University of West London: Recording Business Transactions Project A1

VerifiedAdded on 2023/01/03

|14

|2693

|58

Homework Assignment

AI Summary

This document provides a comprehensive solution to a recording business transactions project. It begins by identifying key decision-makers in accounting and their information needs, focusing on a large, publicly listed company. It then analyzes the advantages and disadvantages of different for-profit business structures from an accountant's perspective. The solution proceeds with detailed journal entries for David Wise's business, followed by the preparation of ledger accounts and a trial balance for Pearce & Son's business. Finally, it presents an income statement for Airman Company and discusses the potential impact of COVID-19 on the company's profitability. The assignment covers various aspects of financial accounting, including transaction recording, financial statement preparation, and financial analysis.

RECORDING BUSINESS

TRANSACTION PROJECT

A1

TRANSACTION PROJECT

A1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

MAIN BODY...................................................................................................................................3

PART 1............................................................................................................................................3

a) Major decision makers of accounting and need of financial information...............................3

b) Advantages and Disadvantages of Recording Financial information are enumerated below 4

PART B............................................................................................................................................6

Journal Entries of David wise Business:.....................................................................................6

PART 3............................................................................................................................................7

a) Preparing Ledger accounts of Pearce & son's business:.....................................................7

b) Trial Balance as at 28 February 2020...................................................................................11

PART 4..........................................................................................................................................12

a) Income Statements of Airman Company for the year ended 30 September 2020................12

b) Possible impact of coved 19 on Airman Company's income statement of profitability

during 10 years since 2009........................................................................................................13

REFERENCES..............................................................................................................................14

MAIN BODY...................................................................................................................................3

PART 1............................................................................................................................................3

a) Major decision makers of accounting and need of financial information...............................3

b) Advantages and Disadvantages of Recording Financial information are enumerated below 4

PART B............................................................................................................................................6

Journal Entries of David wise Business:.....................................................................................6

PART 3............................................................................................................................................7

a) Preparing Ledger accounts of Pearce & son's business:.....................................................7

b) Trial Balance as at 28 February 2020...................................................................................11

PART 4..........................................................................................................................................12

a) Income Statements of Airman Company for the year ended 30 September 2020................12

b) Possible impact of coved 19 on Airman Company's income statement of profitability

during 10 years since 2009........................................................................................................13

REFERENCES..............................................................................................................................14

MAIN BODY

PART 1

Accounting is process of recording, summarizing, and analysing all business transaction.

It provides concise summary of financial transaction over a period of time. It helps organizations

to take decision based on this information

a) Major decision makers of accounting and need of financial information

There are 3 types of users of financial information whose objective is to study the data

widely and taking decision based on these figures.

Internal Users:

Accounting provides financial information to managers that is useful for them in

decisions regarding management of company, Asda store Ltd uses these figures to manage their

internal structure of firm in various forms like assessing how management has discharge its

responsibility for protecting and managing organization's resources. They also use this

information for shaping decision regarding expansion and downsizing and when to borrow or

invest company’s resources (Garbowski and et.al., 2019.). Internal users like managers, owners,

officers, internal auditors, directors and employees. All these users are interested in the

accounting information as they come to know about the profitability of the company and with

help of this they can take major decisions relating to increasing the profitability and effective

management of the company.

External Users:

External entities use these accounting information for many purposes. These users are

divided into six categories. Creditors and investors are the most common external users among

other external users.

Creditors and lenders: loan providing banks and companies use these financial data to

determine that the company has credit worthiness or not, the company will be able to pay

back or will declared bankrupt.

Employees and their unions: Does The Organization like Asda Store Ltd has the ability

to provide long term employment to its workforce also the organization can increase the

pay scale of employees or not.

PART 1

Accounting is process of recording, summarizing, and analysing all business transaction.

It provides concise summary of financial transaction over a period of time. It helps organizations

to take decision based on this information

a) Major decision makers of accounting and need of financial information

There are 3 types of users of financial information whose objective is to study the data

widely and taking decision based on these figures.

Internal Users:

Accounting provides financial information to managers that is useful for them in

decisions regarding management of company, Asda store Ltd uses these figures to manage their

internal structure of firm in various forms like assessing how management has discharge its

responsibility for protecting and managing organization's resources. They also use this

information for shaping decision regarding expansion and downsizing and when to borrow or

invest company’s resources (Garbowski and et.al., 2019.). Internal users like managers, owners,

officers, internal auditors, directors and employees. All these users are interested in the

accounting information as they come to know about the profitability of the company and with

help of this they can take major decisions relating to increasing the profitability and effective

management of the company.

External Users:

External entities use these accounting information for many purposes. These users are

divided into six categories. Creditors and investors are the most common external users among

other external users.

Creditors and lenders: loan providing banks and companies use these financial data to

determine that the company has credit worthiness or not, the company will be able to pay

back or will declared bankrupt.

Employees and their unions: Does The Organization like Asda Store Ltd has the ability

to provide long term employment to its workforce also the organization can increase the

pay scale of employees or not.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Customers: consumer also keep eye on company's information to check that the firm

will survive enough to honour its warranty policies and are they providing good quality

products at fair prices.

Trading Partner: business needs business to do business, associated trading a company

look at the information to identify that they should do particular economic activity or not.

Government Unit: government uses company's financial data to protect interest of

stakeholders and shareholders (McCallig, Robb and Rohde, 2019). So that firm can have

fear of rules and regulation of Govt. and practice fair activities only. General Public: Public also use this information for decision- making that organization

is providing good products without harming environment.

Government/ IRS:

Govt. agencies that uses and track the tax are interested in company's financial

information. They check that the firm is paying taxes according to current tax law or not.

Government uses these data to decide the tax and these charges decide organization's

profitability.

These are various needs of financial information of company for decision makers of Asda

store Ltd.

b) Advantages and Disadvantages of Recording Financial information are enumerated below

Financial accounting is the process of recording all business transaction in form of

financial statements (Roberts, 2020.). It aims at delivering fair and accurate data to stakeholders

so proper decision can be taken and transparency can be maintained.

Advantages:

Maintain Business Records: it records each and every monetary transaction of business

unlike human memory which has limited capacity to remember things financial

accounting can record large amount of transaction.

Prevention and Detection of Fraud: It represents each and every transaction so true

picture of business can be revealed and it also provides time to time information to

internal management so real idea of resources can get through these data.

Acts as legal Evidence: Financial accounting serves as legal evidence that can be used to

overcome business disputes (Muslichah and et.al., 2020.). Misunderstanding and

confusion can be avoided through these financial legal statements.

will survive enough to honour its warranty policies and are they providing good quality

products at fair prices.

Trading Partner: business needs business to do business, associated trading a company

look at the information to identify that they should do particular economic activity or not.

Government Unit: government uses company's financial data to protect interest of

stakeholders and shareholders (McCallig, Robb and Rohde, 2019). So that firm can have

fear of rules and regulation of Govt. and practice fair activities only. General Public: Public also use this information for decision- making that organization

is providing good products without harming environment.

Government/ IRS:

Govt. agencies that uses and track the tax are interested in company's financial

information. They check that the firm is paying taxes according to current tax law or not.

Government uses these data to decide the tax and these charges decide organization's

profitability.

These are various needs of financial information of company for decision makers of Asda

store Ltd.

b) Advantages and Disadvantages of Recording Financial information are enumerated below

Financial accounting is the process of recording all business transaction in form of

financial statements (Roberts, 2020.). It aims at delivering fair and accurate data to stakeholders

so proper decision can be taken and transparency can be maintained.

Advantages:

Maintain Business Records: it records each and every monetary transaction of business

unlike human memory which has limited capacity to remember things financial

accounting can record large amount of transaction.

Prevention and Detection of Fraud: It represents each and every transaction so true

picture of business can be revealed and it also provides time to time information to

internal management so real idea of resources can get through these data.

Acts as legal Evidence: Financial accounting serves as legal evidence that can be used to

overcome business disputes (Muslichah and et.al., 2020.). Misunderstanding and

confusion can be avoided through these financial legal statements.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

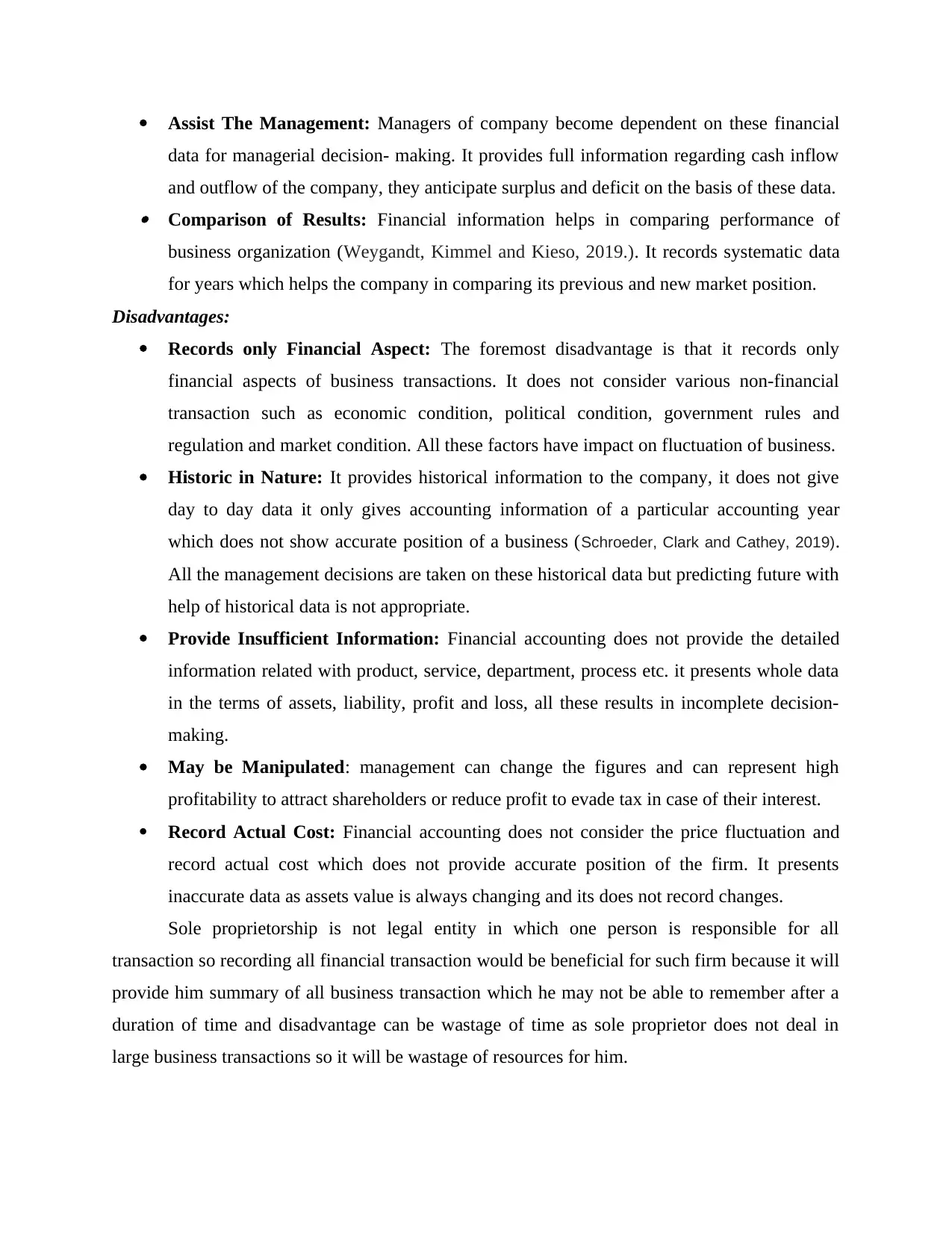

Assist The Management: Managers of company become dependent on these financial

data for managerial decision- making. It provides full information regarding cash inflow

and outflow of the company, they anticipate surplus and deficit on the basis of these data. Comparison of Results: Financial information helps in comparing performance of

business organization (Weygandt, Kimmel and Kieso, 2019.). It records systematic data

for years which helps the company in comparing its previous and new market position.

Disadvantages:

Records only Financial Aspect: The foremost disadvantage is that it records only

financial aspects of business transactions. It does not consider various non-financial

transaction such as economic condition, political condition, government rules and

regulation and market condition. All these factors have impact on fluctuation of business.

Historic in Nature: It provides historical information to the company, it does not give

day to day data it only gives accounting information of a particular accounting year

which does not show accurate position of a business (Schroeder, Clark and Cathey, 2019).

All the management decisions are taken on these historical data but predicting future with

help of historical data is not appropriate.

Provide Insufficient Information: Financial accounting does not provide the detailed

information related with product, service, department, process etc. it presents whole data

in the terms of assets, liability, profit and loss, all these results in incomplete decision-

making.

May be Manipulated: management can change the figures and can represent high

profitability to attract shareholders or reduce profit to evade tax in case of their interest.

Record Actual Cost: Financial accounting does not consider the price fluctuation and

record actual cost which does not provide accurate position of the firm. It presents

inaccurate data as assets value is always changing and its does not record changes.

Sole proprietorship is not legal entity in which one person is responsible for all

transaction so recording all financial transaction would be beneficial for such firm because it will

provide him summary of all business transaction which he may not be able to remember after a

duration of time and disadvantage can be wastage of time as sole proprietor does not deal in

large business transactions so it will be wastage of resources for him.

data for managerial decision- making. It provides full information regarding cash inflow

and outflow of the company, they anticipate surplus and deficit on the basis of these data. Comparison of Results: Financial information helps in comparing performance of

business organization (Weygandt, Kimmel and Kieso, 2019.). It records systematic data

for years which helps the company in comparing its previous and new market position.

Disadvantages:

Records only Financial Aspect: The foremost disadvantage is that it records only

financial aspects of business transactions. It does not consider various non-financial

transaction such as economic condition, political condition, government rules and

regulation and market condition. All these factors have impact on fluctuation of business.

Historic in Nature: It provides historical information to the company, it does not give

day to day data it only gives accounting information of a particular accounting year

which does not show accurate position of a business (Schroeder, Clark and Cathey, 2019).

All the management decisions are taken on these historical data but predicting future with

help of historical data is not appropriate.

Provide Insufficient Information: Financial accounting does not provide the detailed

information related with product, service, department, process etc. it presents whole data

in the terms of assets, liability, profit and loss, all these results in incomplete decision-

making.

May be Manipulated: management can change the figures and can represent high

profitability to attract shareholders or reduce profit to evade tax in case of their interest.

Record Actual Cost: Financial accounting does not consider the price fluctuation and

record actual cost which does not provide accurate position of the firm. It presents

inaccurate data as assets value is always changing and its does not record changes.

Sole proprietorship is not legal entity in which one person is responsible for all

transaction so recording all financial transaction would be beneficial for such firm because it will

provide him summary of all business transaction which he may not be able to remember after a

duration of time and disadvantage can be wastage of time as sole proprietor does not deal in

large business transactions so it will be wastage of resources for him.

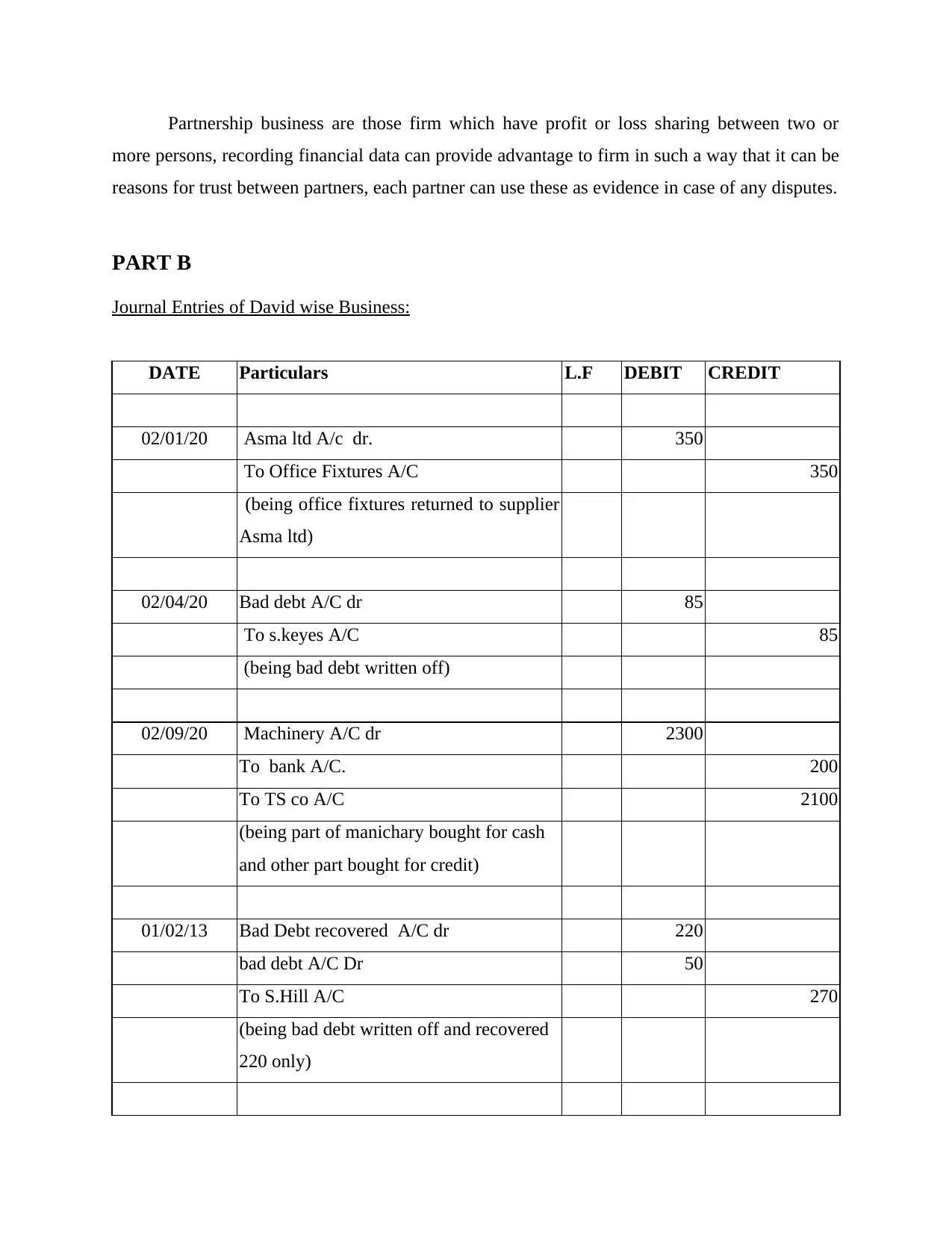

Partnership business are those firm which have profit or loss sharing between two or

more persons, recording financial data can provide advantage to firm in such a way that it can be

reasons for trust between partners, each partner can use these as evidence in case of any disputes.

PART B

Journal Entries of David wise Business:

DATE Particulars L.F DEBIT CREDIT

02/01/20 Asma ltd A/c dr. 350

To Office Fixtures A/C 350

(being office fixtures returned to supplier

Asma ltd)

02/04/20 Bad debt A/C dr 85

To s.keyes A/C 85

(being bad debt written off)

02/09/20 Machinery A/C dr 2300

To bank A/C. 200

To TS co A/C 2100

(being part of manichary bought for cash

and other part bought for credit)

01/02/13 Bad Debt recovered A/C dr 220

bad debt A/C Dr 50

To S.Hill A/C 270

(being bad debt written off and recovered

220 only)

more persons, recording financial data can provide advantage to firm in such a way that it can be

reasons for trust between partners, each partner can use these as evidence in case of any disputes.

PART B

Journal Entries of David wise Business:

DATE Particulars L.F DEBIT CREDIT

02/01/20 Asma ltd A/c dr. 350

To Office Fixtures A/C 350

(being office fixtures returned to supplier

Asma ltd)

02/04/20 Bad debt A/C dr 85

To s.keyes A/C 85

(being bad debt written off)

02/09/20 Machinery A/C dr 2300

To bank A/C. 200

To TS co A/C 2100

(being part of manichary bought for cash

and other part bought for credit)

01/02/13 Bad Debt recovered A/C dr 220

bad debt A/C Dr 50

To S.Hill A/C 270

(being bad debt written off and recovered

220 only)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

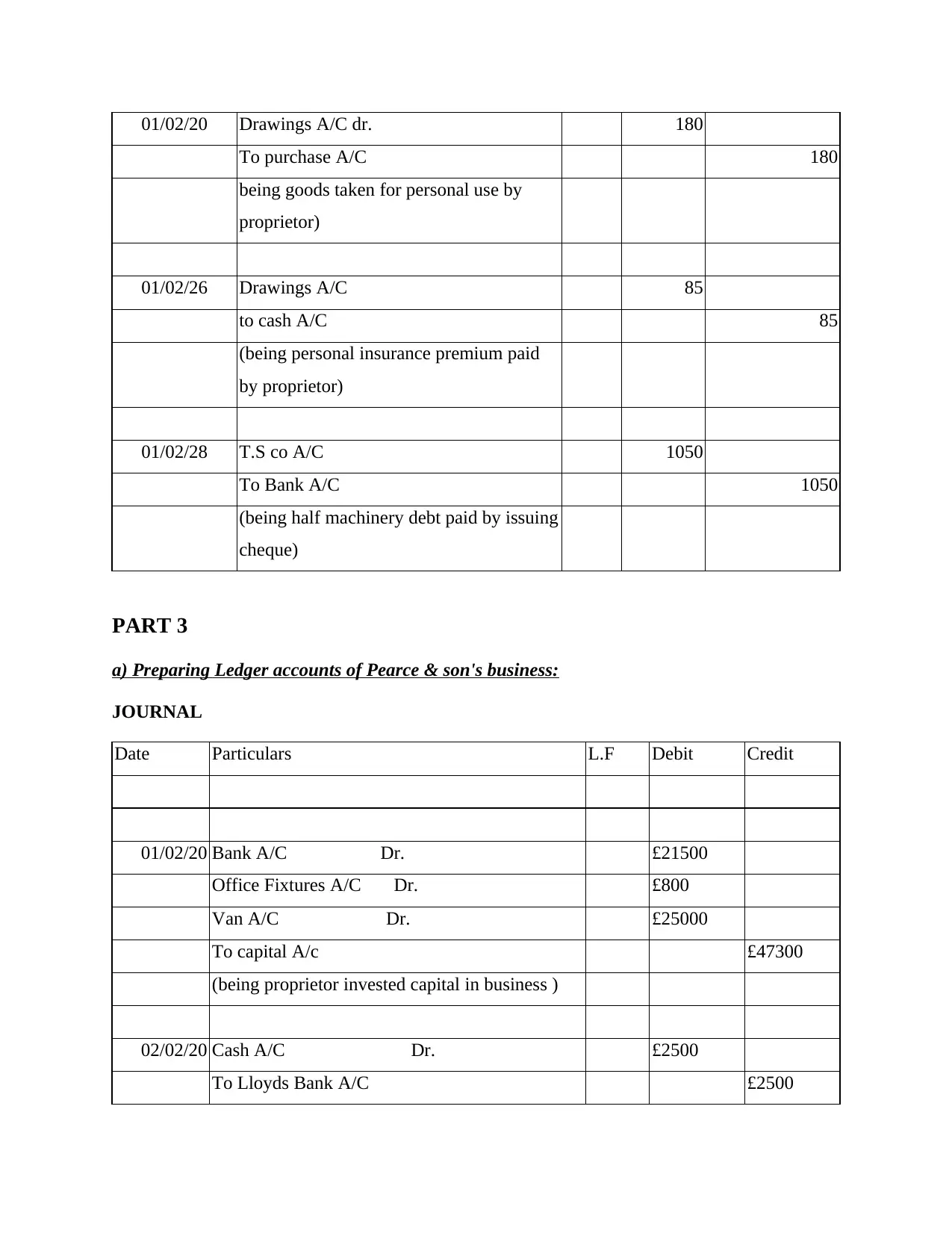

01/02/20 Drawings A/C dr. 180

To purchase A/C 180

being goods taken for personal use by

proprietor)

01/02/26 Drawings A/C 85

to cash A/C 85

(being personal insurance premium paid

by proprietor)

01/02/28 T.S co A/C 1050

To Bank A/C 1050

(being half machinery debt paid by issuing

cheque)

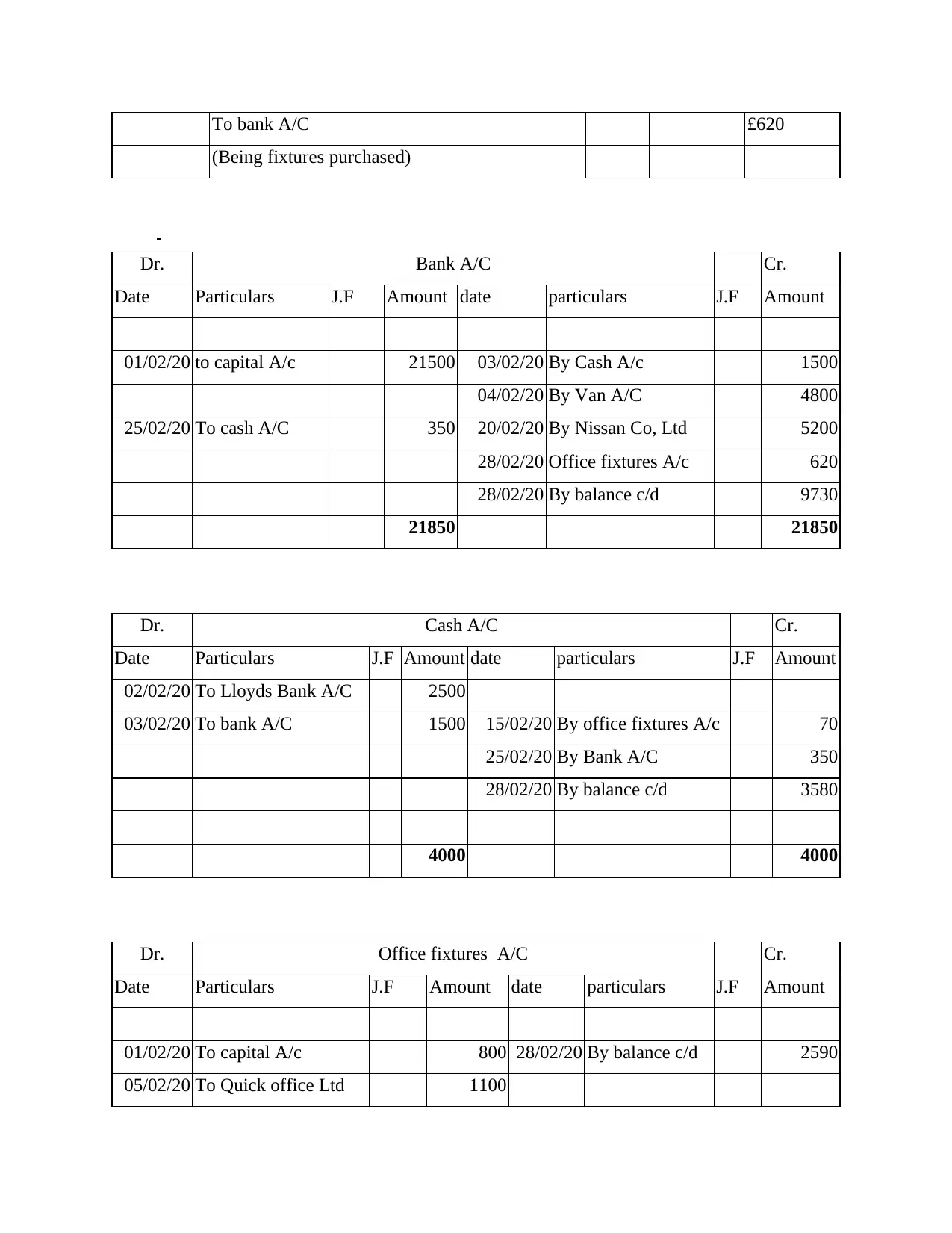

PART 3

a) Preparing Ledger accounts of Pearce & son's business:

JOURNAL

Date Particulars L.F Debit Credit

01/02/20 Bank A/C Dr. £21500

Office Fixtures A/C Dr. £800

Van A/C Dr. £25000

To capital A/c £47300

(being proprietor invested capital in business )

02/02/20 Cash A/C Dr. £2500

To Lloyds Bank A/C £2500

To purchase A/C 180

being goods taken for personal use by

proprietor)

01/02/26 Drawings A/C 85

to cash A/C 85

(being personal insurance premium paid

by proprietor)

01/02/28 T.S co A/C 1050

To Bank A/C 1050

(being half machinery debt paid by issuing

cheque)

PART 3

a) Preparing Ledger accounts of Pearce & son's business:

JOURNAL

Date Particulars L.F Debit Credit

01/02/20 Bank A/C Dr. £21500

Office Fixtures A/C Dr. £800

Van A/C Dr. £25000

To capital A/c £47300

(being proprietor invested capital in business )

02/02/20 Cash A/C Dr. £2500

To Lloyds Bank A/C £2500

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

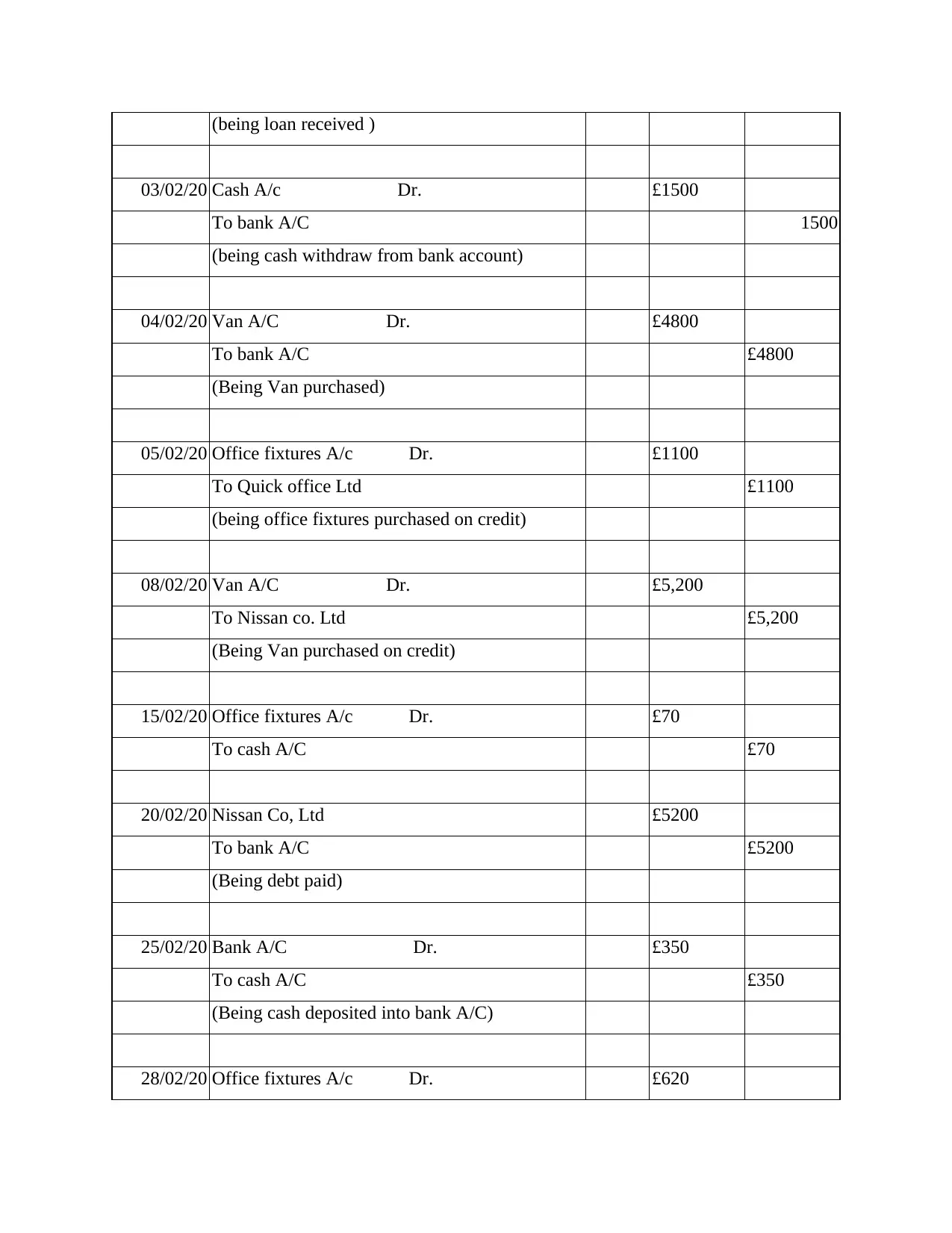

(being loan received )

03/02/20 Cash A/c Dr. £1500

To bank A/C 1500

(being cash withdraw from bank account)

04/02/20 Van A/C Dr. £4800

To bank A/C £4800

(Being Van purchased)

05/02/20 Office fixtures A/c Dr. £1100

To Quick office Ltd £1100

(being office fixtures purchased on credit)

08/02/20 Van A/C Dr. £5,200

To Nissan co. Ltd £5,200

(Being Van purchased on credit)

15/02/20 Office fixtures A/c Dr. £70

To cash A/C £70

20/02/20 Nissan Co, Ltd £5200

To bank A/C £5200

(Being debt paid)

25/02/20 Bank A/C Dr. £350

To cash A/C £350

(Being cash deposited into bank A/C)

28/02/20 Office fixtures A/c Dr. £620

03/02/20 Cash A/c Dr. £1500

To bank A/C 1500

(being cash withdraw from bank account)

04/02/20 Van A/C Dr. £4800

To bank A/C £4800

(Being Van purchased)

05/02/20 Office fixtures A/c Dr. £1100

To Quick office Ltd £1100

(being office fixtures purchased on credit)

08/02/20 Van A/C Dr. £5,200

To Nissan co. Ltd £5,200

(Being Van purchased on credit)

15/02/20 Office fixtures A/c Dr. £70

To cash A/C £70

20/02/20 Nissan Co, Ltd £5200

To bank A/C £5200

(Being debt paid)

25/02/20 Bank A/C Dr. £350

To cash A/C £350

(Being cash deposited into bank A/C)

28/02/20 Office fixtures A/c Dr. £620

To bank A/C £620

(Being fixtures purchased)

Dr. Bank A/C Cr.

Date Particulars J.F Amount date particulars J.F Amount

01/02/20 to capital A/c 21500 03/02/20 By Cash A/c 1500

04/02/20 By Van A/C 4800

25/02/20 To cash A/C 350 20/02/20 By Nissan Co, Ltd 5200

28/02/20 Office fixtures A/c 620

28/02/20 By balance c/d 9730

21850 21850

Dr. Cash A/C Cr.

Date Particulars J.F Amount date particulars J.F Amount

02/02/20 To Lloyds Bank A/C 2500

03/02/20 To bank A/C 1500 15/02/20 By office fixtures A/c 70

25/02/20 By Bank A/C 350

28/02/20 By balance c/d 3580

4000 4000

Dr. Office fixtures A/C Cr.

Date Particulars J.F Amount date particulars J.F Amount

01/02/20 To capital A/c 800 28/02/20 By balance c/d 2590

05/02/20 To Quick office Ltd 1100

(Being fixtures purchased)

Dr. Bank A/C Cr.

Date Particulars J.F Amount date particulars J.F Amount

01/02/20 to capital A/c 21500 03/02/20 By Cash A/c 1500

04/02/20 By Van A/C 4800

25/02/20 To cash A/C 350 20/02/20 By Nissan Co, Ltd 5200

28/02/20 Office fixtures A/c 620

28/02/20 By balance c/d 9730

21850 21850

Dr. Cash A/C Cr.

Date Particulars J.F Amount date particulars J.F Amount

02/02/20 To Lloyds Bank A/C 2500

03/02/20 To bank A/C 1500 15/02/20 By office fixtures A/c 70

25/02/20 By Bank A/C 350

28/02/20 By balance c/d 3580

4000 4000

Dr. Office fixtures A/C Cr.

Date Particulars J.F Amount date particulars J.F Amount

01/02/20 To capital A/c 800 28/02/20 By balance c/d 2590

05/02/20 To Quick office Ltd 1100

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

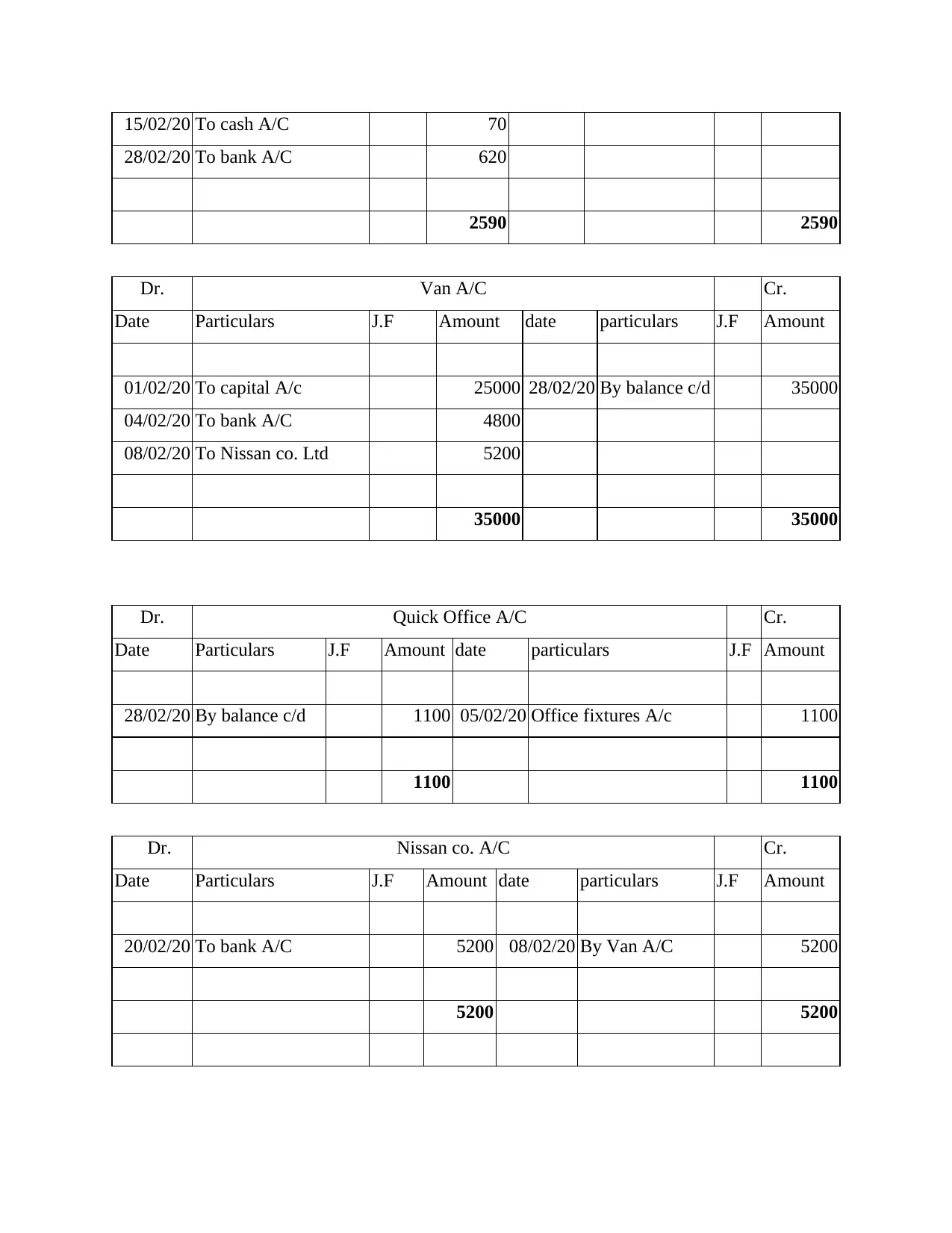

15/02/20 To cash A/C 70

28/02/20 To bank A/C 620

2590 2590

Dr. Van A/C Cr.

Date Particulars J.F Amount date particulars J.F Amount

01/02/20 To capital A/c 25000 28/02/20 By balance c/d 35000

04/02/20 To bank A/C 4800

08/02/20 To Nissan co. Ltd 5200

35000 35000

Dr. Quick Office A/C Cr.

Date Particulars J.F Amount date particulars J.F Amount

28/02/20 By balance c/d 1100 05/02/20 Office fixtures A/c 1100

1100 1100

Dr. Nissan co. A/C Cr.

Date Particulars J.F Amount date particulars J.F Amount

20/02/20 To bank A/C 5200 08/02/20 By Van A/C 5200

5200 5200

28/02/20 To bank A/C 620

2590 2590

Dr. Van A/C Cr.

Date Particulars J.F Amount date particulars J.F Amount

01/02/20 To capital A/c 25000 28/02/20 By balance c/d 35000

04/02/20 To bank A/C 4800

08/02/20 To Nissan co. Ltd 5200

35000 35000

Dr. Quick Office A/C Cr.

Date Particulars J.F Amount date particulars J.F Amount

28/02/20 By balance c/d 1100 05/02/20 Office fixtures A/c 1100

1100 1100

Dr. Nissan co. A/C Cr.

Date Particulars J.F Amount date particulars J.F Amount

20/02/20 To bank A/C 5200 08/02/20 By Van A/C 5200

5200 5200

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Dr. Lloyds Bank A/C (loan) Cr.

Date Particulars J.F Amount date

particular

s J.F Amount

28/02/20 By balance c/d 2500

By cash

A/c 2500

2500 2500

Dr. Capital A/C Cr.

date Particulars J.F Amount date particulars J.F Amount

28/02/20 By balance c/d 47300 01/02/20 By Bank A/C 21500

01/02/20

By Office Fixtures

A/C 800

01/02/20 By Van A/C 25000

47300 47300

b) Trial Balance as at 28 February 2020

Particulars Debit Credit

Bank A/C 9730

Cash A/C 3580

Office fixtures A/C 2590

Van A/C 35000

Quick Office A/C 1100

Lloyds Bank A/C 2500

Capital A/C 47300

Date Particulars J.F Amount date

particular

s J.F Amount

28/02/20 By balance c/d 2500

By cash

A/c 2500

2500 2500

Dr. Capital A/C Cr.

date Particulars J.F Amount date particulars J.F Amount

28/02/20 By balance c/d 47300 01/02/20 By Bank A/C 21500

01/02/20

By Office Fixtures

A/C 800

01/02/20 By Van A/C 25000

47300 47300

b) Trial Balance as at 28 February 2020

Particulars Debit Credit

Bank A/C 9730

Cash A/C 3580

Office fixtures A/C 2590

Van A/C 35000

Quick Office A/C 1100

Lloyds Bank A/C 2500

Capital A/C 47300

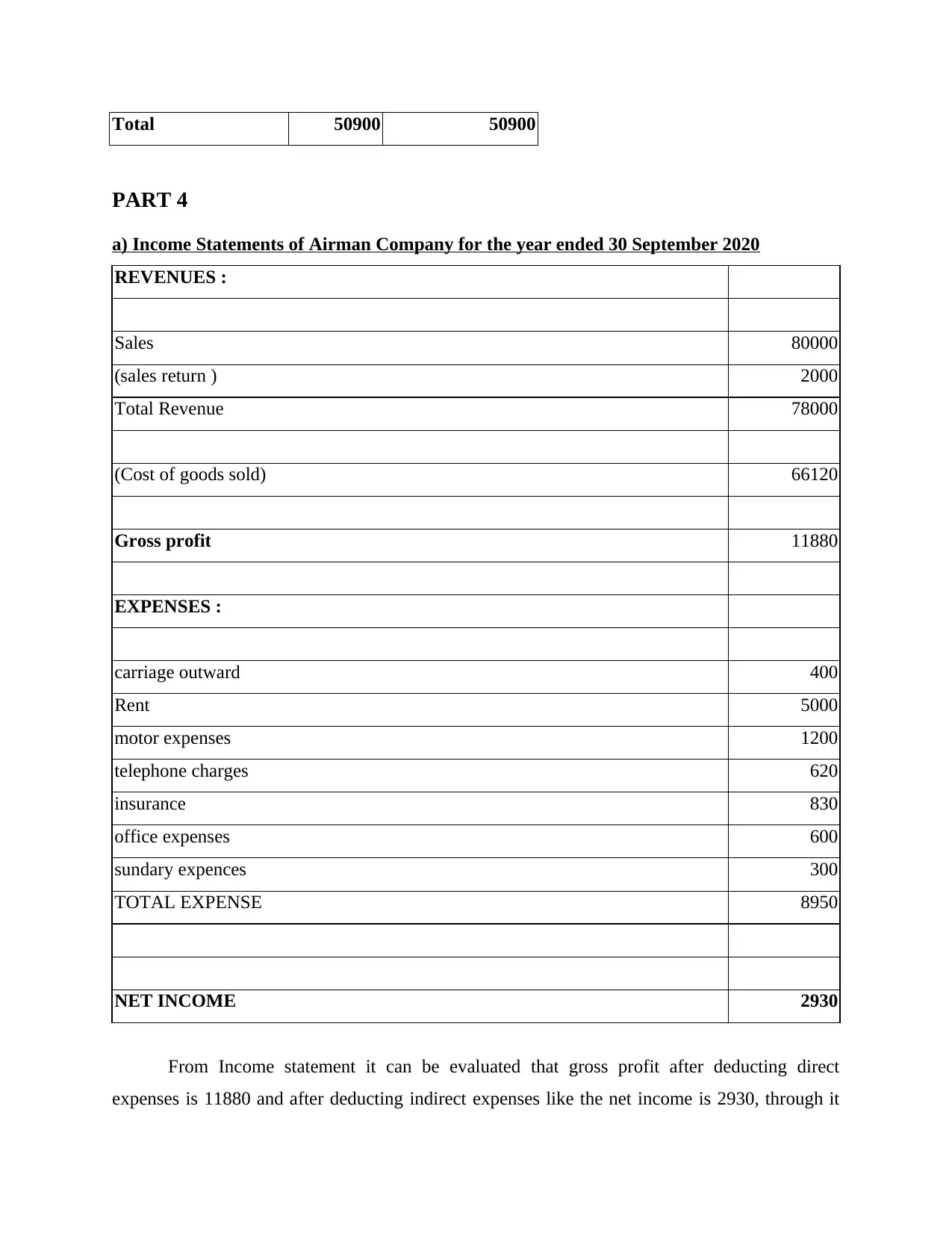

Total 50900 50900

PART 4

a) Income Statements of Airman Company for the year ended 30 September 2020

REVENUES :

Sales 80000

(sales return ) 2000

Total Revenue 78000

(Cost of goods sold) 66120

Gross profit 11880

EXPENSES :

carriage outward 400

Rent 5000

motor expenses 1200

telephone charges 620

insurance 830

office expenses 600

sundary expences 300

TOTAL EXPENSE 8950

NET INCOME 2930

From Income statement it can be evaluated that gross profit after deducting direct

expenses is 11880 and after deducting indirect expenses like the net income is 2930, through it

PART 4

a) Income Statements of Airman Company for the year ended 30 September 2020

REVENUES :

Sales 80000

(sales return ) 2000

Total Revenue 78000

(Cost of goods sold) 66120

Gross profit 11880

EXPENSES :

carriage outward 400

Rent 5000

motor expenses 1200

telephone charges 620

insurance 830

office expenses 600

sundary expences 300

TOTAL EXPENSE 8950

NET INCOME 2930

From Income statement it can be evaluated that gross profit after deducting direct

expenses is 11880 and after deducting indirect expenses like the net income is 2930, through it

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.