University Finance: Rio Tinto Dividend Discount Model Analysis Report

VerifiedAdded on 2022/09/18

|13

|4144

|24

Report

AI Summary

This report provides a comprehensive analysis of Rio Tinto using the Dividend Discount Model (DDM). It begins with rationales for selecting Rio Tinto and the DDM, followed by an overview of Rio Tinto's business operations and the suitability of the DDM for valuation. The report justifies the choice of a three-stage dividend growth model and details the determination of the dividend growth rate, including methods for estimation and relevant calculations. It then estimates the required rate of return using the Capital Asset Pricing Model (CAPM) and interprets the estimation results. The report calculates Rio Tinto's intrinsic value based on the DDM, discusses the findings, and concludes with a summary of the estimation results and a comparison of CAPM and DDM. References are included to support the analysis.

Running head: REPORT 0

RIO TINTO

APRIL 15, 2020

STUDENT DETAILS

RIO TINTO

APRIL 15, 2020

STUDENT DETAILS

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REPORT 1

Contents

Rationales for selection of company and selection of Dividend Discount Model (DDM) –........................2

Brief overview of Rio Tinto....................................................................................................................2

Suitability of Dividend Discount Model (DDM) for Rio Tinto...............................................................2

Justification for the decision on the number of stages of dividend growth..............................................3

Determination of dividend growth rate -......................................................................................................4

Method of estimating dividend growth rate.............................................................................................4

Workings of deriving dividend growth rate.............................................................................................5

Estimation of required rate of return using OLS method and interpretation of estimation results –............6

Specification and estimation of the model...............................................................................................6

Discussion of the estimated results..........................................................................................................8

Calculation of Intrinsic value of Rio Tinto –...............................................................................................8

Discussion and conclusion...........................................................................................................................9

Summary of estimation results................................................................................................................9

Analysis of CAPM and Dividend Discount Model................................................................................10

References.................................................................................................................................................12

Contents

Rationales for selection of company and selection of Dividend Discount Model (DDM) –........................2

Brief overview of Rio Tinto....................................................................................................................2

Suitability of Dividend Discount Model (DDM) for Rio Tinto...............................................................2

Justification for the decision on the number of stages of dividend growth..............................................3

Determination of dividend growth rate -......................................................................................................4

Method of estimating dividend growth rate.............................................................................................4

Workings of deriving dividend growth rate.............................................................................................5

Estimation of required rate of return using OLS method and interpretation of estimation results –............6

Specification and estimation of the model...............................................................................................6

Discussion of the estimated results..........................................................................................................8

Calculation of Intrinsic value of Rio Tinto –...............................................................................................8

Discussion and conclusion...........................................................................................................................9

Summary of estimation results................................................................................................................9

Analysis of CAPM and Dividend Discount Model................................................................................10

References.................................................................................................................................................12

REPORT 2

Rationales for selection of entity and selection of DDM –

The rationales for choosing Rio Tinto as a company and dividend discount model are discussed

below:

Brief overview of Rio Tinto

Rio Tinto is listed mining as well as exploration organisation in Australia and United Kingdom.

Rio Tinto operates its business of mining, finding and processing mineral sources. It is second

biggest metal & mining company of the world, after BHP Billiton. The entity is registered

at London Stock Exchange as well as ASX. It has joint headquarters in both

Melbourne (‘Limited’ in Australia) as well as London (international & ‘PLC’). The divisions of

the organisation include aluminium, energy and minerals, Iron Ore, Copper, and Diamond, along

with different functions. It can see that the company also runs the business of the By-products,

such as gold, lead along with silver. It runs business of iron ore and supplies international sea

borne iron ore trade. The operations related to Iron Ore are placed in Pilbara area of Western

Australia. It can see that operations cover about 5 iron ore products along with 4 port terminals.

The business of aluminium covers alumina refinery, aluminium smelters, as well as bauxite

mines. The bauxite mines are situated in Brazil, Guinea along with Australia. The Copper &

Diamond division has managed several operations in Canada, Mongolia, USA, and Canada.

Additionally, the company runs its non-administrated operations in Indonesia along with Chile.

On the other hand, the energy and minerals segment contains refining, mining, as well as

marketing processes through the subdivisions involving borates, pellets, titanium dioxide, iron

ore concentrate along with uranium (Reuters, 2019).

Suitability of Dividend Discount Model for Rio Tinto

Dividend discount model is considered as quantitative methodology. This method is useful to

determine the stock’s price based on assumption that current price is worth sum of

upcoming dividends while discounted again to PV. This model helps to determine FV of stock

regardless unusual marketing condition and considers dividend pay out elements along with

expected return of marketplace. In a case while value determined from DDM is less in

comparison of current stock price, in that case the stocks are overvalued. In this way, the

overvalued stocks are qualified for purchase, and vice-versa (Bask, 2019).

Rationales for selection of entity and selection of DDM –

The rationales for choosing Rio Tinto as a company and dividend discount model are discussed

below:

Brief overview of Rio Tinto

Rio Tinto is listed mining as well as exploration organisation in Australia and United Kingdom.

Rio Tinto operates its business of mining, finding and processing mineral sources. It is second

biggest metal & mining company of the world, after BHP Billiton. The entity is registered

at London Stock Exchange as well as ASX. It has joint headquarters in both

Melbourne (‘Limited’ in Australia) as well as London (international & ‘PLC’). The divisions of

the organisation include aluminium, energy and minerals, Iron Ore, Copper, and Diamond, along

with different functions. It can see that the company also runs the business of the By-products,

such as gold, lead along with silver. It runs business of iron ore and supplies international sea

borne iron ore trade. The operations related to Iron Ore are placed in Pilbara area of Western

Australia. It can see that operations cover about 5 iron ore products along with 4 port terminals.

The business of aluminium covers alumina refinery, aluminium smelters, as well as bauxite

mines. The bauxite mines are situated in Brazil, Guinea along with Australia. The Copper &

Diamond division has managed several operations in Canada, Mongolia, USA, and Canada.

Additionally, the company runs its non-administrated operations in Indonesia along with Chile.

On the other hand, the energy and minerals segment contains refining, mining, as well as

marketing processes through the subdivisions involving borates, pellets, titanium dioxide, iron

ore concentrate along with uranium (Reuters, 2019).

Suitability of Dividend Discount Model for Rio Tinto

Dividend discount model is considered as quantitative methodology. This method is useful to

determine the stock’s price based on assumption that current price is worth sum of

upcoming dividends while discounted again to PV. This model helps to determine FV of stock

regardless unusual marketing condition and considers dividend pay out elements along with

expected return of marketplace. In a case while value determined from DDM is less in

comparison of current stock price, in that case the stocks are overvalued. In this way, the

overvalued stocks are qualified for purchase, and vice-versa (Bask, 2019).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REPORT 3

Further, DDM is suitable valuation methodology for Rio Tinto. It uses DDM for calculating its

intrinsic value because of theory that stock’s price is weighty of amount of discounted future

payment of dividend. It can see that at a time of making long-term investment, this can be

rationally found that only cash flow received from publicly traded company like Rio Tinto would

be dividends, until selling of stocks. The DDM is appropriate model for a company to determine

worth of the stocks. In different terms, the dividend discount model is considered as method of

valuation method to get intrinsic value through discounted expected dividend that Rio Tinto

would be providing (to shareholder in upcoming period) to the PV (Agosto, Mainini and

Moretto, 2019).

Furthermore, by using the dividend discount model, Rio Tinto discusses that stock’s value has to

be PV of expected dividend above the period. In this way, this model can be seen as strength of

company. This model is useful method for Rio Tinto to evaluate the stocks, for the reason that it

is direct as well as easy method of the valuation of stocks. It states how value of stock can be

determined by easy approach of discounting future cash flow.

Justification for choice regarding number of dividend growth’s level

It can see that three-stage model utilises the expected rate for discounting future income of

dividends. It renders the present value. Three-stage dividend discount model is much like its

unpretentious complements, like two-stage model, H-Model along with Gordon Growth Model.

In actual, three-stage model is fundamentally the mixture of the above-discussed three models,

which is aimed at eliminating certain drawbacks essential to these formulas (Gacus and Hinlo,

2018).

The Gordon Growth Model is the basis for all of these discount formulas. However, the main

shortcoming of Gordon Growth Model is its inherent straightforwardness. It is found that this

model is not specifically correct for the reason that it supposes that dividend grows at the

constant rate continually. On the other hand, the H-Model as well as two-stage model permits to

Further, DDM is suitable valuation methodology for Rio Tinto. It uses DDM for calculating its

intrinsic value because of theory that stock’s price is weighty of amount of discounted future

payment of dividend. It can see that at a time of making long-term investment, this can be

rationally found that only cash flow received from publicly traded company like Rio Tinto would

be dividends, until selling of stocks. The DDM is appropriate model for a company to determine

worth of the stocks. In different terms, the dividend discount model is considered as method of

valuation method to get intrinsic value through discounted expected dividend that Rio Tinto

would be providing (to shareholder in upcoming period) to the PV (Agosto, Mainini and

Moretto, 2019).

Furthermore, by using the dividend discount model, Rio Tinto discusses that stock’s value has to

be PV of expected dividend above the period. In this way, this model can be seen as strength of

company. This model is useful method for Rio Tinto to evaluate the stocks, for the reason that it

is direct as well as easy method of the valuation of stocks. It states how value of stock can be

determined by easy approach of discounting future cash flow.

Justification for choice regarding number of dividend growth’s level

It can see that three-stage model utilises the expected rate for discounting future income of

dividends. It renders the present value. Three-stage dividend discount model is much like its

unpretentious complements, like two-stage model, H-Model along with Gordon Growth Model.

In actual, three-stage model is fundamentally the mixture of the above-discussed three models,

which is aimed at eliminating certain drawbacks essential to these formulas (Gacus and Hinlo,

2018).

The Gordon Growth Model is the basis for all of these discount formulas. However, the main

shortcoming of Gordon Growth Model is its inherent straightforwardness. It is found that this

model is not specifically correct for the reason that it supposes that dividend grows at the

constant rate continually. On the other hand, the H-Model as well as two-stage model permits to

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REPORT 4

change rate of dividend growth. However, only the H-Model gives permission to make

incremental modifications in place of sharp shifting from one constant rate towards other

constant rate. It can see that two-stage model is not helpful to create these incremental changes.

In this way, three-stage model includes the components of all other dividend growth models like

H model along with two stage model. In this way, the difficulty of the formula along with

several growth rates it can provide, this is most likely of other methods to state stock’s value

depended on real information of dividend (Anwar and Kumar, 2018).

Determination of growth rate of dividend -

It is believed that the company pays regular dividend under the dividend discount model. For this

reason, it is essential to determine the dividend growth rate (Annual report, 2019). It can see that

the growth rate is key input of formula using under dividend discount model. The method as well

as working of dividend growth rate is discussed below -

Method to estimate growth rate

It is important to review financial statement or results, as well as perspective of entity at period

of assessment its capability to pay future dividends (Desantes, 2020). It can say that the dividend

investors frequently review the past of enhancing dividends as the positive signal for the stocks.

The main reason is that the dividend’s reduction may be hurtful for the stock prices of company.

The organisation normally enhances the dividend only while it requires keeping high dividend

pay-out. As per this, the dividend growth rate is useful to determine the pricing of security. This

is very significant variable in the Dividend Discount Model (Yao and Kelei, 2019). This rate is

an average percentage the entity enhanced its dividend annually over the historical period.

Therefore, the strong dividend growth rate does not assure the profitable investments, however

this renders the idea of the records of accomplishment of company. An easy way to determine

dividend growth rate is to search growth rates for distributed dividend (Hatemi-J and El-Khatib,

2018). This formula may be utilised to calculate growth rate –

Dividend growth rate = D2/D1 – 1

On the other hand, in certain circumstances, like in finding growth rate in DDM, it is required to

come about the forward-looking approach to find dividend growth rate. In this situation, there are

change rate of dividend growth. However, only the H-Model gives permission to make

incremental modifications in place of sharp shifting from one constant rate towards other

constant rate. It can see that two-stage model is not helpful to create these incremental changes.

In this way, three-stage model includes the components of all other dividend growth models like

H model along with two stage model. In this way, the difficulty of the formula along with

several growth rates it can provide, this is most likely of other methods to state stock’s value

depended on real information of dividend (Anwar and Kumar, 2018).

Determination of growth rate of dividend -

It is believed that the company pays regular dividend under the dividend discount model. For this

reason, it is essential to determine the dividend growth rate (Annual report, 2019). It can see that

the growth rate is key input of formula using under dividend discount model. The method as well

as working of dividend growth rate is discussed below -

Method to estimate growth rate

It is important to review financial statement or results, as well as perspective of entity at period

of assessment its capability to pay future dividends (Desantes, 2020). It can say that the dividend

investors frequently review the past of enhancing dividends as the positive signal for the stocks.

The main reason is that the dividend’s reduction may be hurtful for the stock prices of company.

The organisation normally enhances the dividend only while it requires keeping high dividend

pay-out. As per this, the dividend growth rate is useful to determine the pricing of security. This

is very significant variable in the Dividend Discount Model (Yao and Kelei, 2019). This rate is

an average percentage the entity enhanced its dividend annually over the historical period.

Therefore, the strong dividend growth rate does not assure the profitable investments, however

this renders the idea of the records of accomplishment of company. An easy way to determine

dividend growth rate is to search growth rates for distributed dividend (Hatemi-J and El-Khatib,

2018). This formula may be utilised to calculate growth rate –

Dividend growth rate = D2/D1 – 1

On the other hand, in certain circumstances, like in finding growth rate in DDM, it is required to

come about the forward-looking approach to find dividend growth rate. In this situation, there are

REPORT 5

three forward-looking approaches to find dividend growth rate. These three forward-looking

dividend growth rate approaches are explained as follows –

1. Historical growth rate – with help of historical growth rate, the arithmetic average of

the rates can be calculated easily (Heatone, 2020). In addition, the company can also

utilise historical growth rate for calculating CAGR (compound annual growth rate).

2. Detect the dividend growth rate prevailing in same industry where organisation

runs – it is also a good way to take dividend growth rate of industry. Suppose that the

Average Dividend Growth Rate of industry where XYZ Company is operating at 7%. In

this way, this rate can also be used for MNL Company (Petrellies, 2019).

3. Determine sustainable growth rate – it is very easy way to determine the sustainable

growth rate. A maintainable dividend growth rate is considered as rate with the help of

which an entity may continue to develop without safeguarding the extra funds, like

lacking the extra money or providing new equities. This can see that return on equity is

measure of the profitability of corporation that considers annual return or net income of

entity divided by value of the total shareholder’s equities (Apergis and Rehman, 2018). In

addition, the return on equity conglomerates the balance sheet as well as income

statement as the net profit or net income is compared to the shareholder equity. The

sustainable dividend growth can be calculated as below –

Growth Rate = Return on equity*(1- pay-out ratio)

Working for calculation of dividend growth rate

In case of Rio Tinto, growth rate can be determined by using sustainable growth rate (Zhao and

Jin, 2018). A sustainable growth rate of Rio Tinto is calculated as follows –

(a) Dividend Growth Rate = Return on equity*(1-Dividend payout ratio)

= Return on equity*(1-Retention ratio)

= 15%*53%

= 8%

three forward-looking approaches to find dividend growth rate. These three forward-looking

dividend growth rate approaches are explained as follows –

1. Historical growth rate – with help of historical growth rate, the arithmetic average of

the rates can be calculated easily (Heatone, 2020). In addition, the company can also

utilise historical growth rate for calculating CAGR (compound annual growth rate).

2. Detect the dividend growth rate prevailing in same industry where organisation

runs – it is also a good way to take dividend growth rate of industry. Suppose that the

Average Dividend Growth Rate of industry where XYZ Company is operating at 7%. In

this way, this rate can also be used for MNL Company (Petrellies, 2019).

3. Determine sustainable growth rate – it is very easy way to determine the sustainable

growth rate. A maintainable dividend growth rate is considered as rate with the help of

which an entity may continue to develop without safeguarding the extra funds, like

lacking the extra money or providing new equities. This can see that return on equity is

measure of the profitability of corporation that considers annual return or net income of

entity divided by value of the total shareholder’s equities (Apergis and Rehman, 2018). In

addition, the return on equity conglomerates the balance sheet as well as income

statement as the net profit or net income is compared to the shareholder equity. The

sustainable dividend growth can be calculated as below –

Growth Rate = Return on equity*(1- pay-out ratio)

Working for calculation of dividend growth rate

In case of Rio Tinto, growth rate can be determined by using sustainable growth rate (Zhao and

Jin, 2018). A sustainable growth rate of Rio Tinto is calculated as follows –

(a) Dividend Growth Rate = Return on equity*(1-Dividend payout ratio)

= Return on equity*(1-Retention ratio)

= 15%*53%

= 8%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REPORT 6

Figure 1: Calculation of ROE –

ROE = Net income/Shareholder’s Equity

= 6972/45242

= 15%

Figure 2: Calculation of Retention ratio –

Retention ratio = (Earning per share –Dividend per share) / Earning per share

= (491.4-231)/491.4

= 53%

In this way, dividend growth rate of Rio Tinto is 8%.

Approximation of required rate of return using OLS model and interpretation of estimation

results –

Specification and estimation of the model

In financial context, CAPM is considered as method utilising to determine the supposedly proper

required rate of return of assets, to take decision about adding the asset to the diversified

portfolio in proper manner (Habibi, Habibi and Habibi, 2016). The CAPM is method that defines

relation amid expected rate of return (specifically stock) as well as systematic risk. The return on

the investment is the unidentified variable, which has diversified values related to several

prospects along with risks of making investment in the securities (Kuantan, Siregar and Juhro,

2019). Additionally, the CAPM is greatly utilised through finance for pricing

uncertain security along with producing expected return for the asset provided uncertainty of the

assets along with cost of capital. An equation to calculate expected return of an asset provided

risk is below –

Required rate of return = Rf+ b*(Rm-Rf)

Here,

Rf = Market Risk-free rate

Figure 1: Calculation of ROE –

ROE = Net income/Shareholder’s Equity

= 6972/45242

= 15%

Figure 2: Calculation of Retention ratio –

Retention ratio = (Earning per share –Dividend per share) / Earning per share

= (491.4-231)/491.4

= 53%

In this way, dividend growth rate of Rio Tinto is 8%.

Approximation of required rate of return using OLS model and interpretation of estimation

results –

Specification and estimation of the model

In financial context, CAPM is considered as method utilising to determine the supposedly proper

required rate of return of assets, to take decision about adding the asset to the diversified

portfolio in proper manner (Habibi, Habibi and Habibi, 2016). The CAPM is method that defines

relation amid expected rate of return (specifically stock) as well as systematic risk. The return on

the investment is the unidentified variable, which has diversified values related to several

prospects along with risks of making investment in the securities (Kuantan, Siregar and Juhro,

2019). Additionally, the CAPM is greatly utilised through finance for pricing

uncertain security along with producing expected return for the asset provided uncertainty of the

assets along with cost of capital. An equation to calculate expected return of an asset provided

risk is below –

Required rate of return = Rf+ b*(Rm-Rf)

Here,

Rf = Market Risk-free rate

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REPORT 7

Rm= Market rate of return

Rm-Rf = Market premium

b = Beta

An investor expects to be remunerated for risks as well as TVM. As per CAPM, a risk free rate

accounts for TVM (Sattar, 2017). The different elements of formula of capital asset pricing

model are responsible for the investors considering additional risks. In addition, the beta of

potential investment is degree of how much risk investment would be added to the portfolio that

considers as marketplace. In a case when the stocks are chancier in comparison of market, this

would contain the beta higher than 1. On the other hand, when the stocks have beta of more than

one, an equation supposes this would decrease the portfolio’s risk. Subsequently, the beta of

stock is multiplied by market risk premium. It is resulted into the return expected from

marketplace over the risk free rate. The risk free rate is added to product of beta of stock along

with market risk premium. Market Premium measures expected rate of return on investment. For

the prospective investors, the perfect scenario for the risk based investment will be higher rate of

return with possible smaller risk. There are 3 main concepts to the market premium. These are

needed market premium, historical market premium as well as expected market premium.

Market premium of United Kingdom is 5.60% (Bao and Feng, 2018).

In addition, the risk free rate states interest the investors will suppose from the risk

free investment above the particular time (Pandya, 2016). Thus, the actual risk free rate can be

evaluated by lessening present inflation rate from the Treasury bond return by matching the

investment’s term. It is clear that the risk-free interest rate is considered as rate of return of the

theoretical investment having no economic loss’s uncertainty, over the provided time. Since the

risk free rate may be attained with no any hazard, any other investment having some risk would

have to get high rate of return for inducing the investor for holding this. It can see that risk free

rate of United Kingdom is 1.51% (Yahoo finance).

Besides, the result should give the investors the discount rate or required rate of return that they

may utilise to get the asset’s value. It can say that the main aim of using the formula of CAPM or

capital asset pricing model is to make assessment whether the stocks are valued in fair term,

while the comparison is made between expected return along with time value of money (TVM).

Rm= Market rate of return

Rm-Rf = Market premium

b = Beta

An investor expects to be remunerated for risks as well as TVM. As per CAPM, a risk free rate

accounts for TVM (Sattar, 2017). The different elements of formula of capital asset pricing

model are responsible for the investors considering additional risks. In addition, the beta of

potential investment is degree of how much risk investment would be added to the portfolio that

considers as marketplace. In a case when the stocks are chancier in comparison of market, this

would contain the beta higher than 1. On the other hand, when the stocks have beta of more than

one, an equation supposes this would decrease the portfolio’s risk. Subsequently, the beta of

stock is multiplied by market risk premium. It is resulted into the return expected from

marketplace over the risk free rate. The risk free rate is added to product of beta of stock along

with market risk premium. Market Premium measures expected rate of return on investment. For

the prospective investors, the perfect scenario for the risk based investment will be higher rate of

return with possible smaller risk. There are 3 main concepts to the market premium. These are

needed market premium, historical market premium as well as expected market premium.

Market premium of United Kingdom is 5.60% (Bao and Feng, 2018).

In addition, the risk free rate states interest the investors will suppose from the risk

free investment above the particular time (Pandya, 2016). Thus, the actual risk free rate can be

evaluated by lessening present inflation rate from the Treasury bond return by matching the

investment’s term. It is clear that the risk-free interest rate is considered as rate of return of the

theoretical investment having no economic loss’s uncertainty, over the provided time. Since the

risk free rate may be attained with no any hazard, any other investment having some risk would

have to get high rate of return for inducing the investor for holding this. It can see that risk free

rate of United Kingdom is 1.51% (Yahoo finance).

Besides, the result should give the investors the discount rate or required rate of return that they

may utilise to get the asset’s value. It can say that the main aim of using the formula of CAPM or

capital asset pricing model is to make assessment whether the stocks are valued in fair term,

while the comparison is made between expected return along with time value of money (TVM).

REPORT 8

Expected return of CAPM is utilised for discounting expected dividend along with capital

increment in the stock above anticipated holding period (Bao, Diks and Li, 2018). Further, the

capital asset pricing model as well as OLS method both are same thing. In different term, OLS is

considered as same thing as a linear prediction. CAPM is a linear model to calculate proper

return of assets provided the non-diversifiable risks. OLS is actually the methodology to solve

some categories of the linear model. Therefore, the OLS may be utilised upon the capital asset

pricing model. However, this is utilised on various other models as well. It can see that capital

asset pricing model looks like simpler linear regression model (Gacus and Hinlo, 2018).

Discussion of the estimated results

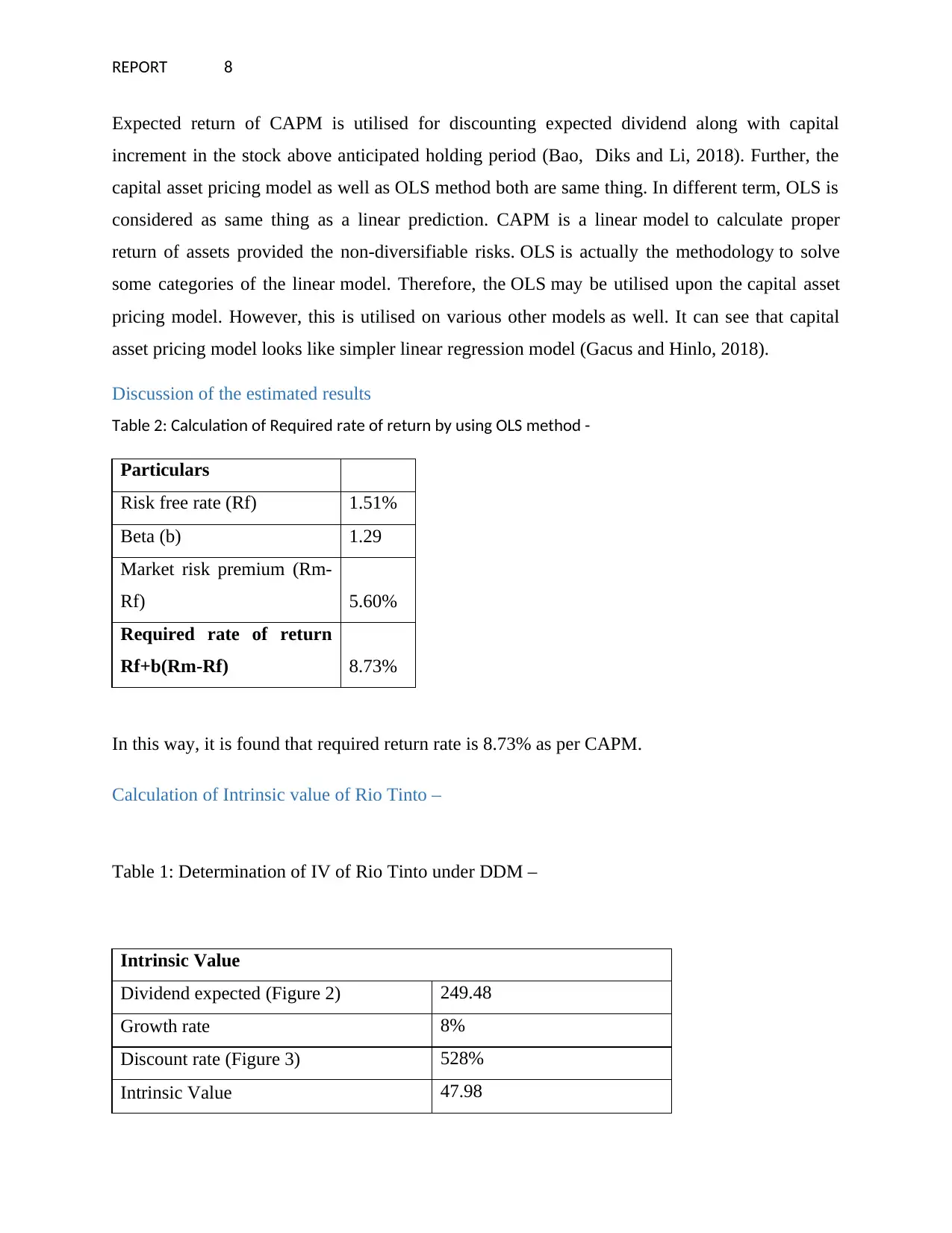

Table 2: Calculation of Required rate of return by using OLS method -

Particulars

Risk free rate (Rf) 1.51%

Beta (b) 1.29

Market risk premium (Rm-

Rf) 5.60%

Required rate of return

Rf+b(Rm-Rf) 8.73%

In this way, it is found that required return rate is 8.73% as per CAPM.

Calculation of Intrinsic value of Rio Tinto –

Table 1: Determination of IV of Rio Tinto under DDM –

Intrinsic Value

Dividend expected (Figure 2) 249.48

Growth rate 8%

Discount rate (Figure 3) 528%

Intrinsic Value 47.98

Expected return of CAPM is utilised for discounting expected dividend along with capital

increment in the stock above anticipated holding period (Bao, Diks and Li, 2018). Further, the

capital asset pricing model as well as OLS method both are same thing. In different term, OLS is

considered as same thing as a linear prediction. CAPM is a linear model to calculate proper

return of assets provided the non-diversifiable risks. OLS is actually the methodology to solve

some categories of the linear model. Therefore, the OLS may be utilised upon the capital asset

pricing model. However, this is utilised on various other models as well. It can see that capital

asset pricing model looks like simpler linear regression model (Gacus and Hinlo, 2018).

Discussion of the estimated results

Table 2: Calculation of Required rate of return by using OLS method -

Particulars

Risk free rate (Rf) 1.51%

Beta (b) 1.29

Market risk premium (Rm-

Rf) 5.60%

Required rate of return

Rf+b(Rm-Rf) 8.73%

In this way, it is found that required return rate is 8.73% as per CAPM.

Calculation of Intrinsic value of Rio Tinto –

Table 1: Determination of IV of Rio Tinto under DDM –

Intrinsic Value

Dividend expected (Figure 2) 249.48

Growth rate 8%

Discount rate (Figure 3) 528%

Intrinsic Value 47.98

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REPORT 9

Share Price 47.99

Overvalued/undervalued

Overvalued with minor

difference

Figure 2: Determination of expected dividend –

Expected Dividend (D1) = Current year dividend*(1+Growth rate)

= 231*(1+.08)

= 249.48 US cents

Figure 3: Calculation of discount rate –

Discount rate = (Dividend expected/current price of share) + rate of growth

= (249.48/47.99)+.08

= 528%

Discussion and conclusion

Summary of estimation results

The intrinsic value as well as market value are different manner for the valuation of organisation.

the market value is only the measurement of how much value of market of the entity, or how

much this will cost for purchasing this. It can say that the market value of the stocks is

considered as amount that investor has related to the company at the specific stage. In simpler

terms, it is a price that one can pay for purchasing the stock of publicly traded company. In

opposition, the intrinsic value is regarded as essential price of shares. It is found that it is

beneficial for Rio Tinto to calculate intrinsic valued under DDM. This is projected actual value

of the organisation notwithstanding the present market price of stock. It is required for

comparing market value as well as intrinsic value of company to get the better results. It is also

concluded that the price of market may be meaningfully lower of higher than stock’s intrinsic

value. In a case when it is higher in comparison of IV, in that matter stock is considered as

Share Price 47.99

Overvalued/undervalued

Overvalued with minor

difference

Figure 2: Determination of expected dividend –

Expected Dividend (D1) = Current year dividend*(1+Growth rate)

= 231*(1+.08)

= 249.48 US cents

Figure 3: Calculation of discount rate –

Discount rate = (Dividend expected/current price of share) + rate of growth

= (249.48/47.99)+.08

= 528%

Discussion and conclusion

Summary of estimation results

The intrinsic value as well as market value are different manner for the valuation of organisation.

the market value is only the measurement of how much value of market of the entity, or how

much this will cost for purchasing this. It can say that the market value of the stocks is

considered as amount that investor has related to the company at the specific stage. In simpler

terms, it is a price that one can pay for purchasing the stock of publicly traded company. In

opposition, the intrinsic value is regarded as essential price of shares. It is found that it is

beneficial for Rio Tinto to calculate intrinsic valued under DDM. This is projected actual value

of the organisation notwithstanding the present market price of stock. It is required for

comparing market value as well as intrinsic value of company to get the better results. It is also

concluded that the price of market may be meaningfully lower of higher than stock’s intrinsic

value. In a case when it is higher in comparison of IV, in that matter stock is considered as

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REPORT 10

overvalued. In opposition, when the market price is lower in comparison of the intrinsic value, it

can be considered as undervalued. It is also found that the investor always looks for undervalued

entities for the investment.

Additionally, from the above discussion it can also say that it is not correct to ignore the stock

that has low intrinsic value in comparison of current price of market. The investor is required to

consider different financial methods of fundamental evaluation to get proper results about the

company before investing in it. In this way, these financial tools are price per book ratio, ROE as

well as price earnings ratio. In this way, the investor can take the investment decision. The

market value is higher in comparison of IV if there is stronger requirement of investment, then it

is resulted into overvaluation. The opposite is correct if there is weak requirement of investment

that can be resulted into undervaluation of the entity. As per the above analysis, it can say that IV

of Rio Tinto is 47.98. In opposition, the current stock price of Rio Tinto is 47.99. This can see

that the current market price of company is above the calculated IV of company. This is clear to

say that the company is overvalued with the minor difference. It can say that the company is

overvalued because of the solid investment demand. However, there is not major difference

between market price and intrinsic value. So it can be beneficial for the investors to invest in Rio

Tinto.

Analysis of DDM and CAPM

DDM and CAPM are two methodologies to appraise investment value. CAPM is modern model

in comparison of the dividend discount model in term of marketplace risk. A key purpose is that

the dividend discount model stresses that investor who prefers to buy assets with high volatility,

should be recompensed with high return than investor who purchases less risky asset. As per the

above analysis, it is found that the required date of return under CAPM is 8.73%. In opposition,

the discount rate under the divided end discount model is 528%. In this way, the company should

choose the CAPM in comparison of DDM because CAPM model is mode simpler and flexible.

overvalued. In opposition, when the market price is lower in comparison of the intrinsic value, it

can be considered as undervalued. It is also found that the investor always looks for undervalued

entities for the investment.

Additionally, from the above discussion it can also say that it is not correct to ignore the stock

that has low intrinsic value in comparison of current price of market. The investor is required to

consider different financial methods of fundamental evaluation to get proper results about the

company before investing in it. In this way, these financial tools are price per book ratio, ROE as

well as price earnings ratio. In this way, the investor can take the investment decision. The

market value is higher in comparison of IV if there is stronger requirement of investment, then it

is resulted into overvaluation. The opposite is correct if there is weak requirement of investment

that can be resulted into undervaluation of the entity. As per the above analysis, it can say that IV

of Rio Tinto is 47.98. In opposition, the current stock price of Rio Tinto is 47.99. This can see

that the current market price of company is above the calculated IV of company. This is clear to

say that the company is overvalued with the minor difference. It can say that the company is

overvalued because of the solid investment demand. However, there is not major difference

between market price and intrinsic value. So it can be beneficial for the investors to invest in Rio

Tinto.

Analysis of DDM and CAPM

DDM and CAPM are two methodologies to appraise investment value. CAPM is modern model

in comparison of the dividend discount model in term of marketplace risk. A key purpose is that

the dividend discount model stresses that investor who prefers to buy assets with high volatility,

should be recompensed with high return than investor who purchases less risky asset. As per the

above analysis, it is found that the required date of return under CAPM is 8.73%. In opposition,

the discount rate under the divided end discount model is 528%. In this way, the company should

choose the CAPM in comparison of DDM because CAPM model is mode simpler and flexible.

REPORT 11

References

Agosto, A., Mainini, A. and Moretto, E., (2019) Stochastic dividend discount model: covariance

of random stock prices. Journal of Economics and Finance, 43(3), pp.552-568.

Annual report (2019) Rio Tinto. Available at: file:///C:/Users/System04090/Downloads/RT-

Annual-report-2019.pdf. [Access on 15/04/2019]

Anwar, M. and Kumar, S., (2018) CAPM-Empirical Evidence from the Indian Stock

Market. Indian Journal of Research in Capital Markets, 5(4), pp.38-52.

Apergis, N. and Rehman, M.U., (2018) Is CAPM a Behavioral Model? Estimating Sentiments

from Rationalism. Journal of Behavioral Finance, 19(4), pp.442-449

Bao, G. and Feng, G., (2018) Testing the Dividend Discount Model in Housing Markets: the

Role of Risk. The Journal of Real Estate Finance and Economics, 57(4), pp.677-701.

Bao, T., Diks, C. and Li, H. (2018) A generalized CAPM model with asymmetric power

distributed errors with an application to portfolio construction. Economic Modelling, 68, pp.611-

621.

Bask, M., (2019) Pure announcement and time effects in the dividend-discount model. The

Quarterly Review of Economics and Finance.

Desantes, J.M., Garcia-Oliver, J.M., Pastor, J.M. and Pandal, A., (2016) A comparison of diesel

sprays CFD modeling approaches: DDM versus Σ-Y Eulerian atomization model. Atomization

and Sprays, 26(7).

Gacus, R.B. and Hinlo, J.E., (2018) The Reliability of Constant Growth Dividend Discount

Model (DDM) in Valuation of Philippine Common Stocks. International Journal of Economics

& Management Sciences, 7.

Habibi, H., Habibi, R. and Habibi, H., (2016) Derivation of Kalman Filter Estimates Using

Bayesian Theory: Application in Time Varying Beta CAPM Model. Journal of Statistical and

Econometric Methods, 5(2), pp.1-16.

References

Agosto, A., Mainini, A. and Moretto, E., (2019) Stochastic dividend discount model: covariance

of random stock prices. Journal of Economics and Finance, 43(3), pp.552-568.

Annual report (2019) Rio Tinto. Available at: file:///C:/Users/System04090/Downloads/RT-

Annual-report-2019.pdf. [Access on 15/04/2019]

Anwar, M. and Kumar, S., (2018) CAPM-Empirical Evidence from the Indian Stock

Market. Indian Journal of Research in Capital Markets, 5(4), pp.38-52.

Apergis, N. and Rehman, M.U., (2018) Is CAPM a Behavioral Model? Estimating Sentiments

from Rationalism. Journal of Behavioral Finance, 19(4), pp.442-449

Bao, G. and Feng, G., (2018) Testing the Dividend Discount Model in Housing Markets: the

Role of Risk. The Journal of Real Estate Finance and Economics, 57(4), pp.677-701.

Bao, T., Diks, C. and Li, H. (2018) A generalized CAPM model with asymmetric power

distributed errors with an application to portfolio construction. Economic Modelling, 68, pp.611-

621.

Bask, M., (2019) Pure announcement and time effects in the dividend-discount model. The

Quarterly Review of Economics and Finance.

Desantes, J.M., Garcia-Oliver, J.M., Pastor, J.M. and Pandal, A., (2016) A comparison of diesel

sprays CFD modeling approaches: DDM versus Σ-Y Eulerian atomization model. Atomization

and Sprays, 26(7).

Gacus, R.B. and Hinlo, J.E., (2018) The Reliability of Constant Growth Dividend Discount

Model (DDM) in Valuation of Philippine Common Stocks. International Journal of Economics

& Management Sciences, 7.

Habibi, H., Habibi, R. and Habibi, H., (2016) Derivation of Kalman Filter Estimates Using

Bayesian Theory: Application in Time Varying Beta CAPM Model. Journal of Statistical and

Econometric Methods, 5(2), pp.1-16.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.