Queensland Cotton: Report on Business Level Strategy and Analysis

VerifiedAdded on 2023/01/19

|35

|8493

|33

Report

AI Summary

This report provides an in-depth analysis of Queensland Cotton, a leading Australian cotton marketing and ginning organization. It examines the company's business units, product lines, and revenue streams, highlighting the importance of its largest revenue units. The report delves into Queensland Cotton's business-level strategies, including cost leadership, differentiation, and integrated approaches, and analyzes its model of competitive reality within the Australian cotton industry. Furthermore, it outlines an implementation plan, an evaluation strategy, and offers recommendations for the future strategic direction of Queensland Cotton. The analysis covers the Australian Stock Exchange's impact, seasonal conditions, and cotton production statistics, providing a comprehensive overview of the company's operations and strategic positioning within the agribusiness sector. The report also references the Cotton Research and Development Corporation (CRDC) and its strategic plan for the cotton industry.

Queensland Cotton 1

QUEENSLAND COTTON

By (Name)

Class

Professor

College

City and State

QUEENSLAND COTTON

By (Name)

Class

Professor

College

City and State

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Queensland Cotton 2

Executive Summary

“Queensland Cotton Corporation Pty Ltd (Queensland Cotton)” was created in 1921, and is the

oldest Australia’s cotton marketing and ginning organization. Importantly, it is a crucial

supplier of premium cotton to the globe’s textile markets. Queensland specializes in all phases

of ginning and processing of cotton seed to the marketing process including acquisition, sales,

risk management, financing, and storage and classification of processed cotton. Queensland

Cotton’s enterprise has a vast knowledge in selling and buying of agricultural products.

Executive Summary

“Queensland Cotton Corporation Pty Ltd (Queensland Cotton)” was created in 1921, and is the

oldest Australia’s cotton marketing and ginning organization. Importantly, it is a crucial

supplier of premium cotton to the globe’s textile markets. Queensland specializes in all phases

of ginning and processing of cotton seed to the marketing process including acquisition, sales,

risk management, financing, and storage and classification of processed cotton. Queensland

Cotton’s enterprise has a vast knowledge in selling and buying of agricultural products.

Queensland Cotton 3

Table of Contents

INTRODUCTION………………………………………………………………………….4

1.1. Introduction…………………………………………………………………………….4

1.2. Objective………………………………………………………………………………..4

1.3. Scope of Report…………………………………………………………………….......5

ANALYSIS………………………………………………………………………………...5

2.1 Australian Stock Exchange…………………………………………………………..…5

2.2 Queensland Cotton……………………………………………………………………...8

2.2.1 Business Units and product and Service Lines………………………………………11

2.2.2 Business Revenue Units and the Importance of the Largest Revenue Units…………15

3.1 Business Level Strategies……………………………………………………………....17

3.1.1. Cost Leadership………………………………………………………………….…..17

3.1.2. Differentiation…………………………………………………………………….….19

3.1.3 Integrated Cost Leadership and Differentiation Strategy………………………….…20

3.1.4 Focus Technique……………………………………………………………...………22

4.1 The Business Level Approach of Queensland Cotton………………………………….25

5.1 Queensland Cotton Model of Competitive Reality in Australia……………………..…25

6.1 Implementation Plan of Queensland Cotton…………………………………...……….27

7.1 Evaluation Strategy of Queensland Cotton………………………………………..……27

8.1 Recommendation………………………………………………………………….…….28

9.1 Conclusion…………………………………………………………………………..…..29

Table of Contents

INTRODUCTION………………………………………………………………………….4

1.1. Introduction…………………………………………………………………………….4

1.2. Objective………………………………………………………………………………..4

1.3. Scope of Report…………………………………………………………………….......5

ANALYSIS………………………………………………………………………………...5

2.1 Australian Stock Exchange…………………………………………………………..…5

2.2 Queensland Cotton……………………………………………………………………...8

2.2.1 Business Units and product and Service Lines………………………………………11

2.2.2 Business Revenue Units and the Importance of the Largest Revenue Units…………15

3.1 Business Level Strategies……………………………………………………………....17

3.1.1. Cost Leadership………………………………………………………………….…..17

3.1.2. Differentiation…………………………………………………………………….….19

3.1.3 Integrated Cost Leadership and Differentiation Strategy………………………….…20

3.1.4 Focus Technique……………………………………………………………...………22

4.1 The Business Level Approach of Queensland Cotton………………………………….25

5.1 Queensland Cotton Model of Competitive Reality in Australia……………………..…25

6.1 Implementation Plan of Queensland Cotton…………………………………...……….27

7.1 Evaluation Strategy of Queensland Cotton………………………………………..……27

8.1 Recommendation………………………………………………………………….…….28

9.1 Conclusion…………………………………………………………………………..…..29

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Queensland Cotton 4

INTRODUCTION

1.1 Introduction

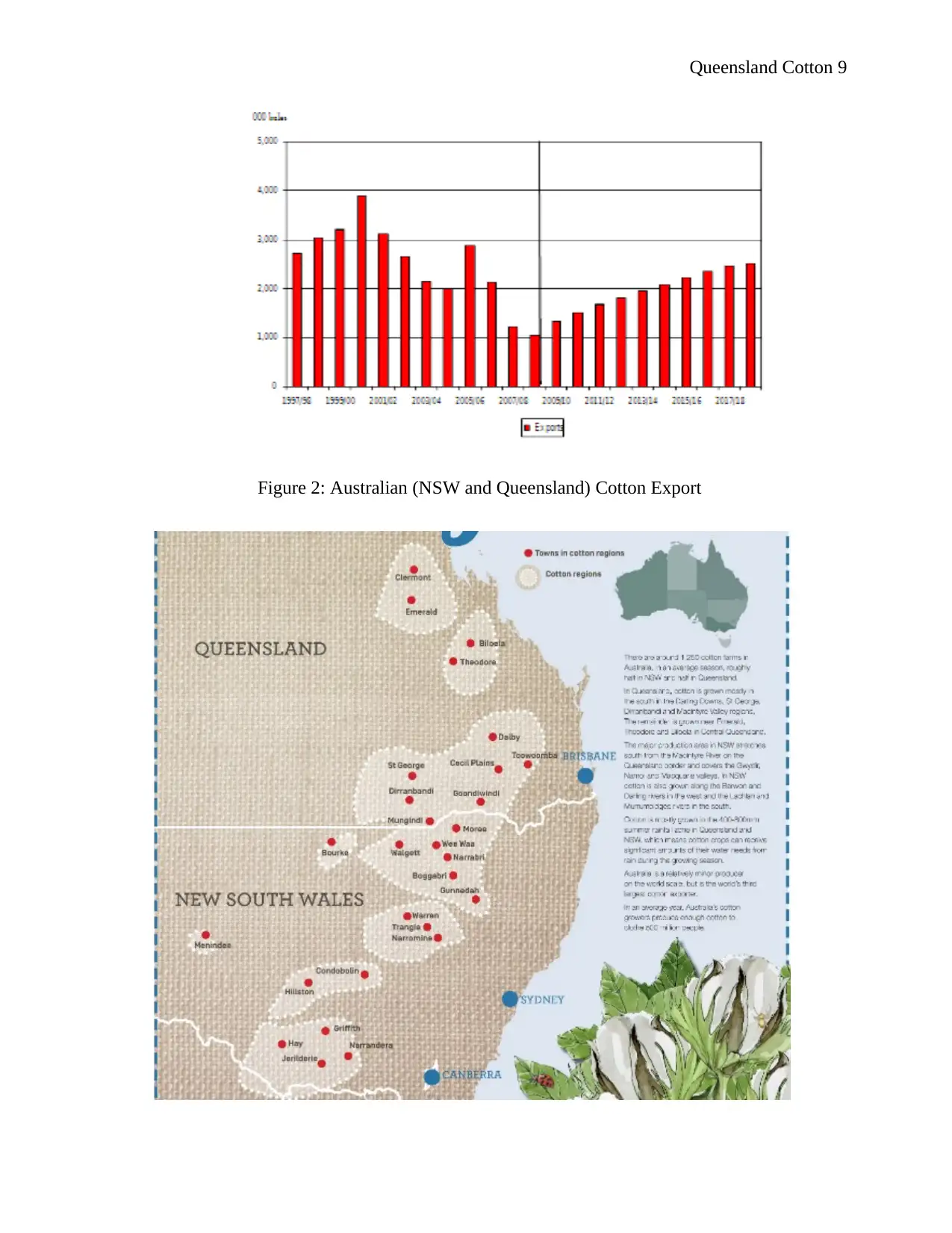

The primary production regions of cotton in Australia stretches from the Macintyre

River on the Queensland border and Macquarie and Namoi valleys. In Queensland, the cotton

grown majorly is in the south in the Macintyre, Darling Downs, and Dirranbandi Valley areas.

The Australian cotton grows seasonally for about six months starting from October, which is the

planting season to ending April, which is the picking season. Notably, irrigation water for

cotton production is limited, which is a primary issue. In addition, water utilization efficiency

has increased by about 240 percent from the 1970s. Alternatively, the best management

programs of cotton practice include “Integrated Pest Management” strategies, and

biotechnology use in minimizing pesticide use by over 85 percent from 2000 to 2010.

Furthermore, cotton production forecasts at approximately 4.8 million bales, while the harvested

region is predicted at 450,000 hectares from 2018 to 2019. The low production is as a result of

low rainfall in most growing areas, and cotton crop damage influenced by herbicide spray drift

over about 36,000 hectares. Conversely, the “Cotton Research and Development Corporation

(CRDC)” delivers outcomes in cotton “Research, Development, and Extension (RD&E)” on

behalf of all Australian cotton growers, and the Australian government. Importantly, CRDC

plays a vital role in the 2018 to 2023 Strategic Plan that aims at building a successful five-year

plan on providing a two billion dollars gross value of cotton production, which will benefit

Australian cotton growers.

1.2 Objective

INTRODUCTION

1.1 Introduction

The primary production regions of cotton in Australia stretches from the Macintyre

River on the Queensland border and Macquarie and Namoi valleys. In Queensland, the cotton

grown majorly is in the south in the Macintyre, Darling Downs, and Dirranbandi Valley areas.

The Australian cotton grows seasonally for about six months starting from October, which is the

planting season to ending April, which is the picking season. Notably, irrigation water for

cotton production is limited, which is a primary issue. In addition, water utilization efficiency

has increased by about 240 percent from the 1970s. Alternatively, the best management

programs of cotton practice include “Integrated Pest Management” strategies, and

biotechnology use in minimizing pesticide use by over 85 percent from 2000 to 2010.

Furthermore, cotton production forecasts at approximately 4.8 million bales, while the harvested

region is predicted at 450,000 hectares from 2018 to 2019. The low production is as a result of

low rainfall in most growing areas, and cotton crop damage influenced by herbicide spray drift

over about 36,000 hectares. Conversely, the “Cotton Research and Development Corporation

(CRDC)” delivers outcomes in cotton “Research, Development, and Extension (RD&E)” on

behalf of all Australian cotton growers, and the Australian government. Importantly, CRDC

plays a vital role in the 2018 to 2023 Strategic Plan that aims at building a successful five-year

plan on providing a two billion dollars gross value of cotton production, which will benefit

Australian cotton growers.

1.2 Objective

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Queensland Cotton 5

The report aims at providing an in-depth analysis of Queensland Cotton, and the business units

and product lines. Also, the report focuses on Queensland Cotton prioritizes on business

strategy, which keeps it ahead of its competition. In spite of that, the article addresses the

following;

1. Queensland Cotton business level approach.

2. Queensland Cotton model of competitive reality.

3. The implementation plan and assessment strategy of Queensland Cotton.

1.3 Scope of Report

The article focuses on Queensland Cotton and how it achieves the cost leadership and

differentiation approach. Also, the business revenue units of Queensland Cotton are provided.

ANALYSIS

2.1 Australian Stock Exchange

“Australia Bureau of Agricultural and Resource Economics (ABARE)” June 2012

estimated that the Australian cotton exports may increase by at least 11.5 percent in 2012 and

2013, which is about 1.2 million tonnes. The forecast in 2012 predicted a 26 percent decrease in

cotton planted areas at 442,000 hectares, while irrigated cotton regions decreased by seven

percent to 418,000 hectares, and the regions of dryland cotton fell by 85 percent to 23,000

hectares. Importantly, Australia is a net cotton exporter, and the prices reflect in USD terms.

The USD is a currency of international cotton trade, which Australian cotton exports denote it

by the US dollar. NSW and Queensland growers predominantly operate an Australian dollar-

denominated enterprise, and prefer to have their sales receipts in “AUD.”

The report aims at providing an in-depth analysis of Queensland Cotton, and the business units

and product lines. Also, the report focuses on Queensland Cotton prioritizes on business

strategy, which keeps it ahead of its competition. In spite of that, the article addresses the

following;

1. Queensland Cotton business level approach.

2. Queensland Cotton model of competitive reality.

3. The implementation plan and assessment strategy of Queensland Cotton.

1.3 Scope of Report

The article focuses on Queensland Cotton and how it achieves the cost leadership and

differentiation approach. Also, the business revenue units of Queensland Cotton are provided.

ANALYSIS

2.1 Australian Stock Exchange

“Australia Bureau of Agricultural and Resource Economics (ABARE)” June 2012

estimated that the Australian cotton exports may increase by at least 11.5 percent in 2012 and

2013, which is about 1.2 million tonnes. The forecast in 2012 predicted a 26 percent decrease in

cotton planted areas at 442,000 hectares, while irrigated cotton regions decreased by seven

percent to 418,000 hectares, and the regions of dryland cotton fell by 85 percent to 23,000

hectares. Importantly, Australia is a net cotton exporter, and the prices reflect in USD terms.

The USD is a currency of international cotton trade, which Australian cotton exports denote it

by the US dollar. NSW and Queensland growers predominantly operate an Australian dollar-

denominated enterprise, and prefer to have their sales receipts in “AUD.”

Queensland Cotton 6

On the other hand, the United States dollar cotton export values ought to be converted

into AUD values, which better suits Queensland cotton growers. The latter prefer their local

currency as AUD per USD rates has a significant influence on the price of AUD locally.

Importantly, local “AUD per Bale price” increases as the Australian dollar rate softens against

the U.S dollar. Most of the contracts between Queensland growers and merchants are in

Australian dollar cash price per bale, where the Australian cotton grower assumes no currency

risk (Australian Cotton Shippers Association, 2008, p.7). Unfortunately, if utilizing an on-call

agreement where the growers fix the three pricing components (basis, futures, and currency)

separately, they, as a result, maintain, and operate a currency risk. Notably, in the case where

the currency is fixed, then the USD cotton value depreciates; as a result, the grower may have

an “over-hedged” currency position, which may develop a higher loss risk.

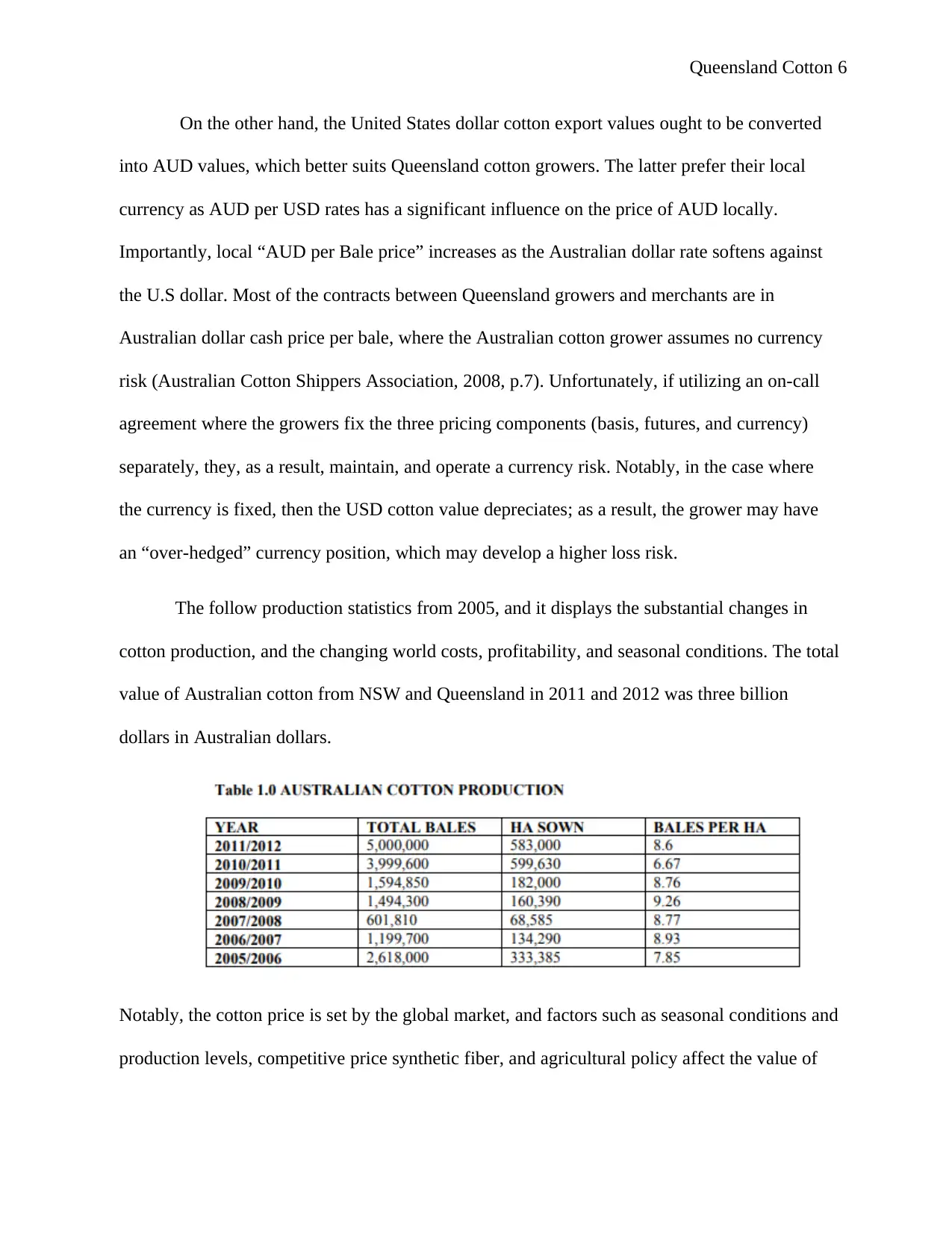

The follow production statistics from 2005, and it displays the substantial changes in

cotton production, and the changing world costs, profitability, and seasonal conditions. The total

value of Australian cotton from NSW and Queensland in 2011 and 2012 was three billion

dollars in Australian dollars.

Notably, the cotton price is set by the global market, and factors such as seasonal conditions and

production levels, competitive price synthetic fiber, and agricultural policy affect the value of

On the other hand, the United States dollar cotton export values ought to be converted

into AUD values, which better suits Queensland cotton growers. The latter prefer their local

currency as AUD per USD rates has a significant influence on the price of AUD locally.

Importantly, local “AUD per Bale price” increases as the Australian dollar rate softens against

the U.S dollar. Most of the contracts between Queensland growers and merchants are in

Australian dollar cash price per bale, where the Australian cotton grower assumes no currency

risk (Australian Cotton Shippers Association, 2008, p.7). Unfortunately, if utilizing an on-call

agreement where the growers fix the three pricing components (basis, futures, and currency)

separately, they, as a result, maintain, and operate a currency risk. Notably, in the case where

the currency is fixed, then the USD cotton value depreciates; as a result, the grower may have

an “over-hedged” currency position, which may develop a higher loss risk.

The follow production statistics from 2005, and it displays the substantial changes in

cotton production, and the changing world costs, profitability, and seasonal conditions. The total

value of Australian cotton from NSW and Queensland in 2011 and 2012 was three billion

dollars in Australian dollars.

Notably, the cotton price is set by the global market, and factors such as seasonal conditions and

production levels, competitive price synthetic fiber, and agricultural policy affect the value of

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Queensland Cotton 7

cotton (De Garis, 2013, p.7). Recently, the cost is about 1,000 Australian dollar per bale, and a

region of 350 dollars to 4000 dollars per Australian bale dollar.

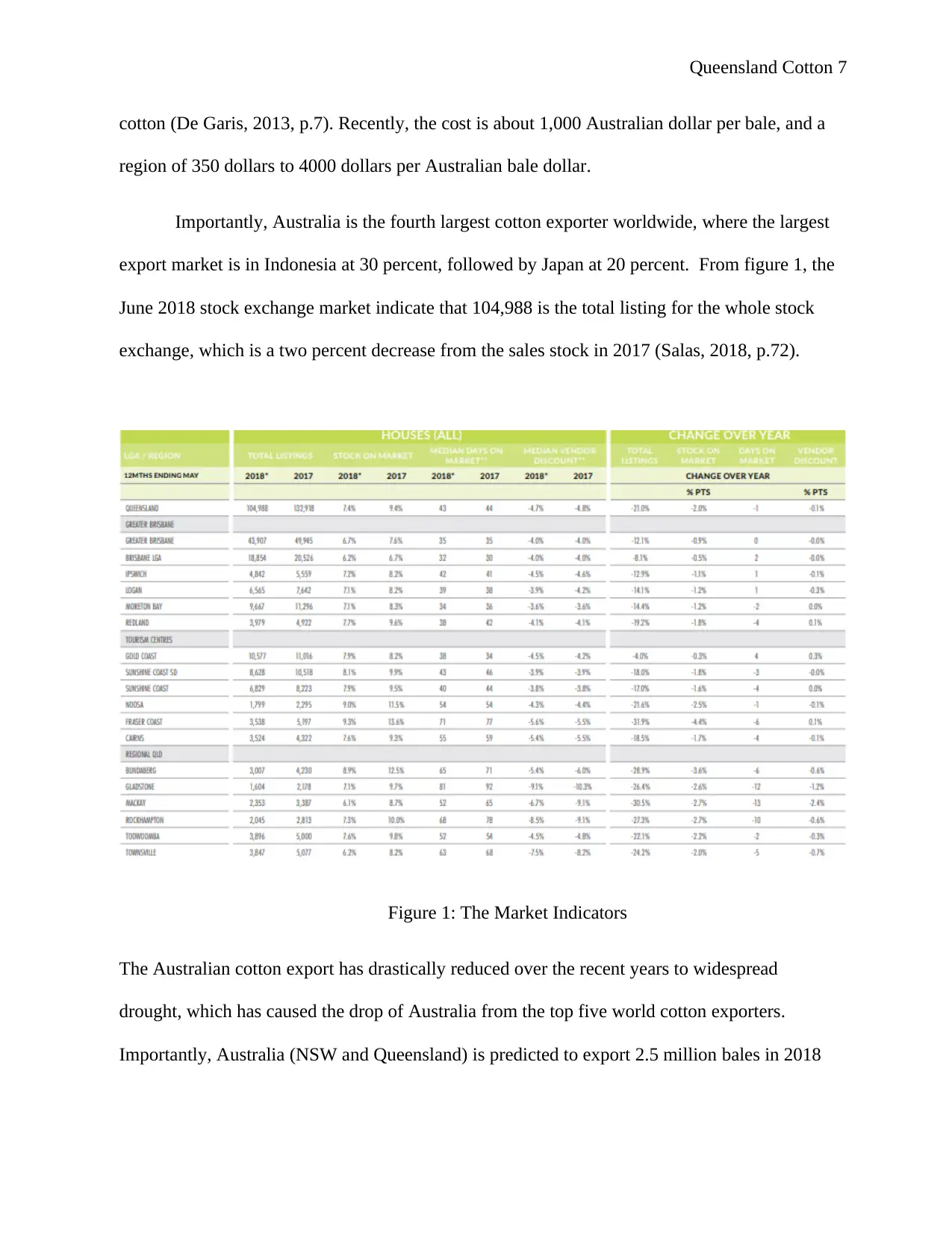

Importantly, Australia is the fourth largest cotton exporter worldwide, where the largest

export market is in Indonesia at 30 percent, followed by Japan at 20 percent. From figure 1, the

June 2018 stock exchange market indicate that 104,988 is the total listing for the whole stock

exchange, which is a two percent decrease from the sales stock in 2017 (Salas, 2018, p.72).

Figure 1: The Market Indicators

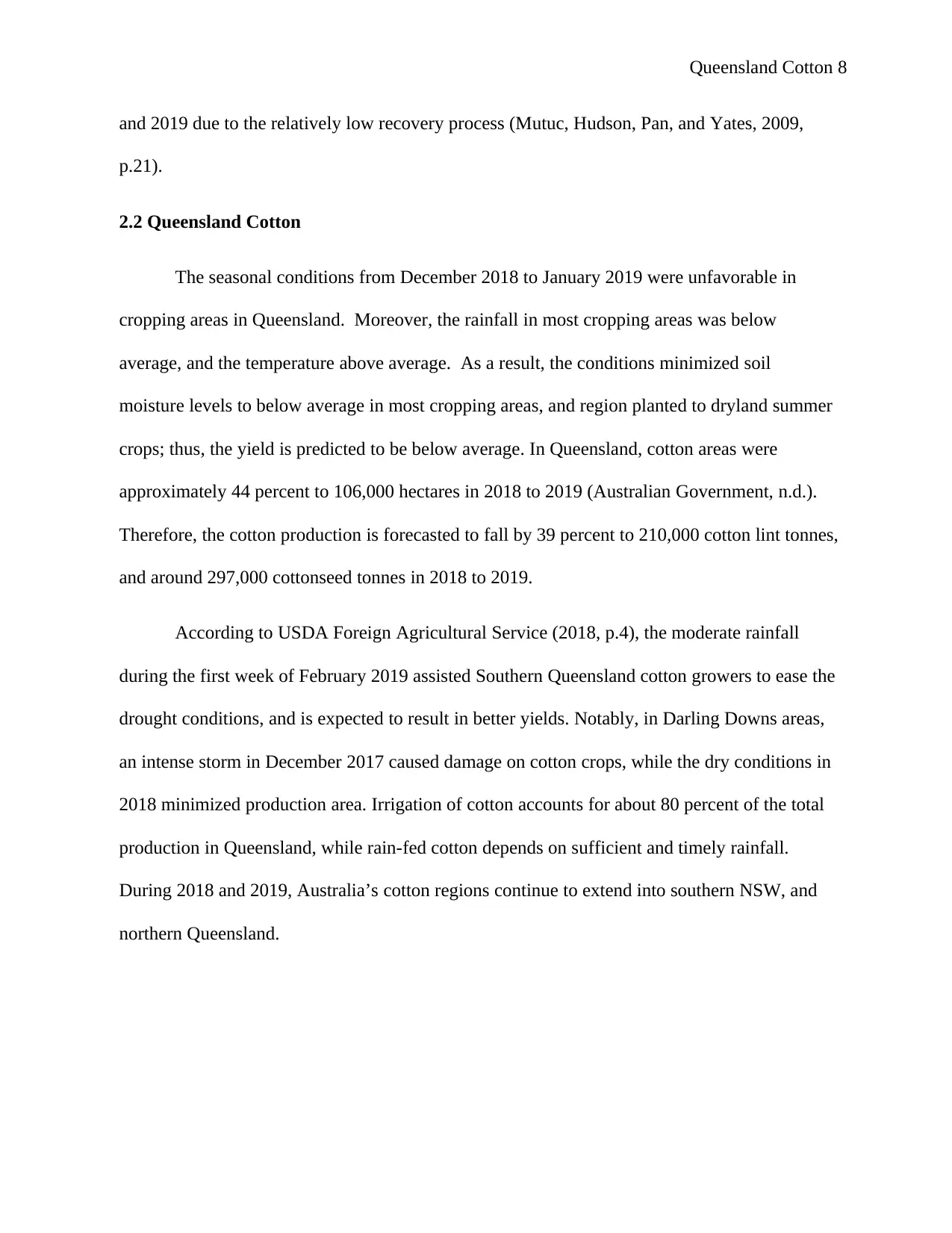

The Australian cotton export has drastically reduced over the recent years to widespread

drought, which has caused the drop of Australia from the top five world cotton exporters.

Importantly, Australia (NSW and Queensland) is predicted to export 2.5 million bales in 2018

cotton (De Garis, 2013, p.7). Recently, the cost is about 1,000 Australian dollar per bale, and a

region of 350 dollars to 4000 dollars per Australian bale dollar.

Importantly, Australia is the fourth largest cotton exporter worldwide, where the largest

export market is in Indonesia at 30 percent, followed by Japan at 20 percent. From figure 1, the

June 2018 stock exchange market indicate that 104,988 is the total listing for the whole stock

exchange, which is a two percent decrease from the sales stock in 2017 (Salas, 2018, p.72).

Figure 1: The Market Indicators

The Australian cotton export has drastically reduced over the recent years to widespread

drought, which has caused the drop of Australia from the top five world cotton exporters.

Importantly, Australia (NSW and Queensland) is predicted to export 2.5 million bales in 2018

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Queensland Cotton 8

and 2019 due to the relatively low recovery process (Mutuc, Hudson, Pan, and Yates, 2009,

p.21).

2.2 Queensland Cotton

The seasonal conditions from December 2018 to January 2019 were unfavorable in

cropping areas in Queensland. Moreover, the rainfall in most cropping areas was below

average, and the temperature above average. As a result, the conditions minimized soil

moisture levels to below average in most cropping areas, and region planted to dryland summer

crops; thus, the yield is predicted to be below average. In Queensland, cotton areas were

approximately 44 percent to 106,000 hectares in 2018 to 2019 (Australian Government, n.d.).

Therefore, the cotton production is forecasted to fall by 39 percent to 210,000 cotton lint tonnes,

and around 297,000 cottonseed tonnes in 2018 to 2019.

According to USDA Foreign Agricultural Service (2018, p.4), the moderate rainfall

during the first week of February 2019 assisted Southern Queensland cotton growers to ease the

drought conditions, and is expected to result in better yields. Notably, in Darling Downs areas,

an intense storm in December 2017 caused damage on cotton crops, while the dry conditions in

2018 minimized production area. Irrigation of cotton accounts for about 80 percent of the total

production in Queensland, while rain-fed cotton depends on sufficient and timely rainfall.

During 2018 and 2019, Australia’s cotton regions continue to extend into southern NSW, and

northern Queensland.

and 2019 due to the relatively low recovery process (Mutuc, Hudson, Pan, and Yates, 2009,

p.21).

2.2 Queensland Cotton

The seasonal conditions from December 2018 to January 2019 were unfavorable in

cropping areas in Queensland. Moreover, the rainfall in most cropping areas was below

average, and the temperature above average. As a result, the conditions minimized soil

moisture levels to below average in most cropping areas, and region planted to dryland summer

crops; thus, the yield is predicted to be below average. In Queensland, cotton areas were

approximately 44 percent to 106,000 hectares in 2018 to 2019 (Australian Government, n.d.).

Therefore, the cotton production is forecasted to fall by 39 percent to 210,000 cotton lint tonnes,

and around 297,000 cottonseed tonnes in 2018 to 2019.

According to USDA Foreign Agricultural Service (2018, p.4), the moderate rainfall

during the first week of February 2019 assisted Southern Queensland cotton growers to ease the

drought conditions, and is expected to result in better yields. Notably, in Darling Downs areas,

an intense storm in December 2017 caused damage on cotton crops, while the dry conditions in

2018 minimized production area. Irrigation of cotton accounts for about 80 percent of the total

production in Queensland, while rain-fed cotton depends on sufficient and timely rainfall.

During 2018 and 2019, Australia’s cotton regions continue to extend into southern NSW, and

northern Queensland.

Queensland Cotton 9

Figure 2: Australian (NSW and Queensland) Cotton Export

Figure 2: Australian (NSW and Queensland) Cotton Export

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Queensland Cotton 10

Figure 3: Queensland and NSW cotton growing areas

The cotton production costs in Australia is among the lowest in the world. The industry

has one of the most exceptional average cotton yields of seven bales in the world, which is

about 2.6 times the world’s average. Notably, Australia has 800 cotton growers with 72 percent

based in NSW, and 28 percent in Queensland. Therefore, the total Australian cotton growing

regions is about 537,000 hectares. NSW and Queensland cotton export about 3million bales

annually, with its major export countries being Indonesia, Japan, China, and Thailand (de Garis,

2013, p.3). Hence, the Australian cotton industry generates credible export revenue of about one

billion dollars annually, and the employment needs for rural communities in Australia.

Queensland Government (2013, p.37) suggest that the GVP for cotton from 2013 to

2014 forecasted a 648 million dollar cash sale of cotton from Queensland, which was two

percent more than the final estimate of DAFF from 2012 and 2013. Notably, this was ten

percent more than the average for the previous five years. The total plated cotton locations in

Queensland decreased in 2013 and 2014 by 500 hectares. Fortunately, the prediction made was

that there was no effect on the average yields as there was a decrease in irrigated cotton farms,

cottonseed and cotton lint mass production.

The cotton cost per bale was expected to remain constant at 400 dollars per bale, and the

price of cottonseed remained steady at 335 dollars per tonne. Alternatively, the irrigated cotton

cropping region was predicted to elevate by five percent to at least 133,000 hectares across

Queensland states. These states include Darling Downs at 35,000 hectares, Dirranbandi areas at

53,000 hectares, Border Rivers at 25,000 hectares, and 20,000 hectares at Central Queensland.

Importantly, the slight decrease in supplies of irrigation water in Macintyre, “Condamine,”

“Barwon and Moonie Rivers,” and “Border Rivers” areas have been experienced since the

Figure 3: Queensland and NSW cotton growing areas

The cotton production costs in Australia is among the lowest in the world. The industry

has one of the most exceptional average cotton yields of seven bales in the world, which is

about 2.6 times the world’s average. Notably, Australia has 800 cotton growers with 72 percent

based in NSW, and 28 percent in Queensland. Therefore, the total Australian cotton growing

regions is about 537,000 hectares. NSW and Queensland cotton export about 3million bales

annually, with its major export countries being Indonesia, Japan, China, and Thailand (de Garis,

2013, p.3). Hence, the Australian cotton industry generates credible export revenue of about one

billion dollars annually, and the employment needs for rural communities in Australia.

Queensland Government (2013, p.37) suggest that the GVP for cotton from 2013 to

2014 forecasted a 648 million dollar cash sale of cotton from Queensland, which was two

percent more than the final estimate of DAFF from 2012 and 2013. Notably, this was ten

percent more than the average for the previous five years. The total plated cotton locations in

Queensland decreased in 2013 and 2014 by 500 hectares. Fortunately, the prediction made was

that there was no effect on the average yields as there was a decrease in irrigated cotton farms,

cottonseed and cotton lint mass production.

The cotton cost per bale was expected to remain constant at 400 dollars per bale, and the

price of cottonseed remained steady at 335 dollars per tonne. Alternatively, the irrigated cotton

cropping region was predicted to elevate by five percent to at least 133,000 hectares across

Queensland states. These states include Darling Downs at 35,000 hectares, Dirranbandi areas at

53,000 hectares, Border Rivers at 25,000 hectares, and 20,000 hectares at Central Queensland.

Importantly, the slight decrease in supplies of irrigation water in Macintyre, “Condamine,”

“Barwon and Moonie Rivers,” and “Border Rivers” areas have been experienced since the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Queensland Cotton 11

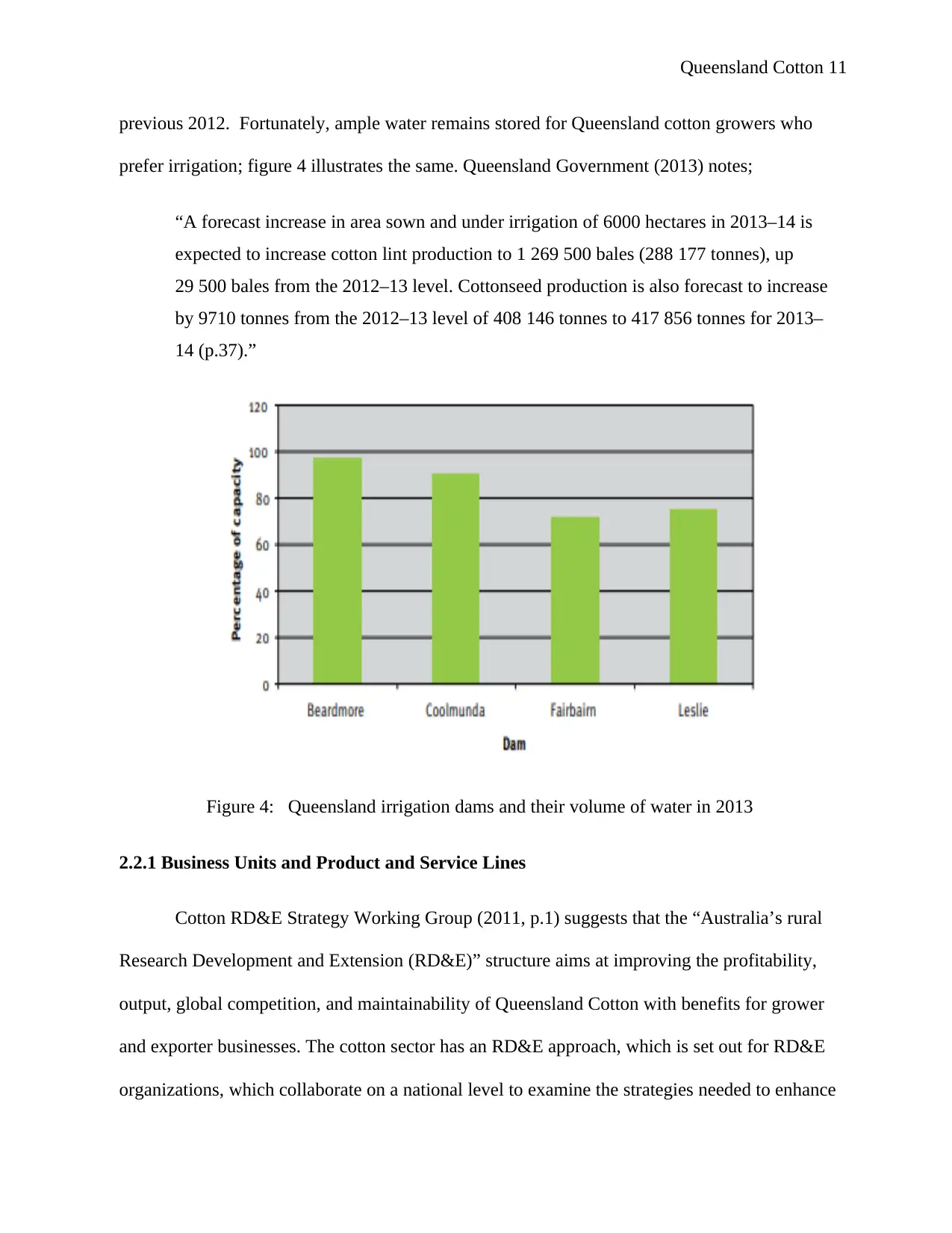

previous 2012. Fortunately, ample water remains stored for Queensland cotton growers who

prefer irrigation; figure 4 illustrates the same. Queensland Government (2013) notes;

“A forecast increase in area sown and under irrigation of 6000 hectares in 2013–14 is

expected to increase cotton lint production to 1 269 500 bales (288 177 tonnes), up

29 500 bales from the 2012–13 level. Cottonseed production is also forecast to increase

by 9710 tonnes from the 2012–13 level of 408 146 tonnes to 417 856 tonnes for 2013–

14 (p.37).”

Figure 4: Queensland irrigation dams and their volume of water in 2013

2.2.1 Business Units and Product and Service Lines

Cotton RD&E Strategy Working Group (2011, p.1) suggests that the “Australia’s rural

Research Development and Extension (RD&E)” structure aims at improving the profitability,

output, global competition, and maintainability of Queensland Cotton with benefits for grower

and exporter businesses. The cotton sector has an RD&E approach, which is set out for RD&E

organizations, which collaborate on a national level to examine the strategies needed to enhance

previous 2012. Fortunately, ample water remains stored for Queensland cotton growers who

prefer irrigation; figure 4 illustrates the same. Queensland Government (2013) notes;

“A forecast increase in area sown and under irrigation of 6000 hectares in 2013–14 is

expected to increase cotton lint production to 1 269 500 bales (288 177 tonnes), up

29 500 bales from the 2012–13 level. Cottonseed production is also forecast to increase

by 9710 tonnes from the 2012–13 level of 408 146 tonnes to 417 856 tonnes for 2013–

14 (p.37).”

Figure 4: Queensland irrigation dams and their volume of water in 2013

2.2.1 Business Units and Product and Service Lines

Cotton RD&E Strategy Working Group (2011, p.1) suggests that the “Australia’s rural

Research Development and Extension (RD&E)” structure aims at improving the profitability,

output, global competition, and maintainability of Queensland Cotton with benefits for grower

and exporter businesses. The cotton sector has an RD&E approach, which is set out for RD&E

organizations, which collaborate on a national level to examine the strategies needed to enhance

Queensland Cotton 12

the sector. These approaches may include establishing a process of allocating resources across

priority regions of cotton growing such as Queensland and NSW, and the ongoing maintenance

of national capacity and effort. Alternatively, RD&E structure establishes a process for the

operation of innovation, which will maximize profits in Queensland Cotton.

The Queensland Cotton utilizes the RD&E strategy to develop through a Working

Group involving “Cotton Research and Development Corporation (CRDC),” “Cotton

Catchment Communities Cooperative Research Centre (Cotton CRC),” and “Cotton Seed

Distributors (CSD).” The Queensland and NSW cotton produces a mean of 499kt cotton lint,

and 688kt of cottonseed annually from 308,000 hectares, although in recent years the sector has

faced challenges due to climate change, which has resulted to long drought periods.

Importantly, the production degree varies depending on water availability, and the extent of the

market of conditions (Cotton Australia, 2008, p.5). Most of the Australian cotton industry relies

on the central and northern NSW, and central and southern Queensland, which give an

economic cornerstone for numerous zonal communities that employ at 13,000 workers.

The environmental sustainability and productivity of the cotton manufacturing have

enhanced enormously over the past 20 years through technology creation, and superior manage

operations. These enhancements underline the swift development of the cotton manufacturing

since the 1990s, and helped in maintaining global competition, and adaptability to famine since

2000s. Queensland Government’s method to attain sustainable economic development focuses

on several policy channels, which are managed by the state’s priorities of innovation,

investment, and infrastructure (Queensland Australia, 2017, p.13). Notably, the main product

line in Queensland Cotton is cotton, and the technique connects to promoting cotton enterprise

exports and investment.

the sector. These approaches may include establishing a process of allocating resources across

priority regions of cotton growing such as Queensland and NSW, and the ongoing maintenance

of national capacity and effort. Alternatively, RD&E structure establishes a process for the

operation of innovation, which will maximize profits in Queensland Cotton.

The Queensland Cotton utilizes the RD&E strategy to develop through a Working

Group involving “Cotton Research and Development Corporation (CRDC),” “Cotton

Catchment Communities Cooperative Research Centre (Cotton CRC),” and “Cotton Seed

Distributors (CSD).” The Queensland and NSW cotton produces a mean of 499kt cotton lint,

and 688kt of cottonseed annually from 308,000 hectares, although in recent years the sector has

faced challenges due to climate change, which has resulted to long drought periods.

Importantly, the production degree varies depending on water availability, and the extent of the

market of conditions (Cotton Australia, 2008, p.5). Most of the Australian cotton industry relies

on the central and northern NSW, and central and southern Queensland, which give an

economic cornerstone for numerous zonal communities that employ at 13,000 workers.

The environmental sustainability and productivity of the cotton manufacturing have

enhanced enormously over the past 20 years through technology creation, and superior manage

operations. These enhancements underline the swift development of the cotton manufacturing

since the 1990s, and helped in maintaining global competition, and adaptability to famine since

2000s. Queensland Government’s method to attain sustainable economic development focuses

on several policy channels, which are managed by the state’s priorities of innovation,

investment, and infrastructure (Queensland Australia, 2017, p.13). Notably, the main product

line in Queensland Cotton is cotton, and the technique connects to promoting cotton enterprise

exports and investment.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 35

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.