Ratio Analysis, Budgeting & Financial Decision Making: A Report

VerifiedAdded on 2023/06/10

|19

|3811

|467

Report

AI Summary

This report provides a comprehensive analysis of accounting and finance principles, focusing on financial ratio analysis, budgeting, and capital budgeting techniques. It begins by calculating and interpreting various financial ratios for Trust PLC, including profitability, efficiency, liquidity, investment, and financial structure ratios, to assess the company's financial health and performance. The report then analyzes the objectives of budgeting for Manor Ltd and differentiates between management and financial accounting. Furthermore, it evaluates two projects, A and B, using the Net Present Value (NPV) and payback period methods, ultimately recommending project A based on its superior financial metrics. The analysis aims to provide insights for strategic decision-making and highlights the importance of sound financial management in achieving organizational objectives. This document is available on Desklib, a platform offering a wide range of study tools and solved assignments for students.

INTRODUCTION TO

ACCOUNTING &

FINANCE

1

ACCOUNTING &

FINANCE

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2

Abstract

Accounting and finance is crucial for making the strategic decision. Financial

ratio is considered to be the metrics that allow the investors and other stakeholders to

analyse the financial performance of the organisation. Budgeting is a very important

factor for any organization to be able to plan the financial activities. The different

between the management accounting and financial accounting is that management

accounting is helpful for the organisation and its competitors for the analysation of

trends and performance whereas, financial accounting is requirement of the

organisation for meeting the corporate governance. The current study has involved

calculation of project A & B by involving NPV and payback period method of capital

budgeting which is depicting that project A is beneficial.

3

Accounting and finance is crucial for making the strategic decision. Financial

ratio is considered to be the metrics that allow the investors and other stakeholders to

analyse the financial performance of the organisation. Budgeting is a very important

factor for any organization to be able to plan the financial activities. The different

between the management accounting and financial accounting is that management

accounting is helpful for the organisation and its competitors for the analysation of

trends and performance whereas, financial accounting is requirement of the

organisation for meeting the corporate governance. The current study has involved

calculation of project A & B by involving NPV and payback period method of capital

budgeting which is depicting that project A is beneficial.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

TABLE OF CONTENTS

INTRODUCTION..........................................................................................................................4

MAIN BODY..................................................................................................................................4

SECTION A...................................................................................................................................4

Profitability Ratios................................................................................................................4

Efficiency ratios.....................................................................................................................6

Liquidity Ratios......................................................................................................................8

Investment ratios...............................................................................................................10

Financial Structure ratios................................................................................................11

SECTION B.................................................................................................................................13

Analysing objectives of budgeting for Manor Ltd...................................................13

Differences between financial and management accounting...........................13

3................................................................................................................................................14

a) Payback Period for the projects A & B..................................................................14

b) calculating the Net Present Value for the projects A & B..............................15

c) Explaining reason for selecting the project.........................................................16

CONCLUSION............................................................................................................................17

REFERENCES............................................................................................................................18

4

INTRODUCTION..........................................................................................................................4

MAIN BODY..................................................................................................................................4

SECTION A...................................................................................................................................4

Profitability Ratios................................................................................................................4

Efficiency ratios.....................................................................................................................6

Liquidity Ratios......................................................................................................................8

Investment ratios...............................................................................................................10

Financial Structure ratios................................................................................................11

SECTION B.................................................................................................................................13

Analysing objectives of budgeting for Manor Ltd...................................................13

Differences between financial and management accounting...........................13

3................................................................................................................................................14

a) Payback Period for the projects A & B..................................................................14

b) calculating the Net Present Value for the projects A & B..............................15

c) Explaining reason for selecting the project.........................................................16

CONCLUSION............................................................................................................................17

REFERENCES............................................................................................................................18

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

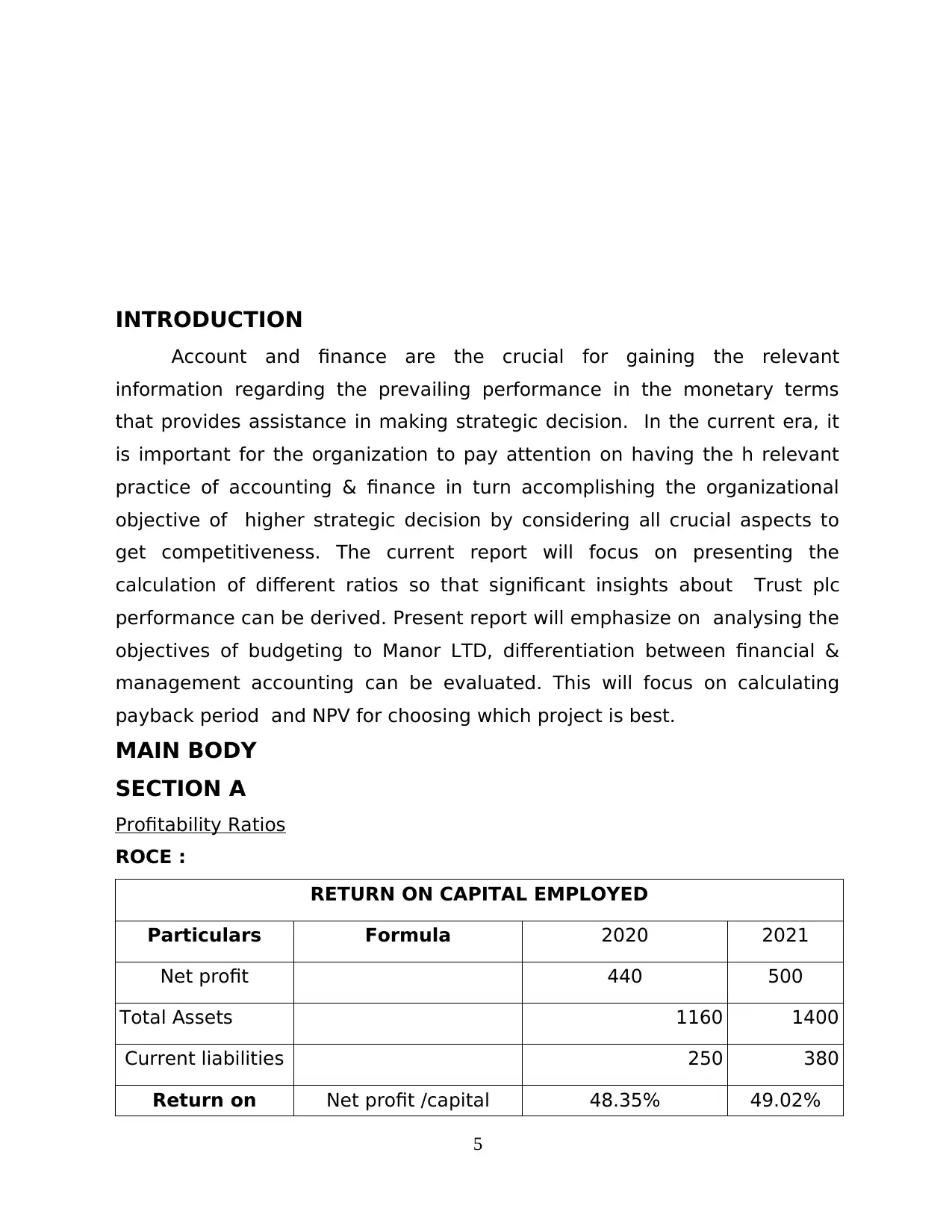

INTRODUCTION

Account and finance are the crucial for gaining the relevant

information regarding the prevailing performance in the monetary terms

that provides assistance in making strategic decision. In the current era, it

is important for the organization to pay attention on having the h relevant

practice of accounting & finance in turn accomplishing the organizational

objective of higher strategic decision by considering all crucial aspects to

get competitiveness. The current report will focus on presenting the

calculation of different ratios so that significant insights about Trust plc

performance can be derived. Present report will emphasize on analysing the

objectives of budgeting to Manor LTD, differentiation between financial &

management accounting can be evaluated. This will focus on calculating

payback period and NPV for choosing which project is best.

MAIN BODY

SECTION A

Profitability Ratios

ROCE :

RETURN ON CAPITAL EMPLOYED

Particulars Formula 2020 2021

Net profit 440 500

Total Assets 1160 1400

Current liabilities 250 380

Return on Net profit /capital 48.35% 49.02%

5

Account and finance are the crucial for gaining the relevant

information regarding the prevailing performance in the monetary terms

that provides assistance in making strategic decision. In the current era, it

is important for the organization to pay attention on having the h relevant

practice of accounting & finance in turn accomplishing the organizational

objective of higher strategic decision by considering all crucial aspects to

get competitiveness. The current report will focus on presenting the

calculation of different ratios so that significant insights about Trust plc

performance can be derived. Present report will emphasize on analysing the

objectives of budgeting to Manor LTD, differentiation between financial &

management accounting can be evaluated. This will focus on calculating

payback period and NPV for choosing which project is best.

MAIN BODY

SECTION A

Profitability Ratios

ROCE :

RETURN ON CAPITAL EMPLOYED

Particulars Formula 2020 2021

Net profit 440 500

Total Assets 1160 1400

Current liabilities 250 380

Return on Net profit /capital 48.35% 49.02%

5

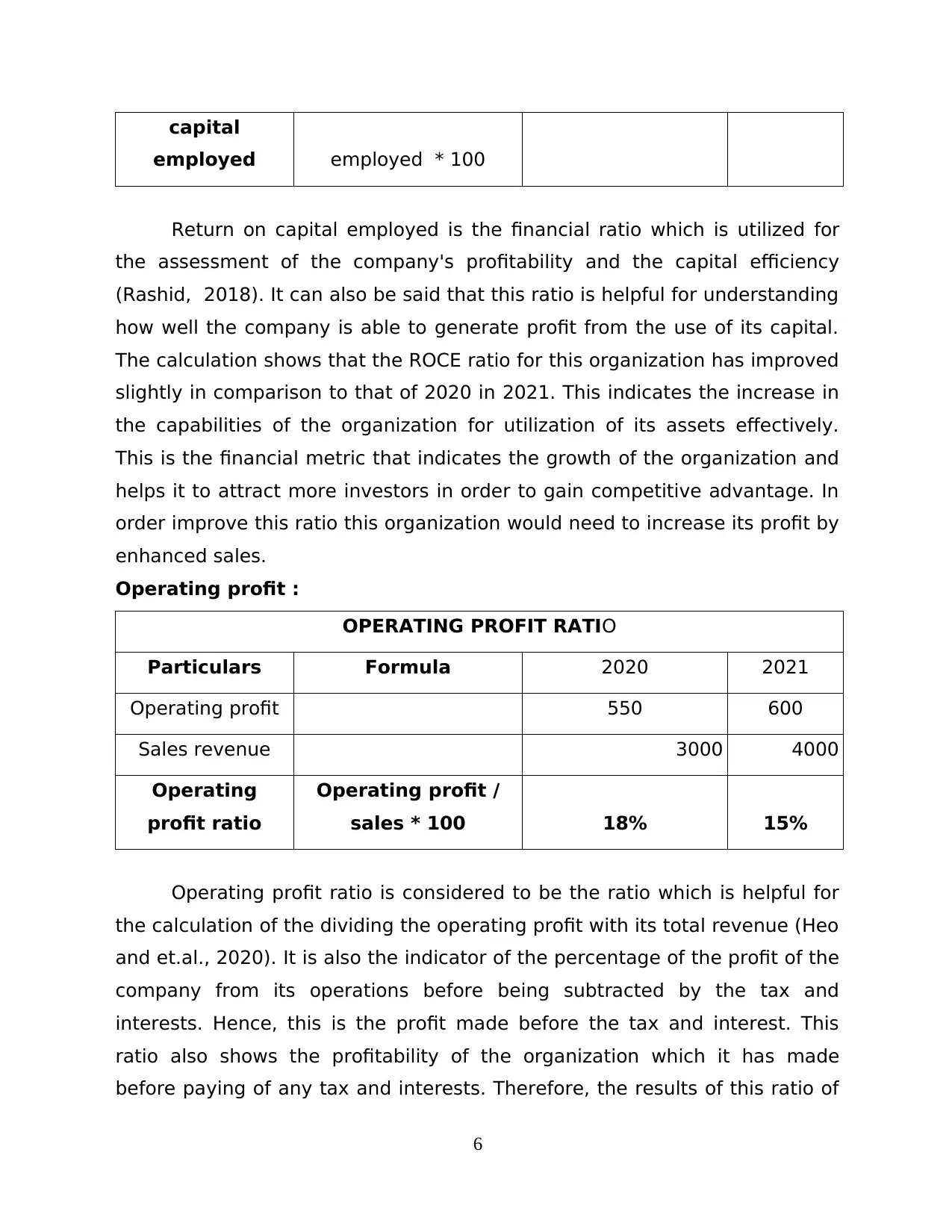

capital

employed employed * 100

Return on capital employed is the financial ratio which is utilized for

the assessment of the company's profitability and the capital efficiency

(Rashid, 2018). It can also be said that this ratio is helpful for understanding

how well the company is able to generate profit from the use of its capital.

The calculation shows that the ROCE ratio for this organization has improved

slightly in comparison to that of 2020 in 2021. This indicates the increase in

the capabilities of the organization for utilization of its assets effectively.

This is the financial metric that indicates the growth of the organization and

helps it to attract more investors in order to gain competitive advantage. In

order improve this ratio this organization would need to increase its profit by

enhanced sales.

Operating profit :

OPERATING PROFIT RATIO

Particulars Formula 2020 2021

Operating profit 550 600

Sales revenue 3000 4000

Operating

profit ratio

Operating profit /

sales * 100 18% 15%

Operating profit ratio is considered to be the ratio which is helpful for

the calculation of the dividing the operating profit with its total revenue (Heo

and et.al., 2020). It is also the indicator of the percentage of the profit of the

company from its operations before being subtracted by the tax and

interests. Hence, this is the profit made before the tax and interest. This

ratio also shows the profitability of the organization which it has made

before paying of any tax and interests. Therefore, the results of this ratio of

6

employed employed * 100

Return on capital employed is the financial ratio which is utilized for

the assessment of the company's profitability and the capital efficiency

(Rashid, 2018). It can also be said that this ratio is helpful for understanding

how well the company is able to generate profit from the use of its capital.

The calculation shows that the ROCE ratio for this organization has improved

slightly in comparison to that of 2020 in 2021. This indicates the increase in

the capabilities of the organization for utilization of its assets effectively.

This is the financial metric that indicates the growth of the organization and

helps it to attract more investors in order to gain competitive advantage. In

order improve this ratio this organization would need to increase its profit by

enhanced sales.

Operating profit :

OPERATING PROFIT RATIO

Particulars Formula 2020 2021

Operating profit 550 600

Sales revenue 3000 4000

Operating

profit ratio

Operating profit /

sales * 100 18% 15%

Operating profit ratio is considered to be the ratio which is helpful for

the calculation of the dividing the operating profit with its total revenue (Heo

and et.al., 2020). It is also the indicator of the percentage of the profit of the

company from its operations before being subtracted by the tax and

interests. Hence, this is the profit made before the tax and interest. This

ratio also shows the profitability of the organization which it has made

before paying of any tax and interests. Therefore, the results of this ratio of

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

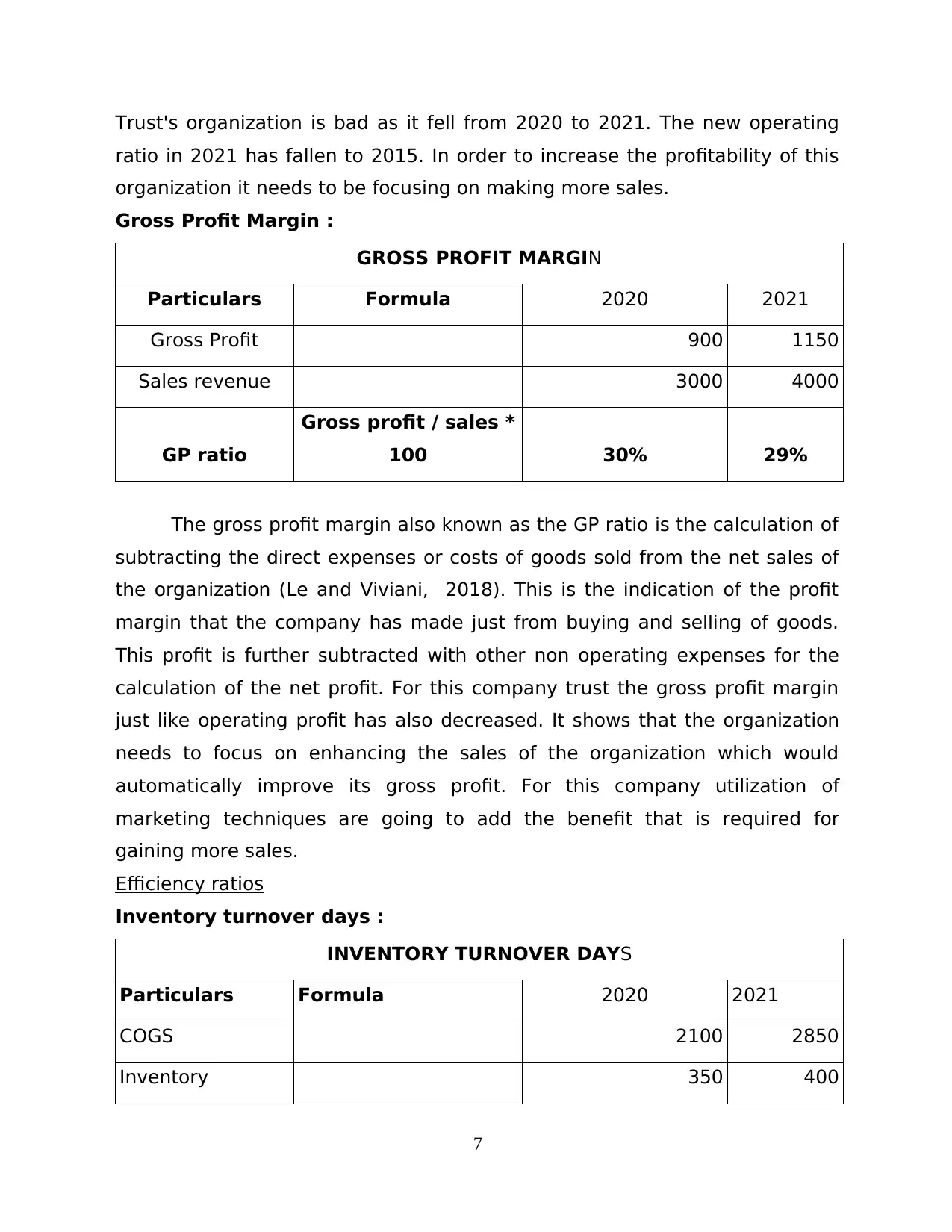

Trust's organization is bad as it fell from 2020 to 2021. The new operating

ratio in 2021 has fallen to 2015. In order to increase the profitability of this

organization it needs to be focusing on making more sales.

Gross Profit Margin :

GROSS PROFIT MARGIN

Particulars Formula 2020 2021

Gross Profit 900 1150

Sales revenue 3000 4000

GP ratio

Gross profit / sales *

100 30% 29%

The gross profit margin also known as the GP ratio is the calculation of

subtracting the direct expenses or costs of goods sold from the net sales of

the organization (Le and Viviani, 2018). This is the indication of the profit

margin that the company has made just from buying and selling of goods.

This profit is further subtracted with other non operating expenses for the

calculation of the net profit. For this company trust the gross profit margin

just like operating profit has also decreased. It shows that the organization

needs to focus on enhancing the sales of the organization which would

automatically improve its gross profit. For this company utilization of

marketing techniques are going to add the benefit that is required for

gaining more sales.

Efficiency ratios

Inventory turnover days :

INVENTORY TURNOVER DAYS

Particulars Formula 2020 2021

COGS 2100 2850

Inventory 350 400

7

ratio in 2021 has fallen to 2015. In order to increase the profitability of this

organization it needs to be focusing on making more sales.

Gross Profit Margin :

GROSS PROFIT MARGIN

Particulars Formula 2020 2021

Gross Profit 900 1150

Sales revenue 3000 4000

GP ratio

Gross profit / sales *

100 30% 29%

The gross profit margin also known as the GP ratio is the calculation of

subtracting the direct expenses or costs of goods sold from the net sales of

the organization (Le and Viviani, 2018). This is the indication of the profit

margin that the company has made just from buying and selling of goods.

This profit is further subtracted with other non operating expenses for the

calculation of the net profit. For this company trust the gross profit margin

just like operating profit has also decreased. It shows that the organization

needs to focus on enhancing the sales of the organization which would

automatically improve its gross profit. For this company utilization of

marketing techniques are going to add the benefit that is required for

gaining more sales.

Efficiency ratios

Inventory turnover days :

INVENTORY TURNOVER DAYS

Particulars Formula 2020 2021

COGS 2100 2850

Inventory 350 400

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

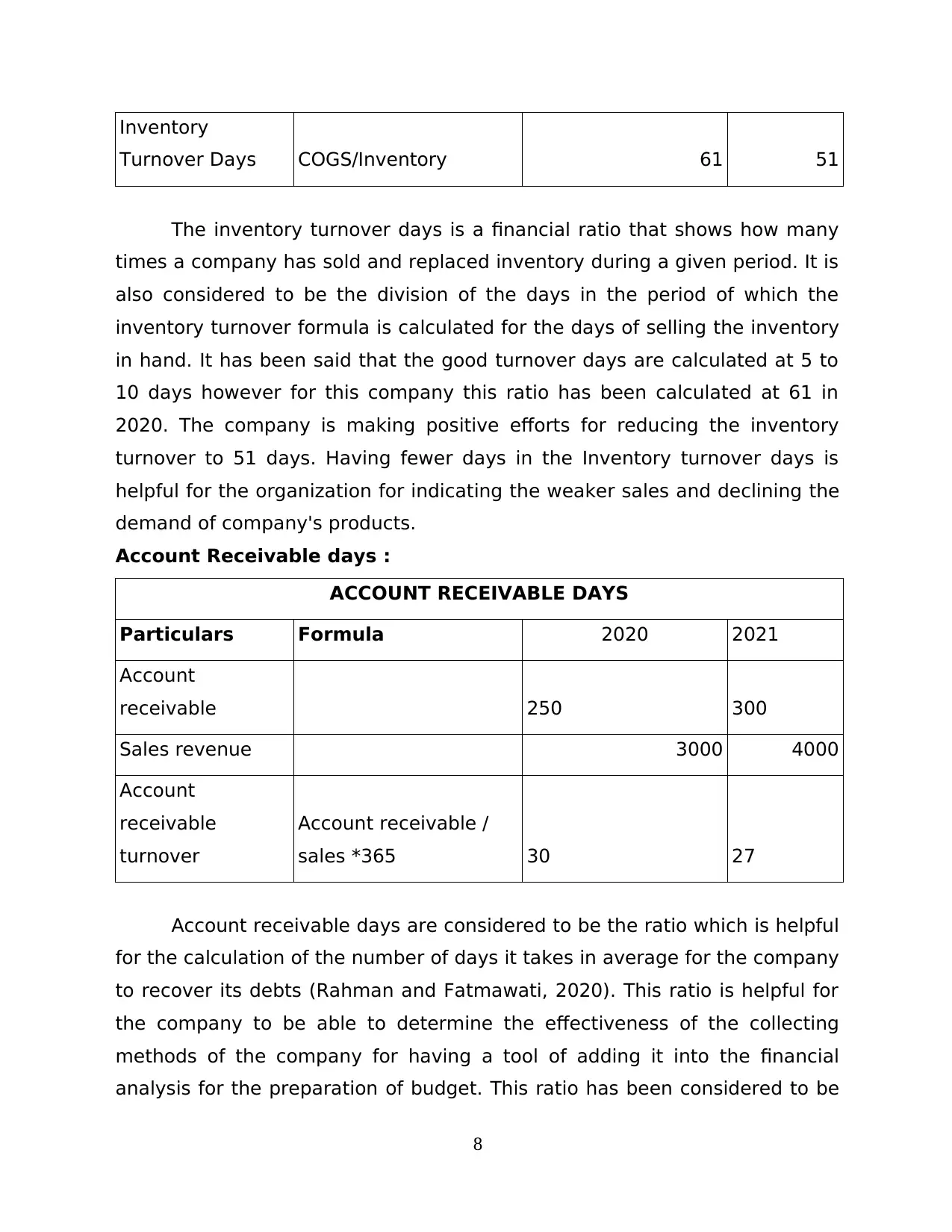

Inventory

Turnover Days COGS/Inventory 61 51

The inventory turnover days is a financial ratio that shows how many

times a company has sold and replaced inventory during a given period. It is

also considered to be the division of the days in the period of which the

inventory turnover formula is calculated for the days of selling the inventory

in hand. It has been said that the good turnover days are calculated at 5 to

10 days however for this company this ratio has been calculated at 61 in

2020. The company is making positive efforts for reducing the inventory

turnover to 51 days. Having fewer days in the Inventory turnover days is

helpful for the organization for indicating the weaker sales and declining the

demand of company's products.

Account Receivable days :

ACCOUNT RECEIVABLE DAYS

Particulars Formula 2020 2021

Account

receivable 250 300

Sales revenue 3000 4000

Account

receivable

turnover

Account receivable /

sales *365 30 27

Account receivable days are considered to be the ratio which is helpful

for the calculation of the number of days it takes in average for the company

to recover its debts (Rahman and Fatmawati, 2020). This ratio is helpful for

the company to be able to determine the effectiveness of the collecting

methods of the company for having a tool of adding it into the financial

analysis for the preparation of budget. This ratio has been considered to be

8

Turnover Days COGS/Inventory 61 51

The inventory turnover days is a financial ratio that shows how many

times a company has sold and replaced inventory during a given period. It is

also considered to be the division of the days in the period of which the

inventory turnover formula is calculated for the days of selling the inventory

in hand. It has been said that the good turnover days are calculated at 5 to

10 days however for this company this ratio has been calculated at 61 in

2020. The company is making positive efforts for reducing the inventory

turnover to 51 days. Having fewer days in the Inventory turnover days is

helpful for the organization for indicating the weaker sales and declining the

demand of company's products.

Account Receivable days :

ACCOUNT RECEIVABLE DAYS

Particulars Formula 2020 2021

Account

receivable 250 300

Sales revenue 3000 4000

Account

receivable

turnover

Account receivable /

sales *365 30 27

Account receivable days are considered to be the ratio which is helpful

for the calculation of the number of days it takes in average for the company

to recover its debts (Rahman and Fatmawati, 2020). This ratio is helpful for

the company to be able to determine the effectiveness of the collecting

methods of the company for having a tool of adding it into the financial

analysis for the preparation of budget. This ratio has been considered to be

8

the most idea when it is the lowest as possible. For this organization in 2020

account receivable days were 30 which has now accountant to 27 in the

year of 2021 which indicates the efficiency of the organization.

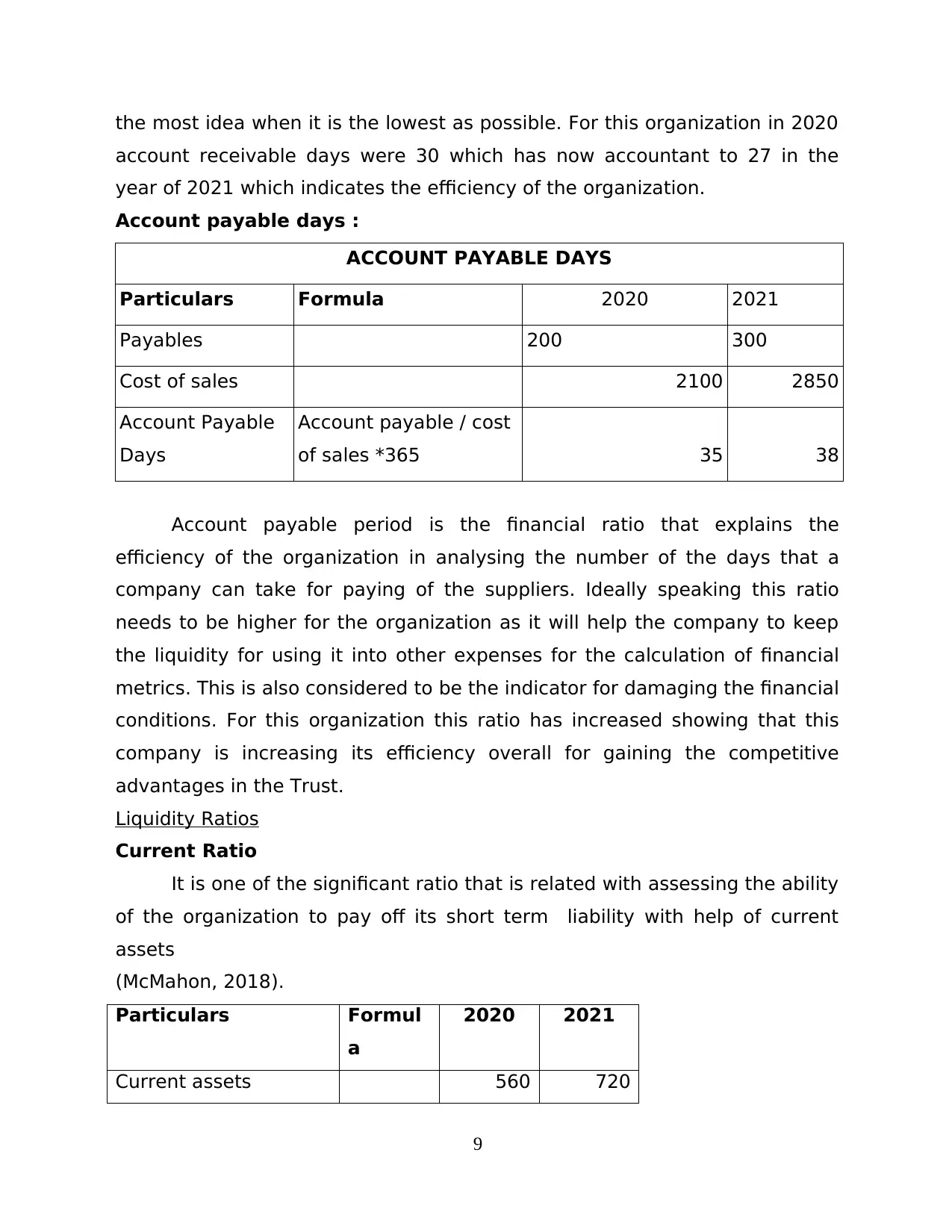

Account payable days :

ACCOUNT PAYABLE DAYS

Particulars Formula 2020 2021

Payables 200 300

Cost of sales 2100 2850

Account Payable

Days

Account payable / cost

of sales *365 35 38

Account payable period is the financial ratio that explains the

efficiency of the organization in analysing the number of the days that a

company can take for paying of the suppliers. Ideally speaking this ratio

needs to be higher for the organization as it will help the company to keep

the liquidity for using it into other expenses for the calculation of financial

metrics. This is also considered to be the indicator for damaging the financial

conditions. For this organization this ratio has increased showing that this

company is increasing its efficiency overall for gaining the competitive

advantages in the Trust.

Liquidity Ratios

Current Ratio

It is one of the significant ratio that is related with assessing the ability

of the organization to pay off its short term liability with help of current

assets

(McMahon, 2018).

Particulars Formul

a

2020 2021

Current assets 560 720

9

account receivable days were 30 which has now accountant to 27 in the

year of 2021 which indicates the efficiency of the organization.

Account payable days :

ACCOUNT PAYABLE DAYS

Particulars Formula 2020 2021

Payables 200 300

Cost of sales 2100 2850

Account Payable

Days

Account payable / cost

of sales *365 35 38

Account payable period is the financial ratio that explains the

efficiency of the organization in analysing the number of the days that a

company can take for paying of the suppliers. Ideally speaking this ratio

needs to be higher for the organization as it will help the company to keep

the liquidity for using it into other expenses for the calculation of financial

metrics. This is also considered to be the indicator for damaging the financial

conditions. For this organization this ratio has increased showing that this

company is increasing its efficiency overall for gaining the competitive

advantages in the Trust.

Liquidity Ratios

Current Ratio

It is one of the significant ratio that is related with assessing the ability

of the organization to pay off its short term liability with help of current

assets

(McMahon, 2018).

Particulars Formul

a

2020 2021

Current assets 560 720

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

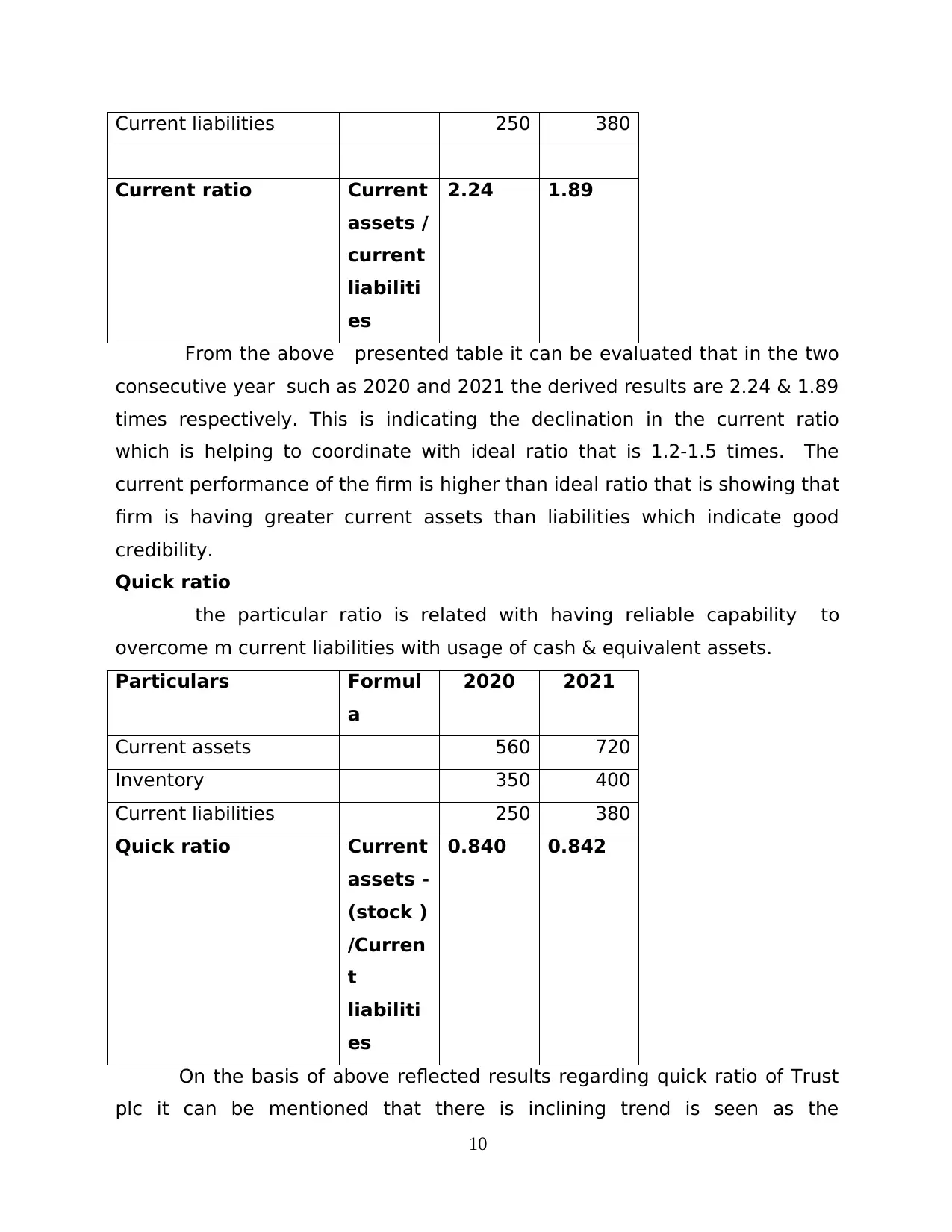

Current liabilities 250 380

Current ratio Current

assets /

current

liabiliti

es

2.24 1.89

From the above presented table it can be evaluated that in the two

consecutive year such as 2020 and 2021 the derived results are 2.24 & 1.89

times respectively. This is indicating the declination in the current ratio

which is helping to coordinate with ideal ratio that is 1.2-1.5 times. The

current performance of the firm is higher than ideal ratio that is showing that

firm is having greater current assets than liabilities which indicate good

credibility.

Quick ratio

the particular ratio is related with having reliable capability to

overcome m current liabilities with usage of cash & equivalent assets.

Particulars Formul

a

2020 2021

Current assets 560 720

Inventory 350 400

Current liabilities 250 380

Quick ratio Current

assets -

(stock )

/Curren

t

liabiliti

es

0.840 0.842

On the basis of above reflected results regarding quick ratio of Trust

plc it can be mentioned that there is inclining trend is seen as the

10

Current ratio Current

assets /

current

liabiliti

es

2.24 1.89

From the above presented table it can be evaluated that in the two

consecutive year such as 2020 and 2021 the derived results are 2.24 & 1.89

times respectively. This is indicating the declination in the current ratio

which is helping to coordinate with ideal ratio that is 1.2-1.5 times. The

current performance of the firm is higher than ideal ratio that is showing that

firm is having greater current assets than liabilities which indicate good

credibility.

Quick ratio

the particular ratio is related with having reliable capability to

overcome m current liabilities with usage of cash & equivalent assets.

Particulars Formul

a

2020 2021

Current assets 560 720

Inventory 350 400

Current liabilities 250 380

Quick ratio Current

assets -

(stock )

/Curren

t

liabiliti

es

0.840 0.842

On the basis of above reflected results regarding quick ratio of Trust

plc it can be mentioned that there is inclining trend is seen as the

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

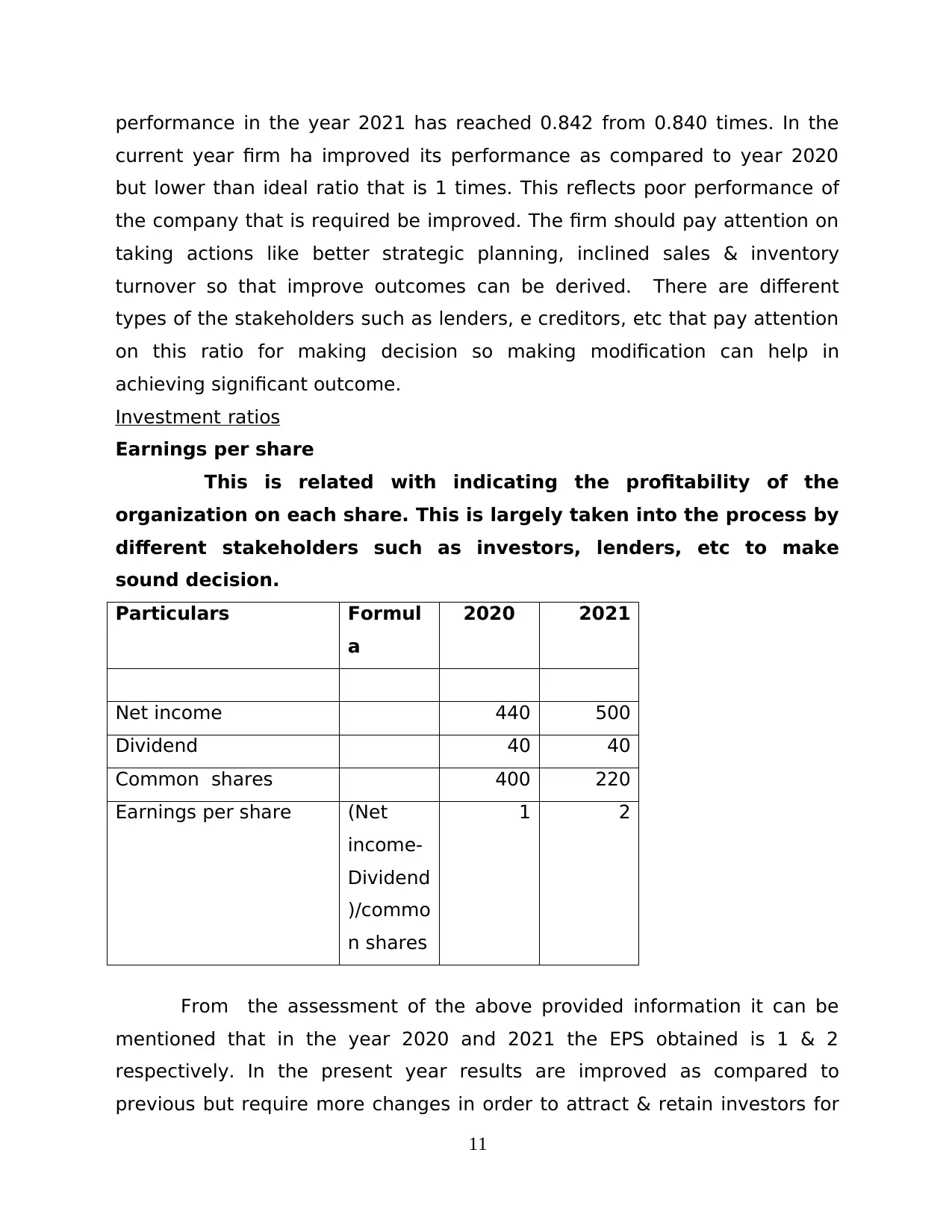

performance in the year 2021 has reached 0.842 from 0.840 times. In the

current year firm ha improved its performance as compared to year 2020

but lower than ideal ratio that is 1 times. This reflects poor performance of

the company that is required be improved. The firm should pay attention on

taking actions like better strategic planning, inclined sales & inventory

turnover so that improve outcomes can be derived. There are different

types of the stakeholders such as lenders, e creditors, etc that pay attention

on this ratio for making decision so making modification can help in

achieving significant outcome.

Investment ratios

Earnings per share

This is related with indicating the profitability of the

organization on each share. This is largely taken into the process by

different stakeholders such as investors, lenders, etc to make

sound decision.

Particulars Formul

a

2020 2021

Net income 440 500

Dividend 40 40

Common shares 400 220

Earnings per share (Net

income-

Dividend

)/commo

n shares

1 2

From the assessment of the above provided information it can be

mentioned that in the year 2020 and 2021 the EPS obtained is 1 & 2

respectively. In the present year results are improved as compared to

previous but require more changes in order to attract & retain investors for

11

current year firm ha improved its performance as compared to year 2020

but lower than ideal ratio that is 1 times. This reflects poor performance of

the company that is required be improved. The firm should pay attention on

taking actions like better strategic planning, inclined sales & inventory

turnover so that improve outcomes can be derived. There are different

types of the stakeholders such as lenders, e creditors, etc that pay attention

on this ratio for making decision so making modification can help in

achieving significant outcome.

Investment ratios

Earnings per share

This is related with indicating the profitability of the

organization on each share. This is largely taken into the process by

different stakeholders such as investors, lenders, etc to make

sound decision.

Particulars Formul

a

2020 2021

Net income 440 500

Dividend 40 40

Common shares 400 220

Earnings per share (Net

income-

Dividend

)/commo

n shares

1 2

From the assessment of the above provided information it can be

mentioned that in the year 2020 and 2021 the EPS obtained is 1 & 2

respectively. In the present year results are improved as compared to

previous but require more changes in order to attract & retain investors for

11

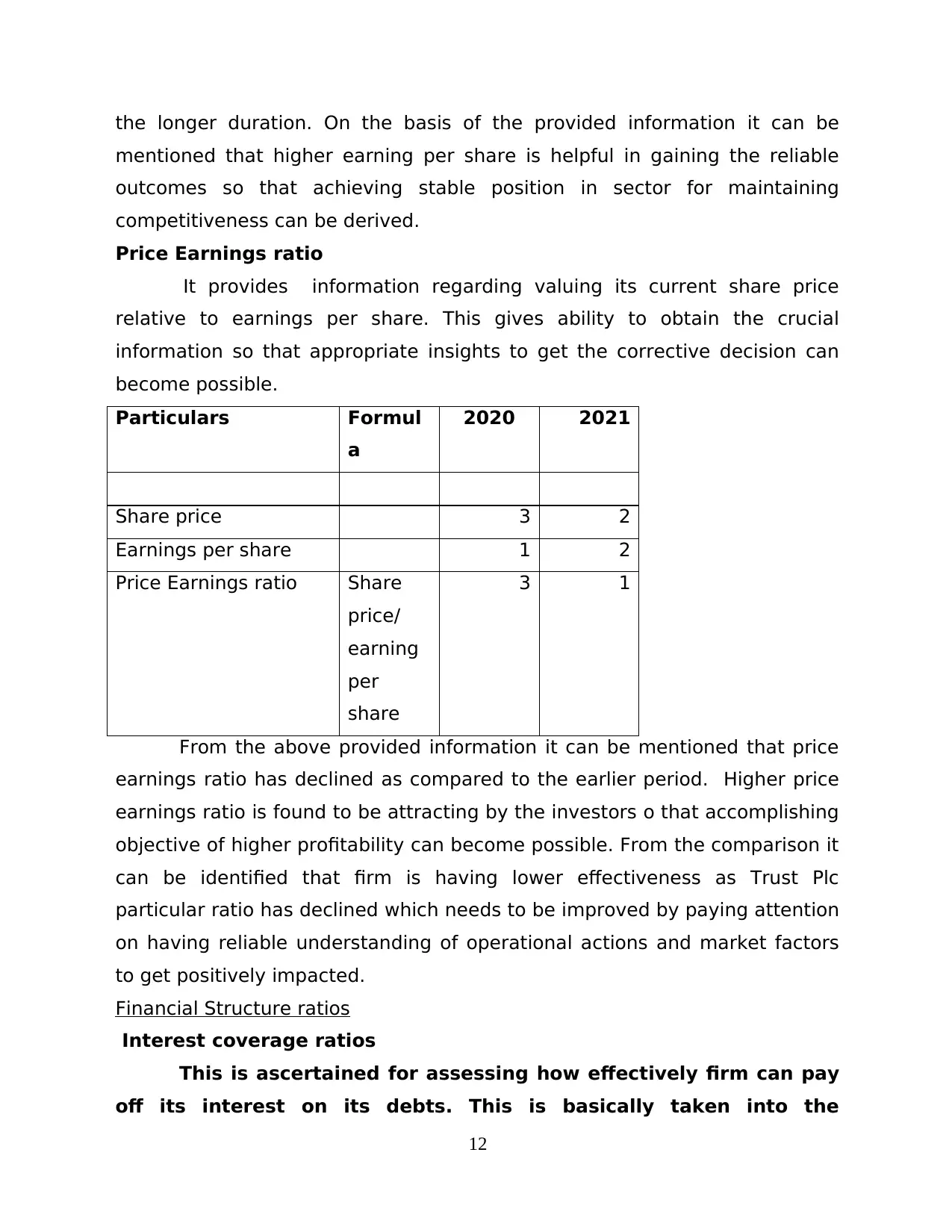

the longer duration. On the basis of the provided information it can be

mentioned that higher earning per share is helpful in gaining the reliable

outcomes so that achieving stable position in sector for maintaining

competitiveness can be derived.

Price Earnings ratio

It provides information regarding valuing its current share price

relative to earnings per share. This gives ability to obtain the crucial

information so that appropriate insights to get the corrective decision can

become possible.

Particulars Formul

a

2020 2021

Share price 3 2

Earnings per share 1 2

Price Earnings ratio Share

price/

earning

per

share

3 1

From the above provided information it can be mentioned that price

earnings ratio has declined as compared to the earlier period. Higher price

earnings ratio is found to be attracting by the investors o that accomplishing

objective of higher profitability can become possible. From the comparison it

can be identified that firm is having lower effectiveness as Trust Plc

particular ratio has declined which needs to be improved by paying attention

on having reliable understanding of operational actions and market factors

to get positively impacted.

Financial Structure ratios

Interest coverage ratios

This is ascertained for assessing how effectively firm can pay

off its interest on its debts. This is basically taken into the

12

mentioned that higher earning per share is helpful in gaining the reliable

outcomes so that achieving stable position in sector for maintaining

competitiveness can be derived.

Price Earnings ratio

It provides information regarding valuing its current share price

relative to earnings per share. This gives ability to obtain the crucial

information so that appropriate insights to get the corrective decision can

become possible.

Particulars Formul

a

2020 2021

Share price 3 2

Earnings per share 1 2

Price Earnings ratio Share

price/

earning

per

share

3 1

From the above provided information it can be mentioned that price

earnings ratio has declined as compared to the earlier period. Higher price

earnings ratio is found to be attracting by the investors o that accomplishing

objective of higher profitability can become possible. From the comparison it

can be identified that firm is having lower effectiveness as Trust Plc

particular ratio has declined which needs to be improved by paying attention

on having reliable understanding of operational actions and market factors

to get positively impacted.

Financial Structure ratios

Interest coverage ratios

This is ascertained for assessing how effectively firm can pay

off its interest on its debts. This is basically taken into the

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.