Real Estate Finance Analysis: Holt Lunsford Commercial Case Study

VerifiedAdded on 2023/01/17

|10

|1878

|97

Report

AI Summary

This report presents a comprehensive analysis of a real estate finance case study involving Holt Lunsford Commercial, a Dallas-based commercial services firm. The core of the report revolves around evaluating two primary options for the company: leasing a property versus purchasing one. The analysis considers various financial factors, including sales, cost of goods sold, business expenses, and tax implications. The report explores the advantages and disadvantages of each option, taking into account market conditions, operational flexibility, initial investment costs, and potential tax benefits. The leasing option is assessed based on square footage, occupancy costs, and the potential for tax shields. The buying option considers the purchase price, operating expenses, interest expenses, and potential salvage value. The report also includes loan amortization and capital gain tax calculations. Ultimately, the report concludes that the leasing option is the more viable and flexible choice for the company's expansion, based on the provided financial analysis and strategic considerations.

Running head: REAL ESTATE FINANCE

Real Estate

Name of the Student:

Name of the University:

Author’s Note:

Real Estate

Name of the Student:

Name of the University:

Author’s Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1REAL ESTATE

Table of Contents

Introduction......................................................................................................................................2

Discussion........................................................................................................................................2

Leasing Option.............................................................................................................................3

Buying Option.............................................................................................................................4

Conclusion.......................................................................................................................................5

References........................................................................................................................................6

Appendix..........................................................................................................................................8

Table of Contents

Introduction......................................................................................................................................2

Discussion........................................................................................................................................2

Leasing Option.............................................................................................................................3

Buying Option.............................................................................................................................4

Conclusion.......................................................................................................................................5

References........................................................................................................................................6

Appendix..........................................................................................................................................8

2REAL ESTATE

Introduction

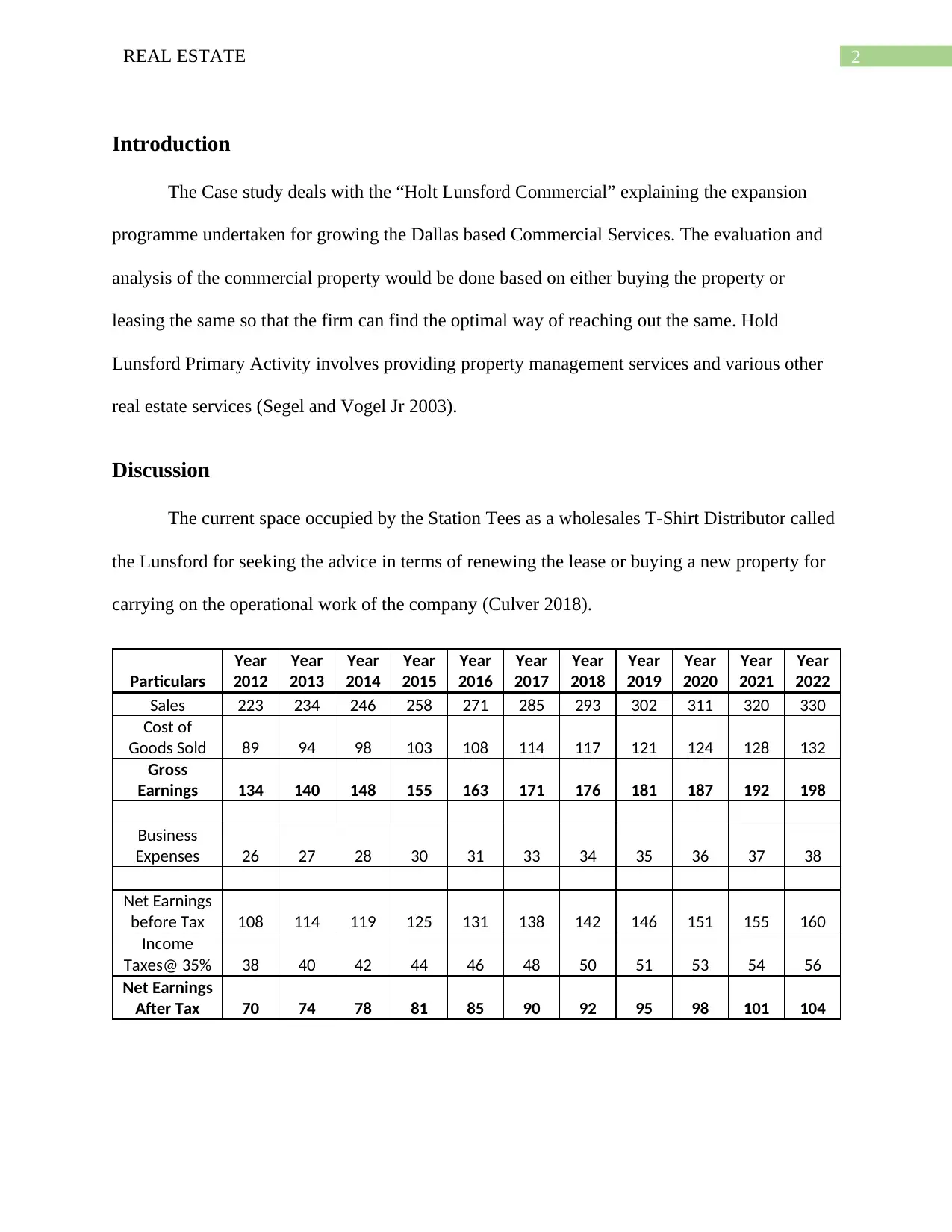

The Case study deals with the “Holt Lunsford Commercial” explaining the expansion

programme undertaken for growing the Dallas based Commercial Services. The evaluation and

analysis of the commercial property would be done based on either buying the property or

leasing the same so that the firm can find the optimal way of reaching out the same. Hold

Lunsford Primary Activity involves providing property management services and various other

real estate services (Segel and Vogel Jr 2003).

Discussion

The current space occupied by the Station Tees as a wholesales T-Shirt Distributor called

the Lunsford for seeking the advice in terms of renewing the lease or buying a new property for

carrying on the operational work of the company (Culver 2018).

Particulars

Year

2012

Year

2013

Year

2014

Year

2015

Year

2016

Year

2017

Year

2018

Year

2019

Year

2020

Year

2021

Year

2022

Sales 223 234 246 258 271 285 293 302 311 320 330

Cost of

Goods Sold 89 94 98 103 108 114 117 121 124 128 132

Gross

Earnings 134 140 148 155 163 171 176 181 187 192 198

Business

Expenses 26 27 28 30 31 33 34 35 36 37 38

Net Earnings

before Tax 108 114 119 125 131 138 142 146 151 155 160

Income

Taxes@ 35% 38 40 42 44 46 48 50 51 53 54 56

Net Earnings

After Tax 70 74 78 81 85 90 92 95 98 101 104

Introduction

The Case study deals with the “Holt Lunsford Commercial” explaining the expansion

programme undertaken for growing the Dallas based Commercial Services. The evaluation and

analysis of the commercial property would be done based on either buying the property or

leasing the same so that the firm can find the optimal way of reaching out the same. Hold

Lunsford Primary Activity involves providing property management services and various other

real estate services (Segel and Vogel Jr 2003).

Discussion

The current space occupied by the Station Tees as a wholesales T-Shirt Distributor called

the Lunsford for seeking the advice in terms of renewing the lease or buying a new property for

carrying on the operational work of the company (Culver 2018).

Particulars

Year

2012

Year

2013

Year

2014

Year

2015

Year

2016

Year

2017

Year

2018

Year

2019

Year

2020

Year

2021

Year

2022

Sales 223 234 246 258 271 285 293 302 311 320 330

Cost of

Goods Sold 89 94 98 103 108 114 117 121 124 128 132

Gross

Earnings 134 140 148 155 163 171 176 181 187 192 198

Business

Expenses 26 27 28 30 31 33 34 35 36 37 38

Net Earnings

before Tax 108 114 119 125 131 138 142 146 151 155 160

Income

Taxes@ 35% 38 40 42 44 46 48 50 51 53 54 56

Net Earnings

After Tax 70 74 78 81 85 90 92 95 98 101 104

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3REAL ESTATE

The profitability and the net earnings of the company was seen to be increasing and the

same was done after accounting with the given business assumptions. The operational work in

the form of logistics operations and distribution networking process is not expected to change

immediately, which shows that the leasing option would be considered as a more flexible option.

The operation and the growth of the company is depended highly on the demand created by the

consumers. It should be noted that the apparels industry might also be affected if there is a major

downward trend in the economy. On the other hand, business risk associated with such type of

apparel industry is also high. Buying a property would entail a huge initial investment making

the fixed overhead costs of the company to be high.

Leasing Option

The space taken into consideration for the purpose of analysis was the 102,718 square

foot front-loaded, industrial warehouse. The ceiling height would be around 24-foot and there

would be various other amenities that would be provided by the property including 107 parking

option, truck court, pick up and drop area and commercial office area. The property market

condition has been non-static with prices of the property to be rising (Bordenave and Stout

2017). However, when accounting and analysing the annual lease cost that the company would

be paying will be around $4.5, which will be the occupancy cost comprising of rent and

operating expenses. The analysis and the estimation of the cost for the tenure of the lease period

that is 10 years of life would be taken into consideration after considering inflation. In every

three years of tenure the occupancy cost of the company is expected to rise by three years and the

same has been adjusted and consideration (Nazlioglu, Gormus and Soytas 2016). If technology

and operations of the company changes in contrast to the market and economic scenario the

company would be having a real option or flexibility in exercising the same. Given the choice

The profitability and the net earnings of the company was seen to be increasing and the

same was done after accounting with the given business assumptions. The operational work in

the form of logistics operations and distribution networking process is not expected to change

immediately, which shows that the leasing option would be considered as a more flexible option.

The operation and the growth of the company is depended highly on the demand created by the

consumers. It should be noted that the apparels industry might also be affected if there is a major

downward trend in the economy. On the other hand, business risk associated with such type of

apparel industry is also high. Buying a property would entail a huge initial investment making

the fixed overhead costs of the company to be high.

Leasing Option

The space taken into consideration for the purpose of analysis was the 102,718 square

foot front-loaded, industrial warehouse. The ceiling height would be around 24-foot and there

would be various other amenities that would be provided by the property including 107 parking

option, truck court, pick up and drop area and commercial office area. The property market

condition has been non-static with prices of the property to be rising (Bordenave and Stout

2017). However, when accounting and analysing the annual lease cost that the company would

be paying will be around $4.5, which will be the occupancy cost comprising of rent and

operating expenses. The analysis and the estimation of the cost for the tenure of the lease period

that is 10 years of life would be taken into consideration after considering inflation. In every

three years of tenure the occupancy cost of the company is expected to rise by three years and the

same has been adjusted and consideration (Nazlioglu, Gormus and Soytas 2016). If technology

and operations of the company changes in contrast to the market and economic scenario the

company would be having a real option or flexibility in exercising the same. Given the choice

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4REAL ESTATE

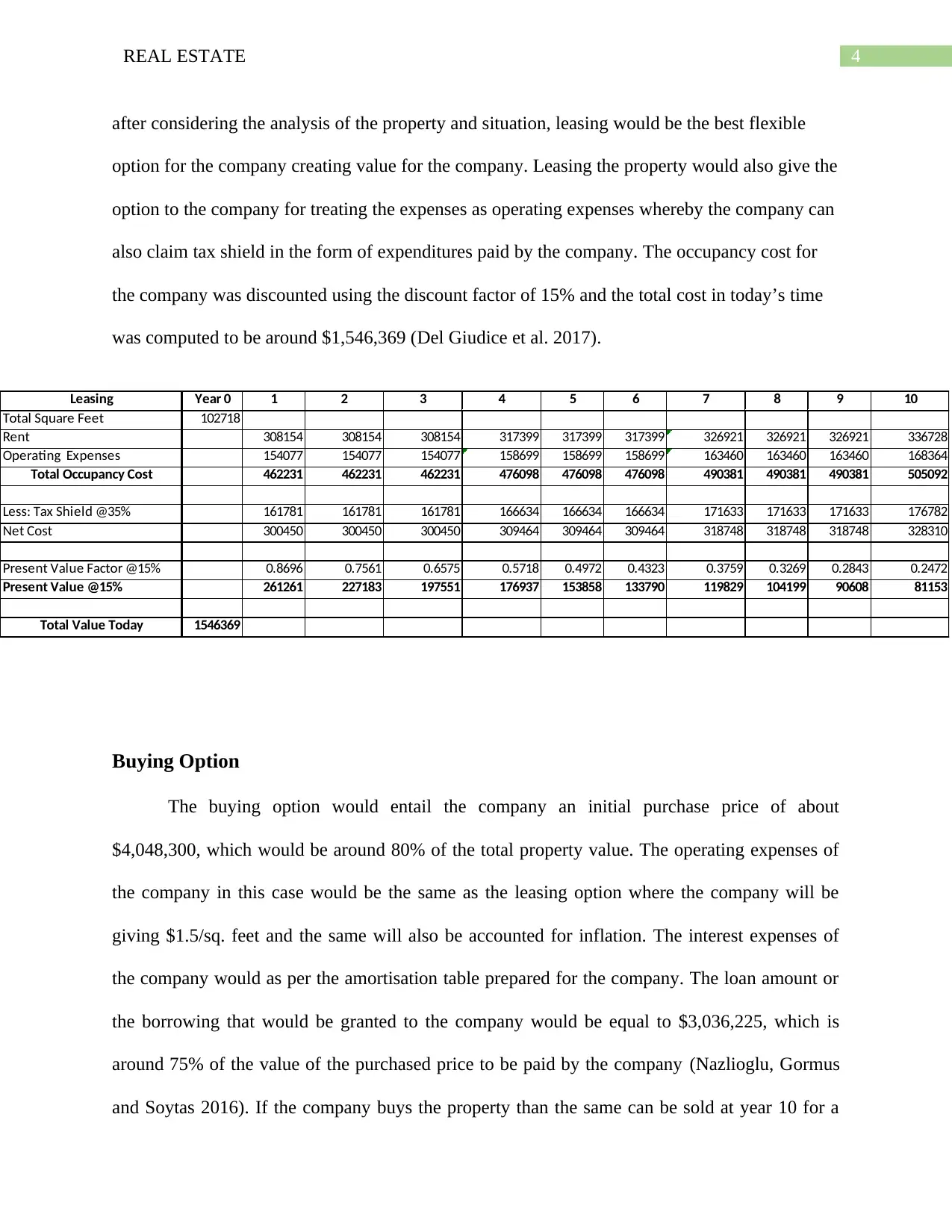

after considering the analysis of the property and situation, leasing would be the best flexible

option for the company creating value for the company. Leasing the property would also give the

option to the company for treating the expenses as operating expenses whereby the company can

also claim tax shield in the form of expenditures paid by the company. The occupancy cost for

the company was discounted using the discount factor of 15% and the total cost in today’s time

was computed to be around $1,546,369 (Del Giudice et al. 2017).

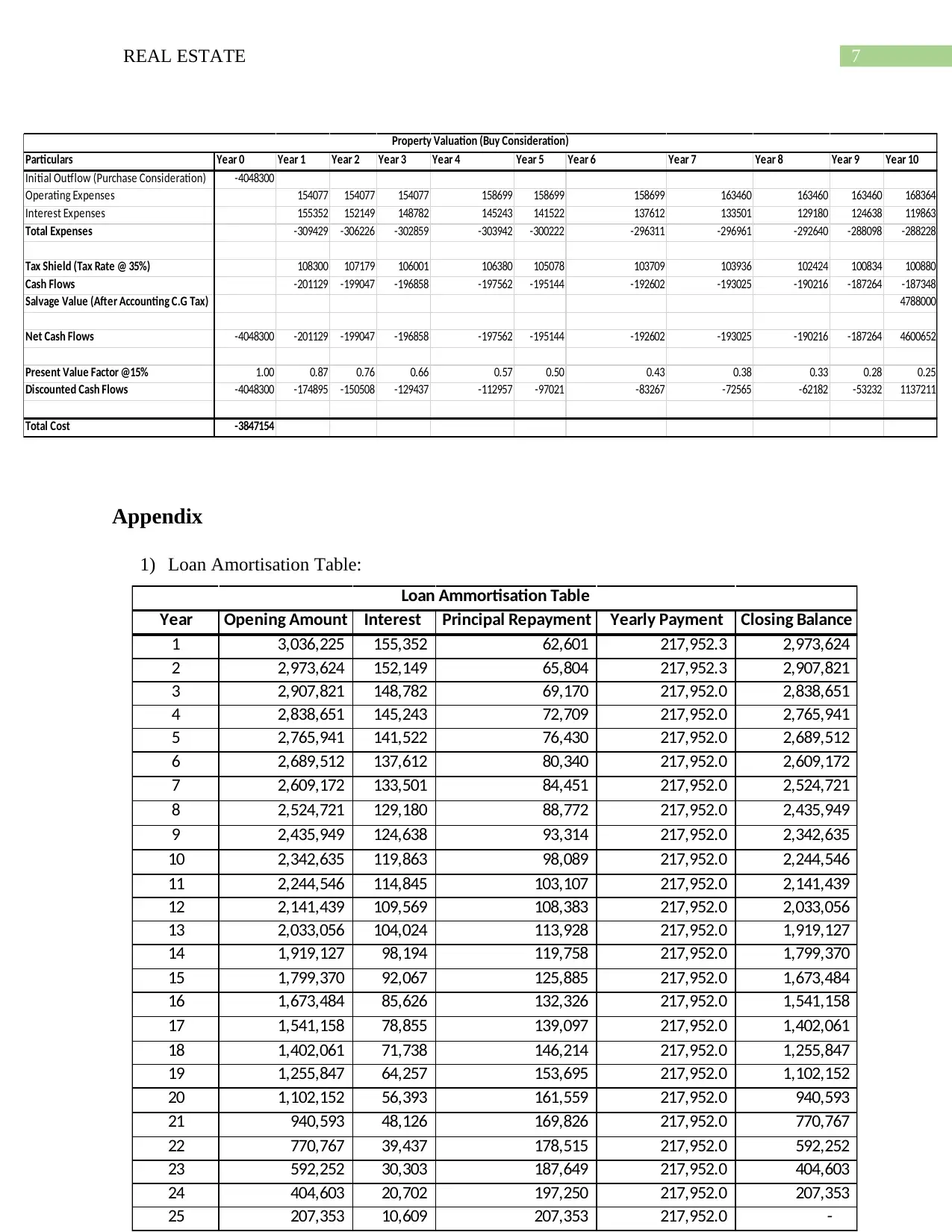

Buying Option

The buying option would entail the company an initial purchase price of about

$4,048,300, which would be around 80% of the total property value. The operating expenses of

the company in this case would be the same as the leasing option where the company will be

giving $1.5/sq. feet and the same will also be accounted for inflation. The interest expenses of

the company would as per the amortisation table prepared for the company. The loan amount or

the borrowing that would be granted to the company would be equal to $3,036,225, which is

around 75% of the value of the purchased price to be paid by the company (Nazlioglu, Gormus

and Soytas 2016). If the company buys the property than the same can be sold at year 10 for a

Leasing Year 0 1 2 3 4 5 6 7 8 9 10

Total Square Feet 102718

Rent 308154 308154 308154 317399 317399 317399 326921 326921 326921 336728

Operating Expenses 154077 154077 154077 158699 158699 158699 163460 163460 163460 168364

Total Occupancy Cost 462231 462231 462231 476098 476098 476098 490381 490381 490381 505092

Less: Tax Shield @35% 161781 161781 161781 166634 166634 166634 171633 171633 171633 176782

Net Cost 300450 300450 300450 309464 309464 309464 318748 318748 318748 328310

Present Value Factor @15% 0.8696 0.7561 0.6575 0.5718 0.4972 0.4323 0.3759 0.3269 0.2843 0.2472

Present Value @15% 261261 227183 197551 176937 153858 133790 119829 104199 90608 81153

Total Value Today 1546369

after considering the analysis of the property and situation, leasing would be the best flexible

option for the company creating value for the company. Leasing the property would also give the

option to the company for treating the expenses as operating expenses whereby the company can

also claim tax shield in the form of expenditures paid by the company. The occupancy cost for

the company was discounted using the discount factor of 15% and the total cost in today’s time

was computed to be around $1,546,369 (Del Giudice et al. 2017).

Buying Option

The buying option would entail the company an initial purchase price of about

$4,048,300, which would be around 80% of the total property value. The operating expenses of

the company in this case would be the same as the leasing option where the company will be

giving $1.5/sq. feet and the same will also be accounted for inflation. The interest expenses of

the company would as per the amortisation table prepared for the company. The loan amount or

the borrowing that would be granted to the company would be equal to $3,036,225, which is

around 75% of the value of the purchased price to be paid by the company (Nazlioglu, Gormus

and Soytas 2016). If the company buys the property than the same can be sold at year 10 for a

Leasing Year 0 1 2 3 4 5 6 7 8 9 10

Total Square Feet 102718

Rent 308154 308154 308154 317399 317399 317399 326921 326921 326921 336728

Operating Expenses 154077 154077 154077 158699 158699 158699 163460 163460 163460 168364

Total Occupancy Cost 462231 462231 462231 476098 476098 476098 490381 490381 490381 505092

Less: Tax Shield @35% 161781 161781 161781 166634 166634 166634 171633 171633 171633 176782

Net Cost 300450 300450 300450 309464 309464 309464 318748 318748 318748 328310

Present Value Factor @15% 0.8696 0.7561 0.6575 0.5718 0.4972 0.4323 0.3759 0.3269 0.2843 0.2472

Present Value @15% 261261 227183 197551 176937 153858 133790 119829 104199 90608 81153

Total Value Today 1546369

5REAL ESTATE

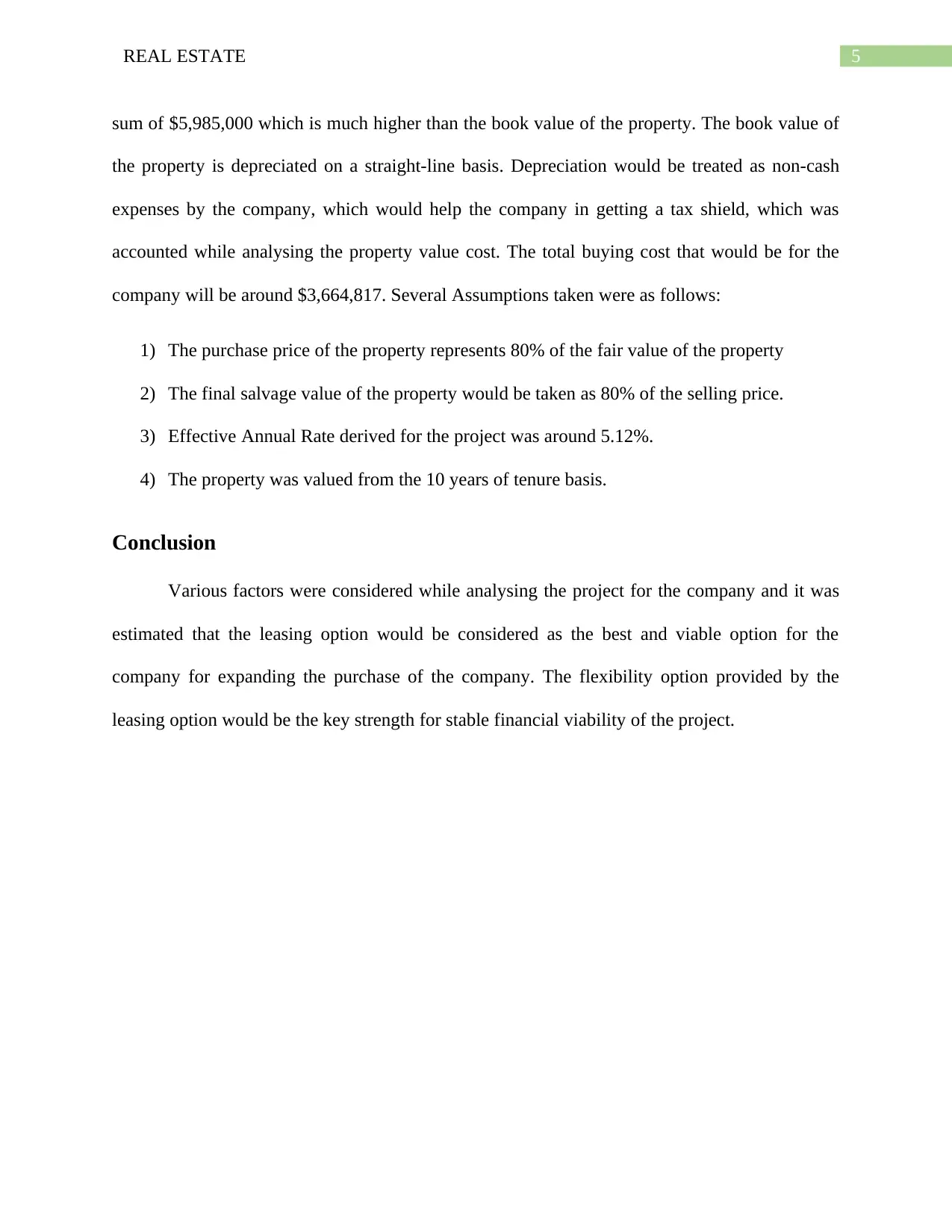

sum of $5,985,000 which is much higher than the book value of the property. The book value of

the property is depreciated on a straight-line basis. Depreciation would be treated as non-cash

expenses by the company, which would help the company in getting a tax shield, which was

accounted while analysing the property value cost. The total buying cost that would be for the

company will be around $3,664,817. Several Assumptions taken were as follows:

1) The purchase price of the property represents 80% of the fair value of the property

2) The final salvage value of the property would be taken as 80% of the selling price.

3) Effective Annual Rate derived for the project was around 5.12%.

4) The property was valued from the 10 years of tenure basis.

Conclusion

Various factors were considered while analysing the project for the company and it was

estimated that the leasing option would be considered as the best and viable option for the

company for expanding the purchase of the company. The flexibility option provided by the

leasing option would be the key strength for stable financial viability of the project.

sum of $5,985,000 which is much higher than the book value of the property. The book value of

the property is depreciated on a straight-line basis. Depreciation would be treated as non-cash

expenses by the company, which would help the company in getting a tax shield, which was

accounted while analysing the property value cost. The total buying cost that would be for the

company will be around $3,664,817. Several Assumptions taken were as follows:

1) The purchase price of the property represents 80% of the fair value of the property

2) The final salvage value of the property would be taken as 80% of the selling price.

3) Effective Annual Rate derived for the project was around 5.12%.

4) The property was valued from the 10 years of tenure basis.

Conclusion

Various factors were considered while analysing the project for the company and it was

estimated that the leasing option would be considered as the best and viable option for the

company for expanding the purchase of the company. The flexibility option provided by the

leasing option would be the key strength for stable financial viability of the project.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6REAL ESTATE

References

Bordenave, J. and Stout, D., 2017. Real Estate Analysis as a Tool for Program Evaluation.

Cityscape, 19(3), pp.475-486.

Culver, J., 2018. False Dilemma. Bad Arguments: 100 of the Most Important Fallacies in

Western Philosophy, pp.346-347.

Del Giudice, V., De Paola, P., Manganelli, B. and Forte, F., 2017. The monetary valuation of

environmental externalities through the analysis of real estate prices. Sustainability, 9(2), p.229.

Nazlioglu, S., Gormus, N.A. and Soytas, U., 2016. Oil prices and real estate investment trusts

(REITs): Gradual-shift causality and volatility transmission analysis. Energy Economics, 60,

pp.168-175.

Nazlioglu, S., Gormus, N.A. and Soytas, U., 2016. Oil prices and real estate investment trusts

(REITs): Gradual-shift causality and volatility transmission analysis. Energy Economics, 60,

pp.168-175.

Segel, A.I. and Vogel Jr, J.H., 2003. Holt Lunsford Commercial.

References

Bordenave, J. and Stout, D., 2017. Real Estate Analysis as a Tool for Program Evaluation.

Cityscape, 19(3), pp.475-486.

Culver, J., 2018. False Dilemma. Bad Arguments: 100 of the Most Important Fallacies in

Western Philosophy, pp.346-347.

Del Giudice, V., De Paola, P., Manganelli, B. and Forte, F., 2017. The monetary valuation of

environmental externalities through the analysis of real estate prices. Sustainability, 9(2), p.229.

Nazlioglu, S., Gormus, N.A. and Soytas, U., 2016. Oil prices and real estate investment trusts

(REITs): Gradual-shift causality and volatility transmission analysis. Energy Economics, 60,

pp.168-175.

Nazlioglu, S., Gormus, N.A. and Soytas, U., 2016. Oil prices and real estate investment trusts

(REITs): Gradual-shift causality and volatility transmission analysis. Energy Economics, 60,

pp.168-175.

Segel, A.I. and Vogel Jr, J.H., 2003. Holt Lunsford Commercial.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7REAL ESTATE

Appendix

1) Loan Amortisation Table:

Year Opening Amount Interest Principal Repayment Yearly Payment Closing Balance

1 3,036,225 155,352 62,601 217,952.3 2,973,624

2 2,973,624 152,149 65,804 217,952.3 2,907,821

3 2,907,821 148,782 69,170 217,952.0 2,838,651

4 2,838,651 145,243 72,709 217,952.0 2,765,941

5 2,765,941 141,522 76,430 217,952.0 2,689,512

6 2,689,512 137,612 80,340 217,952.0 2,609,172

7 2,609,172 133,501 84,451 217,952.0 2,524,721

8 2,524,721 129,180 88,772 217,952.0 2,435,949

9 2,435,949 124,638 93,314 217,952.0 2,342,635

10 2,342,635 119,863 98,089 217,952.0 2,244,546

11 2,244,546 114,845 103,107 217,952.0 2,141,439

12 2,141,439 109,569 108,383 217,952.0 2,033,056

13 2,033,056 104,024 113,928 217,952.0 1,919,127

14 1,919,127 98,194 119,758 217,952.0 1,799,370

15 1,799,370 92,067 125,885 217,952.0 1,673,484

16 1,673,484 85,626 132,326 217,952.0 1,541,158

17 1,541,158 78,855 139,097 217,952.0 1,402,061

18 1,402,061 71,738 146,214 217,952.0 1,255,847

19 1,255,847 64,257 153,695 217,952.0 1,102,152

20 1,102,152 56,393 161,559 217,952.0 940,593

21 940,593 48,126 169,826 217,952.0 770,767

22 770,767 39,437 178,515 217,952.0 592,252

23 592,252 30,303 187,649 217,952.0 404,603

24 404,603 20,702 197,250 217,952.0 207,353

25 207,353 10,609 207,353 217,952.0 -

Loan Ammortisation Table

Particulars Year 0 Year 1 Year 2 Year 3 Year 4 Year 5 Year 6 Year 7 Year 8 Year 9 Year 10

Initial Outflow (Purchase Consideration) -4048300

Operating Expenses 154077 154077 154077 158699 158699 158699 163460 163460 163460 168364

Interest Expenses 155352 152149 148782 145243 141522 137612 133501 129180 124638 119863

Total Expenses -309429 -306226 -302859 -303942 -300222 -296311 -296961 -292640 -288098 -288228

Tax Shield (Tax Rate @ 35%) 108300 107179 106001 106380 105078 103709 103936 102424 100834 100880

Cash Flows -201129 -199047 -196858 -197562 -195144 -192602 -193025 -190216 -187264 -187348

Salvage Value (After Accounting C.G Tax) 4788000

Net Cash Flows -4048300 -201129 -199047 -196858 -197562 -195144 -192602 -193025 -190216 -187264 4600652

Present Value Factor @15% 1.00 0.87 0.76 0.66 0.57 0.50 0.43 0.38 0.33 0.28 0.25

Discounted Cash Flows -4048300 -174895 -150508 -129437 -112957 -97021 -83267 -72565 -62182 -53232 1137211

Total Cost -3847154

Property Valuation (Buy Consideration)

Appendix

1) Loan Amortisation Table:

Year Opening Amount Interest Principal Repayment Yearly Payment Closing Balance

1 3,036,225 155,352 62,601 217,952.3 2,973,624

2 2,973,624 152,149 65,804 217,952.3 2,907,821

3 2,907,821 148,782 69,170 217,952.0 2,838,651

4 2,838,651 145,243 72,709 217,952.0 2,765,941

5 2,765,941 141,522 76,430 217,952.0 2,689,512

6 2,689,512 137,612 80,340 217,952.0 2,609,172

7 2,609,172 133,501 84,451 217,952.0 2,524,721

8 2,524,721 129,180 88,772 217,952.0 2,435,949

9 2,435,949 124,638 93,314 217,952.0 2,342,635

10 2,342,635 119,863 98,089 217,952.0 2,244,546

11 2,244,546 114,845 103,107 217,952.0 2,141,439

12 2,141,439 109,569 108,383 217,952.0 2,033,056

13 2,033,056 104,024 113,928 217,952.0 1,919,127

14 1,919,127 98,194 119,758 217,952.0 1,799,370

15 1,799,370 92,067 125,885 217,952.0 1,673,484

16 1,673,484 85,626 132,326 217,952.0 1,541,158

17 1,541,158 78,855 139,097 217,952.0 1,402,061

18 1,402,061 71,738 146,214 217,952.0 1,255,847

19 1,255,847 64,257 153,695 217,952.0 1,102,152

20 1,102,152 56,393 161,559 217,952.0 940,593

21 940,593 48,126 169,826 217,952.0 770,767

22 770,767 39,437 178,515 217,952.0 592,252

23 592,252 30,303 187,649 217,952.0 404,603

24 404,603 20,702 197,250 217,952.0 207,353

25 207,353 10,609 207,353 217,952.0 -

Loan Ammortisation Table

Particulars Year 0 Year 1 Year 2 Year 3 Year 4 Year 5 Year 6 Year 7 Year 8 Year 9 Year 10

Initial Outflow (Purchase Consideration) -4048300

Operating Expenses 154077 154077 154077 158699 158699 158699 163460 163460 163460 168364

Interest Expenses 155352 152149 148782 145243 141522 137612 133501 129180 124638 119863

Total Expenses -309429 -306226 -302859 -303942 -300222 -296311 -296961 -292640 -288098 -288228

Tax Shield (Tax Rate @ 35%) 108300 107179 106001 106380 105078 103709 103936 102424 100834 100880

Cash Flows -201129 -199047 -196858 -197562 -195144 -192602 -193025 -190216 -187264 -187348

Salvage Value (After Accounting C.G Tax) 4788000

Net Cash Flows -4048300 -201129 -199047 -196858 -197562 -195144 -192602 -193025 -190216 -187264 4600652

Present Value Factor @15% 1.00 0.87 0.76 0.66 0.57 0.50 0.43 0.38 0.33 0.28 0.25

Discounted Cash Flows -4048300 -174895 -150508 -129437 -112957 -97021 -83267 -72565 -62182 -53232 1137211

Total Cost -3847154

Property Valuation (Buy Consideration)

8REAL ESTATE

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9REAL ESTATE

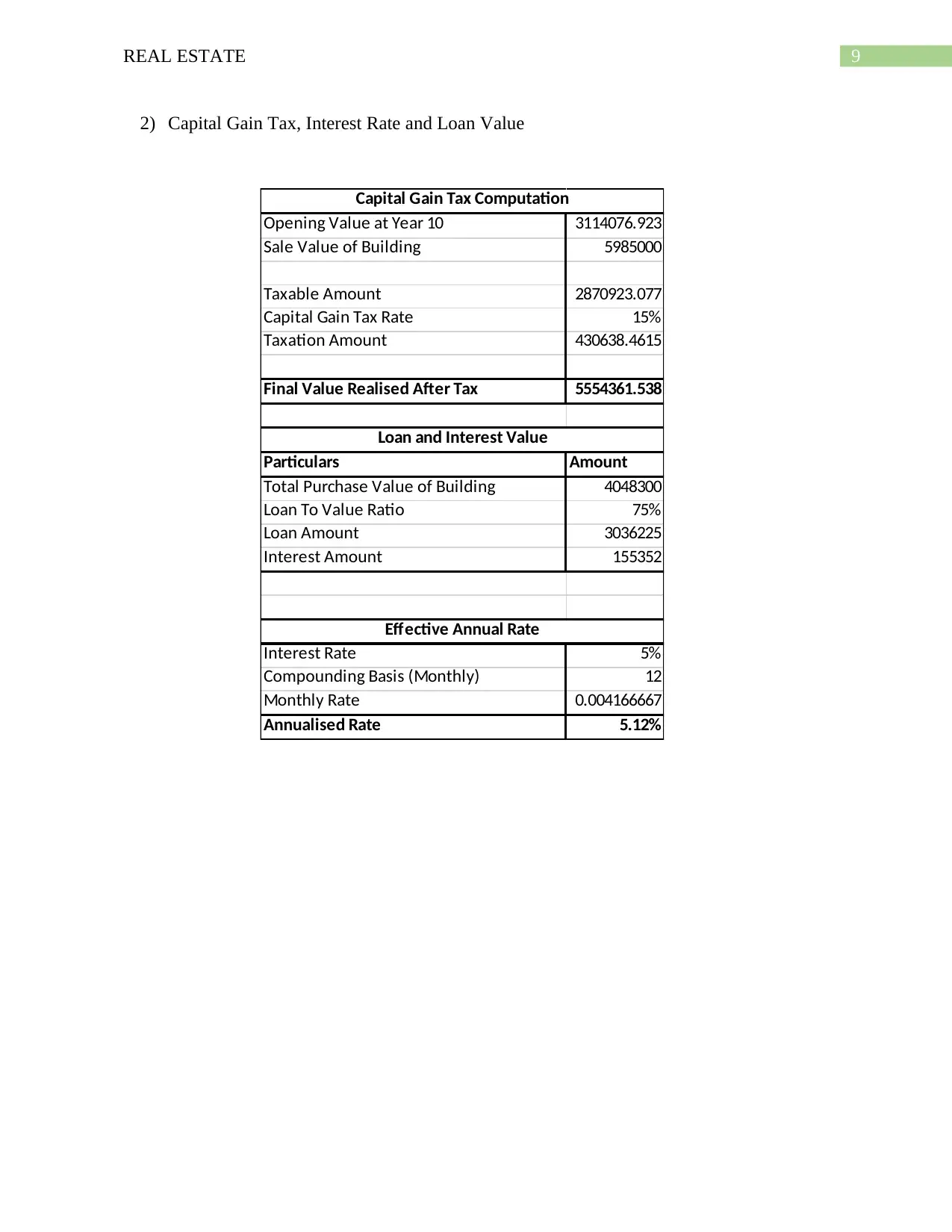

2) Capital Gain Tax, Interest Rate and Loan Value

Opening Value at Year 10 3114076.923

Sale Value of Building 5985000

Taxable Amount 2870923.077

Capital Gain Tax Rate 15%

Taxation Amount 430638.4615

Final Value Realised After Tax 5554361.538

Particulars Amount

Total Purchase Value of Building 4048300

Loan To Value Ratio 75%

Loan Amount 3036225

Interest Amount 155352

Interest Rate 5%

Compounding Basis (Monthly) 12

Monthly Rate 0.004166667

Annualised Rate 5.12%

Capital Gain Tax Computation

Loan and Interest Value

Effective Annual Rate

2) Capital Gain Tax, Interest Rate and Loan Value

Opening Value at Year 10 3114076.923

Sale Value of Building 5985000

Taxable Amount 2870923.077

Capital Gain Tax Rate 15%

Taxation Amount 430638.4615

Final Value Realised After Tax 5554361.538

Particulars Amount

Total Purchase Value of Building 4048300

Loan To Value Ratio 75%

Loan Amount 3036225

Interest Amount 155352

Interest Rate 5%

Compounding Basis (Monthly) 12

Monthly Rate 0.004166667

Annualised Rate 5.12%

Capital Gain Tax Computation

Loan and Interest Value

Effective Annual Rate

1 out of 10

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.