Financial Accounting: Recording Business Transactions Assessment A2

VerifiedAdded on 2022/12/28

|16

|2993

|29

Homework Assignment

AI Summary

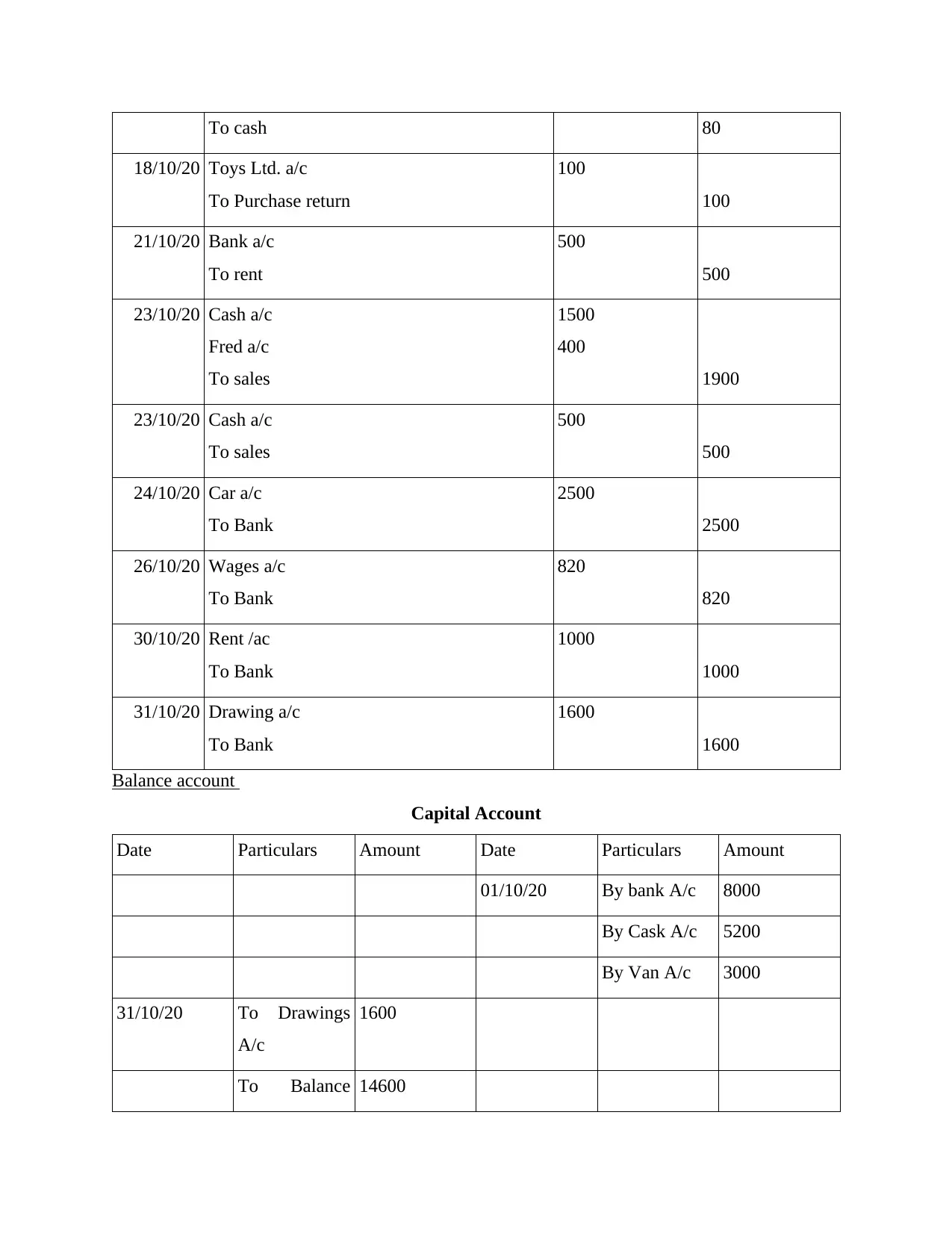

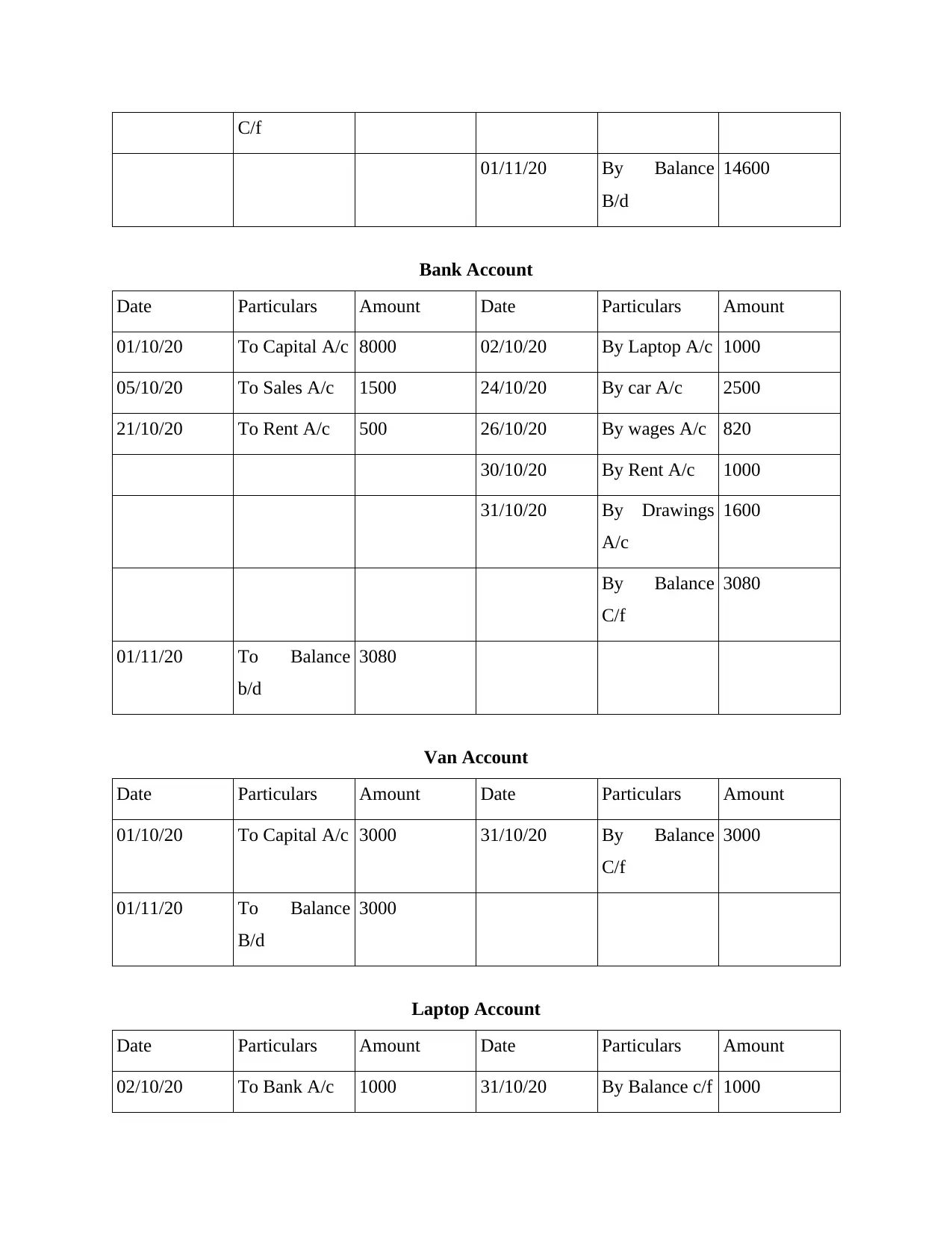

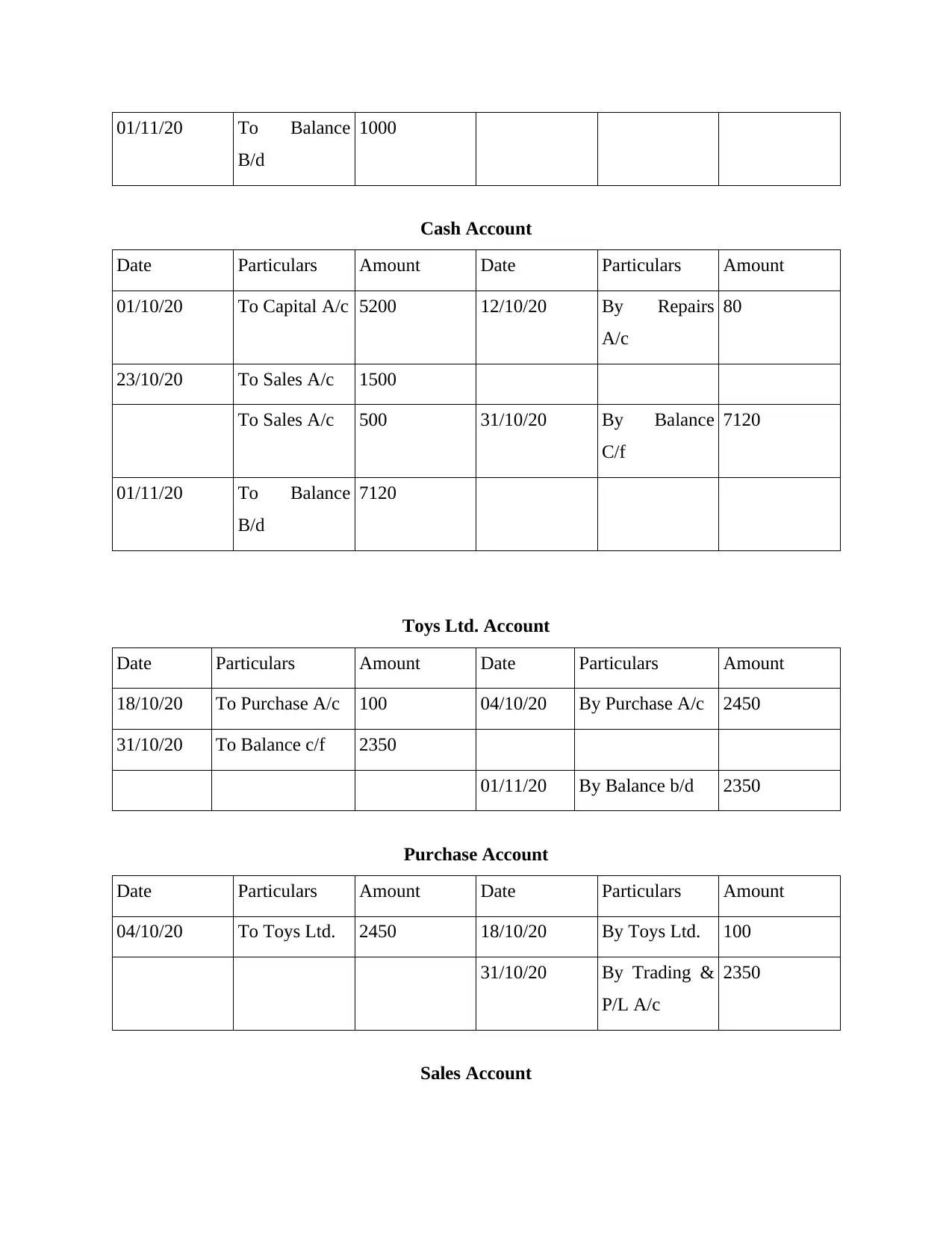

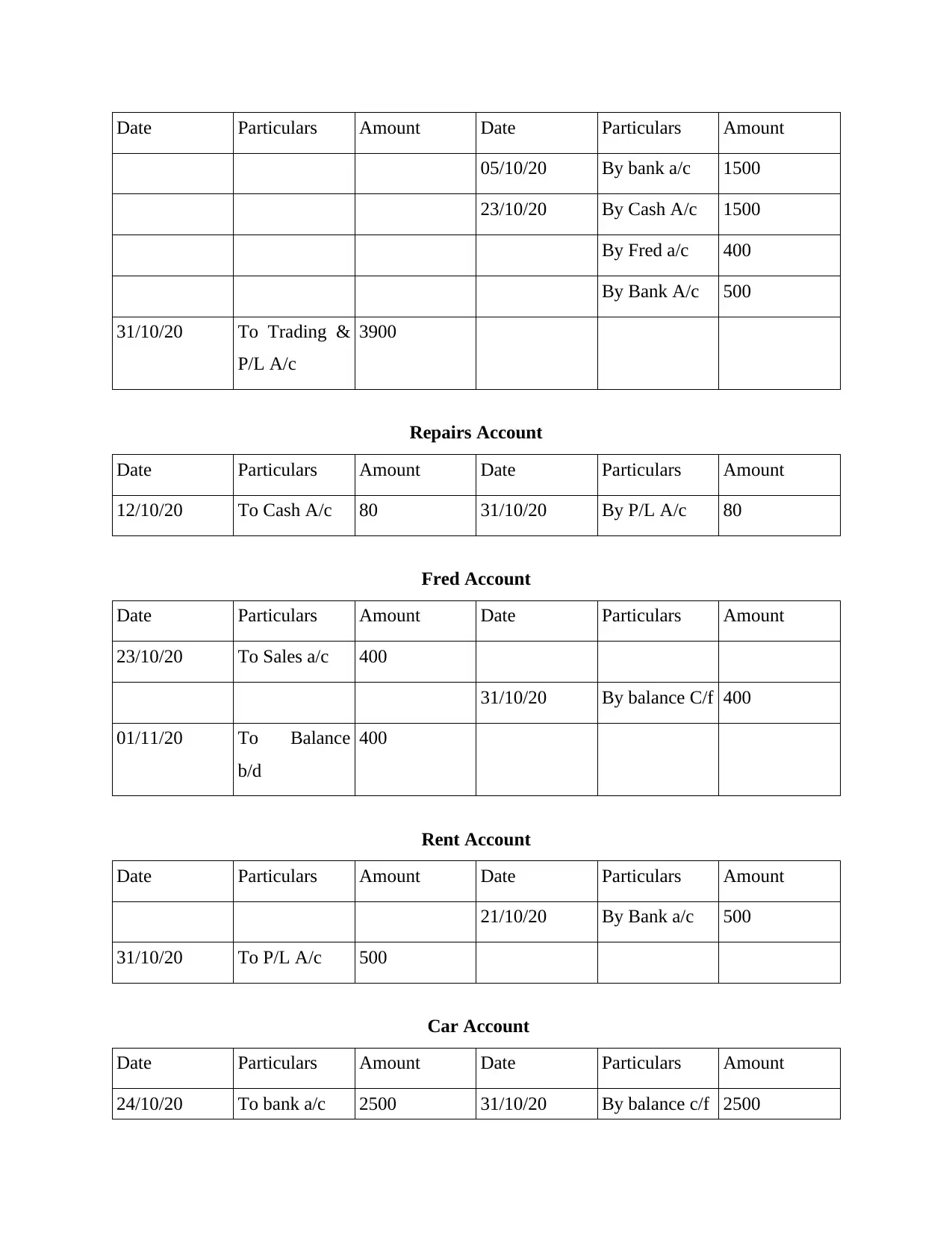

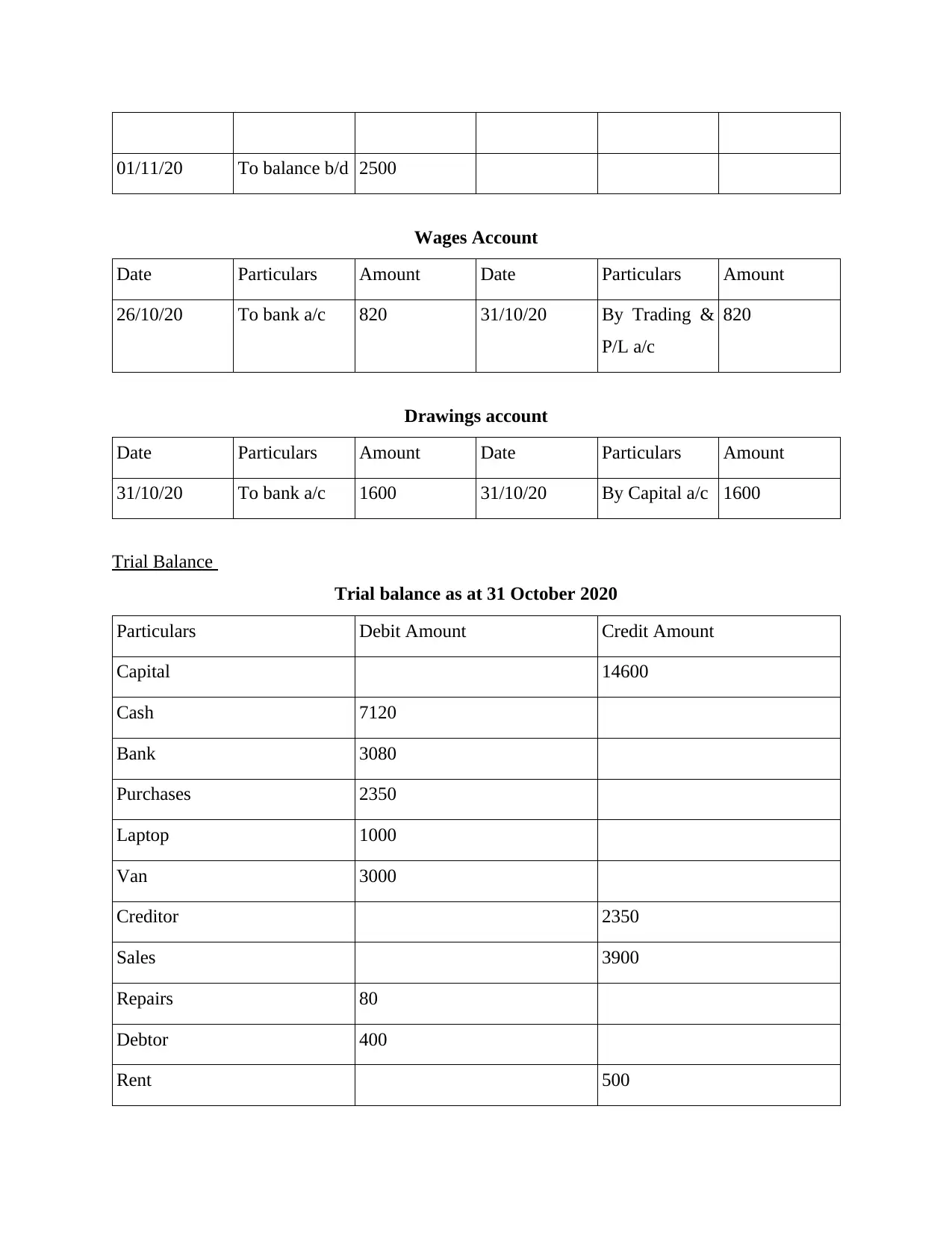

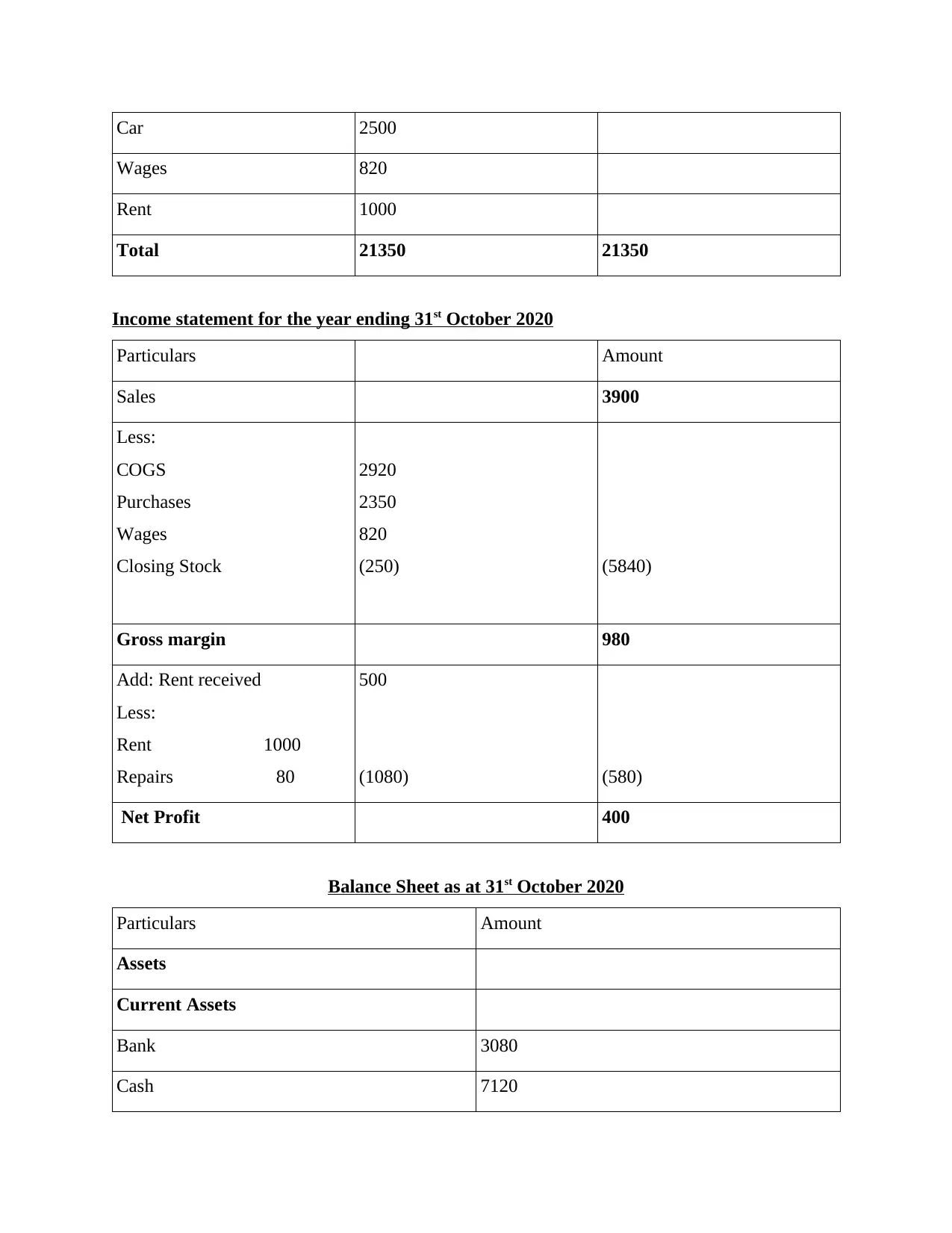

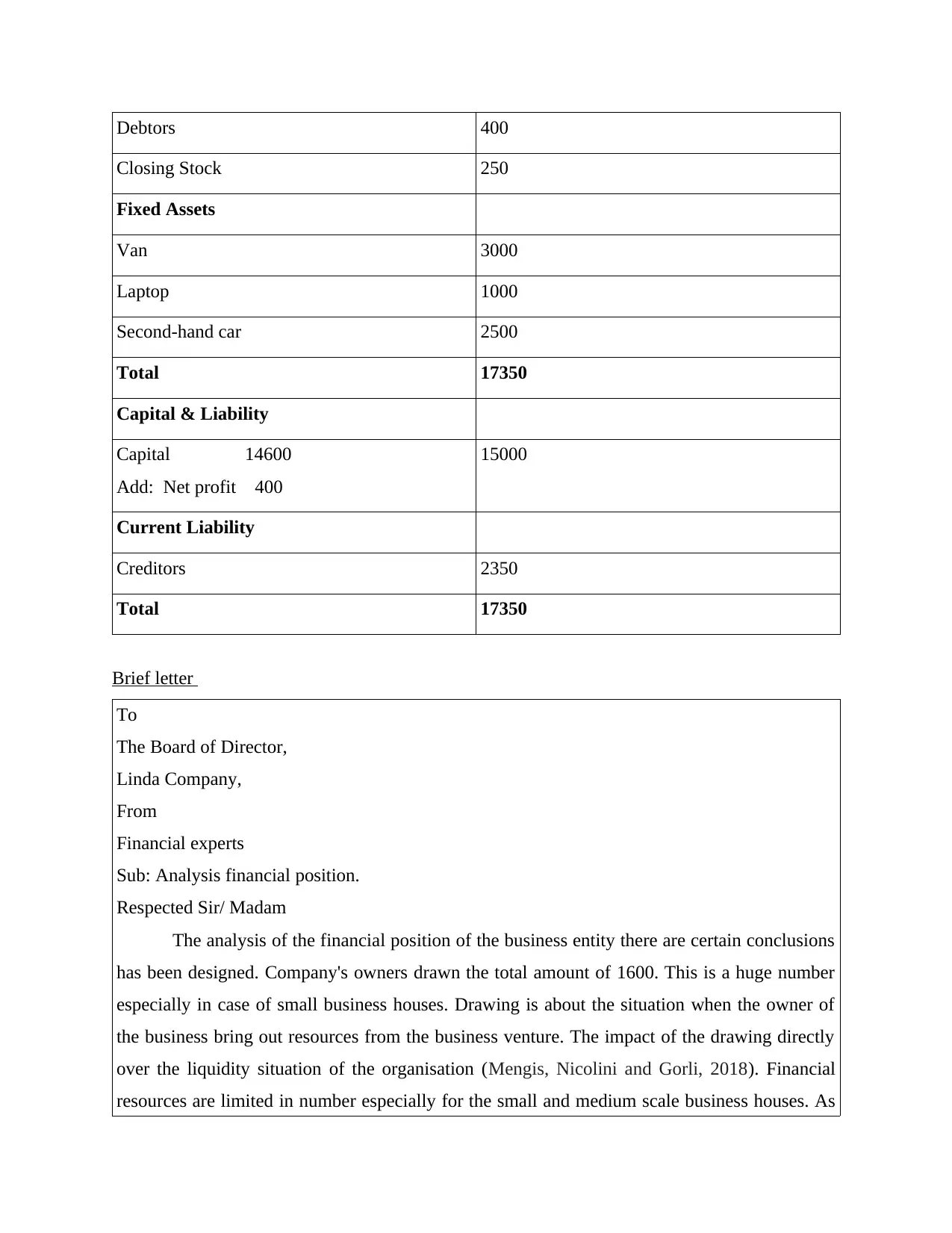

This assignment, "Recording Business Transaction Assessment A2," focuses on the core principles of financial accounting. It begins with a detailed set of journal entries, meticulously recording various business transactions. Following this, the assignment presents individual ledger accounts and culminates in the preparation of a trial balance, income statement, and balance sheet, providing a comprehensive overview of the company's financial performance and position. The assessment also includes a brief letter analyzing the impact of drawings on the company's liquidity. Furthermore, the assignment delves into ratio calculations, including net profit margin, gross profit margin, current ratio, acid-test ratio, and accounts receivable/payable collection periods, offering insights into the company's financial health and performance compared to industry benchmarks. The analysis highlights areas for improvement, particularly in profitability and expense management, offering strategic recommendations for enhanced financial performance.

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.