Analysis of REA Group's Annual Report and Accounting Framework

VerifiedAdded on 2023/04/20

|11

|1909

|343

Report

AI Summary

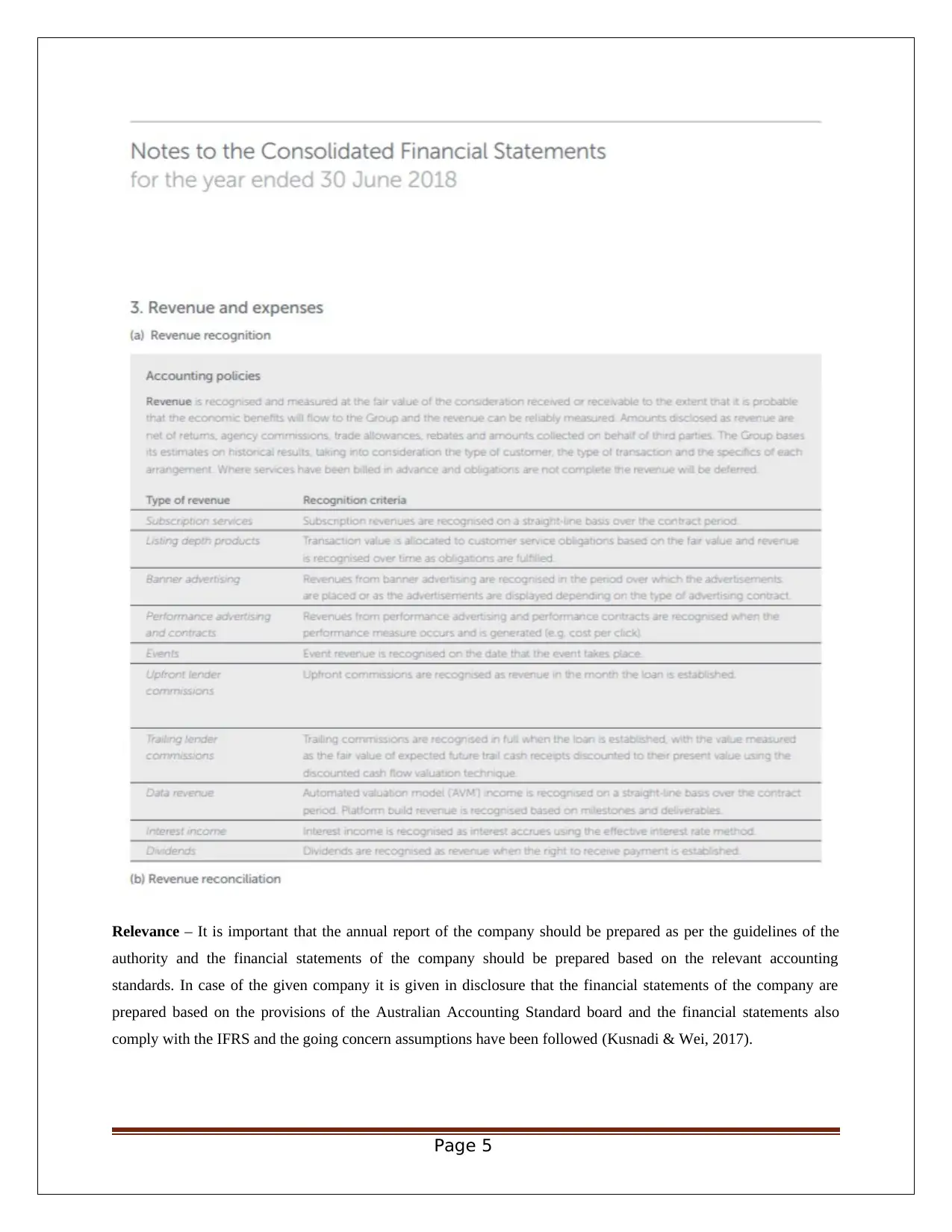

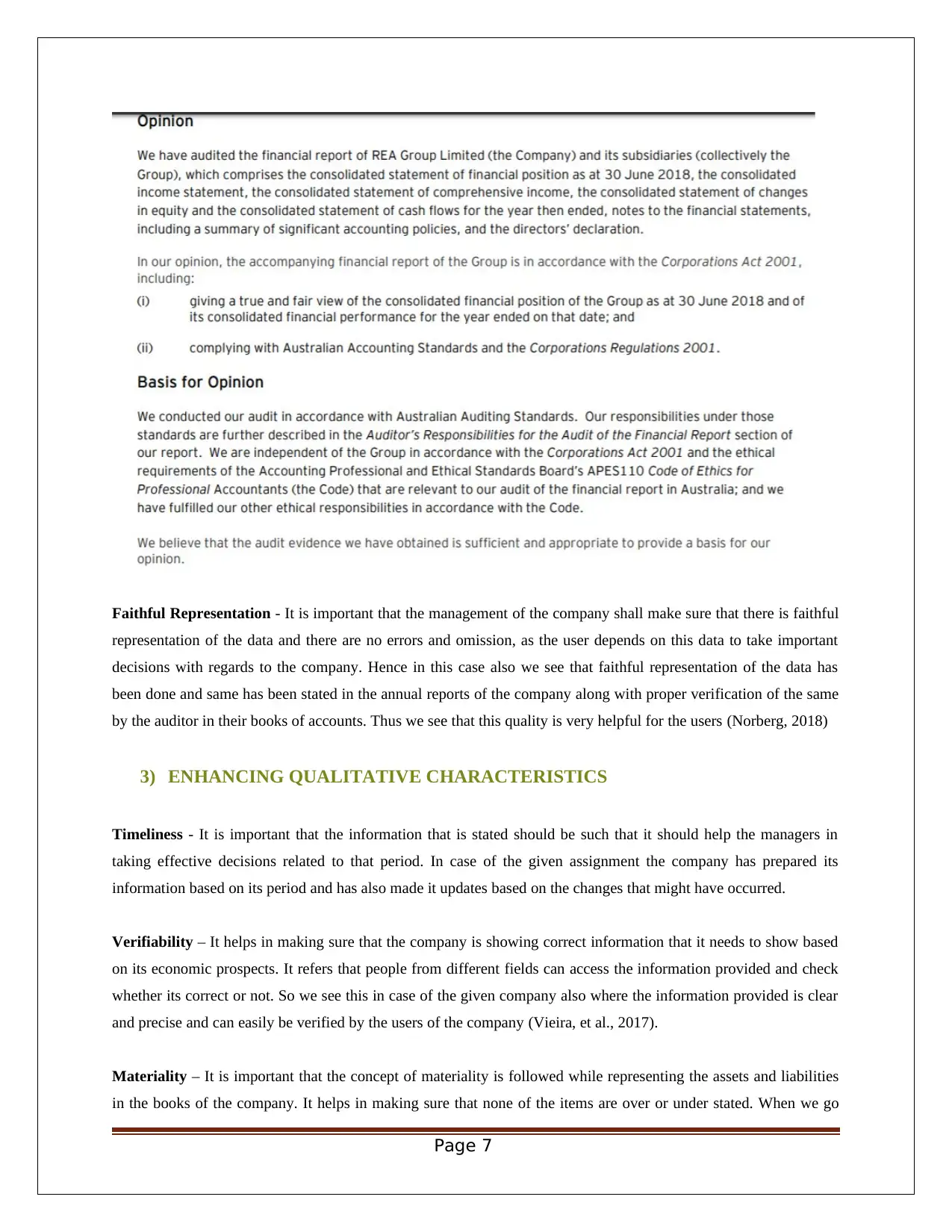

This report provides a detailed analysis of the REA Group's annual report, evaluating its compliance with the conceptual framework of accounting. The report examines the company's adherence to measurement requirements, qualitative characteristics (understandability, relevance, reliability, faithful representation), and enhancing qualitative characteristics (timeliness, verifiability, materiality, comparability). It assesses whether the users of financial reports, including stakeholders and investors, can effectively utilize the information provided in the annual report to make informed decisions. The analysis also addresses whether the company has met the requirements of the general purpose reporting framework, concluding that the company has generally followed the basic policies of the conceptual framework in the preparation of the annual report. The report uses screen prints and academic research to support its arguments and is properly referenced using Harvard style.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.