Business Economics - Effects of Quantitative Easing on Global Economy

VerifiedAdded on 2020/05/28

|12

|2997

|189

Essay

AI Summary

This essay provides a detailed analysis of quantitative easing (QE), an expansionary monetary policy implemented by central banks worldwide to stimulate economic growth, particularly during times of financial crisis and stagnation. The essay begins by defining QE and explaining its operational mechanisms, including lowering market interest rates and increasing the money supply through the purchase of securities. It then examines the historical implementation of QE, starting with Japan and extending to the United States, the United Kingdom, and the Eurozone, especially in response to the 2007-2008 global financial crisis. The essay highlights the benefits of QE, such as lower interest rates, increased borrowing and investment, and reduced unemployment, supported by empirical evidence from the US economy. However, it also critically evaluates the drawbacks, including the potential for asset bubbles, particularly in the housing market, and the associated risks of wealth transfer and market crashes. The essay uses figures and data to illustrate the impacts of QE on GDP and unemployment rates. Finally, it concludes by summarizing the mixed effects of QE, acknowledging its effectiveness in crisis management while cautioning about its potential long-term negative consequences.

Running head: BUSINESS ECONOMICS

Business Economics

Name of the Student

Name of the University

Author Note

Business Economics

Name of the Student

Name of the University

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1BUSINESS ECONOMICS

Introduction

The global economy, over the years, have experienced significant dynamics, much of

which can be attributed to the interactions of the demand and the supply side players, the policy

frameworks of the economies across the world and the financial behavioral patterns of the people

involved. The economy of each country, irrespective of its nature (that is, whether it is a public

economy, a market economy or a mixed one), works under certain policy framework, which

plays a key role in determining and controlling the dynamics of the economy, though the extent

of its control can vary (Mankiw 2014). The economic policy framework in general consists of

two types of policies, the fiscal policies and the monetary policies. While the fiscal policies, in

an economy, deals with the taxing and public spending in the economy, the monetary policies

deal with the market interest rates, the supply of money and other monetary variables and are in

general designed and implemented by the monetary authorities of the countries (Agénor and

Montiel 2015).

The monetary authorities of a country design and implement the monetary policies

according to the needs of the economy and the trends of economic growth, which the concerned

country shows. In general, expansionary monetary policies are taken by the monetary authority

of an economy to increase the money supply and the economic and productive activities, thereby

stimulating the economy, while the contractionary monetary policies are taken to reduce money

supply and the overall economic activities in the country (Schmidt 2013). In this context, one of

the most popular expansionary monetary policies in the contemporary global economic scenario,

which have been implemented in many significant economies across the world, including Japan,

the United States of America and the United Kingdom, is the policy of quantitative easing.

Introduction

The global economy, over the years, have experienced significant dynamics, much of

which can be attributed to the interactions of the demand and the supply side players, the policy

frameworks of the economies across the world and the financial behavioral patterns of the people

involved. The economy of each country, irrespective of its nature (that is, whether it is a public

economy, a market economy or a mixed one), works under certain policy framework, which

plays a key role in determining and controlling the dynamics of the economy, though the extent

of its control can vary (Mankiw 2014). The economic policy framework in general consists of

two types of policies, the fiscal policies and the monetary policies. While the fiscal policies, in

an economy, deals with the taxing and public spending in the economy, the monetary policies

deal with the market interest rates, the supply of money and other monetary variables and are in

general designed and implemented by the monetary authorities of the countries (Agénor and

Montiel 2015).

The monetary authorities of a country design and implement the monetary policies

according to the needs of the economy and the trends of economic growth, which the concerned

country shows. In general, expansionary monetary policies are taken by the monetary authority

of an economy to increase the money supply and the economic and productive activities, thereby

stimulating the economy, while the contractionary monetary policies are taken to reduce money

supply and the overall economic activities in the country (Schmidt 2013). In this context, one of

the most popular expansionary monetary policies in the contemporary global economic scenario,

which have been implemented in many significant economies across the world, including Japan,

the United States of America and the United Kingdom, is the policy of quantitative easing.

2BUSINESS ECONOMICS

Keeping this into consideration, the essay tries to discuss the aspects of quantitative

easing in details, critically examining its implications on the global economy. The essay

highlights the benefits as well as the threats, which the economies face from the implementation

of quantitative easing, in the global framework, supporting the assertions with economic

concepts and empirical evidences available from the economic trends of the countries across the

world.

Quantitative Easing

The term “Quantitative Easing” refers to one of the most significant expansionary

monetary policies, which have been implemented by many significant economies in the world,

with the primary aim of stimulating the economy and to spur the overall economic growth of the

concerned countries. The main mode of operation of this expansionary monetary policy, by

which it tries to increase the activities in an economy, is by lowering down the rate of interest

prevailing in the market (Fawley and Neely 2013). The main notion behind the reduction of the

market interest rate, which works behind the implementation of the quantitative easing strategy,

is that a low interest rate makes it easy for the businesses in the economy to borrow money,

which in turn helps the businesses to expand. This in turn, increases the overall productivity of

the country, thereby stimulating both the aggregate demand as well as the aggregate supply of

the country, thus, taking the economy to the path of sustained growth (Joyce et al. 2012).

Working mechanism of the Quantitative Easing policy

In the contemporary periods of economic stagnation, when the economies need a

stimulus to gain back pace in its path of progress, many a times, the central bank provides the

stimulus in the form of expansion of its open market operations. The central bank of the

Keeping this into consideration, the essay tries to discuss the aspects of quantitative

easing in details, critically examining its implications on the global economy. The essay

highlights the benefits as well as the threats, which the economies face from the implementation

of quantitative easing, in the global framework, supporting the assertions with economic

concepts and empirical evidences available from the economic trends of the countries across the

world.

Quantitative Easing

The term “Quantitative Easing” refers to one of the most significant expansionary

monetary policies, which have been implemented by many significant economies in the world,

with the primary aim of stimulating the economy and to spur the overall economic growth of the

concerned countries. The main mode of operation of this expansionary monetary policy, by

which it tries to increase the activities in an economy, is by lowering down the rate of interest

prevailing in the market (Fawley and Neely 2013). The main notion behind the reduction of the

market interest rate, which works behind the implementation of the quantitative easing strategy,

is that a low interest rate makes it easy for the businesses in the economy to borrow money,

which in turn helps the businesses to expand. This in turn, increases the overall productivity of

the country, thereby stimulating both the aggregate demand as well as the aggregate supply of

the country, thus, taking the economy to the path of sustained growth (Joyce et al. 2012).

Working mechanism of the Quantitative Easing policy

In the contemporary periods of economic stagnation, when the economies need a

stimulus to gain back pace in its path of progress, many a times, the central bank provides the

stimulus in the form of expansion of its open market operations. The central bank of the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3BUSINESS ECONOMICS

concerned economy, buys securities from the other member banks, which in turn increases the

liquidity in the capital market, thereby increasing the money supply. The fall of the rate of

interest, under the quantitative easing policy, allows the banks to lend more, which on one hand

increases commercial investments by making money borrowing easier for the businesses in the

economy. On the other hand also increases the aggregate household demand in the economy by

giving easy credits to them, which in turn increases their demand for the goods and services

(Kapetanios et al. 2012).

The other notion based on which the quantitative easing policy works is that, the

increased money supply under the operational framework of this policy, helps in lowering the

currency value of the concerned country low. This thereby makes the stocks of the country more

attractive to the investors from other counties, which increases the Foreign Direct Investment in

the country, adding to its economic stimuli (Martin and Milas 2012). The exports of the country

also become cheaper, which increases trade prospects of the country in the international scenario

and contributes positively in the economic growth of the country.

Implementation of Quantitative Easing in global economy

The Bank of Japan first implemented quantitative Easing, as a full-fledged monetary

policy, in the Japanese economy, in the early 2000s. The policy was mainly taken by the bank, to

combat the situation of a long persisting deflation and stagnant economic situation in the

country. The Bank of Japan took the quantitative easing strategy by infusing excessive liquidity

in the commercial banks of the country, by providing them with large excess reserves stocks,

which ensured less risks of shortages of liquidity. Increasing number of public bonds was bought

by the BOJ, thereby helping to keep the market interest rate to zero (Pesaran and Smith 2016).

concerned economy, buys securities from the other member banks, which in turn increases the

liquidity in the capital market, thereby increasing the money supply. The fall of the rate of

interest, under the quantitative easing policy, allows the banks to lend more, which on one hand

increases commercial investments by making money borrowing easier for the businesses in the

economy. On the other hand also increases the aggregate household demand in the economy by

giving easy credits to them, which in turn increases their demand for the goods and services

(Kapetanios et al. 2012).

The other notion based on which the quantitative easing policy works is that, the

increased money supply under the operational framework of this policy, helps in lowering the

currency value of the concerned country low. This thereby makes the stocks of the country more

attractive to the investors from other counties, which increases the Foreign Direct Investment in

the country, adding to its economic stimuli (Martin and Milas 2012). The exports of the country

also become cheaper, which increases trade prospects of the country in the international scenario

and contributes positively in the economic growth of the country.

Implementation of Quantitative Easing in global economy

The Bank of Japan first implemented quantitative Easing, as a full-fledged monetary

policy, in the Japanese economy, in the early 2000s. The policy was mainly taken by the bank, to

combat the situation of a long persisting deflation and stagnant economic situation in the

country. The Bank of Japan took the quantitative easing strategy by infusing excessive liquidity

in the commercial banks of the country, by providing them with large excess reserves stocks,

which ensured less risks of shortages of liquidity. Increasing number of public bonds was bought

by the BOJ, thereby helping to keep the market interest rate to zero (Pesaran and Smith 2016).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4BUSINESS ECONOMICS

Though Japan was the first economy to implement this strategy, their footsteps was

followed by the most influential global economies like that of the United States of America as

well as the UK and the Euro zone at the times of the Global Financial Crisis. The Crisis occurred

in 2007-2008 and had long lasting implications (mostly negative) on almost all the significant

economies of the world. The Financial Crisis, during that period, led many of the economies in

the global framework to a severe state of stagnancy by decreasing the overall economic and

productive activities of the countries (Blinder 2010). In such scenarios, it became immensely

important for the countries to stimulate the economic growth in the country to alleviate the crisis.

Quantitative easing as an expansionary monetary has been existing in the policy frameworks of

UK and USA since then as an instrument for increasing money supply, decreasing the rate of

interest and increasing the overall borrowings , thereby facilitating production and consumptions

in the economies (Christensen and Rudebusch 2012).

The policy had mixed effects in the economies, with significant presence of benefits as

well as several threats, which are discussed in the following sections of the essay.

Benefits of the Quantitative Easing Policy

The primary benefit of the expansionary monetary policy of quantitative easing is the

considerable lowering of the market rate of interest in the concerned economy. This happens due

to the excess flow of money supply, which makes the lending institutions to compete with one

another, thereby pulling down the rate of interest prevailing in the market. This in turn benefits

the economy by increasing borrowing, investment, consumption and the overall productivity of

the economy. The empirical evidences of the economy of the USA have supported this, as the

Though Japan was the first economy to implement this strategy, their footsteps was

followed by the most influential global economies like that of the United States of America as

well as the UK and the Euro zone at the times of the Global Financial Crisis. The Crisis occurred

in 2007-2008 and had long lasting implications (mostly negative) on almost all the significant

economies of the world. The Financial Crisis, during that period, led many of the economies in

the global framework to a severe state of stagnancy by decreasing the overall economic and

productive activities of the countries (Blinder 2010). In such scenarios, it became immensely

important for the countries to stimulate the economic growth in the country to alleviate the crisis.

Quantitative easing as an expansionary monetary has been existing in the policy frameworks of

UK and USA since then as an instrument for increasing money supply, decreasing the rate of

interest and increasing the overall borrowings , thereby facilitating production and consumptions

in the economies (Christensen and Rudebusch 2012).

The policy had mixed effects in the economies, with significant presence of benefits as

well as several threats, which are discussed in the following sections of the essay.

Benefits of the Quantitative Easing Policy

The primary benefit of the expansionary monetary policy of quantitative easing is the

considerable lowering of the market rate of interest in the concerned economy. This happens due

to the excess flow of money supply, which makes the lending institutions to compete with one

another, thereby pulling down the rate of interest prevailing in the market. This in turn benefits

the economy by increasing borrowing, investment, consumption and the overall productivity of

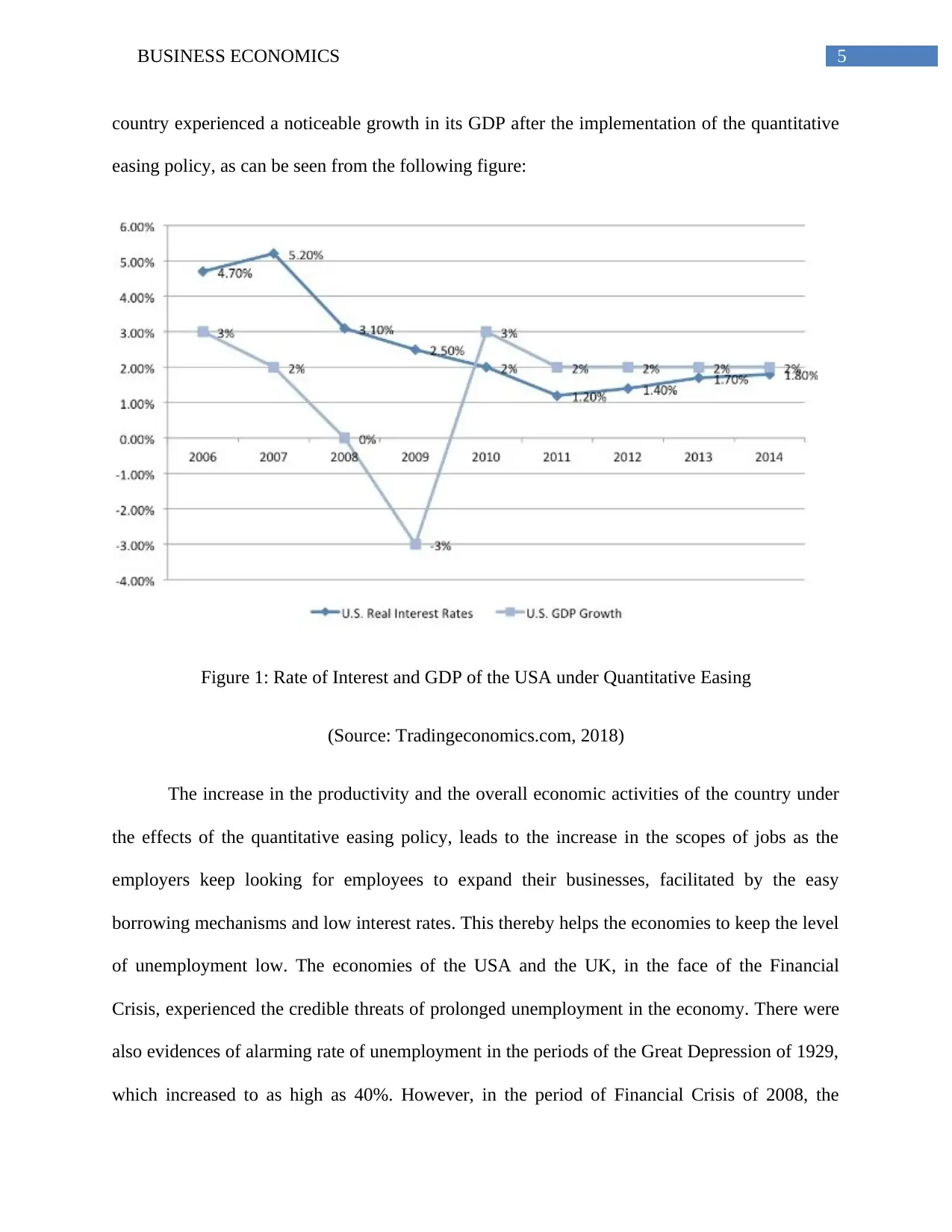

the economy. The empirical evidences of the economy of the USA have supported this, as the

5BUSINESS ECONOMICS

country experienced a noticeable growth in its GDP after the implementation of the quantitative

easing policy, as can be seen from the following figure:

Figure 1: Rate of Interest and GDP of the USA under Quantitative Easing

(Source: Tradingeconomics.com, 2018)

The increase in the productivity and the overall economic activities of the country under

the effects of the quantitative easing policy, leads to the increase in the scopes of jobs as the

employers keep looking for employees to expand their businesses, facilitated by the easy

borrowing mechanisms and low interest rates. This thereby helps the economies to keep the level

of unemployment low. The economies of the USA and the UK, in the face of the Financial

Crisis, experienced the credible threats of prolonged unemployment in the economy. There were

also evidences of alarming rate of unemployment in the periods of the Great Depression of 1929,

which increased to as high as 40%. However, in the period of Financial Crisis of 2008, the

country experienced a noticeable growth in its GDP after the implementation of the quantitative

easing policy, as can be seen from the following figure:

Figure 1: Rate of Interest and GDP of the USA under Quantitative Easing

(Source: Tradingeconomics.com, 2018)

The increase in the productivity and the overall economic activities of the country under

the effects of the quantitative easing policy, leads to the increase in the scopes of jobs as the

employers keep looking for employees to expand their businesses, facilitated by the easy

borrowing mechanisms and low interest rates. This thereby helps the economies to keep the level

of unemployment low. The economies of the USA and the UK, in the face of the Financial

Crisis, experienced the credible threats of prolonged unemployment in the economy. There were

also evidences of alarming rate of unemployment in the periods of the Great Depression of 1929,

which increased to as high as 40%. However, in the period of Financial Crisis of 2008, the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6BUSINESS ECONOMICS

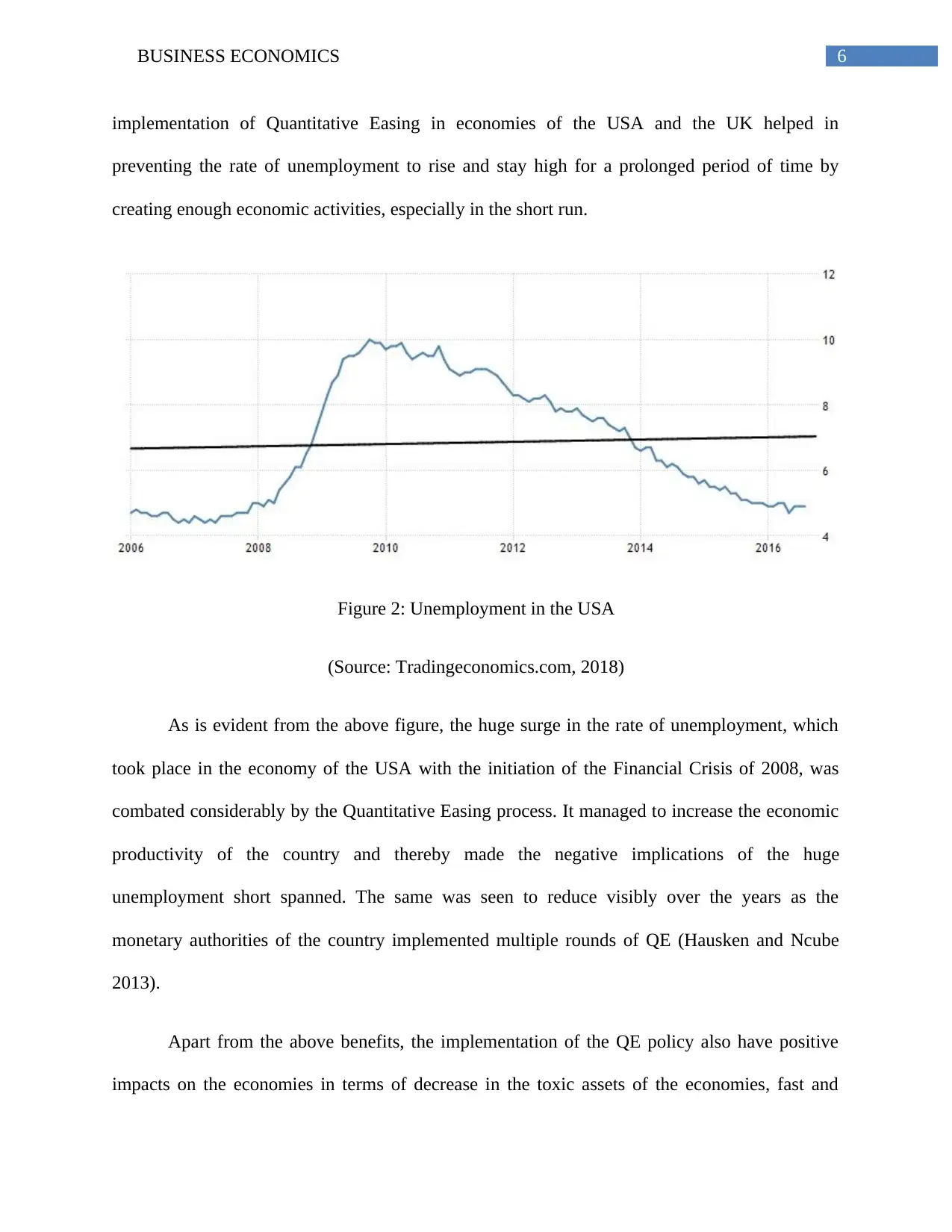

implementation of Quantitative Easing in economies of the USA and the UK helped in

preventing the rate of unemployment to rise and stay high for a prolonged period of time by

creating enough economic activities, especially in the short run.

Figure 2: Unemployment in the USA

(Source: Tradingeconomics.com, 2018)

As is evident from the above figure, the huge surge in the rate of unemployment, which

took place in the economy of the USA with the initiation of the Financial Crisis of 2008, was

combated considerably by the Quantitative Easing process. It managed to increase the economic

productivity of the country and thereby made the negative implications of the huge

unemployment short spanned. The same was seen to reduce visibly over the years as the

monetary authorities of the country implemented multiple rounds of QE (Hausken and Ncube

2013).

Apart from the above benefits, the implementation of the QE policy also have positive

impacts on the economies in terms of decrease in the toxic assets of the economies, fast and

implementation of Quantitative Easing in economies of the USA and the UK helped in

preventing the rate of unemployment to rise and stay high for a prolonged period of time by

creating enough economic activities, especially in the short run.

Figure 2: Unemployment in the USA

(Source: Tradingeconomics.com, 2018)

As is evident from the above figure, the huge surge in the rate of unemployment, which

took place in the economy of the USA with the initiation of the Financial Crisis of 2008, was

combated considerably by the Quantitative Easing process. It managed to increase the economic

productivity of the country and thereby made the negative implications of the huge

unemployment short spanned. The same was seen to reduce visibly over the years as the

monetary authorities of the country implemented multiple rounds of QE (Hausken and Ncube

2013).

Apart from the above benefits, the implementation of the QE policy also have positive

impacts on the economies in terms of decrease in the toxic assets of the economies, fast and

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7BUSINESS ECONOMICS

effective results in the face of acute crisis and also in terms of increased scope of the governing

authorities of the countries in intervening and fixing the situations. This, if left in the hands of

the free markets can lead to even more distortions and negative implications (Maggio, Kermani

and Palmer 2016). The positive effects of the quantitative easing have been prominent in the

significant economies like America, Europe and the UK, which indicates towards the fact that

the policy is significantly effective in most of the cases to combat the situations of economic and

financial crisis and productive stagnancy in the economies. However, there are several

drawbacks and threats, which the policy poses, and there are empirical evidences supporting

these negative aspects, which are discussed as follow.

Drawbacks of the Quantitative Easing Policy

The primary threat of the implementation of the quantitative easing policy in the

contemporary global framework is the threat of formations of extensive asset bubbles in the

economy. This is caused due to the excess supply of money as well as the ease of borrowing,

which on one hand makes investing on assets easy and on the other hand contributes in

increasing economic productivity, thereby increasing employments, salaries and the aggregate

demand for assets. Most of the times the asset bubbles are created in the housing or real estate

market as this market pose as a lucrative form for alternative investments for the households as

well as the investors. The presence of excessive income or money in their hand leads to

increasing demand for these assets, which in turn keeps, on increasing the price of such assets as

the supply for the same cannot be expanded rapidly or unlimitedly (Blanchard, Dell'Ariccia and

Mauro 2013). This in turn created a bubble in the asset markets of the economy implementing

quantitative easing. The asset bubble can however burst with a sudden crash in the market prices

effective results in the face of acute crisis and also in terms of increased scope of the governing

authorities of the countries in intervening and fixing the situations. This, if left in the hands of

the free markets can lead to even more distortions and negative implications (Maggio, Kermani

and Palmer 2016). The positive effects of the quantitative easing have been prominent in the

significant economies like America, Europe and the UK, which indicates towards the fact that

the policy is significantly effective in most of the cases to combat the situations of economic and

financial crisis and productive stagnancy in the economies. However, there are several

drawbacks and threats, which the policy poses, and there are empirical evidences supporting

these negative aspects, which are discussed as follow.

Drawbacks of the Quantitative Easing Policy

The primary threat of the implementation of the quantitative easing policy in the

contemporary global framework is the threat of formations of extensive asset bubbles in the

economy. This is caused due to the excess supply of money as well as the ease of borrowing,

which on one hand makes investing on assets easy and on the other hand contributes in

increasing economic productivity, thereby increasing employments, salaries and the aggregate

demand for assets. Most of the times the asset bubbles are created in the housing or real estate

market as this market pose as a lucrative form for alternative investments for the households as

well as the investors. The presence of excessive income or money in their hand leads to

increasing demand for these assets, which in turn keeps, on increasing the price of such assets as

the supply for the same cannot be expanded rapidly or unlimitedly (Blanchard, Dell'Ariccia and

Mauro 2013). This in turn created a bubble in the asset markets of the economy implementing

quantitative easing. The asset bubble can however burst with a sudden crash in the market prices

8BUSINESS ECONOMICS

of those assets, which in turn can have hugely negative implications on the society in terms of

significant transfers of wealth, defaulting and bankruptcy (Tropeano 2012).

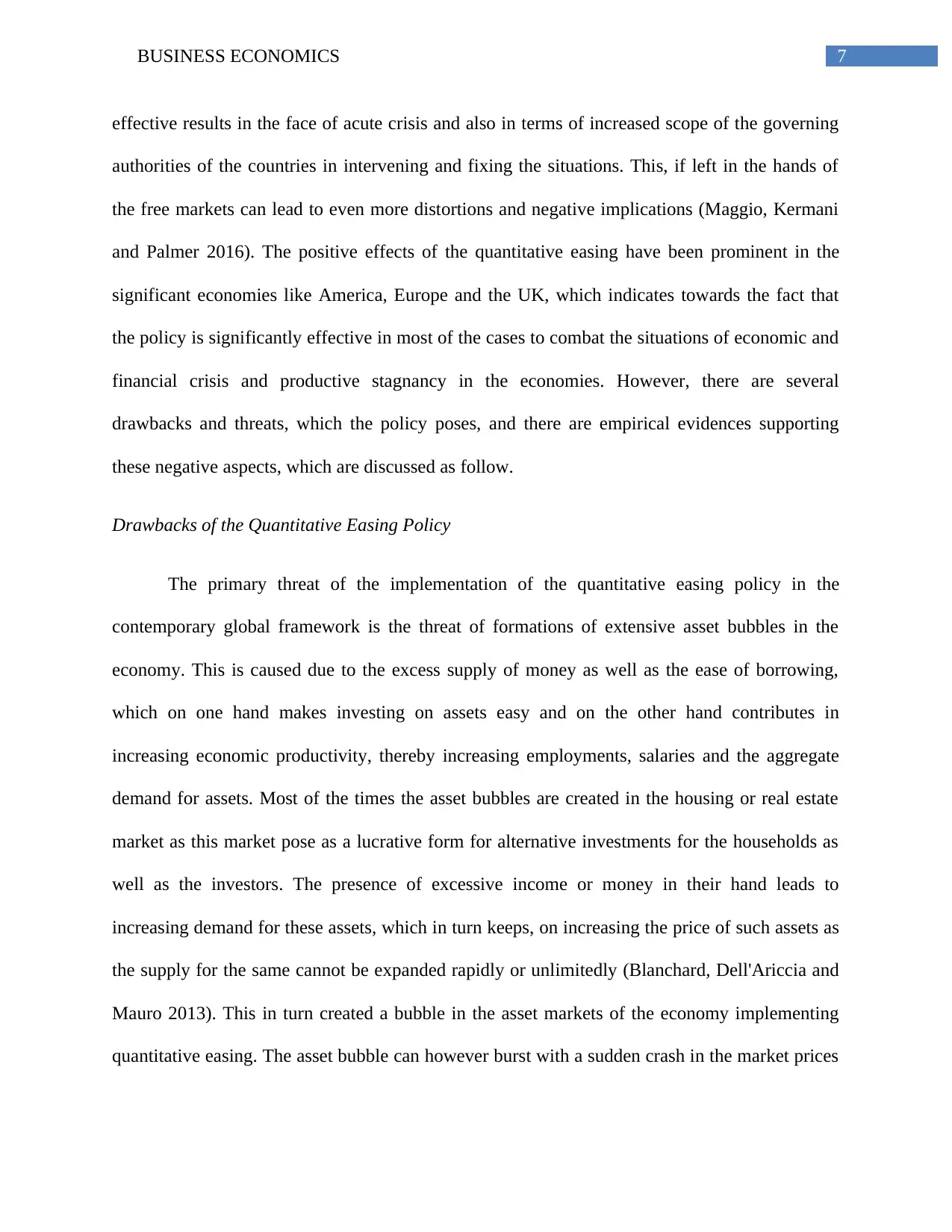

There are evidences of the risks of such housing bubbles in the contemporary economic

scenario. In the last few years, the housing markets are found to be overheating in the economies

of Germany, UK and Norway, much of which can be attributed to the quantitative easing policy

that has been taken up by the European Central Bank. The policy of the bank of buying euro-

dominated assets of almost 60 million Euros every month has led to the dip in the value of the

government bonds of the countries, which is making the asset market more lucrative for the

investors, thereby raising the prices of the housings, which can be seen from the figure below:

Figure 3: Increase in the housing prices over the years

(Source: Moodys.com, 2018)

Thus from the above figure, it can be asserted that under the policy of quantitative easing,

there remains a threat of creation of bubbles in the asset markets, which if burst can lead to

of those assets, which in turn can have hugely negative implications on the society in terms of

significant transfers of wealth, defaulting and bankruptcy (Tropeano 2012).

There are evidences of the risks of such housing bubbles in the contemporary economic

scenario. In the last few years, the housing markets are found to be overheating in the economies

of Germany, UK and Norway, much of which can be attributed to the quantitative easing policy

that has been taken up by the European Central Bank. The policy of the bank of buying euro-

dominated assets of almost 60 million Euros every month has led to the dip in the value of the

government bonds of the countries, which is making the asset market more lucrative for the

investors, thereby raising the prices of the housings, which can be seen from the figure below:

Figure 3: Increase in the housing prices over the years

(Source: Moodys.com, 2018)

Thus from the above figure, it can be asserted that under the policy of quantitative easing,

there remains a threat of creation of bubbles in the asset markets, which if burst can lead to

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9BUSINESS ECONOMICS

immense negative implications for the markets as well as for the economy as a whole (Claeys

and Darvas 2015).

Conclusion

From the above discussion, it can be ascertained that, quantitative easing as an

expansionary monetary policy has gained immense popularity across the significant economies,

especially post the Financial Crisis Period (2007-2008), due to its prospective abilities of taking

the economies out of stagnancy or recessionary situations. The policy has shown some robust

effectiveness in the economies across the world, as is evident from their GDP and other

economic growth statistics. However, the presence of such policy has the potential to create asset

bubbles in the economies, as is evident from the potential bubbles created in different economies

in the contemporary period. This in turn, has the threat to burst which can take the economy

down again on the path of monetary imbalance, distortions, stagnations and bankruptcy.

immense negative implications for the markets as well as for the economy as a whole (Claeys

and Darvas 2015).

Conclusion

From the above discussion, it can be ascertained that, quantitative easing as an

expansionary monetary policy has gained immense popularity across the significant economies,

especially post the Financial Crisis Period (2007-2008), due to its prospective abilities of taking

the economies out of stagnancy or recessionary situations. The policy has shown some robust

effectiveness in the economies across the world, as is evident from their GDP and other

economic growth statistics. However, the presence of such policy has the potential to create asset

bubbles in the economies, as is evident from the potential bubbles created in different economies

in the contemporary period. This in turn, has the threat to burst which can take the economy

down again on the path of monetary imbalance, distortions, stagnations and bankruptcy.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10BUSINESS ECONOMICS

References

Agénor, P.R. and Montiel, P.J., 2015. Development macroeconomics. Princeton university press.

Blanchard, O.J., Dell'Ariccia, M.G. and Mauro, M.P., 2013. Rethinking macro policy II: getting

granular. International Monetary Fund.

Blinder, A.S., 2010. Quantitative easing: entrance and exit strategies. Federal Reserve Bank of

St. Louis Review, 92(6), pp.465-479.

Christensen, J.H. and Rudebusch, G.D., 2012. The response of interest rates to US and UK

quantitative easing. The Economic Journal, 122(564).

Claeys, G. and Darvas, Z.M., 2015. The financial stability risks of ultra-loose monetary

policy (No. 2015/03). Bruegel Policy Contribution.

Fawley, B.W. and Neely, C.J., 2013. Four stories of quantitative easing. Federal Reserve Bank of

St. Louis Review, 95(1), pp.51-88.

Hausken, K. and Ncube, M., 2013. Quantitative Easing and its Impact in the US, Japan, the UK

and Europe.

Joyce, M., Miles, D., Scott, A. and Vayanos, D., 2012. Quantitative easing and unconventional

monetary policy–an introduction. The Economic Journal, 122(564).

Kapetanios, G., Mumtaz, H., Stevens, I. and Theodoridis, K., 2012. Assessing the economy‐wide

effects of quantitative easing. The Economic Journal, 122(564).

Maggio, M.D., Kermani, A. and Palmer, C., 2016. How quantitative easing works: Evidence on

the refinancing channel (No. w22638). National Bureau of Economic Research.

References

Agénor, P.R. and Montiel, P.J., 2015. Development macroeconomics. Princeton university press.

Blanchard, O.J., Dell'Ariccia, M.G. and Mauro, M.P., 2013. Rethinking macro policy II: getting

granular. International Monetary Fund.

Blinder, A.S., 2010. Quantitative easing: entrance and exit strategies. Federal Reserve Bank of

St. Louis Review, 92(6), pp.465-479.

Christensen, J.H. and Rudebusch, G.D., 2012. The response of interest rates to US and UK

quantitative easing. The Economic Journal, 122(564).

Claeys, G. and Darvas, Z.M., 2015. The financial stability risks of ultra-loose monetary

policy (No. 2015/03). Bruegel Policy Contribution.

Fawley, B.W. and Neely, C.J., 2013. Four stories of quantitative easing. Federal Reserve Bank of

St. Louis Review, 95(1), pp.51-88.

Hausken, K. and Ncube, M., 2013. Quantitative Easing and its Impact in the US, Japan, the UK

and Europe.

Joyce, M., Miles, D., Scott, A. and Vayanos, D., 2012. Quantitative easing and unconventional

monetary policy–an introduction. The Economic Journal, 122(564).

Kapetanios, G., Mumtaz, H., Stevens, I. and Theodoridis, K., 2012. Assessing the economy‐wide

effects of quantitative easing. The Economic Journal, 122(564).

Maggio, M.D., Kermani, A. and Palmer, C., 2016. How quantitative easing works: Evidence on

the refinancing channel (No. w22638). National Bureau of Economic Research.

11BUSINESS ECONOMICS

Mankiw, N.G., 2014. Principles of macroeconomics. Cengage Learning.

Martin, C. and Milas, C., 2012. Quantitative easing: a sceptical survey. Oxford Review of

Economic Policy, 28(4), pp.750-764.

Moodys.com (2018). Moody's Public Sector Europe: UK housing associations' stable outlook

for 2018 supported by more favourable policy environment and effective cost management.

[online] Moodys.com. Available at: https://www.moodys.com/research/Moodys-Public-Sector-

Europe-UK-housing-associations-stable-outlook-for--PR_376046 [Accessed 17 Jan. 2018].

Pesaran, M.H. and Smith, R.P., 2016. Counterfactual analysis in macroeconometrics: An

empirical investigation into the effects of quantitative easing. Research in Economics, 70(2),

pp.262-280.

Schmidt, S., 2013. Optimal monetary and fiscal policy with a zero bound on nominal interest

rates. Journal of Money, Credit and Banking, 45(7), pp.1335-1350.

Tradingeconomics.com (2018). United States GDP Growth Rate | 1947-2018 | Data | Chart |

Calendar. [online] Tradingeconomics.com. Available at: https://tradingeconomics.com/united-

states/gdp-growth [Accessed 17 Jan. 2018].

Tradingeconomics.com (2018). United States Unemployment Rate | 1948-2018 | Data | Chart |

Calendar. [online] Tradingeconomics.com. Available at: https://tradingeconomics.com/united-

states/unemployment-rate [Accessed 17 Jan. 2018].

Tropeano, D., 2012. 11. Quantitative easing in the United States after the crisis: conflicting

views. Monetary Policy and Central Banking: New Directions in Post-Keynesian Theory, 227.

Mankiw, N.G., 2014. Principles of macroeconomics. Cengage Learning.

Martin, C. and Milas, C., 2012. Quantitative easing: a sceptical survey. Oxford Review of

Economic Policy, 28(4), pp.750-764.

Moodys.com (2018). Moody's Public Sector Europe: UK housing associations' stable outlook

for 2018 supported by more favourable policy environment and effective cost management.

[online] Moodys.com. Available at: https://www.moodys.com/research/Moodys-Public-Sector-

Europe-UK-housing-associations-stable-outlook-for--PR_376046 [Accessed 17 Jan. 2018].

Pesaran, M.H. and Smith, R.P., 2016. Counterfactual analysis in macroeconometrics: An

empirical investigation into the effects of quantitative easing. Research in Economics, 70(2),

pp.262-280.

Schmidt, S., 2013. Optimal monetary and fiscal policy with a zero bound on nominal interest

rates. Journal of Money, Credit and Banking, 45(7), pp.1335-1350.

Tradingeconomics.com (2018). United States GDP Growth Rate | 1947-2018 | Data | Chart |

Calendar. [online] Tradingeconomics.com. Available at: https://tradingeconomics.com/united-

states/gdp-growth [Accessed 17 Jan. 2018].

Tradingeconomics.com (2018). United States Unemployment Rate | 1948-2018 | Data | Chart |

Calendar. [online] Tradingeconomics.com. Available at: https://tradingeconomics.com/united-

states/unemployment-rate [Accessed 17 Jan. 2018].

Tropeano, D., 2012. 11. Quantitative easing in the United States after the crisis: conflicting

views. Monetary Policy and Central Banking: New Directions in Post-Keynesian Theory, 227.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.