FIN600/FINA6017 Financial Management Report: REA Group Ltd Performance

VerifiedAdded on 2022/12/15

|8

|1961

|365

Report

AI Summary

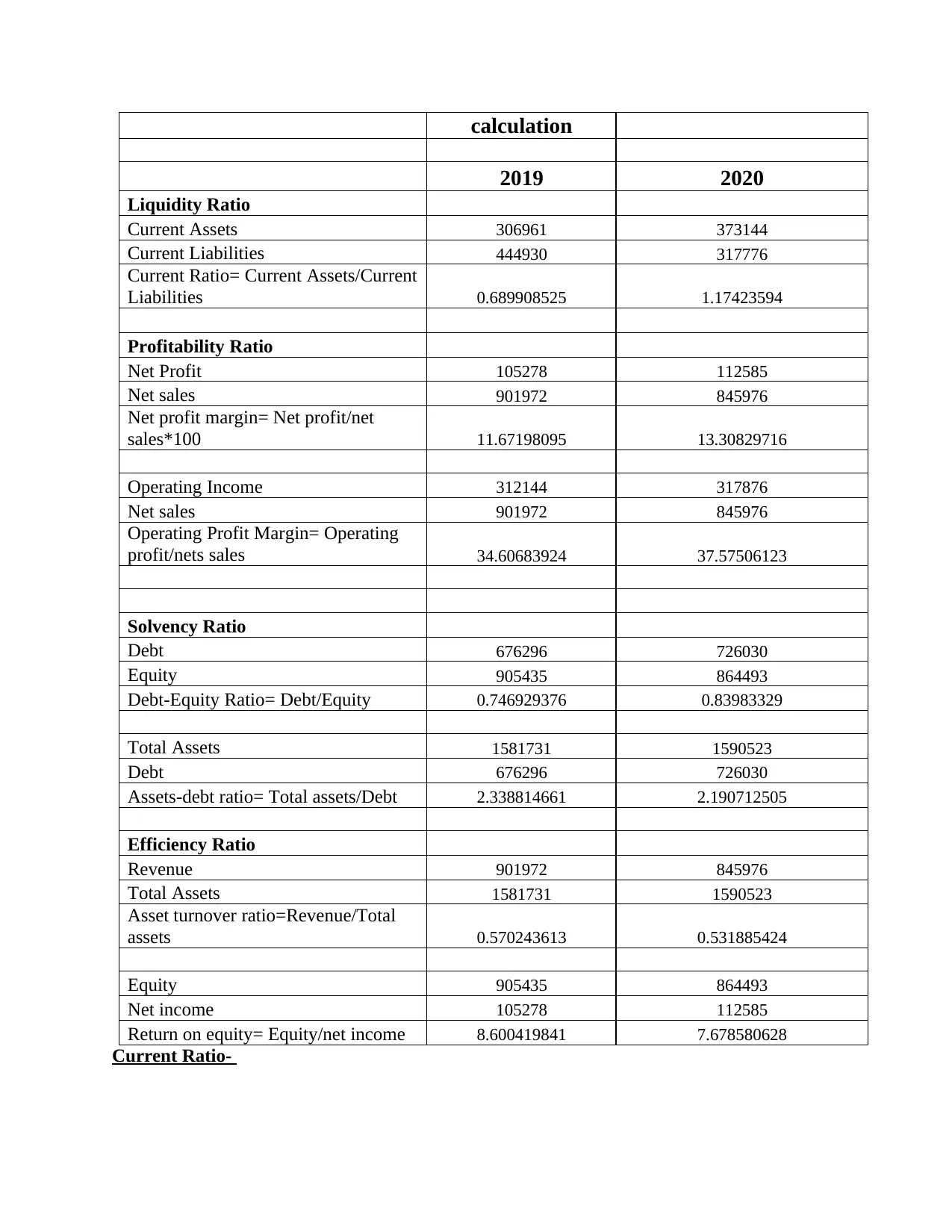

This report provides a comprehensive analysis of the financial management of REA Group Ltd. It begins with an introduction to financial management principles and the objectives of financial management within a company. The report then delves into the specifics of REA Group Ltd, a real estate company, discussing its background, operations, and financial performance. The core of the report focuses on ratio analysis, including liquidity, profitability, solvency, and efficiency ratios. Each ratio is calculated and analyzed for the years 2019 and 2020, with interpretations and comparisons to industry standards. The analysis covers current ratio, net profit margin, operating profit margin, debt-equity ratio, asset-debt ratio, asset turnover ratio, and return on equity. The report concludes with an overall assessment of REA Group Ltd's financial performance, highlighting strengths and weaknesses, and offering recommendations for improvement. The report is based on the company's financial statements and provides insights into the company's ability to manage its finances effectively and its potential for future growth. The report is intended to provide insights into financial performance and is suitable for students and analysts.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.