Recording Transactions: Double Entry Bookkeeping & Ledgers

VerifiedAdded on 2023/06/09

|20

|4336

|237

Report

AI Summary

This report provides a comprehensive overview of bookkeeping principles and practices, focusing on the accurate and timely recording of financial transactions. It begins with an explanation of double-entry bookkeeping, detailing the steps involved in recording transactions, updating accounts, and preparing financial statements. The report then demonstrates the implementation of various business transactions using books of prime entry, ledgers, and journals, including purchases, sales, capital investments, and expense payments, with detailed journal entries and ledger postings. Furthermore, it covers the extraction of ledger balances into a trial balance to ensure the accuracy of recorded transactions and the development of a bank reconciliation statement to reconcile bank-related entries and identify errors. Finally, the report differentiates between suspense and control accounts and performs control account reconciliation for accounts receivable and payable, providing a thorough understanding of essential bookkeeping concepts and their practical application in managing financial records.

UNIT 10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION...........................................................................................................................3

TASK...............................................................................................................................................3

P1. How to record double entry bookkeeping transactions in a timely and accurate way..........3

P2 Implement a range of business transactions with the help of books of prime entry, double

entry bookkeeping, ledgers and journals.....................................................................................4

P3. With the help of data provided, extract ledger balance into a trail balance fir a company to

accurately record transactions....................................................................................................12

P4. Develop a bank reconciliation statement with the help of give information for a company.

...................................................................................................................................................13

P5. State the differences and role among suspense and control accounts.................................15

P6. Perform control account reconciliation for accounts receivable and payable from given

data.............................................................................................................................................17

CONCLUSION..............................................................................................................................18

REFERENCES..............................................................................................................................19

INTRODUCTION...........................................................................................................................3

TASK...............................................................................................................................................3

P1. How to record double entry bookkeeping transactions in a timely and accurate way..........3

P2 Implement a range of business transactions with the help of books of prime entry, double

entry bookkeeping, ledgers and journals.....................................................................................4

P3. With the help of data provided, extract ledger balance into a trail balance fir a company to

accurately record transactions....................................................................................................12

P4. Develop a bank reconciliation statement with the help of give information for a company.

...................................................................................................................................................13

P5. State the differences and role among suspense and control accounts.................................15

P6. Perform control account reconciliation for accounts receivable and payable from given

data.............................................................................................................................................17

CONCLUSION..............................................................................................................................18

REFERENCES..............................................................................................................................19

INTRODUCTION

The report prepared as under takes in account the explanation of Bookkeeping which can be

explained as recording of all finance based transactions which include sales, purchase, payment

and receipts. In the report as under, transactions can be recorded in a chronological order which

would serve as a better technique and method to understand terms in a better way. Ledger

accounts and trial balances would be developed and prepared for showing accurate and reliable

way for recording entries as well as transactions. In addition, bank reconciliation statement

reflects bank related entries and identify errors & omissions being made. It also takes into

account suspense and control account which would be differentiated and performed for accounts

payable and receivable as well (Aleksieva, Valchanov and Huliyan, 2020).

TASK

P1. How to record double entry bookkeeping transactions in a timely and accurate way.

Double Entry bookkeeping is a way of recording the transaction into the books of account

in which at least two accounts get affected one is debit and another one is credit and also have

the same amount.

Double entry bookkeeping contain a process which are as follows-

Produce document: The very first step of double entry bookkeeping is producing a

document which is generally known as invoice. In this document all the information

related to product and the costumer are included like all the items which consumer

purchase from the seller, date of the transaction, address and name of the customer, and

the last amount payable by the customer for purchasing the product.

Recording: The next step of double entry bookkeeping is the recording of the transaction

in the books of accounts by the help of the document which is known as invoice consist

all the information like date, amount, invoice no, and address of the customer, some of

the information from invoice are used in recording the transaction like name, amount and

date.

Update accounts: Each and every account have a separate ledger which contain

information like date and amount. These ledgers may contain various transaction and all

these have to be verified by the accountant of the organisation and if any error is found

The report prepared as under takes in account the explanation of Bookkeeping which can be

explained as recording of all finance based transactions which include sales, purchase, payment

and receipts. In the report as under, transactions can be recorded in a chronological order which

would serve as a better technique and method to understand terms in a better way. Ledger

accounts and trial balances would be developed and prepared for showing accurate and reliable

way for recording entries as well as transactions. In addition, bank reconciliation statement

reflects bank related entries and identify errors & omissions being made. It also takes into

account suspense and control account which would be differentiated and performed for accounts

payable and receivable as well (Aleksieva, Valchanov and Huliyan, 2020).

TASK

P1. How to record double entry bookkeeping transactions in a timely and accurate way.

Double Entry bookkeeping is a way of recording the transaction into the books of account

in which at least two accounts get affected one is debit and another one is credit and also have

the same amount.

Double entry bookkeeping contain a process which are as follows-

Produce document: The very first step of double entry bookkeeping is producing a

document which is generally known as invoice. In this document all the information

related to product and the costumer are included like all the items which consumer

purchase from the seller, date of the transaction, address and name of the customer, and

the last amount payable by the customer for purchasing the product.

Recording: The next step of double entry bookkeeping is the recording of the transaction

in the books of accounts by the help of the document which is known as invoice consist

all the information like date, amount, invoice no, and address of the customer, some of

the information from invoice are used in recording the transaction like name, amount and

date.

Update accounts: Each and every account have a separate ledger which contain

information like date and amount. These ledgers may contain various transaction and all

these have to be verified by the accountant of the organisation and if any error is found

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

then, it has been update through this activity the accounts can be accurate (Baralla and

et.al., 2021).

Debit and Credit: In double entry bookkeeping every transaction have equal debit and

equal credit and if any mistake is done by the organisation then the accounts will not

match so the organisation have to be efficient and focused while recording the

transactions. It helps the organisation to make the business decision if the accounts are

accurate.

Chart of accounts: It refers to the statements in which all transaction related to the

businesses are recorded. It shows the accounts that are needed for running a business and

to prepare financial statements.

Mathematical formula of double entry: It is known as the accounting equation which is

used to maintain the structure of the ledger. The accounting equation is Capital = Assets-

liabilities.

Preparation of Trial Balance: Trail consist all the accounts of the ledgers with their

respective debit and credit balance. It helps the organisation to evaluate all accounts and

rectify those accounts if they have any kind of error.

Preparation of Financial Statements: After preparing trail balance organisations have to

prepare the financial statements of the business which are profit and loss account,

balance-sheet, cash-flow statements and notes to accounts all these accounts and

statements helps the organisation to access the financial position of the business. Like

profit and loss account shows the income and expenditure during the accounting period,

balance-sheet shows the all assets and liabilities of the business, cash flow statement

shows the net inflow and outflow of the cash and Notes to account helps the investors to

understand the financial position of the organisation (Chari, 2022).

P2 Implement a range of business transactions with the help of books of prime entry, double

entry bookkeeping, ledgers and journals.

1. Journals: It is an account which considers all the finance based transactions which are

connected with accounts used for future reconciling and transfer of data such as general

ledger. It consists of the amount of transaction and date which would be a short

description. Main information which is included in journals can be explained as expenses,

sales, inventory, debts and cash. Such transactions would be recorded on a daily basis

et.al., 2021).

Debit and Credit: In double entry bookkeeping every transaction have equal debit and

equal credit and if any mistake is done by the organisation then the accounts will not

match so the organisation have to be efficient and focused while recording the

transactions. It helps the organisation to make the business decision if the accounts are

accurate.

Chart of accounts: It refers to the statements in which all transaction related to the

businesses are recorded. It shows the accounts that are needed for running a business and

to prepare financial statements.

Mathematical formula of double entry: It is known as the accounting equation which is

used to maintain the structure of the ledger. The accounting equation is Capital = Assets-

liabilities.

Preparation of Trial Balance: Trail consist all the accounts of the ledgers with their

respective debit and credit balance. It helps the organisation to evaluate all accounts and

rectify those accounts if they have any kind of error.

Preparation of Financial Statements: After preparing trail balance organisations have to

prepare the financial statements of the business which are profit and loss account,

balance-sheet, cash-flow statements and notes to accounts all these accounts and

statements helps the organisation to access the financial position of the business. Like

profit and loss account shows the income and expenditure during the accounting period,

balance-sheet shows the all assets and liabilities of the business, cash flow statement

shows the net inflow and outflow of the cash and Notes to account helps the investors to

understand the financial position of the organisation (Chari, 2022).

P2 Implement a range of business transactions with the help of books of prime entry, double

entry bookkeeping, ledgers and journals.

1. Journals: It is an account which considers all the finance based transactions which are

connected with accounts used for future reconciling and transfer of data such as general

ledger. It consists of the amount of transaction and date which would be a short

description. Main information which is included in journals can be explained as expenses,

sales, inventory, debts and cash. Such transactions would be recorded on a daily basis

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

because the guess work later might lead to errors and issues (Gerrits, Kromes and

Verdier, 2020).

2. Ledgers: It can be explained as a record or account which is used for storing book

keeping entries which could later be used for income statements and balance sheets as

well. Posting to a ledger can be explained as a procedure to record debit and credit sides.

A ledger is a account where all the accounting entries are being taken into consideration.

3. Double entry book keeping: It can be explained as a concept which is used in present day

book keeping which can be stated as financial transaction which is recorded in two

different ledger accounts for once on credit side and on debit side as well for satisfying

the accounting equation developed.

Accounting equation: Assets = Equity + Liabilities

The double entry book keeping standardises the accounting procedure and improve the accuracy

of financial records and also minimizing the errors as well. For instance, if a company has taken

any loan amount from banking institutions the borrowed fund would raise the liability and asset

of the enterprise as well i.e. there will be a rise in cash funds at bank and also increase in long

term liabilities as well.

4. Book of prime entry: It can be defined as a book where the entries are being recorded and

taken into account before entering into double entry system. These books consider cash

book, daybook and journal as well. For cross checking the transactions, looking after the

ledgers would be tedious task so rather prime books are being used for searching the data

and information. It would further provide a chronological record and errors; mistakes can

be identified in a simpler form. It can also be adapted for future references and providing

backup in case anything goes wrong or renders unplanned results with books of accounts.

Following is the list of business related transactions:

1. Purchased a home for £5400 on 2nd October.

2. Sold goods having a worth of £2800 on 5th October.

3. Capital invested in business enterprise £71800 dividend among cash, car, flat and back

with amounts 4800, 12000, 45000 and 10000 respectively on 1st October 2021.

4. Purchased a printer and computer for £200 and £800 respectively on 4th October.

5. Received rent of £800 on 21st October.

6. Paid £110 for repairs on 12th October.

Verdier, 2020).

2. Ledgers: It can be explained as a record or account which is used for storing book

keeping entries which could later be used for income statements and balance sheets as

well. Posting to a ledger can be explained as a procedure to record debit and credit sides.

A ledger is a account where all the accounting entries are being taken into consideration.

3. Double entry book keeping: It can be explained as a concept which is used in present day

book keeping which can be stated as financial transaction which is recorded in two

different ledger accounts for once on credit side and on debit side as well for satisfying

the accounting equation developed.

Accounting equation: Assets = Equity + Liabilities

The double entry book keeping standardises the accounting procedure and improve the accuracy

of financial records and also minimizing the errors as well. For instance, if a company has taken

any loan amount from banking institutions the borrowed fund would raise the liability and asset

of the enterprise as well i.e. there will be a rise in cash funds at bank and also increase in long

term liabilities as well.

4. Book of prime entry: It can be defined as a book where the entries are being recorded and

taken into account before entering into double entry system. These books consider cash

book, daybook and journal as well. For cross checking the transactions, looking after the

ledgers would be tedious task so rather prime books are being used for searching the data

and information. It would further provide a chronological record and errors; mistakes can

be identified in a simpler form. It can also be adapted for future references and providing

backup in case anything goes wrong or renders unplanned results with books of accounts.

Following is the list of business related transactions:

1. Purchased a home for £5400 on 2nd October.

2. Sold goods having a worth of £2800 on 5th October.

3. Capital invested in business enterprise £71800 dividend among cash, car, flat and back

with amounts 4800, 12000, 45000 and 10000 respectively on 1st October 2021.

4. Purchased a printer and computer for £200 and £800 respectively on 4th October.

5. Received rent of £800 on 21st October.

6. Paid £110 for repairs on 12th October.

7. Sold goods worth £300 on credit and £1800 to Rayan in cash on 23rd October.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

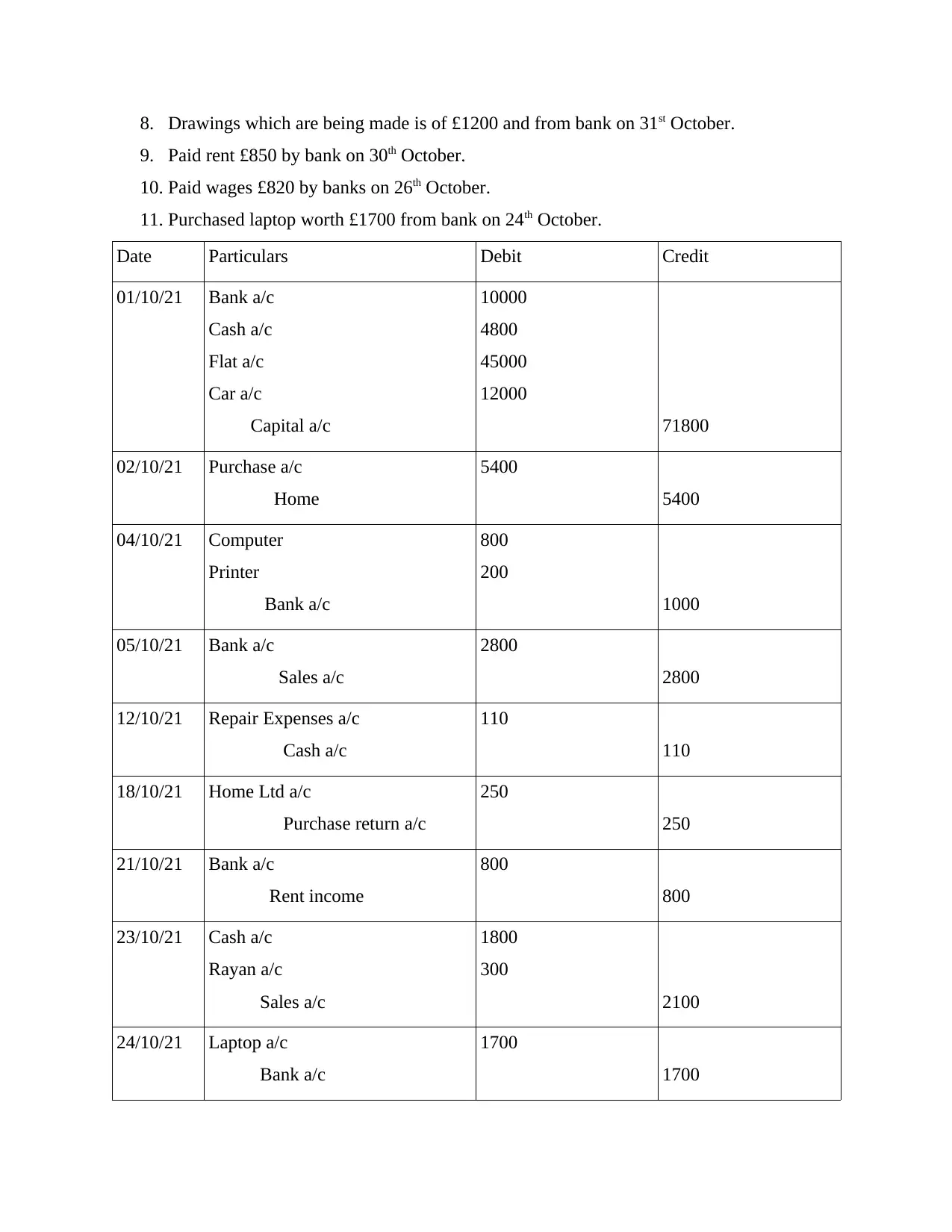

8. Drawings which are being made is of £1200 and from bank on 31st October.

9. Paid rent £850 by bank on 30th October.

10. Paid wages £820 by banks on 26th October.

11. Purchased laptop worth £1700 from bank on 24th October.

Date Particulars Debit Credit

01/10/21 Bank a/c

Cash a/c

Flat a/c

Car a/c

Capital a/c

10000

4800

45000

12000

71800

02/10/21 Purchase a/c

Home

5400

5400

04/10/21 Computer

Printer

Bank a/c

800

200

1000

05/10/21 Bank a/c

Sales a/c

2800

2800

12/10/21 Repair Expenses a/c

Cash a/c

110

110

18/10/21 Home Ltd a/c

Purchase return a/c

250

250

21/10/21 Bank a/c

Rent income

800

800

23/10/21 Cash a/c

Rayan a/c

Sales a/c

1800

300

2100

24/10/21 Laptop a/c

Bank a/c

1700

1700

9. Paid rent £850 by bank on 30th October.

10. Paid wages £820 by banks on 26th October.

11. Purchased laptop worth £1700 from bank on 24th October.

Date Particulars Debit Credit

01/10/21 Bank a/c

Cash a/c

Flat a/c

Car a/c

Capital a/c

10000

4800

45000

12000

71800

02/10/21 Purchase a/c

Home

5400

5400

04/10/21 Computer

Printer

Bank a/c

800

200

1000

05/10/21 Bank a/c

Sales a/c

2800

2800

12/10/21 Repair Expenses a/c

Cash a/c

110

110

18/10/21 Home Ltd a/c

Purchase return a/c

250

250

21/10/21 Bank a/c

Rent income

800

800

23/10/21 Cash a/c

Rayan a/c

Sales a/c

1800

300

2100

24/10/21 Laptop a/c

Bank a/c

1700

1700

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

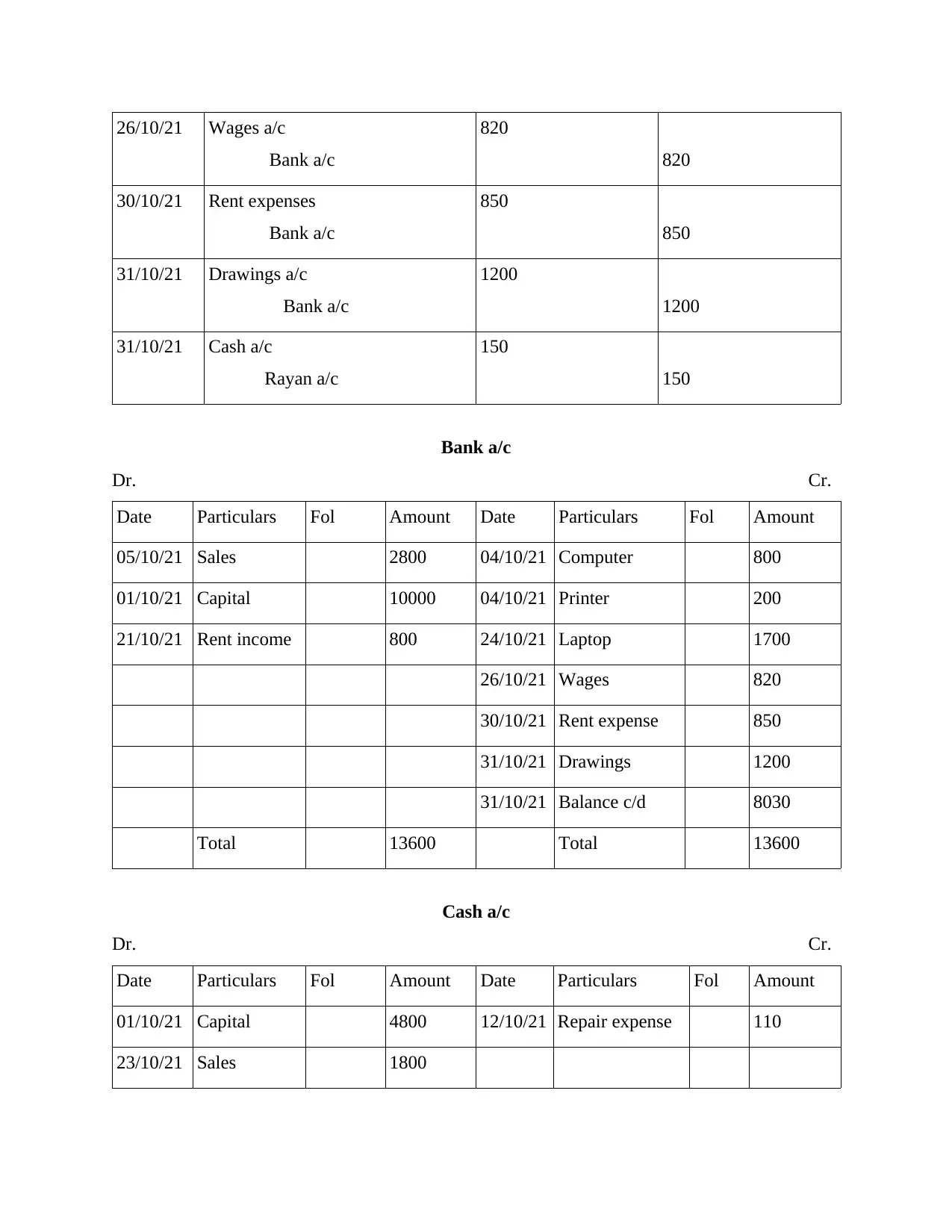

26/10/21 Wages a/c

Bank a/c

820

820

30/10/21 Rent expenses

Bank a/c

850

850

31/10/21 Drawings a/c

Bank a/c

1200

1200

31/10/21 Cash a/c

Rayan a/c

150

150

Bank a/c

Dr. Cr.

Date Particulars Fol Amount Date Particulars Fol Amount

05/10/21 Sales 2800 04/10/21 Computer 800

01/10/21 Capital 10000 04/10/21 Printer 200

21/10/21 Rent income 800 24/10/21 Laptop 1700

26/10/21 Wages 820

30/10/21 Rent expense 850

31/10/21 Drawings 1200

31/10/21 Balance c/d 8030

Total 13600 Total 13600

Cash a/c

Dr. Cr.

Date Particulars Fol Amount Date Particulars Fol Amount

01/10/21 Capital 4800 12/10/21 Repair expense 110

23/10/21 Sales 1800

Bank a/c

820

820

30/10/21 Rent expenses

Bank a/c

850

850

31/10/21 Drawings a/c

Bank a/c

1200

1200

31/10/21 Cash a/c

Rayan a/c

150

150

Bank a/c

Dr. Cr.

Date Particulars Fol Amount Date Particulars Fol Amount

05/10/21 Sales 2800 04/10/21 Computer 800

01/10/21 Capital 10000 04/10/21 Printer 200

21/10/21 Rent income 800 24/10/21 Laptop 1700

26/10/21 Wages 820

30/10/21 Rent expense 850

31/10/21 Drawings 1200

31/10/21 Balance c/d 8030

Total 13600 Total 13600

Cash a/c

Dr. Cr.

Date Particulars Fol Amount Date Particulars Fol Amount

01/10/21 Capital 4800 12/10/21 Repair expense 110

23/10/21 Sales 1800

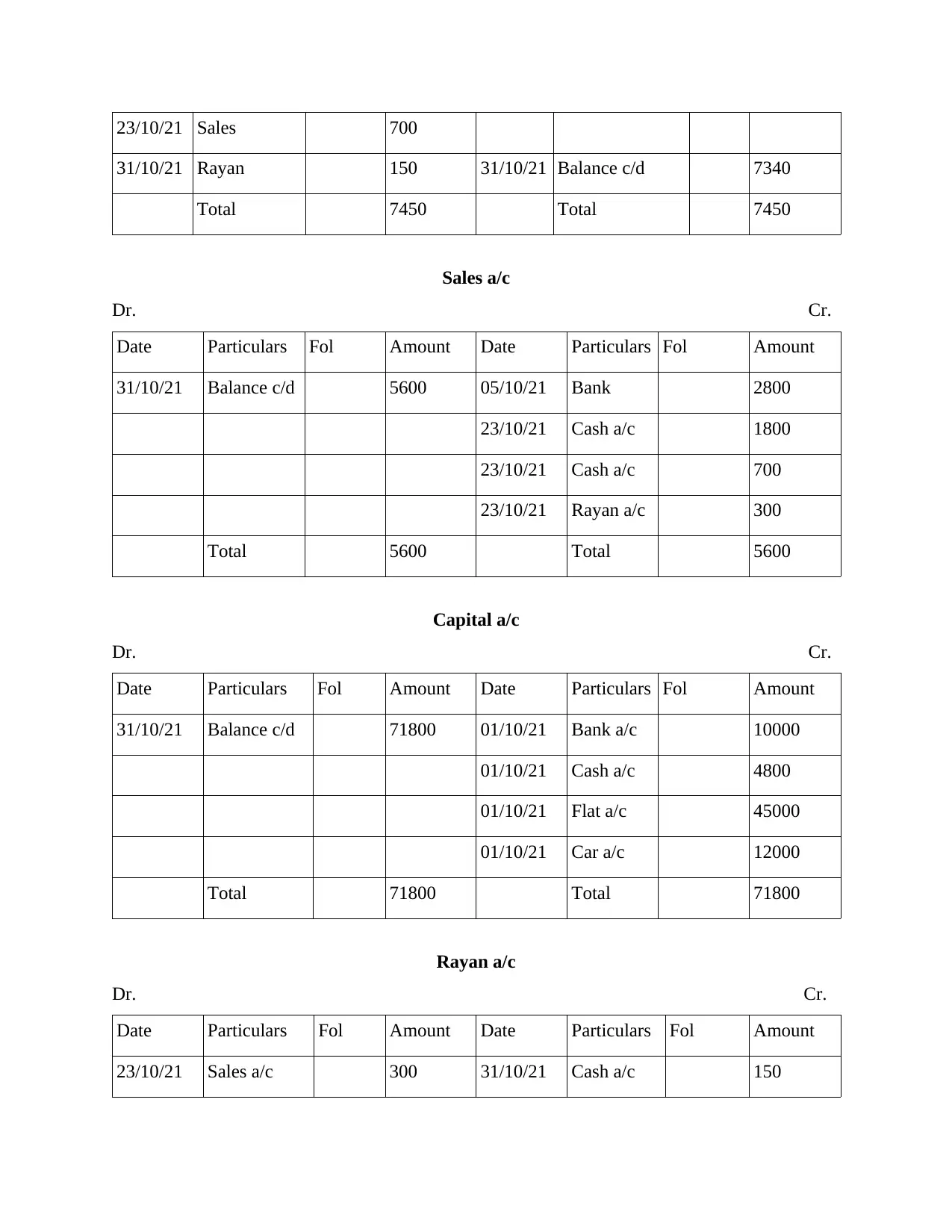

23/10/21 Sales 700

31/10/21 Rayan 150 31/10/21 Balance c/d 7340

Total 7450 Total 7450

Sales a/c

Dr. Cr.

Date Particulars Fol Amount Date Particulars Fol Amount

31/10/21 Balance c/d 5600 05/10/21 Bank 2800

23/10/21 Cash a/c 1800

23/10/21 Cash a/c 700

23/10/21 Rayan a/c 300

Total 5600 Total 5600

Capital a/c

Dr. Cr.

Date Particulars Fol Amount Date Particulars Fol Amount

31/10/21 Balance c/d 71800 01/10/21 Bank a/c 10000

01/10/21 Cash a/c 4800

01/10/21 Flat a/c 45000

01/10/21 Car a/c 12000

Total 71800 Total 71800

Rayan a/c

Dr. Cr.

Date Particulars Fol Amount Date Particulars Fol Amount

23/10/21 Sales a/c 300 31/10/21 Cash a/c 150

31/10/21 Rayan 150 31/10/21 Balance c/d 7340

Total 7450 Total 7450

Sales a/c

Dr. Cr.

Date Particulars Fol Amount Date Particulars Fol Amount

31/10/21 Balance c/d 5600 05/10/21 Bank 2800

23/10/21 Cash a/c 1800

23/10/21 Cash a/c 700

23/10/21 Rayan a/c 300

Total 5600 Total 5600

Capital a/c

Dr. Cr.

Date Particulars Fol Amount Date Particulars Fol Amount

31/10/21 Balance c/d 71800 01/10/21 Bank a/c 10000

01/10/21 Cash a/c 4800

01/10/21 Flat a/c 45000

01/10/21 Car a/c 12000

Total 71800 Total 71800

Rayan a/c

Dr. Cr.

Date Particulars Fol Amount Date Particulars Fol Amount

23/10/21 Sales a/c 300 31/10/21 Cash a/c 150

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

31/10/21 Balance c/d 150

Total 300 Total 300

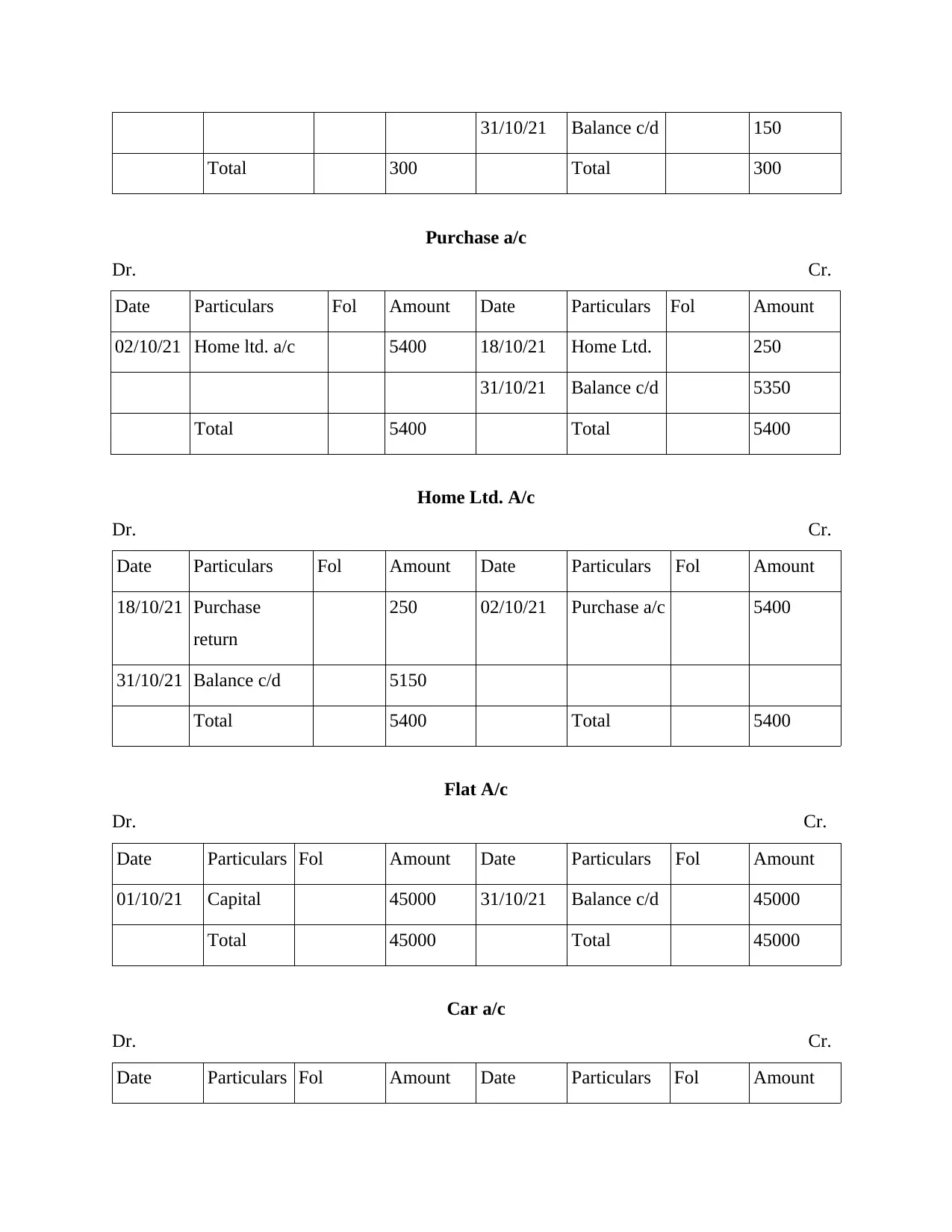

Purchase a/c

Dr. Cr.

Date Particulars Fol Amount Date Particulars Fol Amount

02/10/21 Home ltd. a/c 5400 18/10/21 Home Ltd. 250

31/10/21 Balance c/d 5350

Total 5400 Total 5400

Home Ltd. A/c

Dr. Cr.

Date Particulars Fol Amount Date Particulars Fol Amount

18/10/21 Purchase

return

250 02/10/21 Purchase a/c 5400

31/10/21 Balance c/d 5150

Total 5400 Total 5400

Flat A/c

Dr. Cr.

Date Particulars Fol Amount Date Particulars Fol Amount

01/10/21 Capital 45000 31/10/21 Balance c/d 45000

Total 45000 Total 45000

Car a/c

Dr. Cr.

Date Particulars Fol Amount Date Particulars Fol Amount

Total 300 Total 300

Purchase a/c

Dr. Cr.

Date Particulars Fol Amount Date Particulars Fol Amount

02/10/21 Home ltd. a/c 5400 18/10/21 Home Ltd. 250

31/10/21 Balance c/d 5350

Total 5400 Total 5400

Home Ltd. A/c

Dr. Cr.

Date Particulars Fol Amount Date Particulars Fol Amount

18/10/21 Purchase

return

250 02/10/21 Purchase a/c 5400

31/10/21 Balance c/d 5150

Total 5400 Total 5400

Flat A/c

Dr. Cr.

Date Particulars Fol Amount Date Particulars Fol Amount

01/10/21 Capital 45000 31/10/21 Balance c/d 45000

Total 45000 Total 45000

Car a/c

Dr. Cr.

Date Particulars Fol Amount Date Particulars Fol Amount

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

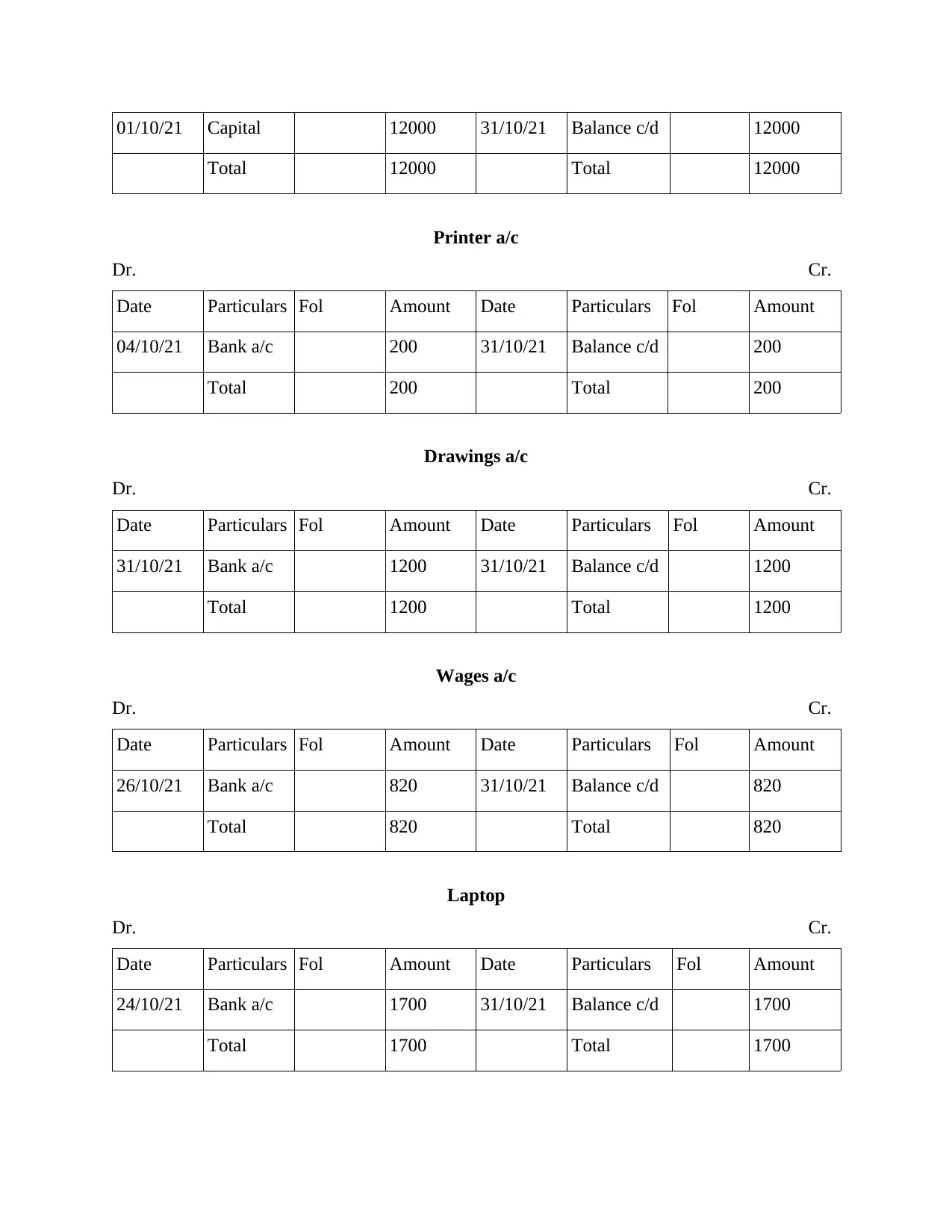

01/10/21 Capital 12000 31/10/21 Balance c/d 12000

Total 12000 Total 12000

Printer a/c

Dr. Cr.

Date Particulars Fol Amount Date Particulars Fol Amount

04/10/21 Bank a/c 200 31/10/21 Balance c/d 200

Total 200 Total 200

Drawings a/c

Dr. Cr.

Date Particulars Fol Amount Date Particulars Fol Amount

31/10/21 Bank a/c 1200 31/10/21 Balance c/d 1200

Total 1200 Total 1200

Wages a/c

Dr. Cr.

Date Particulars Fol Amount Date Particulars Fol Amount

26/10/21 Bank a/c 820 31/10/21 Balance c/d 820

Total 820 Total 820

Laptop

Dr. Cr.

Date Particulars Fol Amount Date Particulars Fol Amount

24/10/21 Bank a/c 1700 31/10/21 Balance c/d 1700

Total 1700 Total 1700

Total 12000 Total 12000

Printer a/c

Dr. Cr.

Date Particulars Fol Amount Date Particulars Fol Amount

04/10/21 Bank a/c 200 31/10/21 Balance c/d 200

Total 200 Total 200

Drawings a/c

Dr. Cr.

Date Particulars Fol Amount Date Particulars Fol Amount

31/10/21 Bank a/c 1200 31/10/21 Balance c/d 1200

Total 1200 Total 1200

Wages a/c

Dr. Cr.

Date Particulars Fol Amount Date Particulars Fol Amount

26/10/21 Bank a/c 820 31/10/21 Balance c/d 820

Total 820 Total 820

Laptop

Dr. Cr.

Date Particulars Fol Amount Date Particulars Fol Amount

24/10/21 Bank a/c 1700 31/10/21 Balance c/d 1700

Total 1700 Total 1700

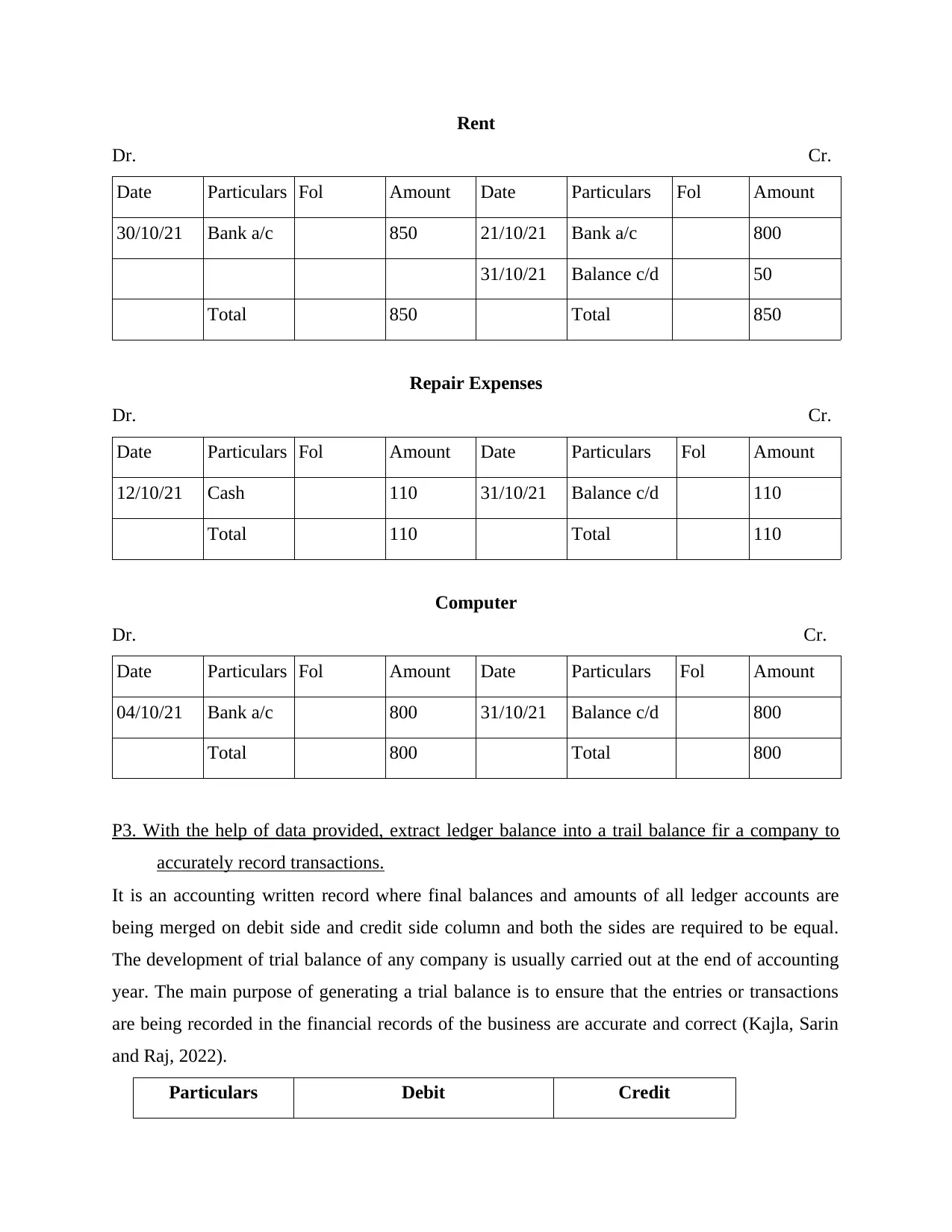

Rent

Dr. Cr.

Date Particulars Fol Amount Date Particulars Fol Amount

30/10/21 Bank a/c 850 21/10/21 Bank a/c 800

31/10/21 Balance c/d 50

Total 850 Total 850

Repair Expenses

Dr. Cr.

Date Particulars Fol Amount Date Particulars Fol Amount

12/10/21 Cash 110 31/10/21 Balance c/d 110

Total 110 Total 110

Computer

Dr. Cr.

Date Particulars Fol Amount Date Particulars Fol Amount

04/10/21 Bank a/c 800 31/10/21 Balance c/d 800

Total 800 Total 800

P3. With the help of data provided, extract ledger balance into a trail balance fir a company to

accurately record transactions.

It is an accounting written record where final balances and amounts of all ledger accounts are

being merged on debit side and credit side column and both the sides are required to be equal.

The development of trial balance of any company is usually carried out at the end of accounting

year. The main purpose of generating a trial balance is to ensure that the entries or transactions

are being recorded in the financial records of the business are accurate and correct (Kajla, Sarin

and Raj, 2022).

Particulars Debit Credit

Dr. Cr.

Date Particulars Fol Amount Date Particulars Fol Amount

30/10/21 Bank a/c 850 21/10/21 Bank a/c 800

31/10/21 Balance c/d 50

Total 850 Total 850

Repair Expenses

Dr. Cr.

Date Particulars Fol Amount Date Particulars Fol Amount

12/10/21 Cash 110 31/10/21 Balance c/d 110

Total 110 Total 110

Computer

Dr. Cr.

Date Particulars Fol Amount Date Particulars Fol Amount

04/10/21 Bank a/c 800 31/10/21 Balance c/d 800

Total 800 Total 800

P3. With the help of data provided, extract ledger balance into a trail balance fir a company to

accurately record transactions.

It is an accounting written record where final balances and amounts of all ledger accounts are

being merged on debit side and credit side column and both the sides are required to be equal.

The development of trial balance of any company is usually carried out at the end of accounting

year. The main purpose of generating a trial balance is to ensure that the entries or transactions

are being recorded in the financial records of the business are accurate and correct (Kajla, Sarin

and Raj, 2022).

Particulars Debit Credit

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.