Financial Network Contagion Simulation and Analysis in R Programming

VerifiedAdded on 2022/11/13

|21

|5953

|377

Project

AI Summary

This project focuses on modeling and simulating financial contagion within banking networks using R programming. The assignment requires generating Erdos-Renyi and Stochastic Block Model networks to represent interbank connections. The core task involves simulating bank failures and analyzing how these failures propagate throughout the network, leading to systemic risk analysis. The project includes implementing specific rules for calculating link weights based on capital buffers and simulating contagion events through Monte Carlo simulations. The goal is to assess the impact of different network structures and parameters on the spread of financial distress, aiming to replicate the results of provided working papers and understand the factors that contribute to financial instability. The analysis includes calculating contagion frequency, average degrees, and visualizing network structures to understand the dynamics of financial contagion.

STATISTICS R

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Abstract................................................................................................................................................2

Introduction.........................................................................................................................................2

Measuring systemic.............................................................................................................................4

Mark-to-Market Values....................................................................................................................11

Primitive Assets, Organizations, & the Cross-Holdings.................................................................13

Values of Organizations....................................................................................................................14

Discontinuities in the Values and the Costs of Failure....................................................................14

Existence of Equilibrium and Multiplicity......................................................................................15

Integration and Diversification.........................................................................................................15

Stochastic Block Model.....................................................................................................................15

Random Networks.............................................................................................................................16

The Consequences of Diversification................................................................................................18

Conclusion..........................................................................................................................................19

References..........................................................................................................................................19

Abstract................................................................................................................................................2

Introduction.........................................................................................................................................2

Measuring systemic.............................................................................................................................4

Mark-to-Market Values....................................................................................................................11

Primitive Assets, Organizations, & the Cross-Holdings.................................................................13

Values of Organizations....................................................................................................................14

Discontinuities in the Values and the Costs of Failure....................................................................14

Existence of Equilibrium and Multiplicity......................................................................................15

Integration and Diversification.........................................................................................................15

Stochastic Block Model.....................................................................................................................15

Random Networks.............................................................................................................................16

The Consequences of Diversification................................................................................................18

Conclusion..........................................................................................................................................19

References..........................................................................................................................................19

Abstract

The main aim of this research is to analyze the financial institution resilience to

determine the techniques that have been employed in complex network theories. The study is

carried out using the Monte Carlos simulations to assess the different networks as well as the

topologies through the contagion model that is applicable in diverse interbank networks. The

banking series is triggered.

We researched a series of different banking crises through each bank in the device and

examined the mechanisms used for propagation which take impact’s the device’s internal

distinctive scenarios. At last, a literature review is conducted to examine the interplay of the

countless imperative drivers of interbank contagions like the interconnectedness, network

topology, homogeneity and leverage throughout the bank sizes and the exposures of the

interbank.

Introduction

The national economy’s complexity has crystal rectifier with several lecturers, for

utilizing the network theory in order to review the results of connectedness and configuration

on money stability. Finding out the national economy as a network is one of the ways which

is accustomed to investigate the general risk’s emergence via the connections of the banks. In

this type of a network structure, each node signifies a bank. Therefore, the links between the

banks area unit is portrayed by the edges. An active interbank market acts as the bond in the

national economy’s stability.

The interbank market’s use has enabled the banks that suffer the shortage of liquidity

to borrow from the banks which have surplus liquidity. Hence, on the national economy, the

interbank market will have an effective result by efficiently sharing the money with the

banks. But, consequently it will make the system vulnerable to the monetary contagion due to

the present linkages of the interbank. For many years, the giant financial establishments were

included as the assorted suspects to destabilize the national economy, whose failure could be

fatal for the bigger national economy (as it is too massive for the fail theory). The

government should support such monetary establishments once they face fiscal distress

because of their general importance and link.

However, if they fail, the smaller money establishments with ample connections

within the interbank market will have an excellent, and highly significant effect on the

The main aim of this research is to analyze the financial institution resilience to

determine the techniques that have been employed in complex network theories. The study is

carried out using the Monte Carlos simulations to assess the different networks as well as the

topologies through the contagion model that is applicable in diverse interbank networks. The

banking series is triggered.

We researched a series of different banking crises through each bank in the device and

examined the mechanisms used for propagation which take impact’s the device’s internal

distinctive scenarios. At last, a literature review is conducted to examine the interplay of the

countless imperative drivers of interbank contagions like the interconnectedness, network

topology, homogeneity and leverage throughout the bank sizes and the exposures of the

interbank.

Introduction

The national economy’s complexity has crystal rectifier with several lecturers, for

utilizing the network theory in order to review the results of connectedness and configuration

on money stability. Finding out the national economy as a network is one of the ways which

is accustomed to investigate the general risk’s emergence via the connections of the banks. In

this type of a network structure, each node signifies a bank. Therefore, the links between the

banks area unit is portrayed by the edges. An active interbank market acts as the bond in the

national economy’s stability.

The interbank market’s use has enabled the banks that suffer the shortage of liquidity

to borrow from the banks which have surplus liquidity. Hence, on the national economy, the

interbank market will have an effective result by efficiently sharing the money with the

banks. But, consequently it will make the system vulnerable to the monetary contagion due to

the present linkages of the interbank. For many years, the giant financial establishments were

included as the assorted suspects to destabilize the national economy, whose failure could be

fatal for the bigger national economy (as it is too massive for the fail theory). The

government should support such monetary establishments once they face fiscal distress

because of their general importance and link.

However, if they fail, the smaller money establishments with ample connections

within the interbank market will have an excellent, and highly significant effect on the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

financial set-up. The interbank network’s higher links will scale back the chance of default,

because several counterparties share transmission of a shock and so it disperses quickly. In

contrast, once the excitement’s magnitude has crossed a vital threshold due to the increase in

connectedness the collapse can unfold into an oversized part of the system then it might cause

defaults in an oversized cascade. Thus, this can be a questionable "robust-yet-fragile"

property which is exhibited by the money systems.

This paper therefore focuses on the direct contagion channel and studies the

effectiveness of varied drivers on the interbank contagion. The flourishing literature which is

derived until today has helped to develop the theoretical models which aims to address the

assorted problems regarding general risk. Contrary to fact simulations on information are

utilized to check interbank contagion beneath completely different eventualities associated

with the interbank network’s topology, the scale of interbank exposures. Therefore, the

degree of heterogeneousness and interconnection among the system. This research tends to

develop a model with the banks connected to one another based on the claims of the

interbank and is investigated with the help of Monte Carlo simulations, however, the

complexness of an interbank network structure impacts the interbank contagion beneath

completely different testable eventualities. This analysis belongs to a part of the theoretical

literature, as we tend to use laptop simulations to construct an oversized range of bank

networks involving entities by closing down bank claim and obligations. Victimization tools

from the complicated network theory’s aim is to develop a model; however, the reaction of

the AN initial default might also unfold from one establishment to a different.

Second, we tend to utilize solely two parts based on the records of a bank, which

includes the equity and loans of the interbank for constructing a penurious regression model.

The regression model has been employed to test the crucial impact drivers recorded in the

experiments regarding simulations experiments on the interbank. Multivariate analysis is also

conjointly utilized by Krause and Guarantee for assessing the role contend by the network's

topological options and record the positions within the transmission of bank failures. The

authors use a model which is a scale-free network model for reviewing the interbank

contagion with massive parameter ranges, and a plenty of parameters for initializing the

record. But, their model becomes inflexible in terms of operation, because it is tough for

checking the simulations by the variable one amongst the settings.

In contrast, this model is well understandable, reproducible and additionally it is

amenable for the interpretation and analysis. We tend to outline the term contagion because

the state of affairs within that the bank’s initial failure ends up as a failure of a minimum of

because several counterparties share transmission of a shock and so it disperses quickly. In

contrast, once the excitement’s magnitude has crossed a vital threshold due to the increase in

connectedness the collapse can unfold into an oversized part of the system then it might cause

defaults in an oversized cascade. Thus, this can be a questionable "robust-yet-fragile"

property which is exhibited by the money systems.

This paper therefore focuses on the direct contagion channel and studies the

effectiveness of varied drivers on the interbank contagion. The flourishing literature which is

derived until today has helped to develop the theoretical models which aims to address the

assorted problems regarding general risk. Contrary to fact simulations on information are

utilized to check interbank contagion beneath completely different eventualities associated

with the interbank network’s topology, the scale of interbank exposures. Therefore, the

degree of heterogeneousness and interconnection among the system. This research tends to

develop a model with the banks connected to one another based on the claims of the

interbank and is investigated with the help of Monte Carlo simulations, however, the

complexness of an interbank network structure impacts the interbank contagion beneath

completely different testable eventualities. This analysis belongs to a part of the theoretical

literature, as we tend to use laptop simulations to construct an oversized range of bank

networks involving entities by closing down bank claim and obligations. Victimization tools

from the complicated network theory’s aim is to develop a model; however, the reaction of

the AN initial default might also unfold from one establishment to a different.

Second, we tend to utilize solely two parts based on the records of a bank, which

includes the equity and loans of the interbank for constructing a penurious regression model.

The regression model has been employed to test the crucial impact drivers recorded in the

experiments regarding simulations experiments on the interbank. Multivariate analysis is also

conjointly utilized by Krause and Guarantee for assessing the role contend by the network's

topological options and record the positions within the transmission of bank failures. The

authors use a model which is a scale-free network model for reviewing the interbank

contagion with massive parameter ranges, and a plenty of parameters for initializing the

record. But, their model becomes inflexible in terms of operation, because it is tough for

checking the simulations by the variable one amongst the settings.

In contrast, this model is well understandable, reproducible and additionally it is

amenable for the interpretation and analysis. We tend to outline the term contagion because

the state of affairs within that the bank’s initial failure ends up as a failure of a minimum of

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

one different bank, whereas the extent of contagion is measured based on the complete

financial loss within the banking industry, because of at least one bank’s inability. On the

other hand, we tend to the area unit principally inquisitive about sleuthing the capital losses’

magnitude within the banking network instead of various banks which were impacted highly.

At last, this paper helps to present the prevailing literature which is examined by using a

comprehensive network model, the knock-on effects. AN initial default will bring into the

interbank network below the idea of randomness.

The idea which the interbank network claims and obligations forms indiscriminately,

allows North American country to capture all potential eventualities that will seem in the

real-world things. Additionally, we tend to avoid the matter knowledge of information

inconvenience as a real data on the exposures area unit of the interbank typically is solely on

the market to central bankers and the regulators, so renders the problematic network’s

empirical analysis.

This research’s findings represent that the heterogeneousness in size of the banks and

interbank exposures matter an excellent deal within the financial set-up’s stability, because its

absorption capability is increased. Additionally, the extent of connectedness vastly affects the

resilience of the system, particularly in smaller and extremely interconnected interbank

networks. At last, a proof is provided that extremely leveraged the type of banks the most

channel through that monetary shocks propagate at intervals the system, and similar result is

additionally pronounced in the massive interbank networks when compared to the smaller

banks.

The remaining paper is subdivided into two sections to discuss the connected

literature on the interbank contagion. Chapter three presents the network model of contagion.

Measuring systemic

A network model projected by Eisenberg and Noe comprises of 3 essential ingredients

namely, a group of n nodes N ¼ f1; 2; ... ; ng, associate n liabilities matrix P ¼ wherever

FTO P zero denotes the due payment from the node i to node j; pii ¼ zero, and a vector c ¼

ðc1; c2; ... ; cnÞ two Rn þ wherever ci P zero represents the worth of outdoor assets control

by node i additionally to its claims on alternative nodes within a network. Generally, ci

comprises of money, mortgages, securities, and alternative applications on the external

entities of a system. Additionally, every node i could have liabilities for the external entities

from the network; we tend to let metallic element P zero represents the total of all similar

obligations of i, that we tend to accept to have equivalent priority with i's liabilities for the

financial loss within the banking industry, because of at least one bank’s inability. On the

other hand, we tend to the area unit principally inquisitive about sleuthing the capital losses’

magnitude within the banking network instead of various banks which were impacted highly.

At last, this paper helps to present the prevailing literature which is examined by using a

comprehensive network model, the knock-on effects. AN initial default will bring into the

interbank network below the idea of randomness.

The idea which the interbank network claims and obligations forms indiscriminately,

allows North American country to capture all potential eventualities that will seem in the

real-world things. Additionally, we tend to avoid the matter knowledge of information

inconvenience as a real data on the exposures area unit of the interbank typically is solely on

the market to central bankers and the regulators, so renders the problematic network’s

empirical analysis.

This research’s findings represent that the heterogeneousness in size of the banks and

interbank exposures matter an excellent deal within the financial set-up’s stability, because its

absorption capability is increased. Additionally, the extent of connectedness vastly affects the

resilience of the system, particularly in smaller and extremely interconnected interbank

networks. At last, a proof is provided that extremely leveraged the type of banks the most

channel through that monetary shocks propagate at intervals the system, and similar result is

additionally pronounced in the massive interbank networks when compared to the smaller

banks.

The remaining paper is subdivided into two sections to discuss the connected

literature on the interbank contagion. Chapter three presents the network model of contagion.

Measuring systemic

A network model projected by Eisenberg and Noe comprises of 3 essential ingredients

namely, a group of n nodes N ¼ f1; 2; ... ; ng, associate n liabilities matrix P ¼ wherever

FTO P zero denotes the due payment from the node i to node j; pii ¼ zero, and a vector c ¼

ðc1; c2; ... ; cnÞ two Rn þ wherever ci P zero represents the worth of outdoor assets control

by node i additionally to its claims on alternative nodes within a network. Generally, ci

comprises of money, mortgages, securities, and alternative applications on the external

entities of a system. Additionally, every node i could have liabilities for the external entities

from the network; we tend to let metallic element P zero represents the total of all similar

obligations of i, that we tend to accept to have equivalent priority with i's liabilities for the

alternative nodes within a network. The quality facet of the node i's record is provided by ci þ

P j–ipji, and therefore the liability facet is provided by pi ¼ metallic element þ P j–pig. Its

web value is that the distinction Badger State ¼ ci þX j–ipji pi: ð1Þ the notation related to the

generic node I, which is represented in the Figure 1. Within a network (indicated by the

dotted line), node I have associate obligation FTO to the node j and also has claim PKI on the

node k. This figure additionally depicts the node I's external assets ci and outdoors liabilities

metallic element. The distinction between the total assets and the total liabilities is that the

node's web value Badger State.

Observe that the I's web value is unrestricted in sign; if it's plus in such case it

communicates to the I equity’s value. We tend to decision the "book price" as a result of it's

supported the nominal or face value of the pji liabilities, instead of the ''market" values which

replicate the ability of the nodes to pay. These market prices rely on the ability of the

alternative nodes to pay the conditional on the realized value of their external assets.

Specifically, let every node's external assets be subjected to a random shock which decreases

the worth of its external assets, and similarly impacts the web value. This area unit shocks the

"fundamentals" which propagates via a network of monetary obligations.

To illustrate the result of a shock, we tend to think about the numerical, that follows

the notational conventions. Above all, the central node includes a web value often as a result

of its one hundred fifty in outside assets, a hundred in the external liabilities, and forty in

liabilities to the alternative nodes within a network. A shock of magnitude ten to the surface

assets deletes the web value of the central node, however, leaves it with only sufficient assets

(140) to cowl its liabilities. A shock of magnitude eighty leaves the primary node with the

assets of seventy, [*fr1] the worth of its liabilities. Below a pro-rata allocation, every liability

is cut in [*fr1]. Therefore every peripheral node gets the payment of five that is simple to

balance assets and liabilities of every peripheral node. Hence, during this case, there exists

central node defaults; however, the peripheral nodes don't. A shock to the primary node's

external asset is bigger when compared to eighty, which could scale back the worth of each

node's assets that is lower than the value of its liabilities.

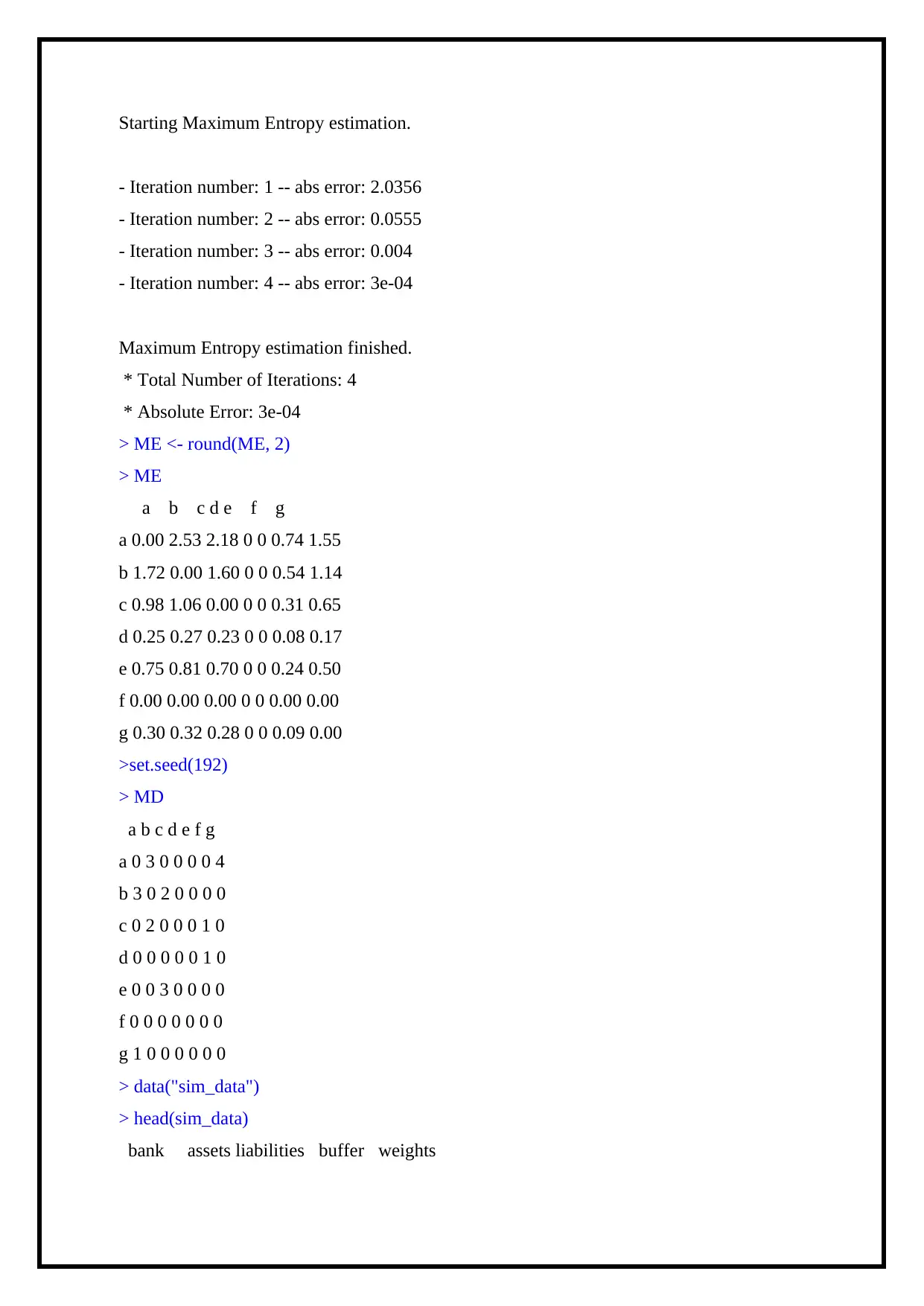

> library(NetworkRiskMeasures)

> ME <- matrix_estimation(rowsums = A, colsums = L, method = "me")

P j–ipji, and therefore the liability facet is provided by pi ¼ metallic element þ P j–pig. Its

web value is that the distinction Badger State ¼ ci þX j–ipji pi: ð1Þ the notation related to the

generic node I, which is represented in the Figure 1. Within a network (indicated by the

dotted line), node I have associate obligation FTO to the node j and also has claim PKI on the

node k. This figure additionally depicts the node I's external assets ci and outdoors liabilities

metallic element. The distinction between the total assets and the total liabilities is that the

node's web value Badger State.

Observe that the I's web value is unrestricted in sign; if it's plus in such case it

communicates to the I equity’s value. We tend to decision the "book price" as a result of it's

supported the nominal or face value of the pji liabilities, instead of the ''market" values which

replicate the ability of the nodes to pay. These market prices rely on the ability of the

alternative nodes to pay the conditional on the realized value of their external assets.

Specifically, let every node's external assets be subjected to a random shock which decreases

the worth of its external assets, and similarly impacts the web value. This area unit shocks the

"fundamentals" which propagates via a network of monetary obligations.

To illustrate the result of a shock, we tend to think about the numerical, that follows

the notational conventions. Above all, the central node includes a web value often as a result

of its one hundred fifty in outside assets, a hundred in the external liabilities, and forty in

liabilities to the alternative nodes within a network. A shock of magnitude ten to the surface

assets deletes the web value of the central node, however, leaves it with only sufficient assets

(140) to cowl its liabilities. A shock of magnitude eighty leaves the primary node with the

assets of seventy, [*fr1] the worth of its liabilities. Below a pro-rata allocation, every liability

is cut in [*fr1]. Therefore every peripheral node gets the payment of five that is simple to

balance assets and liabilities of every peripheral node. Hence, during this case, there exists

central node defaults; however, the peripheral nodes don't. A shock to the primary node's

external asset is bigger when compared to eighty, which could scale back the worth of each

node's assets that is lower than the value of its liabilities.

> library(NetworkRiskMeasures)

> ME <- matrix_estimation(rowsums = A, colsums = L, method = "me")

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Starting Maximum Entropy estimation.

- Iteration number: 1 -- abs error: 2.0356

- Iteration number: 2 -- abs error: 0.0555

- Iteration number: 3 -- abs error: 0.004

- Iteration number: 4 -- abs error: 3e-04

Maximum Entropy estimation finished.

* Total Number of Iterations: 4

* Absolute Error: 3e-04

> ME <- round(ME, 2)

> ME

a b c d e f g

a 0.00 2.53 2.18 0 0 0.74 1.55

b 1.72 0.00 1.60 0 0 0.54 1.14

c 0.98 1.06 0.00 0 0 0.31 0.65

d 0.25 0.27 0.23 0 0 0.08 0.17

e 0.75 0.81 0.70 0 0 0.24 0.50

f 0.00 0.00 0.00 0 0 0.00 0.00

g 0.30 0.32 0.28 0 0 0.09 0.00

>set.seed(192)

> MD

a b c d e f g

a 0 3 0 0 0 0 4

b 3 0 2 0 0 0 0

c 0 2 0 0 0 1 0

d 0 0 0 0 0 1 0

e 0 0 3 0 0 0 0

f 0 0 0 0 0 0 0

g 1 0 0 0 0 0 0

> data("sim_data")

> head(sim_data)

bank assets liabilities buffer weights

- Iteration number: 1 -- abs error: 2.0356

- Iteration number: 2 -- abs error: 0.0555

- Iteration number: 3 -- abs error: 0.004

- Iteration number: 4 -- abs error: 3e-04

Maximum Entropy estimation finished.

* Total Number of Iterations: 4

* Absolute Error: 3e-04

> ME <- round(ME, 2)

> ME

a b c d e f g

a 0.00 2.53 2.18 0 0 0.74 1.55

b 1.72 0.00 1.60 0 0 0.54 1.14

c 0.98 1.06 0.00 0 0 0.31 0.65

d 0.25 0.27 0.23 0 0 0.08 0.17

e 0.75 0.81 0.70 0 0 0.24 0.50

f 0.00 0.00 0.00 0 0 0.00 0.00

g 0.30 0.32 0.28 0 0 0.09 0.00

>set.seed(192)

> MD

a b c d e f g

a 0 3 0 0 0 0 4

b 3 0 2 0 0 0 0

c 0 2 0 0 0 1 0

d 0 0 0 0 0 1 0

e 0 0 3 0 0 0 0

f 0 0 0 0 0 0 0

g 1 0 0 0 0 0 0

> data("sim_data")

> head(sim_data)

bank assets liabilities buffer weights

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

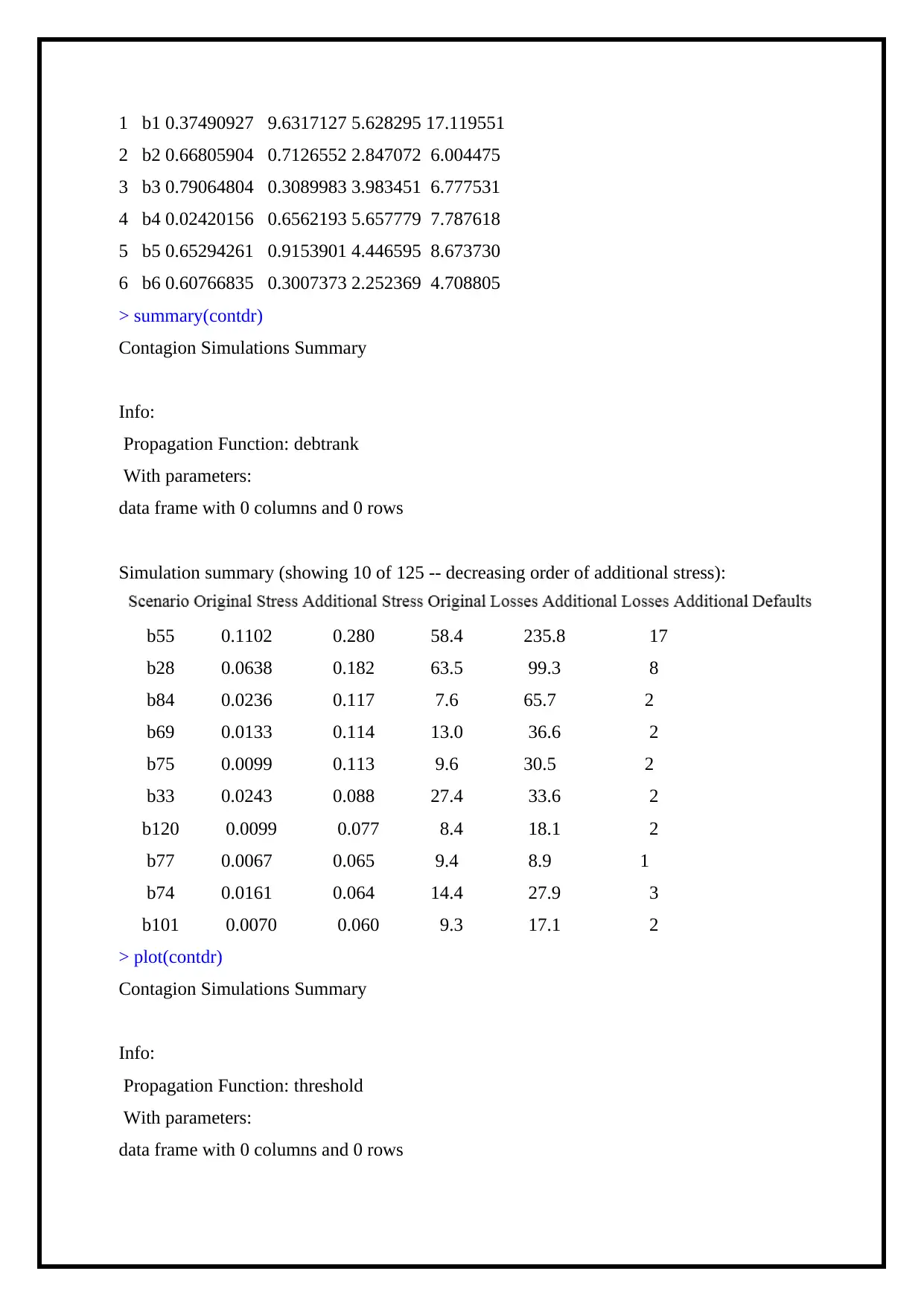

1 b1 0.37490927 9.6317127 5.628295 17.119551

2 b2 0.66805904 0.7126552 2.847072 6.004475

3 b3 0.79064804 0.3089983 3.983451 6.777531

4 b4 0.02420156 0.6562193 5.657779 7.787618

5 b5 0.65294261 0.9153901 4.446595 8.673730

6 b6 0.60766835 0.3007373 2.252369 4.708805

> summary(contdr)

Contagion Simulations Summary

Info:

Propagation Function: debtrank

With parameters:

data frame with 0 columns and 0 rows

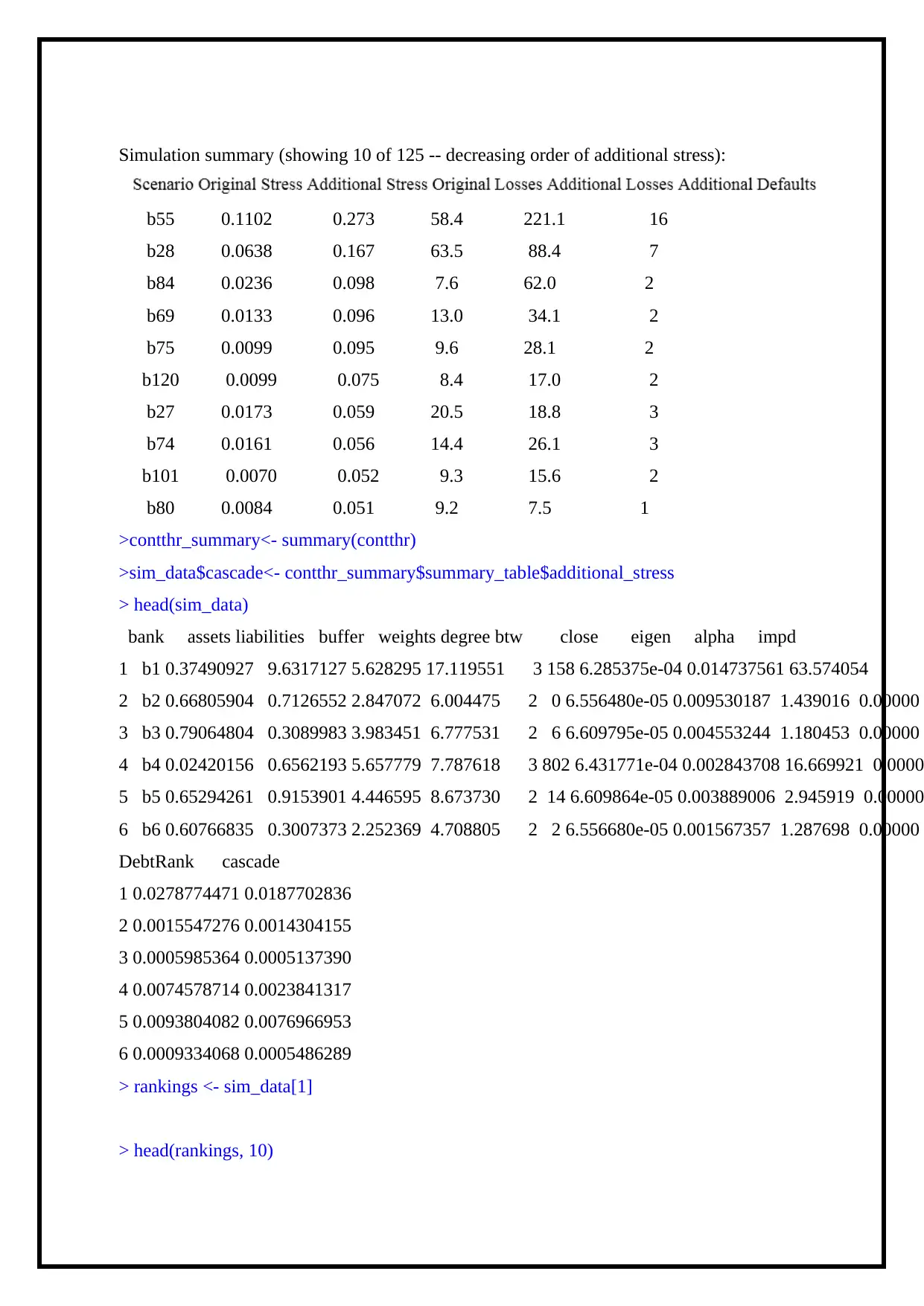

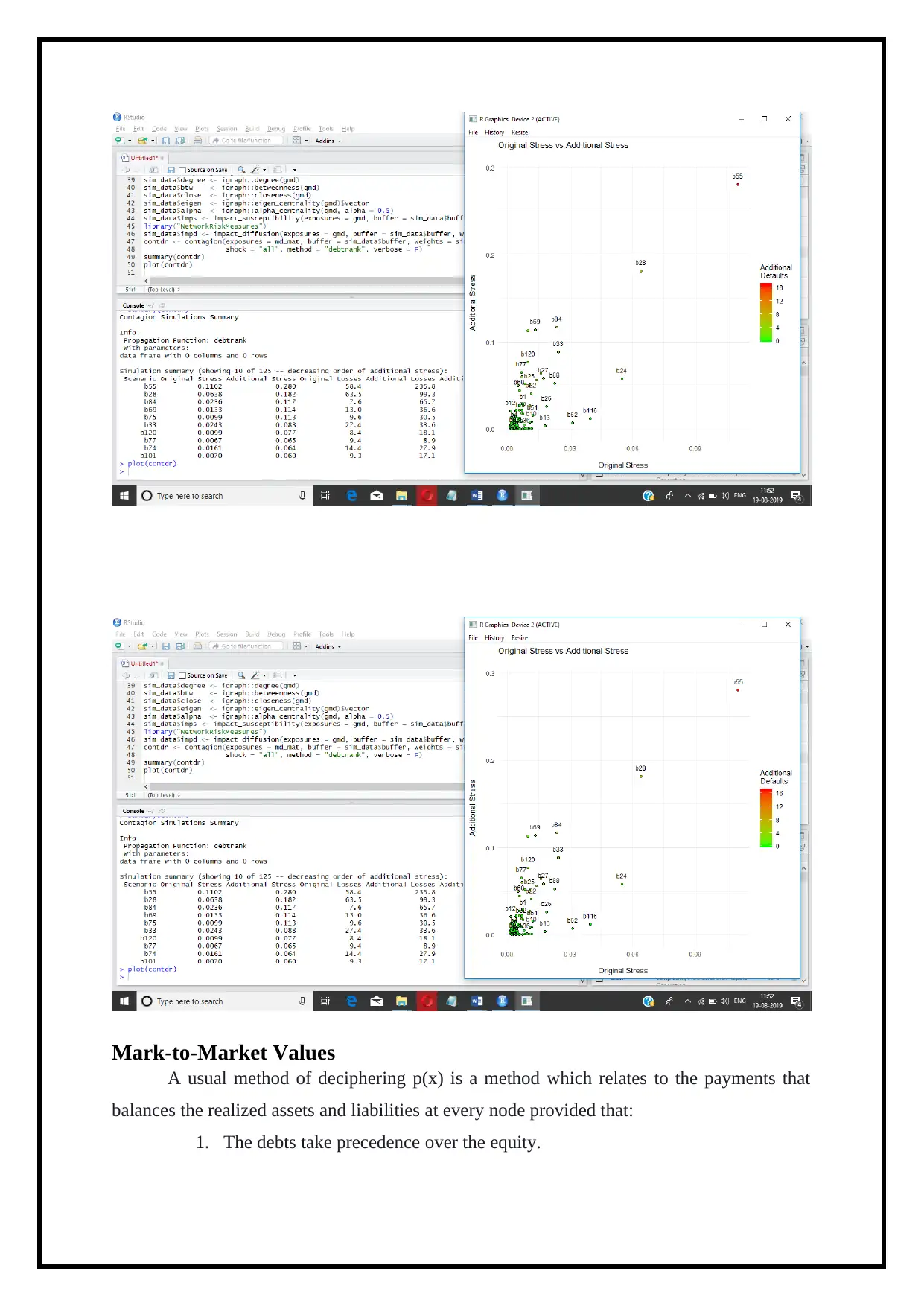

Simulation summary (showing 10 of 125 -- decreasing order of additional stress):

b55 0.1102 0.280 58.4 235.8 17

b28 0.0638 0.182 63.5 99.3 8

b84 0.0236 0.117 7.6 65.7 2

b69 0.0133 0.114 13.0 36.6 2

b75 0.0099 0.113 9.6 30.5 2

b33 0.0243 0.088 27.4 33.6 2

b120 0.0099 0.077 8.4 18.1 2

b77 0.0067 0.065 9.4 8.9 1

b74 0.0161 0.064 14.4 27.9 3

b101 0.0070 0.060 9.3 17.1 2

> plot(contdr)

Contagion Simulations Summary

Info:

Propagation Function: threshold

With parameters:

data frame with 0 columns and 0 rows

2 b2 0.66805904 0.7126552 2.847072 6.004475

3 b3 0.79064804 0.3089983 3.983451 6.777531

4 b4 0.02420156 0.6562193 5.657779 7.787618

5 b5 0.65294261 0.9153901 4.446595 8.673730

6 b6 0.60766835 0.3007373 2.252369 4.708805

> summary(contdr)

Contagion Simulations Summary

Info:

Propagation Function: debtrank

With parameters:

data frame with 0 columns and 0 rows

Simulation summary (showing 10 of 125 -- decreasing order of additional stress):

b55 0.1102 0.280 58.4 235.8 17

b28 0.0638 0.182 63.5 99.3 8

b84 0.0236 0.117 7.6 65.7 2

b69 0.0133 0.114 13.0 36.6 2

b75 0.0099 0.113 9.6 30.5 2

b33 0.0243 0.088 27.4 33.6 2

b120 0.0099 0.077 8.4 18.1 2

b77 0.0067 0.065 9.4 8.9 1

b74 0.0161 0.064 14.4 27.9 3

b101 0.0070 0.060 9.3 17.1 2

> plot(contdr)

Contagion Simulations Summary

Info:

Propagation Function: threshold

With parameters:

data frame with 0 columns and 0 rows

Simulation summary (showing 10 of 125 -- decreasing order of additional stress):

b55 0.1102 0.273 58.4 221.1 16

b28 0.0638 0.167 63.5 88.4 7

b84 0.0236 0.098 7.6 62.0 2

b69 0.0133 0.096 13.0 34.1 2

b75 0.0099 0.095 9.6 28.1 2

b120 0.0099 0.075 8.4 17.0 2

b27 0.0173 0.059 20.5 18.8 3

b74 0.0161 0.056 14.4 26.1 3

b101 0.0070 0.052 9.3 15.6 2

b80 0.0084 0.051 9.2 7.5 1

>contthr_summary<- summary(contthr)

>sim_data$cascade<- contthr_summary$summary_table$additional_stress

> head(sim_data)

bank assets liabilities buffer weights degree btw close eigen alpha impd

1 b1 0.37490927 9.6317127 5.628295 17.119551 3 158 6.285375e-04 0.014737561 63.574054

2 b2 0.66805904 0.7126552 2.847072 6.004475 2 0 6.556480e-05 0.009530187 1.439016 0.00000

3 b3 0.79064804 0.3089983 3.983451 6.777531 2 6 6.609795e-05 0.004553244 1.180453 0.00000

4 b4 0.02420156 0.6562193 5.657779 7.787618 3 802 6.431771e-04 0.002843708 16.669921 0.0000

5 b5 0.65294261 0.9153901 4.446595 8.673730 2 14 6.609864e-05 0.003889006 2.945919 0.00000

6 b6 0.60766835 0.3007373 2.252369 4.708805 2 2 6.556680e-05 0.001567357 1.287698 0.00000

DebtRank cascade

1 0.0278774471 0.0187702836

2 0.0015547276 0.0014304155

3 0.0005985364 0.0005137390

4 0.0074578714 0.0023841317

5 0.0093804082 0.0076966953

6 0.0009334068 0.0005486289

> rankings <- sim_data[1]

> head(rankings, 10)

b55 0.1102 0.273 58.4 221.1 16

b28 0.0638 0.167 63.5 88.4 7

b84 0.0236 0.098 7.6 62.0 2

b69 0.0133 0.096 13.0 34.1 2

b75 0.0099 0.095 9.6 28.1 2

b120 0.0099 0.075 8.4 17.0 2

b27 0.0173 0.059 20.5 18.8 3

b74 0.0161 0.056 14.4 26.1 3

b101 0.0070 0.052 9.3 15.6 2

b80 0.0084 0.051 9.2 7.5 1

>contthr_summary<- summary(contthr)

>sim_data$cascade<- contthr_summary$summary_table$additional_stress

> head(sim_data)

bank assets liabilities buffer weights degree btw close eigen alpha impd

1 b1 0.37490927 9.6317127 5.628295 17.119551 3 158 6.285375e-04 0.014737561 63.574054

2 b2 0.66805904 0.7126552 2.847072 6.004475 2 0 6.556480e-05 0.009530187 1.439016 0.00000

3 b3 0.79064804 0.3089983 3.983451 6.777531 2 6 6.609795e-05 0.004553244 1.180453 0.00000

4 b4 0.02420156 0.6562193 5.657779 7.787618 3 802 6.431771e-04 0.002843708 16.669921 0.0000

5 b5 0.65294261 0.9153901 4.446595 8.673730 2 14 6.609864e-05 0.003889006 2.945919 0.00000

6 b6 0.60766835 0.3007373 2.252369 4.708805 2 2 6.556680e-05 0.001567357 1.287698 0.00000

DebtRank cascade

1 0.0278774471 0.0187702836

2 0.0015547276 0.0014304155

3 0.0005985364 0.0005137390

4 0.0074578714 0.0023841317

5 0.0093804082 0.0076966953

6 0.0009334068 0.0005486289

> rankings <- sim_data[1]

> head(rankings, 10)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

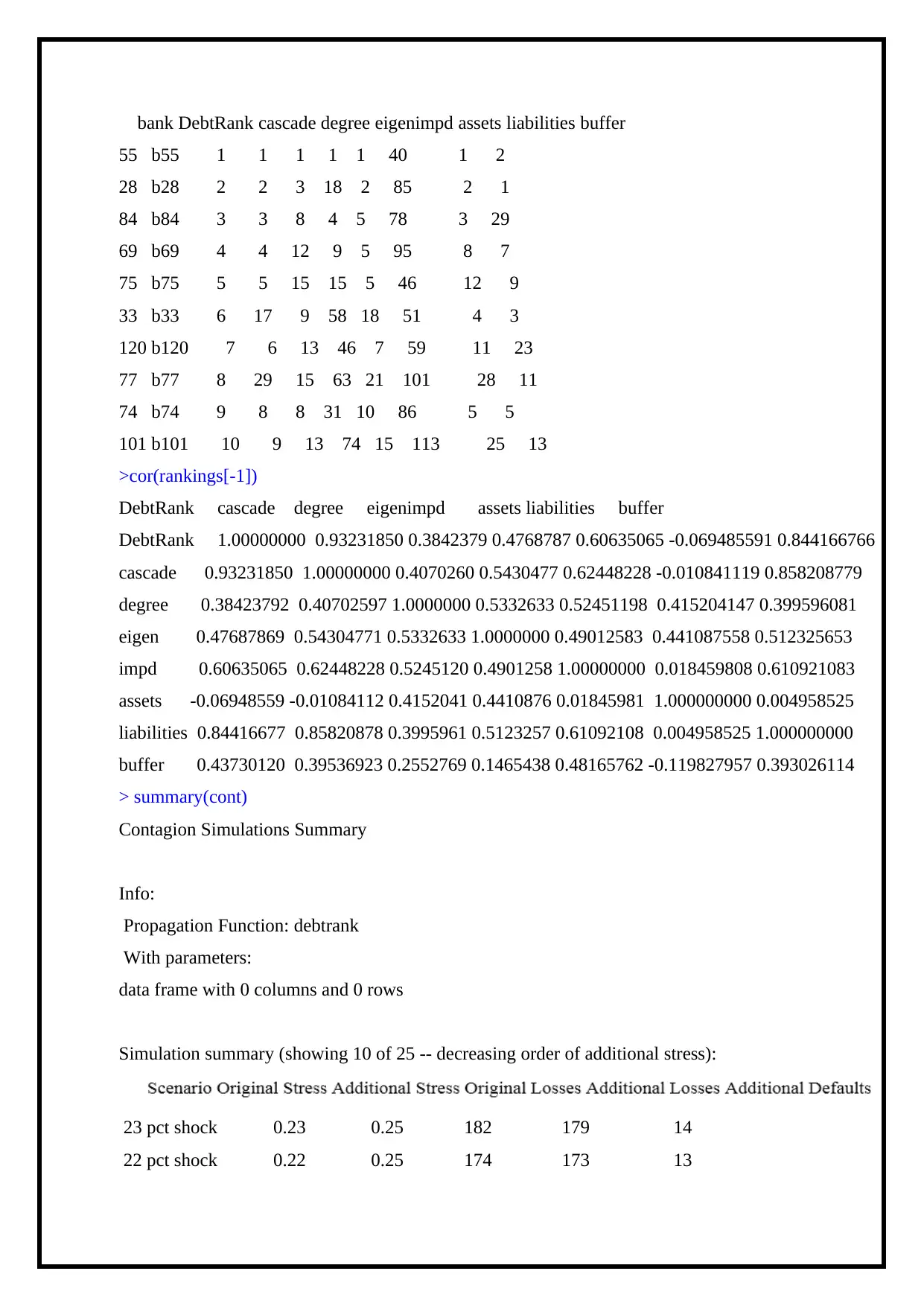

bank DebtRank cascade degree eigenimpd assets liabilities buffer

55 b55 1 1 1 1 1 40 1 2

28 b28 2 2 3 18 2 85 2 1

84 b84 3 3 8 4 5 78 3 29

69 b69 4 4 12 9 5 95 8 7

75 b75 5 5 15 15 5 46 12 9

33 b33 6 17 9 58 18 51 4 3

120 b120 7 6 13 46 7 59 11 23

77 b77 8 29 15 63 21 101 28 11

74 b74 9 8 8 31 10 86 5 5

101 b101 10 9 13 74 15 113 25 13

>cor(rankings[-1])

DebtRank cascade degree eigenimpd assets liabilities buffer

DebtRank 1.00000000 0.93231850 0.3842379 0.4768787 0.60635065 -0.069485591 0.844166766

cascade 0.93231850 1.00000000 0.4070260 0.5430477 0.62448228 -0.010841119 0.858208779

degree 0.38423792 0.40702597 1.0000000 0.5332633 0.52451198 0.415204147 0.399596081

eigen 0.47687869 0.54304771 0.5332633 1.0000000 0.49012583 0.441087558 0.512325653

impd 0.60635065 0.62448228 0.5245120 0.4901258 1.00000000 0.018459808 0.610921083

assets -0.06948559 -0.01084112 0.4152041 0.4410876 0.01845981 1.000000000 0.004958525

liabilities 0.84416677 0.85820878 0.3995961 0.5123257 0.61092108 0.004958525 1.000000000

buffer 0.43730120 0.39536923 0.2552769 0.1465438 0.48165762 -0.119827957 0.393026114

> summary(cont)

Contagion Simulations Summary

Info:

Propagation Function: debtrank

With parameters:

data frame with 0 columns and 0 rows

Simulation summary (showing 10 of 25 -- decreasing order of additional stress):

23 pct shock 0.23 0.25 182 179 14

22 pct shock 0.22 0.25 174 173 13

55 b55 1 1 1 1 1 40 1 2

28 b28 2 2 3 18 2 85 2 1

84 b84 3 3 8 4 5 78 3 29

69 b69 4 4 12 9 5 95 8 7

75 b75 5 5 15 15 5 46 12 9

33 b33 6 17 9 58 18 51 4 3

120 b120 7 6 13 46 7 59 11 23

77 b77 8 29 15 63 21 101 28 11

74 b74 9 8 8 31 10 86 5 5

101 b101 10 9 13 74 15 113 25 13

>cor(rankings[-1])

DebtRank cascade degree eigenimpd assets liabilities buffer

DebtRank 1.00000000 0.93231850 0.3842379 0.4768787 0.60635065 -0.069485591 0.844166766

cascade 0.93231850 1.00000000 0.4070260 0.5430477 0.62448228 -0.010841119 0.858208779

degree 0.38423792 0.40702597 1.0000000 0.5332633 0.52451198 0.415204147 0.399596081

eigen 0.47687869 0.54304771 0.5332633 1.0000000 0.49012583 0.441087558 0.512325653

impd 0.60635065 0.62448228 0.5245120 0.4901258 1.00000000 0.018459808 0.610921083

assets -0.06948559 -0.01084112 0.4152041 0.4410876 0.01845981 1.000000000 0.004958525

liabilities 0.84416677 0.85820878 0.3995961 0.5123257 0.61092108 0.004958525 1.000000000

buffer 0.43730120 0.39536923 0.2552769 0.1465438 0.48165762 -0.119827957 0.393026114

> summary(cont)

Contagion Simulations Summary

Info:

Propagation Function: debtrank

With parameters:

data frame with 0 columns and 0 rows

Simulation summary (showing 10 of 25 -- decreasing order of additional stress):

23 pct shock 0.23 0.25 182 179 14

22 pct shock 0.22 0.25 174 173 13

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

21 pct shock 0.21 0.25 166 167 12

24 pct shock 0.24 0.25 190 185 15

20 pct shock 0.20 0.25 158 161 11

25 pct shock 0.25 0.25 198 191 16

19 pct shock 0.19 0.25 150 155 10

18 pct shock 0.18 0.25 142 149 10

17 pct shock 0.17 0.24 134 142 10

16 pct shock 0.16 0.24 127 136 10

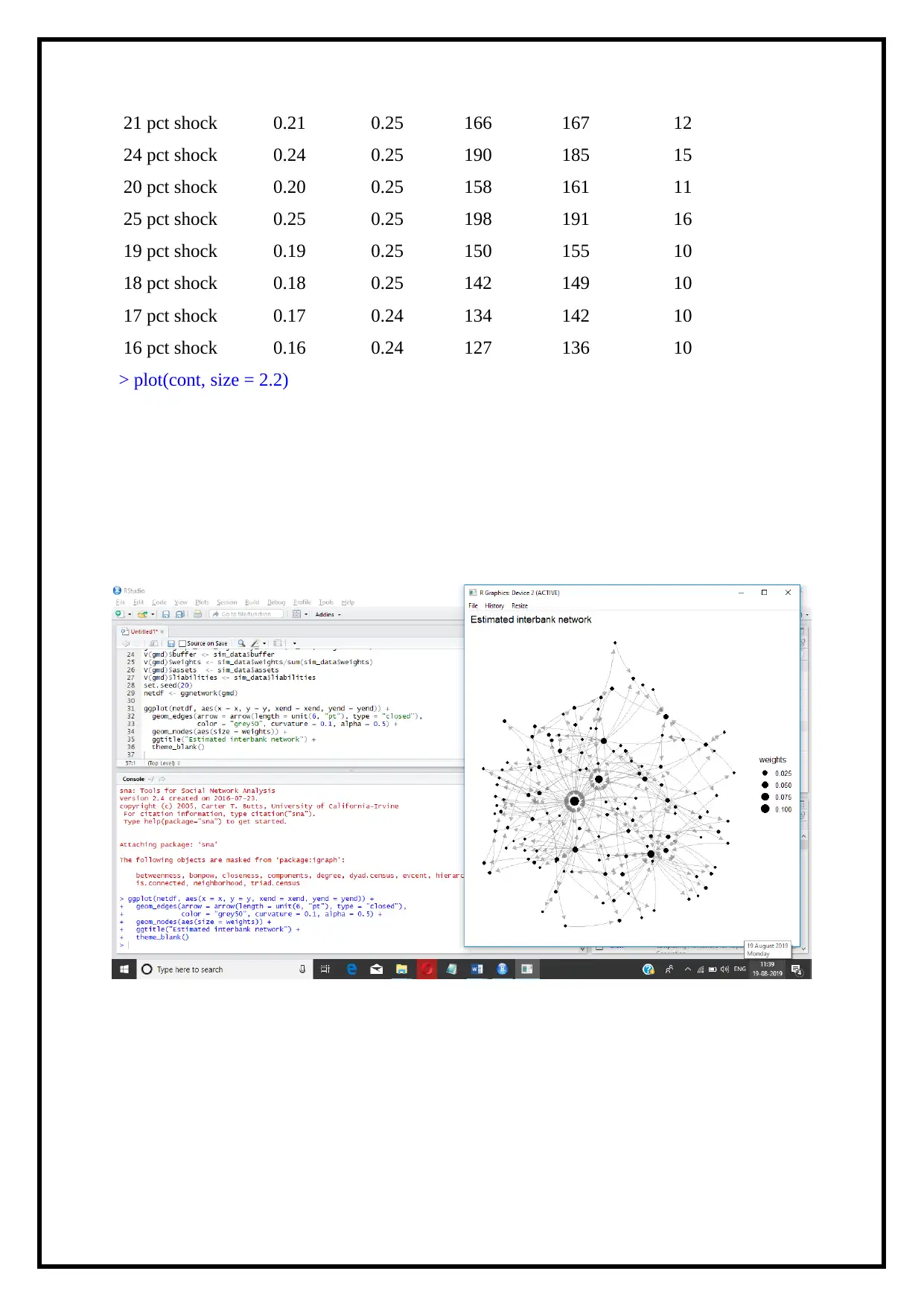

> plot(cont, size = 2.2)

24 pct shock 0.24 0.25 190 185 15

20 pct shock 0.20 0.25 158 161 11

25 pct shock 0.25 0.25 198 191 16

19 pct shock 0.19 0.25 150 155 10

18 pct shock 0.18 0.25 142 149 10

17 pct shock 0.17 0.24 134 142 10

16 pct shock 0.16 0.24 127 136 10

> plot(cont, size = 2.2)

Mark-to-Market Values

A usual method of deciphering p(x) is a method which relates to the payments that

balances the realized assets and liabilities at every node provided that:

1. The debts take precedence over the equity.

A usual method of deciphering p(x) is a method which relates to the payments that

balances the realized assets and liabilities at every node provided that:

1. The debts take precedence over the equity.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 21

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.