Finance Report: Real Estate Investment Analysis and Recommendations

VerifiedAdded on 2023/06/03

|8

|1630

|117

Report

AI Summary

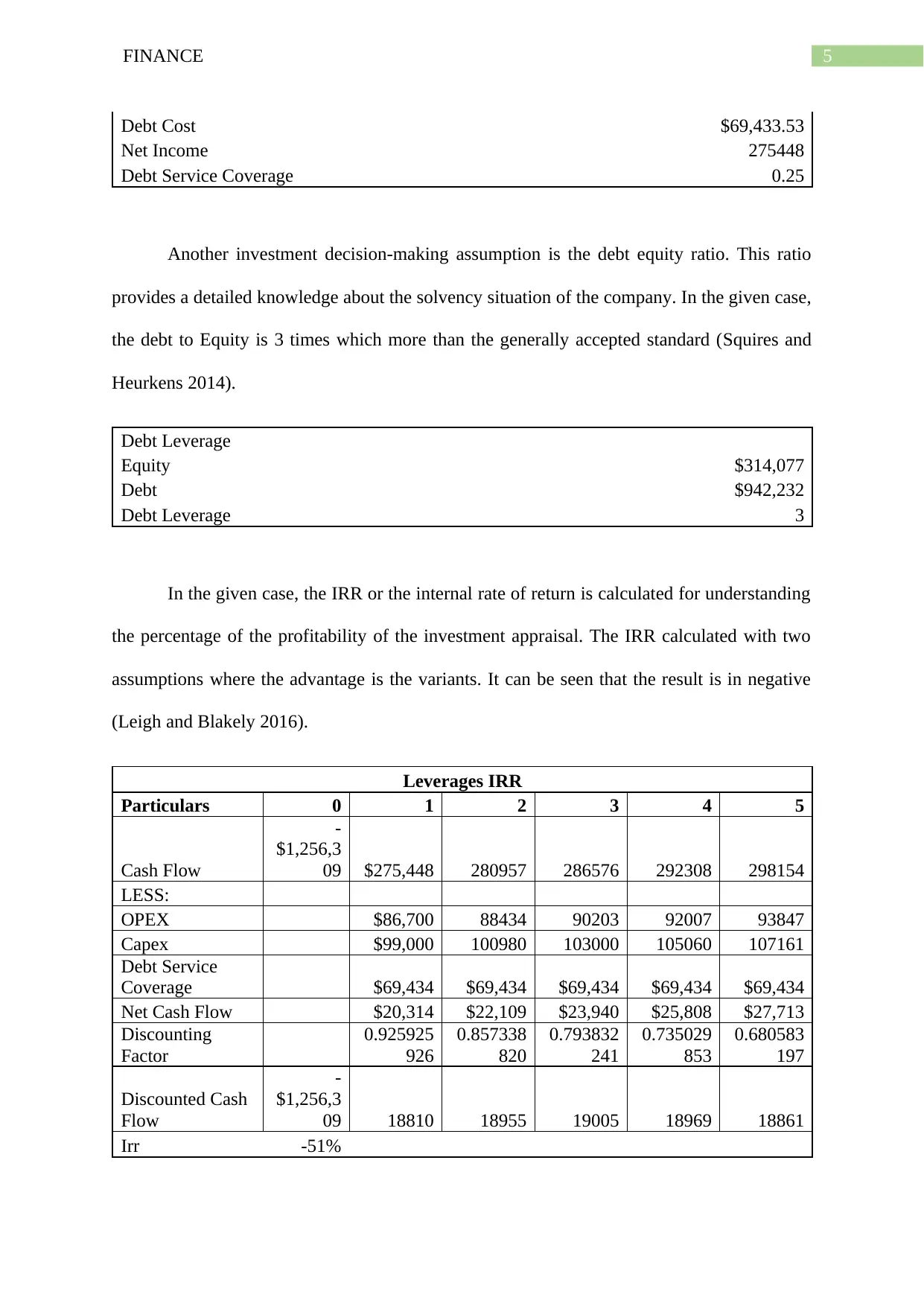

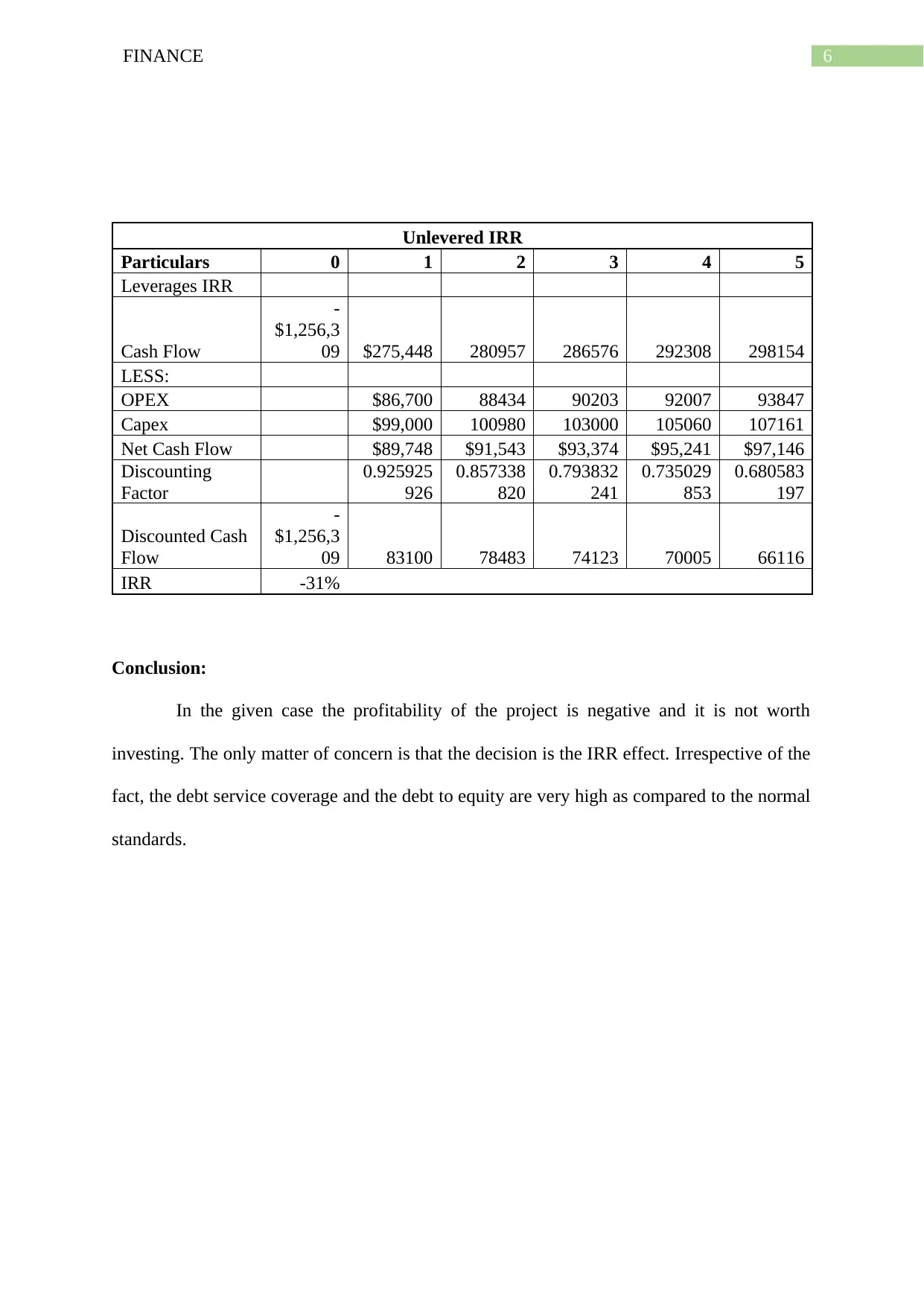

This report presents a financial analysis of a real estate investment opportunity, evaluating its profitability and financial viability. The analysis includes the creation of a property-level income statement, calculation of the going-in cap rate, and projections over a five-year holding period. Key financial metrics such as Net Present Value (NPV), Internal Rate of Return (IRR), Debt Service Coverage Ratio, and Debt Yield are calculated to assess the investment's performance. The report considers factors like rental income, operating expenses, and debt service to determine the project's overall financial health. Based on the financial results, the report provides a recommendation on whether to proceed with the investment, considering the firm's benchmark of investing in the Vanguard S&P 500 mutual fund. The analysis highlights both leveraged and unleveraged scenarios to understand the impact of debt on the project's returns.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.