ACC506 Task 2B: Financial Statement Analysis and Ratios - R Reed Co.

VerifiedAdded on 2023/06/15

|10

|1382

|335

Report

AI Summary

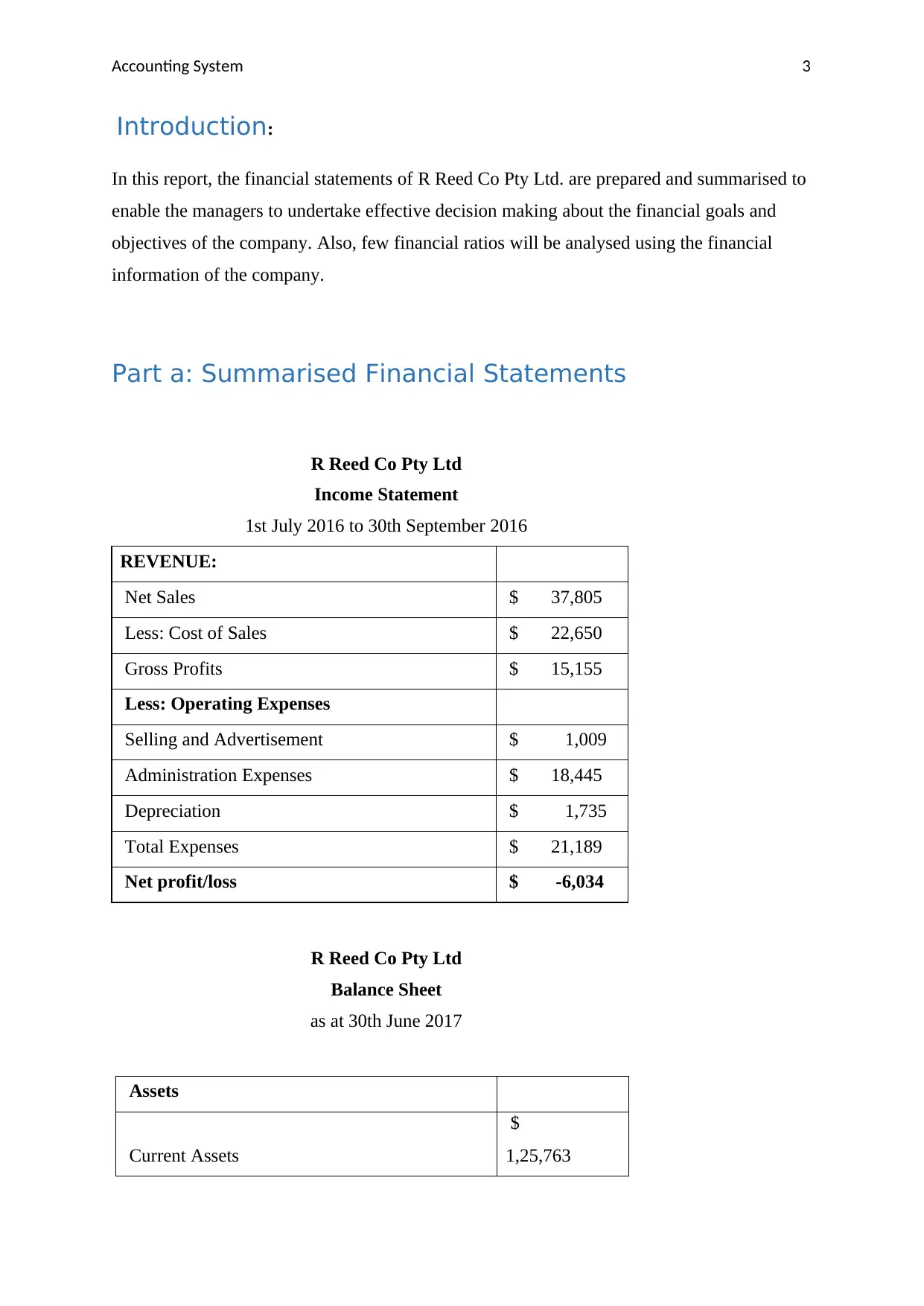

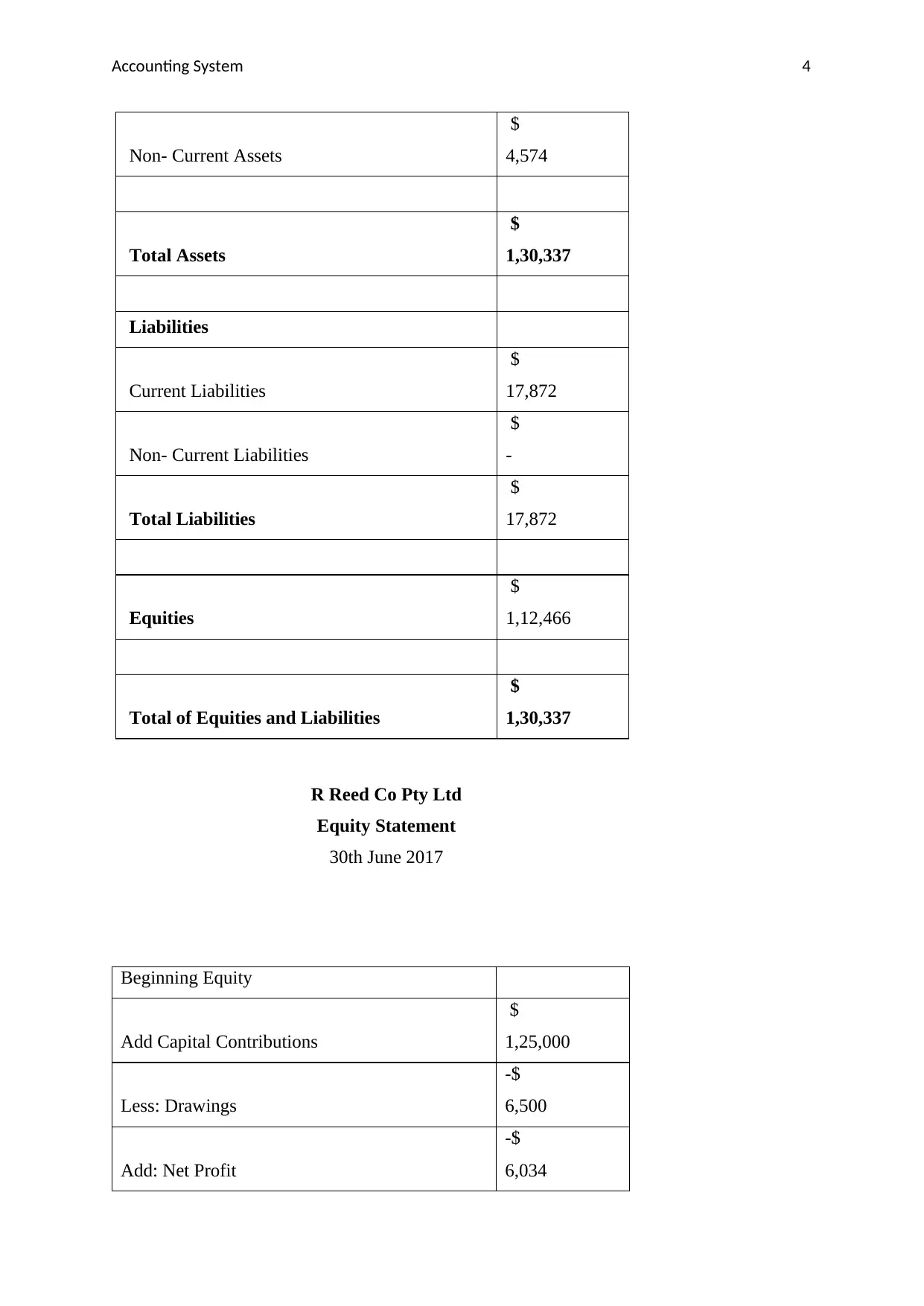

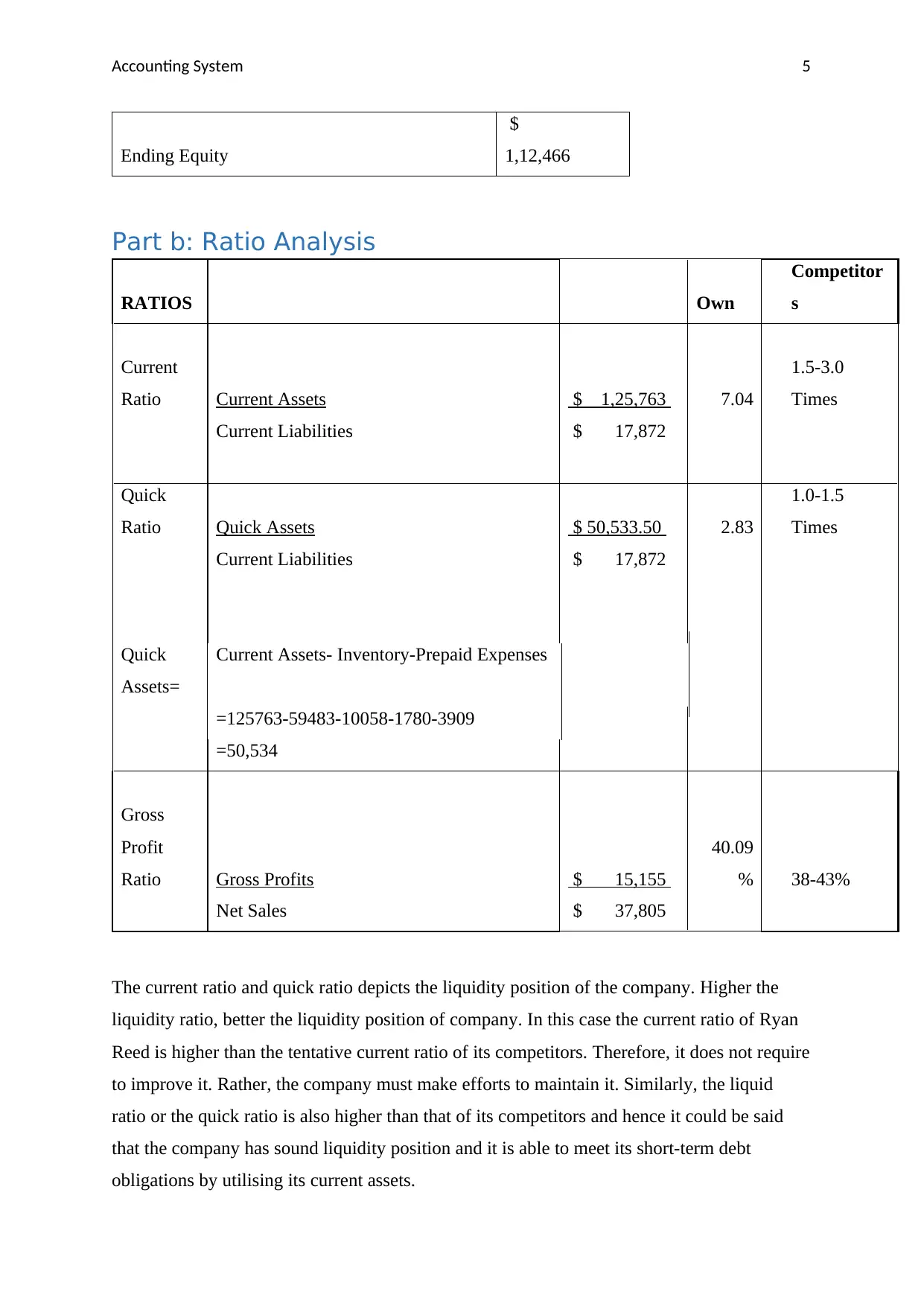

This report presents a summarized analysis of the financial statements for R Reed Co Pty Ltd, covering the period from July 2016 to June 2017. It includes an income statement, balance sheet, and equity statement, followed by a ratio analysis focusing on liquidity and profitability. The current and quick ratios indicate a strong liquidity position compared to competitors, while the gross profit ratio is within the competitive range. However, the company experienced a net loss due to high operating expenses. The report also discusses different depreciation and inventory valuation methods, as well as internal controls that can be implemented to mitigate financial and operational risks. The analysis highlights the importance of understanding accounting concepts for effective financial statement preparation and presentation.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.