Case Study: R plc Financial Analysis for Business Finance BMS512

VerifiedAdded on 2023/06/15

|6

|1273

|81

Case Study

AI Summary

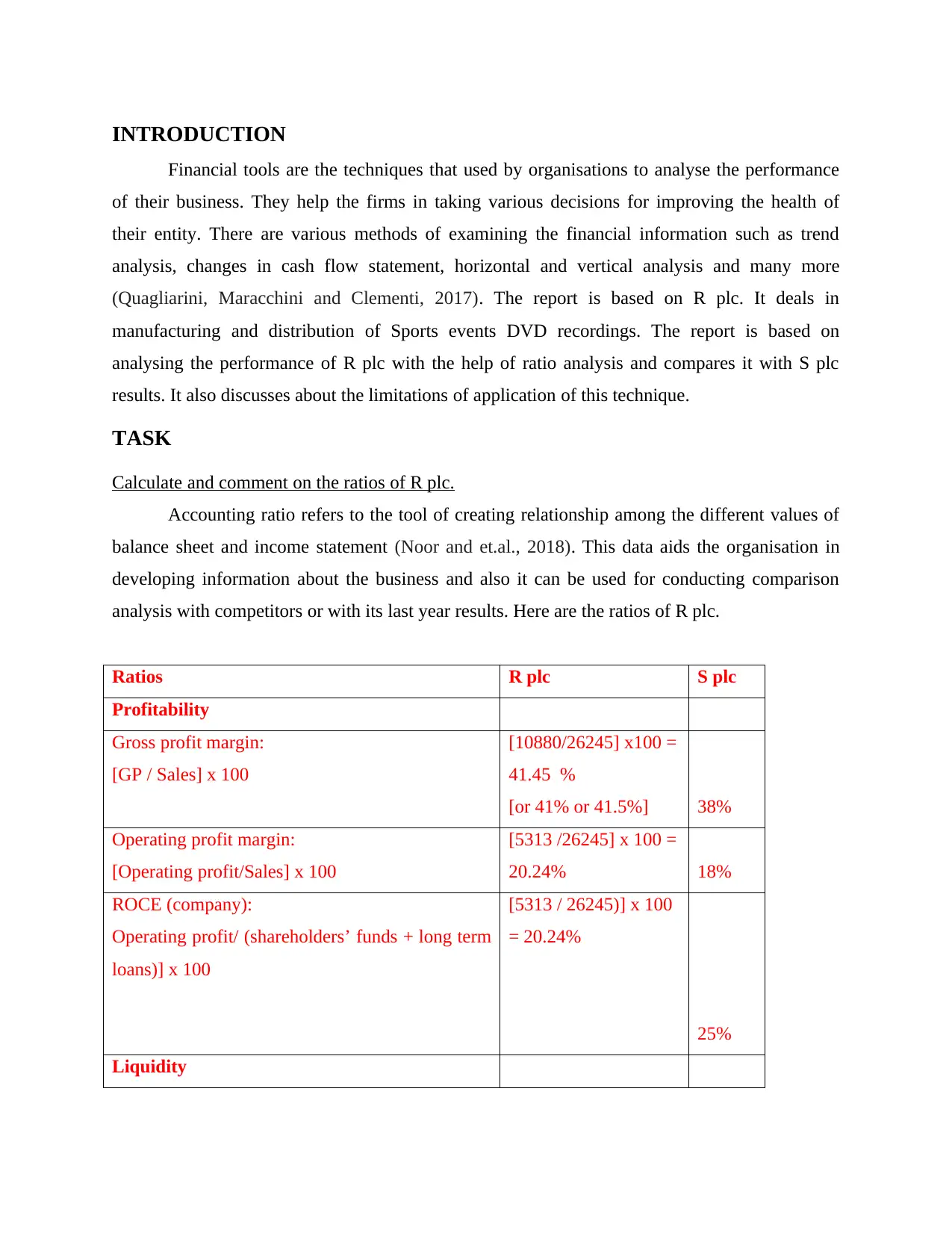

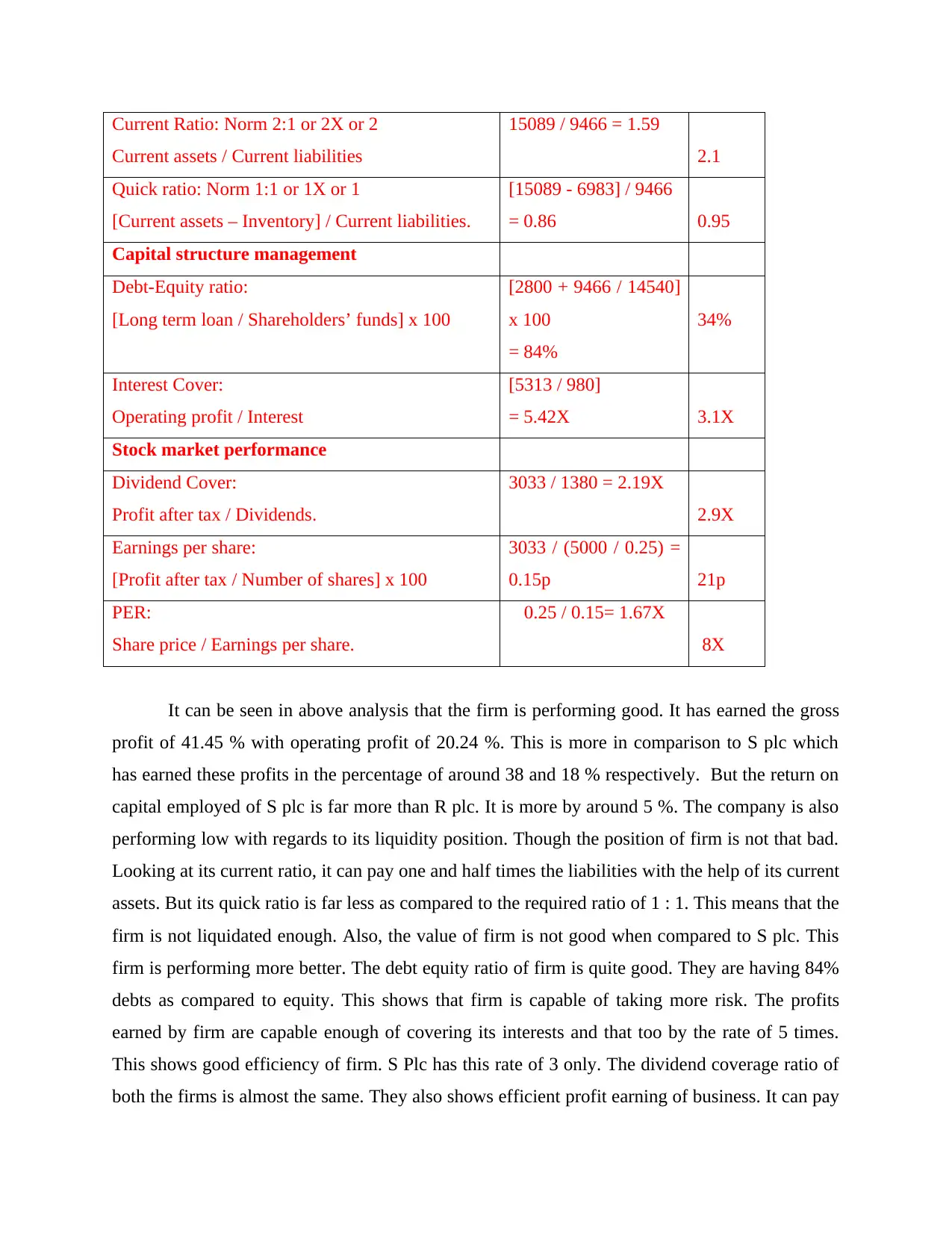

This case study provides a financial analysis of R plc, a company involved in the manufacturing and distribution of sports events DVD recordings, using ratio analysis. It calculates and comments on key financial ratios such as gross profit margin, operating profit margin, ROCE, current ratio, quick ratio, debt-equity ratio, interest cover, dividend cover, earnings per share, and PER. The analysis compares R plc's performance with S plc, highlighting strengths and weaknesses in profitability, liquidity, capital structure, and stock market performance. While R plc demonstrates strong gross profit and operating profit margins, its ROCE and quick ratio lag behind S plc. The study also acknowledges the limitations of ratio analysis, including reliance on potentially manipulated financial statement figures and neglect of qualitative factors. Desklib offers a wealth of similar solved assignments and past papers for students.

1 out of 6

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.