Accounting for Rebates, Financial Statements and Lease Standards

VerifiedAdded on 2023/06/18

|10

|1932

|445

Homework Assignment

AI Summary

This assignment provides solutions to several accounting questions. It includes journal entries for machinery depreciation, salvage value, and new purchases. It analyzes financial statements, including adjustments for inventories, accounts receivable, insurance, and provisions. The assignment also addresses the correct accounting treatment for rebates, discussing relevant accounting theories and the mechanistic hypothesis. Furthermore, it covers revenue recognition for contracts, lease accounting under AASB 117 and AASB 16, and the impact of these standards on financial statements. The assignment concludes with a discussion of bonus plan and debt covenant hypotheses in relation to accounting choices.

Questions

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

QUESTION 1..................................................................................................................................3

Question 2........................................................................................................................................3

Question 3........................................................................................................................................5

Question 4........................................................................................................................................5

1 Correct accounting treatment for rebate...................................................................................5

2 Accounting theory of Rebate....................................................................................................5

3 Mechanistic hypothesis.............................................................................................................6

Question 5........................................................................................................................................6

QUESTION 6..................................................................................................................................8

References......................................................................................................................................10

QUESTION 1..................................................................................................................................3

Question 2........................................................................................................................................3

Question 3........................................................................................................................................5

Question 4........................................................................................................................................5

1 Correct accounting treatment for rebate...................................................................................5

2 Accounting theory of Rebate....................................................................................................5

3 Mechanistic hypothesis.............................................................................................................6

Question 5........................................................................................................................................6

QUESTION 6..................................................................................................................................8

References......................................................................................................................................10

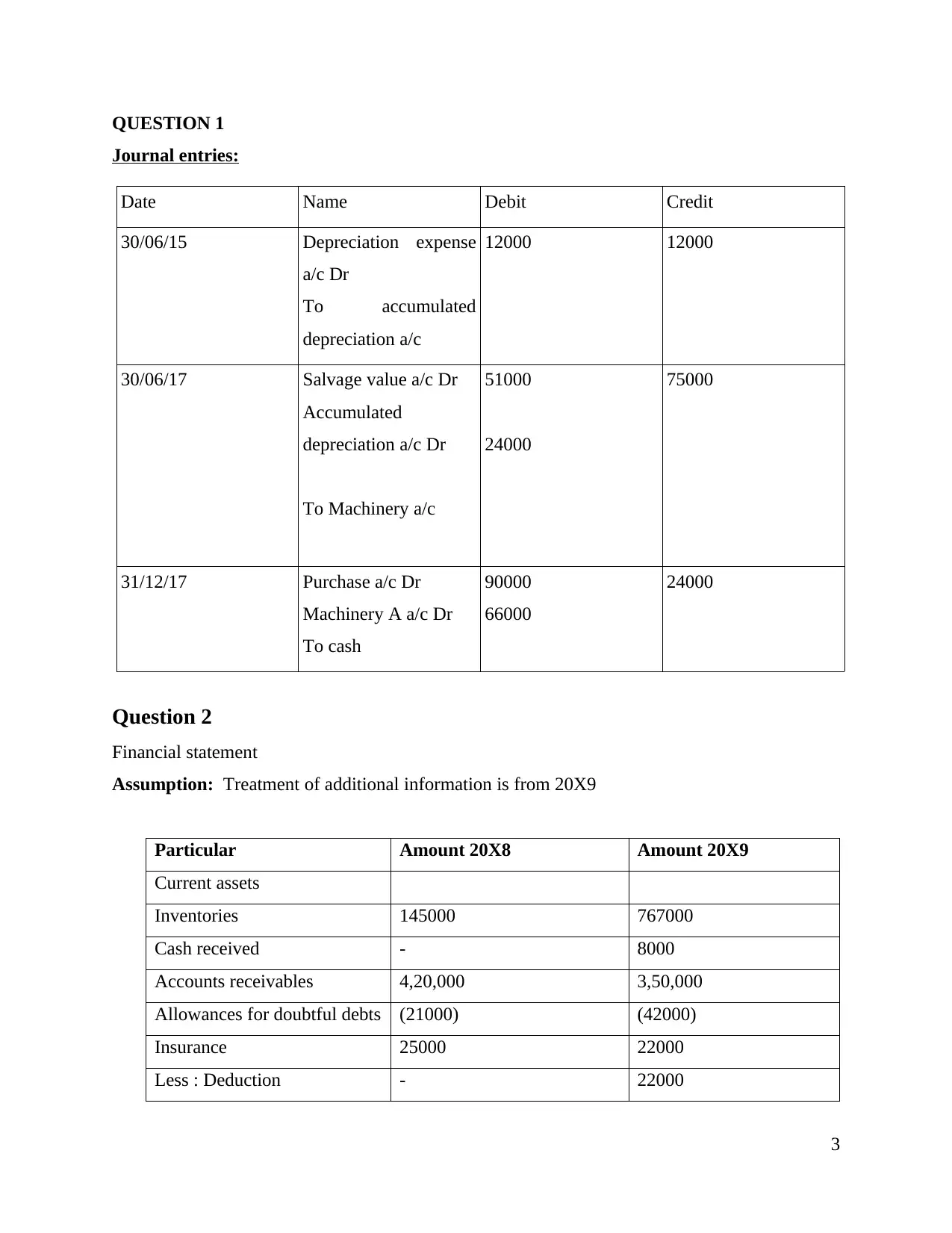

QUESTION 1

Journal entries:

Date Name Debit Credit

30/06/15 Depreciation expense

a/c Dr

To accumulated

depreciation a/c

12000 12000

30/06/17 Salvage value a/c Dr

Accumulated

depreciation a/c Dr

To Machinery a/c

51000

24000

75000

31/12/17 Purchase a/c Dr

Machinery A a/c Dr

To cash

90000

66000

24000

Question 2

Financial statement

Assumption: Treatment of additional information is from 20X9

Particular Amount 20X8 Amount 20X9

Current assets

Inventories 145000 767000

Cash received - 8000

Accounts receivables 4,20,000 3,50,000

Allowances for doubtful debts (21000) (42000)

Insurance 25000 22000

Less : Deduction - 22000

3

Journal entries:

Date Name Debit Credit

30/06/15 Depreciation expense

a/c Dr

To accumulated

depreciation a/c

12000 12000

30/06/17 Salvage value a/c Dr

Accumulated

depreciation a/c Dr

To Machinery a/c

51000

24000

75000

31/12/17 Purchase a/c Dr

Machinery A a/c Dr

To cash

90000

66000

24000

Question 2

Financial statement

Assumption: Treatment of additional information is from 20X9

Particular Amount 20X8 Amount 20X9

Current assets

Inventories 145000 767000

Cash received - 8000

Accounts receivables 4,20,000 3,50,000

Allowances for doubtful debts (21000) (42000)

Insurance 25000 22000

Less : Deduction - 22000

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Equipment 6,00,0000 6,00,0000

Accumulated depreciation (60,000) (120000)

(16107) (16107)

Intangible assets 1,80,000 1,20,000

Goodwill 152,0000 1,56,000

Liabilities

Services revenue received in

advanced

17,000 12500

Warranty payable 35000 1100000

Provision for long services

leave

28000 25000

Taxable profit for 20X9

Particular Amount

Income

Cash received 8000

Account receivable 3,50,0000

Expenses

Services revenue received in advanced 12500

Warranty payable 1,10,000

long services leave 25000

Profit before tax 2,10,5000

Less : Tax (73675)

Total income 136825

Journal entry

Entry Debit Credit

Remit tax payment 73675

To cash 73675

4

Accumulated depreciation (60,000) (120000)

(16107) (16107)

Intangible assets 1,80,000 1,20,000

Goodwill 152,0000 1,56,000

Liabilities

Services revenue received in

advanced

17,000 12500

Warranty payable 35000 1100000

Provision for long services

leave

28000 25000

Taxable profit for 20X9

Particular Amount

Income

Cash received 8000

Account receivable 3,50,0000

Expenses

Services revenue received in advanced 12500

Warranty payable 1,10,000

long services leave 25000

Profit before tax 2,10,5000

Less : Tax (73675)

Total income 136825

Journal entry

Entry Debit Credit

Remit tax payment 73675

To cash 73675

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

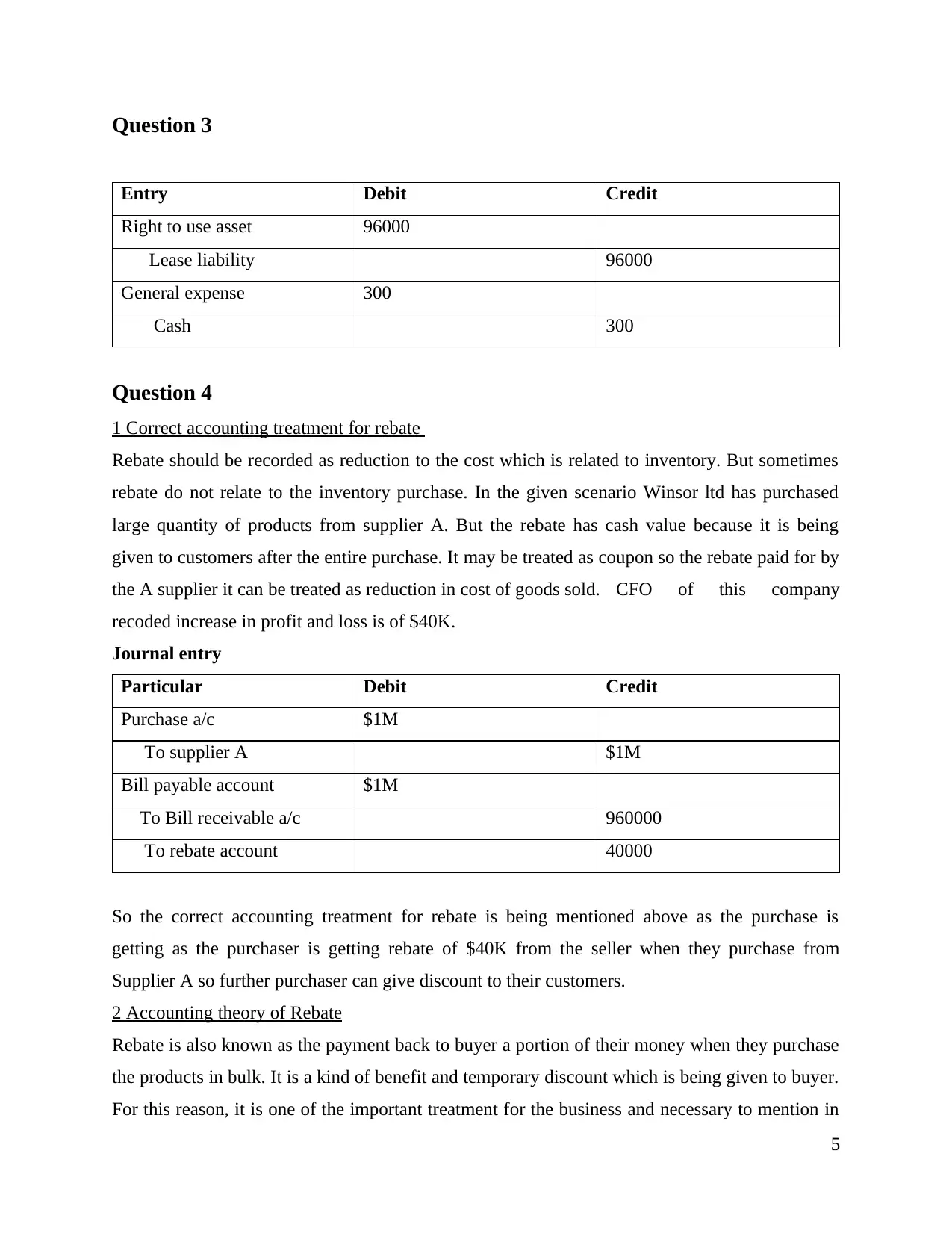

Question 3

Entry Debit Credit

Right to use asset 96000

Lease liability 96000

General expense 300

Cash 300

Question 4

1 Correct accounting treatment for rebate

Rebate should be recorded as reduction to the cost which is related to inventory. But sometimes

rebate do not relate to the inventory purchase. In the given scenario Winsor ltd has purchased

large quantity of products from supplier A. But the rebate has cash value because it is being

given to customers after the entire purchase. It may be treated as coupon so the rebate paid for by

the A supplier it can be treated as reduction in cost of goods sold. CFO of this company

recoded increase in profit and loss is of $40K.

Journal entry

Particular Debit Credit

Purchase a/c $1M

To supplier A $1M

Bill payable account $1M

To Bill receivable a/c 960000

To rebate account 40000

So the correct accounting treatment for rebate is being mentioned above as the purchase is

getting as the purchaser is getting rebate of $40K from the seller when they purchase from

Supplier A so further purchaser can give discount to their customers.

2 Accounting theory of Rebate

Rebate is also known as the payment back to buyer a portion of their money when they purchase

the products in bulk. It is a kind of benefit and temporary discount which is being given to buyer.

For this reason, it is one of the important treatment for the business and necessary to mention in

5

Entry Debit Credit

Right to use asset 96000

Lease liability 96000

General expense 300

Cash 300

Question 4

1 Correct accounting treatment for rebate

Rebate should be recorded as reduction to the cost which is related to inventory. But sometimes

rebate do not relate to the inventory purchase. In the given scenario Winsor ltd has purchased

large quantity of products from supplier A. But the rebate has cash value because it is being

given to customers after the entire purchase. It may be treated as coupon so the rebate paid for by

the A supplier it can be treated as reduction in cost of goods sold. CFO of this company

recoded increase in profit and loss is of $40K.

Journal entry

Particular Debit Credit

Purchase a/c $1M

To supplier A $1M

Bill payable account $1M

To Bill receivable a/c 960000

To rebate account 40000

So the correct accounting treatment for rebate is being mentioned above as the purchase is

getting as the purchaser is getting rebate of $40K from the seller when they purchase from

Supplier A so further purchaser can give discount to their customers.

2 Accounting theory of Rebate

Rebate is also known as the payment back to buyer a portion of their money when they purchase

the products in bulk. It is a kind of benefit and temporary discount which is being given to buyer.

For this reason, it is one of the important treatment for the business and necessary to mention in

5

the books of accounts (Sadeghi and et.al 2021). This is why, CFO of this company has recorded

this in their books. There are few rebate accounting theory is present which states that overall

treatment of rebate is very necessary so that the purchaser may enjoy the benefit of discounts.

Theory of rebate speaks about the various set of assumptions, frame work, and standards which

is being used to make the treatment of rebate. One of the common theory which is used for

rebate is financial accounting theory. This theory says that reporting of transaction is very

important whether it is the transaction of rebate or any other. For this reason, this theory is also

known as positive accounting theory as it shares all the accurate and correct answers.

3 Mechanistic hypothesis

As per the Mechanistic hypothesis, the share price of Winsor Ltd will rise in the market because

the company is doing bulk buying and also they are getting rebate (Rodemeier, 2021). So this

will directly be going to impact the share price and market share of the company. In near future

company will get benefit from this rebate and purchase. Due to the accounting performance of

the company in the fiscal year, company will get new investors as well.

This will further lead to have an impact over the P&L account in terms of making reduction of

profits and raising of loss. It would be right to said that with the implication of new standard of

lease the P&L will affect in terms of making rise in loss and balance sheet will affected in terms

of making changes in the value of assets and liabilities. Similarly, cash flow will also decrease

because lease will be treated as an asset and making it availed to other would lead to have an

impact over decrease in the value of asset in case if the business make any lease to other.

Likewise, the ratio of leverage and Return on Assets will also positively affected because lease

will be treated as an asset and it may positively impact them.

Question 5

1. Revenue to be recorded

Percentage of contract completed:

Labour 61000 (120000 – 59000)

Material 143000 (470000 – 10000 – 7000 310000)

Total completed contract cost 204000

Estimated cost of contract 800000

6

this in their books. There are few rebate accounting theory is present which states that overall

treatment of rebate is very necessary so that the purchaser may enjoy the benefit of discounts.

Theory of rebate speaks about the various set of assumptions, frame work, and standards which

is being used to make the treatment of rebate. One of the common theory which is used for

rebate is financial accounting theory. This theory says that reporting of transaction is very

important whether it is the transaction of rebate or any other. For this reason, this theory is also

known as positive accounting theory as it shares all the accurate and correct answers.

3 Mechanistic hypothesis

As per the Mechanistic hypothesis, the share price of Winsor Ltd will rise in the market because

the company is doing bulk buying and also they are getting rebate (Rodemeier, 2021). So this

will directly be going to impact the share price and market share of the company. In near future

company will get benefit from this rebate and purchase. Due to the accounting performance of

the company in the fiscal year, company will get new investors as well.

This will further lead to have an impact over the P&L account in terms of making reduction of

profits and raising of loss. It would be right to said that with the implication of new standard of

lease the P&L will affect in terms of making rise in loss and balance sheet will affected in terms

of making changes in the value of assets and liabilities. Similarly, cash flow will also decrease

because lease will be treated as an asset and making it availed to other would lead to have an

impact over decrease in the value of asset in case if the business make any lease to other.

Likewise, the ratio of leverage and Return on Assets will also positively affected because lease

will be treated as an asset and it may positively impact them.

Question 5

1. Revenue to be recorded

Percentage of contract completed:

Labour 61000 (120000 – 59000)

Material 143000 (470000 – 10000 – 7000 310000)

Total completed contract cost 204000

Estimated cost of contract 800000

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Percentage of contract completed 204000 / 800000 * 100

= 25.5%

Revenue recognised:

1000000 * 25.5%

= 255000

2. Journal Entry

Cleland Ltd a/c Dr. 255000

To Sales 255000

(Sales being made to Cleland Ltd.)

Bank a/c Dr. 400000

To Clenland Ltd 255000

To advance payment 145000

(Being payment made against the contract output of which only

255000 worth of contract part is completed that will be

recognised as a revenue the rest of the payment will remain

advance till the time contract do not get completed of the

respective part)

3. The material loss will not be capitalised rather it will be treated against the profit for the

respective financial year. This is an abnormal loss which is not capitalised rather treated

as an expense for the respective financial year. There is not any policy specified about the

percentage of material wastage treated as an idle loss so the entire loss would be treated

as abnormal and will treat against the profitability of the respective time.

7

= 25.5%

Revenue recognised:

1000000 * 25.5%

= 255000

2. Journal Entry

Cleland Ltd a/c Dr. 255000

To Sales 255000

(Sales being made to Cleland Ltd.)

Bank a/c Dr. 400000

To Clenland Ltd 255000

To advance payment 145000

(Being payment made against the contract output of which only

255000 worth of contract part is completed that will be

recognised as a revenue the rest of the payment will remain

advance till the time contract do not get completed of the

respective part)

3. The material loss will not be capitalised rather it will be treated against the profit for the

respective financial year. This is an abnormal loss which is not capitalised rather treated

as an expense for the respective financial year. There is not any policy specified about the

percentage of material wastage treated as an idle loss so the entire loss would be treated

as abnormal and will treat against the profitability of the respective time.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

QUESTION 6

A)

As per the lease AASB 117 a lease will be classified and determined as financial lease if

there is a transfer of risk and rewards along with the ownership of the asset. Also finance lease

need to be shown on the asset side of the balance sheet against the liability (Guidance for AASB

16 Leases, 2020).

While AASB 116 make removal of all the distinction between operating and finance lease. It

also raise the recognition of right to use assets and lease liability on balance sheet.

This agreement also make focus towards the aspect that whether there is any existence of

any right that is related with the use or control of asset. This proves to be beneficial with respect

to make identification that whether there is a lease or contract or service or both. However, this

was not made available in case of ASSB 117.

In addition, of this another major difference is the treatment of lease in balance sheet. As in

ASSB 117 the lease asset is shown in balance sheet and treated as an assets with the

charging of depreciation. However, it will be different in case of ASSB 116 which says that all

leases will be treated under single account of lease in balance sheet and treated as finance lease

as per ASSB 117 but with certain exception. This includes making payment of low value assets

or lease within a period of 12 months.

B)

AASB 16 is having a direct and major impact over the firm's financial statements

including profit and loss account along with balance sheet. As per new lease standard all lease

need to be shown in the balance sheet which will lead to raise the value of assets and liabilities.

This will also lead to have a rise in gearing as well as debt measures (New Australian accounting

pronouncements, 2020). This means that it will raise the debt level of the company. With an

increase in debts and gearing the amount of expenses in terms of interest and other expenses also

raise. Likewise, being presence in balance sheet and making treatment as an asset would also

lead to have a raise in the amount of depreciation. This will further lead to have an impact over

the P&L account in terms of making reduction of profits and raising of loss. It would be right to

said that with the implication of new standard of lease the P&L will affect in terms of making

8

A)

As per the lease AASB 117 a lease will be classified and determined as financial lease if

there is a transfer of risk and rewards along with the ownership of the asset. Also finance lease

need to be shown on the asset side of the balance sheet against the liability (Guidance for AASB

16 Leases, 2020).

While AASB 116 make removal of all the distinction between operating and finance lease. It

also raise the recognition of right to use assets and lease liability on balance sheet.

This agreement also make focus towards the aspect that whether there is any existence of

any right that is related with the use or control of asset. This proves to be beneficial with respect

to make identification that whether there is a lease or contract or service or both. However, this

was not made available in case of ASSB 117.

In addition, of this another major difference is the treatment of lease in balance sheet. As in

ASSB 117 the lease asset is shown in balance sheet and treated as an assets with the

charging of depreciation. However, it will be different in case of ASSB 116 which says that all

leases will be treated under single account of lease in balance sheet and treated as finance lease

as per ASSB 117 but with certain exception. This includes making payment of low value assets

or lease within a period of 12 months.

B)

AASB 16 is having a direct and major impact over the firm's financial statements

including profit and loss account along with balance sheet. As per new lease standard all lease

need to be shown in the balance sheet which will lead to raise the value of assets and liabilities.

This will also lead to have a rise in gearing as well as debt measures (New Australian accounting

pronouncements, 2020). This means that it will raise the debt level of the company. With an

increase in debts and gearing the amount of expenses in terms of interest and other expenses also

raise. Likewise, being presence in balance sheet and making treatment as an asset would also

lead to have a raise in the amount of depreciation. This will further lead to have an impact over

the P&L account in terms of making reduction of profits and raising of loss. It would be right to

said that with the implication of new standard of lease the P&L will affect in terms of making

8

rise in loss and balance sheet will affected in terms of making changes in the value of assets and

liabilities. Similarly cash flow will also decrease because lease will be treated as an asset and

making it availed to other would lead to have an impact over decrease in the value of asset in

case if the business make any lease to other. Likewise, the ratio of leverage and Return on Assets

will also positively affected because lease will be treated as an asset and it may positively impact

them.

C)

As per bonus plan hypothesis, managers of the firm want to choose accounting

procedures that enable them to make shift in reported earning from future to current period. This

will lead to have a raise in the percentage of their bonus.

However, debt convent hypothesis states that closure of the firm is having a relation with

the compromising of debt covenants. They are also more likely to make use of accounting

policies which will lead to a shift in the future earning to present.

With regard to the above hypothesis managers will definitely like the AASB 116 because

it enables the long term lease to be present on the balance sheet which will further assist the

managers to make earning which is the priority choice of managers. Likewise, as the AASB 116

make early repayment of short term lease which will further lead to assist the managers in raising

their earning and income.

9

liabilities. Similarly cash flow will also decrease because lease will be treated as an asset and

making it availed to other would lead to have an impact over decrease in the value of asset in

case if the business make any lease to other. Likewise, the ratio of leverage and Return on Assets

will also positively affected because lease will be treated as an asset and it may positively impact

them.

C)

As per bonus plan hypothesis, managers of the firm want to choose accounting

procedures that enable them to make shift in reported earning from future to current period. This

will lead to have a raise in the percentage of their bonus.

However, debt convent hypothesis states that closure of the firm is having a relation with

the compromising of debt covenants. They are also more likely to make use of accounting

policies which will lead to a shift in the future earning to present.

With regard to the above hypothesis managers will definitely like the AASB 116 because

it enables the long term lease to be present on the balance sheet which will further assist the

managers to make earning which is the priority choice of managers. Likewise, as the AASB 116

make early repayment of short term lease which will further lead to assist the managers in raising

their earning and income.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

References

Books and journal

Rodemeier, M., 2021. Buy baits and consumer sophistication: Theory and field evidence from

large-scale rebate promotions (No. 124). CAWM Discussion Paper.

Sadeghi, F. and Hemmati, M., 2021. Rebate Contracts. In Influencing Customer Demand (pp.

59-76). CRC Press.

Online references

Guidance for AASB 16 Leases., 2020. [Online]. Available through

<https://www.treasury.nsw.gov.au/sites/default/files/2017-04/Guidance%20for

%20AASB%2016%20Leases%20-%20New%20Lease%20Standards.pdf>

New Australian accounting pronouncements., 2020. [Online]. Available through

<https://assets.ey.com/content/dam/ey-sites/ey-com/en_au/pdfs/ey-new-au-aactg-

pronouncements-30-april-2020.pdf>

10

Books and journal

Rodemeier, M., 2021. Buy baits and consumer sophistication: Theory and field evidence from

large-scale rebate promotions (No. 124). CAWM Discussion Paper.

Sadeghi, F. and Hemmati, M., 2021. Rebate Contracts. In Influencing Customer Demand (pp.

59-76). CRC Press.

Online references

Guidance for AASB 16 Leases., 2020. [Online]. Available through

<https://www.treasury.nsw.gov.au/sites/default/files/2017-04/Guidance%20for

%20AASB%2016%20Leases%20-%20New%20Lease%20Standards.pdf>

New Australian accounting pronouncements., 2020. [Online]. Available through

<https://assets.ey.com/content/dam/ey-sites/ey-com/en_au/pdfs/ey-new-au-aactg-

pronouncements-30-april-2020.pdf>

10

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.