MATH 1053: Q Events Case Study - Quantitative Business Analysis

VerifiedAdded on 2023/06/07

|14

|2188

|237

Case Study

AI Summary

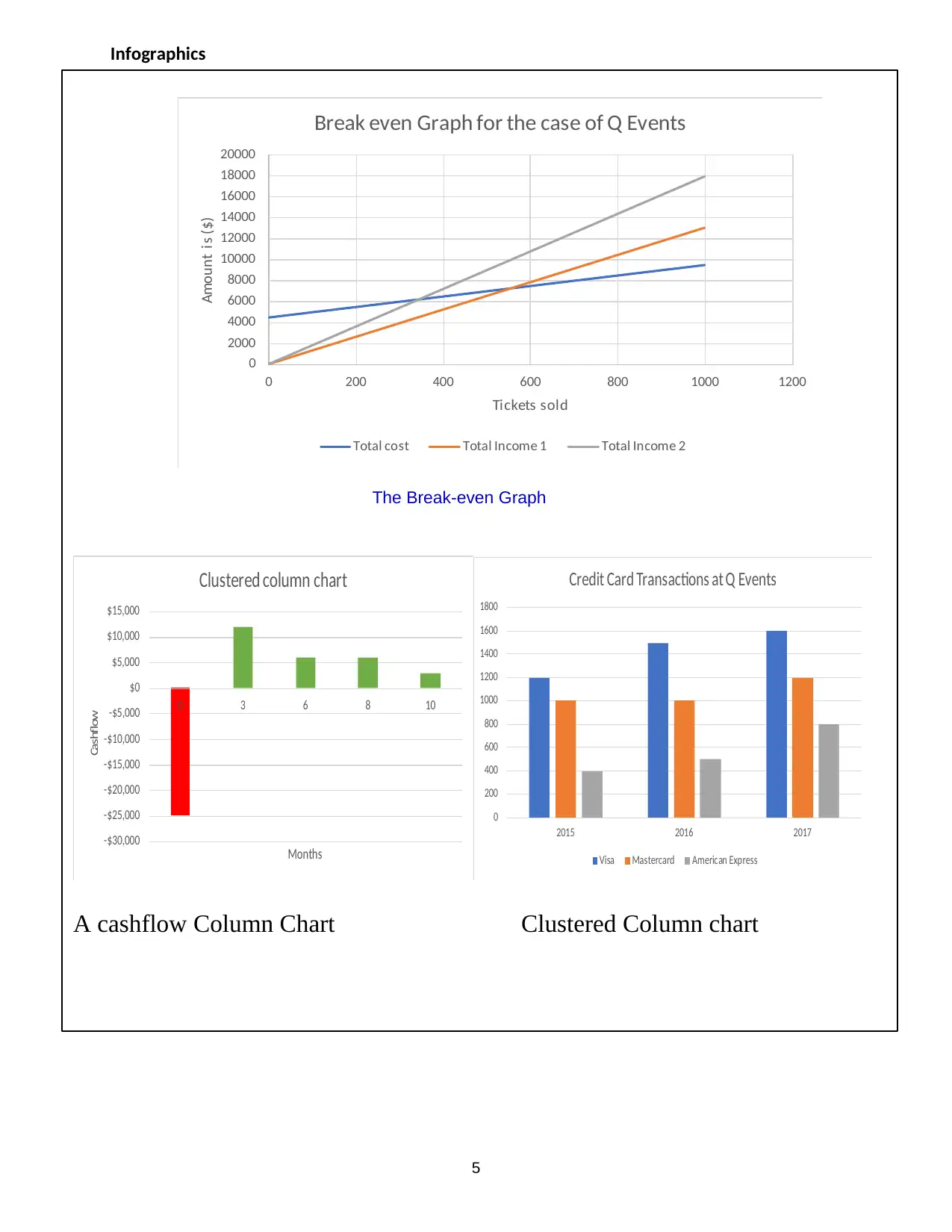

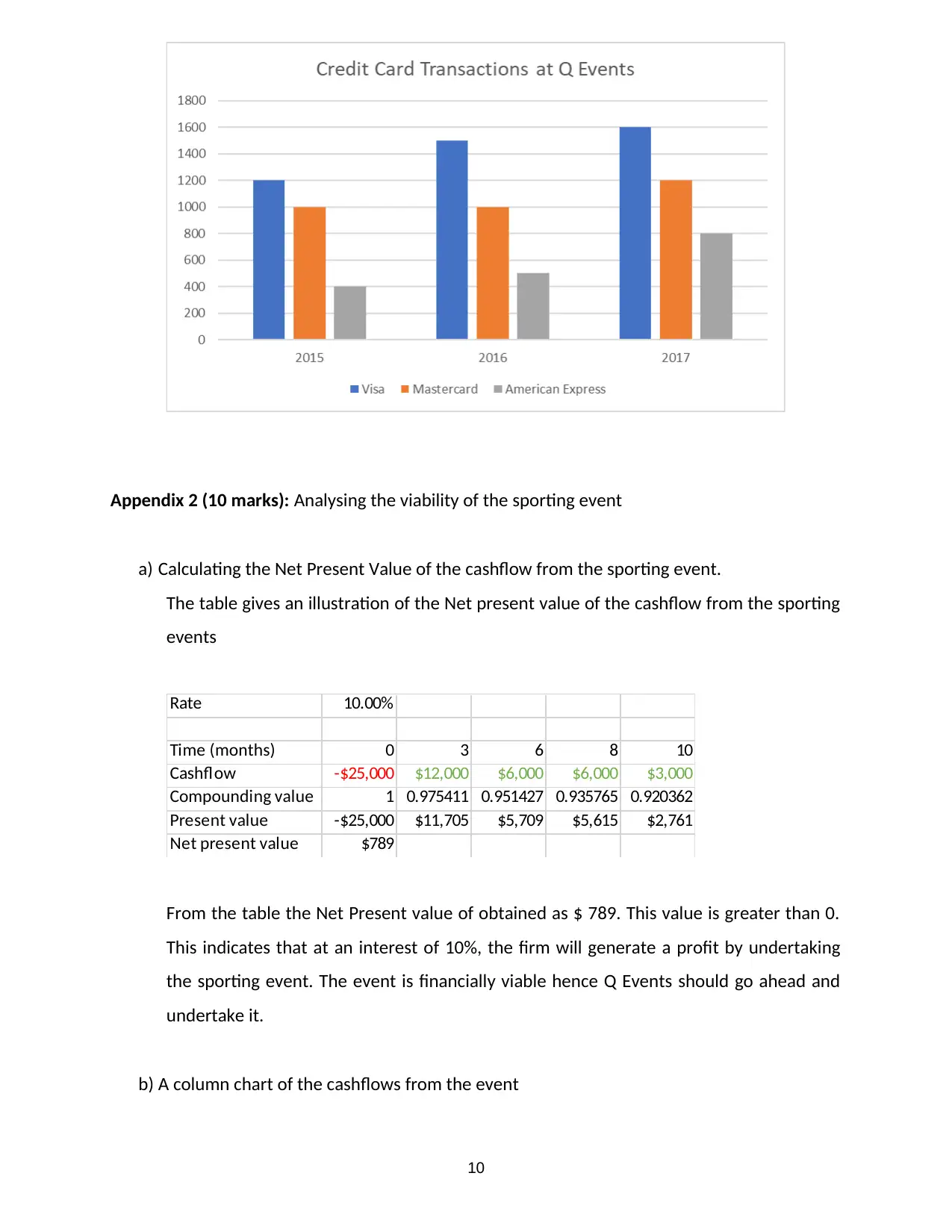

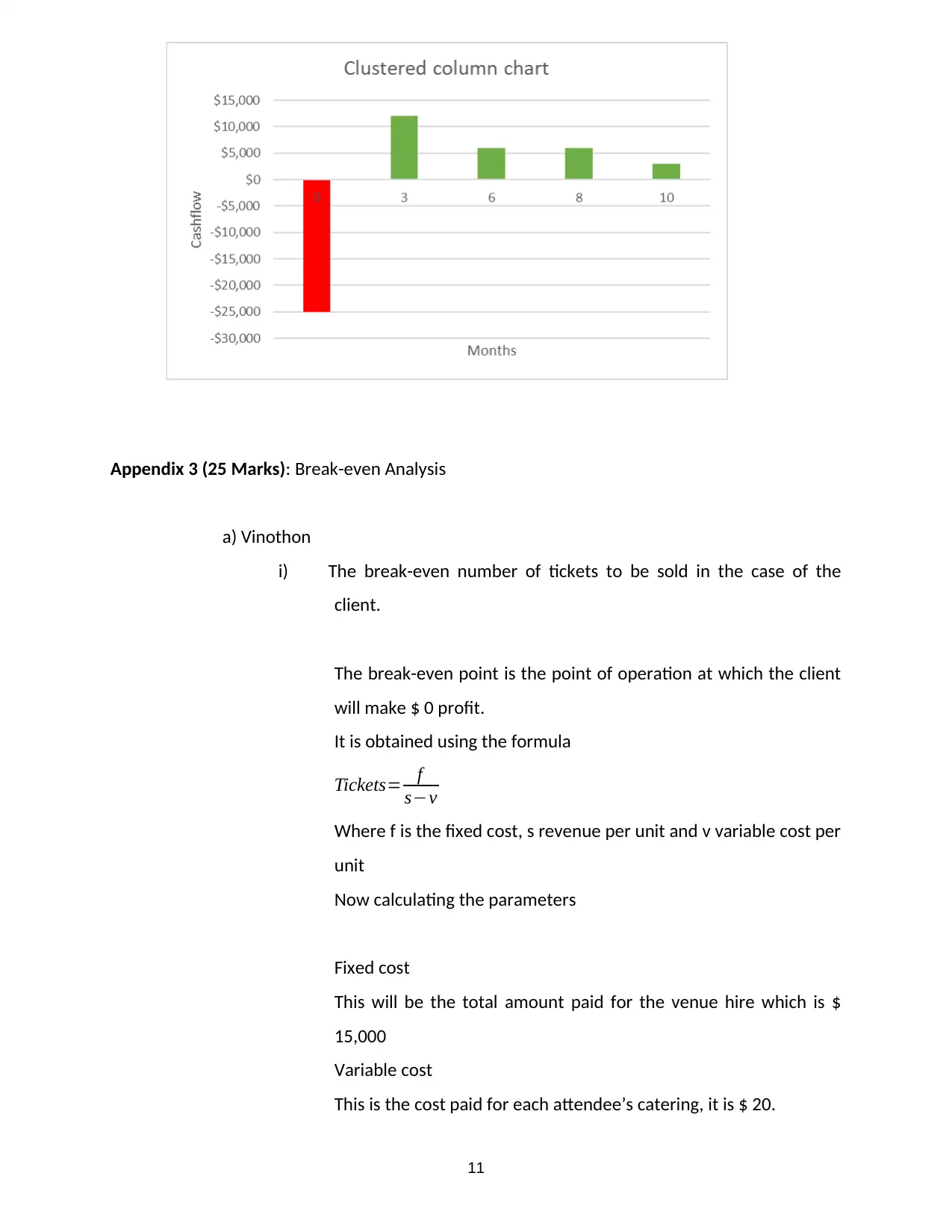

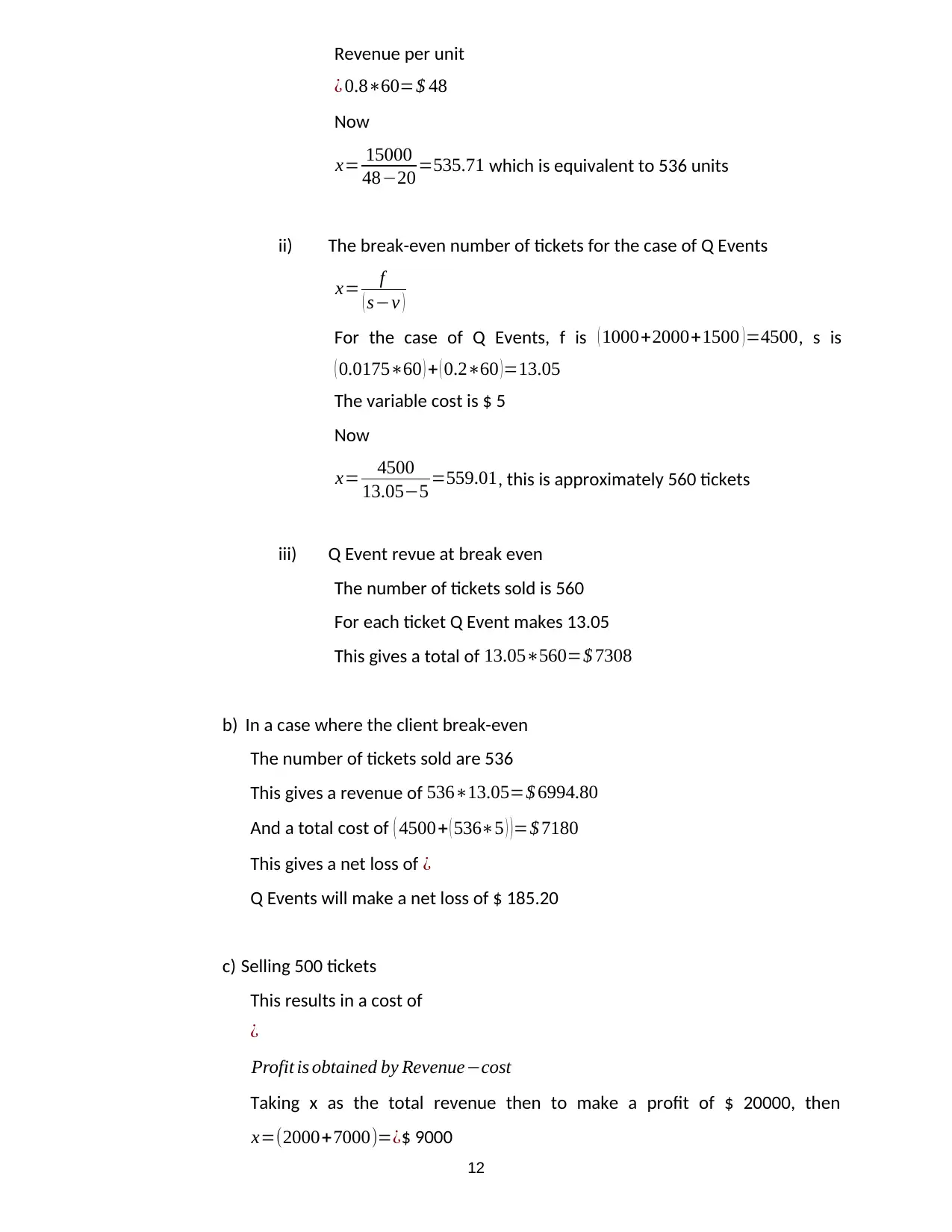

This report provides a quantitative analysis of Q Events' operations, focusing on optimizing profit and improving business practices. It examines credit card usage trends, evaluates the viability of a sporting event, and analyzes the profitability of the Vinothon event for both Q Events and its client. The analysis includes projected values, expected trends, and recommendations for setting ticket prices and minimum sales targets. The report concludes with suggestions to enhance services and maximize revenue generation, emphasizing the importance of critical pricing strategies and the impact of credit card usage patterns on the firm's financial performance. Key findings include the need to sell a minimum number of tickets for economic viability and the potential benefits of adjusting ticket prices to achieve breakeven with fewer sales.

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.