrived at using capitalization rates.

Provisions under note.12 of liabilities with a figure of $ 10,564,000 and $ 9,757,000 in 2018 and

2017 utilized the concept of prudence. (Shortridge & Smith, 2009, pg. 11).

Reject shop company has shown clearly every element regarding their obligations like

borrowings of $ 13000,000 in 2017 and 0 in 2018.this shows that the statements are very reliable

to the user and give every aspect of information it requires. It further lists net assets of the

company of $ 150,986,000 and $ 135,153,000 in 2018 and 2017 respectively. This reliability of

the statement will aid the user make relevant investment decision. (Lim, Lee, Kausar & Walker,

2014, pg. 270).

Relevance is portrayed since the company prepares and present their annual reports yearly with

their financial period ending 2nd July each year. This indicates that the statement is prepared with

the interests of the user in mind. This presentation will aid the user anticipate the declaration of

the performance of the company at a particular time. Under note.17 of 2018 annual reports,

dividends paid are presented to be $6926000 and $12409000 in 2018 and 2017 respectively. This

QUALITATIVE CHARACTERISTICS OF ACCOUNTING INFORMATION 6

information is relevant to potential investors. Shareholders can therefore predict the dividends

for the next year.

security market reaction to the announcement of shares announced to the shareholders will

impact on the value of shares. For instance, Reject company announced to shareholders that they

have made a net profit of $ 16.6 million in the annual report of 2018.security market therefore

will react to this announcement since the company will declare dividends to shareholders in

proportion of their shareholding. The declaration of earnings will also make potential investors

have appetite to invests in the company. (Lee & Masulis, 2009, pg. 450). Performance of the

company is shown in the profit and loss account and the balance sheet and earnings are disclosed

for a company that is publicly quoted. This is to give adequate information to current and

potential investors of the company. It also gives good information to the security market which

tend to influence the share price either to rise or fall. (Mlonzi, Kruger, & Nthoesane, 2011,

pg.150). This is clearly depicted in the annual reports of Reject shop where they announced the

total number of shares issued to be 326,700 in 2017. Dividends paid under note.17 of (6,926)

(12,409) is also disclosed which is in line with good presentation of financial reports. Basic and

diluted earnings per share of reject company is shown as 57.4 and 42.8,56.7 and 42.4 cents

respectively. These is a key information that is very relevant to the investors to make relevant

investment. (Booth, Kallunki, Sahlstro, & Tyynela, 2011, pg.230).

in the ideas of Cready& Gurun (2010), low earnings lead to rise in the market values while

Hussin et al. (2010) established that minimum earnings bring negative reaction in the market.

disclosing the share prices of the company and the profitability will impact on the stock prices

either positively or negatively (Hoggett et al, 2014).

In conclusion, good accounting statement that meets the needs of the user must portray the above

features so that it can be useful to the user. It must be prepared and presented in a form that is

easy to understand and give a true information that is relevant and reliable to the user.

information is relevant to potential investors. Shareholders can therefore predict the dividends

for the next year.

security market reaction to the announcement of shares announced to the shareholders will

impact on the value of shares. For instance, Reject company announced to shareholders that they

have made a net profit of $ 16.6 million in the annual report of 2018.security market therefore

will react to this announcement since the company will declare dividends to shareholders in

proportion of their shareholding. The declaration of earnings will also make potential investors

have appetite to invests in the company. (Lee & Masulis, 2009, pg. 450). Performance of the

company is shown in the profit and loss account and the balance sheet and earnings are disclosed

for a company that is publicly quoted. This is to give adequate information to current and

potential investors of the company. It also gives good information to the security market which

tend to influence the share price either to rise or fall. (Mlonzi, Kruger, & Nthoesane, 2011,

pg.150). This is clearly depicted in the annual reports of Reject shop where they announced the

total number of shares issued to be 326,700 in 2017. Dividends paid under note.17 of (6,926)

(12,409) is also disclosed which is in line with good presentation of financial reports. Basic and

diluted earnings per share of reject company is shown as 57.4 and 42.8,56.7 and 42.4 cents

respectively. These is a key information that is very relevant to the investors to make relevant

investment. (Booth, Kallunki, Sahlstro, & Tyynela, 2011, pg.230).

in the ideas of Cready& Gurun (2010), low earnings lead to rise in the market values while

Hussin et al. (2010) established that minimum earnings bring negative reaction in the market.

disclosing the share prices of the company and the profitability will impact on the stock prices

either positively or negatively (Hoggett et al, 2014).

In conclusion, good accounting statement that meets the needs of the user must portray the above

features so that it can be useful to the user. It must be prepared and presented in a form that is

easy to understand and give a true information that is relevant and reliable to the user.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

QUALITATIVE CHARACTERISTICS OF ACCOUNTING INFORMATION 7

REFERENCES.

Barker, R., 2015. Conservatism, prudence and the IASB's conceptual framework. Accounting

and Business Research, 45(4), pp.514-538.

Cascino, S. and Gassen, J., 2010. Mandatory IFRS adoption and accounting comparability (No.

2010-046). SFB 649 discussion paper.

Christensen, J., 2010. Conceptual frameworks of accounting from an information

perspective. Accounting and Business Research, 40(3), pp.287-299.

Geoffrey Booth, G., Kallunki, J.P., Sahlström, P. and Tyynelä, J., 2011. Foreign vs domestic

investors and the post-announcement drift. International Journal of Managerial Finance, 7(3),

pp.220-237.

Hoggett, J., Edwards, L., Medlin, J., Chalmers, K., Hellmann, A., Beattie, C. and Maxfield, J.,

2014. Financial accounting. John Wiley & Sons.

Karğın, S., 2013. The impact of IFRS on the value relevance of accounting information:

Evidence from Turkish firms. International Journal of Economics and Finance, 5(4), pp.71-80.

Kirschenheiter, M. and Ramakrishnan, R.T., 2010, September. Prudence demands conservatism.

AAA.

Lee, G. and Masulis, R.W., 2009. Seasoned equity offerings: Quality of accounting information

and expected flotation costs. Journal of Financial Economics, 92(3), pp.443-469.

Lim, C.Y., Lee, E., Kausar, A. and Walker, M., 2014. Bank accounting conservatism and bank

loan pricing. Journal of Accounting and Public Policy, 33(3), pp.260-278.

Macintosh, N.B., 2009. Accounting and the truth of earnings reports: philosophical

considerations. European Accounting Review, 18(1), pp.141-175.

Mlonzi, V.F., Kruger, J. and Nthoesane, M.G., 2011. Share price reaction to earnings

announcement on the JSE-ALtX: A test for market efficiency. Southern African Business

Review, 15(3), pp.142-166.

REFERENCES.

Barker, R., 2015. Conservatism, prudence and the IASB's conceptual framework. Accounting

and Business Research, 45(4), pp.514-538.

Cascino, S. and Gassen, J., 2010. Mandatory IFRS adoption and accounting comparability (No.

2010-046). SFB 649 discussion paper.

Christensen, J., 2010. Conceptual frameworks of accounting from an information

perspective. Accounting and Business Research, 40(3), pp.287-299.

Geoffrey Booth, G., Kallunki, J.P., Sahlström, P. and Tyynelä, J., 2011. Foreign vs domestic

investors and the post-announcement drift. International Journal of Managerial Finance, 7(3),

pp.220-237.

Hoggett, J., Edwards, L., Medlin, J., Chalmers, K., Hellmann, A., Beattie, C. and Maxfield, J.,

2014. Financial accounting. John Wiley & Sons.

Karğın, S., 2013. The impact of IFRS on the value relevance of accounting information:

Evidence from Turkish firms. International Journal of Economics and Finance, 5(4), pp.71-80.

Kirschenheiter, M. and Ramakrishnan, R.T., 2010, September. Prudence demands conservatism.

AAA.

Lee, G. and Masulis, R.W., 2009. Seasoned equity offerings: Quality of accounting information

and expected flotation costs. Journal of Financial Economics, 92(3), pp.443-469.

Lim, C.Y., Lee, E., Kausar, A. and Walker, M., 2014. Bank accounting conservatism and bank

loan pricing. Journal of Accounting and Public Policy, 33(3), pp.260-278.

Macintosh, N.B., 2009. Accounting and the truth of earnings reports: philosophical

considerations. European Accounting Review, 18(1), pp.141-175.

Mlonzi, V.F., Kruger, J. and Nthoesane, M.G., 2011. Share price reaction to earnings

announcement on the JSE-ALtX: A test for market efficiency. Southern African Business

Review, 15(3), pp.142-166.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

QUALITATIVE CHARACTERISTICS OF ACCOUNTING INFORMATION 8

Nobes, C.W. and Stadler, C., 2015. The qualitative characteristics of financial information, and

managers’ accounting decisions: evidence from IFRS policy changes. Accounting and Business

Research, 45(5), pp.572-601.

Reject shop company annual

reports<https://www.rejectshop.com.au/aboutus/investorinformation/financialreport>

Shortridge, R.T. and Smith, P.A., 2009. Understanding the changes in accounting

thought. Research in accounting regulation, 21(1), pp.11-18.

Wagenhofer, A., 2009. Global accounting standards: reality and ambitions. Accounting Research

Journal, 22(1), pp.68-80.

Yip, R.W. and Young, D., 2012. Does mandatory IFRS adoption improve information

comparability? The Accounting Review, 87(5), pp.1767-1789.

Yurisandi, T. and Puspitasari, E., 2015. Financial Reporting Quality-Before and After IFRS

Adoption Using NiCE Qualitative Characteristics Measurement. Procedia-Social and

Behavioral Sciences, 211, pp.644-652.

Nobes, C.W. and Stadler, C., 2015. The qualitative characteristics of financial information, and

managers’ accounting decisions: evidence from IFRS policy changes. Accounting and Business

Research, 45(5), pp.572-601.

Reject shop company annual

reports<https://www.rejectshop.com.au/aboutus/investorinformation/financialreport>

Shortridge, R.T. and Smith, P.A., 2009. Understanding the changes in accounting

thought. Research in accounting regulation, 21(1), pp.11-18.

Wagenhofer, A., 2009. Global accounting standards: reality and ambitions. Accounting Research

Journal, 22(1), pp.68-80.

Yip, R.W. and Young, D., 2012. Does mandatory IFRS adoption improve information

comparability? The Accounting Review, 87(5), pp.1767-1789.

Yurisandi, T. and Puspitasari, E., 2015. Financial Reporting Quality-Before and After IFRS

Adoption Using NiCE Qualitative Characteristics Measurement. Procedia-Social and

Behavioral Sciences, 211, pp.644-652.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.