THH3113 Cost & Performance Management for Tourism: Radisson Blu

VerifiedAdded on 2023/06/08

|8

|2259

|79

Report

AI Summary

This report provides a detailed analysis of cost and performance management within the context of Radisson Blu Plaza Hotel Sydney. It identifies key cost drivers, differentiating between fixed and variable costs, and examines their impact on the hotel's financial performance. The report includes a break-even analysis, calculating the number of rooms and revenue required to cover all expenses, and explores target profit implementation strategies, comparing different options for achieving specific profit goals. The analysis considers factors such as labor costs, utilities, marketing expenses, and insurance, ultimately recommending a strategy that maximizes revenue potential and operational efficiency for the hotel during its peak season. This document is available on Desklib, a platform offering a wide range of academic resources for students.

Running head: COST AND PERFORMANCE MANAGEMENT

Cost and Performance Management

Name of the Student

Name of the University

Author’s Note

Cost and Performance Management

Name of the Student

Name of the University

Author’s Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1COST AND PERFORMANCE MANAGEMENT

Table of Contents

Introduction......................................................................................................................................2

Cost Drivers and Cost Behaviors.....................................................................................................2

Break Even Analysis........................................................................................................................3

Target Profit Implementation..........................................................................................................4

Conclusion and Recommendation...................................................................................................5

References........................................................................................................................................6

Table of Contents

Introduction......................................................................................................................................2

Cost Drivers and Cost Behaviors.....................................................................................................2

Break Even Analysis........................................................................................................................3

Target Profit Implementation..........................................................................................................4

Conclusion and Recommendation...................................................................................................5

References........................................................................................................................................6

2COST AND PERFORMANCE MANAGEMENT

Introduction

Cost and performance management is considered as an important factor that the cost

accountants of the companies need to take into account while conducting the costing activities.

In the aspect of cost and performance management, they are needed to divide all the costs

between fixed and variable cost for the ease in the calculation for the total costs (Cooper, 2017).

At the same time, it helps the cost accountants in the identification of the major cost drivers so

that correct decision can be taken related to the selection of the correct costing option. At the

same time, they are also required to take into consideration the break-even analysis to get the

idea about the minimum amount of input they are needed to sell for generating business profit

(Hilton & Platt, 2013). The main aim of this report is to analyze and evaluate different aspects of

coat and performance management of Radisson Blu Plaza Hotel Sydney.

Cost Drivers and Cost Behaviors

Identification as well as the determination of the cost drivers is a major activity in the

cost management of the companies and there is not any exception of this fact in the provide case.

At the time of the determination of the cost drivers of a business, it is needed to mention that the

presence of two types of costs can be seen in the business organizations; they are Fixed costs and

Variable costs; and both these costs are important for the companies at the time to determine the

cost drivers. Fixed costs are independent of output and they remain unchanged throughout the

relevant range. On the contrary, variable costs vary with the outputs (Drury, 2013).

Prior to the determination of the cost drivers, it needs to be mentioned that three types of

cost drivers are there; they are Volume, Time and Charge. Volume cost drivers are dependent on

the units of work and the related cost of the activity increases due to the processing of more

units. Time cost drivers are dependent on the length of time taken for the completion of the

activity and increase in cost of the activity can be seen based on the required time. Charge cost

drivers are directly charged to the cost objectives (Noreen, Brewer & Garrison, 2014).

Cost drivers can be considered as the direct cause of a cost and its effect on the incurred

total cost. The presence of some major cost drivers can be seen in the business of Radisson Blu.

In case of the wages of the fixed as well as casual employees, the cost driver is the number of

labor hours as the company provides their employees with the wages based on the hours they are

working for the hotel (Matherly & Burney, 2013). In case of internet charges, number of hours is

the cost drivers as the company charges for the use of internet based the number of hours the

customers are using internet. Number of guests is the cost driver for free breakfast charges as this

cost depends on the number how many guests are taking breakfast.

The cost driver for electricity and water expenses is number of units used as these costs

are determined based on the usage of the units (Appelbaum et al., 2017). The cost driver for

public liability insurance and superannuation charges for employees is the number of employees

Introduction

Cost and performance management is considered as an important factor that the cost

accountants of the companies need to take into account while conducting the costing activities.

In the aspect of cost and performance management, they are needed to divide all the costs

between fixed and variable cost for the ease in the calculation for the total costs (Cooper, 2017).

At the same time, it helps the cost accountants in the identification of the major cost drivers so

that correct decision can be taken related to the selection of the correct costing option. At the

same time, they are also required to take into consideration the break-even analysis to get the

idea about the minimum amount of input they are needed to sell for generating business profit

(Hilton & Platt, 2013). The main aim of this report is to analyze and evaluate different aspects of

coat and performance management of Radisson Blu Plaza Hotel Sydney.

Cost Drivers and Cost Behaviors

Identification as well as the determination of the cost drivers is a major activity in the

cost management of the companies and there is not any exception of this fact in the provide case.

At the time of the determination of the cost drivers of a business, it is needed to mention that the

presence of two types of costs can be seen in the business organizations; they are Fixed costs and

Variable costs; and both these costs are important for the companies at the time to determine the

cost drivers. Fixed costs are independent of output and they remain unchanged throughout the

relevant range. On the contrary, variable costs vary with the outputs (Drury, 2013).

Prior to the determination of the cost drivers, it needs to be mentioned that three types of

cost drivers are there; they are Volume, Time and Charge. Volume cost drivers are dependent on

the units of work and the related cost of the activity increases due to the processing of more

units. Time cost drivers are dependent on the length of time taken for the completion of the

activity and increase in cost of the activity can be seen based on the required time. Charge cost

drivers are directly charged to the cost objectives (Noreen, Brewer & Garrison, 2014).

Cost drivers can be considered as the direct cause of a cost and its effect on the incurred

total cost. The presence of some major cost drivers can be seen in the business of Radisson Blu.

In case of the wages of the fixed as well as casual employees, the cost driver is the number of

labor hours as the company provides their employees with the wages based on the hours they are

working for the hotel (Matherly & Burney, 2013). In case of internet charges, number of hours is

the cost drivers as the company charges for the use of internet based the number of hours the

customers are using internet. Number of guests is the cost driver for free breakfast charges as this

cost depends on the number how many guests are taking breakfast.

The cost driver for electricity and water expenses is number of units used as these costs

are determined based on the usage of the units (Appelbaum et al., 2017). The cost driver for

public liability insurance and superannuation charges for employees is the number of employees

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3COST AND PERFORMANCE MANAGEMENT

as these expenses are charged based on the number of employees of the hotel. The cost driver for

laundry expenses is the number of guests in the hotel as this expense is charged based on the

number of guests. Number of minutes is the cost driver for telephone expenses as this

expenditure depends on the number of units people talk over the phone (Park & Jang, 2014).

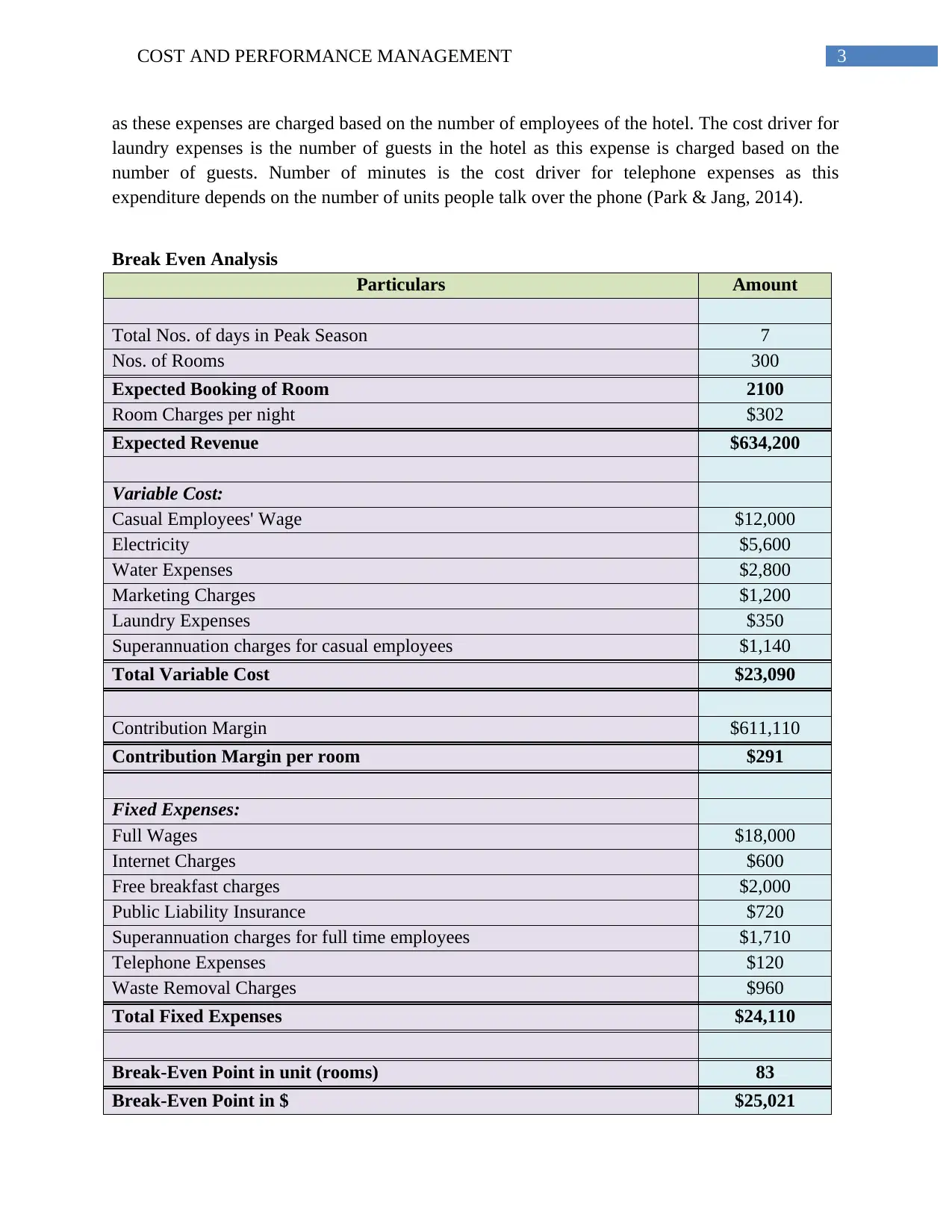

Break Even Analysis

Particulars Amount

Total Nos. of days in Peak Season 7

Nos. of Rooms 300

Expected Booking of Room 2100

Room Charges per night $302

Expected Revenue $634,200

Variable Cost:

Casual Employees' Wage $12,000

Electricity $5,600

Water Expenses $2,800

Marketing Charges $1,200

Laundry Expenses $350

Superannuation charges for casual employees $1,140

Total Variable Cost $23,090

Contribution Margin $611,110

Contribution Margin per room $291

Fixed Expenses:

Full Wages $18,000

Internet Charges $600

Free breakfast charges $2,000

Public Liability Insurance $720

Superannuation charges for full time employees $1,710

Telephone Expenses $120

Waste Removal Charges $960

Total Fixed Expenses $24,110

Break-Even Point in unit (rooms) 83

Break-Even Point in $ $25,021

as these expenses are charged based on the number of employees of the hotel. The cost driver for

laundry expenses is the number of guests in the hotel as this expense is charged based on the

number of guests. Number of minutes is the cost driver for telephone expenses as this

expenditure depends on the number of units people talk over the phone (Park & Jang, 2014).

Break Even Analysis

Particulars Amount

Total Nos. of days in Peak Season 7

Nos. of Rooms 300

Expected Booking of Room 2100

Room Charges per night $302

Expected Revenue $634,200

Variable Cost:

Casual Employees' Wage $12,000

Electricity $5,600

Water Expenses $2,800

Marketing Charges $1,200

Laundry Expenses $350

Superannuation charges for casual employees $1,140

Total Variable Cost $23,090

Contribution Margin $611,110

Contribution Margin per room $291

Fixed Expenses:

Full Wages $18,000

Internet Charges $600

Free breakfast charges $2,000

Public Liability Insurance $720

Superannuation charges for full time employees $1,710

Telephone Expenses $120

Waste Removal Charges $960

Total Fixed Expenses $24,110

Break-Even Point in unit (rooms) 83

Break-Even Point in $ $25,021

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4COST AND PERFORMANCE MANAGEMENT

Break-even point analysis can be considered as a measurement system for the calculation

of margin of safety with the help of the comparison of the revenue amount or units that is needed

to be sold for covering the fixed as well as variable costs associated with sales (Morano &

Tajani, 2017). In other words, t can be considered as a process for calculating the time of

profitability of a project by equating its total revenue with its total expenses. It needs to be

mentioned that the main purpose of the break-even analysis is the calculation of the amount of

sales that makes the revenues equal to expenses; and the amount of excess revenue is considered

as profit after meeting both the fixed and variable costs (Morano & Tajani, 2013). The process to

calculate the break-even point is to divide the total fixed costs of production by the price per unit

less the variable cost.

It can be seen from the above table that the break-even point in unit for Radisson Blu is

83 rooms and the break-even point in $ is $25,021. It implies that in order to cover all the fixed

as well as variable expenses, it is needed for the management of Radisson Blu to do booking of

83 rooms. In other words, the hotel needs to earn revenue of $25,021 in order to cover all the

fixed as well as variable expenses (Nagle & Müller, 2017).

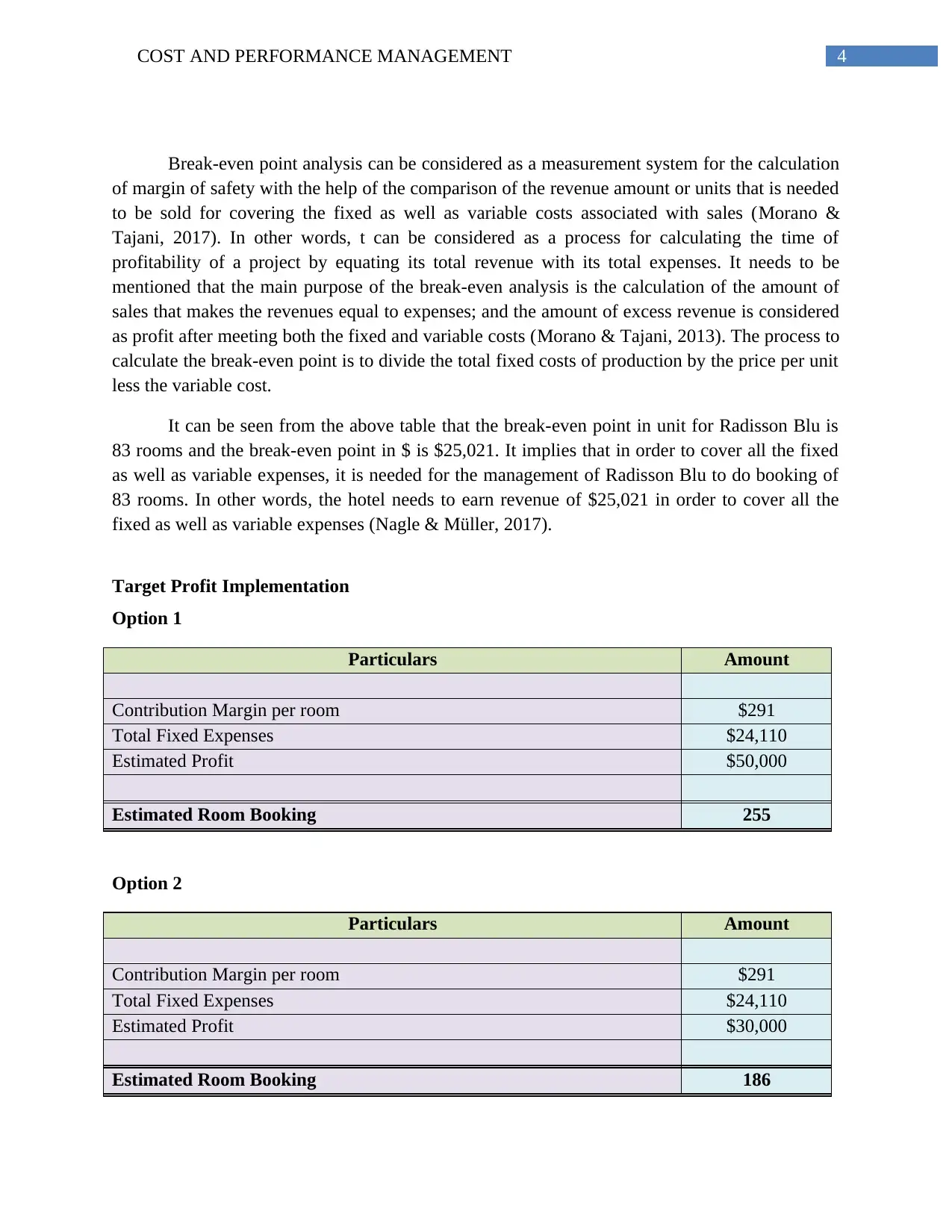

Target Profit Implementation

Option 1

Particulars Amount

Contribution Margin per room $291

Total Fixed Expenses $24,110

Estimated Profit $50,000

Estimated Room Booking 255

Option 2

Particulars Amount

Contribution Margin per room $291

Total Fixed Expenses $24,110

Estimated Profit $30,000

Estimated Room Booking 186

Break-even point analysis can be considered as a measurement system for the calculation

of margin of safety with the help of the comparison of the revenue amount or units that is needed

to be sold for covering the fixed as well as variable costs associated with sales (Morano &

Tajani, 2017). In other words, t can be considered as a process for calculating the time of

profitability of a project by equating its total revenue with its total expenses. It needs to be

mentioned that the main purpose of the break-even analysis is the calculation of the amount of

sales that makes the revenues equal to expenses; and the amount of excess revenue is considered

as profit after meeting both the fixed and variable costs (Morano & Tajani, 2013). The process to

calculate the break-even point is to divide the total fixed costs of production by the price per unit

less the variable cost.

It can be seen from the above table that the break-even point in unit for Radisson Blu is

83 rooms and the break-even point in $ is $25,021. It implies that in order to cover all the fixed

as well as variable expenses, it is needed for the management of Radisson Blu to do booking of

83 rooms. In other words, the hotel needs to earn revenue of $25,021 in order to cover all the

fixed as well as variable expenses (Nagle & Müller, 2017).

Target Profit Implementation

Option 1

Particulars Amount

Contribution Margin per room $291

Total Fixed Expenses $24,110

Estimated Profit $50,000

Estimated Room Booking 255

Option 2

Particulars Amount

Contribution Margin per room $291

Total Fixed Expenses $24,110

Estimated Profit $30,000

Estimated Room Booking 186

5COST AND PERFORMANCE MANAGEMENT

The presence of different kinds of cost drivers can be seen in the earlier discussion. It can

be observed from the above discussion that there are some specific kinds of cost drivers are

related to the fixed as well as the variable costs and it is needed for the cost accountants to take

into account all of these aspects at the time to make the costing related decisions (Christ &

Burritt, 2015). It can be seen in the provide scenario that there are some fixed cost for the hotel

that are constant irrespective of the numbers of guests and employees; such as the expenses for

breakfasts, expenses for the charges of internet and others. All these aspects are needed to take

into consideration at the time to make decision related to the selection of Option A or Option B.

At the same time, the cost accountants are needed to put their attention towards the variable cost

of the hotel. It needs to be mentioned that the variable costs increase or decrease as per the

increase or decrease in the inputs (Rieckhof, Bergmann & Guenther, 2015). This is an important

factor as this factor that can affect the decision related to the selection of Option A and Option B.

As per the provide situation, selection of Option A will lead to the profit of $50,000 and

the selection of Option B will lead to the profit of $30,000. However, it can be seen from the

above table that in Option A, the management of Radisson Blu will have to make the booking of

255 rooms for earning the profit of $50,000 (Laitinen, 2014). On the contrary, the above table

also shows that under the Option B, the management of Radisson Blu will have to do the

booking of 186 rooms through the agency for gaining a profit of $30,000. Under Option B, the

management of Radisson Blu has the option to make the booking of other 114 rooms (300 – 186)

without the travel agents to earn more revenues after covering the break event point. On the other

hand, under Option A, the management of the hotel will not get the opportunity to generate

revenue from the booking without travel agent as they will be left with only 45 rooms (300 –

255) (Klychova, Safiullin & Zakirova, 2014).

Conclusion and Recommendation

The above discussion indicates towards the fact that there are three types of cost drivers

for the companies and the managements of the business organizations are needed to consider

these drivers at the time to make the costing related decisions. Some of the major cost drivers of

the business of Radisson Blu hotel are number of units, number of employees, number of guests

and others.

Based on the above discussion, it can be said that the management of Radisson Blu is

needed to consider the selection of Option B for their peak season as it will provide them with

the opportunity to generate more revenue. The main reason is that they will be able in providing

more hotels for booking without the help of travel agent.

The presence of different kinds of cost drivers can be seen in the earlier discussion. It can

be observed from the above discussion that there are some specific kinds of cost drivers are

related to the fixed as well as the variable costs and it is needed for the cost accountants to take

into account all of these aspects at the time to make the costing related decisions (Christ &

Burritt, 2015). It can be seen in the provide scenario that there are some fixed cost for the hotel

that are constant irrespective of the numbers of guests and employees; such as the expenses for

breakfasts, expenses for the charges of internet and others. All these aspects are needed to take

into consideration at the time to make decision related to the selection of Option A or Option B.

At the same time, the cost accountants are needed to put their attention towards the variable cost

of the hotel. It needs to be mentioned that the variable costs increase or decrease as per the

increase or decrease in the inputs (Rieckhof, Bergmann & Guenther, 2015). This is an important

factor as this factor that can affect the decision related to the selection of Option A and Option B.

As per the provide situation, selection of Option A will lead to the profit of $50,000 and

the selection of Option B will lead to the profit of $30,000. However, it can be seen from the

above table that in Option A, the management of Radisson Blu will have to make the booking of

255 rooms for earning the profit of $50,000 (Laitinen, 2014). On the contrary, the above table

also shows that under the Option B, the management of Radisson Blu will have to do the

booking of 186 rooms through the agency for gaining a profit of $30,000. Under Option B, the

management of Radisson Blu has the option to make the booking of other 114 rooms (300 – 186)

without the travel agents to earn more revenues after covering the break event point. On the other

hand, under Option A, the management of the hotel will not get the opportunity to generate

revenue from the booking without travel agent as they will be left with only 45 rooms (300 –

255) (Klychova, Safiullin & Zakirova, 2014).

Conclusion and Recommendation

The above discussion indicates towards the fact that there are three types of cost drivers

for the companies and the managements of the business organizations are needed to consider

these drivers at the time to make the costing related decisions. Some of the major cost drivers of

the business of Radisson Blu hotel are number of units, number of employees, number of guests

and others.

Based on the above discussion, it can be said that the management of Radisson Blu is

needed to consider the selection of Option B for their peak season as it will provide them with

the opportunity to generate more revenue. The main reason is that they will be able in providing

more hotels for booking without the help of travel agent.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6COST AND PERFORMANCE MANAGEMENT

References

Appelbaum, D., Kogan, A., Vasarhelyi, M., & Yan, Z. (2017). Impact of business analytics and

enterprise systems on managerial accounting. International Journal of Accounting

Information Systems, 25, 29-44.

Christ, K. L., & Burritt, R. L. (2015). Material flow cost accounting: a review and agenda for

future research. Journal of Cleaner Production, 108, 1378-1389.

Cooper, R. (2017). Supply chain development for the lean enterprise: interorganizational cost

management. Routledge.

DRURY, C. M. (2013). Management and cost accounting. Springer.

Hilton, R. W., & Platt, D. E. (2013). Managerial accounting: creating value in a dynamic

business environment. McGraw-Hill Education.

Klychova, G. S., Safiullin, N. Z., & Zakirova, A. R. (2014). Organization of cost accounting of

fur farming in controlling concept. Mediterranean Journal of Social Sciences, 5(18), 219.

Laitinen, E. K. (2014). Influence of cost accounting change on performance of manufacturing

firms. Advances in Accounting, 30(1), 230-240.

Matherly, M., & Burney, L. L. (2013). Active learning activities to revitalize managerial

accounting principles. Issues in Accounting Education, 28(3), 653-680.

Morano, P., & Tajani, F. (2013). Break Even Analysis for the financial verification of urban

regeneration projects. In Applied Mechanics and Materials (Vol. 438, pp. 1830-1835).

Trans Tech Publications.

Morano, P., & Tajani, F. (2017). The break-even analysis applied to urban renewal investments:

a model to evaluate the share of social housing financially sustainable for private

investors. Habitat International, 59, 10-20.

Nagle, T. T., & Müller, G. (2017). The strategy and tactics of pricing: A guide to growing more

profitably. Routledge.

Noreen, E. W., Brewer, P. C., & Garrison, R. H. (2014). Managerial accounting for managers.

New York: McGraw-Hill/Irwin.

Park, K., & Jang, S. (2014). Hospitality finance and managerial accounting research: Suggesting

an interdisciplinary research agenda. International Journal of Contemporary Hospitality

Management, 26(5), 751-777.

References

Appelbaum, D., Kogan, A., Vasarhelyi, M., & Yan, Z. (2017). Impact of business analytics and

enterprise systems on managerial accounting. International Journal of Accounting

Information Systems, 25, 29-44.

Christ, K. L., & Burritt, R. L. (2015). Material flow cost accounting: a review and agenda for

future research. Journal of Cleaner Production, 108, 1378-1389.

Cooper, R. (2017). Supply chain development for the lean enterprise: interorganizational cost

management. Routledge.

DRURY, C. M. (2013). Management and cost accounting. Springer.

Hilton, R. W., & Platt, D. E. (2013). Managerial accounting: creating value in a dynamic

business environment. McGraw-Hill Education.

Klychova, G. S., Safiullin, N. Z., & Zakirova, A. R. (2014). Organization of cost accounting of

fur farming in controlling concept. Mediterranean Journal of Social Sciences, 5(18), 219.

Laitinen, E. K. (2014). Influence of cost accounting change on performance of manufacturing

firms. Advances in Accounting, 30(1), 230-240.

Matherly, M., & Burney, L. L. (2013). Active learning activities to revitalize managerial

accounting principles. Issues in Accounting Education, 28(3), 653-680.

Morano, P., & Tajani, F. (2013). Break Even Analysis for the financial verification of urban

regeneration projects. In Applied Mechanics and Materials (Vol. 438, pp. 1830-1835).

Trans Tech Publications.

Morano, P., & Tajani, F. (2017). The break-even analysis applied to urban renewal investments:

a model to evaluate the share of social housing financially sustainable for private

investors. Habitat International, 59, 10-20.

Nagle, T. T., & Müller, G. (2017). The strategy and tactics of pricing: A guide to growing more

profitably. Routledge.

Noreen, E. W., Brewer, P. C., & Garrison, R. H. (2014). Managerial accounting for managers.

New York: McGraw-Hill/Irwin.

Park, K., & Jang, S. (2014). Hospitality finance and managerial accounting research: Suggesting

an interdisciplinary research agenda. International Journal of Contemporary Hospitality

Management, 26(5), 751-777.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7COST AND PERFORMANCE MANAGEMENT

Rieckhof, R., Bergmann, A., & Guenther, E. (2015). Interrelating material flow cost accounting

with management control systems to introduce resource efficiency into strategy. Journal

of Cleaner Production, 108, 1262-1278.

Rieckhof, R., Bergmann, A., & Guenther, E. (2015). Interrelating material flow cost accounting

with management control systems to introduce resource efficiency into strategy. Journal

of Cleaner Production, 108, 1262-1278.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.