Financial Markets and Institutions: RBA's Monetary Policy Analysis

VerifiedAdded on 2023/06/15

|9

|3252

|90

Report

AI Summary

This report examines the role of the Reserve Bank of Australia (RBA) in conducting monetary policy and its effects on Australian financial markets. It discusses the RBA's objectives, including price stability, full employment, and economic welfare, achieved through an inflation target of 2-3%. The report details the RBA's use of domestic market operations to manage the cash rate and influence interest rates. It also analyzes Australia's economic environment, focusing on inflation, interest rates, and the impact of monetary policy on asset prices, investments, and exchange rates. The importance of leverage in financial stability, particularly in relation to property, is highlighted, along with the risk management strategies employed by Authorised Deposit Institutions (ADIs) to address credit, liquidity, operational, and interest rate risks. Finally, the report touches on the role of Basel Accords in providing banking regulations for capital and risk management. Desklib offers a variety of resources, including past papers and solved assignments, to aid students in their studies.

Running Head: FINANCIAL MARKETS AND INSTITUTIONS

RBA and monetary policy

RBA and monetary policy

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Financial markets and Institution 1

Contents

Introduction...........................................................................................................................................2

Role of RBA in conducting monetary policy.........................................................................................2

Australia’s economic environment and monetary policy effects...........................................................4

Importance of Leverage.........................................................................................................................5

Dealing with risks..................................................................................................................................5

Authorised Deposit Institutions.........................................................................................................5

Basel Accords....................................................................................................................................6

Conclusion.............................................................................................................................................7

References.............................................................................................................................................8

Contents

Introduction...........................................................................................................................................2

Role of RBA in conducting monetary policy.........................................................................................2

Australia’s economic environment and monetary policy effects...........................................................4

Importance of Leverage.........................................................................................................................5

Dealing with risks..................................................................................................................................5

Authorised Deposit Institutions.........................................................................................................5

Basel Accords....................................................................................................................................6

Conclusion.............................................................................................................................................7

References.............................................................................................................................................8

Financial markets and Institution 2

Introduction

The central bank of Australia is set up to execute various activities such as

implementing monetary policies, issuing banknotes, performing functions to maintain a

strong financial system and setting inflation target. RBA also provides banking services to the

Australian Government, official institutes and banks. It also manages gold and foreign

exchange reserves of the country ("About the RBA | RBA", 2017). The following report

contains the role played by RBA in implementing monetary policy and effects of its

implementation on financial markets. It also includes the brief about the current economic

environment of Australia mainly in context with inflation and interest rate and how monetary

policy helps in maintaining the financial stability in the country.

The report also states the importance of leverage for central banks like RBA. A brief

about ADI dealing with credit, liquidity, operating and interest rate risk and also how Basel

Accords help in dealing with these risk is also provided in the report.

Role of RBA in conducting monetary policy

Australia’s central bank is responsible for country’s monetary policy. The main aim

of RBA to implement it is to bring stability in the prices, full employment and overall welfare

of Australian people. To achieve these objectives, bank has set an inflation target and it

focuses on keeping the inflation rate on an average of 2-3 percent in the economy. Monetary

policy focus on achieving this target as it is primary condition to promote sustainable growth

and development of economy. By controlling inflation, the value of money will be preserved

and economy will have a sustainable growth for a longer period of time. The framework of

policy is based on its medium term objective of controlling inflation. The targeted rate is

sufficiently low and does not have a large impact on economic decisions. For taking

monetary policy decision, Reserve Bank Board hold a meeting eleven times every year and

the bank’s staff prepare a paper which contains all the detailed information about

developments taken place in country’s economy and international economies. The meeting is

ended by the senior staff and the decisions taken are communicated to the public ("Monetary

Policy | RBA", 2017).

RBA plays an important role in implementing monetary policy. The domestic market

department of bank has to maintain the conditions prevailing in the money market on a daily

basis, so as to keep the cash rate near to the targeted rate of 2-3 percent which is decided by

the board. Cash rate is that rate which influence other interest rate and is the basis for

formulating the structure of other interest rates. RBA uses its domestic market operations,

also known as open market operations in order to keep the cash rate close to the target. These

operations basically means buying and selling of government securities in open market.

Managing the supply of funds available to the banks, helps RBA in achieving its target

("Monetary Policy | RBA", 2017).

Introduction

The central bank of Australia is set up to execute various activities such as

implementing monetary policies, issuing banknotes, performing functions to maintain a

strong financial system and setting inflation target. RBA also provides banking services to the

Australian Government, official institutes and banks. It also manages gold and foreign

exchange reserves of the country ("About the RBA | RBA", 2017). The following report

contains the role played by RBA in implementing monetary policy and effects of its

implementation on financial markets. It also includes the brief about the current economic

environment of Australia mainly in context with inflation and interest rate and how monetary

policy helps in maintaining the financial stability in the country.

The report also states the importance of leverage for central banks like RBA. A brief

about ADI dealing with credit, liquidity, operating and interest rate risk and also how Basel

Accords help in dealing with these risk is also provided in the report.

Role of RBA in conducting monetary policy

Australia’s central bank is responsible for country’s monetary policy. The main aim

of RBA to implement it is to bring stability in the prices, full employment and overall welfare

of Australian people. To achieve these objectives, bank has set an inflation target and it

focuses on keeping the inflation rate on an average of 2-3 percent in the economy. Monetary

policy focus on achieving this target as it is primary condition to promote sustainable growth

and development of economy. By controlling inflation, the value of money will be preserved

and economy will have a sustainable growth for a longer period of time. The framework of

policy is based on its medium term objective of controlling inflation. The targeted rate is

sufficiently low and does not have a large impact on economic decisions. For taking

monetary policy decision, Reserve Bank Board hold a meeting eleven times every year and

the bank’s staff prepare a paper which contains all the detailed information about

developments taken place in country’s economy and international economies. The meeting is

ended by the senior staff and the decisions taken are communicated to the public ("Monetary

Policy | RBA", 2017).

RBA plays an important role in implementing monetary policy. The domestic market

department of bank has to maintain the conditions prevailing in the money market on a daily

basis, so as to keep the cash rate near to the targeted rate of 2-3 percent which is decided by

the board. Cash rate is that rate which influence other interest rate and is the basis for

formulating the structure of other interest rates. RBA uses its domestic market operations,

also known as open market operations in order to keep the cash rate close to the target. These

operations basically means buying and selling of government securities in open market.

Managing the supply of funds available to the banks, helps RBA in achieving its target

("Monetary Policy | RBA", 2017).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Financial markets and Institution 3

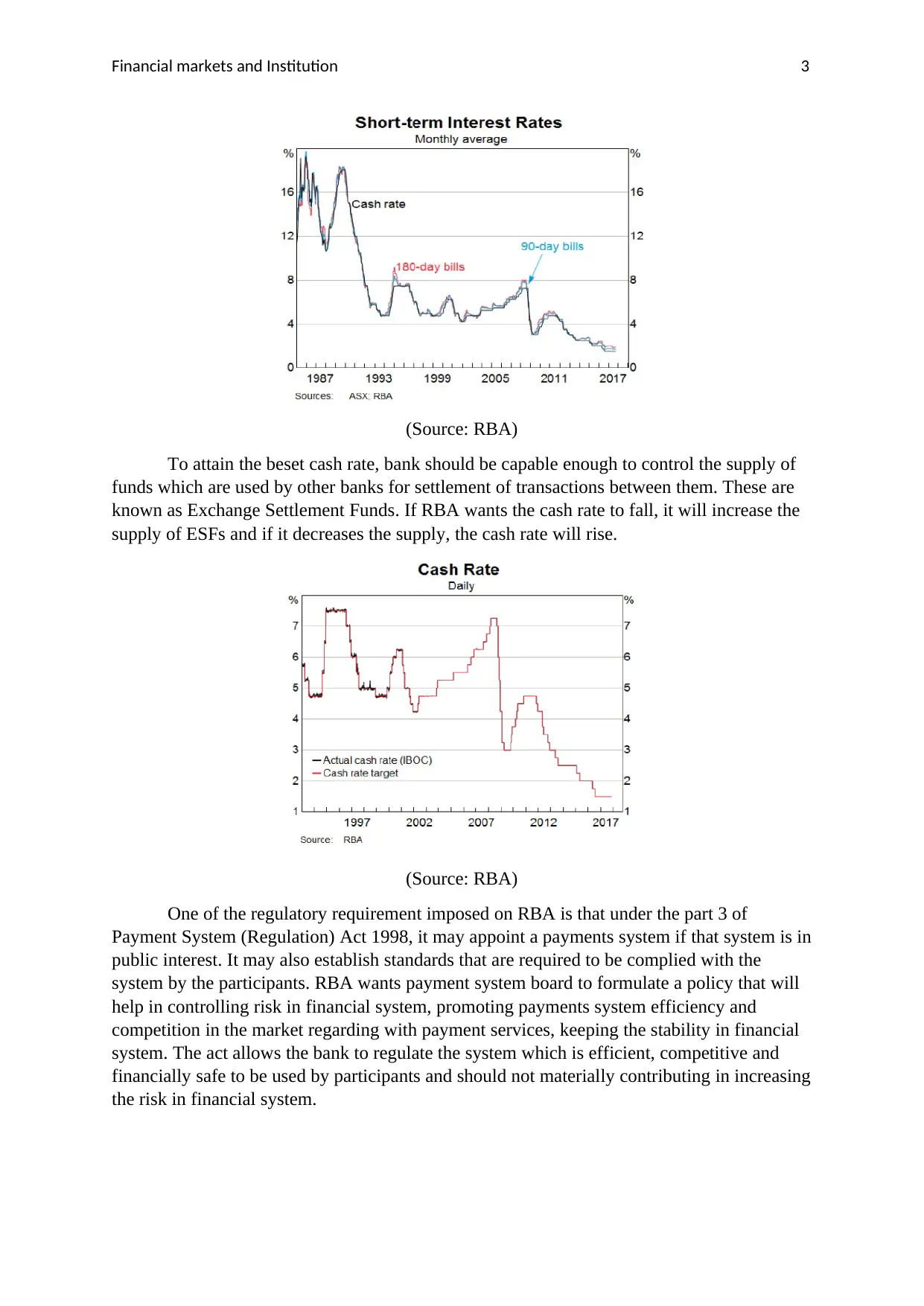

(Source: RBA)

To attain the beset cash rate, bank should be capable enough to control the supply of

funds which are used by other banks for settlement of transactions between them. These are

known as Exchange Settlement Funds. If RBA wants the cash rate to fall, it will increase the

supply of ESFs and if it decreases the supply, the cash rate will rise.

(Source: RBA)

One of the regulatory requirement imposed on RBA is that under the part 3 of

Payment System (Regulation) Act 1998, it may appoint a payments system if that system is in

public interest. It may also establish standards that are required to be complied with the

system by the participants. RBA wants payment system board to formulate a policy that will

help in controlling risk in financial system, promoting payments system efficiency and

competition in the market regarding with payment services, keeping the stability in financial

system. The act allows the bank to regulate the system which is efficient, competitive and

financially safe to be used by participants and should not materially contributing in increasing

the risk in financial system.

(Source: RBA)

To attain the beset cash rate, bank should be capable enough to control the supply of

funds which are used by other banks for settlement of transactions between them. These are

known as Exchange Settlement Funds. If RBA wants the cash rate to fall, it will increase the

supply of ESFs and if it decreases the supply, the cash rate will rise.

(Source: RBA)

One of the regulatory requirement imposed on RBA is that under the part 3 of

Payment System (Regulation) Act 1998, it may appoint a payments system if that system is in

public interest. It may also establish standards that are required to be complied with the

system by the participants. RBA wants payment system board to formulate a policy that will

help in controlling risk in financial system, promoting payments system efficiency and

competition in the market regarding with payment services, keeping the stability in financial

system. The act allows the bank to regulate the system which is efficient, competitive and

financially safe to be used by participants and should not materially contributing in increasing

the risk in financial system.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Financial markets and Institution 4

Australia’s economic environment and monetary policy effects

Australia’s economy is always performing well. Despite of a decreasing global

economy over 2014, country’s economy continues to grow in the areas like exports and

housing investment. Although in recent years, the economy of Australia has been impacted

because of declining investment in mining sector. Investment in non-mining business has

increased and a fall has been noticed in the unemployment rate. As far as inflation is

concerned, it remains moderate in the third quarter of 2017. According to Australian Bureau

of Statistics (ABS), quarter third reading says that higher prices of electricity, tobacco, travel

and accommodation are offset by the lower prices of vegetable, automotive fuels and

telecommunication services.

Inflation rate fell from 1.9% to 1.8% in Q3 which is below the targeted rate 2-3% set

by RBA. It is also noted that from Q4 new weights will be introduced by ABS to calculate

consumer price index. Housing expenditure will be given more importance and while food

and non-alcoholic beverages will be less important ("Australia Economy - GDP, Inflation,

CPI and Interest Rate", 2017).

(Source: Australia Economy)

The interest rate remain unchanged as RBA kept the cash rate at 1.50% since 2016.

After observing the inflation data in Q3, RBA decides to keep a target range of 2-3 percent.

This marked a low price pressures due to the appreciation of Australian dollar and weak

labour cost pressures. In addition to this, the economy seem to be strong on demand side and

the rate of unemployment fall during September. Moreover, changes done by Australian

Prudential regulation Authority (APRA) regarding housing market seems to be successful as

in most of the cities, house prices remain unchanged. This reduces the pressure on bank for

raising rates in short term ("Australia Economy - GDP, Inflation, CPI and Interest Rate",

2017).

(Source: Australia Economy)

The monetary policy implemented by reserve bank of Australia involves determining

the interest rates on the overnight loans in the market. This rate is basically known as cash

rate which influence other interest rates in the economy. The policy deals with price

stabilisation, full employment and economic welfare of Australian people. Financial markets

including value of assets and yields are significantly affected by this policy. The core

objective of the policy is to determine interest rates, which in return states the risk-free rate of

Australia’s economic environment and monetary policy effects

Australia’s economy is always performing well. Despite of a decreasing global

economy over 2014, country’s economy continues to grow in the areas like exports and

housing investment. Although in recent years, the economy of Australia has been impacted

because of declining investment in mining sector. Investment in non-mining business has

increased and a fall has been noticed in the unemployment rate. As far as inflation is

concerned, it remains moderate in the third quarter of 2017. According to Australian Bureau

of Statistics (ABS), quarter third reading says that higher prices of electricity, tobacco, travel

and accommodation are offset by the lower prices of vegetable, automotive fuels and

telecommunication services.

Inflation rate fell from 1.9% to 1.8% in Q3 which is below the targeted rate 2-3% set

by RBA. It is also noted that from Q4 new weights will be introduced by ABS to calculate

consumer price index. Housing expenditure will be given more importance and while food

and non-alcoholic beverages will be less important ("Australia Economy - GDP, Inflation,

CPI and Interest Rate", 2017).

(Source: Australia Economy)

The interest rate remain unchanged as RBA kept the cash rate at 1.50% since 2016.

After observing the inflation data in Q3, RBA decides to keep a target range of 2-3 percent.

This marked a low price pressures due to the appreciation of Australian dollar and weak

labour cost pressures. In addition to this, the economy seem to be strong on demand side and

the rate of unemployment fall during September. Moreover, changes done by Australian

Prudential regulation Authority (APRA) regarding housing market seems to be successful as

in most of the cities, house prices remain unchanged. This reduces the pressure on bank for

raising rates in short term ("Australia Economy - GDP, Inflation, CPI and Interest Rate",

2017).

(Source: Australia Economy)

The monetary policy implemented by reserve bank of Australia involves determining

the interest rates on the overnight loans in the market. This rate is basically known as cash

rate which influence other interest rates in the economy. The policy deals with price

stabilisation, full employment and economic welfare of Australian people. Financial markets

including value of assets and yields are significantly affected by this policy. The core

objective of the policy is to determine interest rates, which in return states the risk-free rate of

Financial markets and Institution 5

return. Demand of all the types of securities and bond are largely affected by the risk-free

rate. At low interest rate, demand for bonds rises results in its yield falling and vice-versa.

RBA is pretty much aware about its ability to affect assets prices through monetary policy. At

the time of recession, it lowers the interest rates which led to an increase in asset prices. This

increase has a mild effect on the economy but fall in the bond yields leads to lower borrowing

cost for government, resulting in increased spending.

The policy also affects the investments. Increased interest rates will reduce the

feasibility of investments and quality of investment spending. Rising rates will make

financial assets more attractive. Changes in the policy also influence the exchange rates

which lead to the changes in imports and exports. Low interest rate lead to rise in exports and

fall in imports whereas high interest rate leads to a rise in imports and fall in exports. Overall,

fluctuations in the monetary policy definitely have its impact on financial markets and overall

economy.

Importance of Leverage

It is said in the statement given by RBA governor that leverage matters a lot. It is the

leverage against those assets that matters. A high leverage can be obtained when a borrowing

is secured against a property. A leveraged property is particularly relevant to the financial

stability of the country with three aspects. First aspect is different average inflation rates

includes different average nominal rates and various decline rates in the burden of a

repayment of mortgage. The second aspect is that there is imperfect information about the

ability and willingness of borrowers to pay. Even the borrowers themselves don’t know about

their capability of paying debt in future. While doing financial stability analysis, it is very

important to maintain some lending standards. Therefore, these credit constraints that are

present should be designed well in order to manage credit risk. Third aspect deals with the

legal definitions of liability that differ and those difference matters a lot between property,

debt and financial stability. Generally companies have limited liabilities unlike individuals

and once proved defaulted, it will be bankrupt and cease to exit. Therefore, properties owned

by the companies must have different credit risk than that of individuals.

All these aspects clearly define that why it is important to have a leveraged property

more than other assets. Having property permitted to be leveraged, it will help in generating

income such as rental income and other. The primary objective of RBA is to perform those

function which helps in maintaining financial stability. In order to achieve this, bank should

take a very careful note particularly of the leveraged dynamics.

Dealing with risks

Authorised Deposit Institutions

ADIs are authorised corporations under Banking Act 1959. They include banks, credit

unions and building societies and are required to comply with the same prudential standards

formed by APRA. ADIs deals with their liquidity risk by holding assets like cash, ES funds,

securities and deposits in the inter-bank market which can be sold to raise additional

liquidity. They permit the customer to repay the loans early and helps the borrowers in raising

funds from financial markets. They can also borrow ES funds from RBA to manage their

liquidity. The prudential standard APS 220 which is related to the issue of credit risk control.

This standard clearly states that the single largest risk faced by ADI is the credit risk and it

must have an efficient credit risk management system that identifies a particular type of risk

return. Demand of all the types of securities and bond are largely affected by the risk-free

rate. At low interest rate, demand for bonds rises results in its yield falling and vice-versa.

RBA is pretty much aware about its ability to affect assets prices through monetary policy. At

the time of recession, it lowers the interest rates which led to an increase in asset prices. This

increase has a mild effect on the economy but fall in the bond yields leads to lower borrowing

cost for government, resulting in increased spending.

The policy also affects the investments. Increased interest rates will reduce the

feasibility of investments and quality of investment spending. Rising rates will make

financial assets more attractive. Changes in the policy also influence the exchange rates

which lead to the changes in imports and exports. Low interest rate lead to rise in exports and

fall in imports whereas high interest rate leads to a rise in imports and fall in exports. Overall,

fluctuations in the monetary policy definitely have its impact on financial markets and overall

economy.

Importance of Leverage

It is said in the statement given by RBA governor that leverage matters a lot. It is the

leverage against those assets that matters. A high leverage can be obtained when a borrowing

is secured against a property. A leveraged property is particularly relevant to the financial

stability of the country with three aspects. First aspect is different average inflation rates

includes different average nominal rates and various decline rates in the burden of a

repayment of mortgage. The second aspect is that there is imperfect information about the

ability and willingness of borrowers to pay. Even the borrowers themselves don’t know about

their capability of paying debt in future. While doing financial stability analysis, it is very

important to maintain some lending standards. Therefore, these credit constraints that are

present should be designed well in order to manage credit risk. Third aspect deals with the

legal definitions of liability that differ and those difference matters a lot between property,

debt and financial stability. Generally companies have limited liabilities unlike individuals

and once proved defaulted, it will be bankrupt and cease to exit. Therefore, properties owned

by the companies must have different credit risk than that of individuals.

All these aspects clearly define that why it is important to have a leveraged property

more than other assets. Having property permitted to be leveraged, it will help in generating

income such as rental income and other. The primary objective of RBA is to perform those

function which helps in maintaining financial stability. In order to achieve this, bank should

take a very careful note particularly of the leveraged dynamics.

Dealing with risks

Authorised Deposit Institutions

ADIs are authorised corporations under Banking Act 1959. They include banks, credit

unions and building societies and are required to comply with the same prudential standards

formed by APRA. ADIs deals with their liquidity risk by holding assets like cash, ES funds,

securities and deposits in the inter-bank market which can be sold to raise additional

liquidity. They permit the customer to repay the loans early and helps the borrowers in raising

funds from financial markets. They can also borrow ES funds from RBA to manage their

liquidity. The prudential standard APS 220 which is related to the issue of credit risk control.

This standard clearly states that the single largest risk faced by ADI is the credit risk and it

must have an efficient credit risk management system that identifies a particular type of risk

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Financial markets and Institution 6

taken by ADI. Board of Directors and senior management is held responsible for the efficient

management of system. They insure that ADI must have appropriate credit risk management

policies and procedures according to the business complexity and scope. Also the internal

controls which consistently identify the provisions and a general reserve should also be

maintained for the credit losses in accordance with standards and framework (Hunt & Terry,

2015).

ADIs financial position deteriorates as interest rate risk increases with time. The risk

is generally split into two parts that are traded and non-traded. Traded interest risk is related

to ADI involved in trading activities. The risk in banking book arises from ADI’s core

banking activities. The techniques used depend upon the indicator choose by ADI for its

financial position. It may be earnings or economic value. Operational risk is the loss resulting

from inappropriate internal process, system and external events. To deal with its operational

risk, ADI require to maintain a regulatory capital ORRC in compliance with Prudential

Standard. A framework is prepared that is used in assessing the risk and then an operational

risk measurement system is formed in which data of the framework is inserted. A risk model

central to the system is prepared by ADI in order to quantify its ORCC.

Basel Accords

Basel Committee on Bank Supervision (BCBS) provides three sets of banking

regulations known as the Basel Accords. These are Basel I, II and III. These sets give

assistance to banking regulations regarding capital, market and operating risk. The main aim

of the accords is to make sure that the banking institutions must have enough capital with

them to meet their liabilities and to cover their uncertain losses. In order to deal with credit

risk, Basel committee set some principles to which all members agree. These principles are

used in evaluating credit risk management system of bank. A credit risk environment is being

established which states the responsibility of Board of Directors for approving and reviewing

the credit risk strategy. Senior management is then responsible for implementing that

strategy. Last, banks should manage the credit risk which is involved in all activities and

products. Appropriate administration of credit and risk management system should be

maintained by bank for managing credit risk. They can also use internal risk rating system for

the same. Also to avoid credit risk, bank must make sure that the function of credit granting is

being effectively and efficiently managed.

In 2010, BCBS issued a new accord Basel III which gives the details about the

regulatory standards on the capital adequacy and liquidity of bank. It was also quoted by the

chairmen of BCBS that the framework of Basel III will protect financial stability and results

in sustainable economic growth. Combing global liquidity standards with high levels of

capital will reduce the chances of bank crisis. Framework of new accord provides an

introduction to the liquidity standards. It emphasis on the use of liquidity coverage ratio and

net stable funding ratios to measure liquidity risk. LCR requires bank to maintain an

appropriate level of liquid assets which do not have any debt against them so that they can be

converted into cash within a year to meets liquidity needs. On the other side, NSFR is set to

support funding of assets and banking activities for a longer period by establishing a

minimum amount of stable funding which is based on the liquidity of bank’s assets and

activities. Further ratios like ROA, NPAR GSR are also used in measuring liquidity (Hunt &

Terry, 2015).

taken by ADI. Board of Directors and senior management is held responsible for the efficient

management of system. They insure that ADI must have appropriate credit risk management

policies and procedures according to the business complexity and scope. Also the internal

controls which consistently identify the provisions and a general reserve should also be

maintained for the credit losses in accordance with standards and framework (Hunt & Terry,

2015).

ADIs financial position deteriorates as interest rate risk increases with time. The risk

is generally split into two parts that are traded and non-traded. Traded interest risk is related

to ADI involved in trading activities. The risk in banking book arises from ADI’s core

banking activities. The techniques used depend upon the indicator choose by ADI for its

financial position. It may be earnings or economic value. Operational risk is the loss resulting

from inappropriate internal process, system and external events. To deal with its operational

risk, ADI require to maintain a regulatory capital ORRC in compliance with Prudential

Standard. A framework is prepared that is used in assessing the risk and then an operational

risk measurement system is formed in which data of the framework is inserted. A risk model

central to the system is prepared by ADI in order to quantify its ORCC.

Basel Accords

Basel Committee on Bank Supervision (BCBS) provides three sets of banking

regulations known as the Basel Accords. These are Basel I, II and III. These sets give

assistance to banking regulations regarding capital, market and operating risk. The main aim

of the accords is to make sure that the banking institutions must have enough capital with

them to meet their liabilities and to cover their uncertain losses. In order to deal with credit

risk, Basel committee set some principles to which all members agree. These principles are

used in evaluating credit risk management system of bank. A credit risk environment is being

established which states the responsibility of Board of Directors for approving and reviewing

the credit risk strategy. Senior management is then responsible for implementing that

strategy. Last, banks should manage the credit risk which is involved in all activities and

products. Appropriate administration of credit and risk management system should be

maintained by bank for managing credit risk. They can also use internal risk rating system for

the same. Also to avoid credit risk, bank must make sure that the function of credit granting is

being effectively and efficiently managed.

In 2010, BCBS issued a new accord Basel III which gives the details about the

regulatory standards on the capital adequacy and liquidity of bank. It was also quoted by the

chairmen of BCBS that the framework of Basel III will protect financial stability and results

in sustainable economic growth. Combing global liquidity standards with high levels of

capital will reduce the chances of bank crisis. Framework of new accord provides an

introduction to the liquidity standards. It emphasis on the use of liquidity coverage ratio and

net stable funding ratios to measure liquidity risk. LCR requires bank to maintain an

appropriate level of liquid assets which do not have any debt against them so that they can be

converted into cash within a year to meets liquidity needs. On the other side, NSFR is set to

support funding of assets and banking activities for a longer period by establishing a

minimum amount of stable funding which is based on the liquidity of bank’s assets and

activities. Further ratios like ROA, NPAR GSR are also used in measuring liquidity (Hunt &

Terry, 2015).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Financial markets and Institution 7

To deal with operational risk, BCBS has designed operational risk modelling practices

for banks and Advanced Measurement Approach (AMA) is used for measuring the risk.

Recently, the committee has revised the operational risk framework which will be based on

single non-model-based method for determining risk capital. This model is termed as

Standardised Measurement Approach (SMA). It provides a standard comparability and

express risk sensitivity of advanced approach ("Standardised Measurement Approach for

operational risk - consultative document", 2016).

Basel accord has set some principles for managing interest rate risk. These principles

defines the risk management process which includes formulating business strategy, assuming

assets and liabilities in banking activities and internal control system. They provide an

effective measurement of interest rate risk, monitoring and control functions within the

process. Principles formed states the responsibility of board of directors to approve the

policies regarding interest rate risk management and to ensure that the senior management

follows them properly. Responsibility of senior management is to make sure that level of

interest rate is properly managed and adequate policies and measures are adopted to control

risks. Third principle states that banks should clearly define the duties to the key elements of

the process to avoid conflicts of interest. They must have functions of measurement,

monitoring and controlling the risk.

Conclusion

The Report concludes that Reserve Bank of India plays a vital role in implementing

monetary policy in the country. RBA sets its inflation target in its policy. Setting a targeted

cash rate will help in controlling the inflation as the changes in cash rate influences other

interest rates which will adversely affect the overall economy of the country. A regulatory

requirement regarding payment system is also imposed on the central bank. The bank is

allowed to design a payment system which is in public interest. The report also concludes that

monetary policy largely affect the economic environment of the country. Particularly, it has

its impact on inflation rate and interest rates. As far as Australian economy is concerned, it is

performing pretty well. A decrease in inflation rate has been there whereas interest rates

remains same. It can also be said from above report that for maintaining financial stability in

the country, bank pay more emphasis on leveraged assets. For central banks like RBA,

leverage matters a lot as a leveraged assets is not only a collateral security but also gives

income such as rental income. Various steps has been taken by ADIs and Basel Accords in

dealing with credit, liquidity, operational and interest rate risks. Several process and policies

are made and implemented to manage these risk effectively and efficiently.

Overall, it can be concluded that RBA plays an important role in managing overall

economy of country by performing various activities and functions. Keeping in view all the

different aspects, it formulates its policy so that its objectives can be achieved.

To deal with operational risk, BCBS has designed operational risk modelling practices

for banks and Advanced Measurement Approach (AMA) is used for measuring the risk.

Recently, the committee has revised the operational risk framework which will be based on

single non-model-based method for determining risk capital. This model is termed as

Standardised Measurement Approach (SMA). It provides a standard comparability and

express risk sensitivity of advanced approach ("Standardised Measurement Approach for

operational risk - consultative document", 2016).

Basel accord has set some principles for managing interest rate risk. These principles

defines the risk management process which includes formulating business strategy, assuming

assets and liabilities in banking activities and internal control system. They provide an

effective measurement of interest rate risk, monitoring and control functions within the

process. Principles formed states the responsibility of board of directors to approve the

policies regarding interest rate risk management and to ensure that the senior management

follows them properly. Responsibility of senior management is to make sure that level of

interest rate is properly managed and adequate policies and measures are adopted to control

risks. Third principle states that banks should clearly define the duties to the key elements of

the process to avoid conflicts of interest. They must have functions of measurement,

monitoring and controlling the risk.

Conclusion

The Report concludes that Reserve Bank of India plays a vital role in implementing

monetary policy in the country. RBA sets its inflation target in its policy. Setting a targeted

cash rate will help in controlling the inflation as the changes in cash rate influences other

interest rates which will adversely affect the overall economy of the country. A regulatory

requirement regarding payment system is also imposed on the central bank. The bank is

allowed to design a payment system which is in public interest. The report also concludes that

monetary policy largely affect the economic environment of the country. Particularly, it has

its impact on inflation rate and interest rates. As far as Australian economy is concerned, it is

performing pretty well. A decrease in inflation rate has been there whereas interest rates

remains same. It can also be said from above report that for maintaining financial stability in

the country, bank pay more emphasis on leveraged assets. For central banks like RBA,

leverage matters a lot as a leveraged assets is not only a collateral security but also gives

income such as rental income. Various steps has been taken by ADIs and Basel Accords in

dealing with credit, liquidity, operational and interest rate risks. Several process and policies

are made and implemented to manage these risk effectively and efficiently.

Overall, it can be concluded that RBA plays an important role in managing overall

economy of country by performing various activities and functions. Keeping in view all the

different aspects, it formulates its policy so that its objectives can be achieved.

Financial markets and Institution 8

References

Monetary Policy | RBA. (2017). Reserve Bank of Australia. Retrieved 1 December 2017,

from https://www.rba.gov.au/monetary-policy/

About the RBA | RBA. (2017). Reserve Bank of Australia. Retrieved 2 December 2017, from

https://www.rba.gov.au/about-rba/

Australia Economy - GDP, Inflation, CPI and Interest Rate. (2017). Focus Economics |

Economic Forecasts from the World's Leading Economists. Retrieved 1 December

2017, from https://www.focus-economics.com/countries/australia

Hunt, B., & Terry, C. (2015). Financial Institutions and Markets. Cengage Learning

Australia.

Standardised Measurement Approach for operational risk - consultative document.

(2016). Bis.org. Retrieved 2 December 2017, from

https://www.bis.org/bcbs/publ/d355.htm

References

Monetary Policy | RBA. (2017). Reserve Bank of Australia. Retrieved 1 December 2017,

from https://www.rba.gov.au/monetary-policy/

About the RBA | RBA. (2017). Reserve Bank of Australia. Retrieved 2 December 2017, from

https://www.rba.gov.au/about-rba/

Australia Economy - GDP, Inflation, CPI and Interest Rate. (2017). Focus Economics |

Economic Forecasts from the World's Leading Economists. Retrieved 1 December

2017, from https://www.focus-economics.com/countries/australia

Hunt, B., & Terry, C. (2015). Financial Institutions and Markets. Cengage Learning

Australia.

Standardised Measurement Approach for operational risk - consultative document.

(2016). Bis.org. Retrieved 2 December 2017, from

https://www.bis.org/bcbs/publ/d355.htm

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.