Analyzing Business Transactions: Journal to Income Statement

VerifiedAdded on 2023/06/14

|13

|2791

|472

Practical Assignment

AI Summary

This assignment focuses on recording business transactions, starting with the steps to start a decorating business in the UK and identifying decision-makers in a large listed company like Tesco. It then delves into practical accounting tasks, including recording journal entries for F Polk's bakery business, preparing general ledger accounts and a trial balance for ABC Enterprise, Maurice and brothers, and creating an income statement for B Moore, along with a prediction for the company's profit or loss in 2022 based on past performance. The assignment demonstrates a comprehensive understanding of financial accounting principles and their application in real-world business scenarios. Desklib provides access to similar solved assignments and study tools for students.

RECORDING BUSINESS

TRANSACTION

TRANSACTION

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

PART A...........................................................................................................................................3

(1) Steps to start new business.....................................................................................................3

(2) Decision-maker of large and listed company.........................................................................4

PART B...........................................................................................................................................5

(1) Recording necessary Journal entries in the books of Bakery business of F Polk..................5

(2) Preparation of General Ledger account and Trial Balance account of ABC Enterprise,

Maurice and brothers...................................................................................................................7

(3) Preparation of Income Statement of B Moore and making prediction................................10

CONCLUSION..............................................................................................................................11

REFERENCES................................................................................................................................1

INTRODUCTION...........................................................................................................................3

PART A...........................................................................................................................................3

(1) Steps to start new business.....................................................................................................3

(2) Decision-maker of large and listed company.........................................................................4

PART B...........................................................................................................................................5

(1) Recording necessary Journal entries in the books of Bakery business of F Polk..................5

(2) Preparation of General Ledger account and Trial Balance account of ABC Enterprise,

Maurice and brothers...................................................................................................................7

(3) Preparation of Income Statement of B Moore and making prediction................................10

CONCLUSION..............................................................................................................................11

REFERENCES................................................................................................................................1

INTRODUCTION

Recording business transaction is a process in which the owner need to maintain proper

books of accounts via recording each and every transaction related to business as per double

entry system. The report will cover the various recording, posting and preparation of trial balance

using the business transactions. Further, using the trail balance of B Moore, the report has also

prepared the income statement of business for the year 2021 along with the prediction of profit

and loss of the company in the year 2022. Lastly, the report has also cover the steps to start a

decorating business in UK along with the identification of decision-maker of Large company

listed on London stock exchange.

PART A

(1) Steps to start new business

In order to start the small business in UK as a Decorator, David Green need to follows the

respective eight steps which are as follows:

Nail down own business model: This is the first stage in which owner need to decide the

model for their small business. In this they have to select whether they will run contract

shop or retail shop. In contract shop customer will supply blanks and business will

decorate it and further charge for it. While in retail shop, the business will supply both

blanks as well as decoration and charge for the same (Thottoli, 2020). In this stage, the

owner also need to decide the location where they will start the business such as UK

industrial location or retail location.

Create a business plan: In the second step, David Green need to create a business plan

for their small business in which they should include products and service they will offer,

target customer, marketing and operational strategies, business structure, budget etc. This

is basically providing road map of the business. Also, owner need to arrange the fund for

starting business and for this they have to decide source such as loan, own capital etc.

Getting equipment ducks in a row: At this stage, owner of sole trader need to make a

short list of all the decoration equipment’s and supplies require for their start-up. Also,

they have to do some market research to identify the best offerings from the supplier of

those equipment’s (Onuoha and Enyi, 2019).

Recording business transaction is a process in which the owner need to maintain proper

books of accounts via recording each and every transaction related to business as per double

entry system. The report will cover the various recording, posting and preparation of trial balance

using the business transactions. Further, using the trail balance of B Moore, the report has also

prepared the income statement of business for the year 2021 along with the prediction of profit

and loss of the company in the year 2022. Lastly, the report has also cover the steps to start a

decorating business in UK along with the identification of decision-maker of Large company

listed on London stock exchange.

PART A

(1) Steps to start new business

In order to start the small business in UK as a Decorator, David Green need to follows the

respective eight steps which are as follows:

Nail down own business model: This is the first stage in which owner need to decide the

model for their small business. In this they have to select whether they will run contract

shop or retail shop. In contract shop customer will supply blanks and business will

decorate it and further charge for it. While in retail shop, the business will supply both

blanks as well as decoration and charge for the same (Thottoli, 2020). In this stage, the

owner also need to decide the location where they will start the business such as UK

industrial location or retail location.

Create a business plan: In the second step, David Green need to create a business plan

for their small business in which they should include products and service they will offer,

target customer, marketing and operational strategies, business structure, budget etc. This

is basically providing road map of the business. Also, owner need to arrange the fund for

starting business and for this they have to decide source such as loan, own capital etc.

Getting equipment ducks in a row: At this stage, owner of sole trader need to make a

short list of all the decoration equipment’s and supplies require for their start-up. Also,

they have to do some market research to identify the best offerings from the supplier of

those equipment’s (Onuoha and Enyi, 2019).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Start blanks shopping: If they want to offer decorated apparel, hard good or both it is

recommended to the owner that they should start shopping with the supplier who can

align with you as per the taste and preference of customers. It is further recommended

that David Green have work with regional supplier of UK to save shipping cost and get

goods faster (Nasir and Talib, 2018).

Getting Logo: In this step, it is advisable to the owner of decoration shop that they should

get their logo along with the business card, broacher, stationery, invoice book with logo

in them. It is because it helps in increasing the brand value of the company in the market.

Social media platform: Further, engaging into social media is basically one of the most

important step for staring any new business. With the help of social media apps, the sole

trader can connect with huge customer and also increase their customer base. It is

advisable that they should post their decorations images over social media apps such as

Instagram, Facebook etc. (Jasim and Raewf, 2020).

Building own website: In this stage, it is recommended to sole trader than they should

build their own website from where customer can easily place online orders and they will

provide online delivery option. This is best to satisfy and keep the customers happy

(Wulanditya and Aprillianita, 2018).

Network in community: Lastly, it is advisable to David Green that they should engage in

community welfare such as donation, sponsoring children sport program etc. to increase

their brand value in the UK local market.

(2) Decision-maker of large and listed company

The decision-maker of listed company are those people which ultimately make the decision

of the company acquisition, expansion and investment. They also need to make the decision

regarding the organization policy along with various tactical, operational, programmed and non-

programmed decisions. The various decision-maker of large company listed on London stock

exchange such as Tesco are as follows:

Shareholders: They are basically the owner of the company who make the decision

regarding whether company need to invest profit or retain within the business. They also

make the decision regarding how much profit is need to be distributed among themselves

as dividend (Jizdan, 2018).

recommended to the owner that they should start shopping with the supplier who can

align with you as per the taste and preference of customers. It is further recommended

that David Green have work with regional supplier of UK to save shipping cost and get

goods faster (Nasir and Talib, 2018).

Getting Logo: In this step, it is advisable to the owner of decoration shop that they should

get their logo along with the business card, broacher, stationery, invoice book with logo

in them. It is because it helps in increasing the brand value of the company in the market.

Social media platform: Further, engaging into social media is basically one of the most

important step for staring any new business. With the help of social media apps, the sole

trader can connect with huge customer and also increase their customer base. It is

advisable that they should post their decorations images over social media apps such as

Instagram, Facebook etc. (Jasim and Raewf, 2020).

Building own website: In this stage, it is recommended to sole trader than they should

build their own website from where customer can easily place online orders and they will

provide online delivery option. This is best to satisfy and keep the customers happy

(Wulanditya and Aprillianita, 2018).

Network in community: Lastly, it is advisable to David Green that they should engage in

community welfare such as donation, sponsoring children sport program etc. to increase

their brand value in the UK local market.

(2) Decision-maker of large and listed company

The decision-maker of listed company are those people which ultimately make the decision

of the company acquisition, expansion and investment. They also need to make the decision

regarding the organization policy along with various tactical, operational, programmed and non-

programmed decisions. The various decision-maker of large company listed on London stock

exchange such as Tesco are as follows:

Shareholders: They are basically the owner of the company who make the decision

regarding whether company need to invest profit or retain within the business. They also

make the decision regarding how much profit is need to be distributed among themselves

as dividend (Jizdan, 2018).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

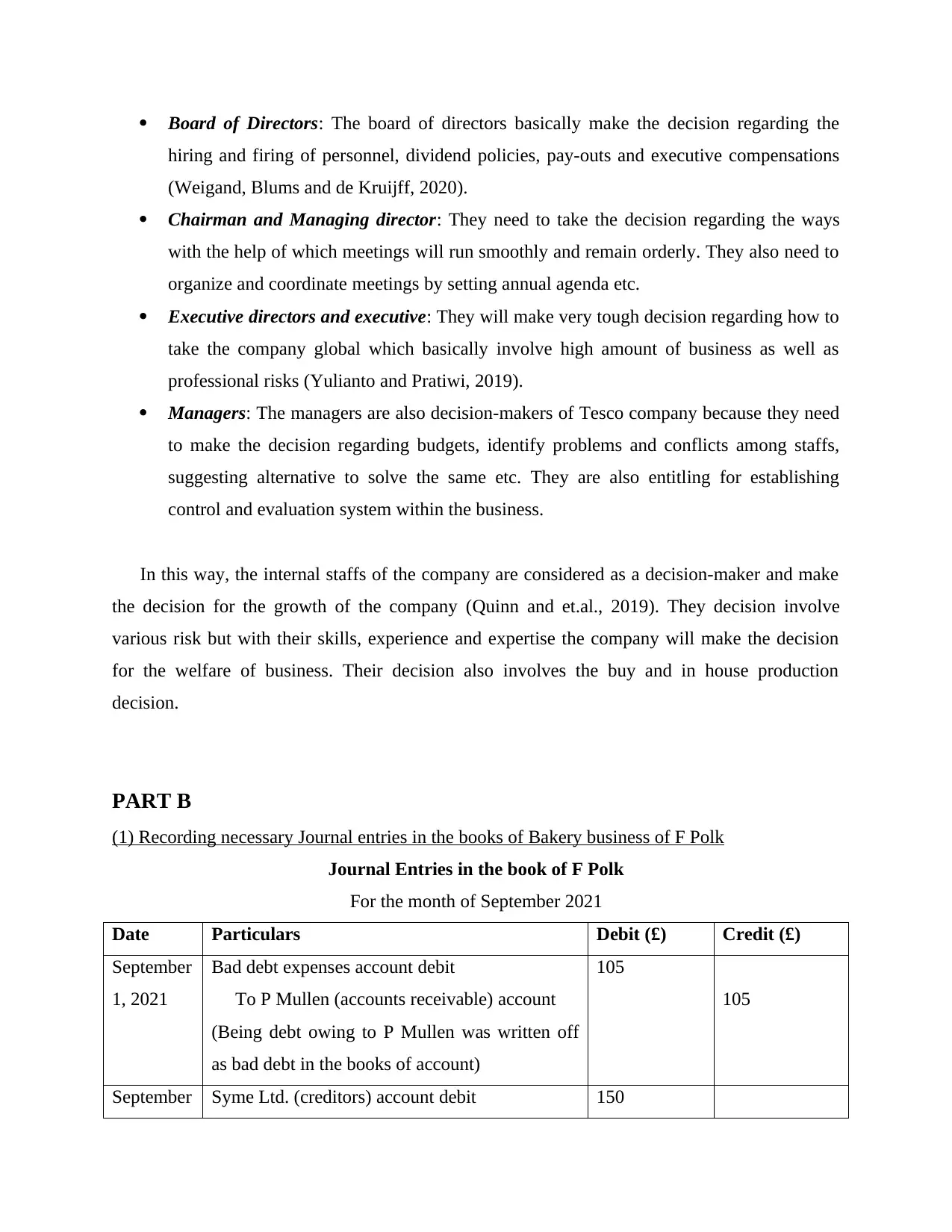

Board of Directors: The board of directors basically make the decision regarding the

hiring and firing of personnel, dividend policies, pay-outs and executive compensations

(Weigand, Blums and de Kruijff, 2020).

Chairman and Managing director: They need to take the decision regarding the ways

with the help of which meetings will run smoothly and remain orderly. They also need to

organize and coordinate meetings by setting annual agenda etc.

Executive directors and executive: They will make very tough decision regarding how to

take the company global which basically involve high amount of business as well as

professional risks (Yulianto and Pratiwi, 2019).

Managers: The managers are also decision-makers of Tesco company because they need

to make the decision regarding budgets, identify problems and conflicts among staffs,

suggesting alternative to solve the same etc. They are also entitling for establishing

control and evaluation system within the business.

In this way, the internal staffs of the company are considered as a decision-maker and make

the decision for the growth of the company (Quinn and et.al., 2019). They decision involve

various risk but with their skills, experience and expertise the company will make the decision

for the welfare of business. Their decision also involves the buy and in house production

decision.

PART B

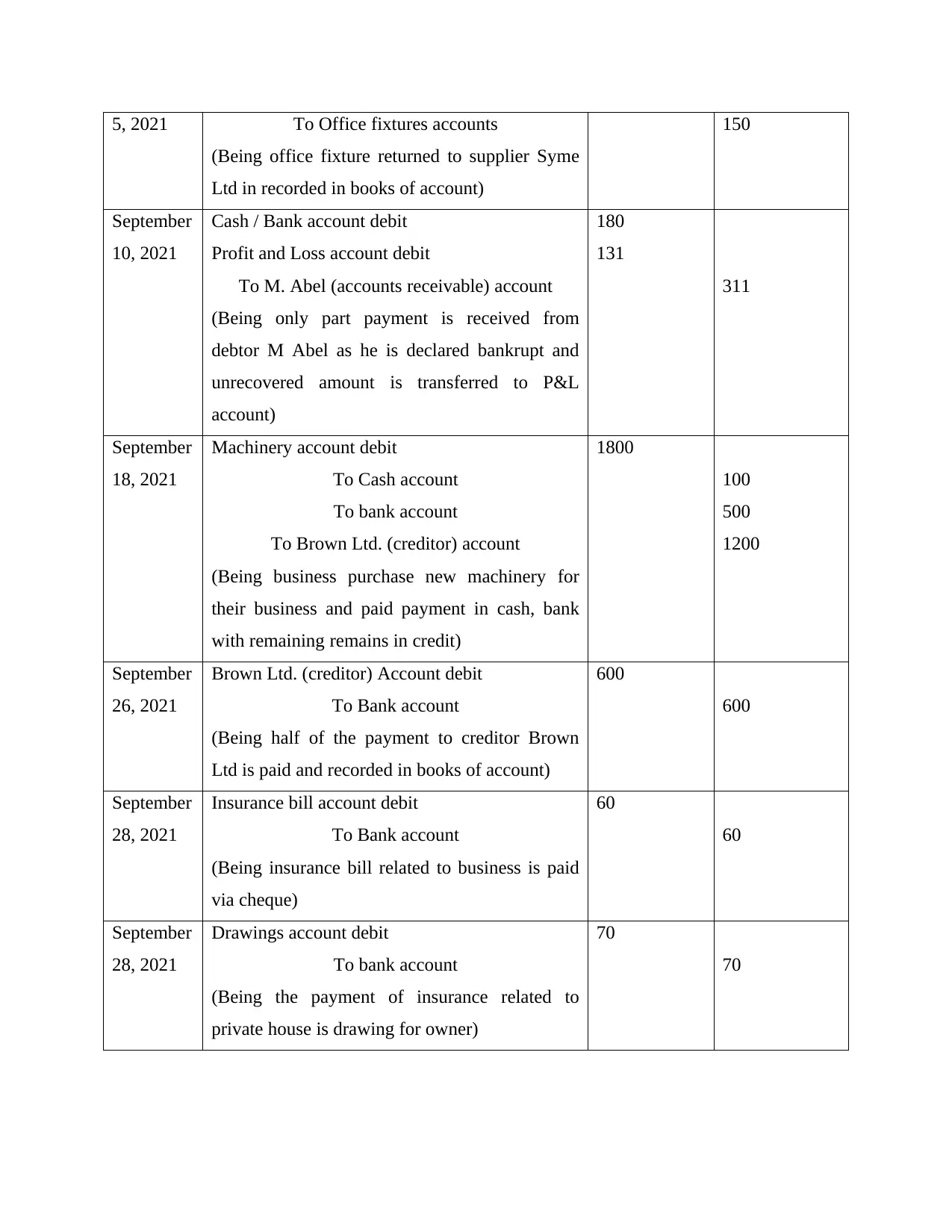

(1) Recording necessary Journal entries in the books of Bakery business of F Polk

Journal Entries in the book of F Polk

For the month of September 2021

Date Particulars Debit (£) Credit (£)

September

1, 2021

Bad debt expenses account debit

To P Mullen (accounts receivable) account

(Being debt owing to P Mullen was written off

as bad debt in the books of account)

105

105

September Syme Ltd. (creditors) account debit 150

hiring and firing of personnel, dividend policies, pay-outs and executive compensations

(Weigand, Blums and de Kruijff, 2020).

Chairman and Managing director: They need to take the decision regarding the ways

with the help of which meetings will run smoothly and remain orderly. They also need to

organize and coordinate meetings by setting annual agenda etc.

Executive directors and executive: They will make very tough decision regarding how to

take the company global which basically involve high amount of business as well as

professional risks (Yulianto and Pratiwi, 2019).

Managers: The managers are also decision-makers of Tesco company because they need

to make the decision regarding budgets, identify problems and conflicts among staffs,

suggesting alternative to solve the same etc. They are also entitling for establishing

control and evaluation system within the business.

In this way, the internal staffs of the company are considered as a decision-maker and make

the decision for the growth of the company (Quinn and et.al., 2019). They decision involve

various risk but with their skills, experience and expertise the company will make the decision

for the welfare of business. Their decision also involves the buy and in house production

decision.

PART B

(1) Recording necessary Journal entries in the books of Bakery business of F Polk

Journal Entries in the book of F Polk

For the month of September 2021

Date Particulars Debit (£) Credit (£)

September

1, 2021

Bad debt expenses account debit

To P Mullen (accounts receivable) account

(Being debt owing to P Mullen was written off

as bad debt in the books of account)

105

105

September Syme Ltd. (creditors) account debit 150

5, 2021 To Office fixtures accounts

(Being office fixture returned to supplier Syme

Ltd in recorded in books of account)

150

September

10, 2021

Cash / Bank account debit

Profit and Loss account debit

To M. Abel (accounts receivable) account

(Being only part payment is received from

debtor M Abel as he is declared bankrupt and

unrecovered amount is transferred to P&L

account)

180

131

311

September

18, 2021

Machinery account debit

To Cash account

To bank account

To Brown Ltd. (creditor) account

(Being business purchase new machinery for

their business and paid payment in cash, bank

with remaining remains in credit)

1800

100

500

1200

September

26, 2021

Brown Ltd. (creditor) Account debit

To Bank account

(Being half of the payment to creditor Brown

Ltd is paid and recorded in books of account)

600

600

September

28, 2021

Insurance bill account debit

To Bank account

(Being insurance bill related to business is paid

via cheque)

60

60

September

28, 2021

Drawings account debit

To bank account

(Being the payment of insurance related to

private house is drawing for owner)

70

70

(Being office fixture returned to supplier Syme

Ltd in recorded in books of account)

150

September

10, 2021

Cash / Bank account debit

Profit and Loss account debit

To M. Abel (accounts receivable) account

(Being only part payment is received from

debtor M Abel as he is declared bankrupt and

unrecovered amount is transferred to P&L

account)

180

131

311

September

18, 2021

Machinery account debit

To Cash account

To bank account

To Brown Ltd. (creditor) account

(Being business purchase new machinery for

their business and paid payment in cash, bank

with remaining remains in credit)

1800

100

500

1200

September

26, 2021

Brown Ltd. (creditor) Account debit

To Bank account

(Being half of the payment to creditor Brown

Ltd is paid and recorded in books of account)

600

600

September

28, 2021

Insurance bill account debit

To Bank account

(Being insurance bill related to business is paid

via cheque)

60

60

September

28, 2021

Drawings account debit

To bank account

(Being the payment of insurance related to

private house is drawing for owner)

70

70

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

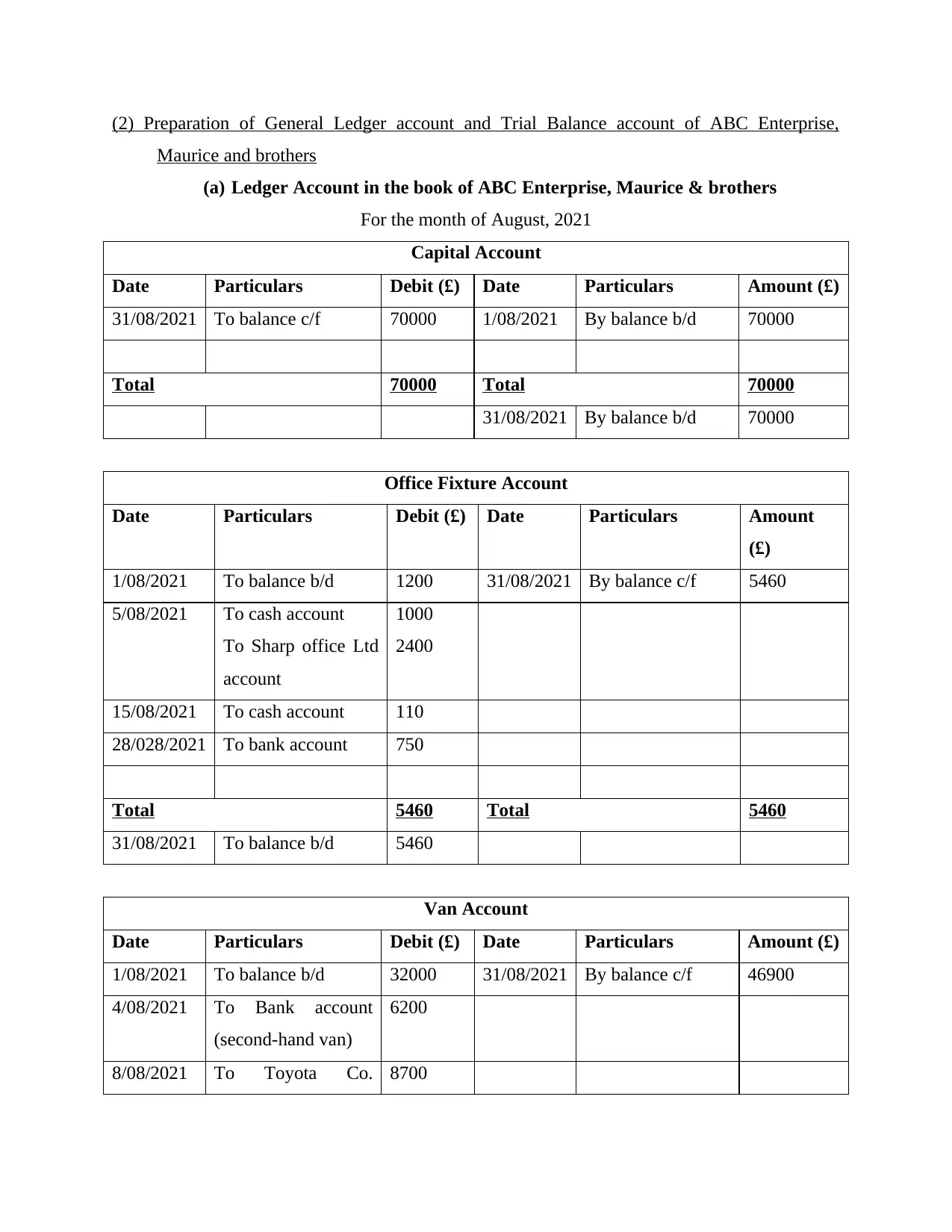

(2) Preparation of General Ledger account and Trial Balance account of ABC Enterprise,

Maurice and brothers

(a) Ledger Account in the book of ABC Enterprise, Maurice & brothers

For the month of August, 2021

Capital Account

Date Particulars Debit (£) Date Particulars Amount (£)

31/08/2021 To balance c/f 70000 1/08/2021 By balance b/d 70000

Total 70000 Total 70000

31/08/2021 By balance b/d 70000

Office Fixture Account

Date Particulars Debit (£) Date Particulars Amount

(£)

1/08/2021 To balance b/d 1200 31/08/2021 By balance c/f 5460

5/08/2021 To cash account

To Sharp office Ltd

account

1000

2400

15/08/2021 To cash account 110

28/028/2021 To bank account 750

Total 5460 Total 5460

31/08/2021 To balance b/d 5460

Van Account

Date Particulars Debit (£) Date Particulars Amount (£)

1/08/2021 To balance b/d 32000 31/08/2021 By balance c/f 46900

4/08/2021 To Bank account

(second-hand van)

6200

8/08/2021 To Toyota Co. 8700

Maurice and brothers

(a) Ledger Account in the book of ABC Enterprise, Maurice & brothers

For the month of August, 2021

Capital Account

Date Particulars Debit (£) Date Particulars Amount (£)

31/08/2021 To balance c/f 70000 1/08/2021 By balance b/d 70000

Total 70000 Total 70000

31/08/2021 By balance b/d 70000

Office Fixture Account

Date Particulars Debit (£) Date Particulars Amount

(£)

1/08/2021 To balance b/d 1200 31/08/2021 By balance c/f 5460

5/08/2021 To cash account

To Sharp office Ltd

account

1000

2400

15/08/2021 To cash account 110

28/028/2021 To bank account 750

Total 5460 Total 5460

31/08/2021 To balance b/d 5460

Van Account

Date Particulars Debit (£) Date Particulars Amount (£)

1/08/2021 To balance b/d 32000 31/08/2021 By balance c/f 46900

4/08/2021 To Bank account

(second-hand van)

6200

8/08/2021 To Toyota Co. 8700

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

account

Total 46900 Total 46900

31/08/2021 To balance b/d 46900

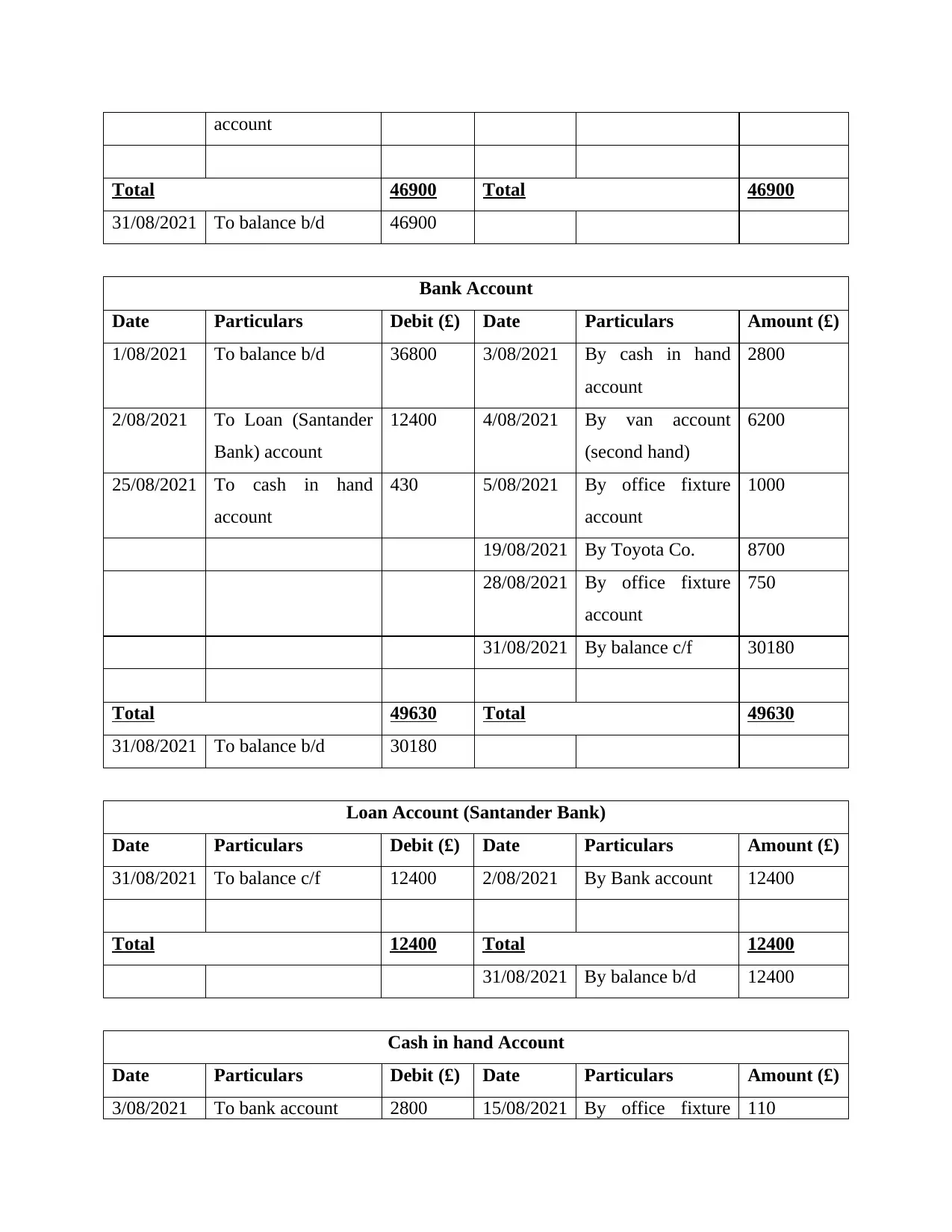

Bank Account

Date Particulars Debit (£) Date Particulars Amount (£)

1/08/2021 To balance b/d 36800 3/08/2021 By cash in hand

account

2800

2/08/2021 To Loan (Santander

Bank) account

12400 4/08/2021 By van account

(second hand)

6200

25/08/2021 To cash in hand

account

430 5/08/2021 By office fixture

account

1000

19/08/2021 By Toyota Co. 8700

28/08/2021 By office fixture

account

750

31/08/2021 By balance c/f 30180

Total 49630 Total 49630

31/08/2021 To balance b/d 30180

Loan Account (Santander Bank)

Date Particulars Debit (£) Date Particulars Amount (£)

31/08/2021 To balance c/f 12400 2/08/2021 By Bank account 12400

Total 12400 Total 12400

31/08/2021 By balance b/d 12400

Cash in hand Account

Date Particulars Debit (£) Date Particulars Amount (£)

3/08/2021 To bank account 2800 15/08/2021 By office fixture 110

Total 46900 Total 46900

31/08/2021 To balance b/d 46900

Bank Account

Date Particulars Debit (£) Date Particulars Amount (£)

1/08/2021 To balance b/d 36800 3/08/2021 By cash in hand

account

2800

2/08/2021 To Loan (Santander

Bank) account

12400 4/08/2021 By van account

(second hand)

6200

25/08/2021 To cash in hand

account

430 5/08/2021 By office fixture

account

1000

19/08/2021 By Toyota Co. 8700

28/08/2021 By office fixture

account

750

31/08/2021 By balance c/f 30180

Total 49630 Total 49630

31/08/2021 To balance b/d 30180

Loan Account (Santander Bank)

Date Particulars Debit (£) Date Particulars Amount (£)

31/08/2021 To balance c/f 12400 2/08/2021 By Bank account 12400

Total 12400 Total 12400

31/08/2021 By balance b/d 12400

Cash in hand Account

Date Particulars Debit (£) Date Particulars Amount (£)

3/08/2021 To bank account 2800 15/08/2021 By office fixture 110

account

25/08/2021 By bank account 430

31/08/2021 By balance c/f 2260

Total 2800 Total 2800

31/08/2021 To balance b/d 2260

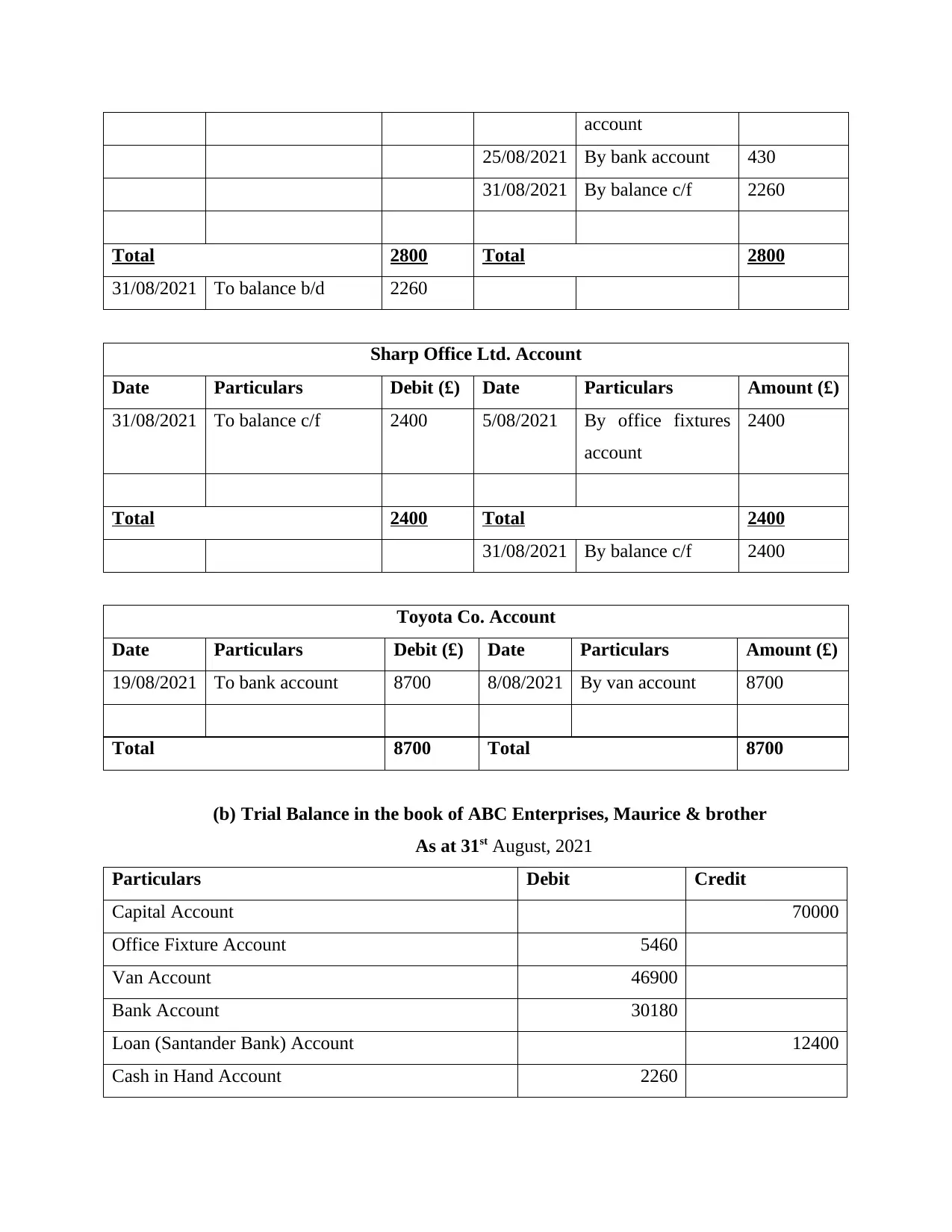

Sharp Office Ltd. Account

Date Particulars Debit (£) Date Particulars Amount (£)

31/08/2021 To balance c/f 2400 5/08/2021 By office fixtures

account

2400

Total 2400 Total 2400

31/08/2021 By balance c/f 2400

Toyota Co. Account

Date Particulars Debit (£) Date Particulars Amount (£)

19/08/2021 To bank account 8700 8/08/2021 By van account 8700

Total 8700 Total 8700

(b) Trial Balance in the book of ABC Enterprises, Maurice & brother

As at 31st August, 2021

Particulars Debit Credit

Capital Account 70000

Office Fixture Account 5460

Van Account 46900

Bank Account 30180

Loan (Santander Bank) Account 12400

Cash in Hand Account 2260

25/08/2021 By bank account 430

31/08/2021 By balance c/f 2260

Total 2800 Total 2800

31/08/2021 To balance b/d 2260

Sharp Office Ltd. Account

Date Particulars Debit (£) Date Particulars Amount (£)

31/08/2021 To balance c/f 2400 5/08/2021 By office fixtures

account

2400

Total 2400 Total 2400

31/08/2021 By balance c/f 2400

Toyota Co. Account

Date Particulars Debit (£) Date Particulars Amount (£)

19/08/2021 To bank account 8700 8/08/2021 By van account 8700

Total 8700 Total 8700

(b) Trial Balance in the book of ABC Enterprises, Maurice & brother

As at 31st August, 2021

Particulars Debit Credit

Capital Account 70000

Office Fixture Account 5460

Van Account 46900

Bank Account 30180

Loan (Santander Bank) Account 12400

Cash in Hand Account 2260

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

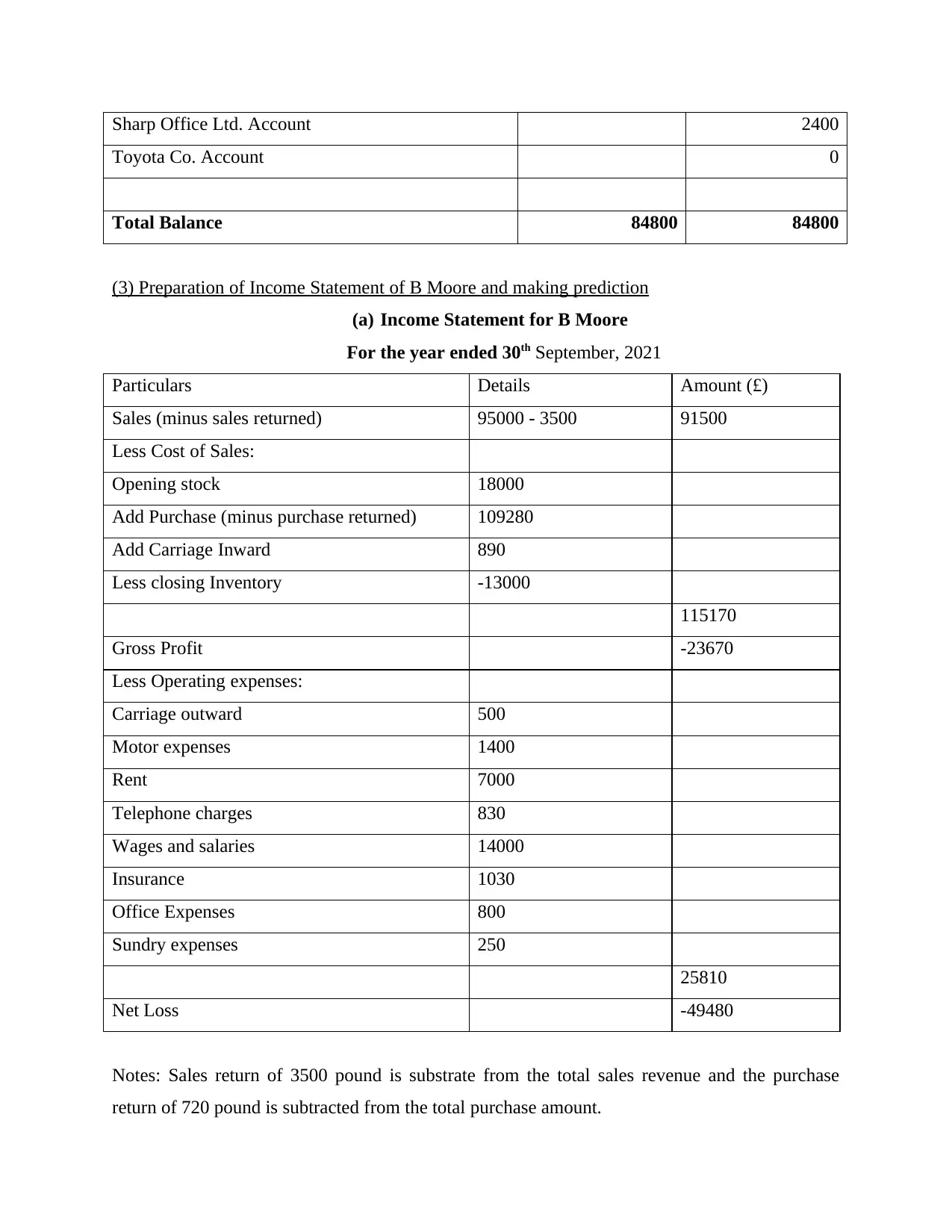

Sharp Office Ltd. Account 2400

Toyota Co. Account 0

Total Balance 84800 84800

(3) Preparation of Income Statement of B Moore and making prediction

(a) Income Statement for B Moore

For the year ended 30th September, 2021

Particulars Details Amount (£)

Sales (minus sales returned) 95000 - 3500 91500

Less Cost of Sales:

Opening stock 18000

Add Purchase (minus purchase returned) 109280

Add Carriage Inward 890

Less closing Inventory -13000

115170

Gross Profit -23670

Less Operating expenses:

Carriage outward 500

Motor expenses 1400

Rent 7000

Telephone charges 830

Wages and salaries 14000

Insurance 1030

Office Expenses 800

Sundry expenses 250

25810

Net Loss -49480

Notes: Sales return of 3500 pound is substrate from the total sales revenue and the purchase

return of 720 pound is subtracted from the total purchase amount.

Toyota Co. Account 0

Total Balance 84800 84800

(3) Preparation of Income Statement of B Moore and making prediction

(a) Income Statement for B Moore

For the year ended 30th September, 2021

Particulars Details Amount (£)

Sales (minus sales returned) 95000 - 3500 91500

Less Cost of Sales:

Opening stock 18000

Add Purchase (minus purchase returned) 109280

Add Carriage Inward 890

Less closing Inventory -13000

115170

Gross Profit -23670

Less Operating expenses:

Carriage outward 500

Motor expenses 1400

Rent 7000

Telephone charges 830

Wages and salaries 14000

Insurance 1030

Office Expenses 800

Sundry expenses 250

25810

Net Loss -49480

Notes: Sales return of 3500 pound is substrate from the total sales revenue and the purchase

return of 720 pound is subtracted from the total purchase amount.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

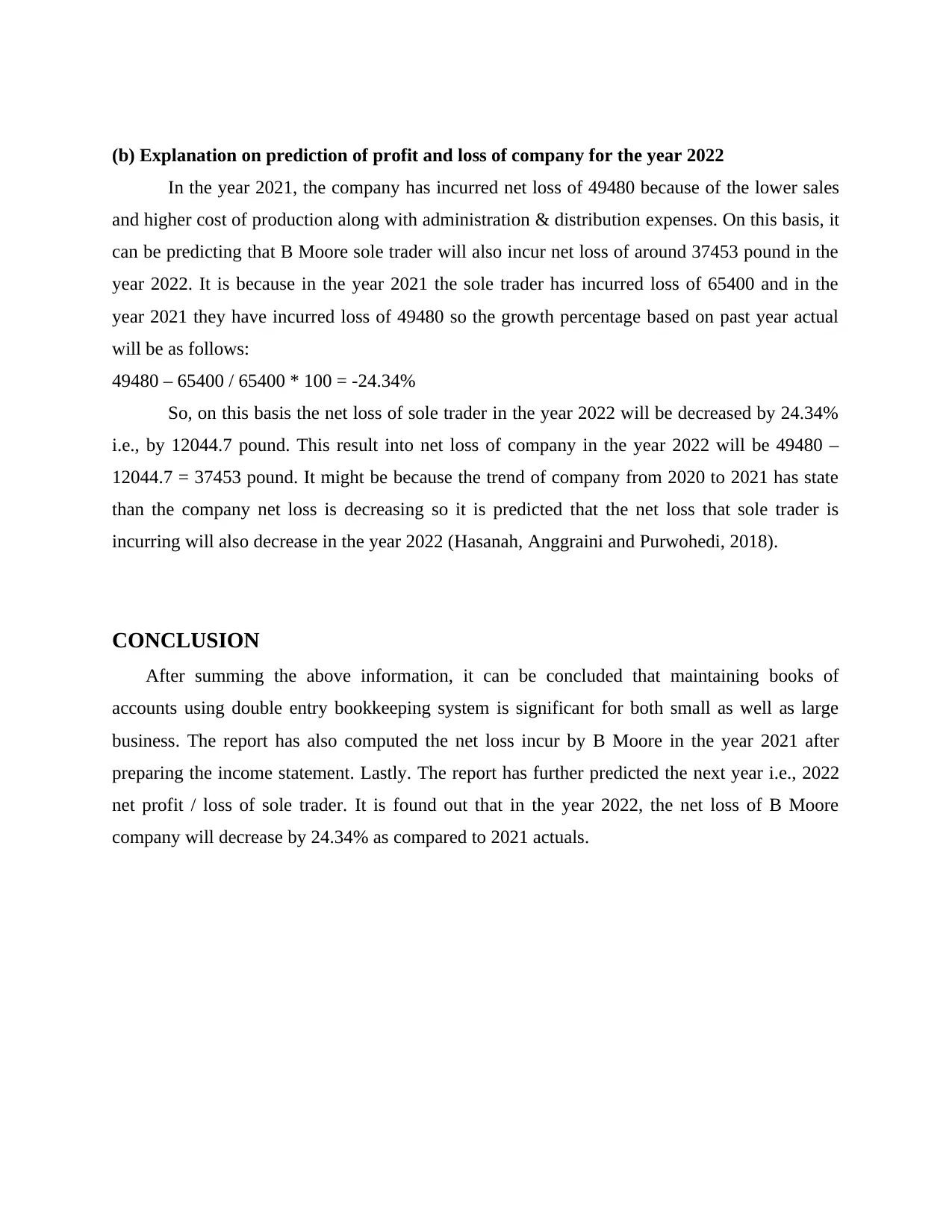

(b) Explanation on prediction of profit and loss of company for the year 2022

In the year 2021, the company has incurred net loss of 49480 because of the lower sales

and higher cost of production along with administration & distribution expenses. On this basis, it

can be predicting that B Moore sole trader will also incur net loss of around 37453 pound in the

year 2022. It is because in the year 2021 the sole trader has incurred loss of 65400 and in the

year 2021 they have incurred loss of 49480 so the growth percentage based on past year actual

will be as follows:

49480 – 65400 / 65400 * 100 = -24.34%

So, on this basis the net loss of sole trader in the year 2022 will be decreased by 24.34%

i.e., by 12044.7 pound. This result into net loss of company in the year 2022 will be 49480 –

12044.7 = 37453 pound. It might be because the trend of company from 2020 to 2021 has state

than the company net loss is decreasing so it is predicted that the net loss that sole trader is

incurring will also decrease in the year 2022 (Hasanah, Anggraini and Purwohedi, 2018).

CONCLUSION

After summing the above information, it can be concluded that maintaining books of

accounts using double entry bookkeeping system is significant for both small as well as large

business. The report has also computed the net loss incur by B Moore in the year 2021 after

preparing the income statement. Lastly. The report has further predicted the next year i.e., 2022

net profit / loss of sole trader. It is found out that in the year 2022, the net loss of B Moore

company will decrease by 24.34% as compared to 2021 actuals.

In the year 2021, the company has incurred net loss of 49480 because of the lower sales

and higher cost of production along with administration & distribution expenses. On this basis, it

can be predicting that B Moore sole trader will also incur net loss of around 37453 pound in the

year 2022. It is because in the year 2021 the sole trader has incurred loss of 65400 and in the

year 2021 they have incurred loss of 49480 so the growth percentage based on past year actual

will be as follows:

49480 – 65400 / 65400 * 100 = -24.34%

So, on this basis the net loss of sole trader in the year 2022 will be decreased by 24.34%

i.e., by 12044.7 pound. This result into net loss of company in the year 2022 will be 49480 –

12044.7 = 37453 pound. It might be because the trend of company from 2020 to 2021 has state

than the company net loss is decreasing so it is predicted that the net loss that sole trader is

incurring will also decrease in the year 2022 (Hasanah, Anggraini and Purwohedi, 2018).

CONCLUSION

After summing the above information, it can be concluded that maintaining books of

accounts using double entry bookkeeping system is significant for both small as well as large

business. The report has also computed the net loss incur by B Moore in the year 2021 after

preparing the income statement. Lastly. The report has further predicted the next year i.e., 2022

net profit / loss of sole trader. It is found out that in the year 2022, the net loss of B Moore

company will decrease by 24.34% as compared to 2021 actuals.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.