Analysis of Measurement and Recognition of Asset Impairment in Finance

VerifiedAdded on 2020/05/28

|7

|1645

|44

Report

AI Summary

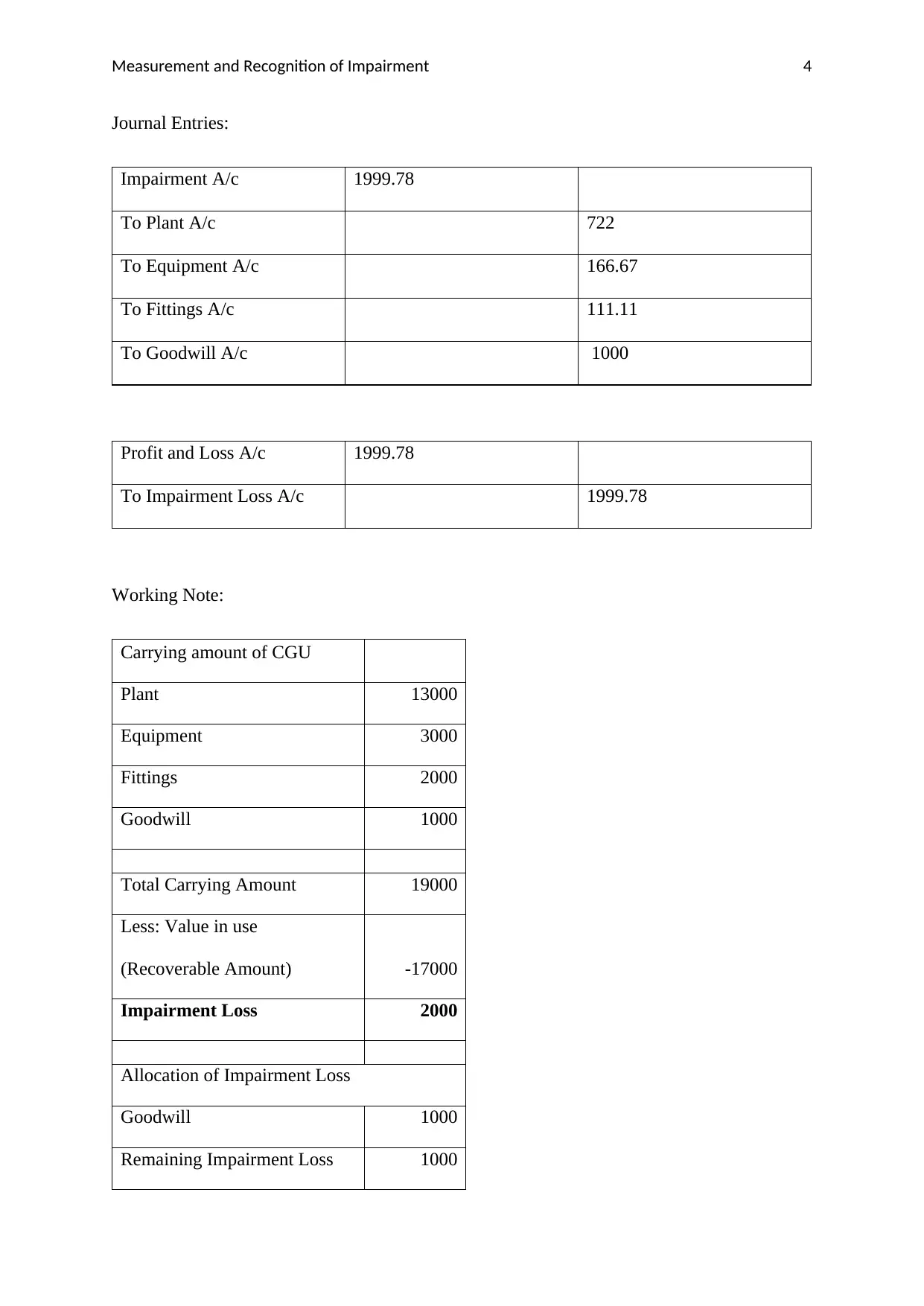

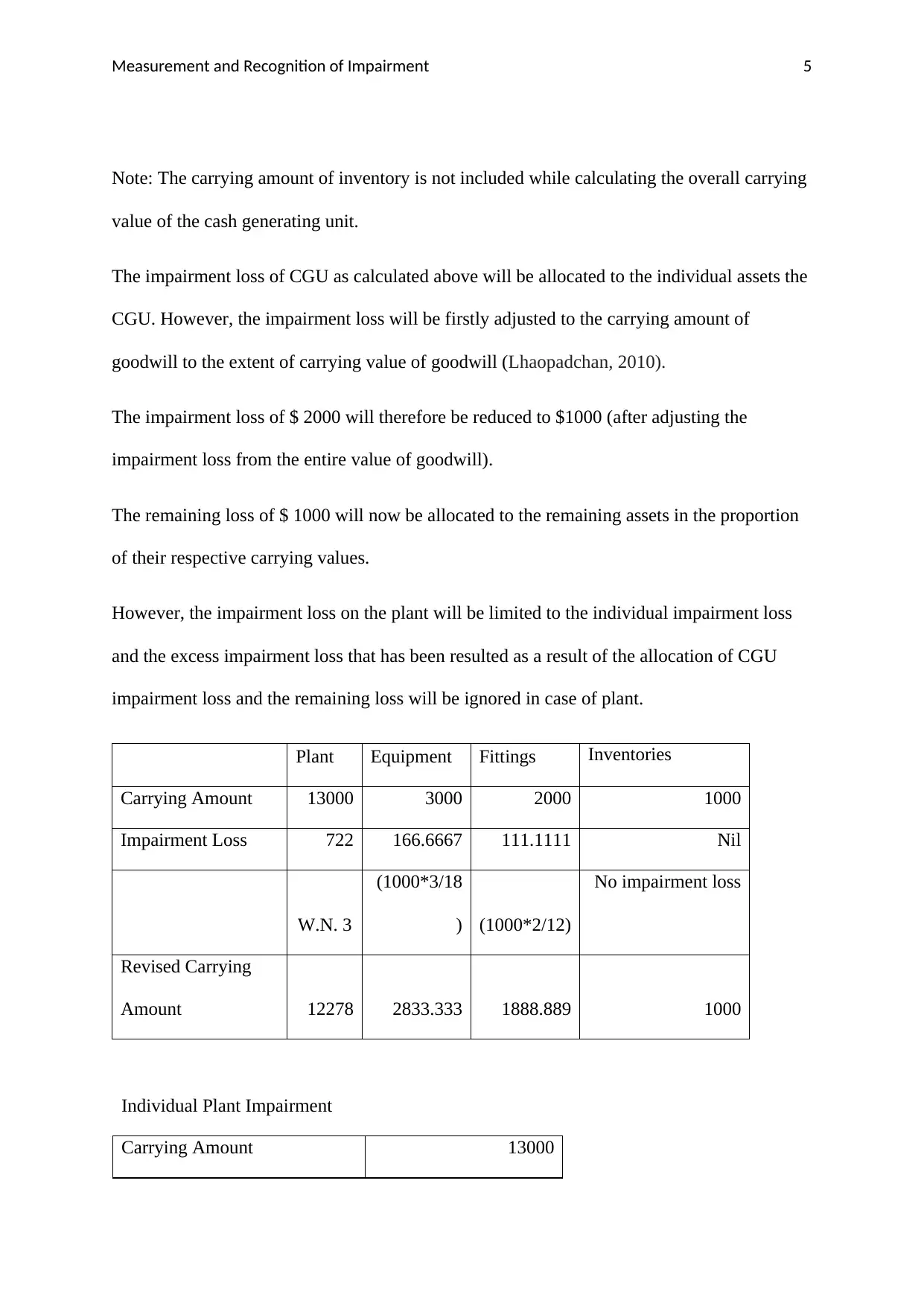

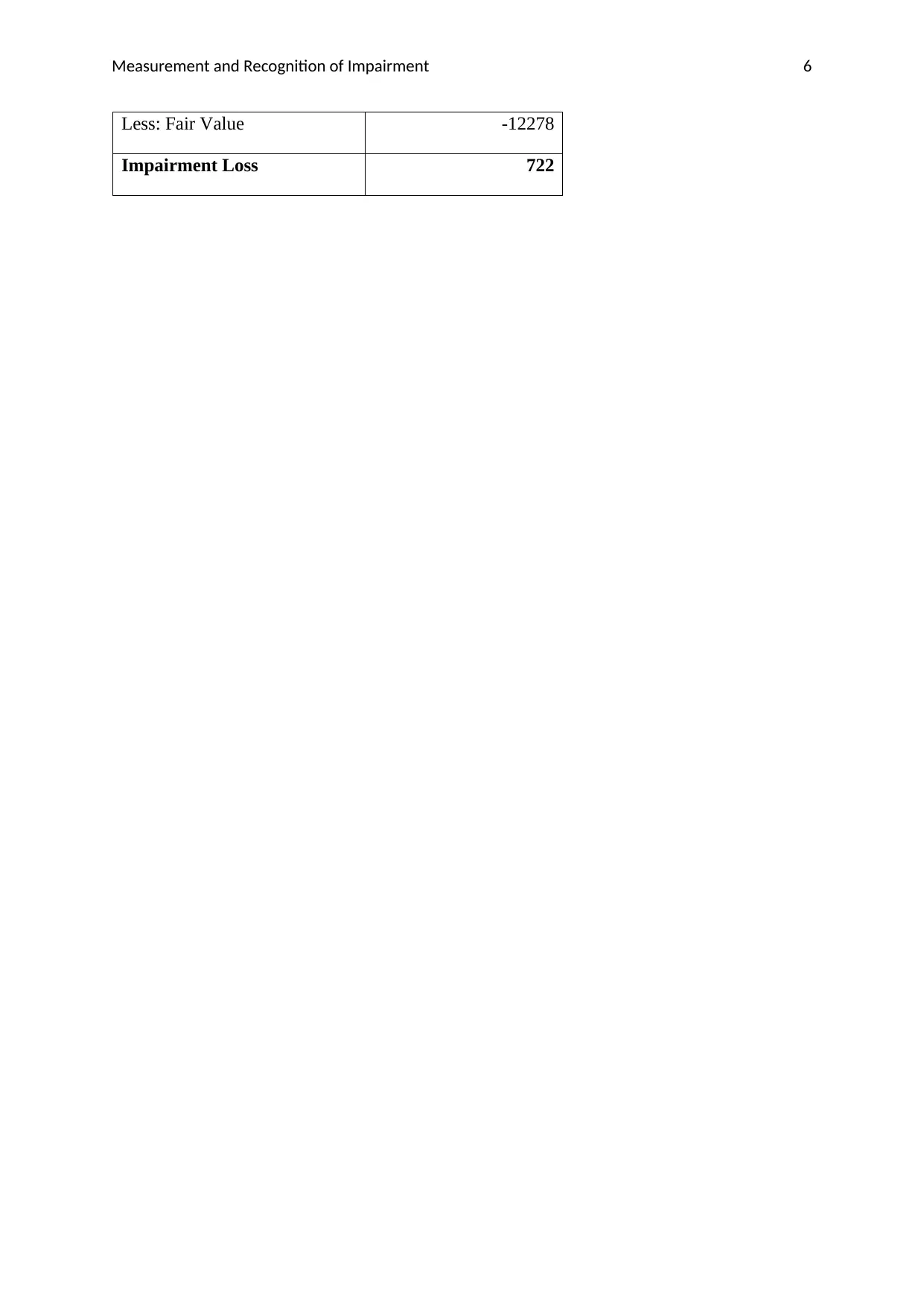

This report delves into the critical aspects of asset impairment, a crucial concept in financial accounting. It meticulously examines the process of assessing and recognizing asset impairment, focusing on the determination of recoverable amounts and carrying amounts. The report outlines the conditions that trigger impairment assessments, including both external and internal indicators, and details the calculation of impairment losses. It explains the allocation of impairment losses, particularly concerning goodwill and other assets within a cash-generating unit (CGU), and provides illustrative journal entries to demonstrate the accounting treatment. The report also covers the reversal of impairment losses, emphasizing the limitations and conditions associated with such reversals. Furthermore, the report highlights the importance of asset impairment in reflecting the true economic value of assets and its impact on financial statements. The report includes references to relevant accounting standards and provides a comprehensive understanding of asset impairment accounting.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.