University of West London: Recording Business Transactions BA30592E

VerifiedAdded on 2023/06/16

|10

|1987

|266

Report

AI Summary

This report provides a detailed analysis of recording business transactions, including the process of starting a new business as a decorator, identifying decision-makers in a London Stock Exchange-listed company, and preparing journal entries and ledger accounts. It includes a comprehensive income statement for P Moore ending September 31st, 2021, and a prediction of the company's profitability for the year 2022 based on previous financial statements. The report also features examples of sales day books, purchase day books, sales returns day books, and purchase ledgers, offering a thorough overview of financial recording and analysis.

Recording Business

Transactions

Table of Contents

1

Transactions

Table of Contents

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Part – A............................................................................................................................................3

(1) Process for starting a new business enterprise as a Decorator..............................................3

(2) Identify the decision makers of the business organization which are responsible for the

process of the decision making in context to the company listed on the London Stock

Exchange.....................................................................................................................................4

Part – B............................................................................................................................................5

(a) Journal Entries for the month September, 2021....................................................................5

Part – 4.............................................................................................................................................9

(a)Income Statement of P Moore ending 31st September, 2021..................................................9

(b) Based on the income statements of previous year predict that whether the company will

attain profits or losses in the year 2022.....................................................................................10

References......................................................................................................................................10

Books & Journals......................................................................................................................10

2

(1) Process for starting a new business enterprise as a Decorator..............................................3

(2) Identify the decision makers of the business organization which are responsible for the

process of the decision making in context to the company listed on the London Stock

Exchange.....................................................................................................................................4

Part – B............................................................................................................................................5

(a) Journal Entries for the month September, 2021....................................................................5

Part – 4.............................................................................................................................................9

(a)Income Statement of P Moore ending 31st September, 2021..................................................9

(b) Based on the income statements of previous year predict that whether the company will

attain profits or losses in the year 2022.....................................................................................10

References......................................................................................................................................10

Books & Journals......................................................................................................................10

2

PART – A

(1) Process for starting a new business enterprise as a Decorator.

Sole A business organisation can be defined as a company that is run by a single natural person

who is responsible for the entire operation (Prewett, Prescott and Phillips, 2020). As a result,

the process of forming a business organisation is stated as follows:

• Idea generation: The first stage in beginning a business is to come up with a concept on

which the entire firm will be built. As a decorator, the owner must carefully consider and

assess what novelties may be presented to the target market in order to entice them to visit

the business. As a result, both the concept of uniqueness and the quality of the work can aid

in gaining a competitive advantage over competitors.

• Funding Proposal: The second and most significant stage is to approach a financial

institution, because it is critical for a firm to have adequate funds to operate. Business

owners must seek out authentic and dependable sources of funding in order to properly

invest in the company and reach a healthy financial position.

• Company location: It is critical for any company to establish itself as one of the best places to

attract and retain a big number of clients on a daily basis. In exchange for your work as a

decorator, you will be offered the opportunity to engage in commercial operations in large

cities. The main reason for this is that there are more options for business organisation, such

as event decoration, and it is relatively easy for a firm to develop and be successful over

time.

• Human Resource Selection: It is critical for a successful company organisation to have an

efficient and productive workforce to assist in the management of its. in the most

appropriate manner to flourish in a more consistent manner in the decorative company

environment, it is vital to have a workforce with the characteristics of innovation, hard

effort, and a high level of devotion.

• Tax planning: Taxes can eat into a company's profits, reducing the amount of money in the

owner's hands. As a result, we advise the respective company to do proper tax planning in

order to lower its tax liability for the current fiscal year.

Creating a business venture: It's time to start the business when you've finished all of

the preceding processes (Maurer, 2017). After completing all of the above-mentioned

3

(1) Process for starting a new business enterprise as a Decorator.

Sole A business organisation can be defined as a company that is run by a single natural person

who is responsible for the entire operation (Prewett, Prescott and Phillips, 2020). As a result,

the process of forming a business organisation is stated as follows:

• Idea generation: The first stage in beginning a business is to come up with a concept on

which the entire firm will be built. As a decorator, the owner must carefully consider and

assess what novelties may be presented to the target market in order to entice them to visit

the business. As a result, both the concept of uniqueness and the quality of the work can aid

in gaining a competitive advantage over competitors.

• Funding Proposal: The second and most significant stage is to approach a financial

institution, because it is critical for a firm to have adequate funds to operate. Business

owners must seek out authentic and dependable sources of funding in order to properly

invest in the company and reach a healthy financial position.

• Company location: It is critical for any company to establish itself as one of the best places to

attract and retain a big number of clients on a daily basis. In exchange for your work as a

decorator, you will be offered the opportunity to engage in commercial operations in large

cities. The main reason for this is that there are more options for business organisation, such

as event decoration, and it is relatively easy for a firm to develop and be successful over

time.

• Human Resource Selection: It is critical for a successful company organisation to have an

efficient and productive workforce to assist in the management of its. in the most

appropriate manner to flourish in a more consistent manner in the decorative company

environment, it is vital to have a workforce with the characteristics of innovation, hard

effort, and a high level of devotion.

• Tax planning: Taxes can eat into a company's profits, reducing the amount of money in the

owner's hands. As a result, we advise the respective company to do proper tax planning in

order to lower its tax liability for the current fiscal year.

Creating a business venture: It's time to start the business when you've finished all of

the preceding processes (Maurer, 2017). After completing all of the above-mentioned

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

processes, methods, and procedures in the Decorator business context, the company may

effectively market with the goal of success and enormous long-term earnings.

(2) Identify the decision makers of the business organization which are responsible for the

process of the decision making in context to the company listed on the London Stock Exchange.

Business managers and leaders in the business who have the ability and power to make various

types of strategic and essential decisions are known as decision makers. Acquisitions,

mergers, and expansions are examples of these decisions (Susanto and Almunawar, 2018) .

Various decision makers are also involved in the decision-making process for all topics

relating to the business at Unilever, which is considered one of the leading businesses on the

London Stock Exchange. The following are the various decision-makers and their respective

organisations:

• CEOs and business owners: Business managers play a critical role in the development of

action plans that help companies achieve their objectives in the most efficient way possible

(Teece, 2018). Managers at Unilever always make sure that all of the company's employees

are functioning efficiently and adopting all of the manager's strategies.

• Investors: They are the company's most crucial decision-makers. The key reason for this is that

they are the ones that contribute to increasing shareholder value, lowering capital expenses,

and establishing a strong reputation in the investment community over time. The investors

are exclusively responsible for making judgments in the many affairs of the firm so that it

can operate properly in the framework of the specific business.

• Analysts: They are proponents of taking a proactive approach before dealing with a specific

type of circumstance. In the case of Unilever, they have a team of analysts who are primarily

involved in the process of examining financial data in order to take action. They also have

excellent company management skills and are most likely to handle all stages of the

decision-making process (Tripathi, 2018).

Part – B

(a) Journal Entries for the month September, 2021

Date Particulars Debit

Amount

Credit

Amount

4

effectively market with the goal of success and enormous long-term earnings.

(2) Identify the decision makers of the business organization which are responsible for the

process of the decision making in context to the company listed on the London Stock Exchange.

Business managers and leaders in the business who have the ability and power to make various

types of strategic and essential decisions are known as decision makers. Acquisitions,

mergers, and expansions are examples of these decisions (Susanto and Almunawar, 2018) .

Various decision makers are also involved in the decision-making process for all topics

relating to the business at Unilever, which is considered one of the leading businesses on the

London Stock Exchange. The following are the various decision-makers and their respective

organisations:

• CEOs and business owners: Business managers play a critical role in the development of

action plans that help companies achieve their objectives in the most efficient way possible

(Teece, 2018). Managers at Unilever always make sure that all of the company's employees

are functioning efficiently and adopting all of the manager's strategies.

• Investors: They are the company's most crucial decision-makers. The key reason for this is that

they are the ones that contribute to increasing shareholder value, lowering capital expenses,

and establishing a strong reputation in the investment community over time. The investors

are exclusively responsible for making judgments in the many affairs of the firm so that it

can operate properly in the framework of the specific business.

• Analysts: They are proponents of taking a proactive approach before dealing with a specific

type of circumstance. In the case of Unilever, they have a team of analysts who are primarily

involved in the process of examining financial data in order to take action. They also have

excellent company management skills and are most likely to handle all stages of the

decision-making process (Tripathi, 2018).

Part – B

(a) Journal Entries for the month September, 2021

Date Particulars Debit

Amount

Credit

Amount

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

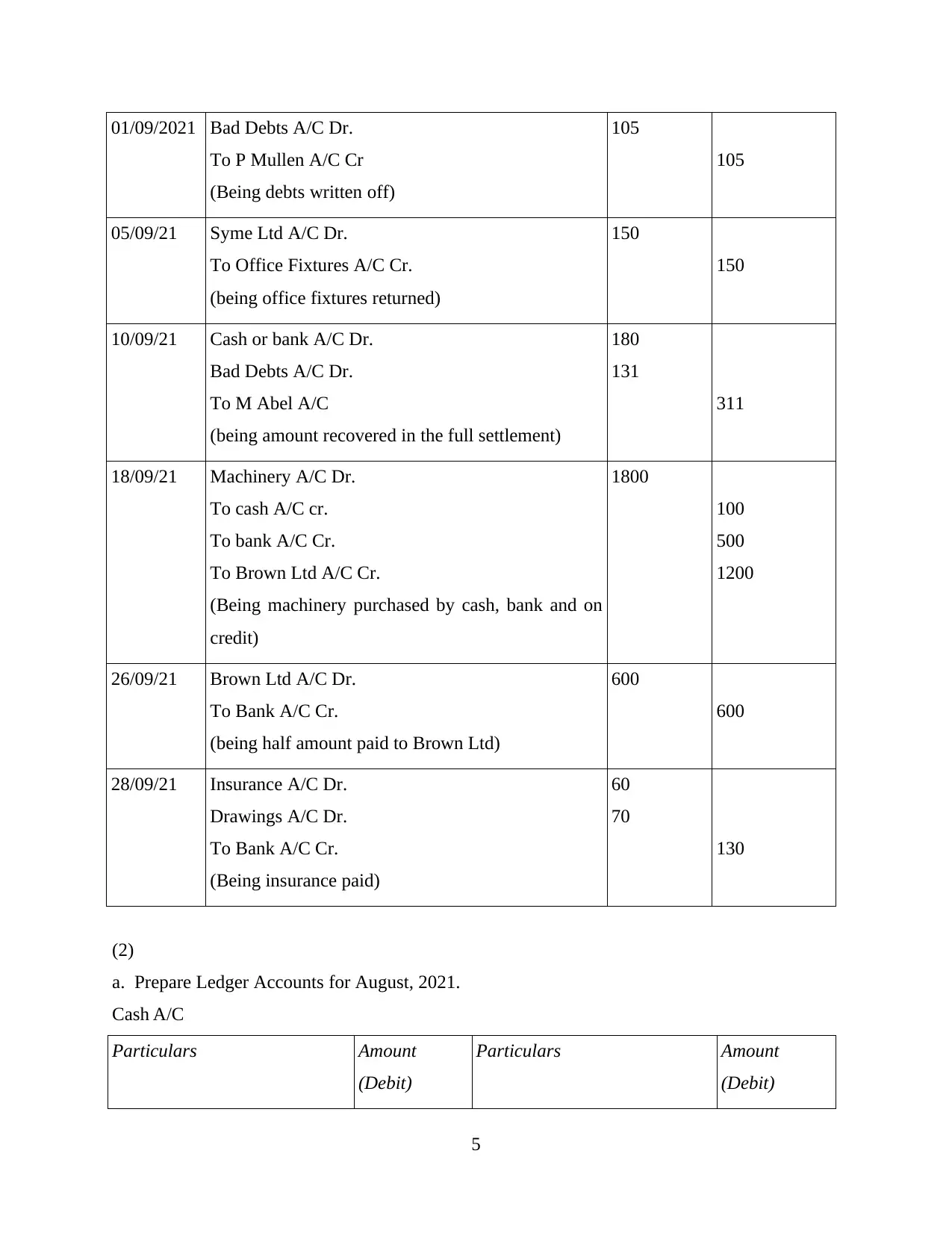

01/09/2021 Bad Debts A/C Dr.

To P Mullen A/C Cr

(Being debts written off)

105

105

05/09/21 Syme Ltd A/C Dr.

To Office Fixtures A/C Cr.

(being office fixtures returned)

150

150

10/09/21 Cash or bank A/C Dr.

Bad Debts A/C Dr.

To M Abel A/C

(being amount recovered in the full settlement)

180

131

311

18/09/21 Machinery A/C Dr.

To cash A/C cr.

To bank A/C Cr.

To Brown Ltd A/C Cr.

(Being machinery purchased by cash, bank and on

credit)

1800

100

500

1200

26/09/21 Brown Ltd A/C Dr.

To Bank A/C Cr.

(being half amount paid to Brown Ltd)

600

600

28/09/21 Insurance A/C Dr.

Drawings A/C Dr.

To Bank A/C Cr.

(Being insurance paid)

60

70

130

(2)

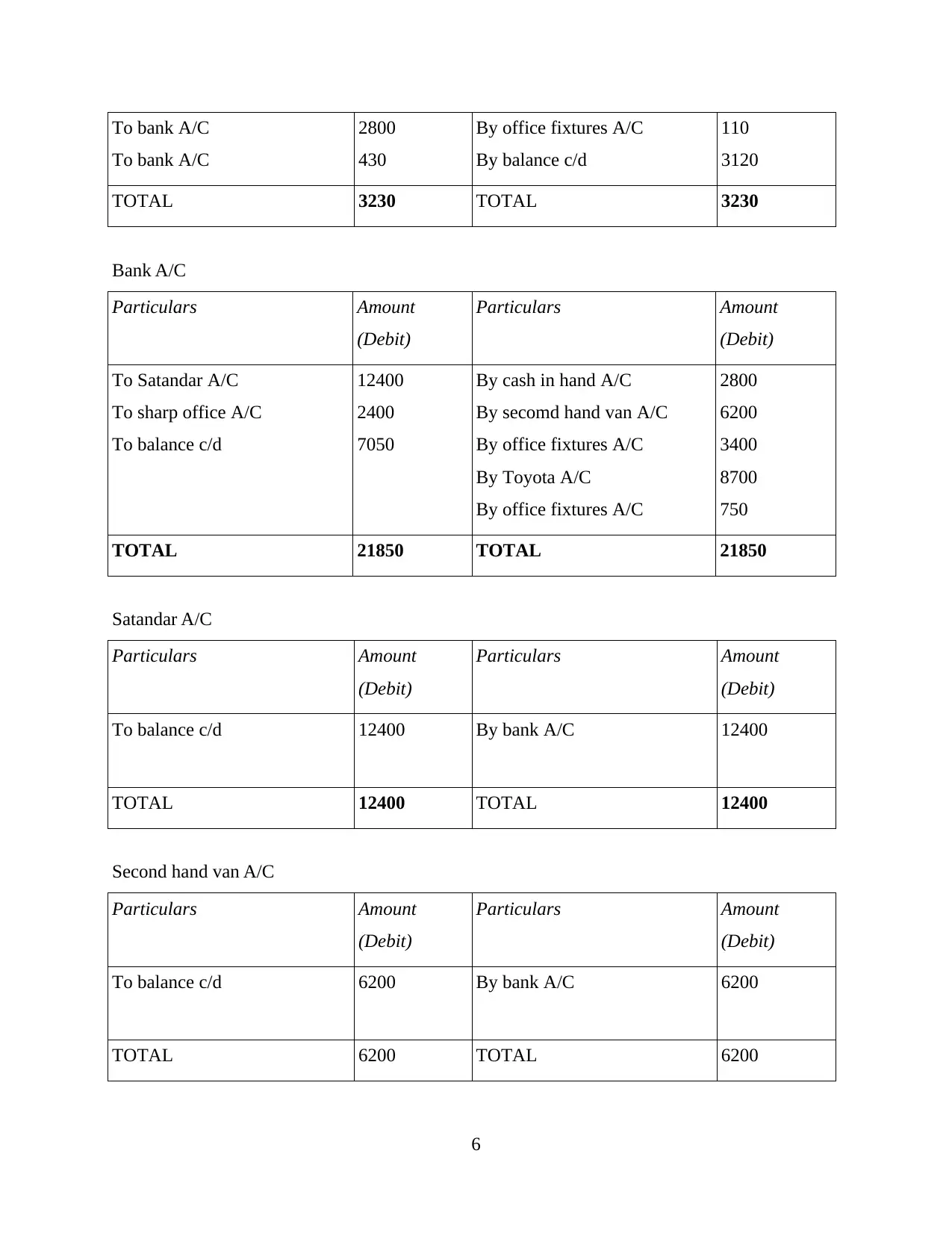

a. Prepare Ledger Accounts for August, 2021.

Cash A/C

Particulars Amount

(Debit)

Particulars Amount

(Debit)

5

To P Mullen A/C Cr

(Being debts written off)

105

105

05/09/21 Syme Ltd A/C Dr.

To Office Fixtures A/C Cr.

(being office fixtures returned)

150

150

10/09/21 Cash or bank A/C Dr.

Bad Debts A/C Dr.

To M Abel A/C

(being amount recovered in the full settlement)

180

131

311

18/09/21 Machinery A/C Dr.

To cash A/C cr.

To bank A/C Cr.

To Brown Ltd A/C Cr.

(Being machinery purchased by cash, bank and on

credit)

1800

100

500

1200

26/09/21 Brown Ltd A/C Dr.

To Bank A/C Cr.

(being half amount paid to Brown Ltd)

600

600

28/09/21 Insurance A/C Dr.

Drawings A/C Dr.

To Bank A/C Cr.

(Being insurance paid)

60

70

130

(2)

a. Prepare Ledger Accounts for August, 2021.

Cash A/C

Particulars Amount

(Debit)

Particulars Amount

(Debit)

5

To bank A/C

To bank A/C

2800

430

By office fixtures A/C

By balance c/d

110

3120

TOTAL 3230 TOTAL 3230

Bank A/C

Particulars Amount

(Debit)

Particulars Amount

(Debit)

To Satandar A/C

To sharp office A/C

To balance c/d

12400

2400

7050

By cash in hand A/C

By secomd hand van A/C

By office fixtures A/C

By Toyota A/C

By office fixtures A/C

2800

6200

3400

8700

750

TOTAL 21850 TOTAL 21850

Satandar A/C

Particulars Amount

(Debit)

Particulars Amount

(Debit)

To balance c/d 12400 By bank A/C 12400

TOTAL 12400 TOTAL 12400

Second hand van A/C

Particulars Amount

(Debit)

Particulars Amount

(Debit)

To balance c/d 6200 By bank A/C 6200

TOTAL 6200 TOTAL 6200

6

To bank A/C

2800

430

By office fixtures A/C

By balance c/d

110

3120

TOTAL 3230 TOTAL 3230

Bank A/C

Particulars Amount

(Debit)

Particulars Amount

(Debit)

To Satandar A/C

To sharp office A/C

To balance c/d

12400

2400

7050

By cash in hand A/C

By secomd hand van A/C

By office fixtures A/C

By Toyota A/C

By office fixtures A/C

2800

6200

3400

8700

750

TOTAL 21850 TOTAL 21850

Satandar A/C

Particulars Amount

(Debit)

Particulars Amount

(Debit)

To balance c/d 12400 By bank A/C 12400

TOTAL 12400 TOTAL 12400

Second hand van A/C

Particulars Amount

(Debit)

Particulars Amount

(Debit)

To balance c/d 6200 By bank A/C 6200

TOTAL 6200 TOTAL 6200

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

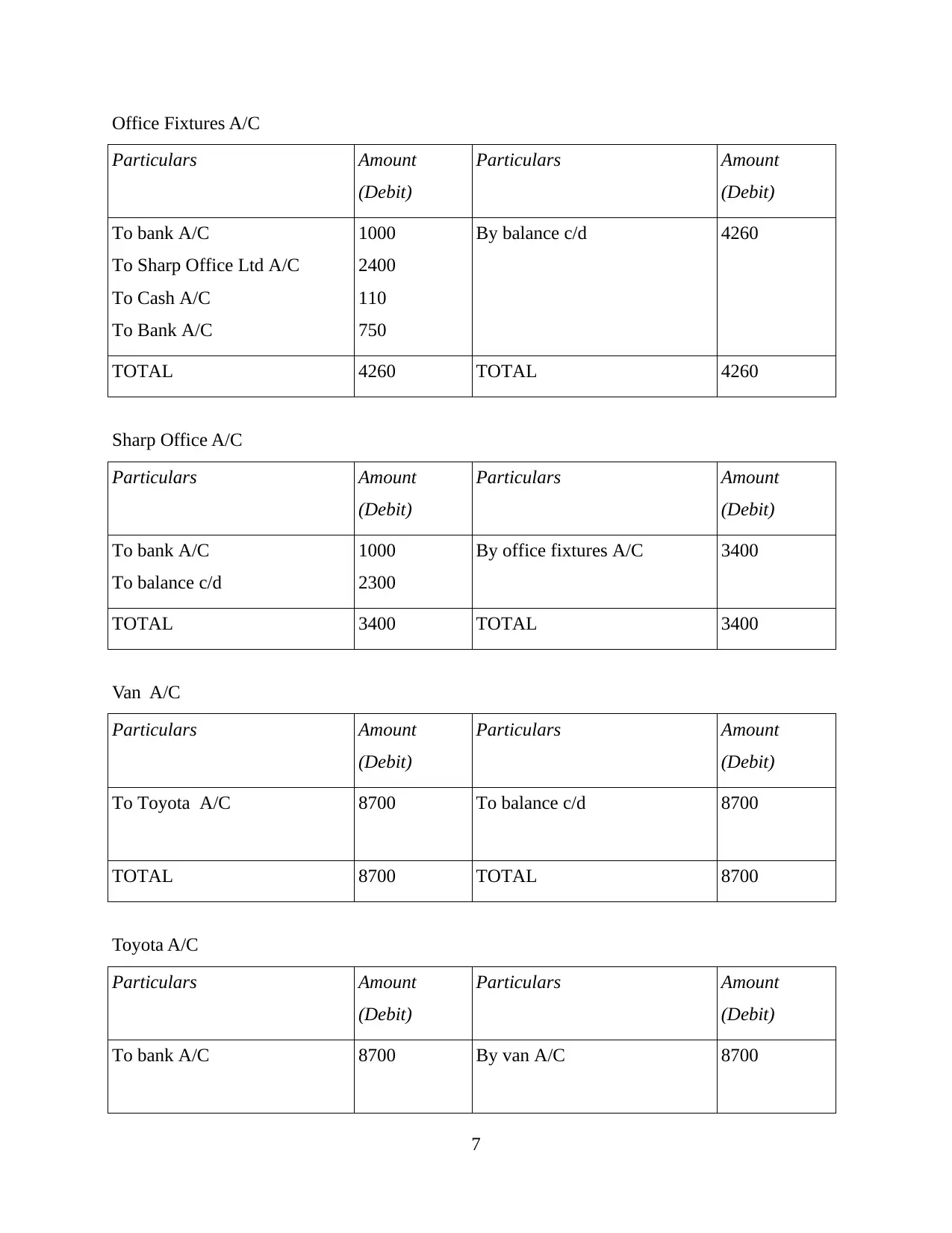

Office Fixtures A/C

Particulars Amount

(Debit)

Particulars Amount

(Debit)

To bank A/C

To Sharp Office Ltd A/C

To Cash A/C

To Bank A/C

1000

2400

110

750

By balance c/d 4260

TOTAL 4260 TOTAL 4260

Sharp Office A/C

Particulars Amount

(Debit)

Particulars Amount

(Debit)

To bank A/C

To balance c/d

1000

2300

By office fixtures A/C 3400

TOTAL 3400 TOTAL 3400

Van A/C

Particulars Amount

(Debit)

Particulars Amount

(Debit)

To Toyota A/C 8700 To balance c/d 8700

TOTAL 8700 TOTAL 8700

Toyota A/C

Particulars Amount

(Debit)

Particulars Amount

(Debit)

To bank A/C 8700 By van A/C 8700

7

Particulars Amount

(Debit)

Particulars Amount

(Debit)

To bank A/C

To Sharp Office Ltd A/C

To Cash A/C

To Bank A/C

1000

2400

110

750

By balance c/d 4260

TOTAL 4260 TOTAL 4260

Sharp Office A/C

Particulars Amount

(Debit)

Particulars Amount

(Debit)

To bank A/C

To balance c/d

1000

2300

By office fixtures A/C 3400

TOTAL 3400 TOTAL 3400

Van A/C

Particulars Amount

(Debit)

Particulars Amount

(Debit)

To Toyota A/C 8700 To balance c/d 8700

TOTAL 8700 TOTAL 8700

Toyota A/C

Particulars Amount

(Debit)

Particulars Amount

(Debit)

To bank A/C 8700 By van A/C 8700

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TOTAL 8700 TOTAL 8700

Trial Balance

Particulars Amount

(Debit)

Amount

(Credit)

Cash A/C 3120

Bank A/C 7050

Satandar A/C 12400

Second hand van A/C 6200

Office fixtures A/C 4260

Sharp office Ltd A/C 2300

Van A/C 8700

Toyota A/C - -

Suspense A/C 11870

TOTAL 27950 27950

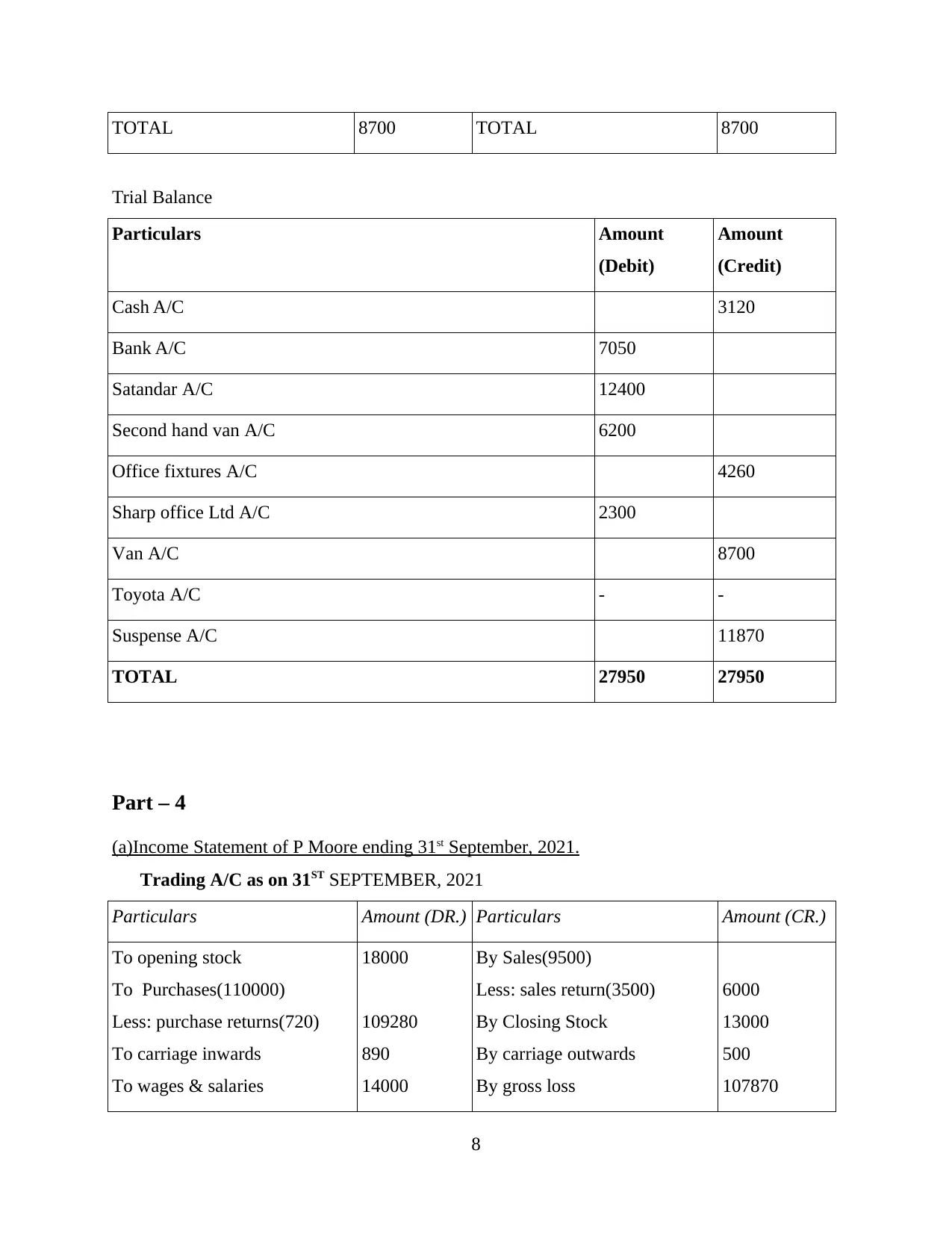

Part – 4

(a)Income Statement of P Moore ending 31st September, 2021.

Trading A/C as on 31ST SEPTEMBER, 2021

Particulars Amount (DR.) Particulars Amount (CR.)

To opening stock

To Purchases(110000)

Less: purchase returns(720)

To carriage inwards

To wages & salaries

18000

109280

890

14000

By Sales(9500)

Less: sales return(3500)

By Closing Stock

By carriage outwards

By gross loss

6000

13000

500

107870

8

Trial Balance

Particulars Amount

(Debit)

Amount

(Credit)

Cash A/C 3120

Bank A/C 7050

Satandar A/C 12400

Second hand van A/C 6200

Office fixtures A/C 4260

Sharp office Ltd A/C 2300

Van A/C 8700

Toyota A/C - -

Suspense A/C 11870

TOTAL 27950 27950

Part – 4

(a)Income Statement of P Moore ending 31st September, 2021.

Trading A/C as on 31ST SEPTEMBER, 2021

Particulars Amount (DR.) Particulars Amount (CR.)

To opening stock

To Purchases(110000)

Less: purchase returns(720)

To carriage inwards

To wages & salaries

18000

109280

890

14000

By Sales(9500)

Less: sales return(3500)

By Closing Stock

By carriage outwards

By gross loss

6000

13000

500

107870

8

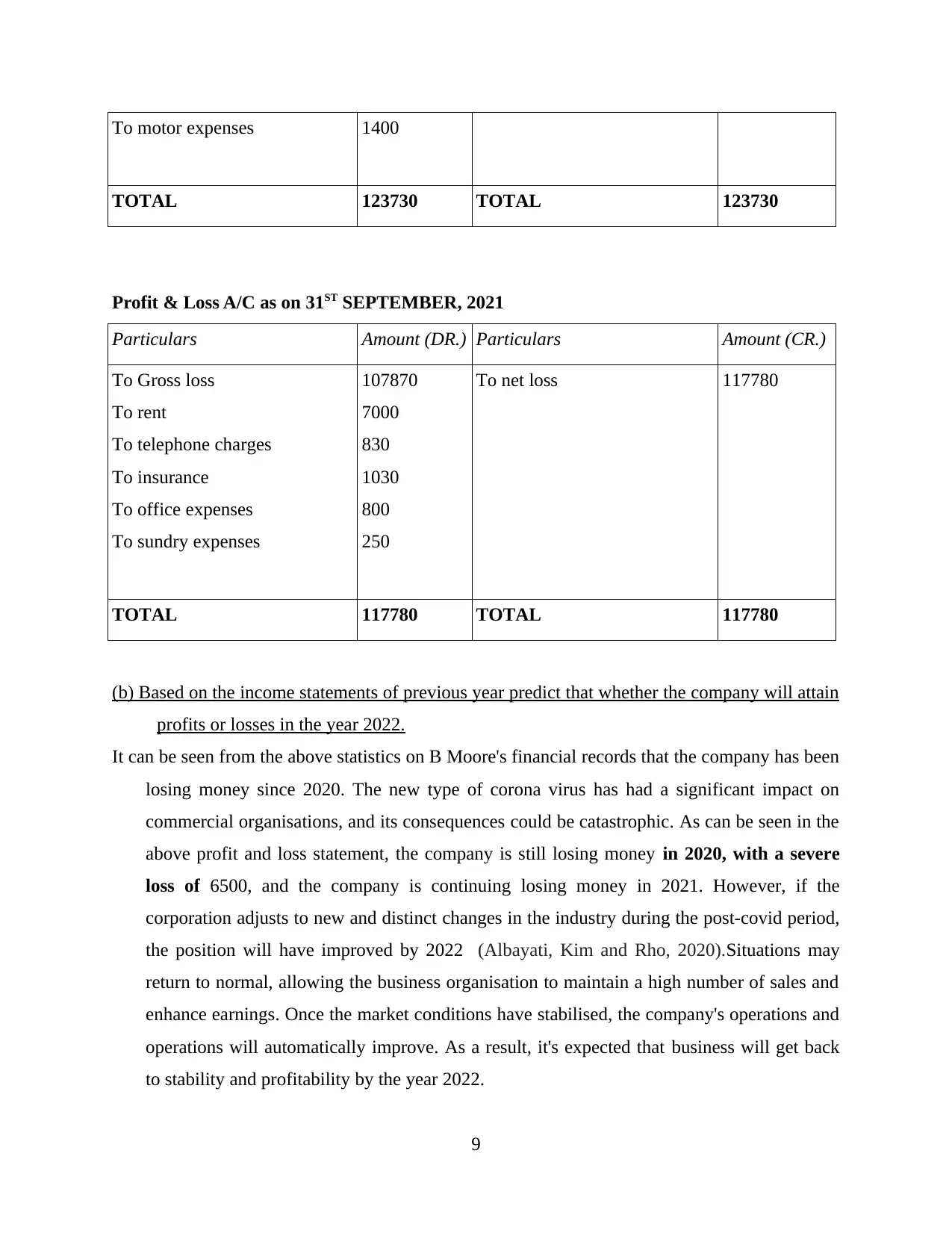

To motor expenses 1400

TOTAL 123730 TOTAL 123730

Profit & Loss A/C as on 31ST SEPTEMBER, 2021

Particulars Amount (DR.) Particulars Amount (CR.)

To Gross loss

To rent

To telephone charges

To insurance

To office expenses

To sundry expenses

107870

7000

830

1030

800

250

To net loss 117780

TOTAL 117780 TOTAL 117780

(b) Based on the income statements of previous year predict that whether the company will attain

profits or losses in the year 2022.

It can be seen from the above statistics on B Moore's financial records that the company has been

losing money since 2020. The new type of corona virus has had a significant impact on

commercial organisations, and its consequences could be catastrophic. As can be seen in the

above profit and loss statement, the company is still losing money in 2020, with a severe

loss of 6500, and the company is continuing losing money in 2021. However, if the

corporation adjusts to new and distinct changes in the industry during the post-covid period,

the position will have improved by 2022 (Albayati, Kim and Rho, 2020).Situations may

return to normal, allowing the business organisation to maintain a high number of sales and

enhance earnings. Once the market conditions have stabilised, the company's operations and

operations will automatically improve. As a result, it's expected that business will get back

to stability and profitability by the year 2022.

9

TOTAL 123730 TOTAL 123730

Profit & Loss A/C as on 31ST SEPTEMBER, 2021

Particulars Amount (DR.) Particulars Amount (CR.)

To Gross loss

To rent

To telephone charges

To insurance

To office expenses

To sundry expenses

107870

7000

830

1030

800

250

To net loss 117780

TOTAL 117780 TOTAL 117780

(b) Based on the income statements of previous year predict that whether the company will attain

profits or losses in the year 2022.

It can be seen from the above statistics on B Moore's financial records that the company has been

losing money since 2020. The new type of corona virus has had a significant impact on

commercial organisations, and its consequences could be catastrophic. As can be seen in the

above profit and loss statement, the company is still losing money in 2020, with a severe

loss of 6500, and the company is continuing losing money in 2021. However, if the

corporation adjusts to new and distinct changes in the industry during the post-covid period,

the position will have improved by 2022 (Albayati, Kim and Rho, 2020).Situations may

return to normal, allowing the business organisation to maintain a high number of sales and

enhance earnings. Once the market conditions have stabilised, the company's operations and

operations will automatically improve. As a result, it's expected that business will get back

to stability and profitability by the year 2022.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

References

Books & Journals

Prewett, K. W., Prescott, G. L. and Phillips, K., 2020. Blockchain adoption is inevitable—

Barriers and risks remain. Journal of Corporate accounting & finance, 31(2), pp.21-28.

Maurer, B., 2017. Money as token and money as record in distributed accounts. Distributed

agency, pp.109-16.

Teece, D. J., 2018. Profiting from innovation in the digital economy: Enabling technologies,

standards, and licensing models in the wireless world. Research Policy, 47(8), pp.1367-

1387.

Albayati, H., Kim, S. K. and Rho, J. J., 2020. Accepting financial transactions using blockchain

technology and cryptocurrency: A customer perspective approach. Technology in

Society, 62, p.101320.

Susanto, H. and Almunawar, M. N., 2018. Information security management systems: A novel

framework and software as a tool for compliance with information security standards.

Apple Academic Press.

Tripathi, A. M., 2018. Learning Robotic Process Automation: Create Software robots and

automate business processes with the leading RPA tool–UiPath. Packt Publishing Ltd.

10

Books & Journals

Prewett, K. W., Prescott, G. L. and Phillips, K., 2020. Blockchain adoption is inevitable—

Barriers and risks remain. Journal of Corporate accounting & finance, 31(2), pp.21-28.

Maurer, B., 2017. Money as token and money as record in distributed accounts. Distributed

agency, pp.109-16.

Teece, D. J., 2018. Profiting from innovation in the digital economy: Enabling technologies,

standards, and licensing models in the wireless world. Research Policy, 47(8), pp.1367-

1387.

Albayati, H., Kim, S. K. and Rho, J. J., 2020. Accepting financial transactions using blockchain

technology and cryptocurrency: A customer perspective approach. Technology in

Society, 62, p.101320.

Susanto, H. and Almunawar, M. N., 2018. Information security management systems: A novel

framework and software as a tool for compliance with information security standards.

Apple Academic Press.

Tripathi, A. M., 2018. Learning Robotic Process Automation: Create Software robots and

automate business processes with the leading RPA tool–UiPath. Packt Publishing Ltd.

10

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.