Comprehensive Financial Analysis: Ramsay Healthcare Ltd Performance

VerifiedAdded on 2023/06/07

|31

|7535

|423

Report

AI Summary

This report provides a detailed financial analysis of Ramsay Healthcare Ltd over a five-year period, comparing its performance against Sonic Healthcare Ltd. Key financial ratios related to profitability, solvency, and liquidity are computed and analyzed to assess Ramsay Healthcare's growth and financial health. The analysis includes an examination of net profit margins, return on equity, return on assets, and return on invested capital for both companies, offering insights into their relative financial positions and operational efficiencies. The report concludes with a comparative analysis, highlighting the strengths and weaknesses of each company's financial performance.

Running head: FUNDAMENTAL OF VALUE CREATION

Fundamental of Value Creation

Name of the Student:

Name of the University

Author’s Note

Fundamental of Value Creation

Name of the Student:

Name of the University

Author’s Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

FUNDAMENTAL OF VALUE CREATION

Executive Summary

The main purpose of this assessment is to analyze the performance of Ramsay Healthcare ltd for

the period of five years in order to estimate whether the business is performing and growing as

per the expectation of the management or not. The assessment contains analysis of the financial

statements in order t analyze the significant items which are included in the annual reports of the

business during the year. The assessment further contains ratio computation of profitability,

solvency and liquidity aspects of the business and provide analysis for the same considering the

growth of the business. The assessment includes analysis of another company’s financial

statements in order to ensure that the performance of Ramsay Healthcare ltd can be measured

against a standard. The company which is selected is one of the close competitors of the business

which is Sonic Healthcare ltd. The assessment includes ratio calculations of Sonic Healthcare ltd

along with comparative analysis for the same.

FUNDAMENTAL OF VALUE CREATION

Executive Summary

The main purpose of this assessment is to analyze the performance of Ramsay Healthcare ltd for

the period of five years in order to estimate whether the business is performing and growing as

per the expectation of the management or not. The assessment contains analysis of the financial

statements in order t analyze the significant items which are included in the annual reports of the

business during the year. The assessment further contains ratio computation of profitability,

solvency and liquidity aspects of the business and provide analysis for the same considering the

growth of the business. The assessment includes analysis of another company’s financial

statements in order to ensure that the performance of Ramsay Healthcare ltd can be measured

against a standard. The company which is selected is one of the close competitors of the business

which is Sonic Healthcare ltd. The assessment includes ratio calculations of Sonic Healthcare ltd

along with comparative analysis for the same.

2

FUNDAMENTAL OF VALUE CREATION

Table of Contents

Introduction......................................................................................................................................3

Profitability Ratio Analysis.............................................................................................................4

Liquidity Ratio Analysis..................................................................................................................9

Solvency Ratio Analysis................................................................................................................14

Industry Analysis...........................................................................................................................18

Conclusion.....................................................................................................................................21

Bibliography..................................................................................................................................23

Appendix........................................................................................................................................25

FUNDAMENTAL OF VALUE CREATION

Table of Contents

Introduction......................................................................................................................................3

Profitability Ratio Analysis.............................................................................................................4

Liquidity Ratio Analysis..................................................................................................................9

Solvency Ratio Analysis................................................................................................................14

Industry Analysis...........................................................................................................................18

Conclusion.....................................................................................................................................21

Bibliography..................................................................................................................................23

Appendix........................................................................................................................................25

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

FUNDAMENTAL OF VALUE CREATION

Introduction

Ramsay Healthcare ltd is one of the leading operators in hospitals and provides health

care services to the clients and hospitals as well. As per approximate figures, the company

operates in around 235 hospitals and day surgery facilities across Australia, France, UK,

Malaysia and Italy. The company operates in 73 hospitals in Australia itself making the country

from which the business generates maximum revenues. In UK, the business has a fair share of

trades with operations in 35 hospitals and also acts as an independent service provider and the

services of the business are also referred by National Health Services (NHS). It is shown in the

annual report that the business employees around 60,000 employees and has around 200

pharmacies. The annual report of the company further shows that the business draws about 50%

of its revenue from the operation in Australia and again around 20% from the market of UK.

The main purpose of this assessment is to analyze the financial performance of the

business of Ramsay Health Care ltd which is engaged in providing healthcare services to the

people and mainly operates in UK and Australia. The assessment will be making a comparative

analysis of the financial statements of the business for a period of five years and then on the basis

of the financial information significant ratios are to be computed. The assessment will also be

considering another company for the purpose of conducting a comparative analysis of the

financial performance of both the companies. The company which is selected for the

comparative analysis is Sonic Health care ltd which is regarded to be one of the close

competitors of the Ramsay Healthcare Ltd. The assessment will be analyzing the financial

statements which is prepared by both the business for the current year in comparison to previous

year as well and with each other to establish which business has a better performance. In addition

to this, key financial ratios of the business will be computed which are related to solvency,

profitability and liquidity aspects of the business (Brochet, Jagolinzer & Riedl, 2013). The main

motive of the assessment is to analyze the development of business in terms of financial

estimates which are to be analyzed considering a five years period. Another objective of the

assessment is to set a competitive analysis in roder to under the financial position of both the

business.

Ramsay Healthcare Ltd is engaged in the business of providing health care services to the

customers and the business operates as a private business firm. The business has its headquarters

FUNDAMENTAL OF VALUE CREATION

Introduction

Ramsay Healthcare ltd is one of the leading operators in hospitals and provides health

care services to the clients and hospitals as well. As per approximate figures, the company

operates in around 235 hospitals and day surgery facilities across Australia, France, UK,

Malaysia and Italy. The company operates in 73 hospitals in Australia itself making the country

from which the business generates maximum revenues. In UK, the business has a fair share of

trades with operations in 35 hospitals and also acts as an independent service provider and the

services of the business are also referred by National Health Services (NHS). It is shown in the

annual report that the business employees around 60,000 employees and has around 200

pharmacies. The annual report of the company further shows that the business draws about 50%

of its revenue from the operation in Australia and again around 20% from the market of UK.

The main purpose of this assessment is to analyze the financial performance of the

business of Ramsay Health Care ltd which is engaged in providing healthcare services to the

people and mainly operates in UK and Australia. The assessment will be making a comparative

analysis of the financial statements of the business for a period of five years and then on the basis

of the financial information significant ratios are to be computed. The assessment will also be

considering another company for the purpose of conducting a comparative analysis of the

financial performance of both the companies. The company which is selected for the

comparative analysis is Sonic Health care ltd which is regarded to be one of the close

competitors of the Ramsay Healthcare Ltd. The assessment will be analyzing the financial

statements which is prepared by both the business for the current year in comparison to previous

year as well and with each other to establish which business has a better performance. In addition

to this, key financial ratios of the business will be computed which are related to solvency,

profitability and liquidity aspects of the business (Brochet, Jagolinzer & Riedl, 2013). The main

motive of the assessment is to analyze the development of business in terms of financial

estimates which are to be analyzed considering a five years period. Another objective of the

assessment is to set a competitive analysis in roder to under the financial position of both the

business.

Ramsay Healthcare Ltd is engaged in the business of providing health care services to the

customers and the business operates as a private business firm. The business has its headquarters

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

FUNDAMENTAL OF VALUE CREATION

in Australia but also has its operations in UK and France. The company specializes in providing

services such as surgery, rehabilitation and psychiatric care for the clients of the business. The

business is a growing business in terms of revenue and profits generation as shown in the

financial statements of the business. On the other hand, the business of Sonic Healthcare ltd is

engaged in providing laboratory services, pathology and radiology services to the customers of

the business. The business of Sonic Healthcare ltd operates in the same industry as Ramsay

Healthcare ltd. The company is regarded to be one of the largest diagnostic companies in the

country. The company also has its operations in several other countries like UK, USA, Germany

and several other countries.

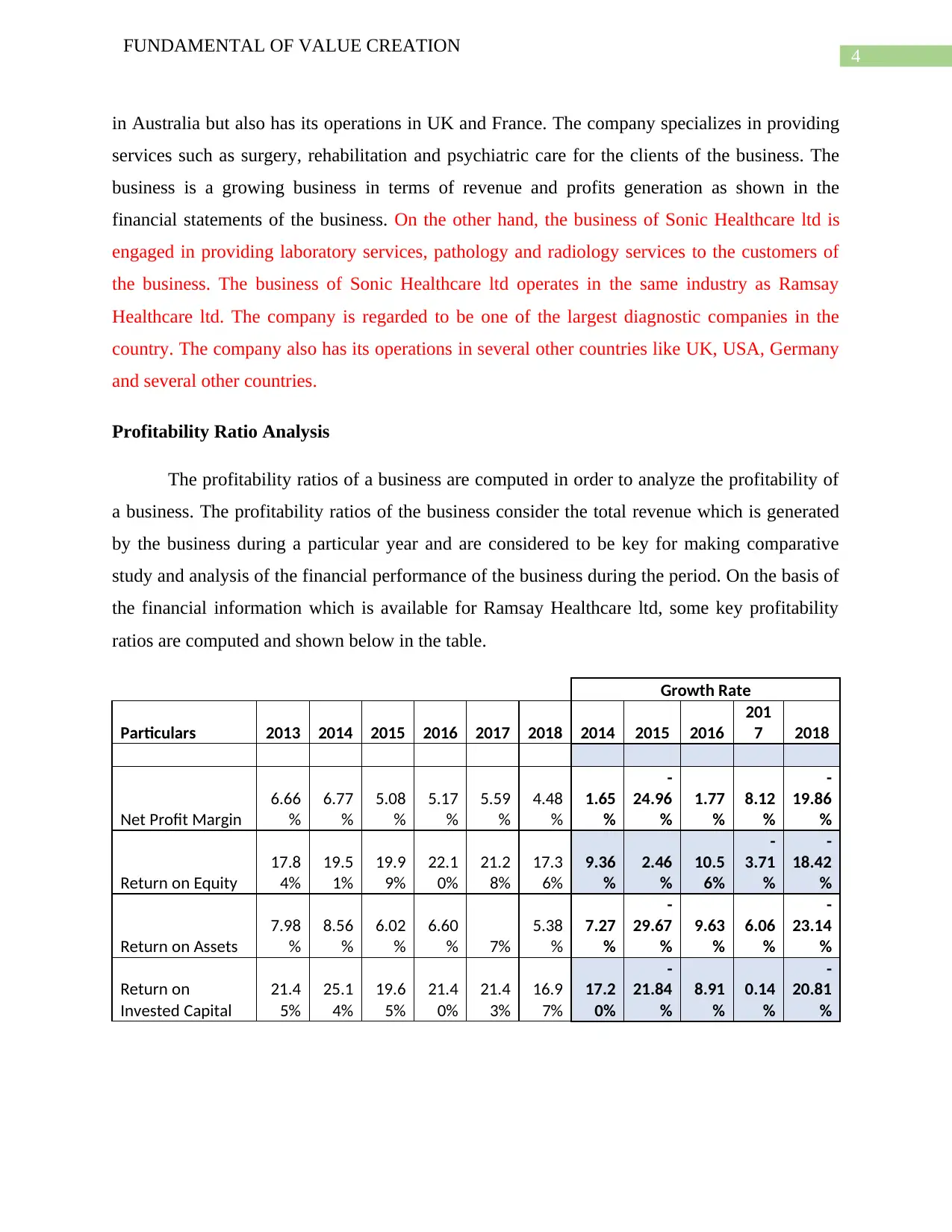

Profitability Ratio Analysis

The profitability ratios of a business are computed in order to analyze the profitability of

a business. The profitability ratios of the business consider the total revenue which is generated

by the business during a particular year and are considered to be key for making comparative

study and analysis of the financial performance of the business during the period. On the basis of

the financial information which is available for Ramsay Healthcare ltd, some key profitability

ratios are computed and shown below in the table.

Growth Rate

Particulars 2013 2014 2015 2016 2017 2018 2014 2015 2016

201

7 2018

Net Profit Margin

6.66

%

6.77

%

5.08

%

5.17

%

5.59

%

4.48

%

1.65

%

-

24.96

%

1.77

%

8.12

%

-

19.86

%

Return on Equity

17.8

4%

19.5

1%

19.9

9%

22.1

0%

21.2

8%

17.3

6%

9.36

%

2.46

%

10.5

6%

-

3.71

%

-

18.42

%

Return on Assets

7.98

%

8.56

%

6.02

%

6.60

% 7%

5.38

%

7.27

%

-

29.67

%

9.63

%

6.06

%

-

23.14

%

Return on

Invested Capital

21.4

5%

25.1

4%

19.6

5%

21.4

0%

21.4

3%

16.9

7%

17.2

0%

-

21.84

%

8.91

%

0.14

%

-

20.81

%

FUNDAMENTAL OF VALUE CREATION

in Australia but also has its operations in UK and France. The company specializes in providing

services such as surgery, rehabilitation and psychiatric care for the clients of the business. The

business is a growing business in terms of revenue and profits generation as shown in the

financial statements of the business. On the other hand, the business of Sonic Healthcare ltd is

engaged in providing laboratory services, pathology and radiology services to the customers of

the business. The business of Sonic Healthcare ltd operates in the same industry as Ramsay

Healthcare ltd. The company is regarded to be one of the largest diagnostic companies in the

country. The company also has its operations in several other countries like UK, USA, Germany

and several other countries.

Profitability Ratio Analysis

The profitability ratios of a business are computed in order to analyze the profitability of

a business. The profitability ratios of the business consider the total revenue which is generated

by the business during a particular year and are considered to be key for making comparative

study and analysis of the financial performance of the business during the period. On the basis of

the financial information which is available for Ramsay Healthcare ltd, some key profitability

ratios are computed and shown below in the table.

Growth Rate

Particulars 2013 2014 2015 2016 2017 2018 2014 2015 2016

201

7 2018

Net Profit Margin

6.66

%

6.77

%

5.08

%

5.17

%

5.59

%

4.48

%

1.65

%

-

24.96

%

1.77

%

8.12

%

-

19.86

%

Return on Equity

17.8

4%

19.5

1%

19.9

9%

22.1

0%

21.2

8%

17.3

6%

9.36

%

2.46

%

10.5

6%

-

3.71

%

-

18.42

%

Return on Assets

7.98

%

8.56

%

6.02

%

6.60

% 7%

5.38

%

7.27

%

-

29.67

%

9.63

%

6.06

%

-

23.14

%

Return on

Invested Capital

21.4

5%

25.1

4%

19.6

5%

21.4

0%

21.4

3%

16.9

7%

17.2

0%

-

21.84

%

8.91

%

0.14

%

-

20.81

%

5

FUNDAMENTAL OF VALUE CREATION

4.48%

17.36%

5.38%

16.97%

Profitability Ratios

Net Profit Margin Return on Equity

Return on Assets Return on Invested Capital

Figure 1: (Pie Chart portraying Profitability ratios for 2018)

Source: (Created by the Author)

The above table shows the computation of net profit margin of a business, return on

assets and equity and return on invested capital of the business which are considered to be key

financial ratios of the business. The pie Chart which is shown in figure 4 reflects profitability

ratios of the business for the year 2018. The net profit margin as shown in the table above has

declined over the years which is due to the high costs of operations of the business. The net

profit margin for the business for the year 2018 is shown to be 4.48% which was shown to be

6.67 in 2014. From 2014, the sales of the business has increased rapidly and so has the costs of

operations and therefore there is a fall in the net profit margin of the business (Carraher & Van

Auken, 2013). The return on assets and return on equity of a business are considered to be

important financial indicator for the success of the business. The return on equity has declined

heavily as compared to 2017 analysis which suggest that the business is not earning enough

returns on its equity and the growth is shown to be negative (Delen, Kuzey & Uyar, 2013). The

return on assets of the business also demonstrate a similar trend and the growth is in negative

which is shown to be -23.14%. The return on invested capital of the business is shown to be on a

fall as well which is due to the fact of fall in the profits of the business. The return on invested

FUNDAMENTAL OF VALUE CREATION

4.48%

17.36%

5.38%

16.97%

Profitability Ratios

Net Profit Margin Return on Equity

Return on Assets Return on Invested Capital

Figure 1: (Pie Chart portraying Profitability ratios for 2018)

Source: (Created by the Author)

The above table shows the computation of net profit margin of a business, return on

assets and equity and return on invested capital of the business which are considered to be key

financial ratios of the business. The pie Chart which is shown in figure 4 reflects profitability

ratios of the business for the year 2018. The net profit margin as shown in the table above has

declined over the years which is due to the high costs of operations of the business. The net

profit margin for the business for the year 2018 is shown to be 4.48% which was shown to be

6.67 in 2014. From 2014, the sales of the business has increased rapidly and so has the costs of

operations and therefore there is a fall in the net profit margin of the business (Carraher & Van

Auken, 2013). The return on assets and return on equity of a business are considered to be

important financial indicator for the success of the business. The return on equity has declined

heavily as compared to 2017 analysis which suggest that the business is not earning enough

returns on its equity and the growth is shown to be negative (Delen, Kuzey & Uyar, 2013). The

return on assets of the business also demonstrate a similar trend and the growth is in negative

which is shown to be -23.14%. The return on invested capital of the business is shown to be on a

fall as well which is due to the fact of fall in the profits of the business. The return on invested

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

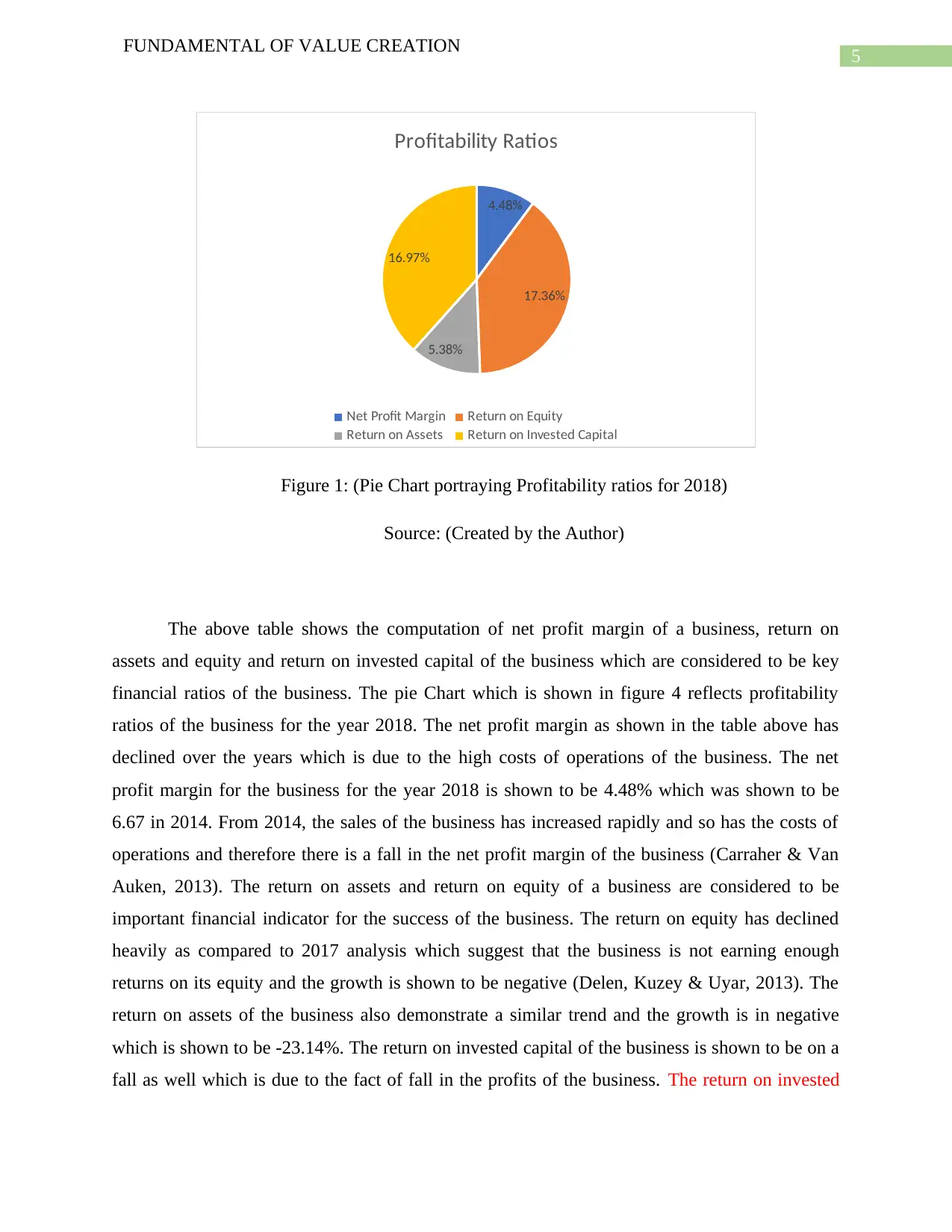

FUNDAMENTAL OF VALUE CREATION

capital of the business is shown to be highest in 2014 for which the return on investment is

computed to be 25.14% and in the next year the return on investment estimate has significantly

reduced as shown in the table which is shown above. The estimate of 2015 is shown to be

19.65% which is shown to have significantly improved in the next two years which is shown to

be 21.40% and 21.43% respectively. In 2018 due to the fall in the profits of the business, the

estimate is shown to have considerably fallen and the same is shown to be 16.97%. The growth

in this estimate is also shown to be in negative and the same is shown to be -20.81%.

Figure 2: (Graph portraying Profitability ratios of Ramsay Healthcare Ltd)

Source: (Created by the Author)

The above graph portrays the profitability ratios of the business and also shows trendlines

depicting growth and fluctuation in the ratios of the business. The above graph shows an analysis

for a five years period as demonstrated above.

FUNDAMENTAL OF VALUE CREATION

capital of the business is shown to be highest in 2014 for which the return on investment is

computed to be 25.14% and in the next year the return on investment estimate has significantly

reduced as shown in the table which is shown above. The estimate of 2015 is shown to be

19.65% which is shown to have significantly improved in the next two years which is shown to

be 21.40% and 21.43% respectively. In 2018 due to the fall in the profits of the business, the

estimate is shown to have considerably fallen and the same is shown to be 16.97%. The growth

in this estimate is also shown to be in negative and the same is shown to be -20.81%.

Figure 2: (Graph portraying Profitability ratios of Ramsay Healthcare Ltd)

Source: (Created by the Author)

The above graph portrays the profitability ratios of the business and also shows trendlines

depicting growth and fluctuation in the ratios of the business. The above graph shows an analysis

for a five years period as demonstrated above.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

FUNDAMENTAL OF VALUE CREATION

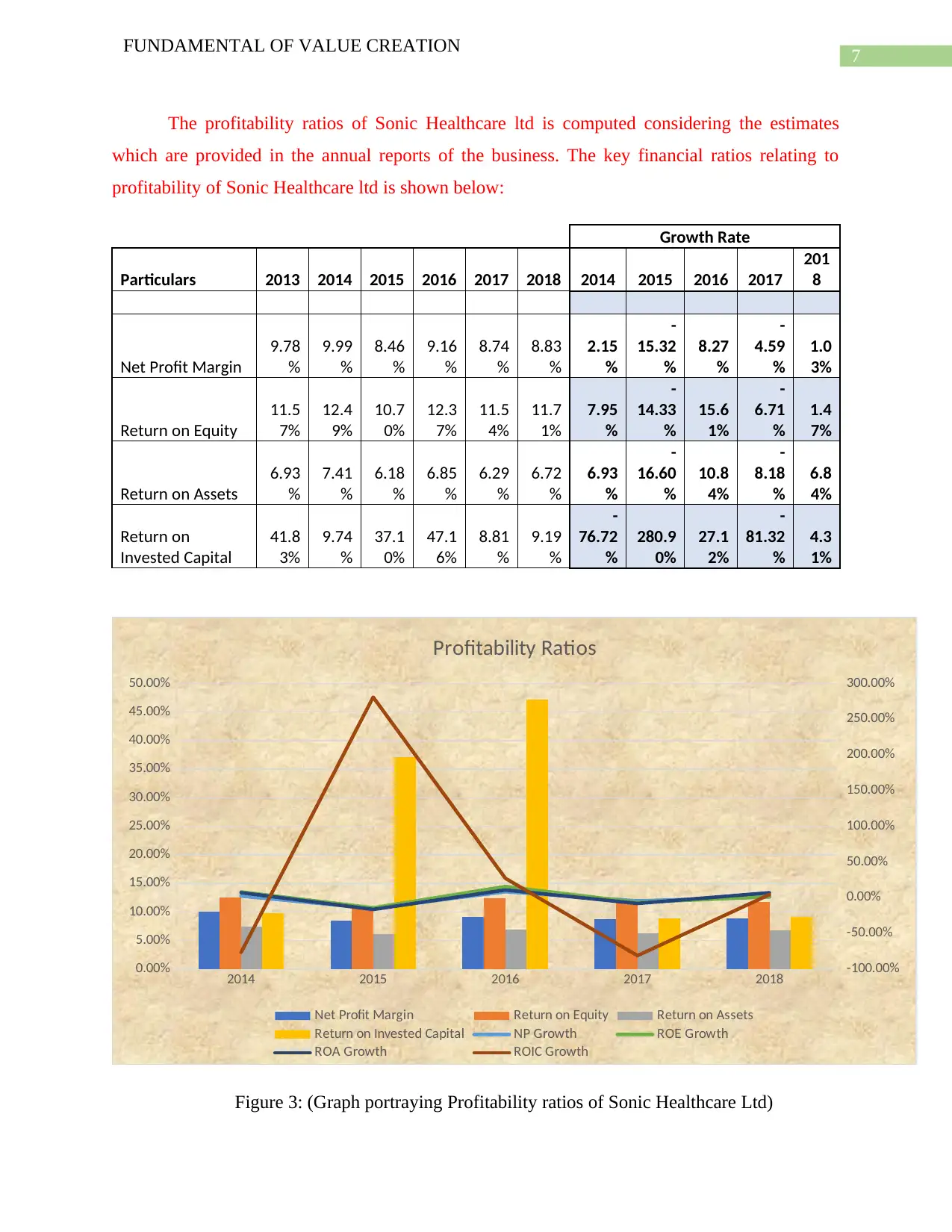

The profitability ratios of Sonic Healthcare ltd is computed considering the estimates

which are provided in the annual reports of the business. The key financial ratios relating to

profitability of Sonic Healthcare ltd is shown below:

Growth Rate

Particulars 2013 2014 2015 2016 2017 2018 2014 2015 2016 2017

201

8

Net Profit Margin

9.78

%

9.99

%

8.46

%

9.16

%

8.74

%

8.83

%

2.15

%

-

15.32

%

8.27

%

-

4.59

%

1.0

3%

Return on Equity

11.5

7%

12.4

9%

10.7

0%

12.3

7%

11.5

4%

11.7

1%

7.95

%

-

14.33

%

15.6

1%

-

6.71

%

1.4

7%

Return on Assets

6.93

%

7.41

%

6.18

%

6.85

%

6.29

%

6.72

%

6.93

%

-

16.60

%

10.8

4%

-

8.18

%

6.8

4%

Return on

Invested Capital

41.8

3%

9.74

%

37.1

0%

47.1

6%

8.81

%

9.19

%

-

76.72

%

280.9

0%

27.1

2%

-

81.32

%

4.3

1%

2014 2015 2016 2017 2018

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

35.00%

40.00%

45.00%

50.00%

-100.00%

-50.00%

0.00%

50.00%

100.00%

150.00%

200.00%

250.00%

300.00%

Profitability Ratios

Net Profit Margin Return on Equity Return on Assets

Return on Invested Capital NP Growth ROE Growth

ROA Growth ROIC Growth

Figure 3: (Graph portraying Profitability ratios of Sonic Healthcare Ltd)

FUNDAMENTAL OF VALUE CREATION

The profitability ratios of Sonic Healthcare ltd is computed considering the estimates

which are provided in the annual reports of the business. The key financial ratios relating to

profitability of Sonic Healthcare ltd is shown below:

Growth Rate

Particulars 2013 2014 2015 2016 2017 2018 2014 2015 2016 2017

201

8

Net Profit Margin

9.78

%

9.99

%

8.46

%

9.16

%

8.74

%

8.83

%

2.15

%

-

15.32

%

8.27

%

-

4.59

%

1.0

3%

Return on Equity

11.5

7%

12.4

9%

10.7

0%

12.3

7%

11.5

4%

11.7

1%

7.95

%

-

14.33

%

15.6

1%

-

6.71

%

1.4

7%

Return on Assets

6.93

%

7.41

%

6.18

%

6.85

%

6.29

%

6.72

%

6.93

%

-

16.60

%

10.8

4%

-

8.18

%

6.8

4%

Return on

Invested Capital

41.8

3%

9.74

%

37.1

0%

47.1

6%

8.81

%

9.19

%

-

76.72

%

280.9

0%

27.1

2%

-

81.32

%

4.3

1%

2014 2015 2016 2017 2018

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

35.00%

40.00%

45.00%

50.00%

-100.00%

-50.00%

0.00%

50.00%

100.00%

150.00%

200.00%

250.00%

300.00%

Profitability Ratios

Net Profit Margin Return on Equity Return on Assets

Return on Invested Capital NP Growth ROE Growth

ROA Growth ROIC Growth

Figure 3: (Graph portraying Profitability ratios of Sonic Healthcare Ltd)

8

FUNDAMENTAL OF VALUE CREATION

Source: (Created by the Author)

The above table and graph shows the key financial ratios of Sonic Healthcare ltd which is

computed considering the key profitability ratios of the business which are net profit margin.

Return on equity, return on assets and return on investment of the business. The net profit margin

of the business shows an estimate of 8.83% for the current year which has improved slightly in

comparison to previous year analysis which is shown to be 8.74. The growth in profit margin in

profit margin of the business is small and therefore there is a growth of 1,03$. The reason for the

low profits may be due to the lower sales which is achieved by the business or higher costs

which are incurred by the business. The return on assets of the business is shown to have

improved significantly in comparison to previous year estimates and this is a positive sign for the

business. The highest return which is computed for return on assets of the business is shown to

be 7.41% for 2014. The return on equity of the business for the year 2018 is shown to be 11.71%

which has improved significantly in comparison to past year estimate however it is still not better

than 2014 estimate which is shown to be 12.94%. The return on invested capital of the business

has reduced significantly during the current year in comparison to past year analysis which needs

to be considered by the management Healthcare ltd.

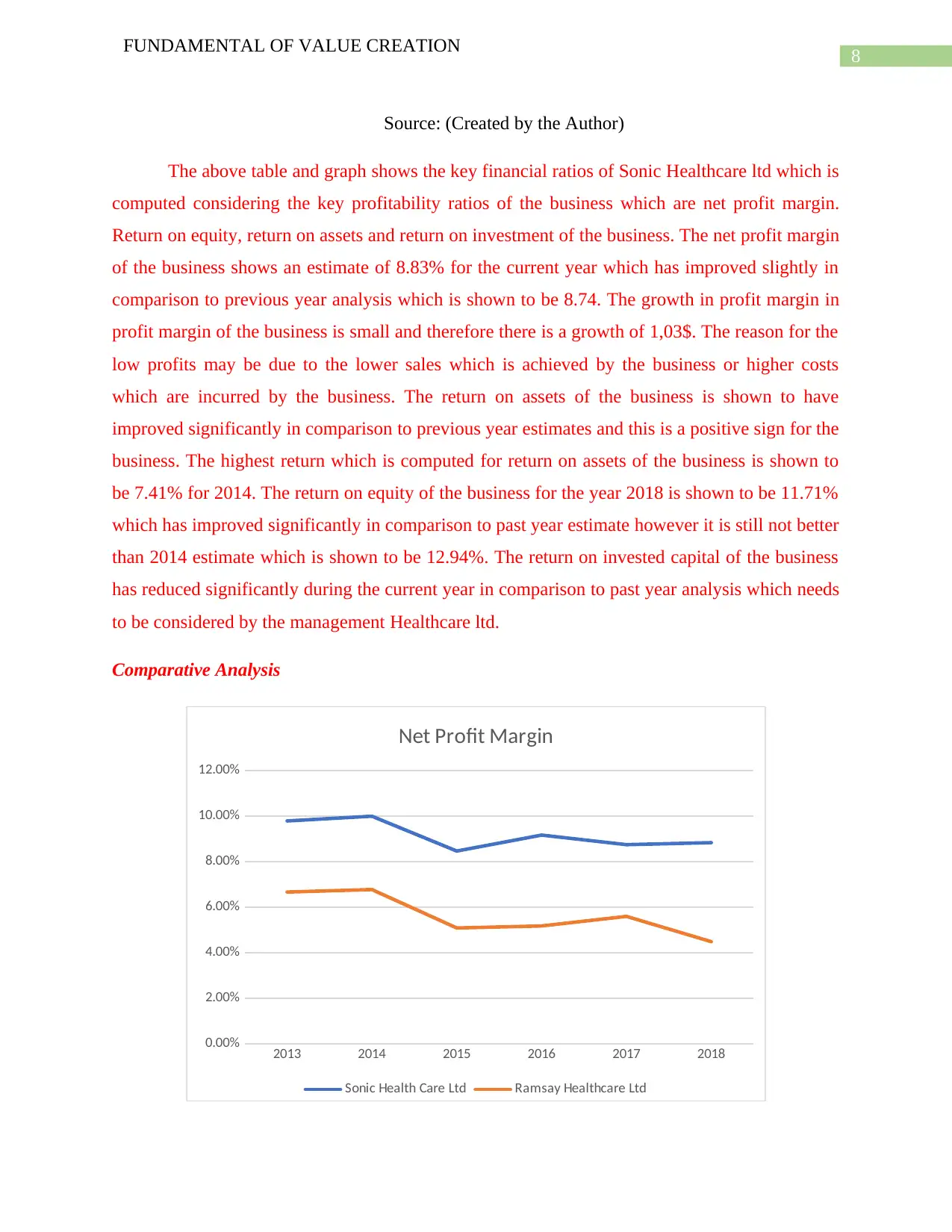

Comparative Analysis

2013 2014 2015 2016 2017 2018

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

12.00%

Net Profit Margin

Sonic Health Care Ltd Ramsay Healthcare Ltd

FUNDAMENTAL OF VALUE CREATION

Source: (Created by the Author)

The above table and graph shows the key financial ratios of Sonic Healthcare ltd which is

computed considering the key profitability ratios of the business which are net profit margin.

Return on equity, return on assets and return on investment of the business. The net profit margin

of the business shows an estimate of 8.83% for the current year which has improved slightly in

comparison to previous year analysis which is shown to be 8.74. The growth in profit margin in

profit margin of the business is small and therefore there is a growth of 1,03$. The reason for the

low profits may be due to the lower sales which is achieved by the business or higher costs

which are incurred by the business. The return on assets of the business is shown to have

improved significantly in comparison to previous year estimates and this is a positive sign for the

business. The highest return which is computed for return on assets of the business is shown to

be 7.41% for 2014. The return on equity of the business for the year 2018 is shown to be 11.71%

which has improved significantly in comparison to past year estimate however it is still not better

than 2014 estimate which is shown to be 12.94%. The return on invested capital of the business

has reduced significantly during the current year in comparison to past year analysis which needs

to be considered by the management Healthcare ltd.

Comparative Analysis

2013 2014 2015 2016 2017 2018

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

12.00%

Net Profit Margin

Sonic Health Care Ltd Ramsay Healthcare Ltd

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

FUNDAMENTAL OF VALUE CREATION

Figure 4: (Graph showing comparative analysis of Net profit Margin of Both Companies)

Source: (Created by the Author)

As shown in the graph above, the net profit margin of Sonic Healthcare ltd is much better

than Ramsay Healthcare ltd. The net profit margin is the most important estimate of profitability

ratios and the same is shown to be better for Sonic Healthcare ltd. The return on assets of the

business for Sonic Healthcare ltd is shown to be better than Ramsay Healthcare ltd in current

year as well in past four years which suggest that the operational structure of Sonic Healthcare

ltd is better than Ramsay Healthcare ltd. The return on equity estimate which is shown for the

Ramsay Healthcare ltd is shown to be 17.36% whereas the same for Sonic Healthcare ltd is

shown to be 11,71% which shows that the management of Ramsay Healthcare ltd fulfills the

needs of the shareholders better than Sonic Healthcare ltd. The return on investment for Ramsay

Healthcare ltd is shown to be better than Sonic Healthcare ltd which is a good sign.

In an overall estimate it can be said that the profitability of Sonic Healthcare ltd is better

than Ramsay Healthcare ltd and therefore the management of Ramsay Healthcare ltd needs to

think about focusing on the profitability aspect of the business.

Liquidity Ratio Analysis

The liquidity ratios of a business show the cash position of the business and also the

ability of the business to meet the current obligations of the business in an effective manner. The

liquidity ratios of the business consist of current ratio and quick ratio which are considered to be

an important indicator for the success of the business (Ongore & Kusa, 2013). In the case of

Ramsay Healthcare ltd, liquidity ratios o the business is computed considering the financial

statements of the business for five year and the same is presented in the table below:

Growth Rate

Particulars

201

3

201

4

201

5

201

6

201

7

201

8 2014 2015 2016 2017 2018

Current Ratio

1.2

3

0.9

7

0.7

6

0.9

2

1.0

3

1.1

9

-

21.14

%

-

21.65

%

21.05

%

11.96

%

15.53

%

Quick Ratio 1.0

9

0.8

3

0.6

7

0.8

2

0.9

1

1.0

5

-

23.85

-

19.28

22.39

%

10.98

%

15.38

%

FUNDAMENTAL OF VALUE CREATION

Figure 4: (Graph showing comparative analysis of Net profit Margin of Both Companies)

Source: (Created by the Author)

As shown in the graph above, the net profit margin of Sonic Healthcare ltd is much better

than Ramsay Healthcare ltd. The net profit margin is the most important estimate of profitability

ratios and the same is shown to be better for Sonic Healthcare ltd. The return on assets of the

business for Sonic Healthcare ltd is shown to be better than Ramsay Healthcare ltd in current

year as well in past four years which suggest that the operational structure of Sonic Healthcare

ltd is better than Ramsay Healthcare ltd. The return on equity estimate which is shown for the

Ramsay Healthcare ltd is shown to be 17.36% whereas the same for Sonic Healthcare ltd is

shown to be 11,71% which shows that the management of Ramsay Healthcare ltd fulfills the

needs of the shareholders better than Sonic Healthcare ltd. The return on investment for Ramsay

Healthcare ltd is shown to be better than Sonic Healthcare ltd which is a good sign.

In an overall estimate it can be said that the profitability of Sonic Healthcare ltd is better

than Ramsay Healthcare ltd and therefore the management of Ramsay Healthcare ltd needs to

think about focusing on the profitability aspect of the business.

Liquidity Ratio Analysis

The liquidity ratios of a business show the cash position of the business and also the

ability of the business to meet the current obligations of the business in an effective manner. The

liquidity ratios of the business consist of current ratio and quick ratio which are considered to be

an important indicator for the success of the business (Ongore & Kusa, 2013). In the case of

Ramsay Healthcare ltd, liquidity ratios o the business is computed considering the financial

statements of the business for five year and the same is presented in the table below:

Growth Rate

Particulars

201

3

201

4

201

5

201

6

201

7

201

8 2014 2015 2016 2017 2018

Current Ratio

1.2

3

0.9

7

0.7

6

0.9

2

1.0

3

1.1

9

-

21.14

%

-

21.65

%

21.05

%

11.96

%

15.53

%

Quick Ratio 1.0

9

0.8

3

0.6

7

0.8

2

0.9

1

1.0

5

-

23.85

-

19.28

22.39

%

10.98

%

15.38

%

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

FUNDAMENTAL OF VALUE CREATION

% %

Net Interest

Cover

7.4

1

7.7

0

6.3

0

6.4

7

6.7

1

6.2

9 3.91%

-

18.18

% 2.70% 3.71%

-

6.26%

14%

12%

74%

Liquidity Ratio

Current Ratio

Quick Ratio

Net Interest Cover

Figure 5: (Pie Chart portraying Profitability ratios for 2018)

Source: (Created by the Author)

The above pie chart depicts the liquidity ratios of the business for the year 2018 and the

various components which are included in the same. The liquidity ratios of the business are

shown in the above figure and the same shows current ratio, quick ratio and net interest coverage

ratio as shown in above table. The current ratio of the business is shown to be 1.19 for the year

2018 which shows that the liquidity position of the business is shown to be favorable. The

current ratio of the business has improved from the year 2016 and the same has achieved growth

as shown in the table above which is 15.53% for 2018. The quick ratio of the business is similar

to current ratios but considers liquid assets for computing the ratios. The quick ratio of the

business is shown to be 1.05 for thee year 2018 which further shows that the liquidity position of

the business is appropriate (Gitman, Juchau & Flanagan, 2015). The net interest cover of the

business is shown to be 6.29 which has slightly reduced in comparison to analysis of 2017. The

net interest cover ratio signifies the ability of the company to meet the current borrowings of the

FUNDAMENTAL OF VALUE CREATION

% %

Net Interest

Cover

7.4

1

7.7

0

6.3

0

6.4

7

6.7

1

6.2

9 3.91%

-

18.18

% 2.70% 3.71%

-

6.26%

14%

12%

74%

Liquidity Ratio

Current Ratio

Quick Ratio

Net Interest Cover

Figure 5: (Pie Chart portraying Profitability ratios for 2018)

Source: (Created by the Author)

The above pie chart depicts the liquidity ratios of the business for the year 2018 and the

various components which are included in the same. The liquidity ratios of the business are

shown in the above figure and the same shows current ratio, quick ratio and net interest coverage

ratio as shown in above table. The current ratio of the business is shown to be 1.19 for the year

2018 which shows that the liquidity position of the business is shown to be favorable. The

current ratio of the business has improved from the year 2016 and the same has achieved growth

as shown in the table above which is 15.53% for 2018. The quick ratio of the business is similar

to current ratios but considers liquid assets for computing the ratios. The quick ratio of the

business is shown to be 1.05 for thee year 2018 which further shows that the liquidity position of

the business is appropriate (Gitman, Juchau & Flanagan, 2015). The net interest cover of the

business is shown to be 6.29 which has slightly reduced in comparison to analysis of 2017. The

net interest cover ratio signifies the ability of the company to meet the current borrowings of the

11

FUNDAMENTAL OF VALUE CREATION

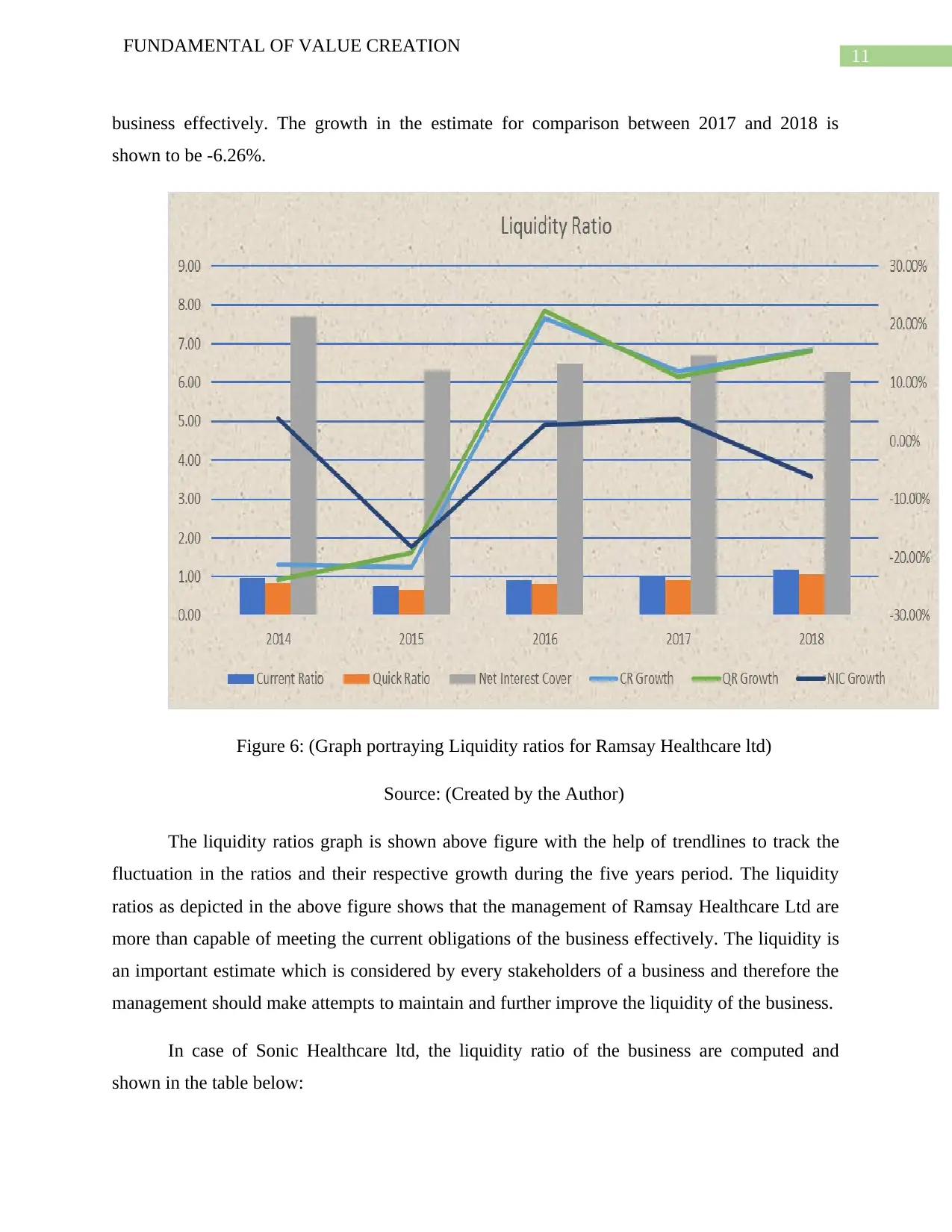

business effectively. The growth in the estimate for comparison between 2017 and 2018 is

shown to be -6.26%.

Figure 6: (Graph portraying Liquidity ratios for Ramsay Healthcare ltd)

Source: (Created by the Author)

The liquidity ratios graph is shown above figure with the help of trendlines to track the

fluctuation in the ratios and their respective growth during the five years period. The liquidity

ratios as depicted in the above figure shows that the management of Ramsay Healthcare Ltd are

more than capable of meeting the current obligations of the business effectively. The liquidity is

an important estimate which is considered by every stakeholders of a business and therefore the

management should make attempts to maintain and further improve the liquidity of the business.

In case of Sonic Healthcare ltd, the liquidity ratio of the business are computed and

shown in the table below:

FUNDAMENTAL OF VALUE CREATION

business effectively. The growth in the estimate for comparison between 2017 and 2018 is

shown to be -6.26%.

Figure 6: (Graph portraying Liquidity ratios for Ramsay Healthcare ltd)

Source: (Created by the Author)

The liquidity ratios graph is shown above figure with the help of trendlines to track the

fluctuation in the ratios and their respective growth during the five years period. The liquidity

ratios as depicted in the above figure shows that the management of Ramsay Healthcare Ltd are

more than capable of meeting the current obligations of the business effectively. The liquidity is

an important estimate which is considered by every stakeholders of a business and therefore the

management should make attempts to maintain and further improve the liquidity of the business.

In case of Sonic Healthcare ltd, the liquidity ratio of the business are computed and

shown in the table below:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 31

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.