Taxation Law Assignment: Analysis of Racing Parts Pty Ltd (LEGL300)

VerifiedAdded on 2023/04/04

|22

|2096

|126

Homework Assignment

AI Summary

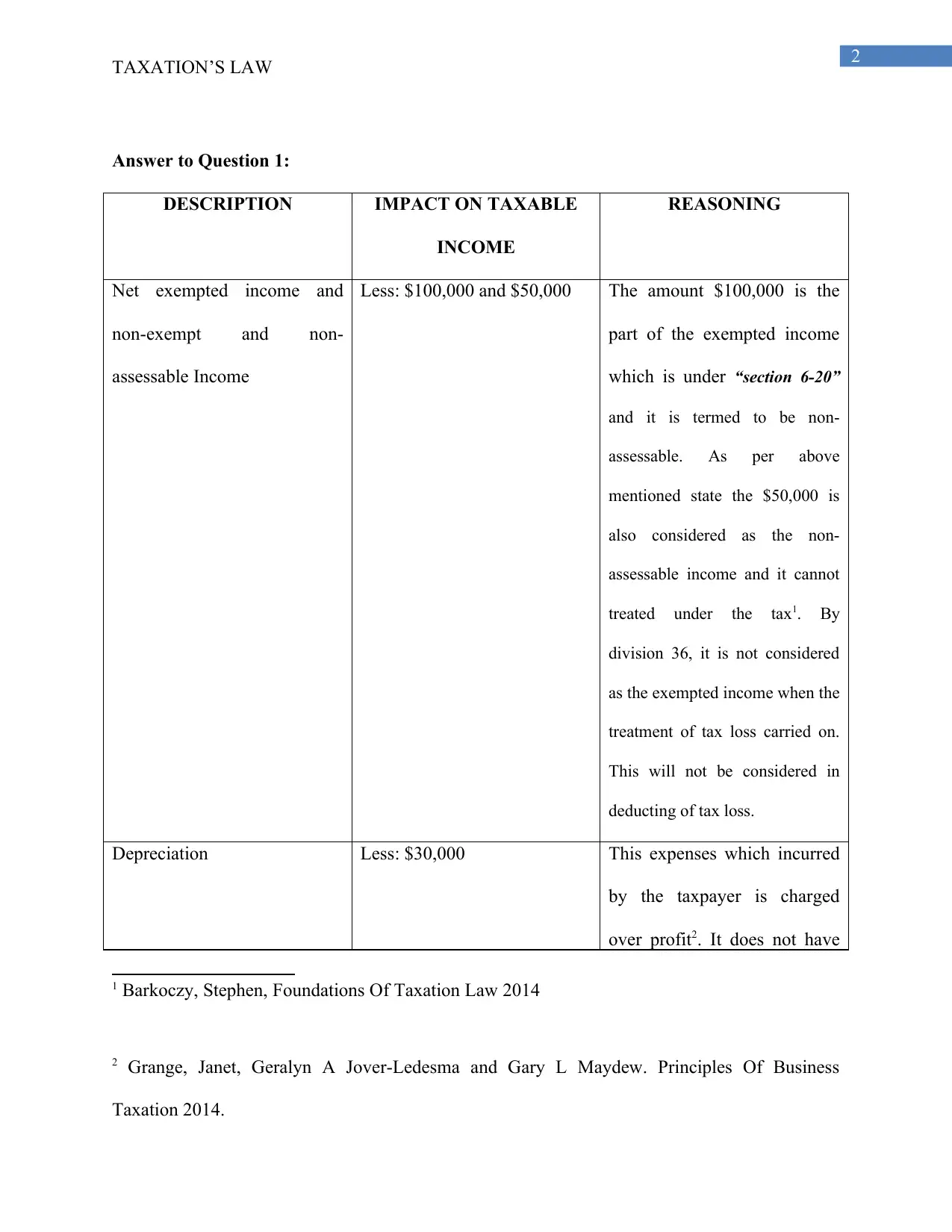

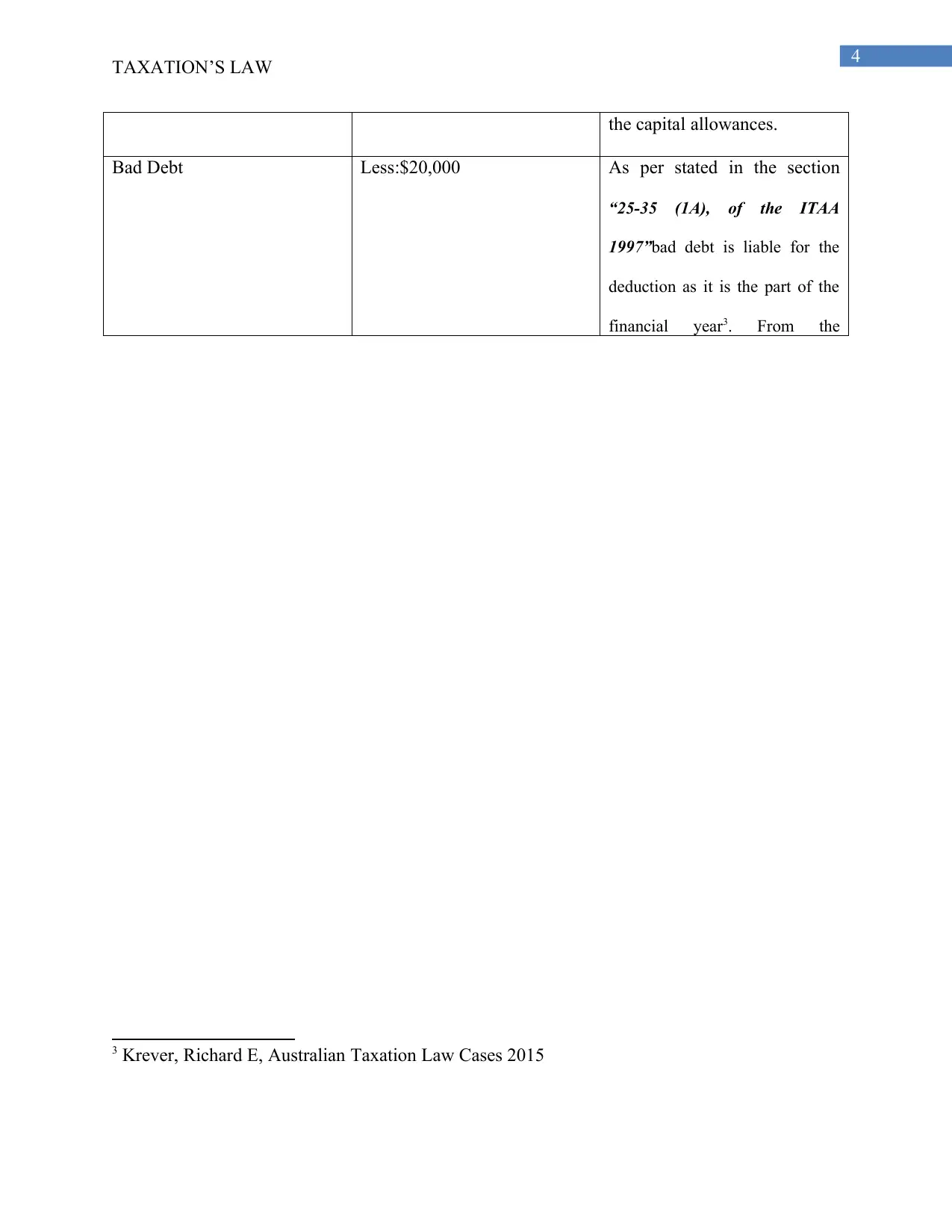

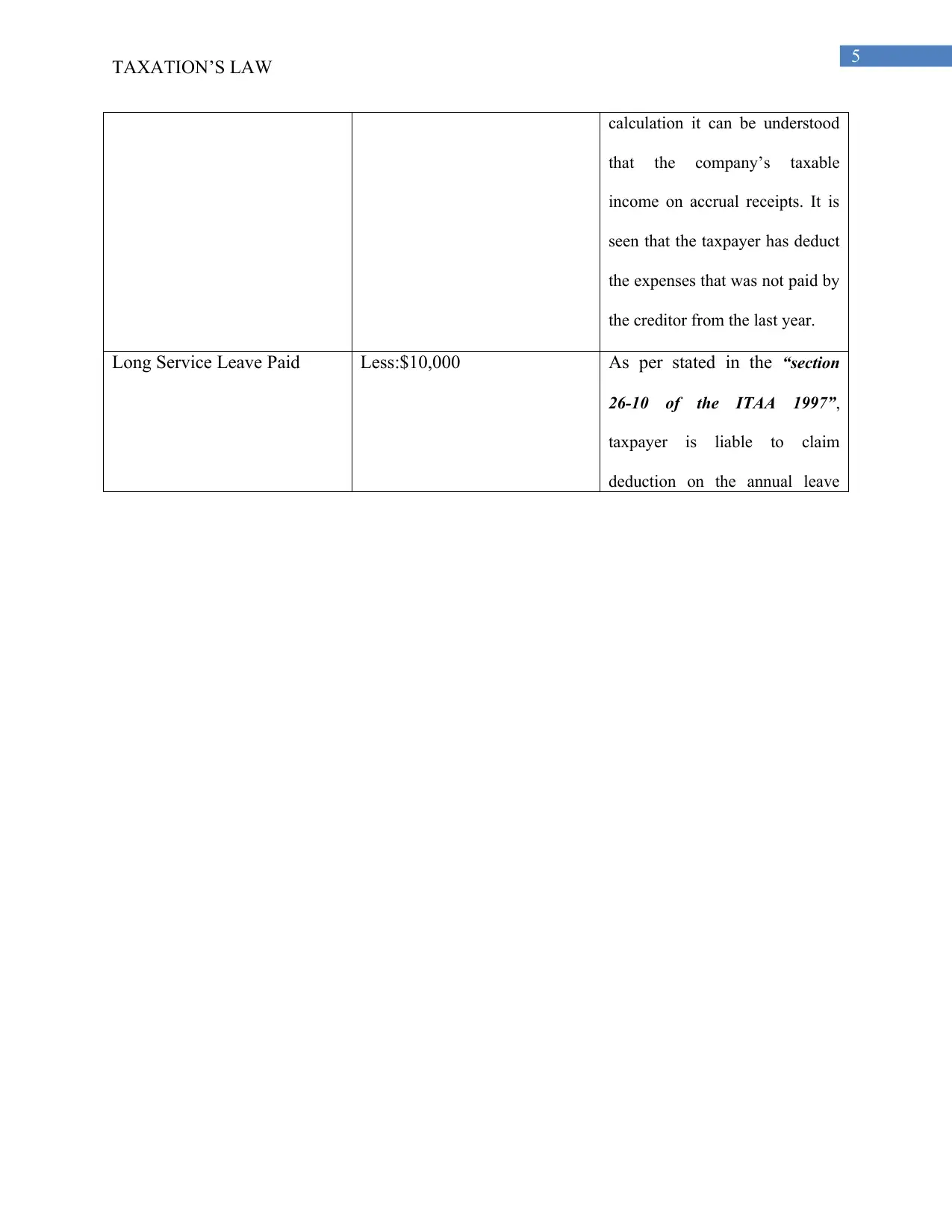

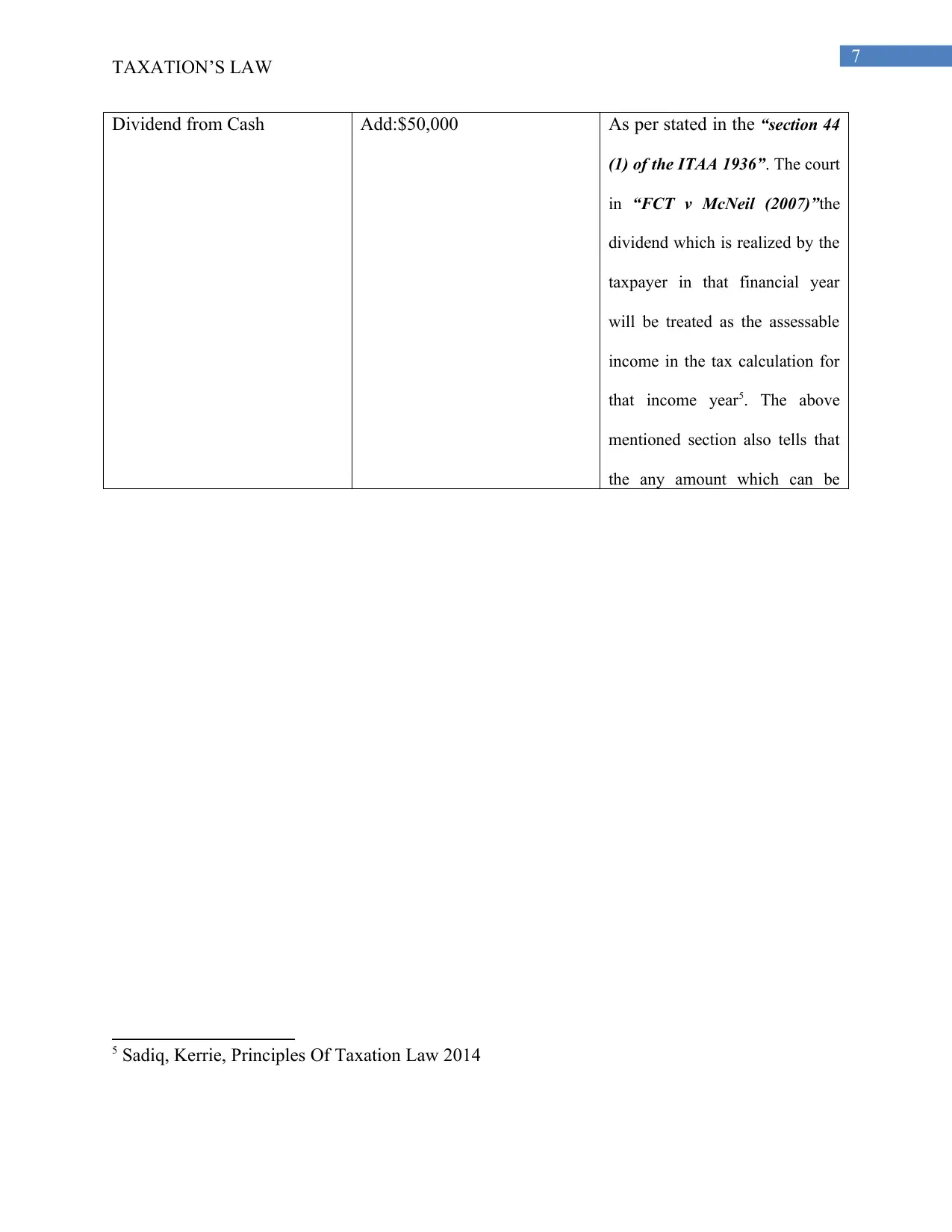

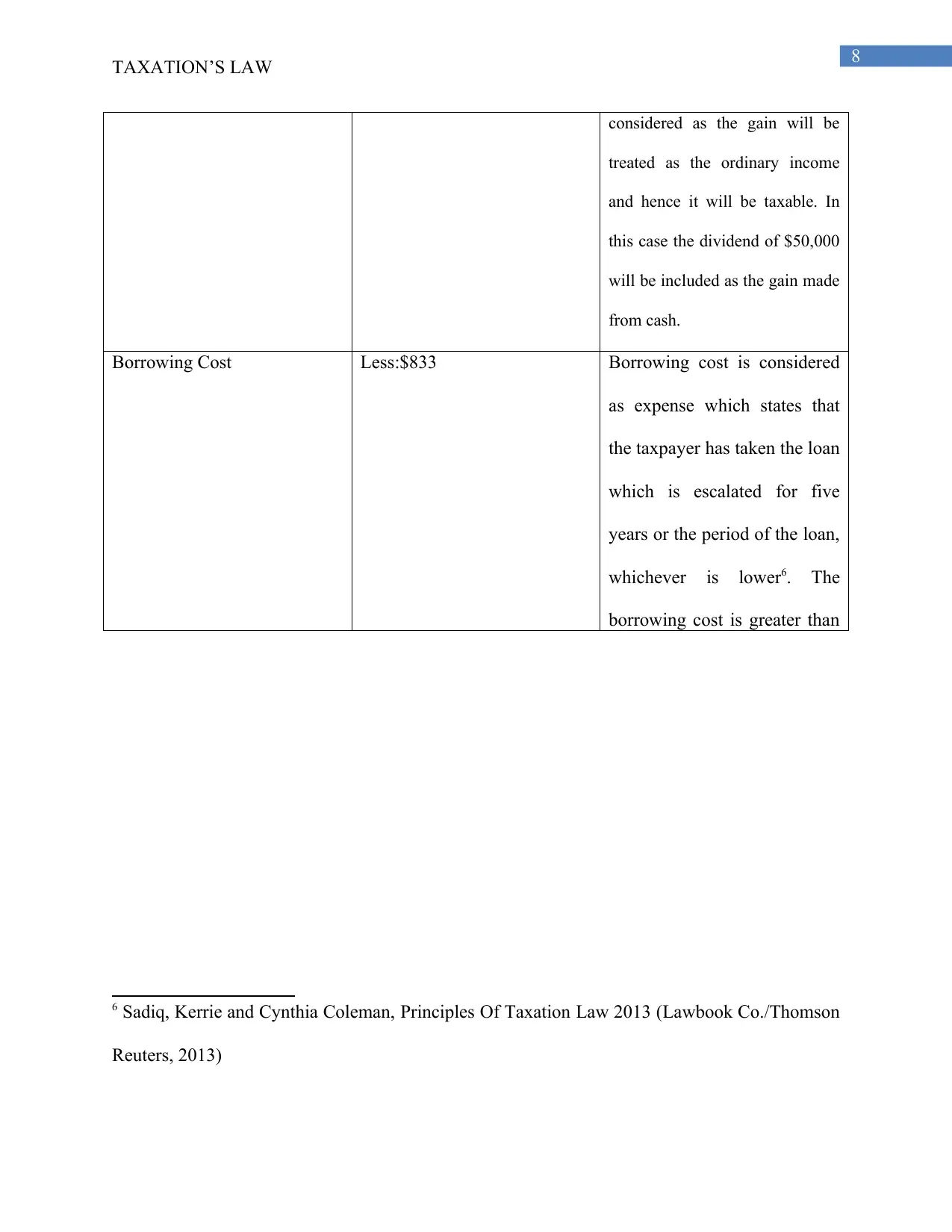

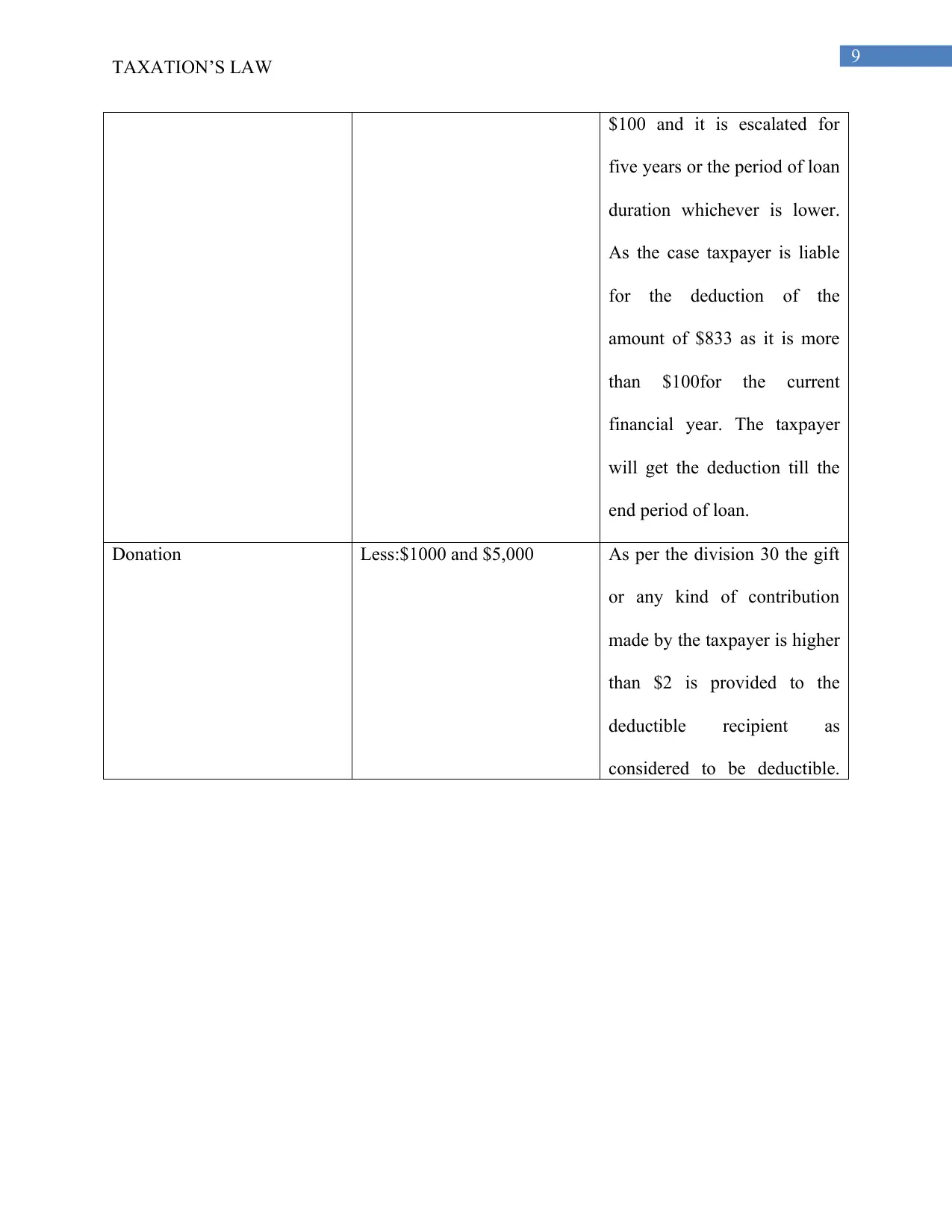

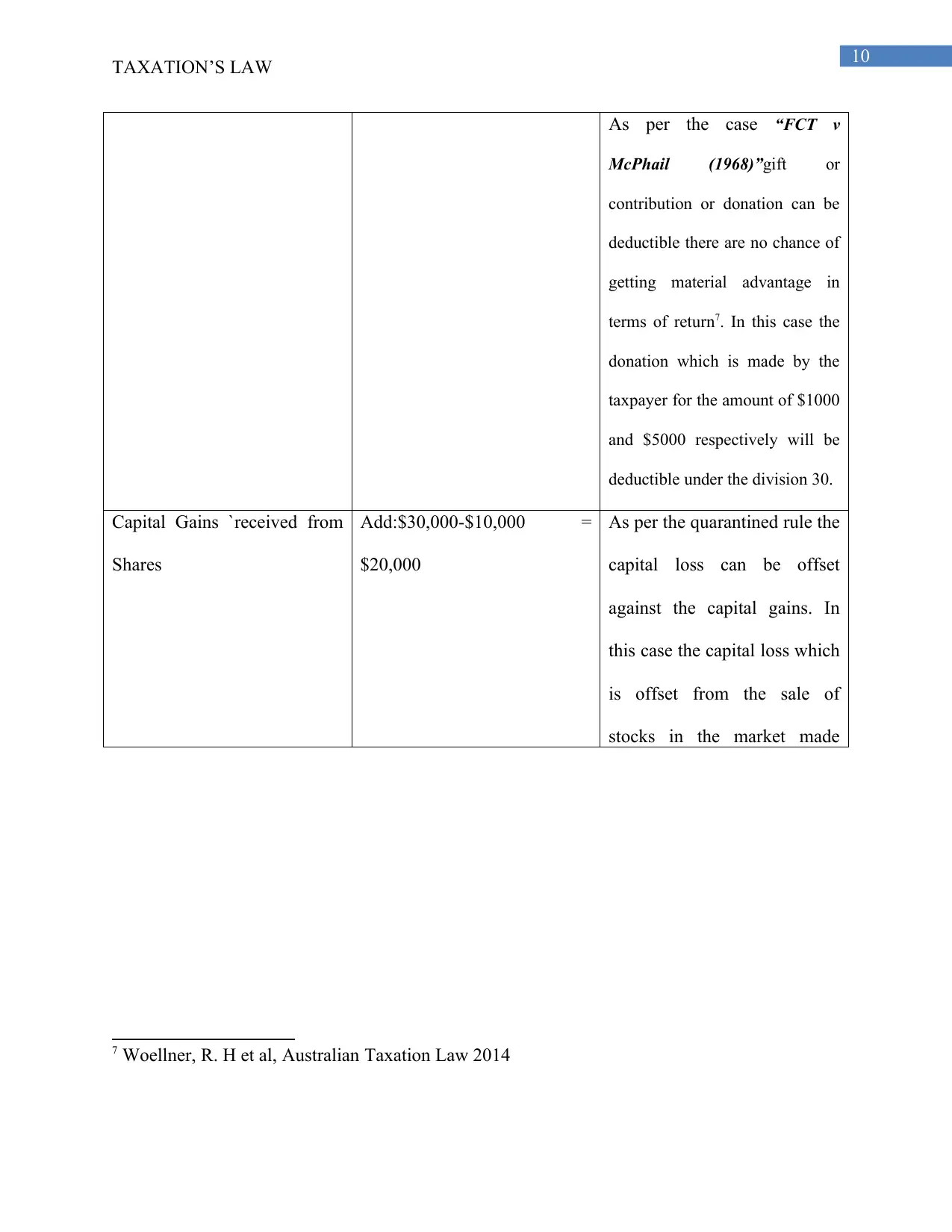

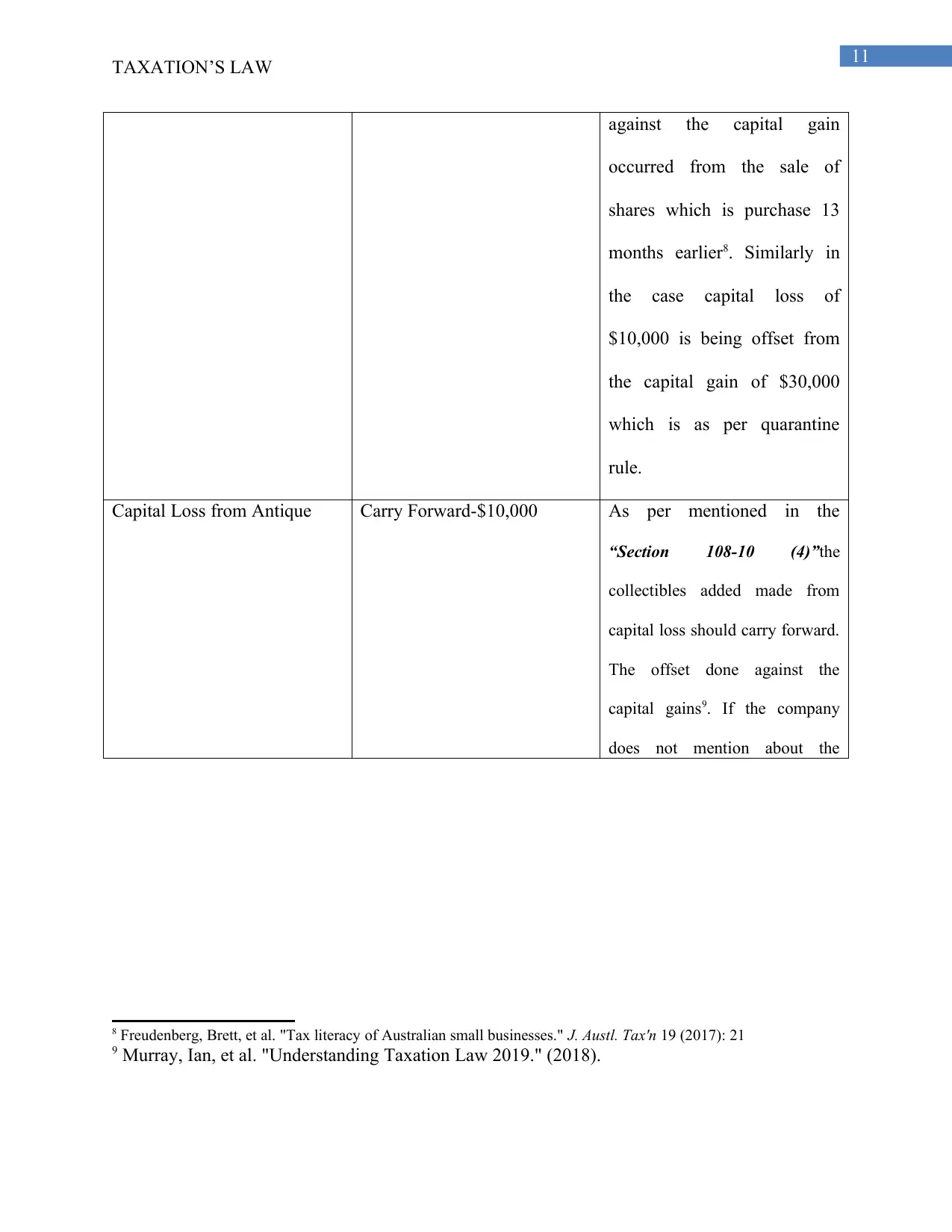

This assignment analyzes the taxation implications for Racing Parts Pty Ltd, an Australian resident private company and small business entity, for the year ended 30 June. The assignment addresses two key questions, with the first question detailing the impact of various income and expense items on taxable income, including depreciation, bad debt, long service leave paid, dividends, borrowing costs, donations, capital gains and losses, and cost of goods sold. The second question examines the tax consequences and reasoning behind specific financial transactions, such as interest on a loan, carpet replacement costs, an antique desk, travel expenses, the sale of a house (partially used as a main residence), and the sale of an antique, outlining what is deductible and what is not. The analysis includes relevant sections from the ITAA and case law to support the tax treatment of each item. The assignment follows AGLC referencing guidelines and is submitted via Turnitin.

1 out of 22

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.