Financial Performance Analysis of Reckitt Benckiser (2010-2014)

VerifiedAdded on 2019/12/28

|10

|3699

|72

Report

AI Summary

This report provides a comprehensive financial analysis of Reckitt Benckiser (RB), a multinational consumer goods company, focusing on its performance from 2010 to 2014. The analysis includes an examination of various financial ratios, such as profitability, liquidity, working capital management, capital structure, and stock market performance. The report delves into the rationale behind selecting RB, highlighting its global presence and the importance of ratio analysis in understanding its financial position relative to competitors. The performance analysis covers key ratios like gross profit margin, current ratio, and debt-to-equity ratio, providing insights into RB's ability to generate profits, manage short-term obligations, and finance its operations. The report concludes with an assessment of RB's financial strengths and weaknesses, offering recommendations for future financial strategies and improvements. The findings reveal fluctuations in profitability, challenges in meeting short-term obligations, and varying trends in leverage and working capital, providing a detailed picture of RB's financial health during the analyzed period.

Financial Analysis

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION................................................................................................................................3

RATIONALE .......................................................................................................................................3

PERFORMANCE ANALYSIS ...........................................................................................................4

Summary of the analysis..................................................................................................................7

LIMITATIONS.....................................................................................................................................7

CONCLUSION ...................................................................................................................................8

RECOMMENDATION .......................................................................................................................9

REFERENCES...................................................................................................................................10

INTRODUCTION................................................................................................................................3

RATIONALE .......................................................................................................................................3

PERFORMANCE ANALYSIS ...........................................................................................................4

Summary of the analysis..................................................................................................................7

LIMITATIONS.....................................................................................................................................7

CONCLUSION ...................................................................................................................................8

RECOMMENDATION .......................................................................................................................9

REFERENCES...................................................................................................................................10

INTRODUCTION

Reckitt Benckiser is a multinational organisation headquartered in London. It produces

consumer goods in the area of hygiene, health and home care. It was formed in 1999 by a merger of

Reckitt & Colman plc and Benckiser NV. The company visions to make the lifestyle of people

better and healthier. Reckitt Benckiser i.e. RB wants to make a difference in the lifestyle of

consumers by generating innovative alternatives for them. It is among the most fast pace growing

company in the world. In the year 2014 particularly RB has generated greater performance. This

was achieved by a purpose driven strategy to enhance revenue and sales for the company. The

purpose of this report is to conduct a study on the financial rations of the company (Uechi and et.al.,

2015). RB is selected for the project as operates around 60 countries and have vast international

presence. Study and comparison of financial ratios is done in order to identify competencies of the

company over the competitors. Financial analysis consists of evaluating figures acquired from

profitability, debt paying ability, liquidity, efficiency and various other factors. The report discusses

about viability, profitability and stability of Reckitt Benckiser over a span of five years. Thus, in

order to do that financial figures ranging from 2010-2012 are assessed and analysed.

RATIONALE

Globalization today has reached to a new height. RB wants to create new products and

provide better services to the consumers. In order to that company have formulated various

strategies over the time. Some of them have proved to be beneficial and raised profitability for the

company. On the other hand, at many instances company failed to achieve desired financial figures

at the end of the year. Reckitt Benckiser is a big name in the United Kingdom as well as other

international markets. It is among the leading organisation that manufactures wide variety of

consumer goods for the public. This company is selected for the research as it is a widely

proclaimed brand and has created various benefits for the economy of UK as well. The main

products are classified under health, home and hygiene. The company has brought great innovations

in the field of pharmaceuticals as well. This company is selected for ratio analysis as it generates

huge revenues and profits. It is important to analyse these ratios to identify the true financial

position of RB in the consumer good industry (Brigham and Ehrhardt, 2013). The rising pressure of

competition and pricing strategies of the companies has created greater pressure for Rb to operate

its business prospects. Company has made profits and incurred losses in many quadrants as well.

RB is responsible to shape the economy of United Kingdom by raising its standard to international

boundary. The company is known to provide employment to thousands of individuals in the United

Kingdom itself. Thus, it is viable to select this company in order to evaluate the financial aspects

and money making strategies of the company. Although the company has a good goodwill in the

Reckitt Benckiser is a multinational organisation headquartered in London. It produces

consumer goods in the area of hygiene, health and home care. It was formed in 1999 by a merger of

Reckitt & Colman plc and Benckiser NV. The company visions to make the lifestyle of people

better and healthier. Reckitt Benckiser i.e. RB wants to make a difference in the lifestyle of

consumers by generating innovative alternatives for them. It is among the most fast pace growing

company in the world. In the year 2014 particularly RB has generated greater performance. This

was achieved by a purpose driven strategy to enhance revenue and sales for the company. The

purpose of this report is to conduct a study on the financial rations of the company (Uechi and et.al.,

2015). RB is selected for the project as operates around 60 countries and have vast international

presence. Study and comparison of financial ratios is done in order to identify competencies of the

company over the competitors. Financial analysis consists of evaluating figures acquired from

profitability, debt paying ability, liquidity, efficiency and various other factors. The report discusses

about viability, profitability and stability of Reckitt Benckiser over a span of five years. Thus, in

order to do that financial figures ranging from 2010-2012 are assessed and analysed.

RATIONALE

Globalization today has reached to a new height. RB wants to create new products and

provide better services to the consumers. In order to that company have formulated various

strategies over the time. Some of them have proved to be beneficial and raised profitability for the

company. On the other hand, at many instances company failed to achieve desired financial figures

at the end of the year. Reckitt Benckiser is a big name in the United Kingdom as well as other

international markets. It is among the leading organisation that manufactures wide variety of

consumer goods for the public. This company is selected for the research as it is a widely

proclaimed brand and has created various benefits for the economy of UK as well. The main

products are classified under health, home and hygiene. The company has brought great innovations

in the field of pharmaceuticals as well. This company is selected for ratio analysis as it generates

huge revenues and profits. It is important to analyse these ratios to identify the true financial

position of RB in the consumer good industry (Brigham and Ehrhardt, 2013). The rising pressure of

competition and pricing strategies of the companies has created greater pressure for Rb to operate

its business prospects. Company has made profits and incurred losses in many quadrants as well.

RB is responsible to shape the economy of United Kingdom by raising its standard to international

boundary. The company is known to provide employment to thousands of individuals in the United

Kingdom itself. Thus, it is viable to select this company in order to evaluate the financial aspects

and money making strategies of the company. Although the company has a good goodwill in the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

market, one can analyse financial strengths and loopholes only by studying the ratios of the

organisation. Hence, to identify the feasibility for future prospects of Rb ratios analysis is done on

the company.

PERFORMANCE ANALYSIS

1. Profitability Ratio- It is a measure to evaluate companies’ profile. It is the main objective

of a company to make profit. Each year RB must aim to increase the profits made from last

year. Profit is the left over part after sailing has been performed in an organisation. Any

organization has to decide for a cost price which includes manufacturing charges of the

product. When a company sells certain products it receives amount. This amount is termed

as the selling price. Profitability ratio is used to analyse the income generated from selling a

product. It shows the capacity of an organization to make profits for the company. In order

to that income statement are compared to calculate the amount yielded from the operations

conducted by the business. It also shows how good a company is performing. For example,

if RB is registering consecutive profits in years (Dokas, Giokas and Tsamis, 2014). This

means that the company is making good profits and all the expenses incurred are been

recovered by the organisation. There are various different ratios used to analyse the

profitability of an organisation. Like gross profit margin, operating margin, return on equity

and many more. This ratio particularly tells about the cost incurred and revenue received by

the company for sale of goods and services.

2. Liquidity Ratio- The relation of liquid assets of a company with the liability to be paid are

used under liquidity ratio. Liquidity for an organisation is defined as the ability of an

organisation to pay its financial debts to the respective party. Thus, it can be stated that

liquidity ratios is used to identify RB's capability to pay for its short term debt. It is very

relevant for an enterprise to pay for its debt within a period. This is done to not let the debts

or liabilities become due for a longer period of time. Liquidity ratios shows the cash

available for the company in terms of current assets. This cash or assets are used to pay the

debts incurred by the organisation. It is considered good for the brand image of an

organisation to be quickly able to convert its current assets into cash to pay of any urgent

dues or liability (Jarrow and Chatterjea, 2013). If the company is not able to raise enough

cash in a shorter period then it is not considered idle for the financial position of a company.

In a business the firm may require to anytime sale its assets like trading securities or

inventory to get cash. If the organisation is able to generate cash out of current assets, only

then it is able to meet with liquidity requirements.

3. Working Capital Management- These ratios is calculated to ensure that the organization is

organisation. Hence, to identify the feasibility for future prospects of Rb ratios analysis is done on

the company.

PERFORMANCE ANALYSIS

1. Profitability Ratio- It is a measure to evaluate companies’ profile. It is the main objective

of a company to make profit. Each year RB must aim to increase the profits made from last

year. Profit is the left over part after sailing has been performed in an organisation. Any

organization has to decide for a cost price which includes manufacturing charges of the

product. When a company sells certain products it receives amount. This amount is termed

as the selling price. Profitability ratio is used to analyse the income generated from selling a

product. It shows the capacity of an organization to make profits for the company. In order

to that income statement are compared to calculate the amount yielded from the operations

conducted by the business. It also shows how good a company is performing. For example,

if RB is registering consecutive profits in years (Dokas, Giokas and Tsamis, 2014). This

means that the company is making good profits and all the expenses incurred are been

recovered by the organisation. There are various different ratios used to analyse the

profitability of an organisation. Like gross profit margin, operating margin, return on equity

and many more. This ratio particularly tells about the cost incurred and revenue received by

the company for sale of goods and services.

2. Liquidity Ratio- The relation of liquid assets of a company with the liability to be paid are

used under liquidity ratio. Liquidity for an organisation is defined as the ability of an

organisation to pay its financial debts to the respective party. Thus, it can be stated that

liquidity ratios is used to identify RB's capability to pay for its short term debt. It is very

relevant for an enterprise to pay for its debt within a period. This is done to not let the debts

or liabilities become due for a longer period of time. Liquidity ratios shows the cash

available for the company in terms of current assets. This cash or assets are used to pay the

debts incurred by the organisation. It is considered good for the brand image of an

organisation to be quickly able to convert its current assets into cash to pay of any urgent

dues or liability (Jarrow and Chatterjea, 2013). If the company is not able to raise enough

cash in a shorter period then it is not considered idle for the financial position of a company.

In a business the firm may require to anytime sale its assets like trading securities or

inventory to get cash. If the organisation is able to generate cash out of current assets, only

then it is able to meet with liquidity requirements.

3. Working Capital Management- These ratios is calculated to ensure that the organization is

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

able to meet with the objectives and goals of its operations. Working capital management

refers to the ability of the organization to manage its inventories, cash, accounts receivables

etc. These ratios are also calculated to identify the maturity of upcoming operational

expenses and short term debt that has to be paid by the company. Any organisation is

required to have sufficient cash flow to meet the requirements of various business activity of

an organisation. Working capital turnover ratio, accounts receivables turnover ratio,

inventory turnover ratio etc. are used to identify the working capital of the company. In

basic working capital is calculated on the basis of the difference between current assets and

liabilities. Here current assets do not include cash (Adrian and Shin, 2014). An ideal

working capital cycle consists of 12 months and it is very critical for a company to pay its

long term debts in that period. An increased working capital ratios depicts that business has

increased its current assets or decreased its current liabilities. For example, if RB has paid its

creditors then the liability side of the balance sheet will reduce.

4. Capital Structure- A capital structure is the ability of the firm to finance its business

prospects to increase growth and profitability for itself. In general capital structure consists

of long term debt, equity and short term debt. This is because these are the sources from

where Reckitt Benckiser can raise its finances. While studying capital structure of a

company it is important to analyse the long term debt proportion to short term. This is

because when a company shows its capital structure it depicts debt to equity ratio (Brigham

and Ehrhardt, 2013). For example if a company raises $10 billion through equity and $90

billion through debt. It will be said that particular company is 10% financed by equity and

90% financed by debt. Thus, capital structure of a company is made up of debt and equity

proportions. The long term dent in capital structure refers to permanent financing. Each

component in capital structure has different cost associated to them. For example, capital

raised through equity is referred to as the capital raised to conduct business operations.

Whereas borrowings are the liabilities for a business. The cost incurred for both the

elements are different in respect to the business particulars of Reckitt Benckiser.

5. Stock Market Performance- These are also refereed to as market measure ratios as these

measures the invested stock by investors in the company. The shareholders are the

individuals who invest their money in shares of a company. They expect a return on

investment on the respective amount bought through shares. The basic relationship with

market and company is the return on value invested in the company. They also demonstrate

the price per share or earnings, assets or growth (Rose and Hudgins, 2014). The ratios used

to analyse stick market performance of a company are earning per share, dividend payout

and price earning share. These ratios are proved to be beneficial for the investors as they like

refers to the ability of the organization to manage its inventories, cash, accounts receivables

etc. These ratios are also calculated to identify the maturity of upcoming operational

expenses and short term debt that has to be paid by the company. Any organisation is

required to have sufficient cash flow to meet the requirements of various business activity of

an organisation. Working capital turnover ratio, accounts receivables turnover ratio,

inventory turnover ratio etc. are used to identify the working capital of the company. In

basic working capital is calculated on the basis of the difference between current assets and

liabilities. Here current assets do not include cash (Adrian and Shin, 2014). An ideal

working capital cycle consists of 12 months and it is very critical for a company to pay its

long term debts in that period. An increased working capital ratios depicts that business has

increased its current assets or decreased its current liabilities. For example, if RB has paid its

creditors then the liability side of the balance sheet will reduce.

4. Capital Structure- A capital structure is the ability of the firm to finance its business

prospects to increase growth and profitability for itself. In general capital structure consists

of long term debt, equity and short term debt. This is because these are the sources from

where Reckitt Benckiser can raise its finances. While studying capital structure of a

company it is important to analyse the long term debt proportion to short term. This is

because when a company shows its capital structure it depicts debt to equity ratio (Brigham

and Ehrhardt, 2013). For example if a company raises $10 billion through equity and $90

billion through debt. It will be said that particular company is 10% financed by equity and

90% financed by debt. Thus, capital structure of a company is made up of debt and equity

proportions. The long term dent in capital structure refers to permanent financing. Each

component in capital structure has different cost associated to them. For example, capital

raised through equity is referred to as the capital raised to conduct business operations.

Whereas borrowings are the liabilities for a business. The cost incurred for both the

elements are different in respect to the business particulars of Reckitt Benckiser.

5. Stock Market Performance- These are also refereed to as market measure ratios as these

measures the invested stock by investors in the company. The shareholders are the

individuals who invest their money in shares of a company. They expect a return on

investment on the respective amount bought through shares. The basic relationship with

market and company is the return on value invested in the company. They also demonstrate

the price per share or earnings, assets or growth (Rose and Hudgins, 2014). The ratios used

to analyse stick market performance of a company are earning per share, dividend payout

and price earning share. These ratios are proved to be beneficial for the investors as they like

to know how much profit is generated by each share.

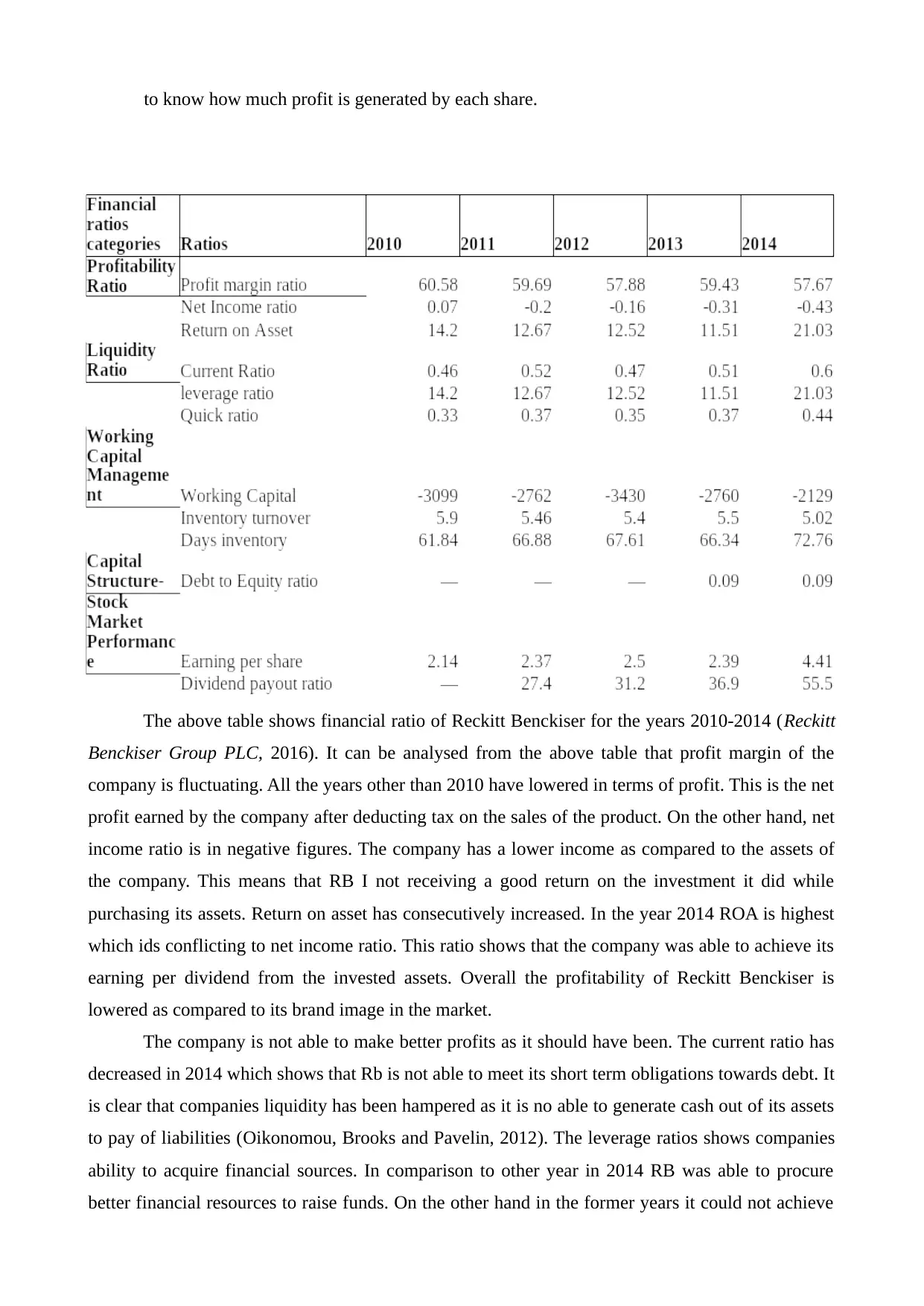

The above table shows financial ratio of Reckitt Benckiser for the years 2010-2014 (Reckitt

Benckiser Group PLC, 2016). It can be analysed from the above table that profit margin of the

company is fluctuating. All the years other than 2010 have lowered in terms of profit. This is the net

profit earned by the company after deducting tax on the sales of the product. On the other hand, net

income ratio is in negative figures. The company has a lower income as compared to the assets of

the company. This means that RB I not receiving a good return on the investment it did while

purchasing its assets. Return on asset has consecutively increased. In the year 2014 ROA is highest

which ids conflicting to net income ratio. This ratio shows that the company was able to achieve its

earning per dividend from the invested assets. Overall the profitability of Reckitt Benckiser is

lowered as compared to its brand image in the market.

The company is not able to make better profits as it should have been. The current ratio has

decreased in 2014 which shows that Rb is not able to meet its short term obligations towards debt. It

is clear that companies liquidity has been hampered as it is no able to generate cash out of its assets

to pay of liabilities (Oikonomou, Brooks and Pavelin, 2012). The leverage ratios shows companies

ability to acquire financial sources. In comparison to other year in 2014 RB was able to procure

better financial resources to raise funds. On the other hand in the former years it could not achieve

The above table shows financial ratio of Reckitt Benckiser for the years 2010-2014 (Reckitt

Benckiser Group PLC, 2016). It can be analysed from the above table that profit margin of the

company is fluctuating. All the years other than 2010 have lowered in terms of profit. This is the net

profit earned by the company after deducting tax on the sales of the product. On the other hand, net

income ratio is in negative figures. The company has a lower income as compared to the assets of

the company. This means that RB I not receiving a good return on the investment it did while

purchasing its assets. Return on asset has consecutively increased. In the year 2014 ROA is highest

which ids conflicting to net income ratio. This ratio shows that the company was able to achieve its

earning per dividend from the invested assets. Overall the profitability of Reckitt Benckiser is

lowered as compared to its brand image in the market.

The company is not able to make better profits as it should have been. The current ratio has

decreased in 2014 which shows that Rb is not able to meet its short term obligations towards debt. It

is clear that companies liquidity has been hampered as it is no able to generate cash out of its assets

to pay of liabilities (Oikonomou, Brooks and Pavelin, 2012). The leverage ratios shows companies

ability to acquire financial sources. In comparison to other year in 2014 RB was able to procure

better financial resources to raise funds. On the other hand in the former years it could not achieve

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

its leverage targets. It also shows companies ability to pay off its debt from the collected sources off

finance. This ratio also shows companies ability handle debt load.

It can be analysed that Reckitt Benckiser is able handle the excessive load of debt payment

and has a good goodwill in the market. According to the Quick ratio companies financial strength

has increased over the years. It has recovered its financial strength and was able to gain greater

liquidity and pay off its debts. A negative working capital shows that RB's current assets are less

than its current liabilities. Although the working capital has consecutively come in negative

numbers but it has also declined. This shows that Reckitt Benckiser is recovering from its due on

the liabilities (Hull, 2012). But it still requires increase in its current assets over liabilities to achieve

a positive working capital. A high number of days inventory ratios depicts that sales are increased

over the time. This is considered as a good condition for the company as it is able to sell its

products and goods.

On the other hand inventory turnover ratios shows that a lot of products are getting

overstocked. Hence, it can be said that although Rb is selling in good numbers it still requires

speeding up. This can be done to maintain the speed of inventory that has to be yet sold out in the

market. It is considered ideal for the investor while investing money in the company if it is able to

effectively manger its inventory (Kaplan and Atkinson, 2015). An increase in the earning per share

proves that company is making good profits per every stock of share. It is clear that now companies

position has improved as it is relatively earned better profits. A high dividend payout ratio shows

that share prices of the company will not increase their value in the market.

Summary of the analysis

From the above analysis it is clear that company is making good improvement with regard to

the past financial figures. The profitability ratios depicted that company is making good profits. But

it can still strive to achieve better figure of profit by increasing selling. This is due to the fact that

Reckitt Benckiser is not paying attention towards the overstocked inventory is negatively affecting

sales. Although company is able to make good capital structure as it has a positive goodwill in the

market (Aebi, Sabato and Schmid, 2012). Market is ready to invest money in the company through

long term and short term equity methods. The working capital shows that RB need to build speed

in paying of its liabilities so it can recover from a negative figure. Overall the liquidity of company

is fine in terms of paying its money.

LIMITATIONS

There are basic limitations which appears while conducting ratio analysis.

Historic- Financial ratios are not an ideal tool to forecast any strategy for future. They are

finance. This ratio also shows companies ability handle debt load.

It can be analysed that Reckitt Benckiser is able handle the excessive load of debt payment

and has a good goodwill in the market. According to the Quick ratio companies financial strength

has increased over the years. It has recovered its financial strength and was able to gain greater

liquidity and pay off its debts. A negative working capital shows that RB's current assets are less

than its current liabilities. Although the working capital has consecutively come in negative

numbers but it has also declined. This shows that Reckitt Benckiser is recovering from its due on

the liabilities (Hull, 2012). But it still requires increase in its current assets over liabilities to achieve

a positive working capital. A high number of days inventory ratios depicts that sales are increased

over the time. This is considered as a good condition for the company as it is able to sell its

products and goods.

On the other hand inventory turnover ratios shows that a lot of products are getting

overstocked. Hence, it can be said that although Rb is selling in good numbers it still requires

speeding up. This can be done to maintain the speed of inventory that has to be yet sold out in the

market. It is considered ideal for the investor while investing money in the company if it is able to

effectively manger its inventory (Kaplan and Atkinson, 2015). An increase in the earning per share

proves that company is making good profits per every stock of share. It is clear that now companies

position has improved as it is relatively earned better profits. A high dividend payout ratio shows

that share prices of the company will not increase their value in the market.

Summary of the analysis

From the above analysis it is clear that company is making good improvement with regard to

the past financial figures. The profitability ratios depicted that company is making good profits. But

it can still strive to achieve better figure of profit by increasing selling. This is due to the fact that

Reckitt Benckiser is not paying attention towards the overstocked inventory is negatively affecting

sales. Although company is able to make good capital structure as it has a positive goodwill in the

market (Aebi, Sabato and Schmid, 2012). Market is ready to invest money in the company through

long term and short term equity methods. The working capital shows that RB need to build speed

in paying of its liabilities so it can recover from a negative figure. Overall the liquidity of company

is fine in terms of paying its money.

LIMITATIONS

There are basic limitations which appears while conducting ratio analysis.

Historic- Financial ratios are not an ideal tool to forecast any strategy for future. They are

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

calculated in the past data of the financial year. It is not viable for the company to analyse its

future potentials based on the last years financial data. This is because past only show what

has happened and it cannot to be used to set future objectives.

Accounting policies- An organization has to implement various policies as per the

accounting standards. These impaired policies forces and accountant or finance manager to

assume some figures (Dokas, Giokas and Tsamis, 2014). Hence, these figures and estimate

negativity affects ratio analysis. Thus, it is not ideal to compare ratios of different industries.

Historic v/s Current- Financial ratio can be misleading if they are calculated based on

wrong information. If they are calculated with incorrect or false information of data they

will not show the right financial results. This disparity may result in an unfruitful condition

for the company.

Business Conditions- Each organization works in a different environment and work culture.

Thus, it has to follow different ratio analysis tools to show their efficiency, growth and

profitability. Each business is entitled to follow their context while calculating ratios for

their company. For examples an increased turnover ratio may be good for some business and

may not be ideal for many.

Inflation- the change in economic policies specially inflation rate may change the basis of

calculation for ratios (DRURY, 2013). For example if in 2013 the inflation rate was low as

compared to 2014. Then all the financial figures will be different form each other. Hence, if

the inflation rates change from the last year then that data can not be used to compared with

the current year.

Strategic analysis- To compare between strategies used by a company, generally ratio

analysis is used. It helps to analysed the feasibilities of the chosen strategies. But on the

other hand it is not ideal for an organisation to use ratio analysis to compare between firms

that are using different strategies.

CONCLUSION

From the above research it is clear that ratio analysis plays a vital role in analysis the

financial position of the company. Reckitt Benckiser is a huge brand in terms of companies growth

and revenue margin. The ratio analysis shows that the company needs to pay attention on some

conflicts that are evident form the figures. The issue of overstocked inventory, increasing sales,

improving negative working capital and improving liquidity of the company. The research studies

that Rb has maintained its strong financial position when it comes to paying debts to the creditors in

the minimum time period. The following are proposed recommendation which are required to be

exercised by Reckitt Benckiser in order to improve its financial prospects.

future potentials based on the last years financial data. This is because past only show what

has happened and it cannot to be used to set future objectives.

Accounting policies- An organization has to implement various policies as per the

accounting standards. These impaired policies forces and accountant or finance manager to

assume some figures (Dokas, Giokas and Tsamis, 2014). Hence, these figures and estimate

negativity affects ratio analysis. Thus, it is not ideal to compare ratios of different industries.

Historic v/s Current- Financial ratio can be misleading if they are calculated based on

wrong information. If they are calculated with incorrect or false information of data they

will not show the right financial results. This disparity may result in an unfruitful condition

for the company.

Business Conditions- Each organization works in a different environment and work culture.

Thus, it has to follow different ratio analysis tools to show their efficiency, growth and

profitability. Each business is entitled to follow their context while calculating ratios for

their company. For examples an increased turnover ratio may be good for some business and

may not be ideal for many.

Inflation- the change in economic policies specially inflation rate may change the basis of

calculation for ratios (DRURY, 2013). For example if in 2013 the inflation rate was low as

compared to 2014. Then all the financial figures will be different form each other. Hence, if

the inflation rates change from the last year then that data can not be used to compared with

the current year.

Strategic analysis- To compare between strategies used by a company, generally ratio

analysis is used. It helps to analysed the feasibilities of the chosen strategies. But on the

other hand it is not ideal for an organisation to use ratio analysis to compare between firms

that are using different strategies.

CONCLUSION

From the above research it is clear that ratio analysis plays a vital role in analysis the

financial position of the company. Reckitt Benckiser is a huge brand in terms of companies growth

and revenue margin. The ratio analysis shows that the company needs to pay attention on some

conflicts that are evident form the figures. The issue of overstocked inventory, increasing sales,

improving negative working capital and improving liquidity of the company. The research studies

that Rb has maintained its strong financial position when it comes to paying debts to the creditors in

the minimum time period. The following are proposed recommendation which are required to be

exercised by Reckitt Benckiser in order to improve its financial prospects.

RECOMMENDATION

It is recommended for Reckitt Benckiser to the following.

Increase sale of inventory stocked- Reckitt Benckiser must pay attention to improve its

inventory which is getting overstocked. The personnels must aim to first sale all the stocked

goods before producing the new goods and services. This way there will more sales and less

wastage in terms of stocked inventory (Brigham and Ehrhardt, 2013). Discounts offers can

be provided to the consumers to lure them. If consumers are attracted more towards

purchasing there will be low chances of overstocked inventory.

Change the negative working capital- The organization have to consider alternative

methods to procure funds for the business. At many time's in shortage of funds company is

not able to conduct its operational prospects. On the other hand suppliers must be paid on

time as well (Hull, 2012). This way RB can negotiate better deals with suppliers and can

purchase raw materials at lowered prices. Management of cash flow must be done

effectively. Apart from this payment methods must be improved by initiating only cash sales

for the customers.

Improve liquidity position- this is very important for Reckitt Benckiser to improve its

liquidity position. Operating expense must be lowered so reduce cost of the products. This

way more profits can be incurred from the business. Business have to sell off those assets

which are of no use for the company (Uechi and et.al., 2015). By doing this it can liquidate

the value of assets in cash. Strategies must be formulated to increase profit making ability

of the company. Only more profits will generate revenue which will further improve

company financial capacities.

It is recommended for Reckitt Benckiser to the following.

Increase sale of inventory stocked- Reckitt Benckiser must pay attention to improve its

inventory which is getting overstocked. The personnels must aim to first sale all the stocked

goods before producing the new goods and services. This way there will more sales and less

wastage in terms of stocked inventory (Brigham and Ehrhardt, 2013). Discounts offers can

be provided to the consumers to lure them. If consumers are attracted more towards

purchasing there will be low chances of overstocked inventory.

Change the negative working capital- The organization have to consider alternative

methods to procure funds for the business. At many time's in shortage of funds company is

not able to conduct its operational prospects. On the other hand suppliers must be paid on

time as well (Hull, 2012). This way RB can negotiate better deals with suppliers and can

purchase raw materials at lowered prices. Management of cash flow must be done

effectively. Apart from this payment methods must be improved by initiating only cash sales

for the customers.

Improve liquidity position- this is very important for Reckitt Benckiser to improve its

liquidity position. Operating expense must be lowered so reduce cost of the products. This

way more profits can be incurred from the business. Business have to sell off those assets

which are of no use for the company (Uechi and et.al., 2015). By doing this it can liquidate

the value of assets in cash. Strategies must be formulated to increase profit making ability

of the company. Only more profits will generate revenue which will further improve

company financial capacities.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REFERENCES

Books and Journal

Adrian, T. and Shin, H.S., 2014. Financial intermediary balance sheet management. In A Flow-of-

Funds Perspective on the Financial Crisis (pp. 177-202). Palgrave Macmillan UK.

Aebi, V., Sabato, G. and Schmid, M., 2012. Risk management, corporate governance, and bank

performance in the financial crisis. Journal of Banking & Finance, 36(12), pp.3213-3226.

Brigham, E. and Ehrhardt, M., 2013. Financial management: Theory & practice. Cengage

Learning.

Christoffersen, P.F., 2012. Elements of financial risk management. Academic Press.

Dokas, I., Giokas, D. and Tsamis, A., 2014. Liquidity efficiency in the Greek listed firms: a

financial ratio based on data envelopment analysis. International Journal of Corporate

Finance and Accounting (IJCFA), 1(1), pp.40-59.

DRURY, C.M., 2013. Management and cost accounting. Springer.

Hull, J., 2012. Risk Management and Financial Institutions,+ Web Site (Vol. 733). John Wiley &

Sons.Christoffersen, P.F., 2012. Elements of financial risk management. Academic Press.

Jarrow, R.A. and Chatterjea, A., 2013. An introduction to derivative securities, financial markets,

and risk management. WW Norton & Company.

Kaplan, R.S. and Atkinson, A.A., 2015. Advanced management accounting. PHI Learning.

Oikonomou, I., Brooks, C. and Pavelin, S., 2012. The impact of corporate social performance on

financial risk and utility: A longitudinal analysis. Financial Management, 41(2), pp.483-515.

Rose, P. and Hudgins, S., 2014. Bank Management & Financial Services, 9th.

Uechi, L. and et.al., 2015. Sector dominance ratio analysis of financial markets. Physica A:

Statistical Mechanics and its Applications, 421, pp.488-509.

Online

Reckitt Benckiser Group PLC. 2016. [Online]. Available through:

<http://financials.morningstar.com/ratios/r.html?t=RBGPF>. [Accessed on: 16th February, 2016].

Books and Journal

Adrian, T. and Shin, H.S., 2014. Financial intermediary balance sheet management. In A Flow-of-

Funds Perspective on the Financial Crisis (pp. 177-202). Palgrave Macmillan UK.

Aebi, V., Sabato, G. and Schmid, M., 2012. Risk management, corporate governance, and bank

performance in the financial crisis. Journal of Banking & Finance, 36(12), pp.3213-3226.

Brigham, E. and Ehrhardt, M., 2013. Financial management: Theory & practice. Cengage

Learning.

Christoffersen, P.F., 2012. Elements of financial risk management. Academic Press.

Dokas, I., Giokas, D. and Tsamis, A., 2014. Liquidity efficiency in the Greek listed firms: a

financial ratio based on data envelopment analysis. International Journal of Corporate

Finance and Accounting (IJCFA), 1(1), pp.40-59.

DRURY, C.M., 2013. Management and cost accounting. Springer.

Hull, J., 2012. Risk Management and Financial Institutions,+ Web Site (Vol. 733). John Wiley &

Sons.Christoffersen, P.F., 2012. Elements of financial risk management. Academic Press.

Jarrow, R.A. and Chatterjea, A., 2013. An introduction to derivative securities, financial markets,

and risk management. WW Norton & Company.

Kaplan, R.S. and Atkinson, A.A., 2015. Advanced management accounting. PHI Learning.

Oikonomou, I., Brooks, C. and Pavelin, S., 2012. The impact of corporate social performance on

financial risk and utility: A longitudinal analysis. Financial Management, 41(2), pp.483-515.

Rose, P. and Hudgins, S., 2014. Bank Management & Financial Services, 9th.

Uechi, L. and et.al., 2015. Sector dominance ratio analysis of financial markets. Physica A:

Statistical Mechanics and its Applications, 421, pp.488-509.

Online

Reckitt Benckiser Group PLC. 2016. [Online]. Available through:

<http://financials.morningstar.com/ratios/r.html?t=RBGPF>. [Accessed on: 16th February, 2016].

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.