SIT718 Real World Analytics: BP Share Price Analysis Report

VerifiedAdded on 2023/05/29

|8

|1236

|469

Report

AI Summary

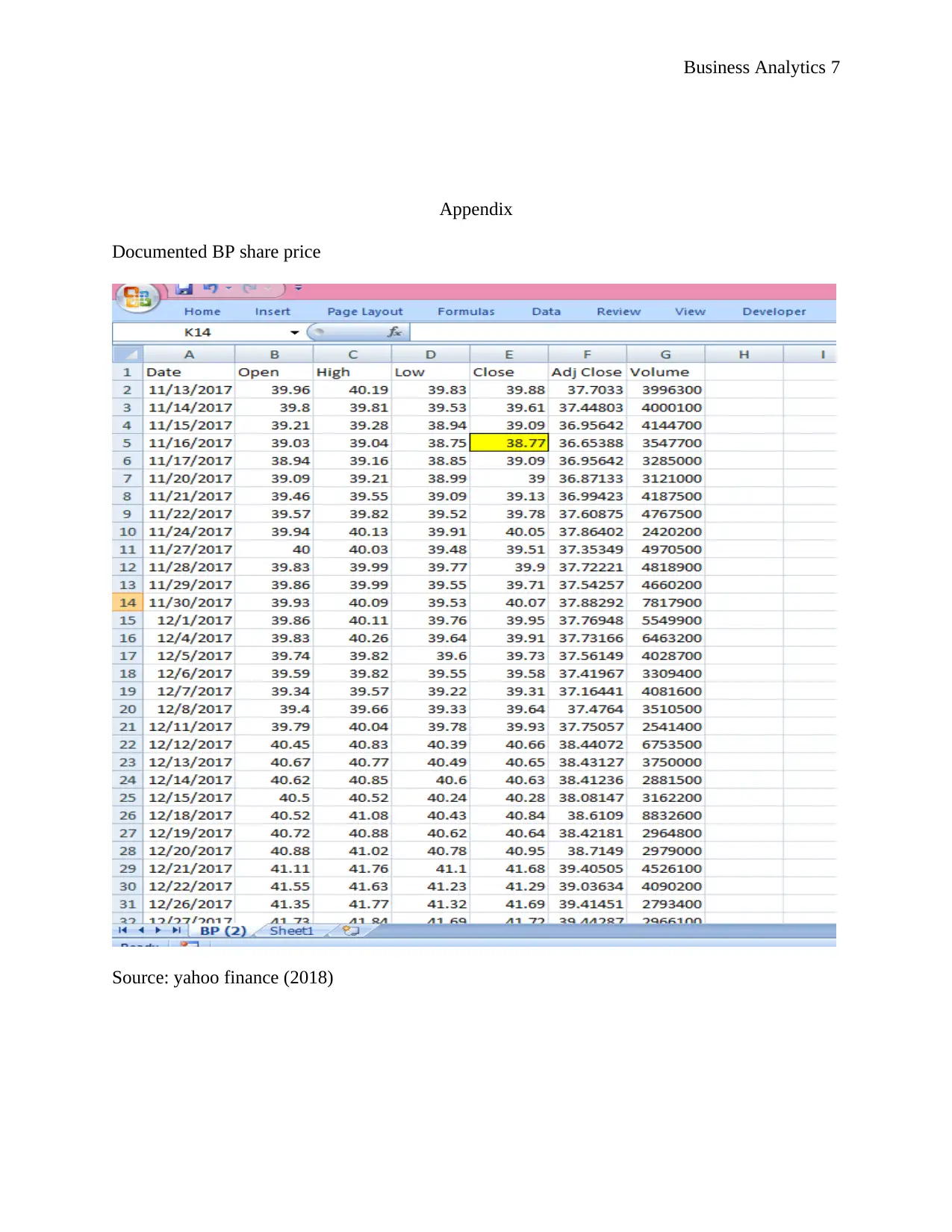

This report analyzes British Petroleum (BP) share prices using real-world data and the application of business analytics techniques. It begins by explaining key concepts like variance, drift, and the assumptions underlying stock price modeling. The report then presents a time series plot of BP's closing prices and details the use of geometric Brownian motion (GBM) to model share price behavior. Calculations of drift and volatility are presented, along with a comparison to documented volatility data. The report also simulates share prices using GBM and compares the results to published data, discussing the limitations of the model. The analysis includes references to relevant literature and appendices with data from Yahoo Finance. The report concludes that GBM can be used to predict future share prices with accuracy.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.