Nottingham Trent University: Real Estate Funding and Finance Report

VerifiedAdded on 2022/10/19

|11

|2499

|16

Report

AI Summary

This report analyzes the impact of borrowing costs on real estate investment returns, focusing on the UK market using FTSE 350 data. It examines how factors like lending conditions, capital structure, and the cost of equity and debt influence real estate investments. The analysis includes the application of the Capital Asset Pricing Model (CAPM) to determine the cost of equity and considers factors like the loan-to-value ratio and working capital. The report also explores the impact of the 2008 financial crisis on capital availability and the role of debt financing in the real estate sector, highlighting the interplay of financial risk and capital structure decisions. Ultimately, the report provides a comprehensive overview of how financial factors shape real estate investment returns and risk.

Running head: REAL ESTATE FUNDING AND FINANCE

Real Estate

Name of the Student:

Name of the University:

Author’s Note:

Real Estate

Name of the Student:

Name of the University:

Author’s Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1REAL ESTATE FUNDING AND FINANCE

Executive Summary

The aim of the assignment is to conduct analysis about the various impact on the

borrowing costs that could affect the return generated by the real estate industry.

Investment return in any kind of sector is affected by a multiple factors that potentially

affects the overall return generated by the particular industry. The borrowing cost of the

company can be well determined with the help of the Weighted Average Cost of Capital

for the company and the Cost of Equity for the company can also be determined with

the help of Capital Asset Pricing Model for the firm. Factors associated in terms of

availability of capital and changes in the Loan to value ratio were some of the crucial

aspects that were undertaken by us for the purpose of analysis. The real estate return

could also be affected with the liquidity factor or working capital that may significantly

affect the operations and investment activities of an company.

Executive Summary

The aim of the assignment is to conduct analysis about the various impact on the

borrowing costs that could affect the return generated by the real estate industry.

Investment return in any kind of sector is affected by a multiple factors that potentially

affects the overall return generated by the particular industry. The borrowing cost of the

company can be well determined with the help of the Weighted Average Cost of Capital

for the company and the Cost of Equity for the company can also be determined with

the help of Capital Asset Pricing Model for the firm. Factors associated in terms of

availability of capital and changes in the Loan to value ratio were some of the crucial

aspects that were undertaken by us for the purpose of analysis. The real estate return

could also be affected with the liquidity factor or working capital that may significantly

affect the operations and investment activities of an company.

2REAL ESTATE FUNDING AND FINANCE

Introduction

The analysis of the real estate investment returns could be done with the help of

the volatile borrowing costs that have significantly impacted the cost of borrowing for the

company. The return generated by the real estate industry is impacted by a multiple

factors amongst, which borrowing costs along and economic conditions could be one of

the key reasons that would impact the overall return generated by the Real Estate

Industry. The country that has been selected for the purpose of analysis would be

United Kingdom where the FTSE 350 Real Estate Historical Data would be taken into

consideration. On the other hand for the purpose of determining the risk free rate or the

borrowing costs in associated with the Bond Year Bond Yield was analyzed for a five-

year trend period (Investing.com UK 2019). In terms of determining the rate of return on

the market index the FTSE 100 Stock was calculated and analyzed (Nazlioglu, S.,

Gormus, N.A. and Soytas 2016). The Capital Asset Pricing Model was then applied for

the purpose of determining the cost of equity for the company. The key factors that were

included in the determination of the cost of equity for the company were the risk free

rate of return and the return generated on the market index (Andonov, Eichholtz and

Kok 2015).

Discussion

Changes in Lending Conditions

The capital requirement of the firm is dependent on various factors including the

availability of the capital and the costs associated with each of the financing source of

capital. Traditionally, companies have been using the use of equity and debt financing

Introduction

The analysis of the real estate investment returns could be done with the help of

the volatile borrowing costs that have significantly impacted the cost of borrowing for the

company. The return generated by the real estate industry is impacted by a multiple

factors amongst, which borrowing costs along and economic conditions could be one of

the key reasons that would impact the overall return generated by the Real Estate

Industry. The country that has been selected for the purpose of analysis would be

United Kingdom where the FTSE 350 Real Estate Historical Data would be taken into

consideration. On the other hand for the purpose of determining the risk free rate or the

borrowing costs in associated with the Bond Year Bond Yield was analyzed for a five-

year trend period (Investing.com UK 2019). In terms of determining the rate of return on

the market index the FTSE 100 Stock was calculated and analyzed (Nazlioglu, S.,

Gormus, N.A. and Soytas 2016). The Capital Asset Pricing Model was then applied for

the purpose of determining the cost of equity for the company. The key factors that were

included in the determination of the cost of equity for the company were the risk free

rate of return and the return generated on the market index (Andonov, Eichholtz and

Kok 2015).

Discussion

Changes in Lending Conditions

The capital requirement of the firm is dependent on various factors including the

availability of the capital and the costs associated with each of the financing source of

capital. Traditionally, companies have been using the use of equity and debt financing

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3REAL ESTATE FUNDING AND FINANCE

for the purpose of financing the operations of the company (Van Loon and Aalbers

2017). The weightage of equity and debt in the capital structure of the company has

been taken in accordance with the business and financial risk associated with the

company so that the same does not create a burden on the company. The lending rates

for the economy could be well analyzed with the help of the changing costs or the

interest rate level in the economy (Investing.com UK 2019). If the interest rates

prevailing in the economy is considerably very high then the same would be affecting

the availability of capital and the overall associated return that could potentially affect

the investment in the real estate returns (Baum 2015). Investment in the real estate

sector is primarily done with the help of debt financing whereby the companies have

been undertaking various forms of short-term and long-term debt in order to finance and

execute various types of transactions. The interest rate prevailing should be at a

predetermined level so that more of investment activities takes place, however as

analyzed the interest rates or the bond yield generated could be well analyzed with the

help of the 10-year bond yield of UK (Salzman and Zwinkels 2017). The requirement of

working capital availability in the firm in their financial assets is also of prime concern

that otherwise would be affecting the profitability of the company and the various

operational works that the company should undertake. The factor of liquidity analysis in

the course of business is very important and the same should be analyzed from the

view point of working capital available with the firm for meeting the current liabilities and

the various activities it undertakes to do. After, the crisis of 2008, it was seen that the

availability of capital especially debt financing has been predominately affected in terms

of availability of the capital (Hoesli, M., Oikarinen, E. and Serrano 2015). The loan to

for the purpose of financing the operations of the company (Van Loon and Aalbers

2017). The weightage of equity and debt in the capital structure of the company has

been taken in accordance with the business and financial risk associated with the

company so that the same does not create a burden on the company. The lending rates

for the economy could be well analyzed with the help of the changing costs or the

interest rate level in the economy (Investing.com UK 2019). If the interest rates

prevailing in the economy is considerably very high then the same would be affecting

the availability of capital and the overall associated return that could potentially affect

the investment in the real estate returns (Baum 2015). Investment in the real estate

sector is primarily done with the help of debt financing whereby the companies have

been undertaking various forms of short-term and long-term debt in order to finance and

execute various types of transactions. The interest rate prevailing should be at a

predetermined level so that more of investment activities takes place, however as

analyzed the interest rates or the bond yield generated could be well analyzed with the

help of the 10-year bond yield of UK (Salzman and Zwinkels 2017). The requirement of

working capital availability in the firm in their financial assets is also of prime concern

that otherwise would be affecting the profitability of the company and the various

operational works that the company should undertake. The factor of liquidity analysis in

the course of business is very important and the same should be analyzed from the

view point of working capital available with the firm for meeting the current liabilities and

the various activities it undertakes to do. After, the crisis of 2008, it was seen that the

availability of capital especially debt financing has been predominately affected in terms

of availability of the capital (Hoesli, M., Oikarinen, E. and Serrano 2015). The loan to

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4REAL ESTATE FUNDING AND FINANCE

value ratio for the real estate industry was especially affected with aftermath of 2008

crisis where banks and financial institutions were not willing up to leverage real estate

companies with excess amount of debt. Financial risk in the real estate industry is of

prime concern and there are various factors that the companies and organization

undertake to reduce the same in the context of business operations (Investing.com UK

2019).

Capital Structure of Real Estate Companies

The capital structure of the real estate companies is predominately taken on a

side basis whereby the real estate companies have given much more emphasis on debt

financing rather than equity financing. Systematic and business risk associated within

the real estate company is also high that incorporates the high amount of systemic

changes in the context of economic and sector wise changes in the real estate industry

that could potentially affect the return on real estate investment. However, despite the

high amount of risk associated with the debt financing companies operating in the real

estate industry tend to select debt finance as the cost of financing is generally very low

as compared to other modes/sources of financing (Briere, Oosterlinck and Szafarz

2015). Firms that high sales and operating income tend to utilize more of the benefits of

debt financing in order to get benefits from high financial leverage in the form of tax

deductible interest expenses. The primary source of income for the real estate

companies is the rent and revenue received from the purchase and selling of real estate

properties. On the one hand side the rental income can be seen as a form of

sustainable income for the company but on the contrary side, revenue from purchase

and sell of real estate industry can be regarded as an unstable income that is earned by

value ratio for the real estate industry was especially affected with aftermath of 2008

crisis where banks and financial institutions were not willing up to leverage real estate

companies with excess amount of debt. Financial risk in the real estate industry is of

prime concern and there are various factors that the companies and organization

undertake to reduce the same in the context of business operations (Investing.com UK

2019).

Capital Structure of Real Estate Companies

The capital structure of the real estate companies is predominately taken on a

side basis whereby the real estate companies have given much more emphasis on debt

financing rather than equity financing. Systematic and business risk associated within

the real estate company is also high that incorporates the high amount of systemic

changes in the context of economic and sector wise changes in the real estate industry

that could potentially affect the return on real estate investment. However, despite the

high amount of risk associated with the debt financing companies operating in the real

estate industry tend to select debt finance as the cost of financing is generally very low

as compared to other modes/sources of financing (Briere, Oosterlinck and Szafarz

2015). Firms that high sales and operating income tend to utilize more of the benefits of

debt financing in order to get benefits from high financial leverage in the form of tax

deductible interest expenses. The primary source of income for the real estate

companies is the rent and revenue received from the purchase and selling of real estate

properties. On the one hand side the rental income can be seen as a form of

sustainable income for the company but on the contrary side, revenue from purchase

and sell of real estate industry can be regarded as an unstable income that is earned by

5REAL ESTATE FUNDING AND FINANCE

the company (Investing.com UK 2019). It is of great importance that the capital structure

of the company stays predominately at a stable rate so that the profitability returns

generated by the company does not get affected materially by the capital structure of

the company (Investing.com UK. 2019). Debt financing for the company on a

predominant basis could be materially affected with the availability and the associated

cost.

The capital structure of the company should be such that the same does not

affect the weighted average cost of capital that ultimately would be taken as the

required rate of return on the various capital budgeting projects that would be

undertaken. In a predominant basis it could be considered that debt financing would be

reducing the cost of capital for the company but on the other hand, side companies

would also be materially increasing the associated financial risk of the company

(Investing.com UK 2019).

Debt financing for the company could also be well explained with the help of the

various benefits associated with it for the purpose of financing. The key benefit that

companies and organizations can get from the same would be in the form of debt tax

relief that they would be getting in the associated financing. Companies would always

be getting an additive tax advantage from the tax deductible interest expenses that

would be paid by companies (Investing.com UK 2019). On the other hand side

companies would also be getting the benefit of low cost financing that ultimately would

be lowering down the cost of capital for the company. The reduced cost of capital or

required return would be allowing the companies to undertake more and more projects

the company (Investing.com UK 2019). It is of great importance that the capital structure

of the company stays predominately at a stable rate so that the profitability returns

generated by the company does not get affected materially by the capital structure of

the company (Investing.com UK. 2019). Debt financing for the company on a

predominant basis could be materially affected with the availability and the associated

cost.

The capital structure of the company should be such that the same does not

affect the weighted average cost of capital that ultimately would be taken as the

required rate of return on the various capital budgeting projects that would be

undertaken. In a predominant basis it could be considered that debt financing would be

reducing the cost of capital for the company but on the other hand, side companies

would also be materially increasing the associated financial risk of the company

(Investing.com UK 2019).

Debt financing for the company could also be well explained with the help of the

various benefits associated with it for the purpose of financing. The key benefit that

companies and organizations can get from the same would be in the form of debt tax

relief that they would be getting in the associated financing. Companies would always

be getting an additive tax advantage from the tax deductible interest expenses that

would be paid by companies (Investing.com UK 2019). On the other hand side

companies would also be getting the benefit of low cost financing that ultimately would

be lowering down the cost of capital for the company. The reduced cost of capital or

required return would be allowing the companies to undertake more and more projects

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6REAL ESTATE FUNDING AND FINANCE

for the purpose of investment and undertaken operational activity (Investing.com UK

2019).

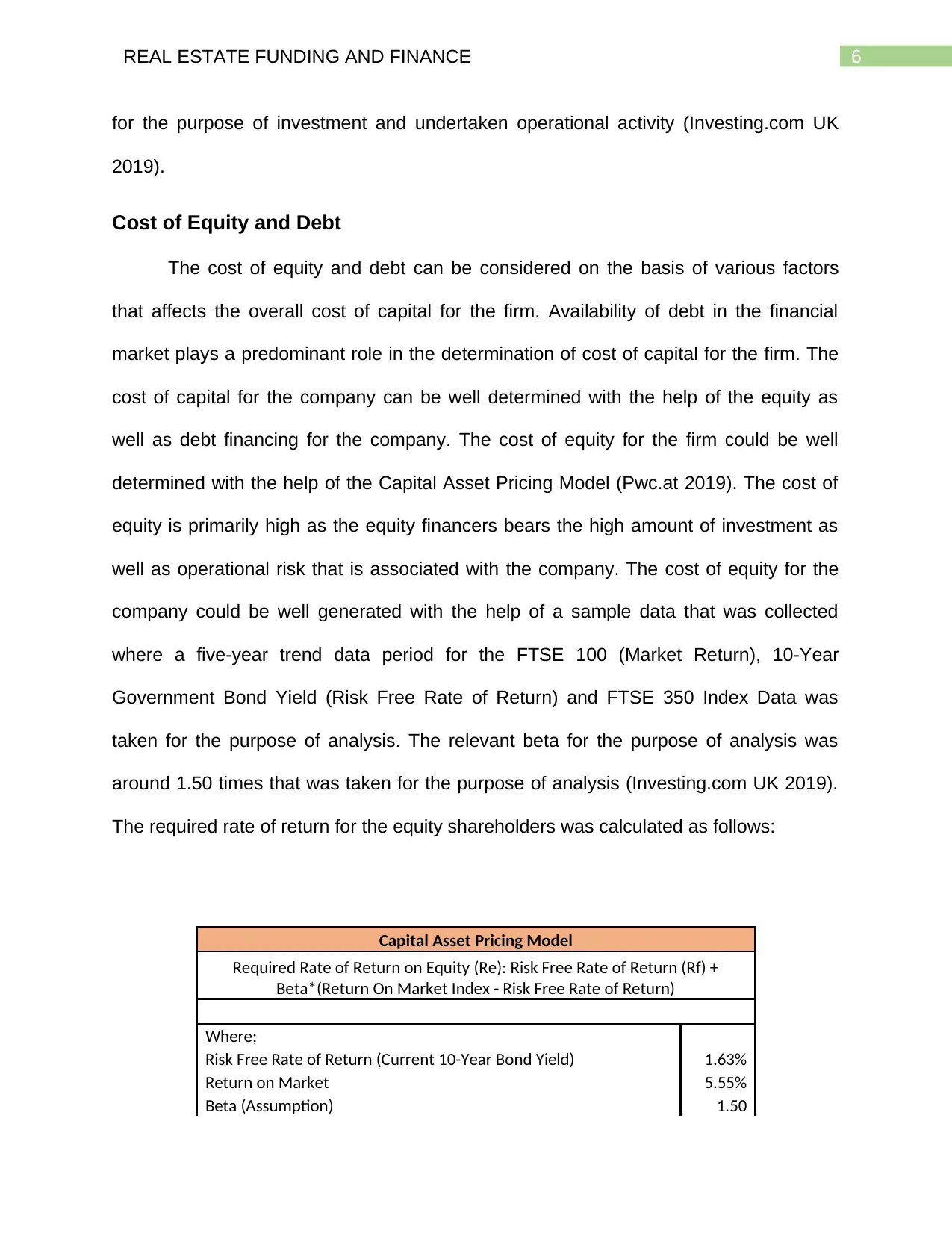

Cost of Equity and Debt

The cost of equity and debt can be considered on the basis of various factors

that affects the overall cost of capital for the firm. Availability of debt in the financial

market plays a predominant role in the determination of cost of capital for the firm. The

cost of capital for the company can be well determined with the help of the equity as

well as debt financing for the company. The cost of equity for the firm could be well

determined with the help of the Capital Asset Pricing Model (Pwc.at 2019). The cost of

equity is primarily high as the equity financers bears the high amount of investment as

well as operational risk that is associated with the company. The cost of equity for the

company could be well generated with the help of a sample data that was collected

where a five-year trend data period for the FTSE 100 (Market Return), 10-Year

Government Bond Yield (Risk Free Rate of Return) and FTSE 350 Index Data was

taken for the purpose of analysis. The relevant beta for the purpose of analysis was

around 1.50 times that was taken for the purpose of analysis (Investing.com UK 2019).

The required rate of return for the equity shareholders was calculated as follows:

Capital Asset Pricing Model

Required Rate of Return on Equity (Re): Risk Free Rate of Return (Rf) +

Beta*(Return On Market Index - Risk Free Rate of Return)

Where;

Risk Free Rate of Return (Current 10-Year Bond Yield) 1.63%

Return on Market 5.55%

Beta (Assumption) 1.50

for the purpose of investment and undertaken operational activity (Investing.com UK

2019).

Cost of Equity and Debt

The cost of equity and debt can be considered on the basis of various factors

that affects the overall cost of capital for the firm. Availability of debt in the financial

market plays a predominant role in the determination of cost of capital for the firm. The

cost of capital for the company can be well determined with the help of the equity as

well as debt financing for the company. The cost of equity for the firm could be well

determined with the help of the Capital Asset Pricing Model (Pwc.at 2019). The cost of

equity is primarily high as the equity financers bears the high amount of investment as

well as operational risk that is associated with the company. The cost of equity for the

company could be well generated with the help of a sample data that was collected

where a five-year trend data period for the FTSE 100 (Market Return), 10-Year

Government Bond Yield (Risk Free Rate of Return) and FTSE 350 Index Data was

taken for the purpose of analysis. The relevant beta for the purpose of analysis was

around 1.50 times that was taken for the purpose of analysis (Investing.com UK 2019).

The required rate of return for the equity shareholders was calculated as follows:

Capital Asset Pricing Model

Required Rate of Return on Equity (Re): Risk Free Rate of Return (Rf) +

Beta*(Return On Market Index - Risk Free Rate of Return)

Where;

Risk Free Rate of Return (Current 10-Year Bond Yield) 1.63%

Return on Market 5.55%

Beta (Assumption) 1.50

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7REAL ESTATE FUNDING AND FINANCE

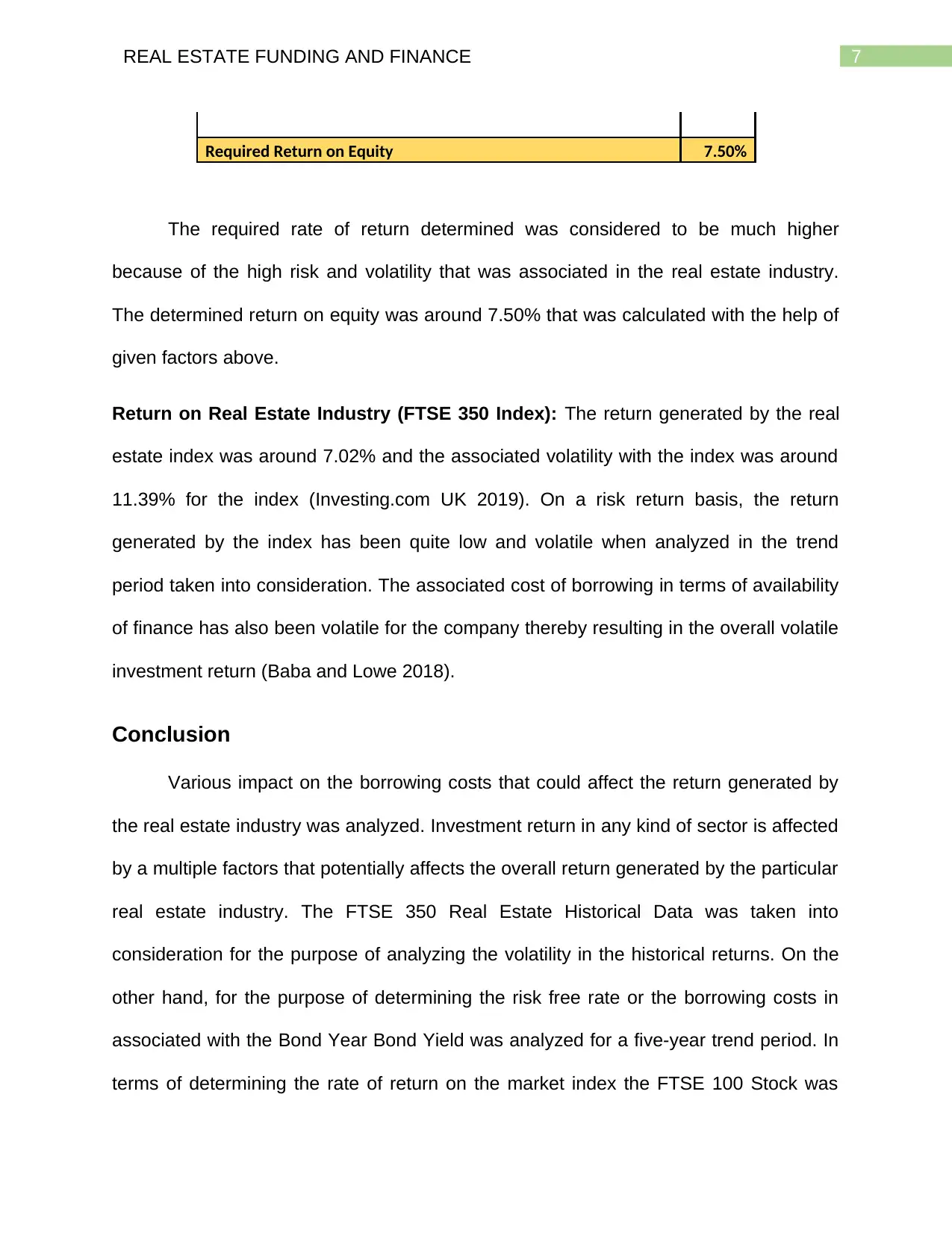

Required Return on Equity 7.50%

The required rate of return determined was considered to be much higher

because of the high risk and volatility that was associated in the real estate industry.

The determined return on equity was around 7.50% that was calculated with the help of

given factors above.

Return on Real Estate Industry (FTSE 350 Index): The return generated by the real

estate index was around 7.02% and the associated volatility with the index was around

11.39% for the index (Investing.com UK 2019). On a risk return basis, the return

generated by the index has been quite low and volatile when analyzed in the trend

period taken into consideration. The associated cost of borrowing in terms of availability

of finance has also been volatile for the company thereby resulting in the overall volatile

investment return (Baba and Lowe 2018).

Conclusion

Various impact on the borrowing costs that could affect the return generated by

the real estate industry was analyzed. Investment return in any kind of sector is affected

by a multiple factors that potentially affects the overall return generated by the particular

real estate industry. The FTSE 350 Real Estate Historical Data was taken into

consideration for the purpose of analyzing the volatility in the historical returns. On the

other hand, for the purpose of determining the risk free rate or the borrowing costs in

associated with the Bond Year Bond Yield was analyzed for a five-year trend period. In

terms of determining the rate of return on the market index the FTSE 100 Stock was

Required Return on Equity 7.50%

The required rate of return determined was considered to be much higher

because of the high risk and volatility that was associated in the real estate industry.

The determined return on equity was around 7.50% that was calculated with the help of

given factors above.

Return on Real Estate Industry (FTSE 350 Index): The return generated by the real

estate index was around 7.02% and the associated volatility with the index was around

11.39% for the index (Investing.com UK 2019). On a risk return basis, the return

generated by the index has been quite low and volatile when analyzed in the trend

period taken into consideration. The associated cost of borrowing in terms of availability

of finance has also been volatile for the company thereby resulting in the overall volatile

investment return (Baba and Lowe 2018).

Conclusion

Various impact on the borrowing costs that could affect the return generated by

the real estate industry was analyzed. Investment return in any kind of sector is affected

by a multiple factors that potentially affects the overall return generated by the particular

real estate industry. The FTSE 350 Real Estate Historical Data was taken into

consideration for the purpose of analyzing the volatility in the historical returns. On the

other hand, for the purpose of determining the risk free rate or the borrowing costs in

associated with the Bond Year Bond Yield was analyzed for a five-year trend period. In

terms of determining the rate of return on the market index the FTSE 100 Stock was

8REAL ESTATE FUNDING AND FINANCE

calculated and analyzed. The Capital Asset Pricing Model was then applied for the

purpose of determining the cost of equity for the company. Overall, it was found that the

investment returns in the real estate industry could be well analyzed and explained with

the help of changing capital structure and cost of financing for real estate companies.

calculated and analyzed. The Capital Asset Pricing Model was then applied for the

purpose of determining the cost of equity for the company. Overall, it was found that the

investment returns in the real estate industry could be well analyzed and explained with

the help of changing capital structure and cost of financing for real estate companies.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9REAL ESTATE FUNDING AND FINANCE

References

Andonov, A., Eichholtz, P. and Kok, N., 2015. Intermediated investment management in

private markets: Evidence from pension fund investments in real estate. Journal of

Financial Markets, 22, pp.73-103.

Baba, R. and Lowe, R. 2018. UK real estate outlook 2019: Brexit to test the market.

[online] IPE RA. Available at: https://realassets.ipe.com/news/uk-real-estate-outlook-

2019-brexit-to-test-the-market/realassets.ipe.com/news/uk-real-estate-outlook-2019-

brexit-to-test-the-market/10028464.fullarticle [Accessed 31 Jul. 2019].

Baum, A., 2015. Real estate investment: A strategic approach. Routledge.

Briere, M., Oosterlinck, K. and Szafarz, A., 2015. Virtual currency, tangible return:

Portfolio diversification with bitcoin. Journal of Asset Management, 16(6), pp.365-373.

Hoesli, M., Oikarinen, E. and Serrano, C., 2015. Do public real estate returns really lead

private returns?. The Journal of Portfolio Management, 41(6), pp.105-117.

Investing.com UK. 2019. FTSE 100 Historical Rates - Investing.com UK. [online]

Available at: https://uk.investing.com/indices/uk-100-historical-data [Accessed 31 Jul.

2019].

Investing.com UK. 2019. FTSE 350 Real Estate Chart - Investing.com UK. [online]

Available at: https://uk.investing.com/indices/ftse-supersector-real-estat-chart [Accessed

31 Jul. 2019].

References

Andonov, A., Eichholtz, P. and Kok, N., 2015. Intermediated investment management in

private markets: Evidence from pension fund investments in real estate. Journal of

Financial Markets, 22, pp.73-103.

Baba, R. and Lowe, R. 2018. UK real estate outlook 2019: Brexit to test the market.

[online] IPE RA. Available at: https://realassets.ipe.com/news/uk-real-estate-outlook-

2019-brexit-to-test-the-market/realassets.ipe.com/news/uk-real-estate-outlook-2019-

brexit-to-test-the-market/10028464.fullarticle [Accessed 31 Jul. 2019].

Baum, A., 2015. Real estate investment: A strategic approach. Routledge.

Briere, M., Oosterlinck, K. and Szafarz, A., 2015. Virtual currency, tangible return:

Portfolio diversification with bitcoin. Journal of Asset Management, 16(6), pp.365-373.

Hoesli, M., Oikarinen, E. and Serrano, C., 2015. Do public real estate returns really lead

private returns?. The Journal of Portfolio Management, 41(6), pp.105-117.

Investing.com UK. 2019. FTSE 100 Historical Rates - Investing.com UK. [online]

Available at: https://uk.investing.com/indices/uk-100-historical-data [Accessed 31 Jul.

2019].

Investing.com UK. 2019. FTSE 350 Real Estate Chart - Investing.com UK. [online]

Available at: https://uk.investing.com/indices/ftse-supersector-real-estat-chart [Accessed

31 Jul. 2019].

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10REAL ESTATE FUNDING AND FINANCE

Investing.com UK. 2019. United Kingdom 10-Year Bond Historical Data - Investing.com

UK. [online] Available at: https://uk.investing.com/rates-bonds/uk-10-year-bond-yield-

historical-data [Accessed 31 Jul. 2019].

Nazlioglu, S., Gormus, N.A. and Soytas, U., 2016. Oil prices and real estate investment

trusts (REITs): Gradual-shift causality and volatility transmission analysis. Energy

Economics, 60, pp.168-175.

Pwc.at. 2019. [online] Available at: https://www.pwc.at/de/publikationen/branchen-und-

wirtschaftsstudien/pwc-emerging-trends-in-real-estate-europe-2019.pdf [Accessed 31

Jul. 2019].

Salzman, D. and Zwinkels, R.C., 2017. Behavioral real estate. Journal of Real Estate

Literature, 25(1), pp.77-106.

van Loon, J. and Aalbers, M.B., 2017. How real estate became ‘just another asset

class’: The financialization of the investment strategies of Dutch institutional

investors. European Planning Studies, 25(2), pp.221-240.

Investing.com UK. 2019. United Kingdom 10-Year Bond Historical Data - Investing.com

UK. [online] Available at: https://uk.investing.com/rates-bonds/uk-10-year-bond-yield-

historical-data [Accessed 31 Jul. 2019].

Nazlioglu, S., Gormus, N.A. and Soytas, U., 2016. Oil prices and real estate investment

trusts (REITs): Gradual-shift causality and volatility transmission analysis. Energy

Economics, 60, pp.168-175.

Pwc.at. 2019. [online] Available at: https://www.pwc.at/de/publikationen/branchen-und-

wirtschaftsstudien/pwc-emerging-trends-in-real-estate-europe-2019.pdf [Accessed 31

Jul. 2019].

Salzman, D. and Zwinkels, R.C., 2017. Behavioral real estate. Journal of Real Estate

Literature, 25(1), pp.77-106.

van Loon, J. and Aalbers, M.B., 2017. How real estate became ‘just another asset

class’: The financialization of the investment strategies of Dutch institutional

investors. European Planning Studies, 25(2), pp.221-240.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.