ACCG8025: Management Accounting - Quiet Logistics Case Study Analysis

VerifiedAdded on 2023/01/12

|7

|998

|28

Case Study

AI Summary

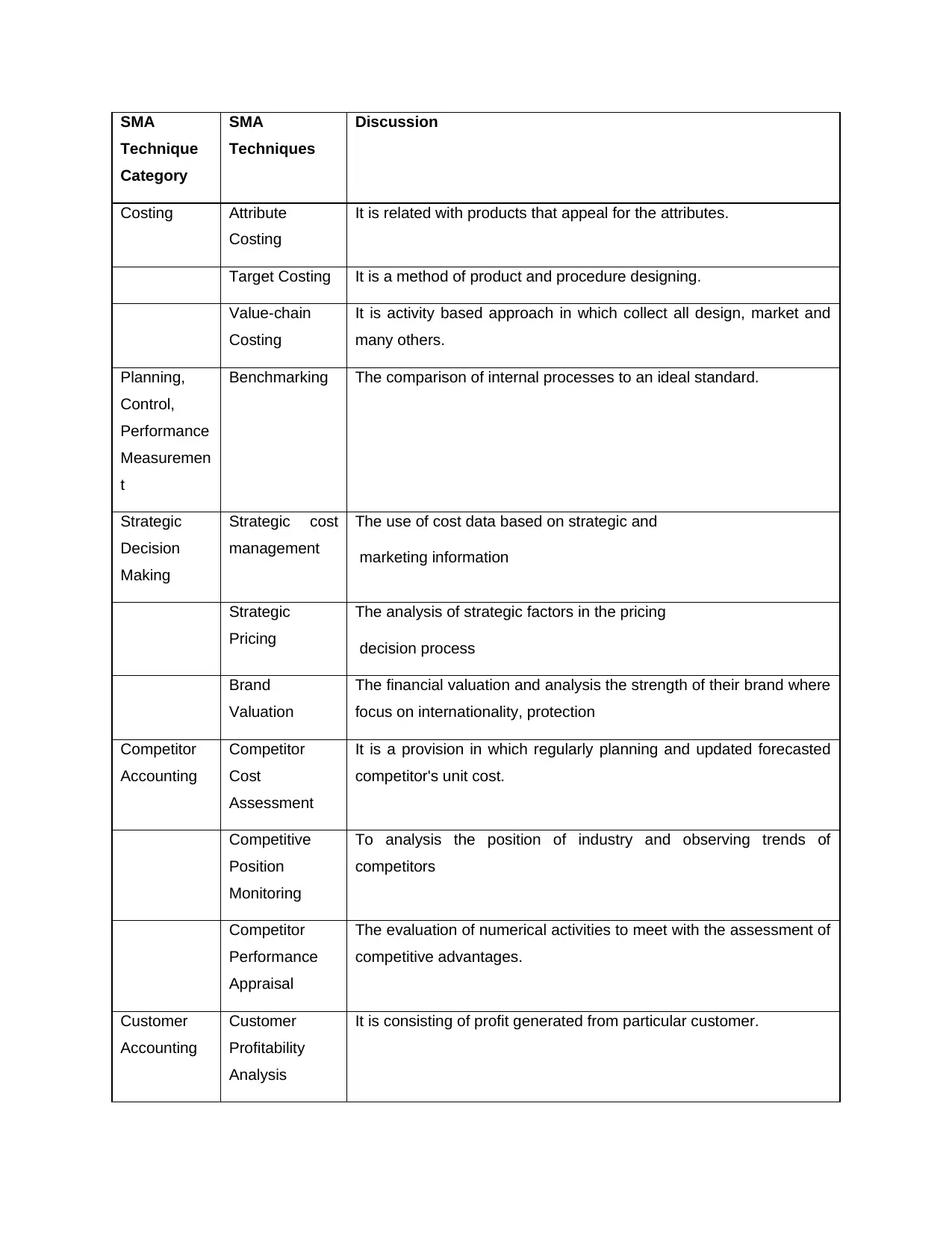

This case study analyzes Quiet Logistics, focusing on the application of strategic management accounting (SMA) techniques. The analysis includes an examination of SMA's role in decision-making, the importance of long-term and outward-looking orientations, and the utilization of techniques such as target costing, value-chain costing, and benchmarking. The study explores how management accountants should participate in strategic decision-making, emphasizing customer orientation and close relationships across functions. It further details Quiet Logistics' business strategy, the use of SMA for planning and control, and the importance of strategic formulation in overcoming competition. The conclusion highlights the essential role of SMA in handling business activities, reflecting on accounting methods, and meeting global challenges. The case study also references relevant literature on lean manufacturing and accounting systems.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.