Research Project: Effectiveness of Ratio Analysis in TESCO

VerifiedAdded on 2019/12/03

|31

|9080

|409

Report

AI Summary

This research project investigates the effectiveness of ratio analysis in the business decision-making process, using Tesco PLC as a case study. The report begins with an introduction to the background of the research, the organization (Tesco), the statement of the problem, aims and objectives, and the importance of the study. A comprehensive literature review follows, covering financial statement analysis, users of financial information, the importance and limitations of ratio analysis, and different types of ratios. The methodology section outlines the research approaches and methods employed. The data findings section presents ratio calculations and analysis, along with findings from a questionnaire. The results and discussion section interprets the data, followed by a discussion of the research's limitations and areas for further consideration. The research aims to determine how ratio analysis can aid shareholders, investors, suppliers, creditors, employees, managers, and other stakeholders in making informed decisions about a company's past performance, present condition, and future potential. The report emphasizes the role of financial ratios in assessing profitability, solvency, and overall financial health, providing insights into how these tools contribute to strategic decision-making within a major retail organization like Tesco.

Research Project

Effectiveness of Ratio Analysis

in business decision making

process: Study on TESCO

Effectiveness of Ratio Analysis

in business decision making

process: Study on TESCO

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

TABLE OF CONTENTS

1 INTRODUCTION........................................................................................................................1

1.1 Background of the research...................................................................................................1

1.2 Background of the organization.............................................................................................2

1.3 Statement of problem.............................................................................................................2

1.4 Aims & Objectives of the research........................................................................................3

1.5 Importance of the study.........................................................................................................3

2 LITERATURE REVIEW.............................................................................................................3

2.1 Introduction............................................................................................................................3

2.2 Financial statement analysis..................................................................................................4

2.3 Users of the financial information.........................................................................................4

2.4 IMPORTANCE RATIO ANALYSIS.....................................................................................5

2.5 Limitations of ratio analysis..................................................................................................6

2.6 Different types of ratios in ratio analysis...............................................................................7

3 RESEARCH APPROACHES & METHODS............................................................................11

3.1 Introduction..........................................................................................................................11

3.2 Research approaches............................................................................................................11

4 DATA FINDINGS......................................................................................................................15

4.1 Introduction..........................................................................................................................15

4.2 Ratio Calculation.................................................................................................................15

4.3 Ratio Analysis......................................................................................................................16

4.4 Findings from the questionnaire..........................................................................................19

RESULTS AND DISCUSSION....................................................................................................23

LIMITATIONS OF THE RESEARCH & AREAS OF FURTHER CONSIDERATION............24

CONCLUSION..............................................................................................................................24

1 INTRODUCTION........................................................................................................................1

1.1 Background of the research...................................................................................................1

1.2 Background of the organization.............................................................................................2

1.3 Statement of problem.............................................................................................................2

1.4 Aims & Objectives of the research........................................................................................3

1.5 Importance of the study.........................................................................................................3

2 LITERATURE REVIEW.............................................................................................................3

2.1 Introduction............................................................................................................................3

2.2 Financial statement analysis..................................................................................................4

2.3 Users of the financial information.........................................................................................4

2.4 IMPORTANCE RATIO ANALYSIS.....................................................................................5

2.5 Limitations of ratio analysis..................................................................................................6

2.6 Different types of ratios in ratio analysis...............................................................................7

3 RESEARCH APPROACHES & METHODS............................................................................11

3.1 Introduction..........................................................................................................................11

3.2 Research approaches............................................................................................................11

4 DATA FINDINGS......................................................................................................................15

4.1 Introduction..........................................................................................................................15

4.2 Ratio Calculation.................................................................................................................15

4.3 Ratio Analysis......................................................................................................................16

4.4 Findings from the questionnaire..........................................................................................19

RESULTS AND DISCUSSION....................................................................................................23

LIMITATIONS OF THE RESEARCH & AREAS OF FURTHER CONSIDERATION............24

CONCLUSION..............................................................................................................................24

REFERENCES..............................................................................................................................26

1 INTRODUCTION

1.1 Background of the research

Every kind of business whether it is small or big makes efforts to attain profitability and

solvency. Profitability is the situation which describes the ability of the company to make profits.

On the other side, solvency is the potential of the business to pay its debts as they come due

(Palepu and Healy, 2007). However it is not easy to attain these objectives. It requires efficient

management of business resources through forecasting, budgeting, planning, control and

decision making. Further there is a need to identify strength and weakness of the company and

then take corrective actions. Accounting offers that information which facilitates the above

functions (Ahrendsen and Katchova, 2012). Generally the accounting records and evaluates

economic information which is required for decision making. The information is derived from

three financial `statement produced by a company. These include balance sheet, income

statement and cash flow statement. The income statement reflects the profitability and

operational performance of the business and the balance sheet discloses the solvency position

(Argouslidis, 2008).

In order to judge the financial performance, profits related to various items in statements

are used as the basis. It helps in obtaining meaningful and useful information for decision

making. It is to be noted that due to the summarized nature of these documents, a lot of facts are

still undiscovered (Bennouna and Marchant, 2010). Hence for that purpose they are analyzed and

interpreted through the technique of ratio analysis. It enables the users to understand the meaning

of absolute amounts and to make informed business decisions. The business statements are

enclosed with lots of financial details which are hidden in the figures (Bourne, franco, and

Wilkes, 2006). These figures become more useful when they are related to each other or to some

other relevant financial data. Hence the users need to go further in order to establish relationship

among the data in the statements.

Ratio analysis is a tool which measures the company’s performance and contributes

towards making of many important business decisions. Ratios play an important role in the

business world (Cole, Branson and Breesch, 2012). It can be defined as a proportion or fraction

or percentage which expresses the relationship between different items in the financial statement.

The ratios are the most powerful tool which is used in evaluation and interpretation of

statements.

1

1.1 Background of the research

Every kind of business whether it is small or big makes efforts to attain profitability and

solvency. Profitability is the situation which describes the ability of the company to make profits.

On the other side, solvency is the potential of the business to pay its debts as they come due

(Palepu and Healy, 2007). However it is not easy to attain these objectives. It requires efficient

management of business resources through forecasting, budgeting, planning, control and

decision making. Further there is a need to identify strength and weakness of the company and

then take corrective actions. Accounting offers that information which facilitates the above

functions (Ahrendsen and Katchova, 2012). Generally the accounting records and evaluates

economic information which is required for decision making. The information is derived from

three financial `statement produced by a company. These include balance sheet, income

statement and cash flow statement. The income statement reflects the profitability and

operational performance of the business and the balance sheet discloses the solvency position

(Argouslidis, 2008).

In order to judge the financial performance, profits related to various items in statements

are used as the basis. It helps in obtaining meaningful and useful information for decision

making. It is to be noted that due to the summarized nature of these documents, a lot of facts are

still undiscovered (Bennouna and Marchant, 2010). Hence for that purpose they are analyzed and

interpreted through the technique of ratio analysis. It enables the users to understand the meaning

of absolute amounts and to make informed business decisions. The business statements are

enclosed with lots of financial details which are hidden in the figures (Bourne, franco, and

Wilkes, 2006). These figures become more useful when they are related to each other or to some

other relevant financial data. Hence the users need to go further in order to establish relationship

among the data in the statements.

Ratio analysis is a tool which measures the company’s performance and contributes

towards making of many important business decisions. Ratios play an important role in the

business world (Cole, Branson and Breesch, 2012). It can be defined as a proportion or fraction

or percentage which expresses the relationship between different items in the financial statement.

The ratios are the most powerful tool which is used in evaluation and interpretation of

statements.

1

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

According to Ittelson, (2009), decision making is a conscious process of making choices

out of one or more alternatives with the purpose of moving towards some desired state of affairs.

The choices are related to the allocation and it ensures use of business resources to achieve

objectives. It is to be noted that decision making requires appropriate information (Siano,

Kitchen and Confetto, 2010). Managers require appropriate data so that they can make out

something meaningful and productive. Proper use of the data has to be ensured so that sound

decisions can be made. Decisions related to investment or disinvestment, make or buy, expansion

or contraction, etc. cannot be made without the use of financial ratios (Tracy, 2012). It gives an

idea about the financial strengths and weaknesses of a particular business and also highlights the

aspects which need further investigation.

This research study is being performed to reflect how tool of ratio analysis can help

shareholders, investors, suppliers, creditors, employees, managers and other stakeholder in

making their respective decisions. The decisions are taken about the past performance, present

condition and future potential of the company.

1.2 Background of the organization

Tesco PLC is a British Multinational grocery and general merchandise retailer. It is

headquartered in Cheshnut, Hertforshire in England. It is the third largest retailer across the

world in terms of profits. It holds the largest share in the retail market (Moyer, McGuigan and

Rao, 2011). It is greatest in terms of number of employees and number of stores. It is a leading

brand in the retail sector and that is the reason every investor keeps an eye on the share prices of

the company. Change in the share prices of Tesco affects investing decisions of several investors.

This research report identifies how technique of ratio analysis can be useful in taking of different

types of decisions. It will calculate the financial ratios for the Tesco and evaluates its business

performance. For this research, Tesco has been selected because it will be interesting to know

how decisions can be made within such big organization on the basis of ratio analysis. Further it

can be identified that, this tool is a good reflector of financial performance or not.

1.3 Statement of problem

Hence it is clear now that financial information offered in the statements is very useful in

taking business decisions. They act as a mean to achieve end and not an end in themselves. It is

2

out of one or more alternatives with the purpose of moving towards some desired state of affairs.

The choices are related to the allocation and it ensures use of business resources to achieve

objectives. It is to be noted that decision making requires appropriate information (Siano,

Kitchen and Confetto, 2010). Managers require appropriate data so that they can make out

something meaningful and productive. Proper use of the data has to be ensured so that sound

decisions can be made. Decisions related to investment or disinvestment, make or buy, expansion

or contraction, etc. cannot be made without the use of financial ratios (Tracy, 2012). It gives an

idea about the financial strengths and weaknesses of a particular business and also highlights the

aspects which need further investigation.

This research study is being performed to reflect how tool of ratio analysis can help

shareholders, investors, suppliers, creditors, employees, managers and other stakeholder in

making their respective decisions. The decisions are taken about the past performance, present

condition and future potential of the company.

1.2 Background of the organization

Tesco PLC is a British Multinational grocery and general merchandise retailer. It is

headquartered in Cheshnut, Hertforshire in England. It is the third largest retailer across the

world in terms of profits. It holds the largest share in the retail market (Moyer, McGuigan and

Rao, 2011). It is greatest in terms of number of employees and number of stores. It is a leading

brand in the retail sector and that is the reason every investor keeps an eye on the share prices of

the company. Change in the share prices of Tesco affects investing decisions of several investors.

This research report identifies how technique of ratio analysis can be useful in taking of different

types of decisions. It will calculate the financial ratios for the Tesco and evaluates its business

performance. For this research, Tesco has been selected because it will be interesting to know

how decisions can be made within such big organization on the basis of ratio analysis. Further it

can be identified that, this tool is a good reflector of financial performance or not.

1.3 Statement of problem

Hence it is clear now that financial information offered in the statements is very useful in

taking business decisions. They act as a mean to achieve end and not an end in themselves. It is

2

evident that information is presented in summarized statements, so it needs to be interpreted by

using a suitable technique. It enables the management and stakeholder to understand and to make

well informed decisions. Further many users of these documents are not intellectual about the

accounting ratios and also do not know how they are applied. Despite of several advantages,

there are also many limitations associated with the use of ratio analysis. Hence this research is

undertaken to ensure that how this tool can be used in appropriate manner.

1.4 Aims & Objectives of the research

The major aim of the study is to identify the effectiveness of Ratio Analysis in business

decision making process. Following objectives have been framed:

To discover the importance of Ratio Analysis in decision making process

To identify the drawbacks of the Ratio Analysis for the business

To provide suggestions for improvements

Research question

Why business managers should rely on financial ratios for decision making?

1.5 Importance of the study

Every research has its own significance. This research will be carried out in order to find

out whether ratio analysis is an effective tool for decision making or not. The management of an

organization depends on the accounting information for taking various types of strategic

decisions (Palepu and Healy, 2007). This information is generated by analyzing and interpreting

the financial statements. A sustainable company like Tesco needs effective planning and good

financial management. This research will compute the accounting ratios for Tesco and then show

how decisions are made. Along with that it will also talk about the benefits and drawbacks of

using ratio analysis for decision making.

2 LITERATURE REVIEW

2.1 Introduction

Recording and summarising of the financial data are essential part of the accounting

information system. The financial statements are required to be analyzed and interpreted so that

3

using a suitable technique. It enables the management and stakeholder to understand and to make

well informed decisions. Further many users of these documents are not intellectual about the

accounting ratios and also do not know how they are applied. Despite of several advantages,

there are also many limitations associated with the use of ratio analysis. Hence this research is

undertaken to ensure that how this tool can be used in appropriate manner.

1.4 Aims & Objectives of the research

The major aim of the study is to identify the effectiveness of Ratio Analysis in business

decision making process. Following objectives have been framed:

To discover the importance of Ratio Analysis in decision making process

To identify the drawbacks of the Ratio Analysis for the business

To provide suggestions for improvements

Research question

Why business managers should rely on financial ratios for decision making?

1.5 Importance of the study

Every research has its own significance. This research will be carried out in order to find

out whether ratio analysis is an effective tool for decision making or not. The management of an

organization depends on the accounting information for taking various types of strategic

decisions (Palepu and Healy, 2007). This information is generated by analyzing and interpreting

the financial statements. A sustainable company like Tesco needs effective planning and good

financial management. This research will compute the accounting ratios for Tesco and then show

how decisions are made. Along with that it will also talk about the benefits and drawbacks of

using ratio analysis for decision making.

2 LITERATURE REVIEW

2.1 Introduction

Recording and summarising of the financial data are essential part of the accounting

information system. The financial statements are required to be analyzed and interpreted so that

3

truths hidden behind the information can be unveiled. Interestingly such analysis can be done on

the basis of ratio analysis and comparisons. Literature Review will reveal the theories and

concepts related to the analysis.

2.2 Financial statement analysis

According to Sabău, (2013), financial statement analysis consists of application of

analysis tools and technique so that meaningful information can be derived. The main purpose is

to establish relationship between various items contained in the statements. In this way various

conclusions are drawn about the past performance, existing position and future potential of the

company (Evans, and Porter, 2010). The analysis is done find out where the business is lacking

and how the improvements can be done. Most importantly it identifies the strengths and

weaknesses of the firm.

Business decision making is a difficult process as it requires consideration of different

types of factors. The decisions are taken after making some evaluations. It is considered as the

most important element in management of all the activities (Ainsworth and Deines, 2008).

Financial performance of the company is measured in order to find out how the business is

performing. There are different types of techniques for measuring the performance and ratio

analysis is one of them. Ratio Analysis is a quantitative analysis of information which is

contained in the company’s financial statements. It records the performance of the business in

terms of liquidity, profitability, solvency etc (Broadbent and Cullen, 2012). It applies different

types of ratios for the comparison of similar variables. It manipulates the figures in systematic

manner in order to produce information which is used in investment decision making process.

The trend of these ratios over time is studied in order to check whether they are improving or

deteriorating (Cadle and et.al., 2010). The analysis is regarded as the cornerstone of fundamental

analysis. This research is about investigating the effectiveness of ratio analysis in the business

decision making process within the context of Tesco.

2.3 Users of the financial information

The users of the financial information can be divided into two categories that is internal

users and external users (Ainsworth, and Deines, 2008). Their need can be described in the

following manner:

4

the basis of ratio analysis and comparisons. Literature Review will reveal the theories and

concepts related to the analysis.

2.2 Financial statement analysis

According to Sabău, (2013), financial statement analysis consists of application of

analysis tools and technique so that meaningful information can be derived. The main purpose is

to establish relationship between various items contained in the statements. In this way various

conclusions are drawn about the past performance, existing position and future potential of the

company (Evans, and Porter, 2010). The analysis is done find out where the business is lacking

and how the improvements can be done. Most importantly it identifies the strengths and

weaknesses of the firm.

Business decision making is a difficult process as it requires consideration of different

types of factors. The decisions are taken after making some evaluations. It is considered as the

most important element in management of all the activities (Ainsworth and Deines, 2008).

Financial performance of the company is measured in order to find out how the business is

performing. There are different types of techniques for measuring the performance and ratio

analysis is one of them. Ratio Analysis is a quantitative analysis of information which is

contained in the company’s financial statements. It records the performance of the business in

terms of liquidity, profitability, solvency etc (Broadbent and Cullen, 2012). It applies different

types of ratios for the comparison of similar variables. It manipulates the figures in systematic

manner in order to produce information which is used in investment decision making process.

The trend of these ratios over time is studied in order to check whether they are improving or

deteriorating (Cadle and et.al., 2010). The analysis is regarded as the cornerstone of fundamental

analysis. This research is about investigating the effectiveness of ratio analysis in the business

decision making process within the context of Tesco.

2.3 Users of the financial information

The users of the financial information can be divided into two categories that is internal

users and external users (Ainsworth, and Deines, 2008). Their need can be described in the

following manner:

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Management and Employees – The data helps the management and employees in

identifying the financial position, operating results and future potential of the company.

Employees can take decisions related to their career and growth opportunities (Broadbent

and Cullen, 2012)

Shareholders - It helps the shareholder to know about the return on their investments.

They can also ascertain the profitability of the company (Cadle, and et.all., 2010)

Investors & Creditors – Investors are interested in knowing the return on investments

within the business of the company. Creditors want to have a check on the payment

making ability of the organization (Dey, 2002). Financial information helps the creditors

to know about the liquidity of the firm to pay its debts when they fall due.

Debenture holders – The people who lend the money to the company would be interested

in knowing whether it is capable of repaying the both the interests and the principal on

maturity charged on the loan (Giacomello, 2008)

Financial analysts – These people need financial information so that they can offer

professional advice to the clients regarding the investments.

Tax authorities – These bodies makes sure that company fulfils the legal and regulatory

requirements related to the business (Harrison, and Horngren 2007). They want to make

sure that business is paying it taxes in timely manner.

Government – Government keeps an eye watch on the business practices of the firm.

Government expects that it does not indulge into wrong practices and activities.

2.4 IMPORTANCE RATIO ANALYSIS

Following are the advantages derived from the technique of ratio analysis:

Analysing the Financial Statements – The ratios are very useful in understanding the

financial position of the business. Different types of stakeholders such as management,

bankers, creditors etc make use of ratio analysis in order to fulfil their respective financial

objectives (Moyer, McGuigan and Rao, 2011).

Judging efficiency – It is a very effective tool in judging the efficiency of the

organization in terms of operations and management. It shows the ability of the business

related to utilization of assets and earning of profits (Palepu and Healy, 2007).

5

identifying the financial position, operating results and future potential of the company.

Employees can take decisions related to their career and growth opportunities (Broadbent

and Cullen, 2012)

Shareholders - It helps the shareholder to know about the return on their investments.

They can also ascertain the profitability of the company (Cadle, and et.all., 2010)

Investors & Creditors – Investors are interested in knowing the return on investments

within the business of the company. Creditors want to have a check on the payment

making ability of the organization (Dey, 2002). Financial information helps the creditors

to know about the liquidity of the firm to pay its debts when they fall due.

Debenture holders – The people who lend the money to the company would be interested

in knowing whether it is capable of repaying the both the interests and the principal on

maturity charged on the loan (Giacomello, 2008)

Financial analysts – These people need financial information so that they can offer

professional advice to the clients regarding the investments.

Tax authorities – These bodies makes sure that company fulfils the legal and regulatory

requirements related to the business (Harrison, and Horngren 2007). They want to make

sure that business is paying it taxes in timely manner.

Government – Government keeps an eye watch on the business practices of the firm.

Government expects that it does not indulge into wrong practices and activities.

2.4 IMPORTANCE RATIO ANALYSIS

Following are the advantages derived from the technique of ratio analysis:

Analysing the Financial Statements – The ratios are very useful in understanding the

financial position of the business. Different types of stakeholders such as management,

bankers, creditors etc make use of ratio analysis in order to fulfil their respective financial

objectives (Moyer, McGuigan and Rao, 2011).

Judging efficiency – It is a very effective tool in judging the efficiency of the

organization in terms of operations and management. It shows the ability of the business

related to utilization of assets and earning of profits (Palepu and Healy, 2007).

5

Identifying the weakness – It is also very effective in locating any kind of weakness or

errors within the business. By identifying the weakness, company can pay attention on

adopting remedial measures to remove the weakness

Formulating plans – Apart from evaluating the existing financial performance, ratios can

also be used to formulate future plans related to growth and development. It decides the

path of progress for the company (Ahrendsen and Katchova, 2012)

Comparing performance - It is very imperative for the organization to analyze how well it

is performing as compared to the other companies in the similar industry.

Trend analysis: By undertaking trend analysis organization can predict its performers that

whether it is increasing or decreasing over the coming years (Sinclair, Northcott and

Hooper, 2014). Through this, company is able to frame suitable strategies which help it in

taking advantage over others.

2.5 Limitations of ratio analysis

There are several limitations are prevailed in the ratio analysis which affects its

importance are enumerated below: Lack of standard: There is the lack universal standard regarding ratio analysis so it is

very difficult for the company to comment on the basis of the results of ratio analysis

(Cole, Branson and Breesch, 2012). Moreover, different company may use different

methods to assess its financial and liquidity position. It is one of the main aspects which

impact the utility of ratio analysis. Inflationary effects: Firm cannot undertake inflationary aspects or measures while

calculating the financial ratios (Ross, Westerfield and Jordan, 2015). Therefore, outcomes

of the ratio analysis will unable to give ideas in relation to the changes in price level. Not a substitute of financial statements: Techniques of ratio analysis can never be taken

as a substitute of the financial statements. It only summarizes the various aspects of

financial statements in the form of percentage (Moyer, McGuigan and Rao, 2011).

Only a Quantitative measure: It is only a quantitative measure of the organizational

performance. It exclusively states the liquidity, solvency and efficiency of the business

operations and activities. Nevertheless, it does not indicate the cause behind the poor

performance of the organization (Siano, Kitchen and Confetto, 2010). In addition to this,

6

errors within the business. By identifying the weakness, company can pay attention on

adopting remedial measures to remove the weakness

Formulating plans – Apart from evaluating the existing financial performance, ratios can

also be used to formulate future plans related to growth and development. It decides the

path of progress for the company (Ahrendsen and Katchova, 2012)

Comparing performance - It is very imperative for the organization to analyze how well it

is performing as compared to the other companies in the similar industry.

Trend analysis: By undertaking trend analysis organization can predict its performers that

whether it is increasing or decreasing over the coming years (Sinclair, Northcott and

Hooper, 2014). Through this, company is able to frame suitable strategies which help it in

taking advantage over others.

2.5 Limitations of ratio analysis

There are several limitations are prevailed in the ratio analysis which affects its

importance are enumerated below: Lack of standard: There is the lack universal standard regarding ratio analysis so it is

very difficult for the company to comment on the basis of the results of ratio analysis

(Cole, Branson and Breesch, 2012). Moreover, different company may use different

methods to assess its financial and liquidity position. It is one of the main aspects which

impact the utility of ratio analysis. Inflationary effects: Firm cannot undertake inflationary aspects or measures while

calculating the financial ratios (Ross, Westerfield and Jordan, 2015). Therefore, outcomes

of the ratio analysis will unable to give ideas in relation to the changes in price level. Not a substitute of financial statements: Techniques of ratio analysis can never be taken

as a substitute of the financial statements. It only summarizes the various aspects of

financial statements in the form of percentage (Moyer, McGuigan and Rao, 2011).

Only a Quantitative measure: It is only a quantitative measure of the organizational

performance. It exclusively states the liquidity, solvency and efficiency of the business

operations and activities. Nevertheless, it does not indicate the cause behind the poor

performance of the organization (Siano, Kitchen and Confetto, 2010). In addition to this,

6

ratio analysis techniques do not entails the effective measures which company needs to be

taken to improve the business operations. Window dressing: Different ratio are calculated with the help of the values financial

statements to assess the financial health and performance of the company. Nevertheless,

one can easily manipulate the values of the financial statements or misrepresents the fact.

It also negatively affects the utility of ratio analysis technique (Bennouna and Marchant

2010).

Changes in the accounting methods: Accounting methods which are used by the company

make impact upon the results of the ratio analysis. In this case, enterprise is not able to

compare its present performance with the past performance or results. For instance:

Corporation undertakes LIFO method to assess the value of the inventory in the current

financial year (Wahlen, Baginski and Bradshaw, 2014). Whereas it uses FIFO method in

the previous year for the same purpose then the value of stock and stock turnover ratio

deviates due to changes in the accounting methods.

2.6 Different types of ratios in ratio analysis

There are various types of ratios are prevailed in the techniques of ratio analysis. It

provides more assistance in making assessment of financial health and performance of the

organization which are enumerated below:

Profitability ratios

It indicates the efficiency and effectiveness of the business in making use of

organizational resources in order to earn more profit. This entails success or the failure of the

firm during a predetermined time period (Bourne, franco and Wilkes, 2006). Sound profitability

condition ensures and attracts more existing and potential stakeholders to make investment in the

organization.

Gross profit ratio (GP): It is the profitability measure which states the comparison of the

gross margin or cost of goods sold to net sales. It indicates efficiency and effectiveness of

the company in the selling of its goods or services (Cole, Branson and Breesch, 2012).

Through this, company can easily assess the effectiveness of its own strategies and

policies in achieving success. It also enables enterprise to compare its current

performance with the past where price fluctuations take place more frequently. GP

margin also provides deeper insight to company regarding the sales pattern (Nobes,

7

taken to improve the business operations. Window dressing: Different ratio are calculated with the help of the values financial

statements to assess the financial health and performance of the company. Nevertheless,

one can easily manipulate the values of the financial statements or misrepresents the fact.

It also negatively affects the utility of ratio analysis technique (Bennouna and Marchant

2010).

Changes in the accounting methods: Accounting methods which are used by the company

make impact upon the results of the ratio analysis. In this case, enterprise is not able to

compare its present performance with the past performance or results. For instance:

Corporation undertakes LIFO method to assess the value of the inventory in the current

financial year (Wahlen, Baginski and Bradshaw, 2014). Whereas it uses FIFO method in

the previous year for the same purpose then the value of stock and stock turnover ratio

deviates due to changes in the accounting methods.

2.6 Different types of ratios in ratio analysis

There are various types of ratios are prevailed in the techniques of ratio analysis. It

provides more assistance in making assessment of financial health and performance of the

organization which are enumerated below:

Profitability ratios

It indicates the efficiency and effectiveness of the business in making use of

organizational resources in order to earn more profit. This entails success or the failure of the

firm during a predetermined time period (Bourne, franco and Wilkes, 2006). Sound profitability

condition ensures and attracts more existing and potential stakeholders to make investment in the

organization.

Gross profit ratio (GP): It is the profitability measure which states the comparison of the

gross margin or cost of goods sold to net sales. It indicates efficiency and effectiveness of

the company in the selling of its goods or services (Cole, Branson and Breesch, 2012).

Through this, company can easily assess the effectiveness of its own strategies and

policies in achieving success. It also enables enterprise to compare its current

performance with the past where price fluctuations take place more frequently. GP

margin also provides deeper insight to company regarding the sales pattern (Nobes,

7

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

2014). On the basis this, firm can easily estimate the inventory level and manage cost

more effectively. To calculate GP ration firm can use the following formula to assess its

efficiency level such as follows:

Gross profit ratio: Gross profit/Net sales*100

Net profit ratio (NP): It is also known as NP ratio which states relationship between the

net profit after tax and sales of the company. One can calculate net profit by subtracting

company's expenses such as operating expenses, material and other costs from the total

revenue of the company (Sinclair, Northcott and Hooper, 2014). It is the strategic way

through company assess the level of expenditure and make control upon it. This measure

proves to be more beneficial for the company which helps it in increase profitability

margin. company can assess its net profit margin by undertaking the following formula:

Net profit ratio: Net profit/Net Sales*100 (Siano, Kitchen and Confetto ,2010)

Operating profit ratio: Operating profit ratio is also known as operating profit margin. It

states the percentage of revenue which left over with the company after the payment of

all the operating expenses. This ratio plays a significant from the investors or

shareholders point of views (Evans and Porter 2010). Operating profit margin indicates

the soundness of company's operation. Through this, company is able to attract more

investors because every person wants to invest in the organization whose business

operations are very sound and profitable (Freeman and et.al., 2014). It also assists

various stakeholders in determining the company's ability in running the smooth business

operations and functions. Operating profit or margin is calculated by deduction the

operating expenses, interest expenses, depreciation and tax from gross income or revue.

Formula to calculate the operating profit margin are given below:

Operating profit margin/ratio: Operating profit/Net sales*100

Liquidity ratios

Liquidity ratio defines the organizational abilities to meet or cover its short term

obligations which are due to the company. It helps enterprise in making effective decision in

relation to cash related activities such as investment etc. Further, this ratio also provides deeper

insight to the corporation about the assets which can be easily controverter into cash (Minnis and

Sutherland, 2014).

8

more effectively. To calculate GP ration firm can use the following formula to assess its

efficiency level such as follows:

Gross profit ratio: Gross profit/Net sales*100

Net profit ratio (NP): It is also known as NP ratio which states relationship between the

net profit after tax and sales of the company. One can calculate net profit by subtracting

company's expenses such as operating expenses, material and other costs from the total

revenue of the company (Sinclair, Northcott and Hooper, 2014). It is the strategic way

through company assess the level of expenditure and make control upon it. This measure

proves to be more beneficial for the company which helps it in increase profitability

margin. company can assess its net profit margin by undertaking the following formula:

Net profit ratio: Net profit/Net Sales*100 (Siano, Kitchen and Confetto ,2010)

Operating profit ratio: Operating profit ratio is also known as operating profit margin. It

states the percentage of revenue which left over with the company after the payment of

all the operating expenses. This ratio plays a significant from the investors or

shareholders point of views (Evans and Porter 2010). Operating profit margin indicates

the soundness of company's operation. Through this, company is able to attract more

investors because every person wants to invest in the organization whose business

operations are very sound and profitable (Freeman and et.al., 2014). It also assists

various stakeholders in determining the company's ability in running the smooth business

operations and functions. Operating profit or margin is calculated by deduction the

operating expenses, interest expenses, depreciation and tax from gross income or revue.

Formula to calculate the operating profit margin are given below:

Operating profit margin/ratio: Operating profit/Net sales*100

Liquidity ratios

Liquidity ratio defines the organizational abilities to meet or cover its short term

obligations which are due to the company. It helps enterprise in making effective decision in

relation to cash related activities such as investment etc. Further, this ratio also provides deeper

insight to the corporation about the assets which can be easily controverter into cash (Minnis and

Sutherland, 2014).

8

Current ratio: It is the financial measure which assesses the financial health and

performance of the company (Broadbent and Cullen, 2012). It states the firm's ability or

condition that whether or not it has the enough amount of fund to meet its current

obligation over the current assets of the company. It is also knows as working capital

ratio which helps enterprise in framing competent strategies (Sun, Roth and Black, 2014).

Through this, organization or other stakeholders can identify the financial capability and

soundness of the firm.

The ideal current ratio of the company is 2:1. It represents that to survive in the

competitive business environment firm needs to have 2 current assets to meet its 1 current

obligations (Bourne, franco and Wilkes, 2006). If company is very near to this ratio then it is

recognized as financially sound and strong. It plays a significant role in building and maintaining

faith of the stakeholders in the functions and operations of business organization. Formula of the

current ratio is as follows:

Current ratio: Current assets/Current liabilities

Quick ratio: It is also called as acid test ratio which are used by the organization to gauge

its financial performance. This ratio will help company in assessing the the cash and cash

equivalents which can be easily converted into cash. Nevertheless, current and which

ratio differs significantly (Pal, Mehra and Pal, 2015). As company excluded inventory

while calculating the quick ratio because inventory might not turn into cash quickly.

Quick ratio considers marketable securities and account receivable which can be change

into a liquid from within the 90 days. One can calculate the quick ratio of the company by

using the following formula:

Quick ratio: Cash and cash equivalents + marketable securities+ accounts receivable

/Current liabilities (Siano, Kitchen and Confetto, 2010)

Efficiency ratios

This ratio states the firm's ability that how successfully the firms use its asset and there

by improves profitability. Besides this, it also shows the firm's ability in managing its liabilities.

In order to cope up with the dynamic business environment each and every requires to take

effective use of its assets to attain high level of profitability (Templeton and et.al., 2014). It

enables company to take competitive advantage over others and there by fulfilling organizational

aims and objectives.

9

performance of the company (Broadbent and Cullen, 2012). It states the firm's ability or

condition that whether or not it has the enough amount of fund to meet its current

obligation over the current assets of the company. It is also knows as working capital

ratio which helps enterprise in framing competent strategies (Sun, Roth and Black, 2014).

Through this, organization or other stakeholders can identify the financial capability and

soundness of the firm.

The ideal current ratio of the company is 2:1. It represents that to survive in the

competitive business environment firm needs to have 2 current assets to meet its 1 current

obligations (Bourne, franco and Wilkes, 2006). If company is very near to this ratio then it is

recognized as financially sound and strong. It plays a significant role in building and maintaining

faith of the stakeholders in the functions and operations of business organization. Formula of the

current ratio is as follows:

Current ratio: Current assets/Current liabilities

Quick ratio: It is also called as acid test ratio which are used by the organization to gauge

its financial performance. This ratio will help company in assessing the the cash and cash

equivalents which can be easily converted into cash. Nevertheless, current and which

ratio differs significantly (Pal, Mehra and Pal, 2015). As company excluded inventory

while calculating the quick ratio because inventory might not turn into cash quickly.

Quick ratio considers marketable securities and account receivable which can be change

into a liquid from within the 90 days. One can calculate the quick ratio of the company by

using the following formula:

Quick ratio: Cash and cash equivalents + marketable securities+ accounts receivable

/Current liabilities (Siano, Kitchen and Confetto, 2010)

Efficiency ratios

This ratio states the firm's ability that how successfully the firms use its asset and there

by improves profitability. Besides this, it also shows the firm's ability in managing its liabilities.

In order to cope up with the dynamic business environment each and every requires to take

effective use of its assets to attain high level of profitability (Templeton and et.al., 2014). It

enables company to take competitive advantage over others and there by fulfilling organizational

aims and objectives.

9

Total asset turnover ratio: It is the measure which enables company to assess its

effectiveness in making use of the long term and short assets. This ratio will help

manager in assessing the success or failure of the assets (Evan and Porter, 2010). Total

asset turnover ratio provides idea to the manager about the isolation of plant and

machinery. It helps company in making right decision about the sales of the asset at the

right time and thereby improving the sales revenue.

Asset turnover ratio: Net sales / Total assets

Inventory turnover ratio: It helps in determining the capability of the company in

managing its inventory level. If it is too low then it indicates that firm fails to manage its

inventory and faces difficulties in pushing sales to customers (Burt and Amin, 2014). In

contrary to this, if inventory turnover ratio of the company is high then it shows that

inventory policy of the company is sound and it should follow the existing strategy to

manage its inventory level. It can measured as: (Cole, Branson and Breesch, 2012)

Inventory turnover ratio: Cost of goods sold / Average inventory

Gearing or Solvency ratios

Solvency ratio defines the cash position of the firm which encompasses that it is able to

meet its short term and long term liabilities.

Debt-equity ratio: This ratio shows the relative proportion of shareholders and debt which

are used by the corporation to finance the assets. To become a sound and well organized

firm, enterprise needs to make efforts so they come to near ideal debt equity ratio which

is .5:1 It represents that organization needs to raise more finance through equity shares

rather than debt (Siano, Kitchen and Confetto, 2010). Moreover, when company raise

finance through debt then it has to pay interest to the debt holders whether firm make

profit or not. In case of shares, company have no compulsion in relation to the payment

of dividend and there by reduces the financial burden (Erasmus and et.al., 2015). But

organization requires paying dividend to shareholders whenever it makes profit to

maintain faith of the investors in business operations.

Debt-equity ratio: Debt / Equity

Times interest ratio: time interest ratio is also known as time coverage ratio which

measures the proportionate income which company can use in meeting its interest

expenses (Bennouna and Marchant, 2010). It states firm ability to make debt interest

10

effectiveness in making use of the long term and short assets. This ratio will help

manager in assessing the success or failure of the assets (Evan and Porter, 2010). Total

asset turnover ratio provides idea to the manager about the isolation of plant and

machinery. It helps company in making right decision about the sales of the asset at the

right time and thereby improving the sales revenue.

Asset turnover ratio: Net sales / Total assets

Inventory turnover ratio: It helps in determining the capability of the company in

managing its inventory level. If it is too low then it indicates that firm fails to manage its

inventory and faces difficulties in pushing sales to customers (Burt and Amin, 2014). In

contrary to this, if inventory turnover ratio of the company is high then it shows that

inventory policy of the company is sound and it should follow the existing strategy to

manage its inventory level. It can measured as: (Cole, Branson and Breesch, 2012)

Inventory turnover ratio: Cost of goods sold / Average inventory

Gearing or Solvency ratios

Solvency ratio defines the cash position of the firm which encompasses that it is able to

meet its short term and long term liabilities.

Debt-equity ratio: This ratio shows the relative proportion of shareholders and debt which

are used by the corporation to finance the assets. To become a sound and well organized

firm, enterprise needs to make efforts so they come to near ideal debt equity ratio which

is .5:1 It represents that organization needs to raise more finance through equity shares

rather than debt (Siano, Kitchen and Confetto, 2010). Moreover, when company raise

finance through debt then it has to pay interest to the debt holders whether firm make

profit or not. In case of shares, company have no compulsion in relation to the payment

of dividend and there by reduces the financial burden (Erasmus and et.al., 2015). But

organization requires paying dividend to shareholders whenever it makes profit to

maintain faith of the investors in business operations.

Debt-equity ratio: Debt / Equity

Times interest ratio: time interest ratio is also known as time coverage ratio which

measures the proportionate income which company can use in meeting its interest

expenses (Bennouna and Marchant, 2010). It states firm ability to make debt interest

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

payment on time. It helps company in raising fund through debt instruments.

Organization can assess time interest ratio with the help of following formula such as:

Times interest ratio: Net income/ Interest expenses

Accounts receivable turnover: It entails that how many times company is able collect its

receivables from the debtors. It is the measure which enables company to identify the

period during which it is able to generate cash (Togashi and et.al., 2014). It also helps

company in making further investment and other cash related decisions.

Accounts receivable turnover: Net credit sales / Net receivables

Payment turnover ratio: It states the ability of the firm in relation to the payment of credit

purchase within a period (Perini and et.al., 2014). If company fails to make payment to

the supplier within a short period then it states that financial condition of the firm is too

weak. Through this, company is able to take corrective measure on time and take benefit

from it.

Payment turnover ratio: Net credit purchase / Average accounts payable (Siano, Kitchen,

and Confetto, 2010)

3 RESEARCH APPROACHES & METHODS

3.1 Introduction

It includes the methodology section of the research. It consists of research tools and

techniques which help in the data collection for the study. These tools help in achieving the

stated goals and objectives of the research. This section is very important from the research point

of view (Arthur, and et.al., 2012). It is the background against which the researcher evaluates the

findings and the conclusions.

3.2 Research approaches

Research Design

Research design is the blue print of the research. The study has used the survey design to

find out the effectiveness of the ratio analysis in making business decisions. It is appropriate for

the research because the study is descriptive and analytical in nature (Bruce and Martin 2012). It

is expected that this design will achieve the goals and objectives of the study.

Data Collection

11

Organization can assess time interest ratio with the help of following formula such as:

Times interest ratio: Net income/ Interest expenses

Accounts receivable turnover: It entails that how many times company is able collect its

receivables from the debtors. It is the measure which enables company to identify the

period during which it is able to generate cash (Togashi and et.al., 2014). It also helps

company in making further investment and other cash related decisions.

Accounts receivable turnover: Net credit sales / Net receivables

Payment turnover ratio: It states the ability of the firm in relation to the payment of credit

purchase within a period (Perini and et.al., 2014). If company fails to make payment to

the supplier within a short period then it states that financial condition of the firm is too

weak. Through this, company is able to take corrective measure on time and take benefit

from it.

Payment turnover ratio: Net credit purchase / Average accounts payable (Siano, Kitchen,

and Confetto, 2010)

3 RESEARCH APPROACHES & METHODS

3.1 Introduction

It includes the methodology section of the research. It consists of research tools and

techniques which help in the data collection for the study. These tools help in achieving the

stated goals and objectives of the research. This section is very important from the research point

of view (Arthur, and et.al., 2012). It is the background against which the researcher evaluates the

findings and the conclusions.

3.2 Research approaches

Research Design

Research design is the blue print of the research. The study has used the survey design to

find out the effectiveness of the ratio analysis in making business decisions. It is appropriate for

the research because the study is descriptive and analytical in nature (Bruce and Martin 2012). It

is expected that this design will achieve the goals and objectives of the study.

Data Collection

11

There are two main source of data collection which can be described as follows:

Primary Sources – It is the first hand information which is collected by the researcher

himself. It is very raw and fresh in nature. It is available through techniques such as

questionnaire, interview, focus group, direct observation (Chilisa, 2012). For this study

primary data has been collected through questionnaire approach. It is appropriate because

it helps in gathering large volume of data.

Secondary sources – It is the data available from published sources such as books,

journals, magazines, newspapers, articles etc. For this research secondary information has

been collected from company’s website, annual reports, journals, books etc (Dr. Lazar,

Dr. Feng and Dr. Hochheiser 2010).

Sampling

Sampling is done to identify the representative sample for the research from which the

valuable information can be obtained. This activity makes the data collection work easier and

simpler. For this research, purposive sampling has been applied. It is suitable because it helps in

selecting the sample on the basis of preference. The data has been collected from 10 managers of

Tesco. This sample size is appropriate according to the size and scale of the study.

Instrument for data collection

Data Collection is the most important part of the research. Secondary data is the

something that is available from published sources. It is available for use by anyone. For this

study, data will be collected from secondary sources such as books, journals, newspapers,

internet, annual reports of Tesco, etc (Giacomello, 2008). Questionnaire has been designed for

the data collection and analysis. The questionnaire used for the research is made up of 10

questions. It is constructed in a manner that alternative answers were produced for the

respondents (Kallio and Kallio, 2014). Questionnaires were distributed on random basis. It was

appropriate for the study because this tool helps in collecting large volume of data.

Data Analysis

For the purpose of data evaluation, technique of ratio analysis will be used. This tool will

judge the financial performance of Tesco on the basis of liquidity, solvency and turnover ratios.

This data analysis plan is appropriate because it fulfils the purpose of the study (Dey, 2002).

12

Primary Sources – It is the first hand information which is collected by the researcher

himself. It is very raw and fresh in nature. It is available through techniques such as

questionnaire, interview, focus group, direct observation (Chilisa, 2012). For this study

primary data has been collected through questionnaire approach. It is appropriate because

it helps in gathering large volume of data.

Secondary sources – It is the data available from published sources such as books,

journals, magazines, newspapers, articles etc. For this research secondary information has

been collected from company’s website, annual reports, journals, books etc (Dr. Lazar,

Dr. Feng and Dr. Hochheiser 2010).

Sampling

Sampling is done to identify the representative sample for the research from which the

valuable information can be obtained. This activity makes the data collection work easier and

simpler. For this research, purposive sampling has been applied. It is suitable because it helps in

selecting the sample on the basis of preference. The data has been collected from 10 managers of

Tesco. This sample size is appropriate according to the size and scale of the study.

Instrument for data collection

Data Collection is the most important part of the research. Secondary data is the

something that is available from published sources. It is available for use by anyone. For this

study, data will be collected from secondary sources such as books, journals, newspapers,

internet, annual reports of Tesco, etc (Giacomello, 2008). Questionnaire has been designed for

the data collection and analysis. The questionnaire used for the research is made up of 10

questions. It is constructed in a manner that alternative answers were produced for the

respondents (Kallio and Kallio, 2014). Questionnaires were distributed on random basis. It was

appropriate for the study because this tool helps in collecting large volume of data.

Data Analysis

For the purpose of data evaluation, technique of ratio analysis will be used. This tool will

judge the financial performance of Tesco on the basis of liquidity, solvency and turnover ratios.

This data analysis plan is appropriate because it fulfils the purpose of the study (Dey, 2002).

12

Along with that data collected from the questionnaire process has been presented in form of

graphs, tables and pie charts.

Ethical consideration

There are some ethical considerations associated with the research. Data has been

collected from valid and authentic sources. Further no manipulation has been done with the

information and it is presented in the same manner as it was derived (Kothari, 2004). During the

questionnaire process, complete freedom and liberty has been given to the participants. Before

commencing the process, goals and objectives were communicated to them in proper manner. No

data has been obtained directly from any source (Kotzab and et.al., 2006). Proper referencing and

citation has been done.

Research Limitations

Following limitations were encountered while the course of the research:

Lack of time

Lack of data

Convincing the participants

Pressure of quality (Walliman, 2011)

13

graphs, tables and pie charts.

Ethical consideration

There are some ethical considerations associated with the research. Data has been

collected from valid and authentic sources. Further no manipulation has been done with the

information and it is presented in the same manner as it was derived (Kothari, 2004). During the

questionnaire process, complete freedom and liberty has been given to the participants. Before

commencing the process, goals and objectives were communicated to them in proper manner. No

data has been obtained directly from any source (Kotzab and et.al., 2006). Proper referencing and

citation has been done.

Research Limitations

Following limitations were encountered while the course of the research:

Lack of time

Lack of data

Convincing the participants

Pressure of quality (Walliman, 2011)

13

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Questionnaire

Gender

Position in the company

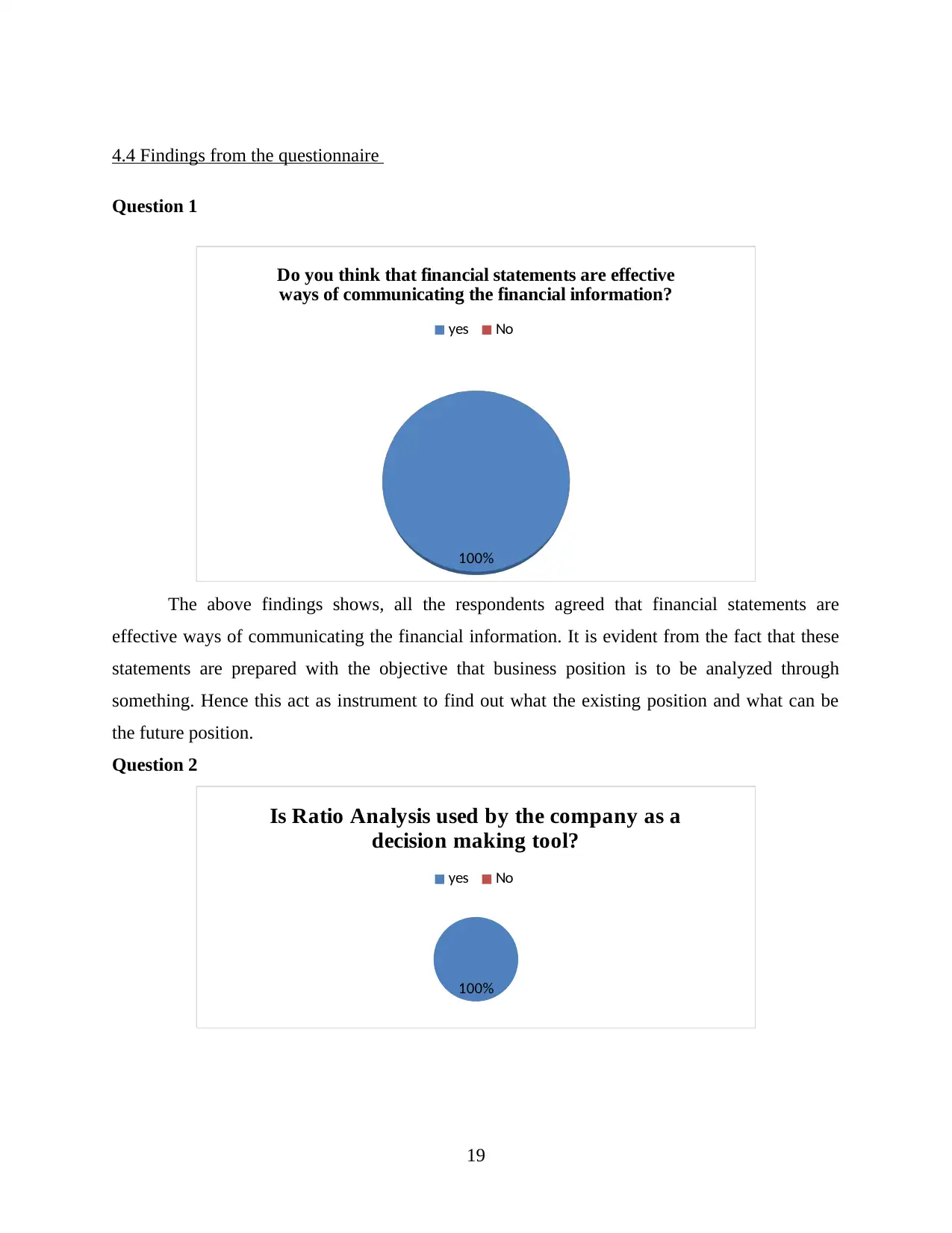

Do you think that financial statements are effective ways of communicating the financial

information?

Yes

No

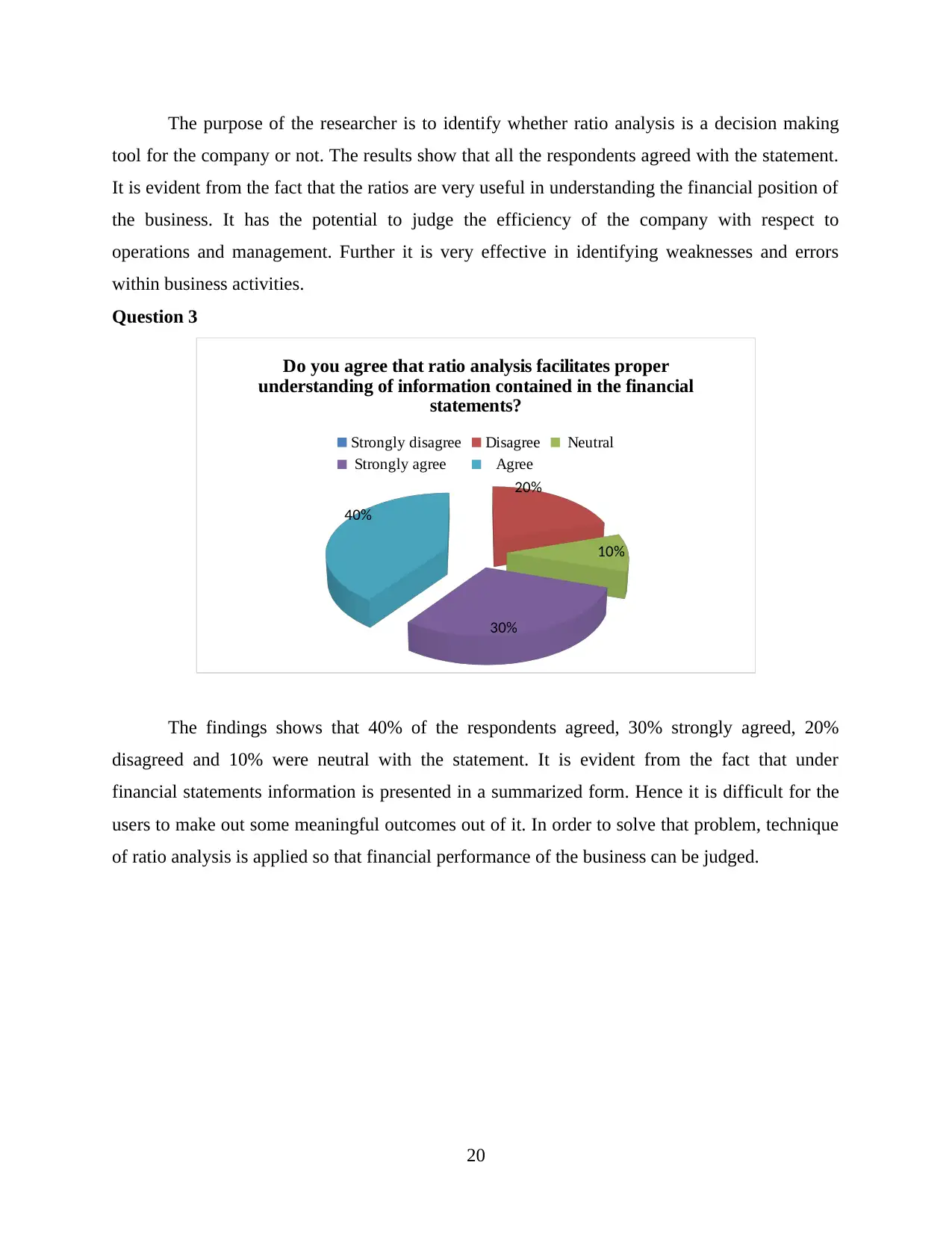

Is Ratio Analysis used by the company as a decision making tool?

Yes

No

Do you agree that ratio analysis facilitates proper understanding of information contained

in the financial statements?

Strongly disagree

Disagree

Neutral

Strongly agree

Agree

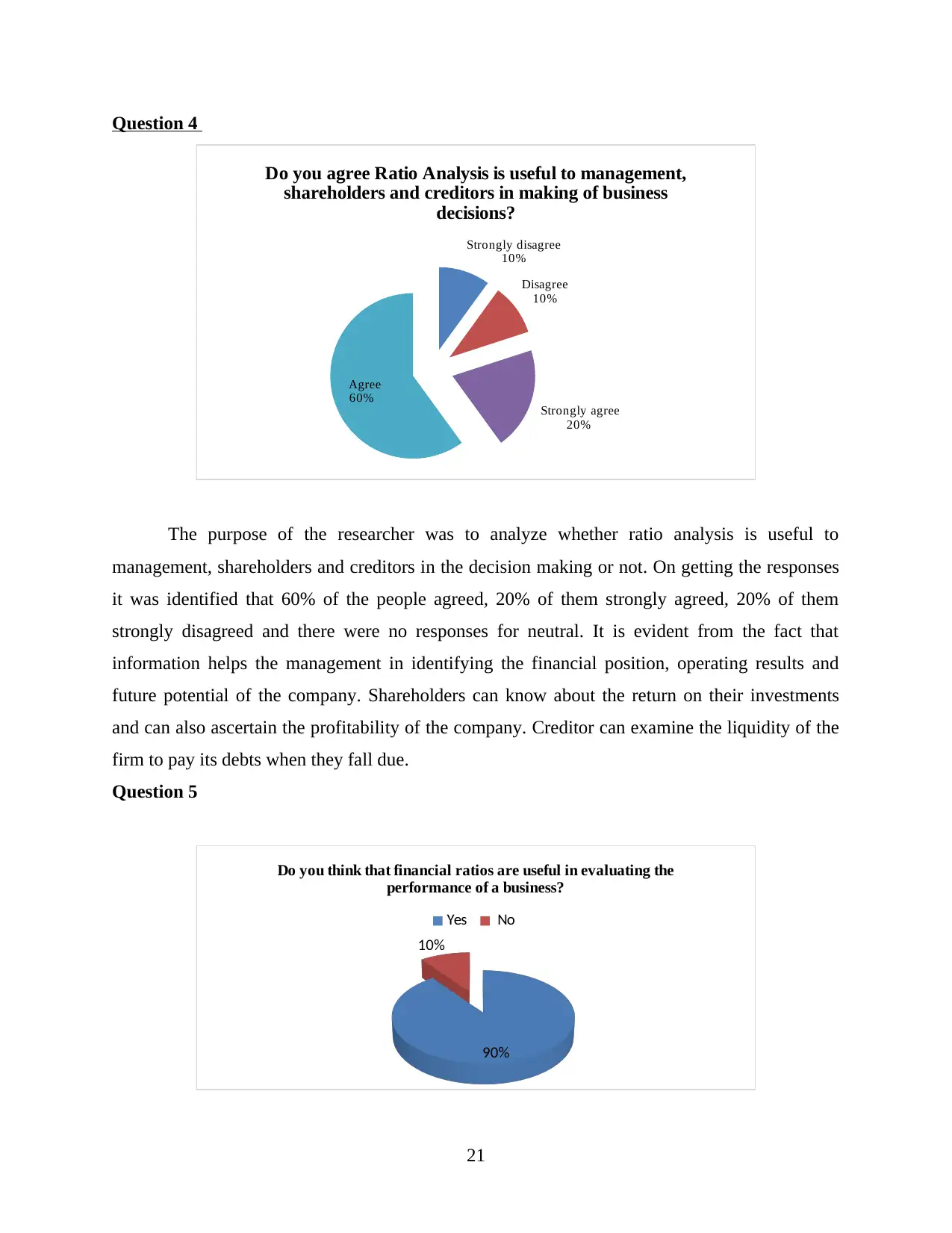

Do you agree Ratio Analysis is useful to management, shareholders and creditors in

making of business decisions?

Strongly disagree

Disagree

Neutral

Strongly agree

Agree

14

Gender

Position in the company

Do you think that financial statements are effective ways of communicating the financial

information?

Yes

No

Is Ratio Analysis used by the company as a decision making tool?

Yes

No

Do you agree that ratio analysis facilitates proper understanding of information contained

in the financial statements?

Strongly disagree

Disagree

Neutral

Strongly agree

Agree

Do you agree Ratio Analysis is useful to management, shareholders and creditors in

making of business decisions?

Strongly disagree

Disagree

Neutral

Strongly agree

Agree

14

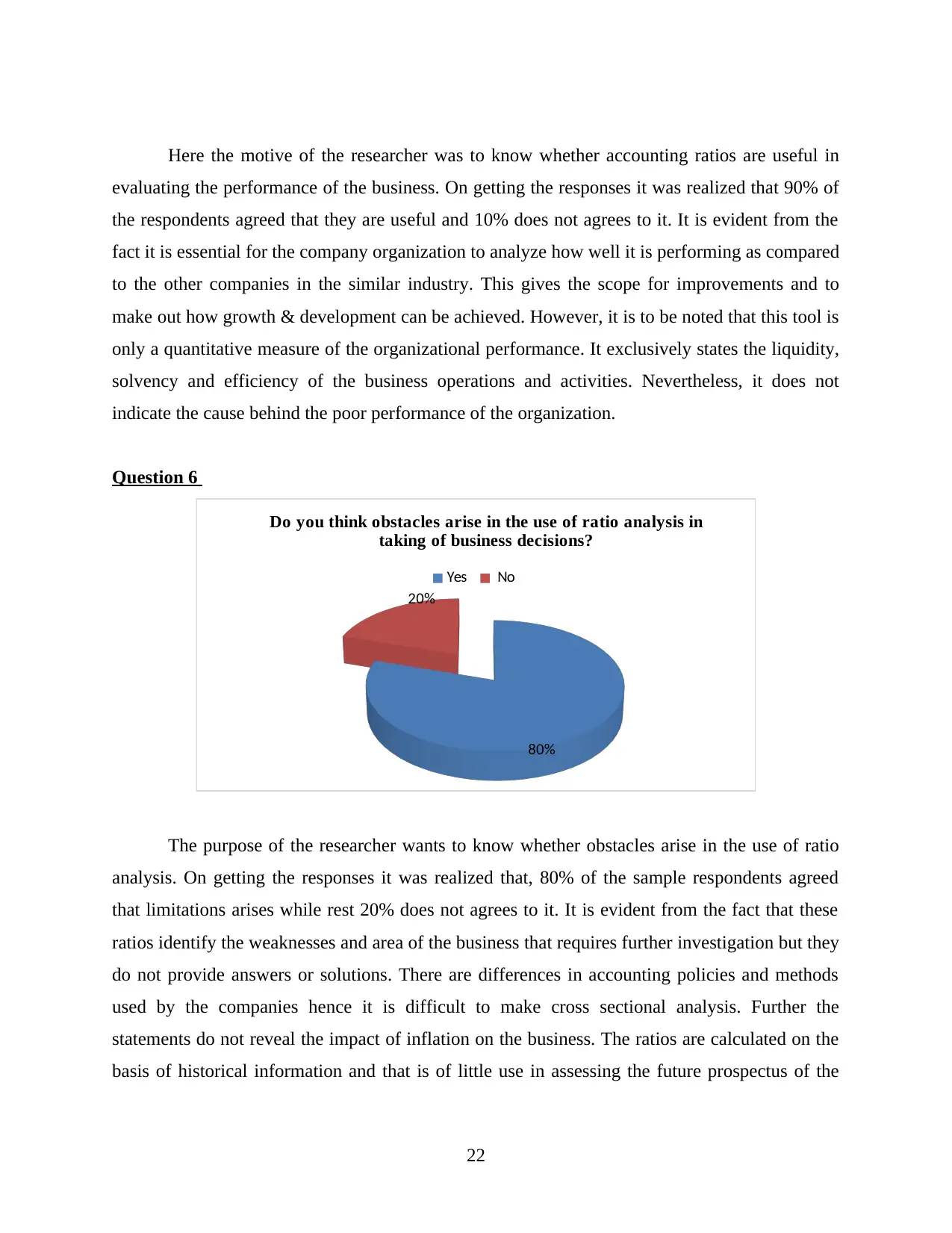

Do you think that financial ratios are useful in evaluating the performance of a business?

Yes

No

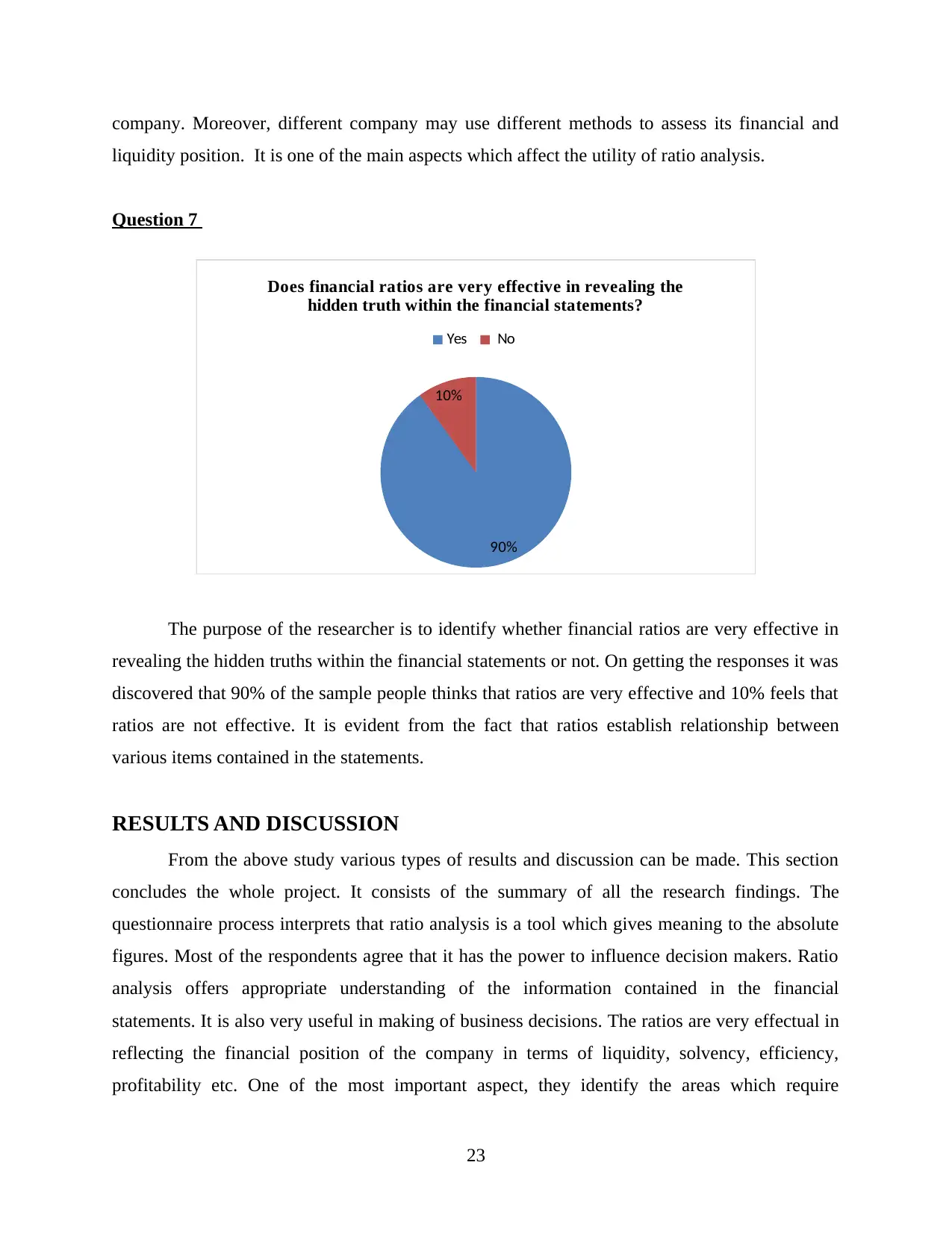

Do you think obstacles arise in the use of ratio analysis in taking of business decisions?

Yes

No

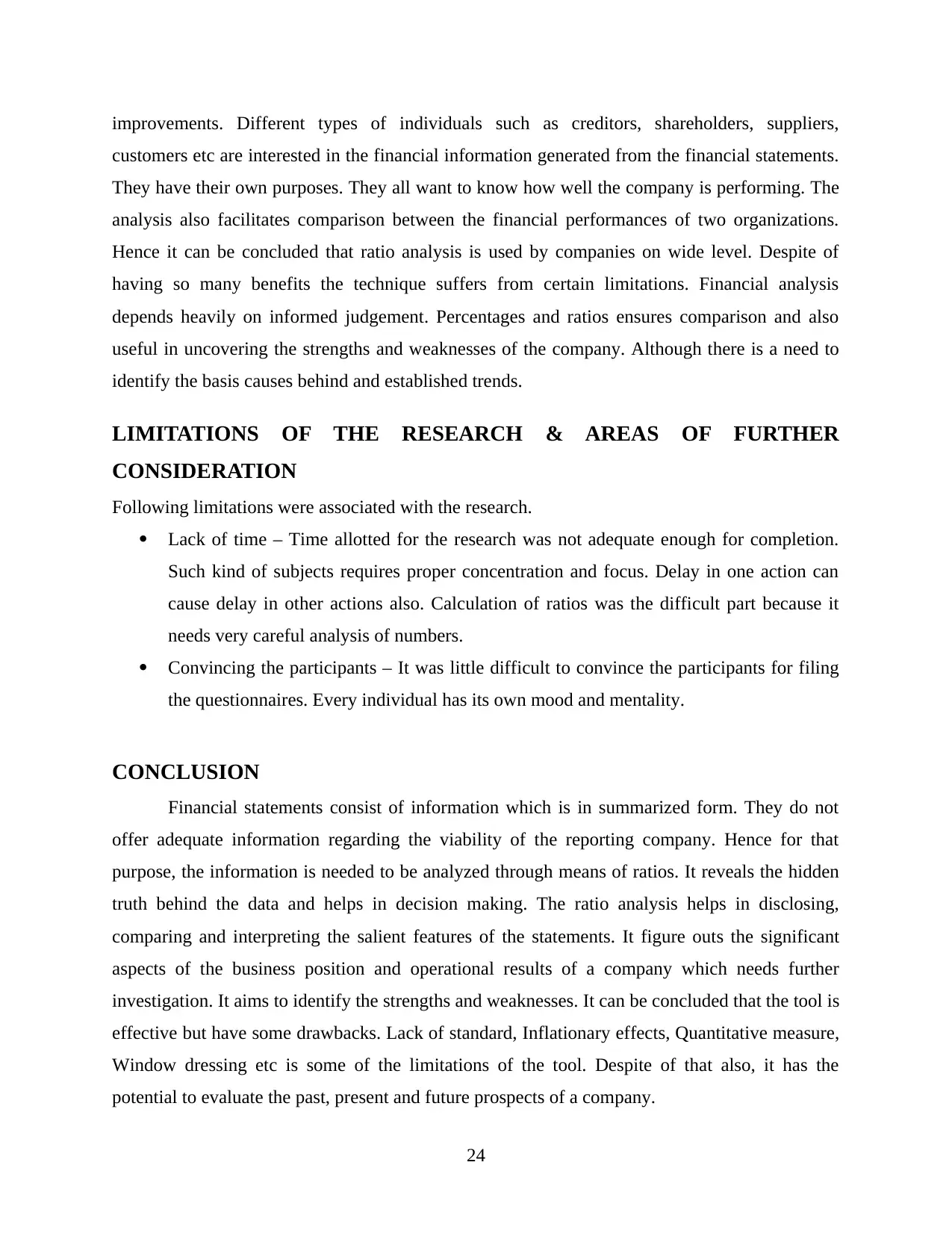

Does financial ratios are very effective in revealing the hidden truth within the financial

statements?

Yes

No

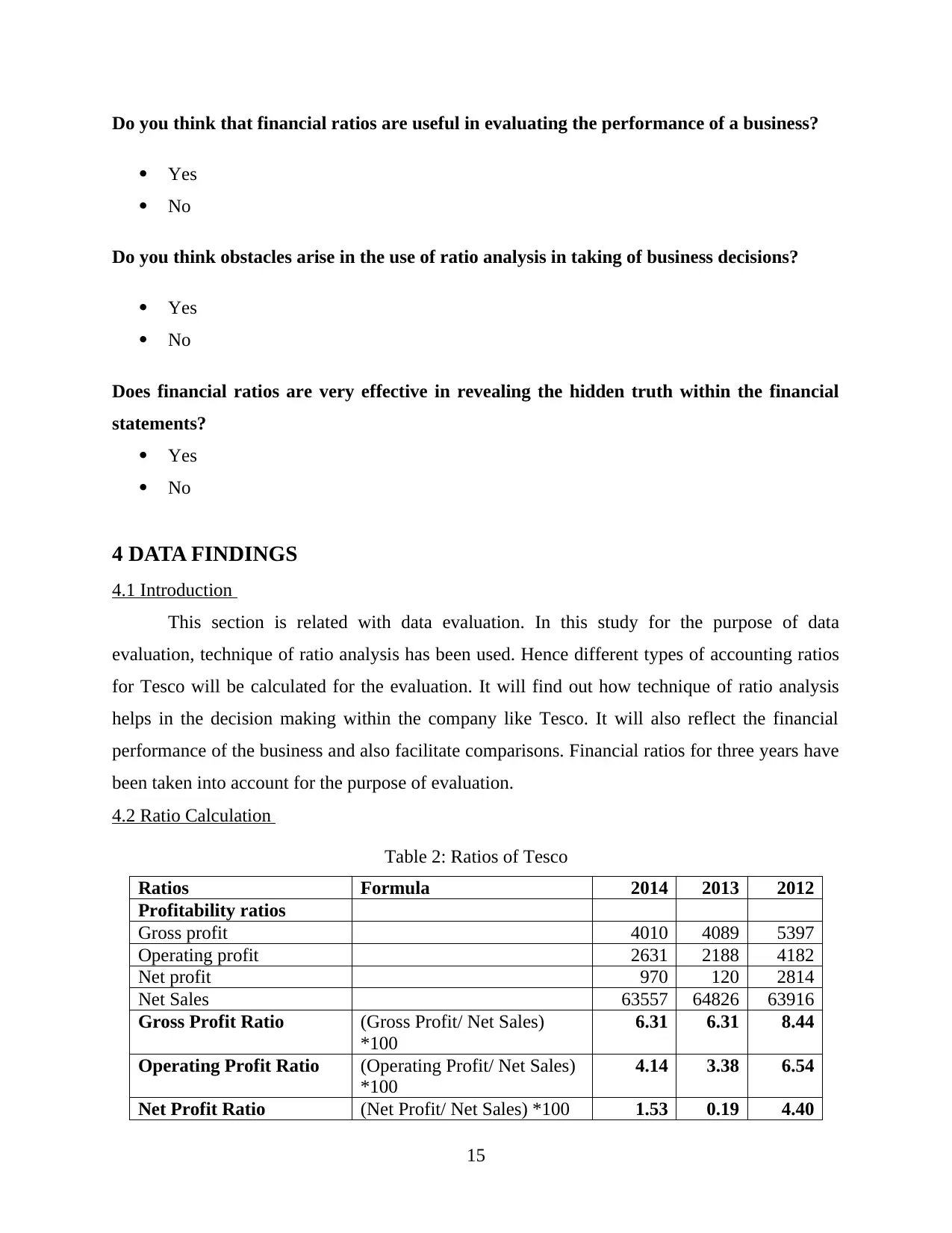

4 DATA FINDINGS

4.1 Introduction

This section is related with data evaluation. In this study for the purpose of data

evaluation, technique of ratio analysis has been used. Hence different types of accounting ratios

for Tesco will be calculated for the evaluation. It will find out how technique of ratio analysis

helps in the decision making within the company like Tesco. It will also reflect the financial

performance of the business and also facilitate comparisons. Financial ratios for three years have

been taken into account for the purpose of evaluation.

4.2 Ratio Calculation

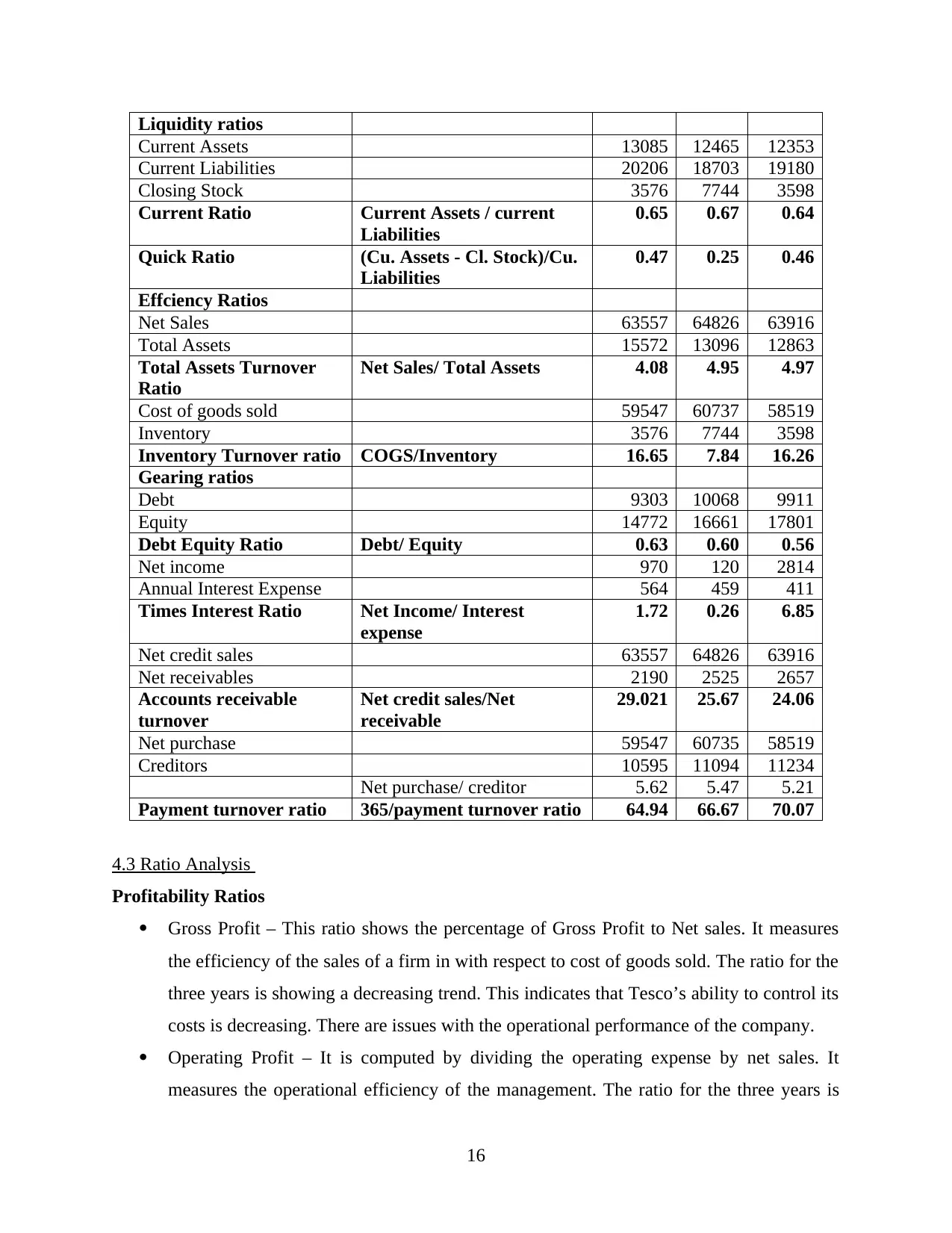

Table 2: Ratios of Tesco

Ratios Formula 2014 2013 2012

Profitability ratios

Gross profit 4010 4089 5397

Operating profit 2631 2188 4182

Net profit 970 120 2814

Net Sales 63557 64826 63916

Gross Profit Ratio (Gross Profit/ Net Sales)

*100

6.31 6.31 8.44

Operating Profit Ratio (Operating Profit/ Net Sales)

*100

4.14 3.38 6.54

Net Profit Ratio (Net Profit/ Net Sales) *100 1.53 0.19 4.40

15

Yes

No

Do you think obstacles arise in the use of ratio analysis in taking of business decisions?

Yes

No

Does financial ratios are very effective in revealing the hidden truth within the financial

statements?

Yes

No

4 DATA FINDINGS

4.1 Introduction

This section is related with data evaluation. In this study for the purpose of data

evaluation, technique of ratio analysis has been used. Hence different types of accounting ratios

for Tesco will be calculated for the evaluation. It will find out how technique of ratio analysis

helps in the decision making within the company like Tesco. It will also reflect the financial

performance of the business and also facilitate comparisons. Financial ratios for three years have

been taken into account for the purpose of evaluation.

4.2 Ratio Calculation

Table 2: Ratios of Tesco

Ratios Formula 2014 2013 2012

Profitability ratios

Gross profit 4010 4089 5397

Operating profit 2631 2188 4182

Net profit 970 120 2814

Net Sales 63557 64826 63916

Gross Profit Ratio (Gross Profit/ Net Sales)

*100

6.31 6.31 8.44

Operating Profit Ratio (Operating Profit/ Net Sales)

*100

4.14 3.38 6.54

Net Profit Ratio (Net Profit/ Net Sales) *100 1.53 0.19 4.40

15

Liquidity ratios

Current Assets 13085 12465 12353

Current Liabilities 20206 18703 19180

Closing Stock 3576 7744 3598

Current Ratio Current Assets / current

Liabilities

0.65 0.67 0.64

Quick Ratio (Cu. Assets - Cl. Stock)/Cu.

Liabilities

0.47 0.25 0.46

Effciency Ratios

Net Sales 63557 64826 63916

Total Assets 15572 13096 12863

Total Assets Turnover

Ratio

Net Sales/ Total Assets 4.08 4.95 4.97

Cost of goods sold 59547 60737 58519

Inventory 3576 7744 3598

Inventory Turnover ratio COGS/Inventory 16.65 7.84 16.26

Gearing ratios

Debt 9303 10068 9911

Equity 14772 16661 17801

Debt Equity Ratio Debt/ Equity 0.63 0.60 0.56

Net income 970 120 2814

Annual Interest Expense 564 459 411

Times Interest Ratio Net Income/ Interest

expense

1.72 0.26 6.85

Net credit sales 63557 64826 63916

Net receivables 2190 2525 2657

Accounts receivable

turnover

Net credit sales/Net

receivable

29.021 25.67 24.06

Net purchase 59547 60735 58519

Creditors 10595 11094 11234

Net purchase/ creditor 5.62 5.47 5.21

Payment turnover ratio 365/payment turnover ratio 64.94 66.67 70.07

4.3 Ratio Analysis

Profitability Ratios

Gross Profit – This ratio shows the percentage of Gross Profit to Net sales. It measures

the efficiency of the sales of a firm in with respect to cost of goods sold. The ratio for the

three years is showing a decreasing trend. This indicates that Tesco’s ability to control its

costs is decreasing. There are issues with the operational performance of the company.

Operating Profit – It is computed by dividing the operating expense by net sales. It

measures the operational efficiency of the management. The ratio for the three years is

16

Current Assets 13085 12465 12353

Current Liabilities 20206 18703 19180

Closing Stock 3576 7744 3598

Current Ratio Current Assets / current

Liabilities

0.65 0.67 0.64

Quick Ratio (Cu. Assets - Cl. Stock)/Cu.

Liabilities

0.47 0.25 0.46

Effciency Ratios

Net Sales 63557 64826 63916

Total Assets 15572 13096 12863

Total Assets Turnover

Ratio

Net Sales/ Total Assets 4.08 4.95 4.97

Cost of goods sold 59547 60737 58519

Inventory 3576 7744 3598

Inventory Turnover ratio COGS/Inventory 16.65 7.84 16.26

Gearing ratios

Debt 9303 10068 9911

Equity 14772 16661 17801

Debt Equity Ratio Debt/ Equity 0.63 0.60 0.56

Net income 970 120 2814

Annual Interest Expense 564 459 411

Times Interest Ratio Net Income/ Interest

expense

1.72 0.26 6.85

Net credit sales 63557 64826 63916

Net receivables 2190 2525 2657

Accounts receivable

turnover

Net credit sales/Net

receivable

29.021 25.67 24.06

Net purchase 59547 60735 58519

Creditors 10595 11094 11234

Net purchase/ creditor 5.62 5.47 5.21

Payment turnover ratio 365/payment turnover ratio 64.94 66.67 70.07

4.3 Ratio Analysis

Profitability Ratios

Gross Profit – This ratio shows the percentage of Gross Profit to Net sales. It measures

the efficiency of the sales of a firm in with respect to cost of goods sold. The ratio for the

three years is showing a decreasing trend. This indicates that Tesco’s ability to control its

costs is decreasing. There are issues with the operational performance of the company.

Operating Profit – It is computed by dividing the operating expense by net sales. It

measures the operational efficiency of the management. The ratio for the three years is

16

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

showing a fluctuating trend which means Tesco must concentrate on improving its

operational performance. The ratio needs to be stagnant.

Net Profit Ratio – It shows the ability of the company to control operating and non-

operating expenses. Decrease in the net profit ratio can be noticed. It shows that Tesco is

finding difficult to control its operating and non-operating expenses.

Liquidity Ratio

Current Ratio – It evaluates the short term solvency position of the company. The ratio

for the three years is showing a very consistent trend but it is very low from business

point of view. It shows that Tesco is finding issues in fulfilling its short term obligations.

Quick ratio - It examines the potential of the company in paying its short term debts. It

measures the relationship between liquid assets and current liabilities. The ratio appears

to be less than 1 which indicates that company is having fast moving inventories.

Efficiency Ratios

Total Assets Turnover Ratio – It measure the efficiency of the assets within the company.

Tesco has able to maintain a very successful assets turnover ratio in the last three years. It

means every dollar invested in the assets of Tesco produces 4.50% of the sales. It means

company is using its assets in best manner.

Inventory turnover ratio – It evaluate the liquidity of inventories of an organization. It

shows how many times the inventory has been replaced and sold during a certain period

of time. This ratio for the three years is showing a very fluctuating trend. Tesco takes 28

days to sell its average inventory. It shows that there is a very effective management of

stocks and it is possible through effective supply chain management.

Gearing Ratios