BA30592E Assignment: Recording Business Transactions Analysis

VerifiedAdded on 2022/12/28

|15

|1842

|20

Homework Assignment

AI Summary

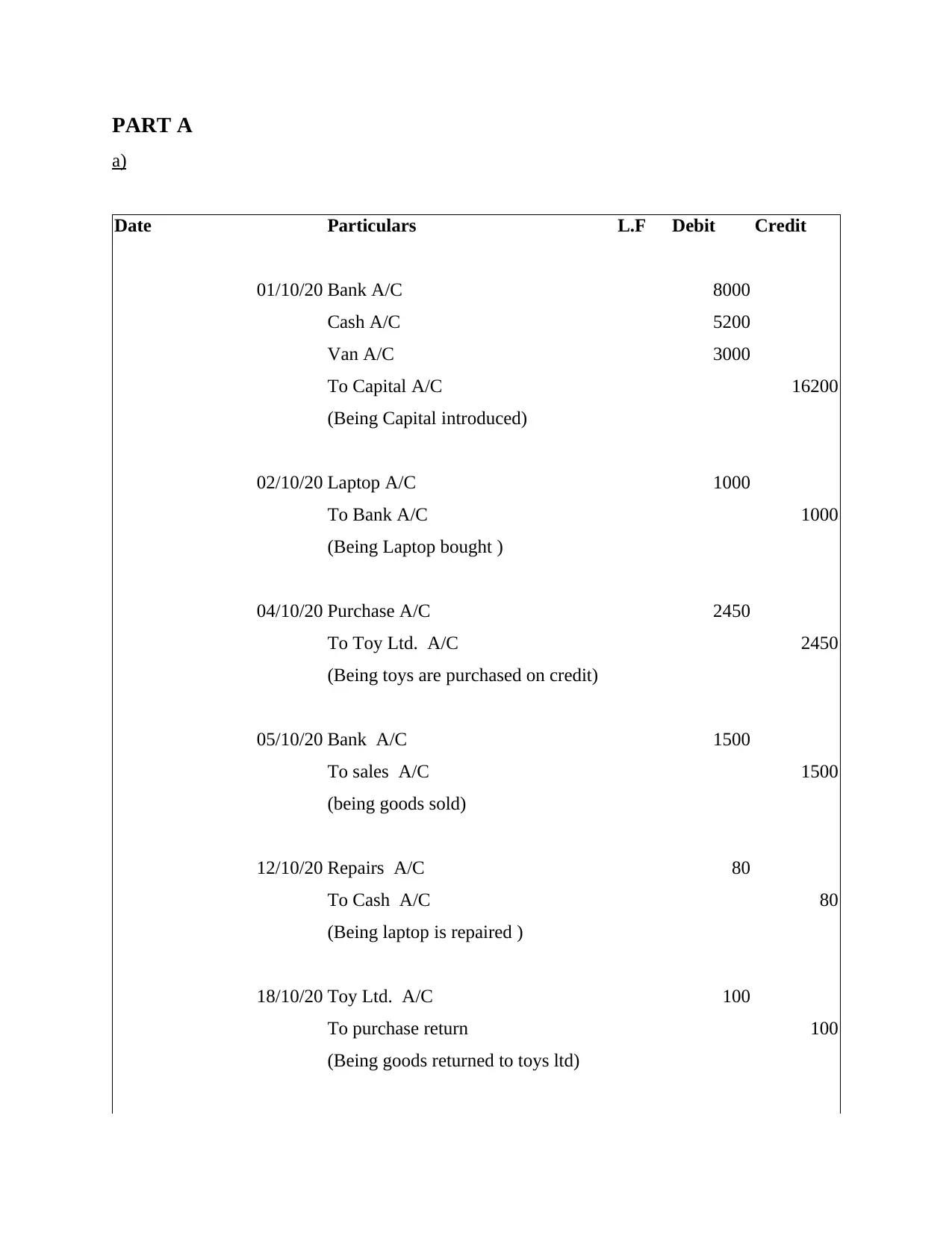

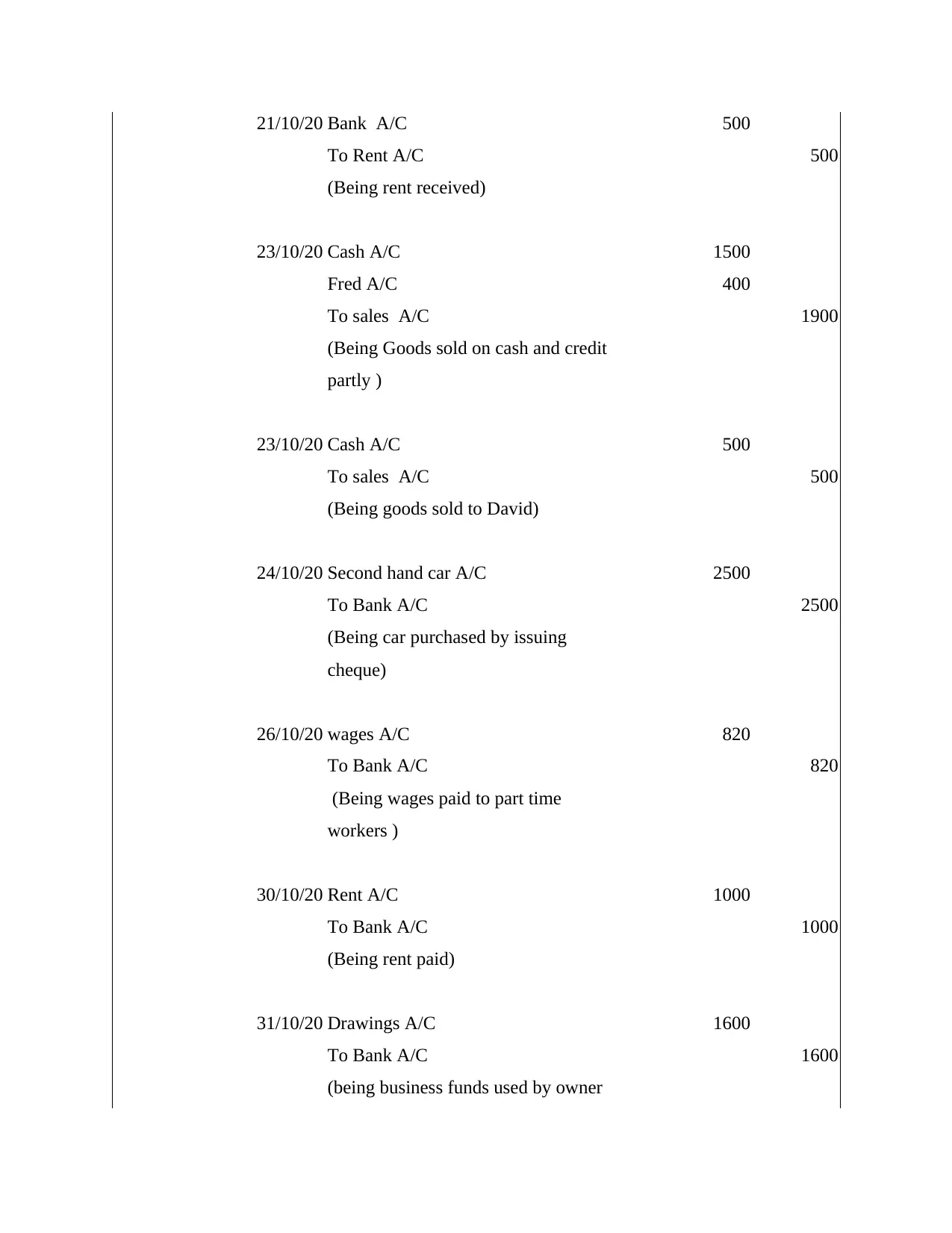

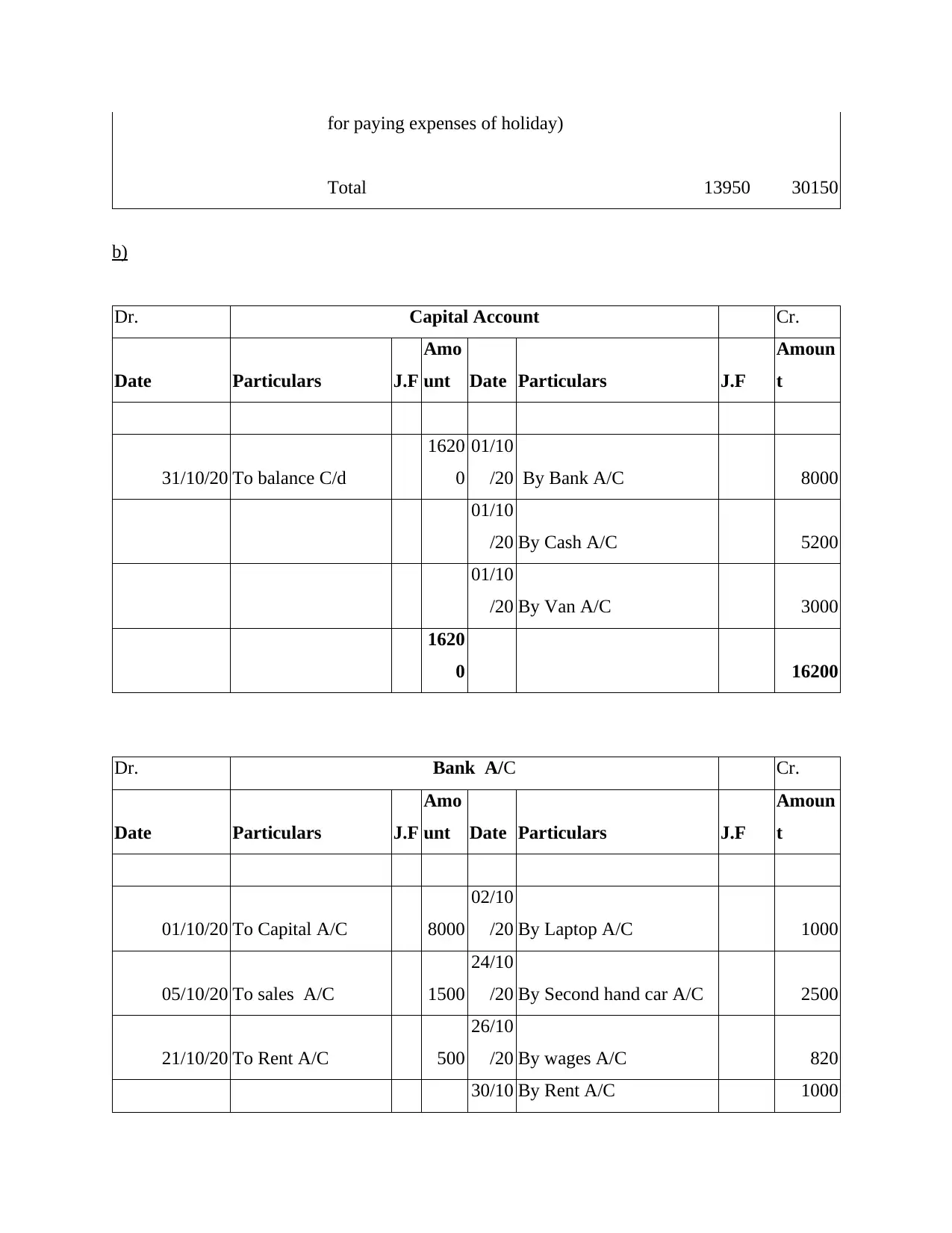

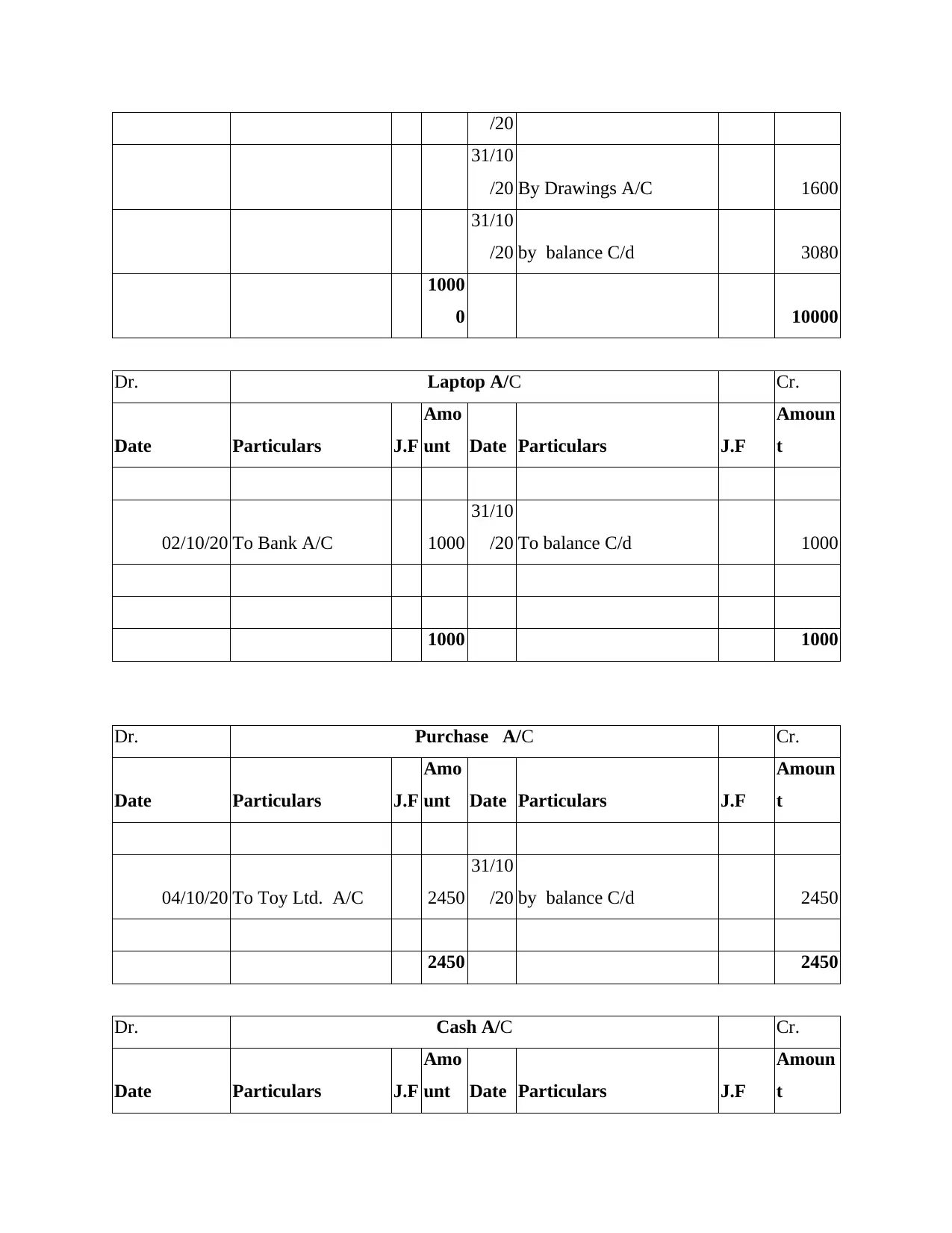

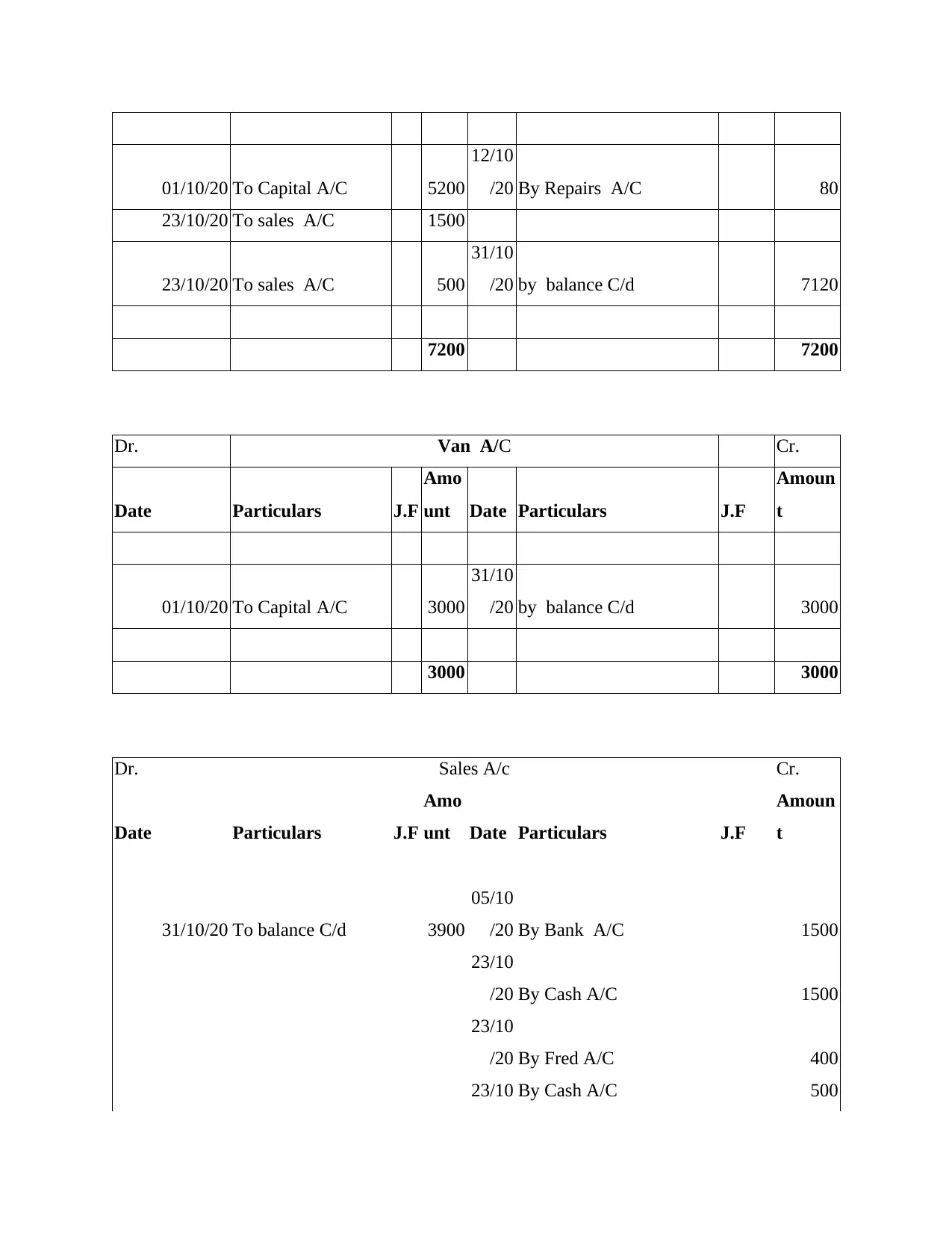

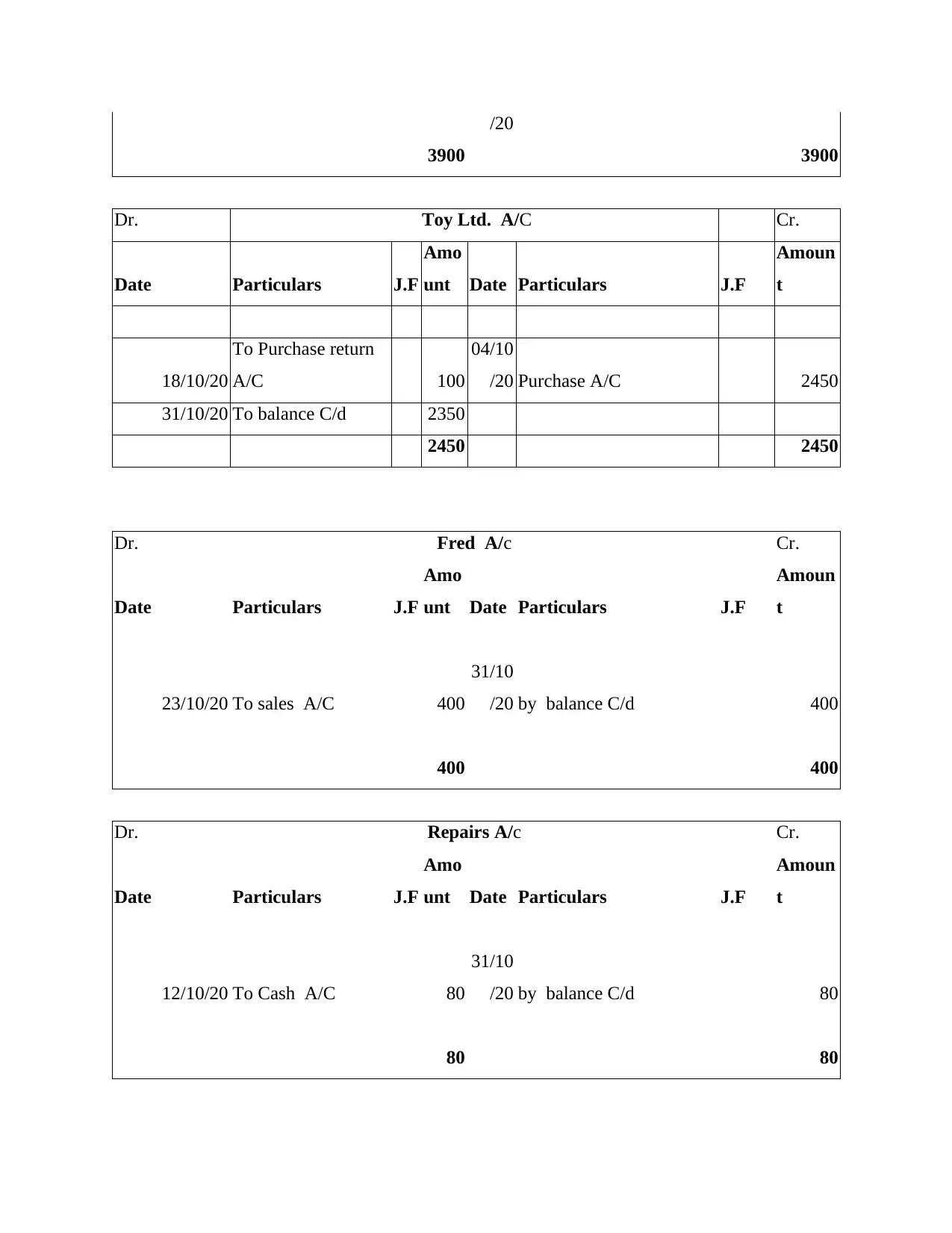

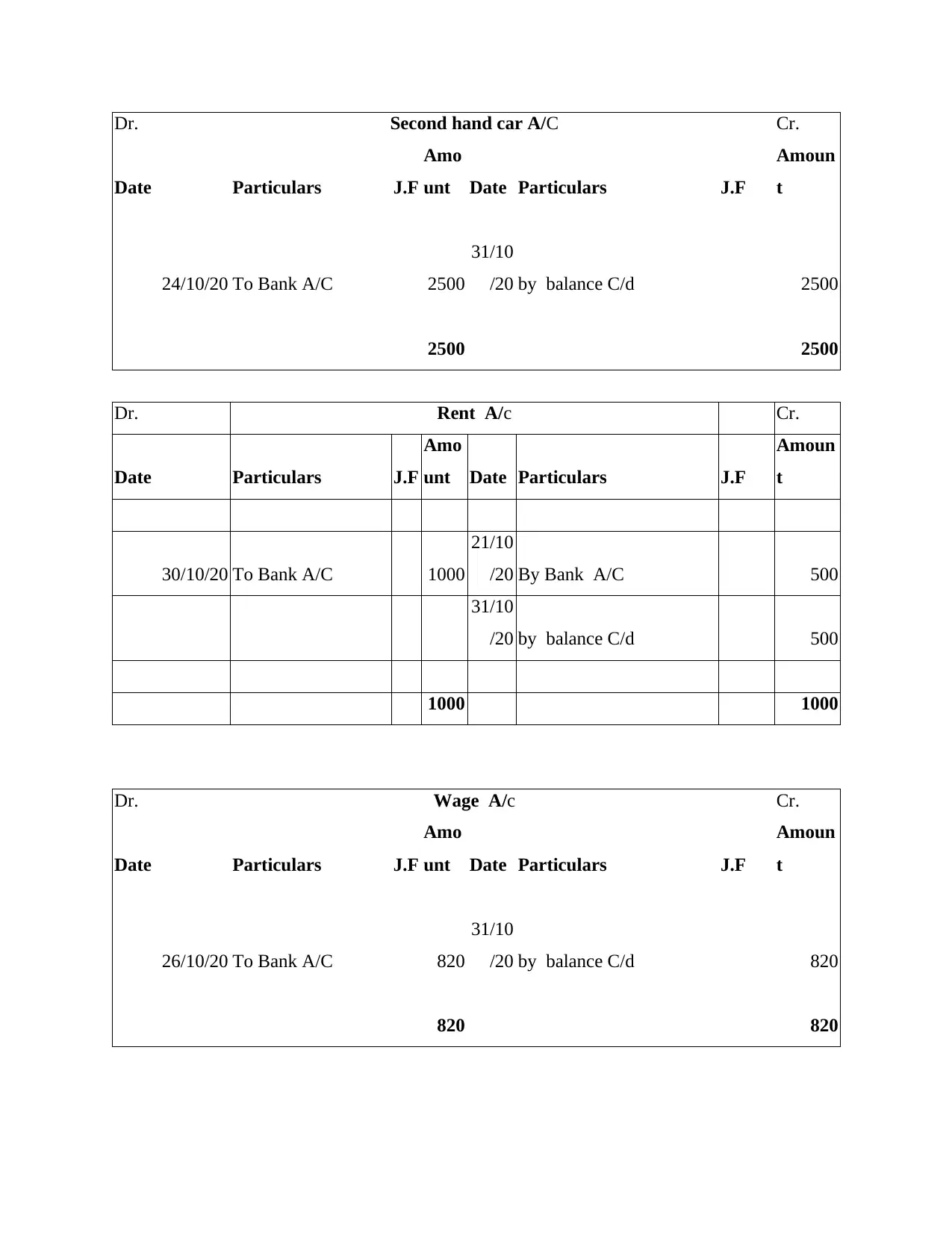

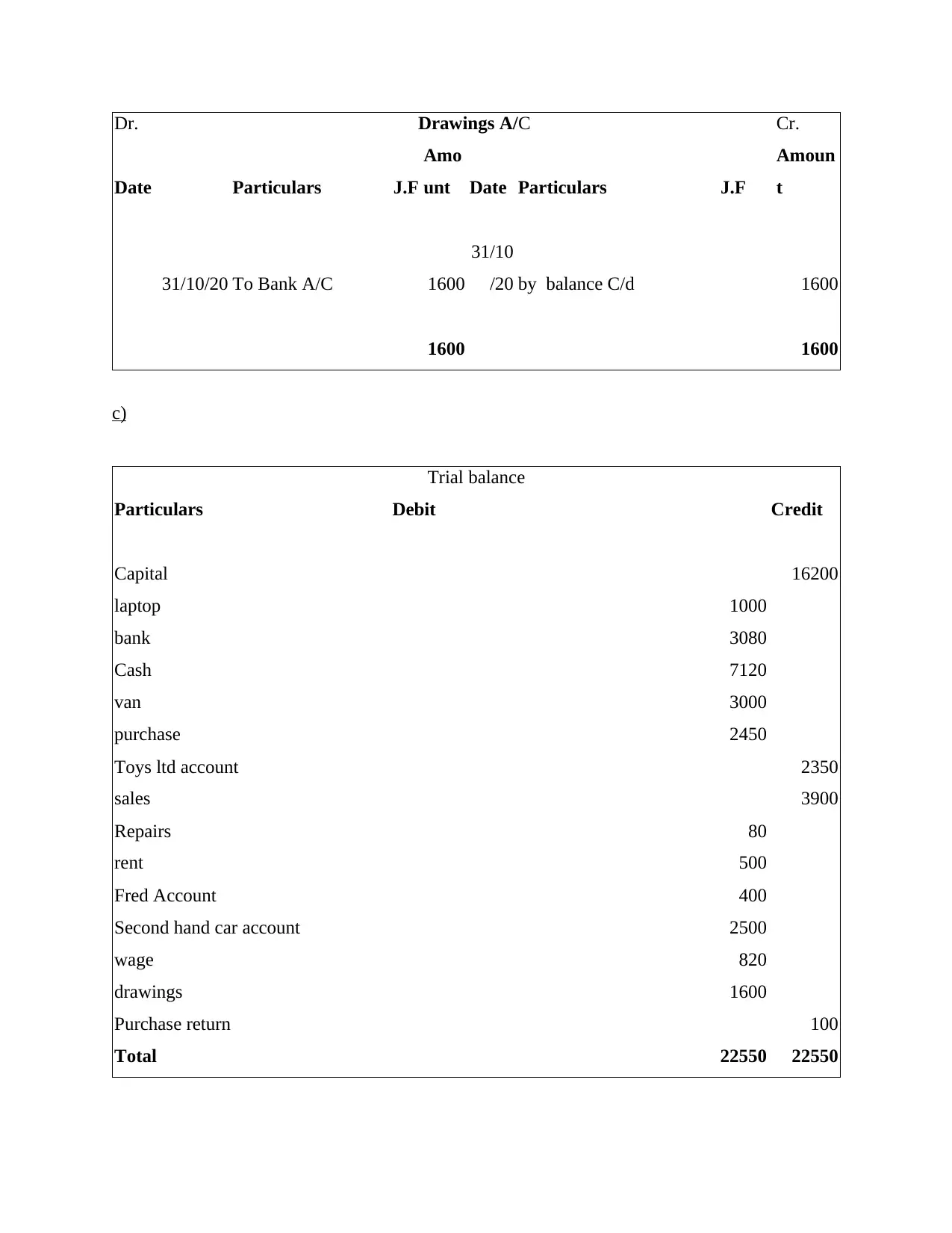

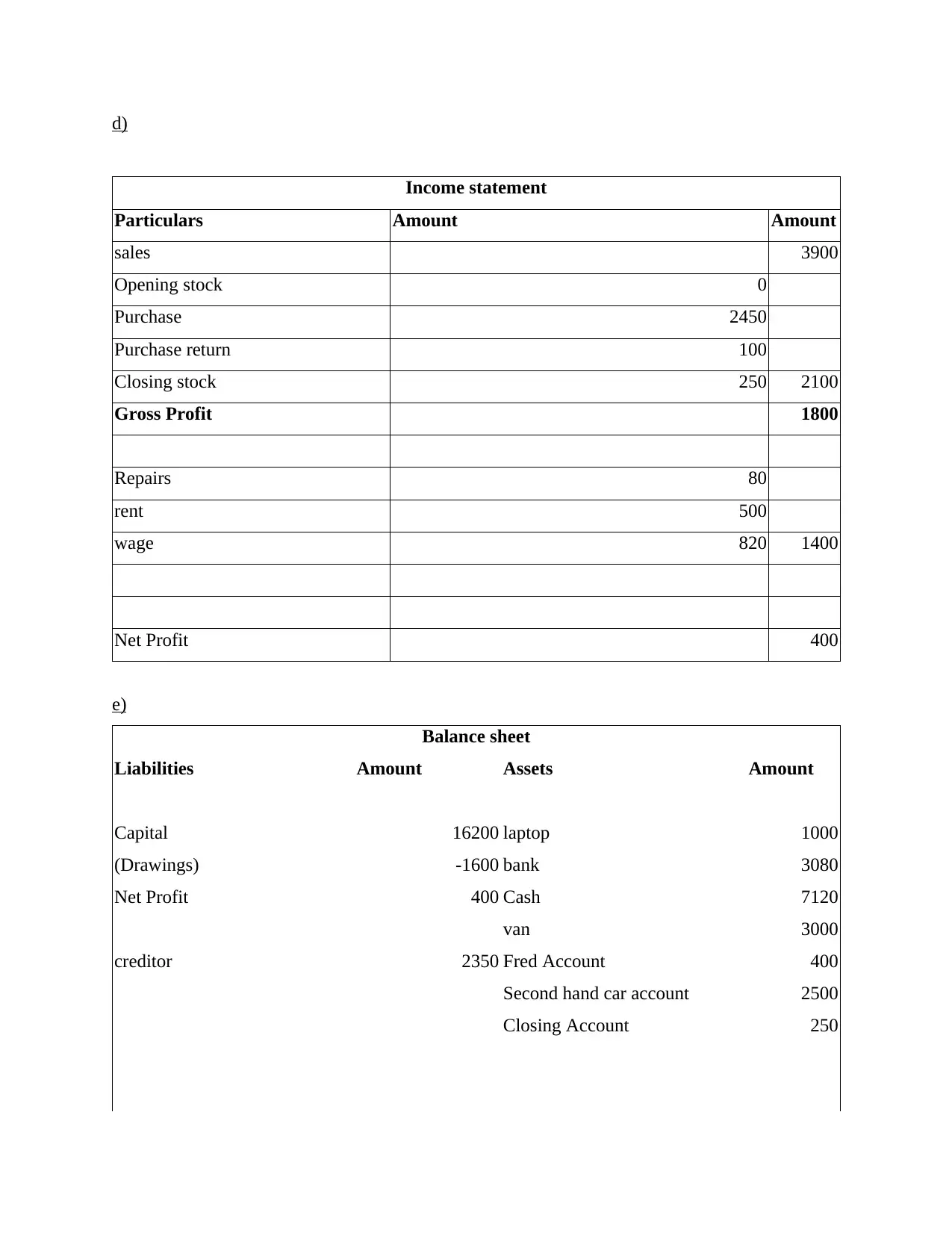

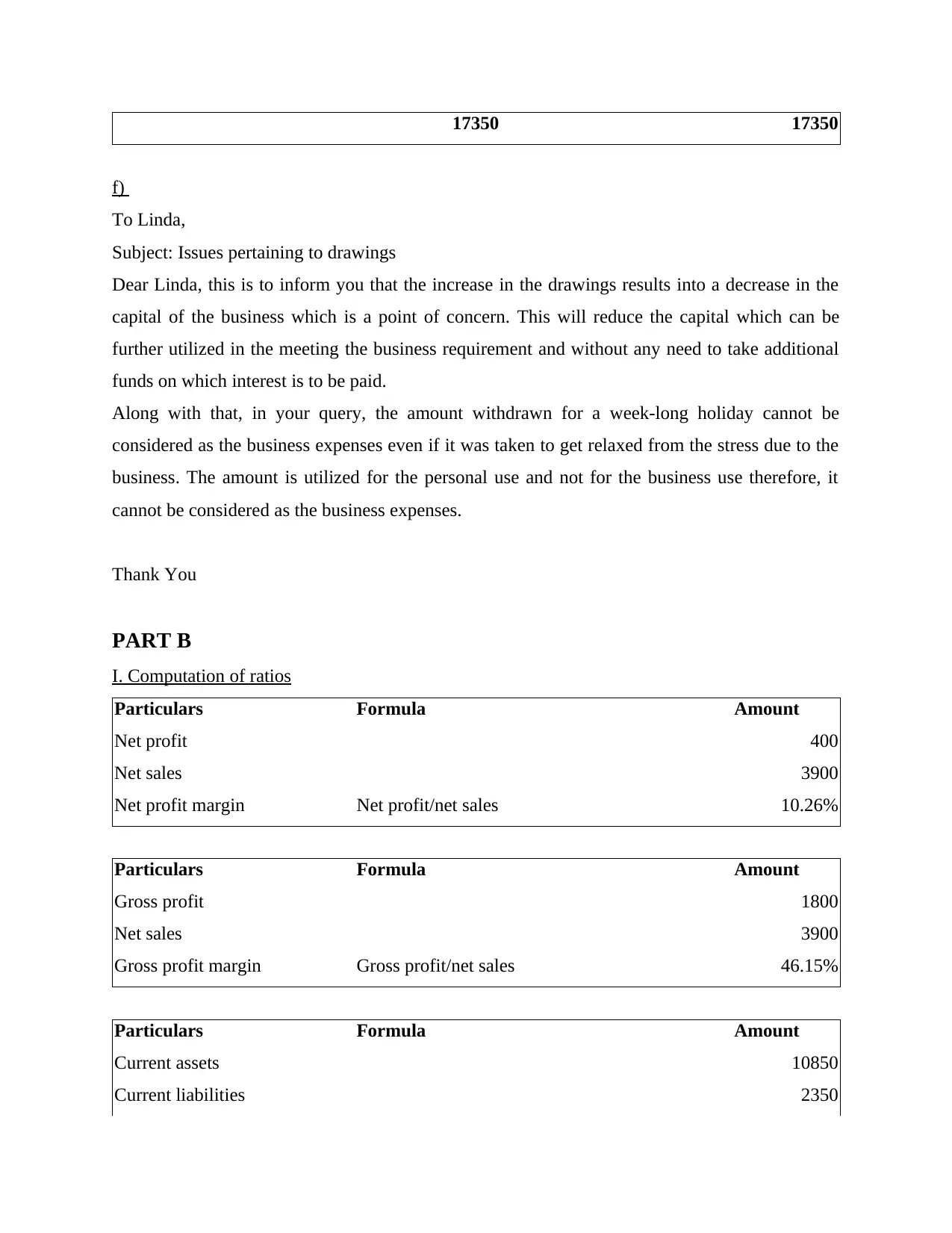

This homework assignment focuses on recording business transactions for a toy business in Oxford during October 2020. The solution begins with journal entries for various transactions, including capital contributions, purchases, sales, and expenses. It then proceeds to create ledger accounts (Capital, Bank, Laptop, Purchase, Cash, Van, Sales, Toys Ltd, Fred, Repairs, Second-hand car, Rent, Wages, Drawings) and a trial balance. The assignment continues with the preparation of an income statement and balance sheet. Finally, it includes a computation and analysis of financial ratios, comparing the business's performance with competitors, and a letter addressing concerns about drawings and business expenses. The assignment demonstrates a comprehensive understanding of accounting principles and financial statement analysis.

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.