Financial Planning, Sources, and Project Evaluation: Radisson Plc

VerifiedAdded on 2023/04/17

|20

|4470

|250

Report

AI Summary

This report provides a comprehensive analysis of financial planning for Radisson Plc, covering various aspects such as procurement, utilization, and management of funds. It explores traditional and non-traditional financial sources, including retained profits, ownership capital, bank loans, hire purchase, and factoring, while also highlighting the legal, financial, dilution, and bankruptcy implications of each. The report identifies loans as a suitable option for Radisson Plc due to tax benefits and control retention. It further discusses the benefits of financial planning, information needs of stakeholders, and the differences in financial reporting requirements for various organizational structures. The document also delves into the cost of equity versus debt financing, emphasizing the advantages of loan financing, and concludes with an overview of project evaluation techniques for making informed investment decisions.

MFRD

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................................3

TASK 1..........................................................................................................................................................3

A..............................................................................................................................................................3

B..............................................................................................................................................................6

TASK 2..........................................................................................................................................................7

A..............................................................................................................................................................7

B..............................................................................................................................................................7

C..............................................................................................................................................................9

TASK 3........................................................................................................................................................10

A............................................................................................................................................................10

B............................................................................................................................................................12

C............................................................................................................................................................12

TASK 4........................................................................................................................................................14

A............................................................................................................................................................14

B............................................................................................................................................................16

CONCLUSION.............................................................................................................................................17

REFERENCES..............................................................................................................................................19

INTRODUCTION...........................................................................................................................................3

TASK 1..........................................................................................................................................................3

A..............................................................................................................................................................3

B..............................................................................................................................................................6

TASK 2..........................................................................................................................................................7

A..............................................................................................................................................................7

B..............................................................................................................................................................7

C..............................................................................................................................................................9

TASK 3........................................................................................................................................................10

A............................................................................................................................................................10

B............................................................................................................................................................12

C............................................................................................................................................................12

TASK 4........................................................................................................................................................14

A............................................................................................................................................................14

B............................................................................................................................................................16

CONCLUSION.............................................................................................................................................17

REFERENCES..............................................................................................................................................19

INTRODUCTION

Financial planning refers to the process of procurement, utilization and proper

management of money to control overspending, meet capital as well as daily business need,

maintain cash surplus and so on. Every company involves in such activities may be either to start

a new business or expand existing business in new markets. This assignment will guide an

individual about various ways through which they can gather money to meet out their financial

commitments. Moreover, the report will also highlight the key differences among all the sources

on the basis of legal, financial, dilution, and bankruptcy implications to identify the best source

of money. Along with this, report will guide about various managerial techniques that how

money can be managed properly through financial planning and cash budgeting. Apart from this,

sometimes, businesses require huge amount of funds to pay capital expenditures like to buy

property, machinery and equipments. It can drive both the risks and return to the entity,

henceforth, companies have to identify the project that will yield better return. In order to fulfill

that objective, project evaluation techniques will be considered best as it examine both the risk

inherited and possibility of return so as to determine the most profitable and beneficial project.

At the closure of the report, it will analyze differences in the financial reporting requirement of

different organizations i.e. sole trader, partnership and company.

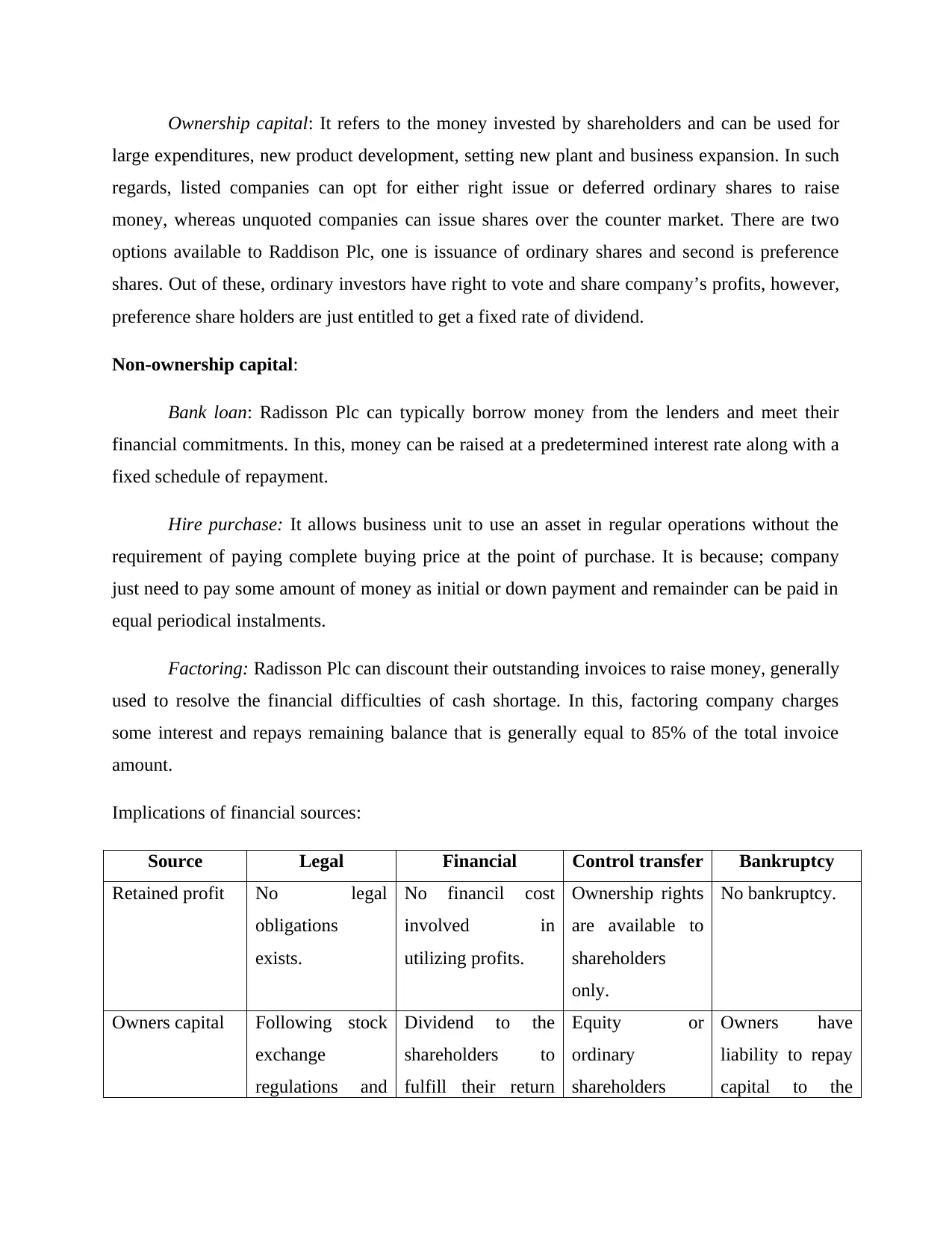

TASK 1

A

In order to finance long-term contract, Radisson Plc can choose any of the below

mentioned sources or combination of one or more financial source depending upon the time

period and amount of money. It can be categorized into three parts, that are explained hereunder:

Traditional financial sources:

Retained profits: Sum of profits that not had been reinvested or distributed among

shareholders by Radisson Plc is called retained or residual yield (Broadbent and Cullen 2012). It

can be used by the company to meet out their capital need for the contract without any legal

obligation and financial cost.

Financial planning refers to the process of procurement, utilization and proper

management of money to control overspending, meet capital as well as daily business need,

maintain cash surplus and so on. Every company involves in such activities may be either to start

a new business or expand existing business in new markets. This assignment will guide an

individual about various ways through which they can gather money to meet out their financial

commitments. Moreover, the report will also highlight the key differences among all the sources

on the basis of legal, financial, dilution, and bankruptcy implications to identify the best source

of money. Along with this, report will guide about various managerial techniques that how

money can be managed properly through financial planning and cash budgeting. Apart from this,

sometimes, businesses require huge amount of funds to pay capital expenditures like to buy

property, machinery and equipments. It can drive both the risks and return to the entity,

henceforth, companies have to identify the project that will yield better return. In order to fulfill

that objective, project evaluation techniques will be considered best as it examine both the risk

inherited and possibility of return so as to determine the most profitable and beneficial project.

At the closure of the report, it will analyze differences in the financial reporting requirement of

different organizations i.e. sole trader, partnership and company.

TASK 1

A

In order to finance long-term contract, Radisson Plc can choose any of the below

mentioned sources or combination of one or more financial source depending upon the time

period and amount of money. It can be categorized into three parts, that are explained hereunder:

Traditional financial sources:

Retained profits: Sum of profits that not had been reinvested or distributed among

shareholders by Radisson Plc is called retained or residual yield (Broadbent and Cullen 2012). It

can be used by the company to meet out their capital need for the contract without any legal

obligation and financial cost.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Ownership capital: It refers to the money invested by shareholders and can be used for

large expenditures, new product development, setting new plant and business expansion. In such

regards, listed companies can opt for either right issue or deferred ordinary shares to raise

money, whereas unquoted companies can issue shares over the counter market. There are two

options available to Raddison Plc, one is issuance of ordinary shares and second is preference

shares. Out of these, ordinary investors have right to vote and share company’s profits, however,

preference share holders are just entitled to get a fixed rate of dividend.

Non-ownership capital:

Bank loan: Radisson Plc can typically borrow money from the lenders and meet their

financial commitments. In this, money can be raised at a predetermined interest rate along with a

fixed schedule of repayment.

Hire purchase: It allows business unit to use an asset in regular operations without the

requirement of paying complete buying price at the point of purchase. It is because; company

just need to pay some amount of money as initial or down payment and remainder can be paid in

equal periodical instalments.

Factoring: Radisson Plc can discount their outstanding invoices to raise money, generally

used to resolve the financial difficulties of cash shortage. In this, factoring company charges

some interest and repays remaining balance that is generally equal to 85% of the total invoice

amount.

Implications of financial sources:

Source Legal Financial Control transfer Bankruptcy

Retained profit No legal

obligations

exists.

No financil cost

involved in

utilizing profits.

Ownership rights

are available to

shareholders

only.

No bankruptcy.

Owners capital Following stock

exchange

regulations and

Dividend to the

shareholders to

fulfill their return

Equity or

ordinary

shareholders

Owners have

liability to repay

capital to the

large expenditures, new product development, setting new plant and business expansion. In such

regards, listed companies can opt for either right issue or deferred ordinary shares to raise

money, whereas unquoted companies can issue shares over the counter market. There are two

options available to Raddison Plc, one is issuance of ordinary shares and second is preference

shares. Out of these, ordinary investors have right to vote and share company’s profits, however,

preference share holders are just entitled to get a fixed rate of dividend.

Non-ownership capital:

Bank loan: Radisson Plc can typically borrow money from the lenders and meet their

financial commitments. In this, money can be raised at a predetermined interest rate along with a

fixed schedule of repayment.

Hire purchase: It allows business unit to use an asset in regular operations without the

requirement of paying complete buying price at the point of purchase. It is because; company

just need to pay some amount of money as initial or down payment and remainder can be paid in

equal periodical instalments.

Factoring: Radisson Plc can discount their outstanding invoices to raise money, generally

used to resolve the financial difficulties of cash shortage. In this, factoring company charges

some interest and repays remaining balance that is generally equal to 85% of the total invoice

amount.

Implications of financial sources:

Source Legal Financial Control transfer Bankruptcy

Retained profit No legal

obligations

exists.

No financil cost

involved in

utilizing profits.

Ownership rights

are available to

shareholders

only.

No bankruptcy.

Owners capital Following stock

exchange

regulations and

Dividend to the

shareholders to

fulfill their return

Equity or

ordinary

shareholders

Owners have

liability to repay

capital to the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

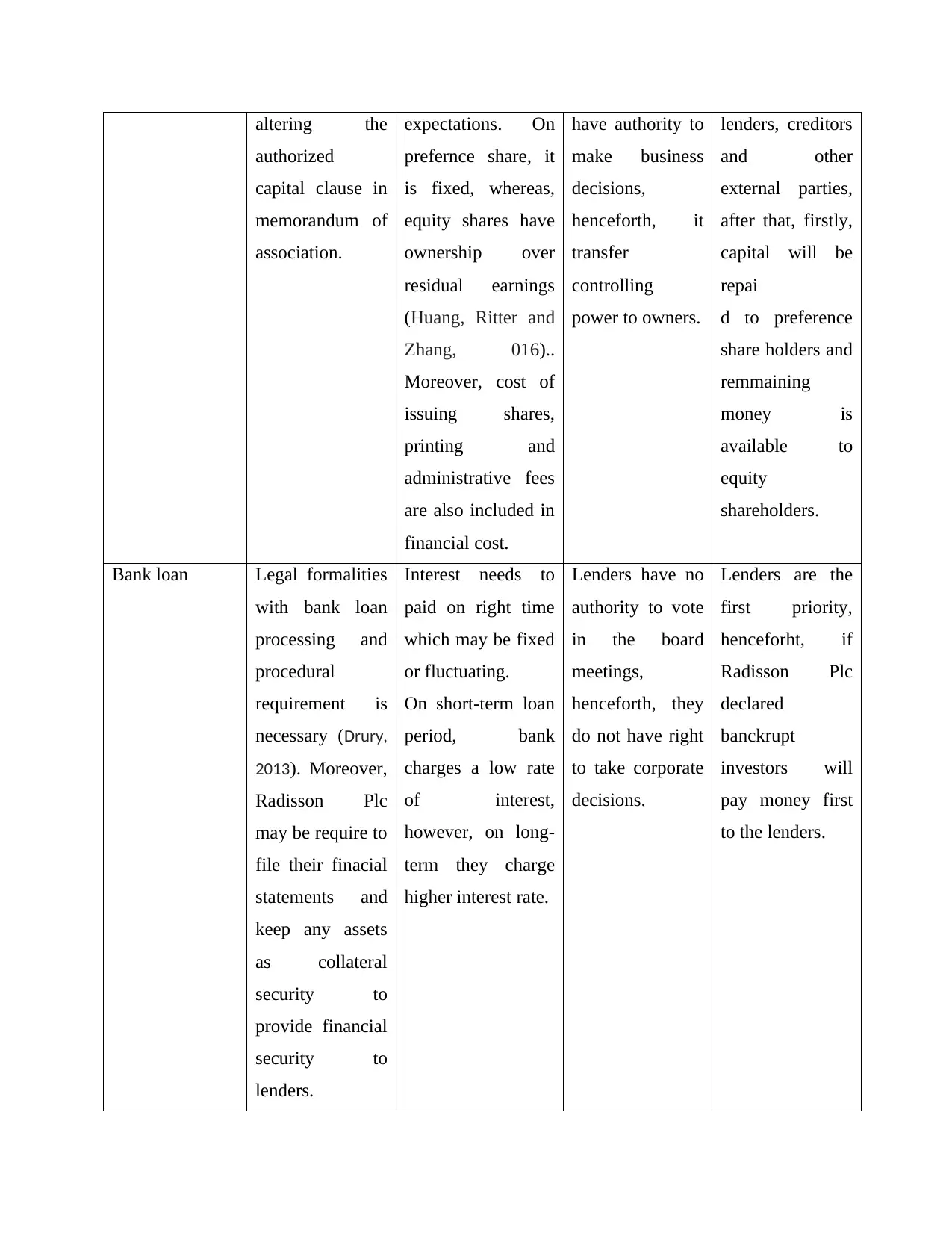

altering the

authorized

capital clause in

memorandum of

association.

expectations. On

prefernce share, it

is fixed, whereas,

equity shares have

ownership over

residual earnings

(Huang, Ritter and

Zhang, 016)..

Moreover, cost of

issuing shares,

printing and

administrative fees

are also included in

financial cost.

have authority to

make business

decisions,

henceforth, it

transfer

controlling

power to owners.

lenders, creditors

and other

external parties,

after that, firstly,

capital will be

repai

d to preference

share holders and

remmaining

money is

available to

equity

shareholders.

Bank loan Legal formalities

with bank loan

processing and

procedural

requirement is

necessary (Drury,

2013). Moreover,

Radisson Plc

may be require to

file their finacial

statements and

keep any assets

as collateral

security to

provide financial

security to

lenders.

Interest needs to

paid on right time

which may be fixed

or fluctuating.

On short-term loan

period, bank

charges a low rate

of interest,

however, on long-

term they charge

higher interest rate.

Lenders have no

authority to vote

in the board

meetings,

henceforth, they

do not have right

to take corporate

decisions.

Lenders are the

first priority,

henceforht, if

Radisson Plc

declared

banckrupt

investors will

pay money first

to the lenders.

authorized

capital clause in

memorandum of

association.

expectations. On

prefernce share, it

is fixed, whereas,

equity shares have

ownership over

residual earnings

(Huang, Ritter and

Zhang, 016)..

Moreover, cost of

issuing shares,

printing and

administrative fees

are also included in

financial cost.

have authority to

make business

decisions,

henceforth, it

transfer

controlling

power to owners.

lenders, creditors

and other

external parties,

after that, firstly,

capital will be

repai

d to preference

share holders and

remmaining

money is

available to

equity

shareholders.

Bank loan Legal formalities

with bank loan

processing and

procedural

requirement is

necessary (Drury,

2013). Moreover,

Radisson Plc

may be require to

file their finacial

statements and

keep any assets

as collateral

security to

provide financial

security to

lenders.

Interest needs to

paid on right time

which may be fixed

or fluctuating.

On short-term loan

period, bank

charges a low rate

of interest,

however, on long-

term they charge

higher interest rate.

Lenders have no

authority to vote

in the board

meetings,

henceforth, they

do not have right

to take corporate

decisions.

Lenders are the

first priority,

henceforht, if

Radisson Plc

declared

banckrupt

investors will

pay money first

to the lenders.

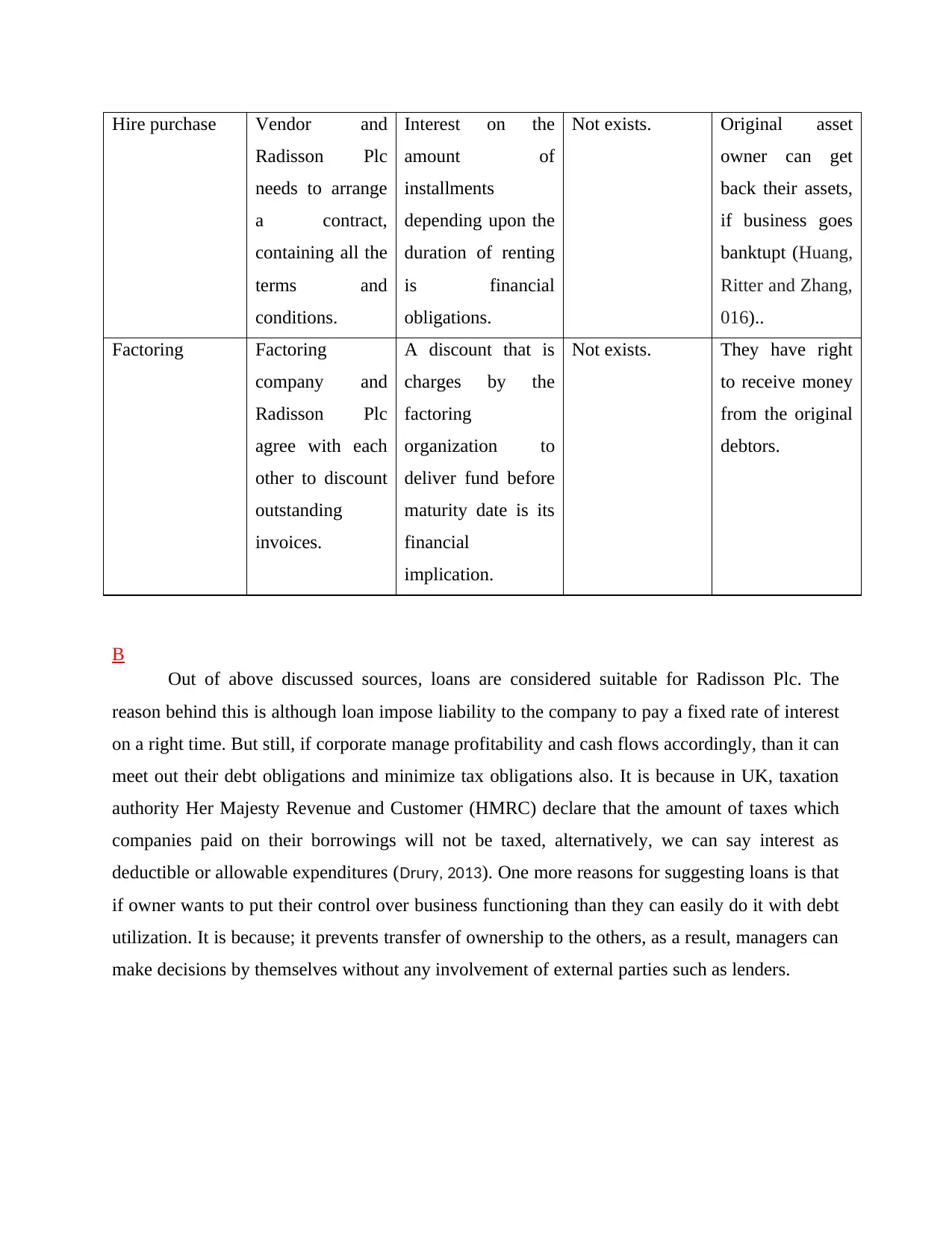

Hire purchase Vendor and

Radisson Plc

needs to arrange

a contract,

containing all the

terms and

conditions.

Interest on the

amount of

installments

depending upon the

duration of renting

is financial

obligations.

Not exists. Original asset

owner can get

back their assets,

if business goes

banktupt (Huang,

Ritter and Zhang,

016)..

Factoring Factoring

company and

Radisson Plc

agree with each

other to discount

outstanding

invoices.

A discount that is

charges by the

factoring

organization to

deliver fund before

maturity date is its

financial

implication.

Not exists. They have right

to receive money

from the original

debtors.

B

Out of above discussed sources, loans are considered suitable for Radisson Plc. The

reason behind this is although loan impose liability to the company to pay a fixed rate of interest

on a right time. But still, if corporate manage profitability and cash flows accordingly, than it can

meet out their debt obligations and minimize tax obligations also. It is because in UK, taxation

authority Her Majesty Revenue and Customer (HMRC) declare that the amount of taxes which

companies paid on their borrowings will not be taxed, alternatively, we can say interest as

deductible or allowable expenditures (Drury, 2013). One more reasons for suggesting loans is that

if owner wants to put their control over business functioning than they can easily do it with debt

utilization. It is because; it prevents transfer of ownership to the others, as a result, managers can

make decisions by themselves without any involvement of external parties such as lenders.

Radisson Plc

needs to arrange

a contract,

containing all the

terms and

conditions.

Interest on the

amount of

installments

depending upon the

duration of renting

is financial

obligations.

Not exists. Original asset

owner can get

back their assets,

if business goes

banktupt (Huang,

Ritter and Zhang,

016)..

Factoring Factoring

company and

Radisson Plc

agree with each

other to discount

outstanding

invoices.

A discount that is

charges by the

factoring

organization to

deliver fund before

maturity date is its

financial

implication.

Not exists. They have right

to receive money

from the original

debtors.

B

Out of above discussed sources, loans are considered suitable for Radisson Plc. The

reason behind this is although loan impose liability to the company to pay a fixed rate of interest

on a right time. But still, if corporate manage profitability and cash flows accordingly, than it can

meet out their debt obligations and minimize tax obligations also. It is because in UK, taxation

authority Her Majesty Revenue and Customer (HMRC) declare that the amount of taxes which

companies paid on their borrowings will not be taxed, alternatively, we can say interest as

deductible or allowable expenditures (Drury, 2013). One more reasons for suggesting loans is that

if owner wants to put their control over business functioning than they can easily do it with debt

utilization. It is because; it prevents transfer of ownership to the others, as a result, managers can

make decisions by themselves without any involvement of external parties such as lenders.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

TASK 2

A

Cost of equity versus debt financing: As said earlier, that on equity share capital,

Radisson Plc is not liable to pay predetermined rate of return (Huang, Ritter and Zhang, 2016).

Moreover, the cost of issuing and printing shares, listing fees in stock exchange and

administrative fees are also included in cost. However, on the other side, on the borrowed

money, Radisson Plc’s financial executives have to manage cash flows so as to pay installments

on due date and repay borrowed money on maturity date. It also has to file its annual accounts to

represent information to the lenders about their financial status, profitability, solvency, debt

burden capacity, interest payment ability and credit worthiness (Sources of funds, 2014). Although,

rate of dividend on equity is not fixed, while on debt capital, it is fixed, but still, loans are

considered beneficial because tax benefits are available on loan facilities. Moreover, equity

capital transfer controlling power to owners whereas it is not so with the borrowed money. All

the evaluation clealry depicts that loan financing are considered cheaper source of finance as

compared to equity, therefore, Radisson Plc must chose this source.

Interest is the cost of debt as Radisson Plc will be requires to pay dividend to the debt

holders as per their loan repayment schedule. However, it provides tax benefits to the fim as

HMRC consider payment of loan as an allowed expense for tax determination.

On the other side, cost of equity is dividend about which company does not have any

legal compulsion, henceforth dividend payment decisions can be taken on the basis of

availability of profitability.

B

Financial planning, also called monetary planning refers to the process of meeting

financial goals through the proper and effective utilization of money. It consists of various

functions such as setting targets, analyzing current financial status, estimating future capital

requirement and coming with a suitable strategic plan or approach to reach goals (De Wit, 2016).

The benefits of the financial planning are described here underneath:

Prior and advance planning provides direction to the Radisson Plc’s managers about the

way how they can utilize resource optimally and manage cost.

A

Cost of equity versus debt financing: As said earlier, that on equity share capital,

Radisson Plc is not liable to pay predetermined rate of return (Huang, Ritter and Zhang, 2016).

Moreover, the cost of issuing and printing shares, listing fees in stock exchange and

administrative fees are also included in cost. However, on the other side, on the borrowed

money, Radisson Plc’s financial executives have to manage cash flows so as to pay installments

on due date and repay borrowed money on maturity date. It also has to file its annual accounts to

represent information to the lenders about their financial status, profitability, solvency, debt

burden capacity, interest payment ability and credit worthiness (Sources of funds, 2014). Although,

rate of dividend on equity is not fixed, while on debt capital, it is fixed, but still, loans are

considered beneficial because tax benefits are available on loan facilities. Moreover, equity

capital transfer controlling power to owners whereas it is not so with the borrowed money. All

the evaluation clealry depicts that loan financing are considered cheaper source of finance as

compared to equity, therefore, Radisson Plc must chose this source.

Interest is the cost of debt as Radisson Plc will be requires to pay dividend to the debt

holders as per their loan repayment schedule. However, it provides tax benefits to the fim as

HMRC consider payment of loan as an allowed expense for tax determination.

On the other side, cost of equity is dividend about which company does not have any

legal compulsion, henceforth dividend payment decisions can be taken on the basis of

availability of profitability.

B

Financial planning, also called monetary planning refers to the process of meeting

financial goals through the proper and effective utilization of money. It consists of various

functions such as setting targets, analyzing current financial status, estimating future capital

requirement and coming with a suitable strategic plan or approach to reach goals (De Wit, 2016).

The benefits of the financial planning are described here underneath:

Prior and advance planning provides direction to the Radisson Plc’s managers about the

way how they can utilize resource optimally and manage cost.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

It also works as an insurance against financial risk which enables Radisson Plc to take

necessary steps to overcome financial risk and adverse shocks like high cost of debt,

sudden increase in supplier prices, and downward movement in demand and so on

(Broadbent and Cullen, 2012).

With the help of the best financial strategy and plan, management of the firm will be able

to manage effectively their revenues and allocate it in regular functioning, so as to make

sure surplus or positive cash balance.

It enables Radisson Plc’s executives and directors to formulate various growth, expansion

and development plans and strategic move to reach targets (Huang, Ritter and Zhang,

2016).

It helps corporate entity to gather sufficient or appropriate quantity of capital sources

from the most suitable financial source at an affordable cost of capital.

Information need

Every person or organization that have some interest or concern in Radisson Plc and

affected by its policies, actions and objectives are called stakeholders. Some of the key

stakeholders along with their information requirement are enumerated underneath:

System developers: It consists of analyst, system designers, programmers, quality

assurance team, trainers and Radisson Plc’s project managers which have high level of stake in

specification of final product as per the customer requirement. System development team highly

focuses to develop software as per the actual requirement or preferences of people.

Users/Consumers: People or businesses that finally operate Radisson Plc’s developed or

designed software are called users. They require information about product features, frequency

of system usage, and experience of system usage and so on. They will only use particular product

or service if it fulfill their expectations.

Legislators: Professional bodies, trade union, quality assurance auditors, legal

representative, governmental agencies and safety executors are called legislators who produce

guidelines and principles affecting designing, developing and operating process of the system.

They need information to know that whether Radisson Plc has complied with acts or not like

Data Protection Act, defense standard, quality manual, auditors by an external auditor and so on

necessary steps to overcome financial risk and adverse shocks like high cost of debt,

sudden increase in supplier prices, and downward movement in demand and so on

(Broadbent and Cullen, 2012).

With the help of the best financial strategy and plan, management of the firm will be able

to manage effectively their revenues and allocate it in regular functioning, so as to make

sure surplus or positive cash balance.

It enables Radisson Plc’s executives and directors to formulate various growth, expansion

and development plans and strategic move to reach targets (Huang, Ritter and Zhang,

2016).

It helps corporate entity to gather sufficient or appropriate quantity of capital sources

from the most suitable financial source at an affordable cost of capital.

Information need

Every person or organization that have some interest or concern in Radisson Plc and

affected by its policies, actions and objectives are called stakeholders. Some of the key

stakeholders along with their information requirement are enumerated underneath:

System developers: It consists of analyst, system designers, programmers, quality

assurance team, trainers and Radisson Plc’s project managers which have high level of stake in

specification of final product as per the customer requirement. System development team highly

focuses to develop software as per the actual requirement or preferences of people.

Users/Consumers: People or businesses that finally operate Radisson Plc’s developed or

designed software are called users. They require information about product features, frequency

of system usage, and experience of system usage and so on. They will only use particular product

or service if it fulfill their expectations.

Legislators: Professional bodies, trade union, quality assurance auditors, legal

representative, governmental agencies and safety executors are called legislators who produce

guidelines and principles affecting designing, developing and operating process of the system.

They need information to know that whether Radisson Plc has complied with acts or not like

Data Protection Act, defense standard, quality manual, auditors by an external auditor and so on

(Speybroeck and et.al., 2015). Moreover, taxation agencies like HMRC gather information about

corporate taxes so as to make it sure that Radisson Plc paid correct amount of taxes on time or

not. If company does not follow any of the law and principle than it gives right to the authority to

charge law suit.

Decision-makers: It encompasses development team managers, financial controller and

other executives. They have power to alter decisions regards to system or software development,

operational processes and set standards.

Shareholders: They just want to make sure that Radisson Plc will pay good return to their

investors as a financial return for the money being invested. They examine risk associated with

their fund, potential yield, business profitability, dividend policy and stock performance to make

solid investment decisions.

Lenders: They lend money after satisfying themselves that Radisson Plc’s executives and

directors will pay timely their fixed loan liability as per the repayment schedule. Moreover, they

assess capital structure to examine financial risk, business capacity to bear more debt burden and

interest payment ability, profitability, liquidity and solvency position also (Coleman, Cotei and

Farhat, 2016).

Employees: Employees are interested in the business to get better salary for respective

efforts, good working conditions, training, welfare activities and various growth opportunity for

their career advancement.

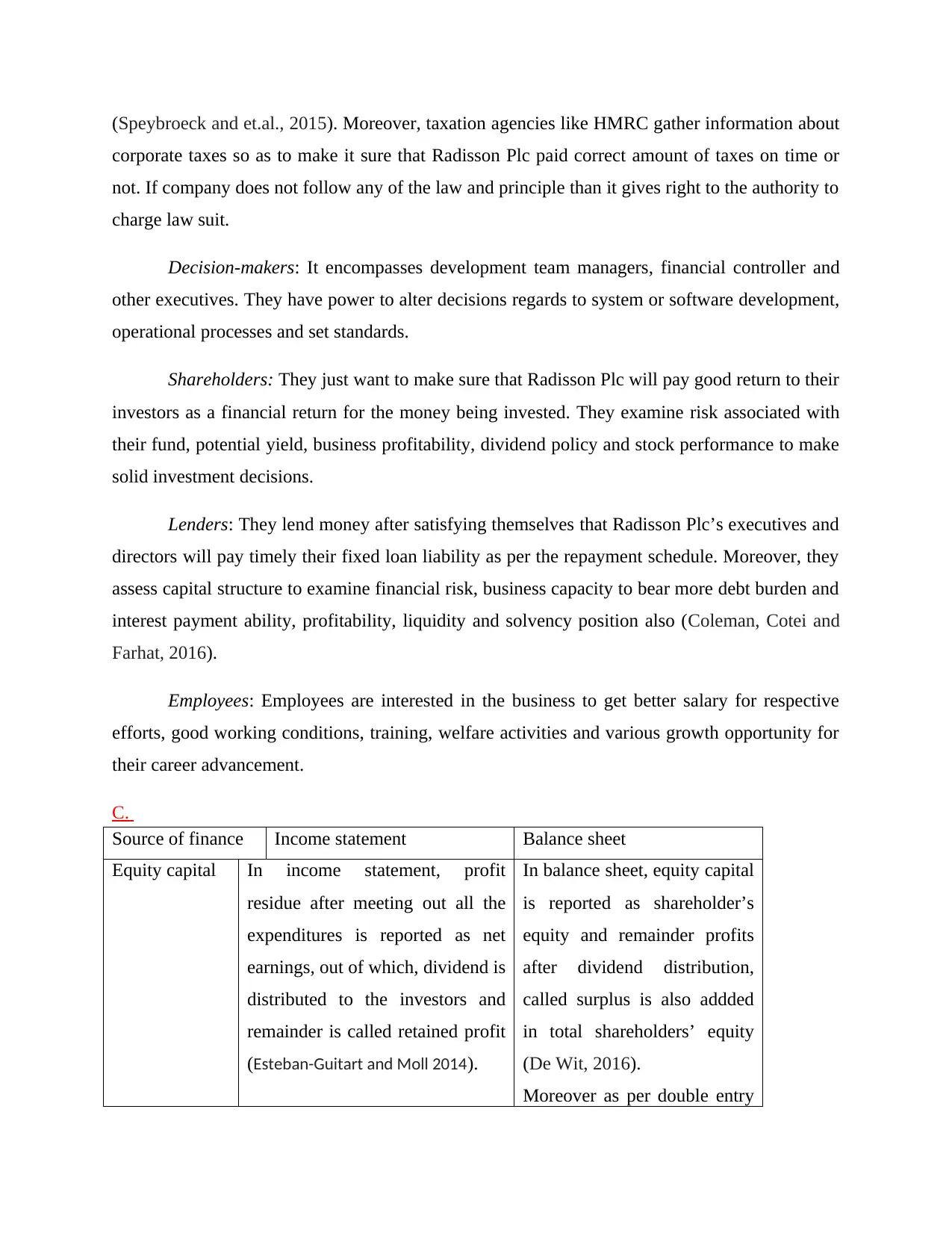

C.

Source of finance Income statement Balance sheet

Equity capital In income statement, profit

residue after meeting out all the

expenditures is reported as net

earnings, out of which, dividend is

distributed to the investors and

remainder is called retained profit

(Esteban-Guitart and Moll 2014).

In balance sheet, equity capital

is reported as shareholder’s

equity and remainder profits

after dividend distribution,

called surplus is also addded

in total shareholders’ equity

(De Wit, 2016).

Moreover as per double entry

corporate taxes so as to make it sure that Radisson Plc paid correct amount of taxes on time or

not. If company does not follow any of the law and principle than it gives right to the authority to

charge law suit.

Decision-makers: It encompasses development team managers, financial controller and

other executives. They have power to alter decisions regards to system or software development,

operational processes and set standards.

Shareholders: They just want to make sure that Radisson Plc will pay good return to their

investors as a financial return for the money being invested. They examine risk associated with

their fund, potential yield, business profitability, dividend policy and stock performance to make

solid investment decisions.

Lenders: They lend money after satisfying themselves that Radisson Plc’s executives and

directors will pay timely their fixed loan liability as per the repayment schedule. Moreover, they

assess capital structure to examine financial risk, business capacity to bear more debt burden and

interest payment ability, profitability, liquidity and solvency position also (Coleman, Cotei and

Farhat, 2016).

Employees: Employees are interested in the business to get better salary for respective

efforts, good working conditions, training, welfare activities and various growth opportunity for

their career advancement.

C.

Source of finance Income statement Balance sheet

Equity capital In income statement, profit

residue after meeting out all the

expenditures is reported as net

earnings, out of which, dividend is

distributed to the investors and

remainder is called retained profit

(Esteban-Guitart and Moll 2014).

In balance sheet, equity capital

is reported as shareholder’s

equity and remainder profits

after dividend distribution,

called surplus is also addded

in total shareholders’ equity

(De Wit, 2016).

Moreover as per double entry

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

accounting, in the assets side,

it increase total cash balance

of the Radisson Plc.

Debt financing In profit and loss account, debt

interest is shown as financial cost

and minimizes earning after

interest.

In balance sheet, it is shown

under the head long-term

liabilities.

However, in the assets side,

similar to equity financing, it

raises liquidity sources in the

form of more cash.

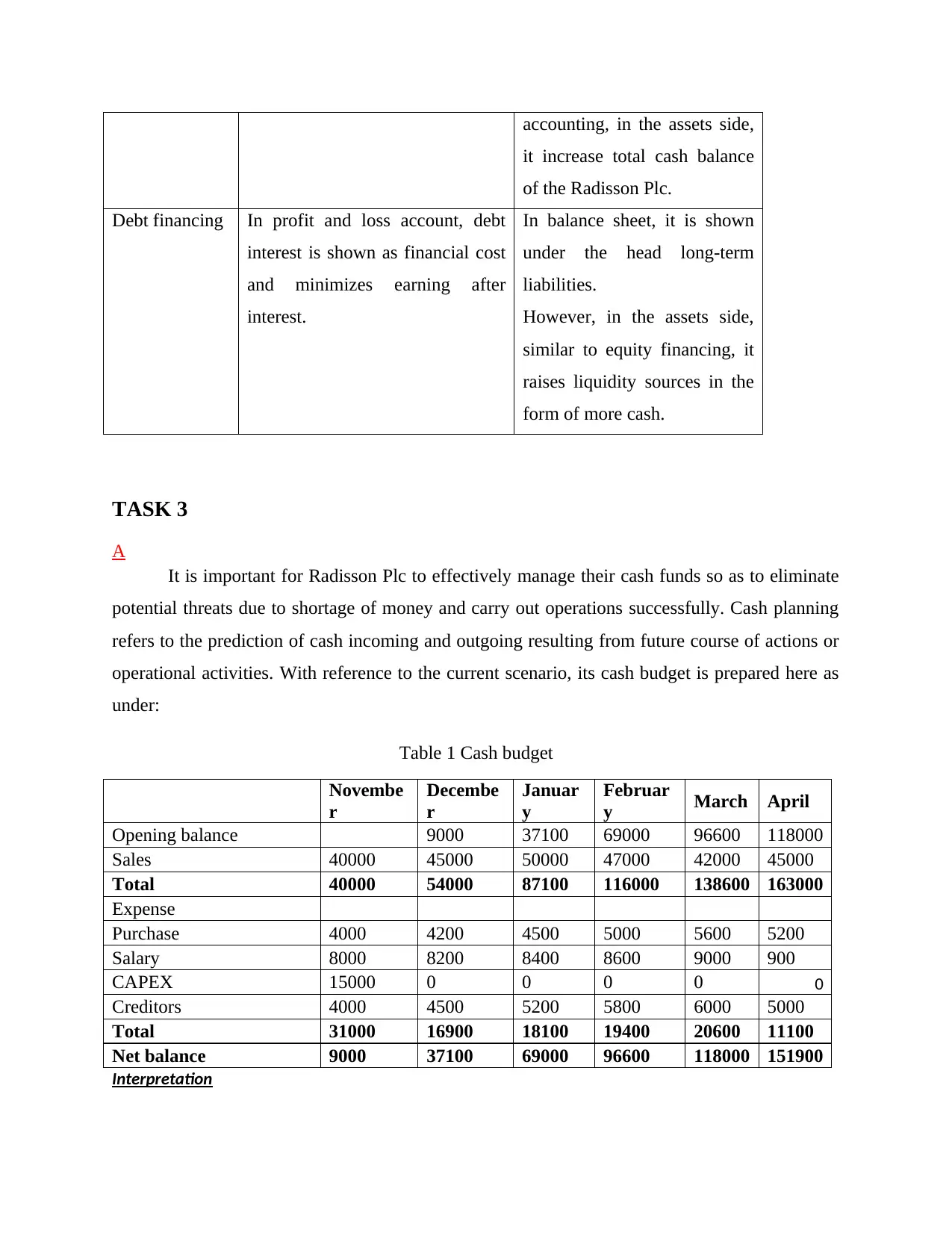

TASK 3

A

It is important for Radisson Plc to effectively manage their cash funds so as to eliminate

potential threats due to shortage of money and carry out operations successfully. Cash planning

refers to the prediction of cash incoming and outgoing resulting from future course of actions or

operational activities. With reference to the current scenario, its cash budget is prepared here as

under:

Table 1 Cash budget

Novembe

r

Decembe

r

Januar

y

Februar

y March April

Opening balance 9000 37100 69000 96600 118000

Sales 40000 45000 50000 47000 42000 45000

Total 40000 54000 87100 116000 138600 163000

Expense

Purchase 4000 4200 4500 5000 5600 5200

Salary 8000 8200 8400 8600 9000 900

CAPEX 15000 0 0 0 0 0

Creditors 4000 4500 5200 5800 6000 5000

Total 31000 16900 18100 19400 20600 11100

Net balance 9000 37100 69000 96600 118000 151900

Interpretation

it increase total cash balance

of the Radisson Plc.

Debt financing In profit and loss account, debt

interest is shown as financial cost

and minimizes earning after

interest.

In balance sheet, it is shown

under the head long-term

liabilities.

However, in the assets side,

similar to equity financing, it

raises liquidity sources in the

form of more cash.

TASK 3

A

It is important for Radisson Plc to effectively manage their cash funds so as to eliminate

potential threats due to shortage of money and carry out operations successfully. Cash planning

refers to the prediction of cash incoming and outgoing resulting from future course of actions or

operational activities. With reference to the current scenario, its cash budget is prepared here as

under:

Table 1 Cash budget

Novembe

r

Decembe

r

Januar

y

Februar

y March April

Opening balance 9000 37100 69000 96600 118000

Sales 40000 45000 50000 47000 42000 45000

Total 40000 54000 87100 116000 138600 163000

Expense

Purchase 4000 4200 4500 5000 5600 5200

Salary 8000 8200 8400 8600 9000 900

CAPEX 15000 0 0 0 0 0

Creditors 4000 4500 5200 5800 6000 5000

Total 31000 16900 18100 19400 20600 11100

Net balance 9000 37100 69000 96600 118000 151900

Interpretation

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

From the cash budget given above it can be seen that cash balance of the firm is

increasing consistently. It can be noted that rate of growth in the value of cash flow is high in the

month of November, December, January and February. However, in other months trend get

changed and growth rate decline sharply (Huang, Ritter and Zhang, 2016). It can be seen from

the budget that sales increase in first three months. Thereafter ti declined sharply and on last

month of the budget it again increase. Interesting fact is the even sales get declined firm

expenses elevate consistently. In last month which is April decline is observed in sales. This

reflects that firm is not tracking changes in the business environment properly. On hope that

business conditions will get improved firm consistently made expenses in the month when sales

is reduced. Firm needs to take its business decisions cautiously.

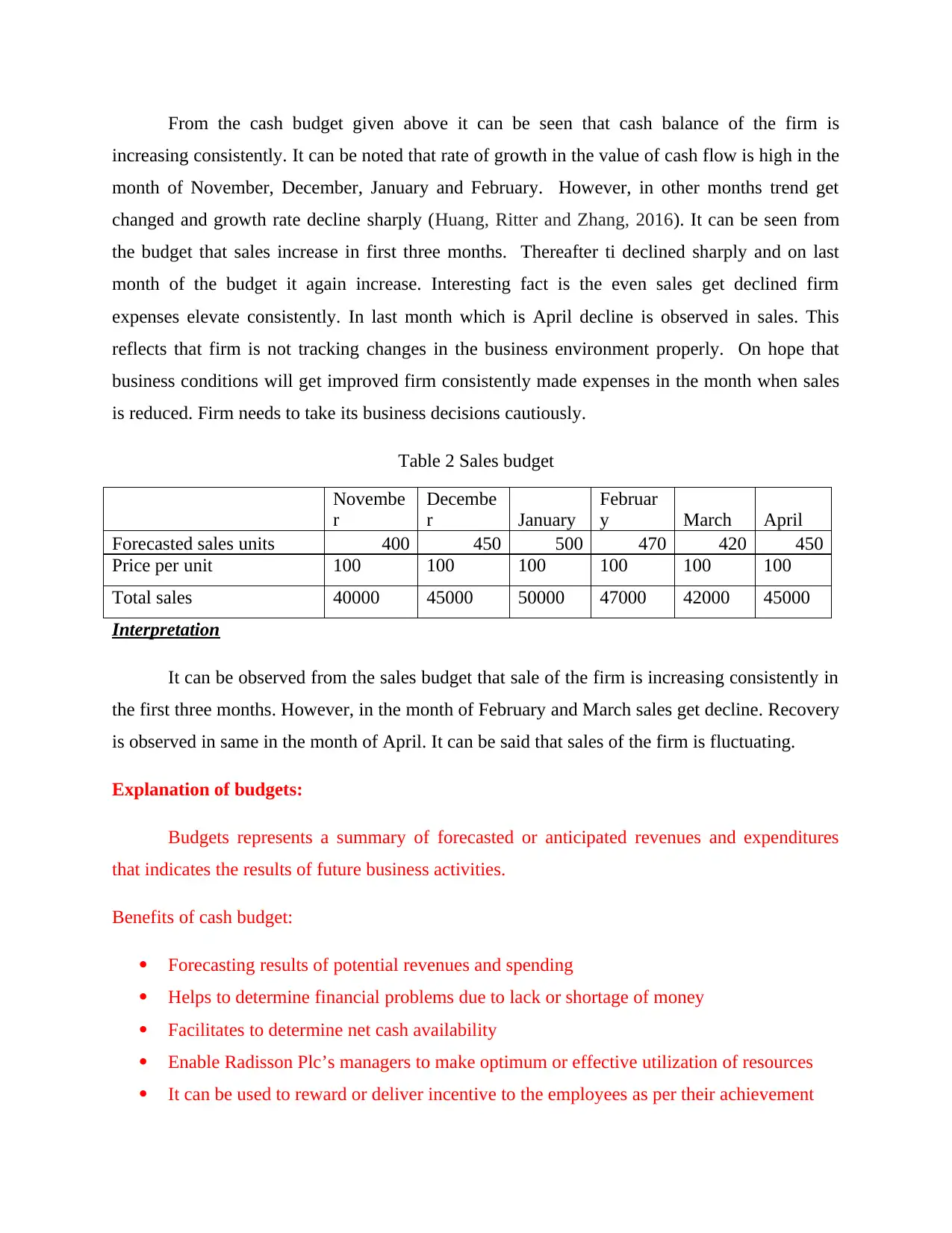

Table 2 Sales budget

Novembe

r

Decembe

r January

Februar

y March April

Forecasted sales units 400 450 500 470 420 450

Price per unit 100 100 100 100 100 100

Total sales 40000 45000 50000 47000 42000 45000

Interpretation

It can be observed from the sales budget that sale of the firm is increasing consistently in

the first three months. However, in the month of February and March sales get decline. Recovery

is observed in same in the month of April. It can be said that sales of the firm is fluctuating.

Explanation of budgets:

Budgets represents a summary of forecasted or anticipated revenues and expenditures

that indicates the results of future business activities.

Benefits of cash budget:

Forecasting results of potential revenues and spending

Helps to determine financial problems due to lack or shortage of money

Facilitates to determine net cash availability

Enable Radisson Plc’s managers to make optimum or effective utilization of resources

It can be used to reward or deliver incentive to the employees as per their achievement

increasing consistently. It can be noted that rate of growth in the value of cash flow is high in the

month of November, December, January and February. However, in other months trend get

changed and growth rate decline sharply (Huang, Ritter and Zhang, 2016). It can be seen from

the budget that sales increase in first three months. Thereafter ti declined sharply and on last

month of the budget it again increase. Interesting fact is the even sales get declined firm

expenses elevate consistently. In last month which is April decline is observed in sales. This

reflects that firm is not tracking changes in the business environment properly. On hope that

business conditions will get improved firm consistently made expenses in the month when sales

is reduced. Firm needs to take its business decisions cautiously.

Table 2 Sales budget

Novembe

r

Decembe

r January

Februar

y March April

Forecasted sales units 400 450 500 470 420 450

Price per unit 100 100 100 100 100 100

Total sales 40000 45000 50000 47000 42000 45000

Interpretation

It can be observed from the sales budget that sale of the firm is increasing consistently in

the first three months. However, in the month of February and March sales get decline. Recovery

is observed in same in the month of April. It can be said that sales of the firm is fluctuating.

Explanation of budgets:

Budgets represents a summary of forecasted or anticipated revenues and expenditures

that indicates the results of future business activities.

Benefits of cash budget:

Forecasting results of potential revenues and spending

Helps to determine financial problems due to lack or shortage of money

Facilitates to determine net cash availability

Enable Radisson Plc’s managers to make optimum or effective utilization of resources

It can be used to reward or deliver incentive to the employees as per their achievement

Helps to accomplish financial goals by controlling expenditures and generating target

revenues

B

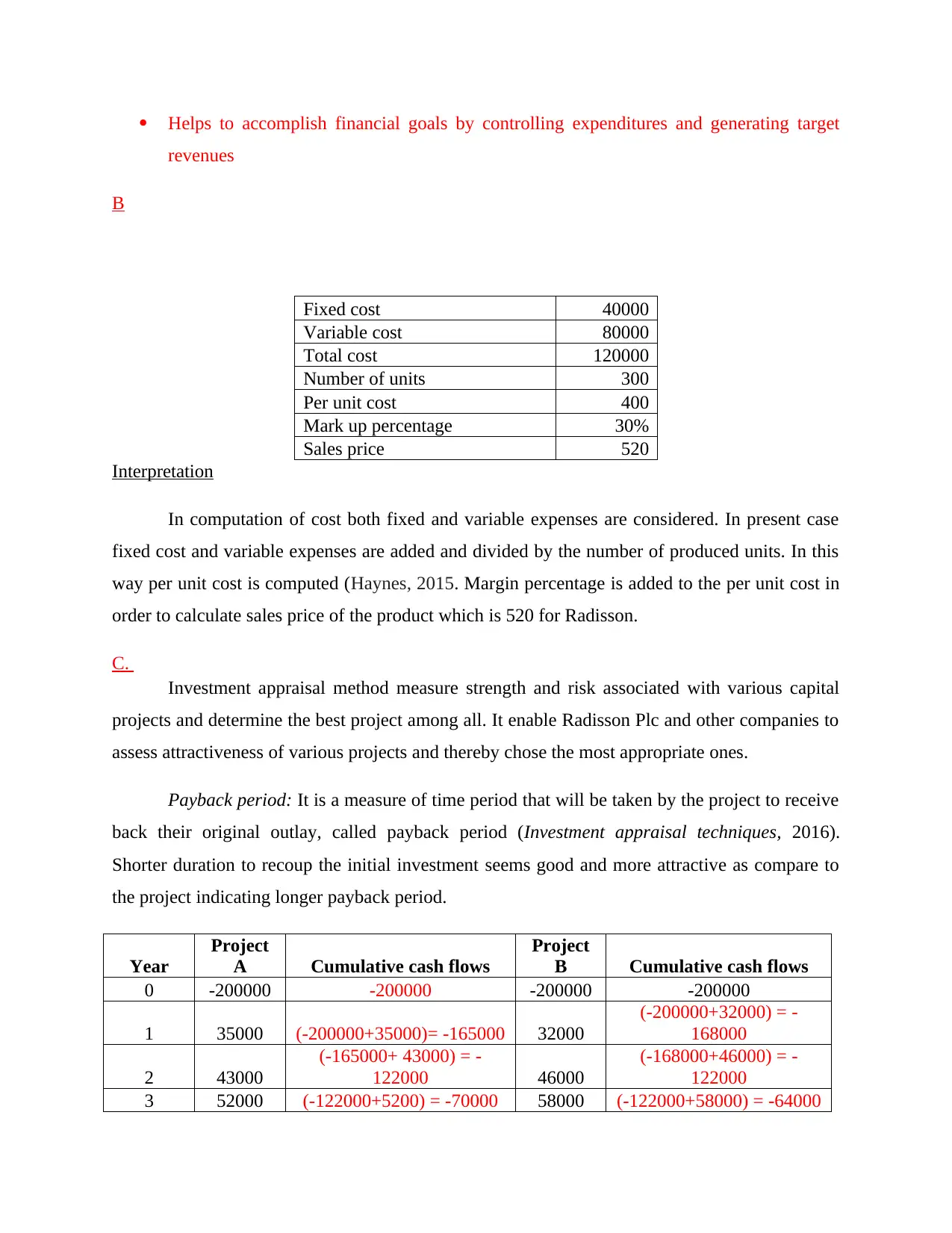

Fixed cost 40000

Variable cost 80000

Total cost 120000

Number of units 300

Per unit cost 400

Mark up percentage 30%

Sales price 520

Interpretation

In computation of cost both fixed and variable expenses are considered. In present case

fixed cost and variable expenses are added and divided by the number of produced units. In this

way per unit cost is computed (Haynes, 2015. Margin percentage is added to the per unit cost in

order to calculate sales price of the product which is 520 for Radisson.

C.

Investment appraisal method measure strength and risk associated with various capital

projects and determine the best project among all. It enable Radisson Plc and other companies to

assess attractiveness of various projects and thereby chose the most appropriate ones.

Payback period: It is a measure of time period that will be taken by the project to receive

back their original outlay, called payback period (Investment appraisal techniques, 2016).

Shorter duration to recoup the initial investment seems good and more attractive as compare to

the project indicating longer payback period.

Year

Project

A Cumulative cash flows

Project

B Cumulative cash flows

0 -200000 -200000 -200000 -200000

1 35000 (-200000+35000)= -165000 32000

(-200000+32000) = -

168000

2 43000

(-165000+ 43000) = -

122000 46000

(-168000+46000) = -

122000

3 52000 (-122000+5200) = -70000 58000 (-122000+58000) = -64000

revenues

B

Fixed cost 40000

Variable cost 80000

Total cost 120000

Number of units 300

Per unit cost 400

Mark up percentage 30%

Sales price 520

Interpretation

In computation of cost both fixed and variable expenses are considered. In present case

fixed cost and variable expenses are added and divided by the number of produced units. In this

way per unit cost is computed (Haynes, 2015. Margin percentage is added to the per unit cost in

order to calculate sales price of the product which is 520 for Radisson.

C.

Investment appraisal method measure strength and risk associated with various capital

projects and determine the best project among all. It enable Radisson Plc and other companies to

assess attractiveness of various projects and thereby chose the most appropriate ones.

Payback period: It is a measure of time period that will be taken by the project to receive

back their original outlay, called payback period (Investment appraisal techniques, 2016).

Shorter duration to recoup the initial investment seems good and more attractive as compare to

the project indicating longer payback period.

Year

Project

A Cumulative cash flows

Project

B Cumulative cash flows

0 -200000 -200000 -200000 -200000

1 35000 (-200000+35000)= -165000 32000

(-200000+32000) = -

168000

2 43000

(-165000+ 43000) = -

122000 46000

(-168000+46000) = -

122000

3 52000 (-122000+5200) = -70000 58000 (-122000+58000) = -64000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.