Financial Performance Analysis of Rangemaster Plc (2018-2019)

VerifiedAdded on 2023/01/09

|14

|3568

|40

Report

AI Summary

This report provides a comprehensive financial analysis of Rangemaster Plc, a manufacturing company supplying catering equipment, focusing on its performance in 2018 and 2019. The analysis includes a summary of the income statement and statement of financial position, highlighting key changes in sales revenue, gross profit, operating profit, and net profit. The report delves into various financial ratios, including profitability (Return on Capital Employed, Gross Profit Margin, Net Operating Profit), efficiency (Asset Turnover, Inventory Turnover), liquidity (Current Ratio, Acid Test), and capital structure (Debt to Equity, Debt to Capital). Each ratio is calculated and interpreted, identifying trends and their impact on the company's financial health. The report also examines creditor's days, debtor's days, and interest coverage, offering a detailed assessment of Rangemaster Plc's financial standing and performance over the specified period.

Financial Management in

Hotel Industry

Hotel Industry

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

EXECUTIVE SUMMARY.........................................................................................................................4

MAIN BODY..............................................................................................................................................4

Summary of results..................................................................................................................................4

Analysis of each of the families of ratios.................................................................................................5

CONCLUSION...........................................................................................................................................9

REFERENCES..........................................................................................................................................11

APPENDICES...........................................................................................................................................12

EXECUTIVE SUMMARY.........................................................................................................................4

MAIN BODY..............................................................................................................................................4

Summary of results..................................................................................................................................4

Analysis of each of the families of ratios.................................................................................................5

CONCLUSION...........................................................................................................................................9

REFERENCES..........................................................................................................................................11

APPENDICES...........................................................................................................................................12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

EXECUTIVE SUMMARY

Finance represents the lifeline of any company. Finance, indeed, is still limited and so are

most other tools. Financial management is first component of the economic reporting

presentation. It is critical for any company that the finances it acquires are expended in such a

way that perhaps the profits from the expenditure are greater than financing costs. Financial

management is the method of business administration dedicated to a selective need for wealth

and an appropriate examination of the revenue source to encourage an expenditure department to

follow the path of achieving the objectives (Alsemgeest, 2015). This report based on

Rangemaster Plc which is a manufacturing company that produce and supply of catering

machine to hotel, restaurants and public services in United Kingdom. In this report analysis the

financial performance of company and identify the changes that are coming in 2019 as compare

of 2018. Along with focus on the financial ratio that accurately define the problem of the

business.

MAIN BODY

Summary of results

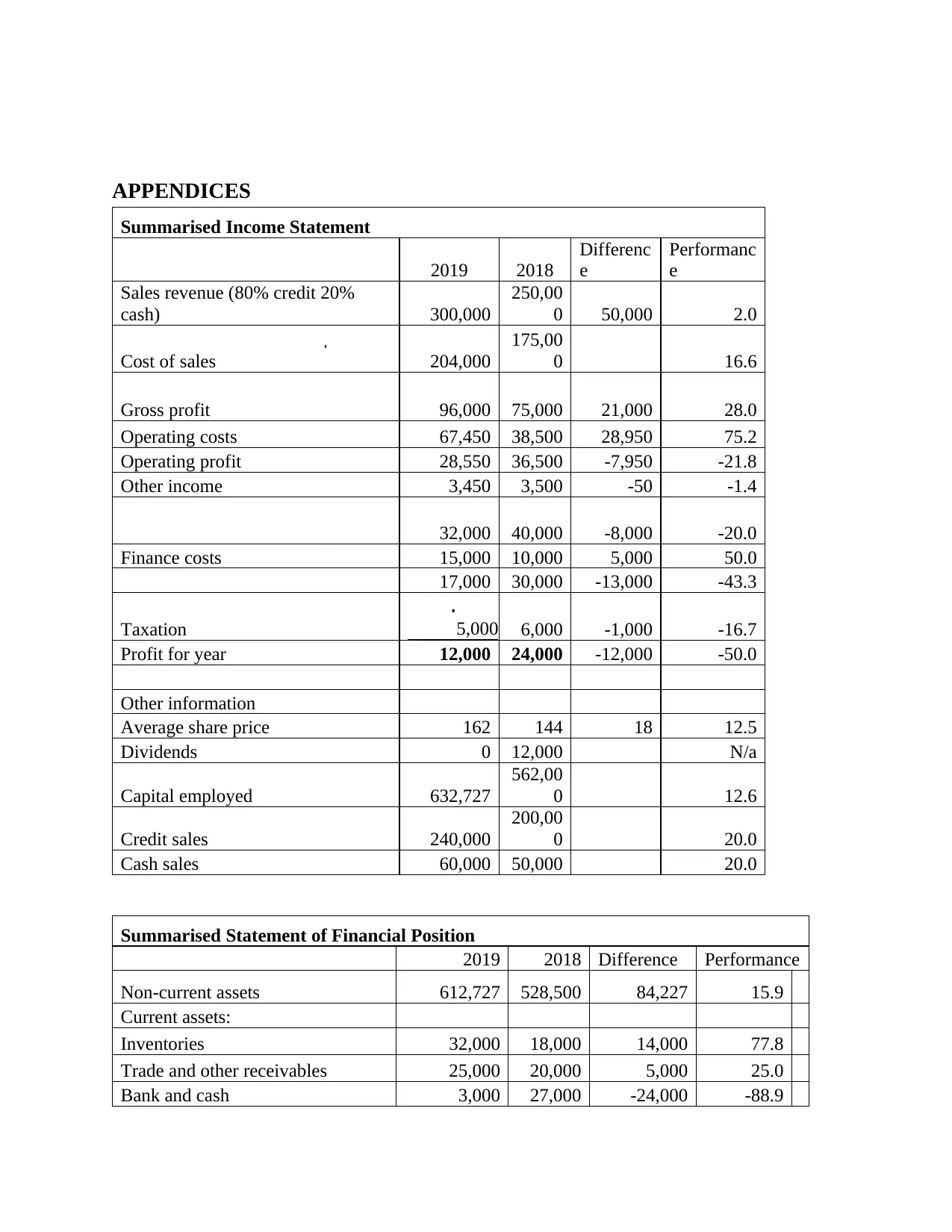

Summarized income statement: The main purpose is preparing of this statement to know net

profit in particular accounting period. The company prepares this statement for the year 2018 and

2019 and analysis the differences in both years. In the year, 2018 sales revenue was 250,000 and

in 2019 increase by 50000 reach on 300,000. The gross profit was 75000 in 2018 but increase in

2019 and calculated 96000 that show the performance 28.0. The operating profit was decreased

in 2019 as compare of 2018 due increase operating cost and notifies performance -21.8. After

deduction all the expenses, cost and taxation from the operating profit at the end of year get net

profit of the year which was 24000 in 2018 and 12000 in 2019. It denotes huge differences -

12000, and performance was -50.

Summarized statement of financial position: The main aim is preparing of this statement to

present actual financial position of company in particular year along with presents total assets

and total liabilities. The non-current assets were 528500 in 2018 that were increasing in 2019 by

84227 and reach on 612727 so identify the performance 15.9. Total assets of the company in

Finance represents the lifeline of any company. Finance, indeed, is still limited and so are

most other tools. Financial management is first component of the economic reporting

presentation. It is critical for any company that the finances it acquires are expended in such a

way that perhaps the profits from the expenditure are greater than financing costs. Financial

management is the method of business administration dedicated to a selective need for wealth

and an appropriate examination of the revenue source to encourage an expenditure department to

follow the path of achieving the objectives (Alsemgeest, 2015). This report based on

Rangemaster Plc which is a manufacturing company that produce and supply of catering

machine to hotel, restaurants and public services in United Kingdom. In this report analysis the

financial performance of company and identify the changes that are coming in 2019 as compare

of 2018. Along with focus on the financial ratio that accurately define the problem of the

business.

MAIN BODY

Summary of results

Summarized income statement: The main purpose is preparing of this statement to know net

profit in particular accounting period. The company prepares this statement for the year 2018 and

2019 and analysis the differences in both years. In the year, 2018 sales revenue was 250,000 and

in 2019 increase by 50000 reach on 300,000. The gross profit was 75000 in 2018 but increase in

2019 and calculated 96000 that show the performance 28.0. The operating profit was decreased

in 2019 as compare of 2018 due increase operating cost and notifies performance -21.8. After

deduction all the expenses, cost and taxation from the operating profit at the end of year get net

profit of the year which was 24000 in 2018 and 12000 in 2019. It denotes huge differences -

12000, and performance was -50.

Summarized statement of financial position: The main aim is preparing of this statement to

present actual financial position of company in particular year along with presents total assets

and total liabilities. The non-current assets were 528500 in 2018 that were increasing in 2019 by

84227 and reach on 612727 so identify the performance 15.9. Total assets of the company in

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2018 was 593500 and 2019 was 672,727. Thus, identify the differences was 79227 and

performance 13.3. On the other side liabilities, total liabilities was 131500 in 2018 and 190000 in

2019 so difference was 8500 and performance 27.0. Total equity of company 462000 in 2018

and 482727 in 2019 so the difference 20727 and performance was 4.5.

Analysis of each of the families of ratios

Profitability: Profitability ratios are a category of accounting measures which are calculated

across period to measure the capacity of a company to produce profits compared to its sales,

operational expenses, balance sheet resources and shareholders' equity, using information from a

particular duration period. Getting a greater valuation compared to a level comparable to the very

same ratio from an original period for certain financing activities shows that the business is

doing really well. Ratios are most insightful and beneficial when used to equate a commercial

area with other, comparable businesses, the corporation's own background, or the firm's

corporate business proportions overall (Das and Swain, 2018). In this ratio contain various types

of ratio and Rangemaster plc calculates the ratio to analysis the financial performance of the

company such as:

Return on capital employed: The return on capital employed (ROCE) is a financial

formula which can be used to measure the effectiveness and competitiveness of a business. In

other terms, the ratio will aid in understanding how leverage a business produces income in its

resources. The ROCE ratio has been one of the profitability ratios that could be used by

investment analysts, shareholders and prospective buyers when assessing a corporation for

development. As per the calculation it is analyzed that in 2018 capital employed was 6.5 but in

2019 decreased by -2.0 and reach on 4.5 that present the performance of company -2.0. These

changes are coming in this ratio due to changes in capital employed of the company.

Assets turnover: The asset turnover ratio tests the effectiveness of the company's assets

for income or sales production. This relates the profits or earnings in dollars to the overall assets.

The inventory turnover of assets computes generated from each dollar of their asset value. To

analysis the turnover of assets in business and identify 0.44 and 0.47 in 2018 & 2019

respectively. This ratio presents the performance 6.6.

performance 13.3. On the other side liabilities, total liabilities was 131500 in 2018 and 190000 in

2019 so difference was 8500 and performance 27.0. Total equity of company 462000 in 2018

and 482727 in 2019 so the difference 20727 and performance was 4.5.

Analysis of each of the families of ratios

Profitability: Profitability ratios are a category of accounting measures which are calculated

across period to measure the capacity of a company to produce profits compared to its sales,

operational expenses, balance sheet resources and shareholders' equity, using information from a

particular duration period. Getting a greater valuation compared to a level comparable to the very

same ratio from an original period for certain financing activities shows that the business is

doing really well. Ratios are most insightful and beneficial when used to equate a commercial

area with other, comparable businesses, the corporation's own background, or the firm's

corporate business proportions overall (Das and Swain, 2018). In this ratio contain various types

of ratio and Rangemaster plc calculates the ratio to analysis the financial performance of the

company such as:

Return on capital employed: The return on capital employed (ROCE) is a financial

formula which can be used to measure the effectiveness and competitiveness of a business. In

other terms, the ratio will aid in understanding how leverage a business produces income in its

resources. The ROCE ratio has been one of the profitability ratios that could be used by

investment analysts, shareholders and prospective buyers when assessing a corporation for

development. As per the calculation it is analyzed that in 2018 capital employed was 6.5 but in

2019 decreased by -2.0 and reach on 4.5 that present the performance of company -2.0. These

changes are coming in this ratio due to changes in capital employed of the company.

Assets turnover: The asset turnover ratio tests the effectiveness of the company's assets

for income or sales production. This relates the profits or earnings in dollars to the overall assets.

The inventory turnover of assets computes generated from each dollar of their asset value. To

analysis the turnover of assets in business and identify 0.44 and 0.47 in 2018 & 2019

respectively. This ratio presents the performance 6.6.

Gross profit: Also known as the Gross Profit Margin ratio, it provides a company's net

profit received and net operating income (net sales) produced. The gross profit margin is a

financial measure calculated as a proportion, and is thus multiplying the result by 100. Net sales,

on the other hand, include all card payment revenue; gross profit is measured as net sales minus

COGS. The gross profit ratio aims to analyze optimal sales rates and enhance the effectiveness of

economic activity (Dwiastanti, 2015). It also aims to sort out the least popular cost of goods per

product to the degree that a loss does not result for the company. As per the calculation it is

analyzing that 30% in 2018 and 32% in 2019. Due to increase gross profit of company in 2019

increase performance by 2% that present good position of the company.

Net operating profit: The operating margin calculates how often cash a company from a

dollar of earnings, after accounting for adjustable manufacturing costs, including such salaries

and manufactured goods, and just before making payments or taxes. It is computed by

subtracting the operating income of an organization by its net revenue. As per the computation it

is getting that 14.6% generate in 2018 whether 9.2% in 2019. It does not present good

performance of company in order to less operating profit.

Efficiency: Generally, the efficiency ratio is used to assess how efficiently an organization

effectively manages its resources and responsibilities. An output ratio can be used to measure the

receivables turnover, the redemption of liabilities, the volume and use of equity, and the overall

utilization of stock and machinery (Dzhandzhugazova and et.al, 2015). This ratio can also be

used to monitor and evaluate financial and commercial bank results. Experts use output ratios,

also named operation ratios, to monitor the effectiveness of the short-term or present quality of a

product. Both of these calculations utilize figures in the existing assets of a corporation or

interest expense, evaluating the economic activities.

Non-current assets turnover: Asset turnover ratio is the ratio between both the sum of

the profits or income of a corporation and the amount of its properties. This is an measure of the

efficiently a company deploys its assets to generate earnings the revenues. It tests the institution's

capacity to produce revenue in its company employees. A probable version is the profit margin

of intangible assets (revenue − non-current assets). This ratio calculate by company to analysis

the efficiency and as per the calculate it is analyzing that 0.47 in 2018 and 0.49 in 2019 so it

direct impact on the performance that identify 3.5 which is not good.

profit received and net operating income (net sales) produced. The gross profit margin is a

financial measure calculated as a proportion, and is thus multiplying the result by 100. Net sales,

on the other hand, include all card payment revenue; gross profit is measured as net sales minus

COGS. The gross profit ratio aims to analyze optimal sales rates and enhance the effectiveness of

economic activity (Dwiastanti, 2015). It also aims to sort out the least popular cost of goods per

product to the degree that a loss does not result for the company. As per the calculation it is

analyzing that 30% in 2018 and 32% in 2019. Due to increase gross profit of company in 2019

increase performance by 2% that present good position of the company.

Net operating profit: The operating margin calculates how often cash a company from a

dollar of earnings, after accounting for adjustable manufacturing costs, including such salaries

and manufactured goods, and just before making payments or taxes. It is computed by

subtracting the operating income of an organization by its net revenue. As per the computation it

is getting that 14.6% generate in 2018 whether 9.2% in 2019. It does not present good

performance of company in order to less operating profit.

Efficiency: Generally, the efficiency ratio is used to assess how efficiently an organization

effectively manages its resources and responsibilities. An output ratio can be used to measure the

receivables turnover, the redemption of liabilities, the volume and use of equity, and the overall

utilization of stock and machinery (Dzhandzhugazova and et.al, 2015). This ratio can also be

used to monitor and evaluate financial and commercial bank results. Experts use output ratios,

also named operation ratios, to monitor the effectiveness of the short-term or present quality of a

product. Both of these calculations utilize figures in the existing assets of a corporation or

interest expense, evaluating the economic activities.

Non-current assets turnover: Asset turnover ratio is the ratio between both the sum of

the profits or income of a corporation and the amount of its properties. This is an measure of the

efficiently a company deploys its assets to generate earnings the revenues. It tests the institution's

capacity to produce revenue in its company employees. A probable version is the profit margin

of intangible assets (revenue − non-current assets). This ratio calculate by company to analysis

the efficiency and as per the calculate it is analyzing that 0.47 in 2018 and 0.49 in 2019 so it

direct impact on the performance that identify 3.5 which is not good.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Inventory turnover: Inventory turnover is a measure that indicates how often years a

company owns and position update in a specified timeframe. A firm will then multiply the times

by the inventory turnover equation in the timeframe to measure the days it sells directly to its

customer on board. In the year 2018, 37.5 turnover of inventory and 57.3 in the year 2019. It is

not presenting good for business and this change come in the company due to sale out and

purchase assets. Due to come changes in sales impact on the calculation in direct manner.

Liquidity: The word liquidity is characterized as an organization to meet its payment

commitments whenever due. Therefore, the liquidity ratio is a calculation used to calculate the

capacity of a firm to pay its quick-term liabilities. There are 3 main formulas which fall

underneath the liquidity ratio classification. The present ratio of the three is by far the most

progressive. Acid ratio follows, and cash ratio follows. When trying to reliably calculate a firm's

liquidity, such three measures are frequently clustered together via money managers (Florido,

Adame and Tagle, 2015). Liquidity ratios are an essential category of financial indicators used to

evaluate the efficacy of a borrower to repay existing debt while requiring outside assets.

Liquidity ratios calculate the willingness of a business to meet debt obligations and their margin

of safety by measuring indicators like current ratio, rapid ratio and cash conversion cycle.

Current ratio: The current ratio is a financial ratio, which calculates the ability of the firm to

meet short-term or unpaid commitments in one period. This shows shareholders how a firm can

optimize its helps users of financial statements position to pay its gross obligations and other

current liabilities (Valaskova, Kliestik and Kovacova, 2018). From the calculation it is saying

that in the year meets with the ideal ratio 2.1 in 2018 and in the 2019 reach on 1.5 and did not

meet with the ideal ratio which is 2:1. These changes are coming in this ratio changes in current

assets and current liabilities. It presents effect on performance in negative manner -28.6.

Acid test: As per the analysis it is understand that in the year 2018 get 1.5 and in 2019 0.7 which

is not presenting good liquidity position. In the year 2019 did not meet with the ideal ratio which

is 1:1.

Creditor’s days: When company takes loan from the outsider so require paying off in particular

time period. In 2018 creditor day 65.7 days but it increase in 2019 was 71.6 days which is

increased for company and good for the company.

company owns and position update in a specified timeframe. A firm will then multiply the times

by the inventory turnover equation in the timeframe to measure the days it sells directly to its

customer on board. In the year 2018, 37.5 turnover of inventory and 57.3 in the year 2019. It is

not presenting good for business and this change come in the company due to sale out and

purchase assets. Due to come changes in sales impact on the calculation in direct manner.

Liquidity: The word liquidity is characterized as an organization to meet its payment

commitments whenever due. Therefore, the liquidity ratio is a calculation used to calculate the

capacity of a firm to pay its quick-term liabilities. There are 3 main formulas which fall

underneath the liquidity ratio classification. The present ratio of the three is by far the most

progressive. Acid ratio follows, and cash ratio follows. When trying to reliably calculate a firm's

liquidity, such three measures are frequently clustered together via money managers (Florido,

Adame and Tagle, 2015). Liquidity ratios are an essential category of financial indicators used to

evaluate the efficacy of a borrower to repay existing debt while requiring outside assets.

Liquidity ratios calculate the willingness of a business to meet debt obligations and their margin

of safety by measuring indicators like current ratio, rapid ratio and cash conversion cycle.

Current ratio: The current ratio is a financial ratio, which calculates the ability of the firm to

meet short-term or unpaid commitments in one period. This shows shareholders how a firm can

optimize its helps users of financial statements position to pay its gross obligations and other

current liabilities (Valaskova, Kliestik and Kovacova, 2018). From the calculation it is saying

that in the year meets with the ideal ratio 2.1 in 2018 and in the 2019 reach on 1.5 and did not

meet with the ideal ratio which is 2:1. These changes are coming in this ratio changes in current

assets and current liabilities. It presents effect on performance in negative manner -28.6.

Acid test: As per the analysis it is understand that in the year 2018 get 1.5 and in 2019 0.7 which

is not presenting good liquidity position. In the year 2019 did not meet with the ideal ratio which

is 1:1.

Creditor’s days: When company takes loan from the outsider so require paying off in particular

time period. In 2018 creditor day 65.7 days but it increase in 2019 was 71.6 days which is

increased for company and good for the company.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Debtor’s days: The Company collects the amount from the debtors and for this set the specific

time frame. In 2018 debtor time period were 36.5 and in 2019 increase 38 which s not good for

the company. Due to increase days company collect amount late that impact on the interest and

others payment activities directly (Hussain, Salia and Karim, 2018).

Capital structure: This ratio is the fundamental measure of capital structure, which is measured

mostly during balance sheet portion of the horizontal examination of the obligations. It's being

used to test the quality of the equality and economic as regards overseas investment. The greater

the score, the stronger the corporate accounting position and thus improve the organization's

solvency and financial health (increased debt feel increasingly the potential to incur new liability

in the long term). If the value of the standard is small, review of the corporate profitability is

advised to test the explanations for high levels of debt: higher long-term debt influences the

financial health, whereas higher quick-term debt influences investment capacity.

Debt to equity: This ratio calculation presents that 21.6 in 2018 and 31.1 in 2019 and the

changes in ratio based on the debtors and equity of the company.

Debt to capital: This ratio based on the debt and capital of the company and in 2018 it is

calculated 17.8 and in 2019 23.7. These changes impact on the performance and identify 5.9 in

the business.

Interest cover: The interest coverage ratio is used to determine how often magnitudes an

enterprise including its accessible income can handle its existing loan repayments (Kinyua,

Mwangi and Riro, 2015). The ratio is computed by subtracting profits of a business until taxes

and interest (EBIT) by interest expenditures of the business for much the same duration. From

the calculation of this ratio analysis that how many times covers interest and gets that in 2018

was 3.6 and n 2019 was 1.9.

Investments: The investment benefit ratio is the ratio of the total equity profits of an insurance

firm to the paid bonuses. The investment benefit ratio measures the profits an insurance agency

receives from its bank lending instead of from its activities. This is used to assess one

compensation firm’s profitability. Investment measures used to measure the effectiveness of a

company's assets, such as the profit ratio, operating income and profits rate. While also being of

time frame. In 2018 debtor time period were 36.5 and in 2019 increase 38 which s not good for

the company. Due to increase days company collect amount late that impact on the interest and

others payment activities directly (Hussain, Salia and Karim, 2018).

Capital structure: This ratio is the fundamental measure of capital structure, which is measured

mostly during balance sheet portion of the horizontal examination of the obligations. It's being

used to test the quality of the equality and economic as regards overseas investment. The greater

the score, the stronger the corporate accounting position and thus improve the organization's

solvency and financial health (increased debt feel increasingly the potential to incur new liability

in the long term). If the value of the standard is small, review of the corporate profitability is

advised to test the explanations for high levels of debt: higher long-term debt influences the

financial health, whereas higher quick-term debt influences investment capacity.

Debt to equity: This ratio calculation presents that 21.6 in 2018 and 31.1 in 2019 and the

changes in ratio based on the debtors and equity of the company.

Debt to capital: This ratio based on the debt and capital of the company and in 2018 it is

calculated 17.8 and in 2019 23.7. These changes impact on the performance and identify 5.9 in

the business.

Interest cover: The interest coverage ratio is used to determine how often magnitudes an

enterprise including its accessible income can handle its existing loan repayments (Kinyua,

Mwangi and Riro, 2015). The ratio is computed by subtracting profits of a business until taxes

and interest (EBIT) by interest expenditures of the business for much the same duration. From

the calculation of this ratio analysis that how many times covers interest and gets that in 2018

was 3.6 and n 2019 was 1.9.

Investments: The investment benefit ratio is the ratio of the total equity profits of an insurance

firm to the paid bonuses. The investment benefit ratio measures the profits an insurance agency

receives from its bank lending instead of from its activities. This is used to assess one

compensation firm’s profitability. Investment measures used to measure the effectiveness of a

company's assets, such as the profit ratio, operating income and profits rate. While also being of

significant concern to the common stockholders, valuation ratios are of concern to prospective

buyers, consultants and rivals as well.

Earnings per share: As per the calculation of this ratio it is analyzing that in the year 2018

generate earnings 8.0 and in 2019 generate 4.0.

Price earnings ratio: Essentially, the price-to-profits ratio shows the total sum that a shareholder

would plan to pay in a product to promote one total of the profits from that company

(Linnerooth-Bayer and Hochrainer-Stigler, 2015). That's why the P / E are often called the

variable quality, since it indicates how much shareholders are paying per dollar of income. After

the calculation of this ratio get results 18.0 and 40.5 in 2018 & 2019 respectively.

Dividends per share: Dividend per share ( DPS) is the amount of declared dividends for every

outstanding common share issued by a corporation. The estimate is measured by deducting over

an amount of time the maximum payments made by an enterprise such as stock dividends by the

weighted average amount of ordinary share capital. The company gives dividends to

shareholders on their share and for this calculate dividend every year which was 4 in 2018 and in

2019 did not allocate any dividend due to face many losses.

Dividends percentage payout: The payout ratio for dividends is the aggregate amount of

dividends per share comparable to the firm's total revenue (Morozko and Didenko, 2018). It is

the proportion of earnings income invested by shareholders. From the calculation it is getting

that percentage payout 50 in 2018 and no payout in 2019.

CONCLUSION

As per the above report it has been concluded that in a business conduct various types of

financial activities that manage by the business in systematic manner. Financial management is

the operation involved in designing, collecting, managing and maintaining the resources used

throughout the enterprise. Calculating turnover ratio can allow clients make more informed

decisions about pricing, manufacturing, marketing and available stock purchases. Due to low

liquidity position in 2019 face problem of pay off short term debt. For the improvement require

to arrange funds to maintain liquidity in business. A healthy debt-to - equity ratio is between

around 1 and 1.5. The optimal debt-to - equity ratio, nevertheless, can differ vary by industry, as

buyers, consultants and rivals as well.

Earnings per share: As per the calculation of this ratio it is analyzing that in the year 2018

generate earnings 8.0 and in 2019 generate 4.0.

Price earnings ratio: Essentially, the price-to-profits ratio shows the total sum that a shareholder

would plan to pay in a product to promote one total of the profits from that company

(Linnerooth-Bayer and Hochrainer-Stigler, 2015). That's why the P / E are often called the

variable quality, since it indicates how much shareholders are paying per dollar of income. After

the calculation of this ratio get results 18.0 and 40.5 in 2018 & 2019 respectively.

Dividends per share: Dividend per share ( DPS) is the amount of declared dividends for every

outstanding common share issued by a corporation. The estimate is measured by deducting over

an amount of time the maximum payments made by an enterprise such as stock dividends by the

weighted average amount of ordinary share capital. The company gives dividends to

shareholders on their share and for this calculate dividend every year which was 4 in 2018 and in

2019 did not allocate any dividend due to face many losses.

Dividends percentage payout: The payout ratio for dividends is the aggregate amount of

dividends per share comparable to the firm's total revenue (Morozko and Didenko, 2018). It is

the proportion of earnings income invested by shareholders. From the calculation it is getting

that percentage payout 50 in 2018 and no payout in 2019.

CONCLUSION

As per the above report it has been concluded that in a business conduct various types of

financial activities that manage by the business in systematic manner. Financial management is

the operation involved in designing, collecting, managing and maintaining the resources used

throughout the enterprise. Calculating turnover ratio can allow clients make more informed

decisions about pricing, manufacturing, marketing and available stock purchases. Due to low

liquidity position in 2019 face problem of pay off short term debt. For the improvement require

to arrange funds to maintain liquidity in business. A healthy debt-to - equity ratio is between

around 1 and 1.5. The optimal debt-to - equity ratio, nevertheless, can differ vary by industry, as

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

some businesses use much more debt funding than others. Capital-intensive industries such as

the economic and industrial sectors often have higher percentages, which may exceed 2. The

company tries to generate more profitability to pay dividend to shareholders and for this set

effective brand image of the company. For this improvements require to in the perspective of a

dividend shareholder, a level of 35 per cent to 55 per cent is considered safe and acceptable. A

business that is expected to pay about half of its profits as dividends shows the business is very

well known and a growing market. A business with a strong earnings per share is possible to

manufacture a considerable profit for shareholders, or it could pouching the money directly into

its sector for further development; in either case, a high ratio implies a possibly wise investment,

dependent on the stock prices.

the economic and industrial sectors often have higher percentages, which may exceed 2. The

company tries to generate more profitability to pay dividend to shareholders and for this set

effective brand image of the company. For this improvements require to in the perspective of a

dividend shareholder, a level of 35 per cent to 55 per cent is considered safe and acceptable. A

business that is expected to pay about half of its profits as dividends shows the business is very

well known and a growing market. A business with a strong earnings per share is possible to

manufacture a considerable profit for shareholders, or it could pouching the money directly into

its sector for further development; in either case, a high ratio implies a possibly wise investment,

dependent on the stock prices.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journal

Alsemgeest, L., 2015. Arguments for and against financial literacy education: where to go from

here?. International Journal of Consumer Studies. 39(2). pp.155-161.

Das, C. P. and Swain, R. K., 2018. Influence of capital structure on financial

performance. Parikalpana: KIIT Journal of Management. 14(1). pp.161-171.

Dwiastanti, A., 2015. Financial Literacy as the Foundation for Individual Financial

Behavior. Journal of Education and Practice. 6(33). pp.99-105.

Dzhandzhugazova, E. A. and et.al, 2015. Chaplyuk, VZ Methodological aspects of strategic

management of financial risks during construction of hotel business objects. Asian Social

Science. 11(20). pp.229-234.

Florido, J. S. V., Adame, M. G. and Tagle, M. A. O., 2015. Financial Strategies, the Professional

Development of Employers and Performance of SME's (AGUASCALIENTES

case). Procedia-Social and Behavioral Sciences. 174. pp.768-775.

Hussain, J., Salia, S. and Karim, A., 2018. Is knowledge that powerful? Financial literacy and

access to finance. Journal of Small Business and Enterprise Development.

Kinyua, M. M., Mwangi, A. W. and Riro, G. K., 2015. Financial Management Aspect on

Sustainability of Community Managed Water Projects in Kieni West District, Nyeri

County, Kenya.

Linnerooth-Bayer, J. and Hochrainer-Stigler, S., 2015. Financial instruments for disaster risk

management and climate change adaptation. Climatic Change. 133(1). pp.85-100.

Morozko, N. and Didenko, V., 2018. Financial management of small organizations based on a

cognitive approach.

Valaskova, K., Kliestik, T. and Kovacova, M., 2018. Management of financial risks in Slovak

enterprises using regression analysis. Oeconomia Copernicana. 9(1). pp.105-121.

Books and Journal

Alsemgeest, L., 2015. Arguments for and against financial literacy education: where to go from

here?. International Journal of Consumer Studies. 39(2). pp.155-161.

Das, C. P. and Swain, R. K., 2018. Influence of capital structure on financial

performance. Parikalpana: KIIT Journal of Management. 14(1). pp.161-171.

Dwiastanti, A., 2015. Financial Literacy as the Foundation for Individual Financial

Behavior. Journal of Education and Practice. 6(33). pp.99-105.

Dzhandzhugazova, E. A. and et.al, 2015. Chaplyuk, VZ Methodological aspects of strategic

management of financial risks during construction of hotel business objects. Asian Social

Science. 11(20). pp.229-234.

Florido, J. S. V., Adame, M. G. and Tagle, M. A. O., 2015. Financial Strategies, the Professional

Development of Employers and Performance of SME's (AGUASCALIENTES

case). Procedia-Social and Behavioral Sciences. 174. pp.768-775.

Hussain, J., Salia, S. and Karim, A., 2018. Is knowledge that powerful? Financial literacy and

access to finance. Journal of Small Business and Enterprise Development.

Kinyua, M. M., Mwangi, A. W. and Riro, G. K., 2015. Financial Management Aspect on

Sustainability of Community Managed Water Projects in Kieni West District, Nyeri

County, Kenya.

Linnerooth-Bayer, J. and Hochrainer-Stigler, S., 2015. Financial instruments for disaster risk

management and climate change adaptation. Climatic Change. 133(1). pp.85-100.

Morozko, N. and Didenko, V., 2018. Financial management of small organizations based on a

cognitive approach.

Valaskova, K., Kliestik, T. and Kovacova, M., 2018. Management of financial risks in Slovak

enterprises using regression analysis. Oeconomia Copernicana. 9(1). pp.105-121.

APPENDICES

Summarised Income Statement

2019 2018

Differenc

e

Performanc

e

Sales revenue (80% credit 20%

cash) 300,000

250,00

0 50,000 2.0

Cost of sales 204,000

175,00

0 16.6

Gross profit 96,000 75,000 21,000 28.0

Operating costs 67,450 38,500 28,950 75.2

Operating profit 28,550 36,500 -7,950 -21.8

Other income 3,450 3,500 -50 -1.4

32,000 40,000 -8,000 -20.0

Finance costs 15,000 10,000 5,000 50.0

17,000 30,000 -13,000 -43.3

Taxation 5,000 6,000 -1,000 -16.7

Profit for year 12,000 24,000 -12,000 -50.0

Other information

Average share price 162 144 18 12.5

Dividends 0 12,000 N/a

Capital employed 632,727

562,00

0 12.6

Credit sales 240,000

200,00

0 20.0

Cash sales 60,000 50,000 20.0

Summarised Statement of Financial Position

2019 2018 Difference Performance

Non-current assets 612,727 528,500 84,227 15.9

Current assets:

Inventories 32,000 18,000 14,000 77.8

Trade and other receivables 25,000 20,000 5,000 25.0

Bank and cash 3,000 27,000 -24,000 -88.9

Summarised Income Statement

2019 2018

Differenc

e

Performanc

e

Sales revenue (80% credit 20%

cash) 300,000

250,00

0 50,000 2.0

Cost of sales 204,000

175,00

0 16.6

Gross profit 96,000 75,000 21,000 28.0

Operating costs 67,450 38,500 28,950 75.2

Operating profit 28,550 36,500 -7,950 -21.8

Other income 3,450 3,500 -50 -1.4

32,000 40,000 -8,000 -20.0

Finance costs 15,000 10,000 5,000 50.0

17,000 30,000 -13,000 -43.3

Taxation 5,000 6,000 -1,000 -16.7

Profit for year 12,000 24,000 -12,000 -50.0

Other information

Average share price 162 144 18 12.5

Dividends 0 12,000 N/a

Capital employed 632,727

562,00

0 12.6

Credit sales 240,000

200,00

0 20.0

Cash sales 60,000 50,000 20.0

Summarised Statement of Financial Position

2019 2018 Difference Performance

Non-current assets 612,727 528,500 84,227 15.9

Current assets:

Inventories 32,000 18,000 14,000 77.8

Trade and other receivables 25,000 20,000 5,000 25.0

Bank and cash 3,000 27,000 -24,000 -88.9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.