Analyzing Business Transactions and Financial Reporting: A Report

VerifiedAdded on 2023/01/05

|23

|3365

|72

Report

AI Summary

This report comprehensively examines the process of recording business transactions, encompassing journal entries, ledger accounts, and trial balances. It begins with an introduction to business transactions, emphasizing their importance in financial reporting and decision-making. The report then delves into specific examples, including journal entries with narrations for various transactions and the preparation of ledger accounts and trial balances. Furthermore, it includes the creation of income statements, analysis of the impact of COVID-19 on financial statement items, and a detailed ratio analysis. The report concludes with a summary of key findings and recommendations for effective financial management, providing a valuable resource for students and professionals alike.

Recording Business

Transactions

Transactions

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

ASSESSMENT 1.............................................................................................................................1

PART 1............................................................................................................................................1

Decision makers and their need for accounting information: .....................................................1

Advantage and Disadvantage of recording accounting information:..........................................2

PART 2............................................................................................................................................3

Journal entries with narration for the David wises:.....................................................................3

PART 3............................................................................................................................................4

Ledger and trail balance of Pearce & sons:................................................................................4

PART 4............................................................................................................................................6

Income statement for Airman co.:...............................................................................................6

Impact of COVID 19 on company income statement items:.......................................................6

ASSESSMENT 2.............................................................................................................................7

PART A...........................................................................................................................................7

Journal transactions of T- accounts:............................................................................................7

Balance the accounts and an opening balances:..........................................................................8

Trial balance:.............................................................................................................................11

Income statement for the period 31st Oct. 2020:.......................................................................12

Preparation of financial position 31st Oct. 2020:......................................................................12

PART B..........................................................................................................................................13

Ratio calculation for Linda's business:......................................................................................13

Analysis of ratio analysis in comparison to its competitors:.....................................................14

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................16

INTRODUCTION...........................................................................................................................1

ASSESSMENT 1.............................................................................................................................1

PART 1............................................................................................................................................1

Decision makers and their need for accounting information: .....................................................1

Advantage and Disadvantage of recording accounting information:..........................................2

PART 2............................................................................................................................................3

Journal entries with narration for the David wises:.....................................................................3

PART 3............................................................................................................................................4

Ledger and trail balance of Pearce & sons:................................................................................4

PART 4............................................................................................................................................6

Income statement for Airman co.:...............................................................................................6

Impact of COVID 19 on company income statement items:.......................................................6

ASSESSMENT 2.............................................................................................................................7

PART A...........................................................................................................................................7

Journal transactions of T- accounts:............................................................................................7

Balance the accounts and an opening balances:..........................................................................8

Trial balance:.............................................................................................................................11

Income statement for the period 31st Oct. 2020:.......................................................................12

Preparation of financial position 31st Oct. 2020:......................................................................12

PART B..........................................................................................................................................13

Ratio calculation for Linda's business:......................................................................................13

Analysis of ratio analysis in comparison to its competitors:.....................................................14

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................16

INTRODUCTION

A business transaction is an event that includes transactions of goods, money and services

between two or more than two parties. Business transactions are events that must be measurable

in money and recorded in accounting system. For example; Buying machinery from suppliers.

Business transactions are activity which is measured in monetary terms and which affects the

financial position of the company. These transactions affects on such accounting elements-

capital, assets, liabilities, expenses and income (Brennan, Canning and McDowell, 2020).

Business transaction recording are important in any business in order to know about its financial

position and growth. This report is based on various companies business records. This covers

topics such as journal, ledger and trial balance. Apart from this it also covers cash account and

ratio analysis in comparison to competitors.

ASSESSMENT 1

PART 1

Decision makers and their need for accounting information:

Financial accounting is a element of accounting that oversee the position of the company.

Under standard guidelines, transactions are summarising, recording and presented in the financial

statements such as profit and loss account and balance sheet. These statements are known as

external because they used to given to the outside of the company such as clients and

shareholders. The reason behind it financial statements are used by various people in various

ways, it has common standard that is known as Accounting standard and Generally accepted

accounting principles (GAAP) (Chaffey, Edmundson-Bird and Hemphill, 2019). It provides

information to managers so that they can make decisions regarding companies activities.

Investors and analyst also used this information for the valuation and worth of the company in

order to allow them to set prices and shares prices. Financial account is helps firm to track its

activities for future decision-making. It also helps companies for day to day activities and

identify what can give it future benefits for its growth.

Financial accounts shows all the information related to monetary terms of the company

which helps management and shareholders in order to decision-making process. This helps

management for knowing resources which are profitable to company and which gives insight to

managers for budget making (Chen, Liao and Wang, 2020). Through this company can compare

1

A business transaction is an event that includes transactions of goods, money and services

between two or more than two parties. Business transactions are events that must be measurable

in money and recorded in accounting system. For example; Buying machinery from suppliers.

Business transactions are activity which is measured in monetary terms and which affects the

financial position of the company. These transactions affects on such accounting elements-

capital, assets, liabilities, expenses and income (Brennan, Canning and McDowell, 2020).

Business transaction recording are important in any business in order to know about its financial

position and growth. This report is based on various companies business records. This covers

topics such as journal, ledger and trial balance. Apart from this it also covers cash account and

ratio analysis in comparison to competitors.

ASSESSMENT 1

PART 1

Decision makers and their need for accounting information:

Financial accounting is a element of accounting that oversee the position of the company.

Under standard guidelines, transactions are summarising, recording and presented in the financial

statements such as profit and loss account and balance sheet. These statements are known as

external because they used to given to the outside of the company such as clients and

shareholders. The reason behind it financial statements are used by various people in various

ways, it has common standard that is known as Accounting standard and Generally accepted

accounting principles (GAAP) (Chaffey, Edmundson-Bird and Hemphill, 2019). It provides

information to managers so that they can make decisions regarding companies activities.

Investors and analyst also used this information for the valuation and worth of the company in

order to allow them to set prices and shares prices. Financial account is helps firm to track its

activities for future decision-making. It also helps companies for day to day activities and

identify what can give it future benefits for its growth.

Financial accounts shows all the information related to monetary terms of the company

which helps management and shareholders in order to decision-making process. This helps

management for knowing resources which are profitable to company and which gives insight to

managers for budget making (Chen, Liao and Wang, 2020). Through this company can compare

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

itself by past data and know the reasons regarding changes in the year. The information is used

by internal managers such as internal decision making, also helps in hiring, compensation, sales

and promotional activities, marketing, investment etc.

Advantage and Disadvantage of recording accounting information:

Accounting refers to a process in which financial transactions of the businesses are

recorded. The process of accounting includes summarising, analysing and reporting those

transactions which are related to oversight agencies, regulatory bodies and tax collection

companies. It is useful in business for measurement, processing and communication of financial

information for running its activities (Samuels, 2019). It helps managers for decision making

regarding sales, activities, promotional activities, employees hiring and investments. it has

common standard that is known as Accounting standard and Generally accepted accounting

principles (GAAP).

Advantages: Mentioned below are some advantages related to recording accounting

information:

Main business records: Accounting shows each and every transaction of the business

finance because it systematically maintain the books of all business monetary

transactions. It helps in tax paying and to estimate about the budget. It records all

transactions that are occurs in its day to day activities in credit and cash basis. For

example, if company buy furniture that it records it in its accounting books (Johnson,

2015).

Helps in preparing financial statements: Preparation of financial statements is

necessary for knowing all losses and profits and real value of the organisation. It helps in

knowing all relevant accounting data for the preparation of financial statements such as

profit and loss account (Rezaei, ed., 2017). Through journal, ledger and trial balance

companies prepares its financial statements as p & l and balance sheet.

Disadvantages: Disadvantages of recording transactions are mentioned below:

Provides insufficient information: Financial accounting not provides detailed

information related to different department and processes and other activities within the

organisation. It provides information of whole organisation as an unity liabilities, assets,

loss and profits of organisation. It refers overall transactions of the company at a one

place only without any department guidelines.

2

by internal managers such as internal decision making, also helps in hiring, compensation, sales

and promotional activities, marketing, investment etc.

Advantage and Disadvantage of recording accounting information:

Accounting refers to a process in which financial transactions of the businesses are

recorded. The process of accounting includes summarising, analysing and reporting those

transactions which are related to oversight agencies, regulatory bodies and tax collection

companies. It is useful in business for measurement, processing and communication of financial

information for running its activities (Samuels, 2019). It helps managers for decision making

regarding sales, activities, promotional activities, employees hiring and investments. it has

common standard that is known as Accounting standard and Generally accepted accounting

principles (GAAP).

Advantages: Mentioned below are some advantages related to recording accounting

information:

Main business records: Accounting shows each and every transaction of the business

finance because it systematically maintain the books of all business monetary

transactions. It helps in tax paying and to estimate about the budget. It records all

transactions that are occurs in its day to day activities in credit and cash basis. For

example, if company buy furniture that it records it in its accounting books (Johnson,

2015).

Helps in preparing financial statements: Preparation of financial statements is

necessary for knowing all losses and profits and real value of the organisation. It helps in

knowing all relevant accounting data for the preparation of financial statements such as

profit and loss account (Rezaei, ed., 2017). Through journal, ledger and trial balance

companies prepares its financial statements as p & l and balance sheet.

Disadvantages: Disadvantages of recording transactions are mentioned below:

Provides insufficient information: Financial accounting not provides detailed

information related to different department and processes and other activities within the

organisation. It provides information of whole organisation as an unity liabilities, assets,

loss and profits of organisation. It refers overall transactions of the company at a one

place only without any department guidelines.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

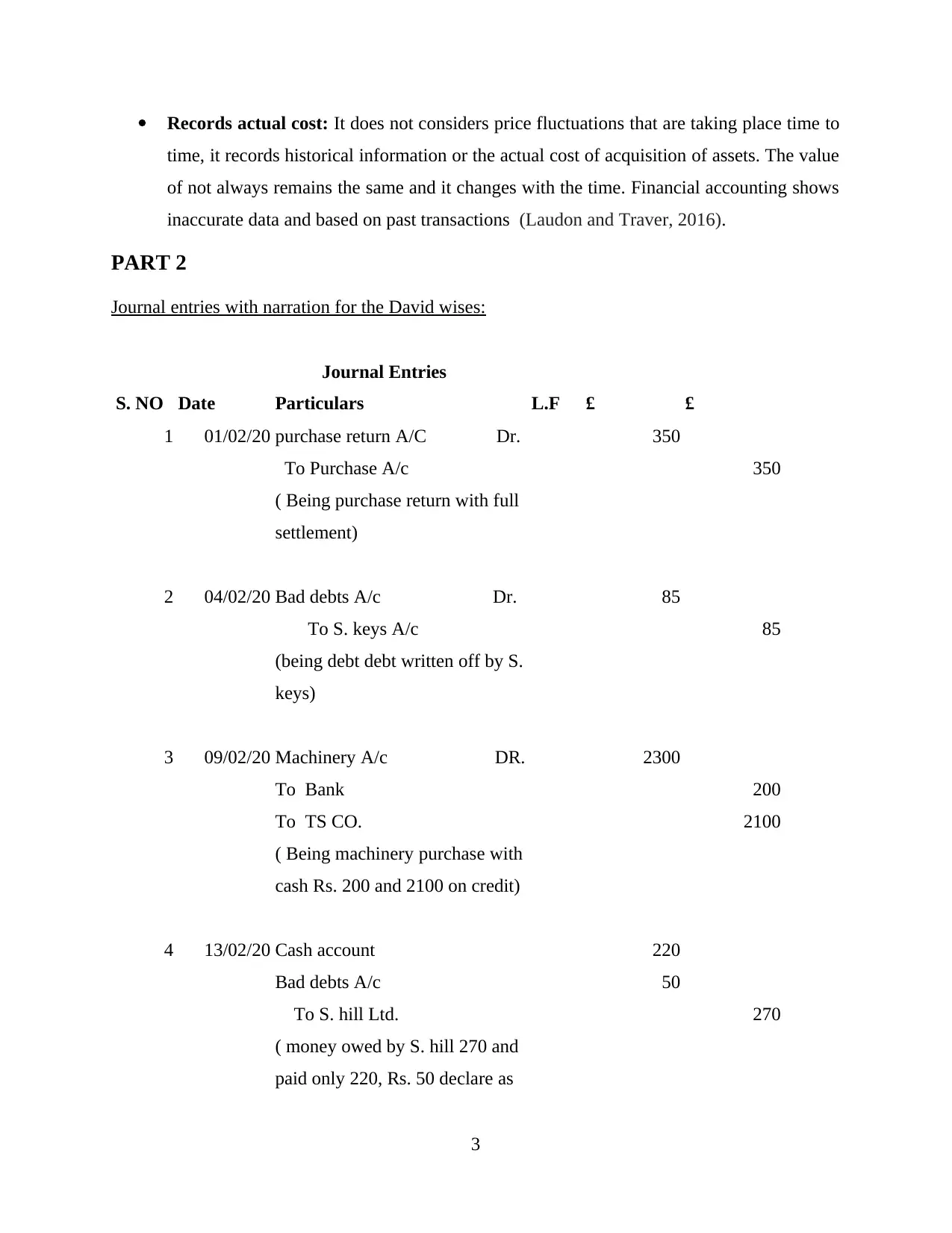

Records actual cost: It does not considers price fluctuations that are taking place time to

time, it records historical information or the actual cost of acquisition of assets. The value

of not always remains the same and it changes with the time. Financial accounting shows

inaccurate data and based on past transactions (Laudon and Traver, 2016).

PART 2

Journal entries with narration for the David wises:

Journal Entries

S. NO Date Particulars L.F £ £

1 01/02/20 purchase return A/C Dr. 350

To Purchase A/c 350

( Being purchase return with full

settlement)

2 04/02/20 Bad debts A/c Dr. 85

To S. keys A/c 85

(being debt debt written off by S.

keys)

3 09/02/20 Machinery A/c DR. 2300

To Bank 200

To TS CO. 2100

( Being machinery purchase with

cash Rs. 200 and 2100 on credit)

4 13/02/20 Cash account 220

Bad debts A/c 50

To S. hill Ltd. 270

( money owed by S. hill 270 and

paid only 220, Rs. 50 declare as

3

time, it records historical information or the actual cost of acquisition of assets. The value

of not always remains the same and it changes with the time. Financial accounting shows

inaccurate data and based on past transactions (Laudon and Traver, 2016).

PART 2

Journal entries with narration for the David wises:

Journal Entries

S. NO Date Particulars L.F £ £

1 01/02/20 purchase return A/C Dr. 350

To Purchase A/c 350

( Being purchase return with full

settlement)

2 04/02/20 Bad debts A/c Dr. 85

To S. keys A/c 85

(being debt debt written off by S.

keys)

3 09/02/20 Machinery A/c DR. 2300

To Bank 200

To TS CO. 2100

( Being machinery purchase with

cash Rs. 200 and 2100 on credit)

4 13/02/20 Cash account 220

Bad debts A/c 50

To S. hill Ltd. 270

( money owed by S. hill 270 and

paid only 220, Rs. 50 declare as

3

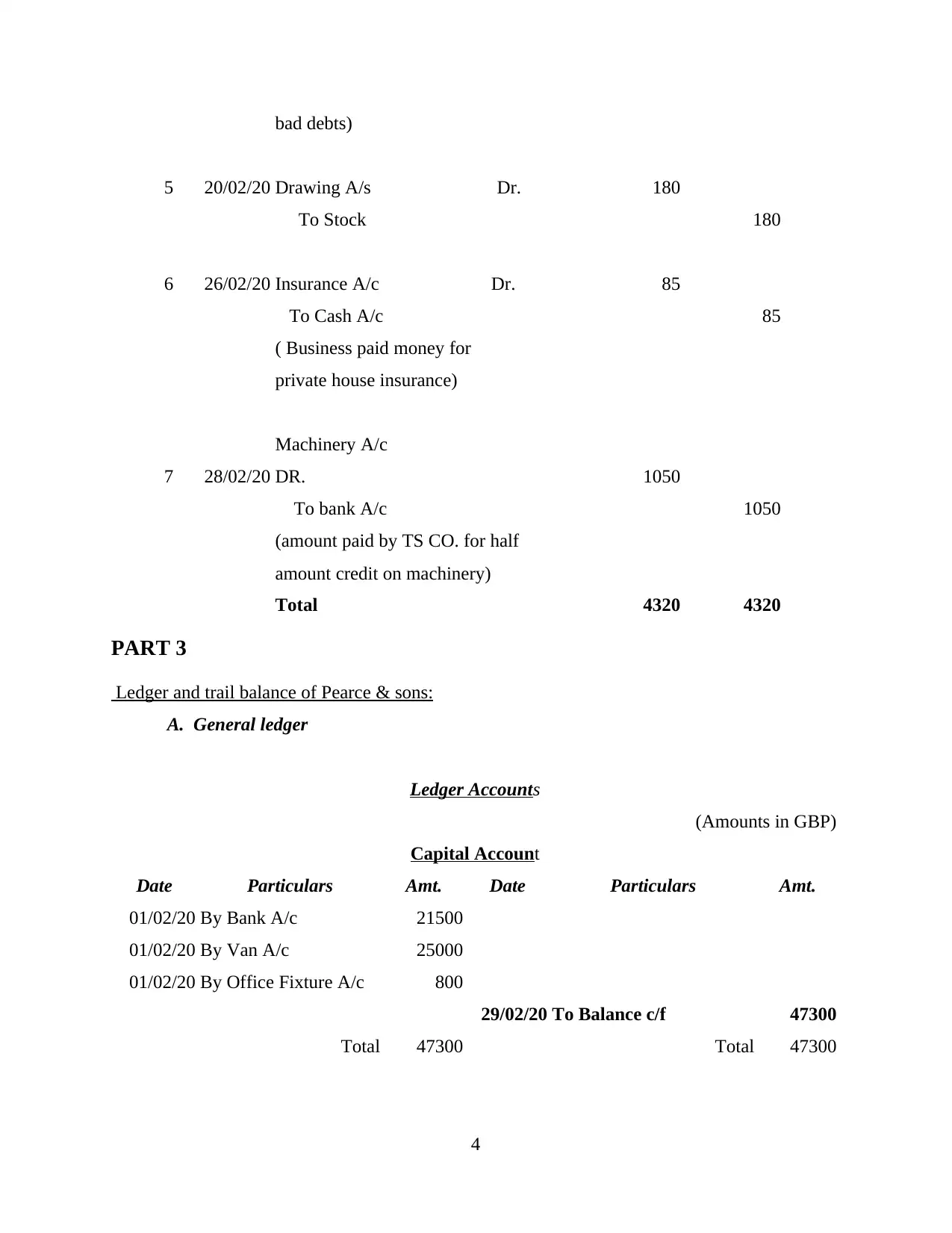

bad debts)

5 20/02/20 Drawing A/s Dr. 180

To Stock 180

6 26/02/20 Insurance A/c Dr. 85

To Cash A/c 85

( Business paid money for

private house insurance)

7 28/02/20

Machinery A/c

DR. 1050

To bank A/c 1050

(amount paid by TS CO. for half

amount credit on machinery)

Total 4320 4320

PART 3

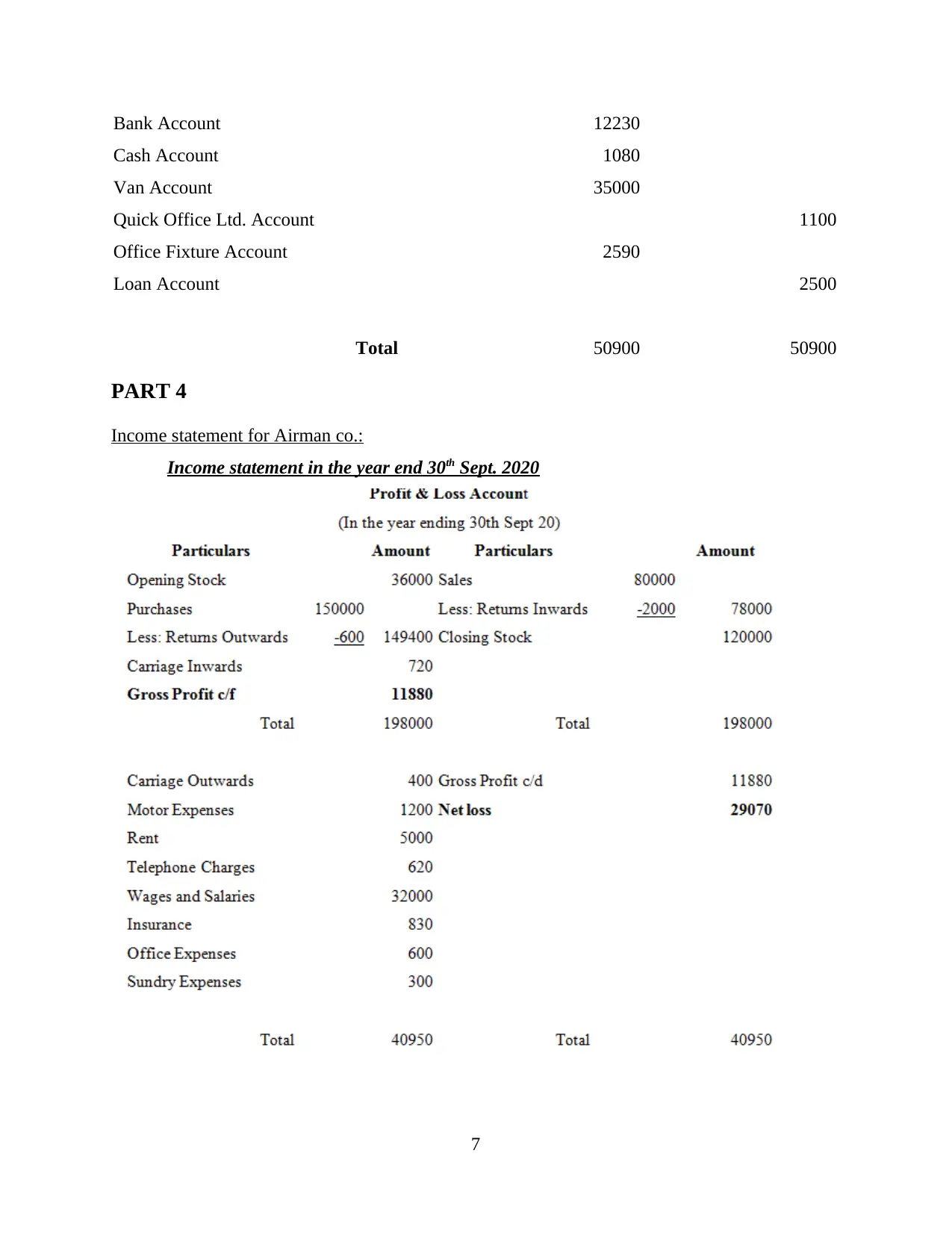

Ledger and trail balance of Pearce & sons:

A. General ledger

Ledger Accounts

(Amounts in GBP)

Capital Account

Date Particulars Amt. Date Particulars Amt.

01/02/20 By Bank A/c 21500

01/02/20 By Van A/c 25000

01/02/20 By Office Fixture A/c 800

29/02/20 To Balance c/f 47300

Total 47300 Total 47300

4

5 20/02/20 Drawing A/s Dr. 180

To Stock 180

6 26/02/20 Insurance A/c Dr. 85

To Cash A/c 85

( Business paid money for

private house insurance)

7 28/02/20

Machinery A/c

DR. 1050

To bank A/c 1050

(amount paid by TS CO. for half

amount credit on machinery)

Total 4320 4320

PART 3

Ledger and trail balance of Pearce & sons:

A. General ledger

Ledger Accounts

(Amounts in GBP)

Capital Account

Date Particulars Amt. Date Particulars Amt.

01/02/20 By Bank A/c 21500

01/02/20 By Van A/c 25000

01/02/20 By Office Fixture A/c 800

29/02/20 To Balance c/f 47300

Total 47300 Total 47300

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

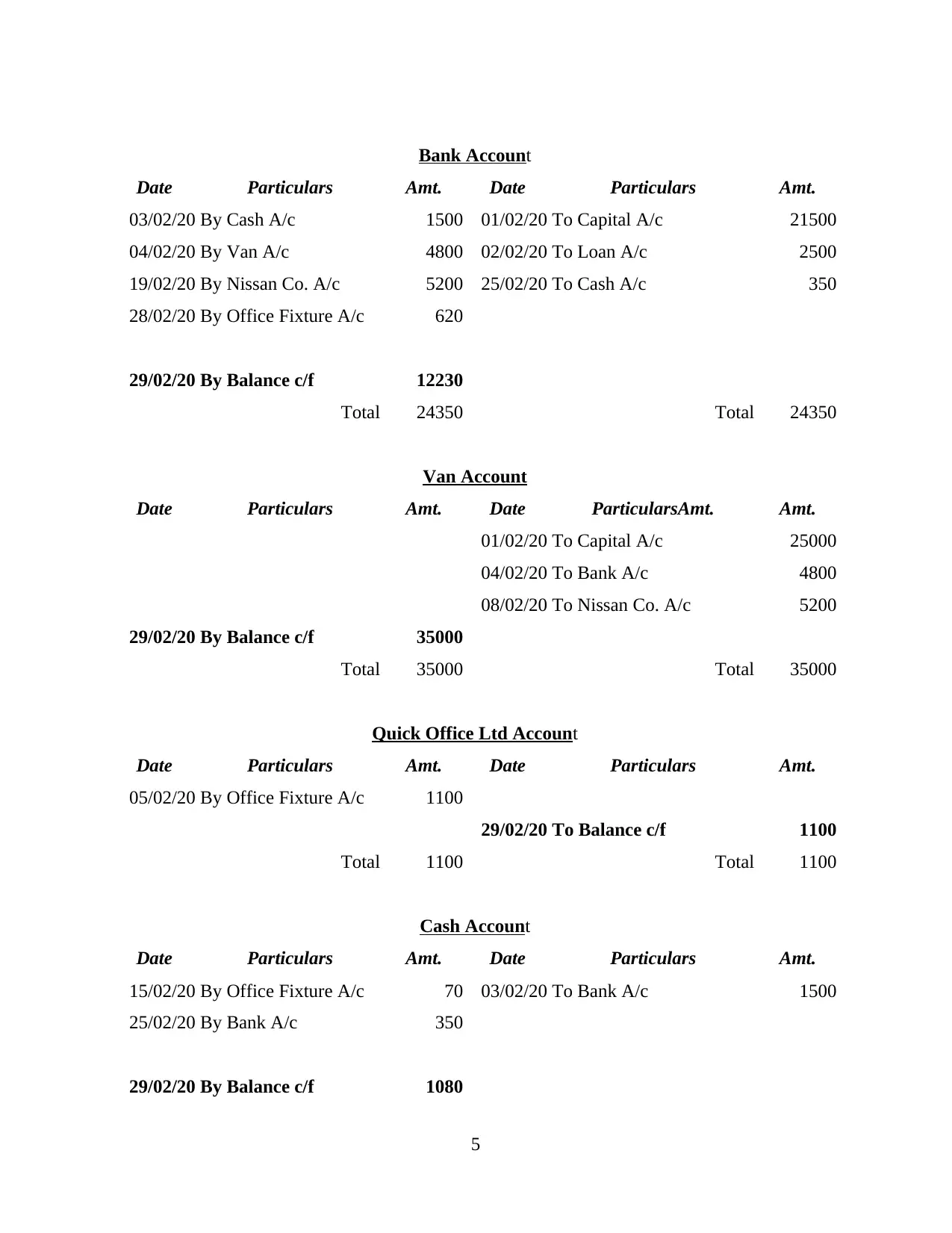

Bank Account

Date Particulars Amt. Date Particulars Amt.

03/02/20 By Cash A/c 1500 01/02/20 To Capital A/c 21500

04/02/20 By Van A/c 4800 02/02/20 To Loan A/c 2500

19/02/20 By Nissan Co. A/c 5200 25/02/20 To Cash A/c 350

28/02/20 By Office Fixture A/c 620

29/02/20 By Balance c/f 12230

Total 24350 Total 24350

Van Account

Date Particulars Amt. Date ParticularsAmt. Amt.

01/02/20 To Capital A/c 25000

04/02/20 To Bank A/c 4800

08/02/20 To Nissan Co. A/c 5200

29/02/20 By Balance c/f 35000

Total 35000 Total 35000

Quick Office Ltd Account

Date Particulars Amt. Date Particulars Amt.

05/02/20 By Office Fixture A/c 1100

29/02/20 To Balance c/f 1100

Total 1100 Total 1100

Cash Account

Date Particulars Amt. Date Particulars Amt.

15/02/20 By Office Fixture A/c 70 03/02/20 To Bank A/c 1500

25/02/20 By Bank A/c 350

29/02/20 By Balance c/f 1080

5

Date Particulars Amt. Date Particulars Amt.

03/02/20 By Cash A/c 1500 01/02/20 To Capital A/c 21500

04/02/20 By Van A/c 4800 02/02/20 To Loan A/c 2500

19/02/20 By Nissan Co. A/c 5200 25/02/20 To Cash A/c 350

28/02/20 By Office Fixture A/c 620

29/02/20 By Balance c/f 12230

Total 24350 Total 24350

Van Account

Date Particulars Amt. Date ParticularsAmt. Amt.

01/02/20 To Capital A/c 25000

04/02/20 To Bank A/c 4800

08/02/20 To Nissan Co. A/c 5200

29/02/20 By Balance c/f 35000

Total 35000 Total 35000

Quick Office Ltd Account

Date Particulars Amt. Date Particulars Amt.

05/02/20 By Office Fixture A/c 1100

29/02/20 To Balance c/f 1100

Total 1100 Total 1100

Cash Account

Date Particulars Amt. Date Particulars Amt.

15/02/20 By Office Fixture A/c 70 03/02/20 To Bank A/c 1500

25/02/20 By Bank A/c 350

29/02/20 By Balance c/f 1080

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

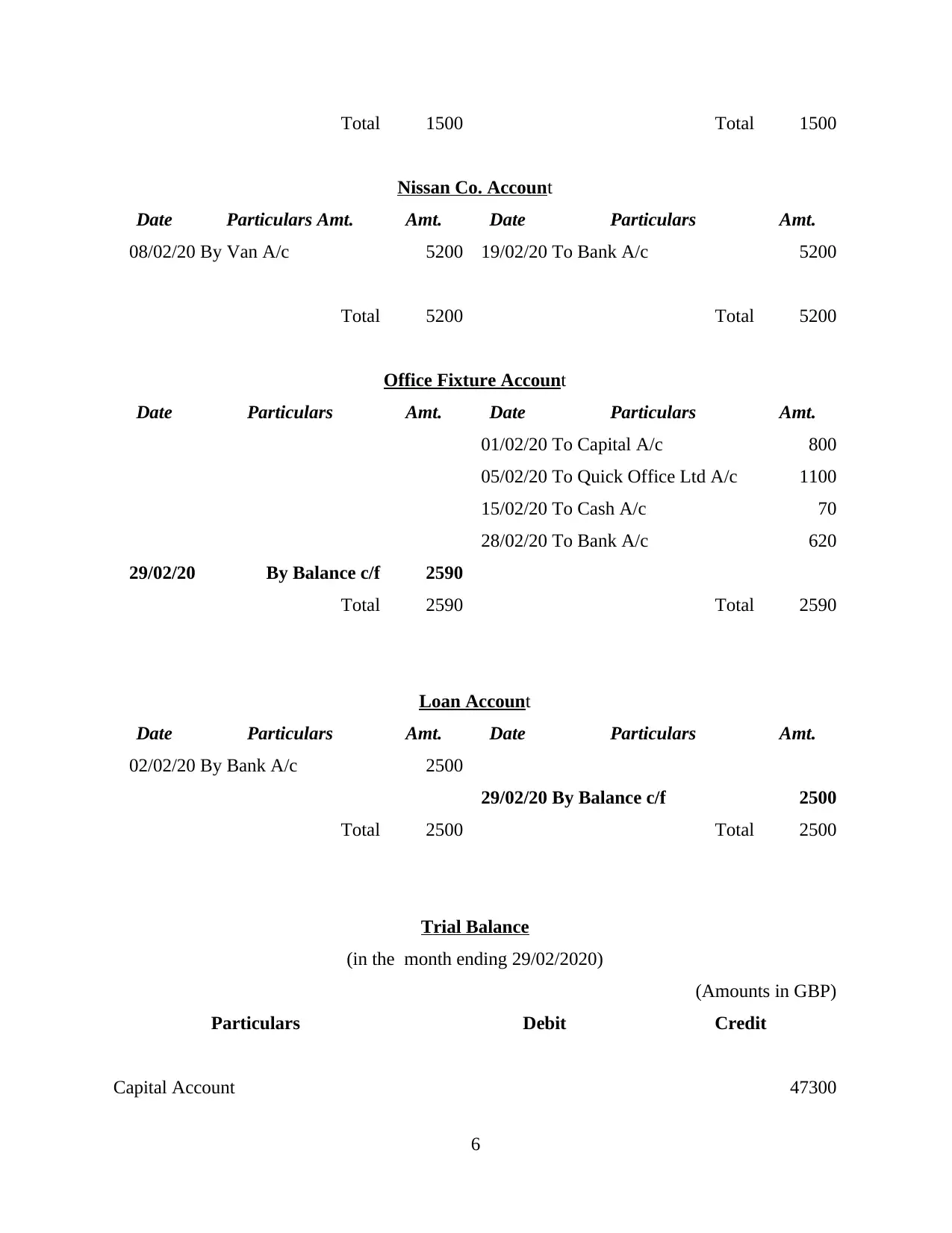

Total 1500 Total 1500

Nissan Co. Account

Date Particulars Amt. Amt. Date Particulars Amt.

08/02/20 By Van A/c 5200 19/02/20 To Bank A/c 5200

Total 5200 Total 5200

Office Fixture Account

Date Particulars Amt. Date Particulars Amt.

01/02/20 To Capital A/c 800

05/02/20 To Quick Office Ltd A/c 1100

15/02/20 To Cash A/c 70

28/02/20 To Bank A/c 620

29/02/20 By Balance c/f 2590

Total 2590 Total 2590

Loan Account

Date Particulars Amt. Date Particulars Amt.

02/02/20 By Bank A/c 2500

29/02/20 By Balance c/f 2500

Total 2500 Total 2500

Trial Balance

(in the month ending 29/02/2020)

(Amounts in GBP)

Particulars Debit Credit

Capital Account 47300

6

Nissan Co. Account

Date Particulars Amt. Amt. Date Particulars Amt.

08/02/20 By Van A/c 5200 19/02/20 To Bank A/c 5200

Total 5200 Total 5200

Office Fixture Account

Date Particulars Amt. Date Particulars Amt.

01/02/20 To Capital A/c 800

05/02/20 To Quick Office Ltd A/c 1100

15/02/20 To Cash A/c 70

28/02/20 To Bank A/c 620

29/02/20 By Balance c/f 2590

Total 2590 Total 2590

Loan Account

Date Particulars Amt. Date Particulars Amt.

02/02/20 By Bank A/c 2500

29/02/20 By Balance c/f 2500

Total 2500 Total 2500

Trial Balance

(in the month ending 29/02/2020)

(Amounts in GBP)

Particulars Debit Credit

Capital Account 47300

6

Bank Account 12230

Cash Account 1080

Van Account 35000

Quick Office Ltd. Account 1100

Office Fixture Account 2590

Loan Account 2500

Total 50900 50900

PART 4

Income statement for Airman co.:

Income statement in the year end 30th Sept. 2020

7

Cash Account 1080

Van Account 35000

Quick Office Ltd. Account 1100

Office Fixture Account 2590

Loan Account 2500

Total 50900 50900

PART 4

Income statement for Airman co.:

Income statement in the year end 30th Sept. 2020

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Impact of COVID 19 on company income statement items:

Every business can impacted by its internal and external environment. Internal

environment involves its culture, employees and activities. External environment refers political,

social, technological, economic, environmental and legal factors. As in year 2020 world has

faces COVID 19 that impacts businesses directly. Company Airman co. gain profits from last 10

year but in 2020 it faces various problems due to Lock down. It impacts on its sales and profits of

the company, it faces loss during the year. After march firms sales goes directly break down and

impacts the profitability of the company (Leemans and van der Aalst, 2015). Due to this situation

company has fire many employees because of no work in the company. COVID 19 makes

various financial and operational challenges for the organisations. It impacts business by

reducing cash flows with the manufacturing sector. Due to this, company faces financial

problems because of its less sales and it has to paid fixed charges as it is. Firm has potential

growth in half quarter but after Lockdown March, it has to close its selling, in that time online

selling were not considers also. Various people were staying at there homes without any

compensation that decreases cuistomers demand towards purchasing goods and services that is

the reason for reducing sales (Levin and Light, eds., 2015).

ASSESSMENT 2

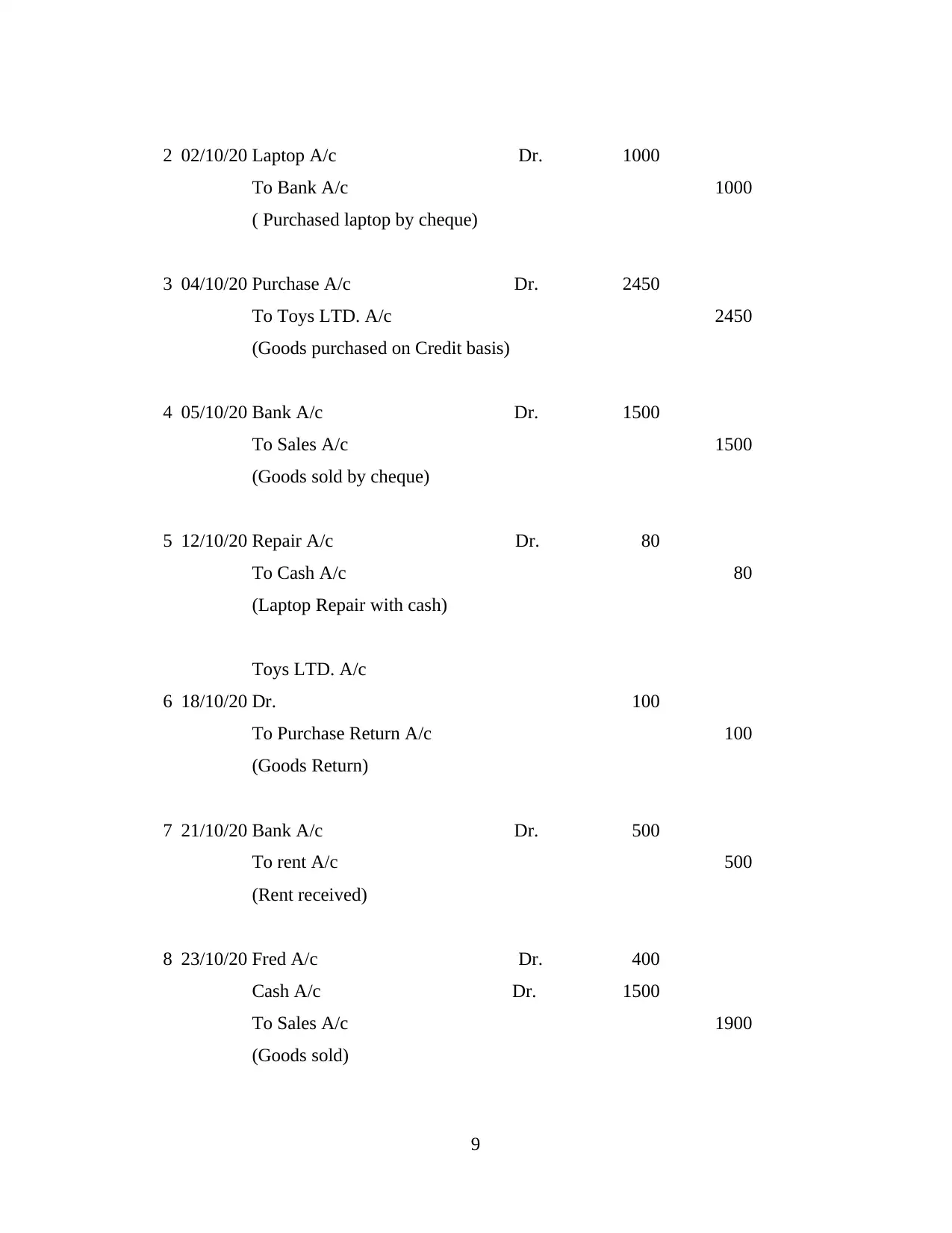

PART A

Journal transactions of T- accounts:

JOURNAL ENTRIES

S.NO Date Particulars L.F £ £

2020

1 01/10/20 Cash A/c Dr. 5200

Bank A/c Dr. 8000

Van A/c Dr. 3000

To Capital A/c 16200

(Capital invested into business)

8

Every business can impacted by its internal and external environment. Internal

environment involves its culture, employees and activities. External environment refers political,

social, technological, economic, environmental and legal factors. As in year 2020 world has

faces COVID 19 that impacts businesses directly. Company Airman co. gain profits from last 10

year but in 2020 it faces various problems due to Lock down. It impacts on its sales and profits of

the company, it faces loss during the year. After march firms sales goes directly break down and

impacts the profitability of the company (Leemans and van der Aalst, 2015). Due to this situation

company has fire many employees because of no work in the company. COVID 19 makes

various financial and operational challenges for the organisations. It impacts business by

reducing cash flows with the manufacturing sector. Due to this, company faces financial

problems because of its less sales and it has to paid fixed charges as it is. Firm has potential

growth in half quarter but after Lockdown March, it has to close its selling, in that time online

selling were not considers also. Various people were staying at there homes without any

compensation that decreases cuistomers demand towards purchasing goods and services that is

the reason for reducing sales (Levin and Light, eds., 2015).

ASSESSMENT 2

PART A

Journal transactions of T- accounts:

JOURNAL ENTRIES

S.NO Date Particulars L.F £ £

2020

1 01/10/20 Cash A/c Dr. 5200

Bank A/c Dr. 8000

Van A/c Dr. 3000

To Capital A/c 16200

(Capital invested into business)

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2 02/10/20 Laptop A/c Dr. 1000

To Bank A/c 1000

( Purchased laptop by cheque)

3 04/10/20 Purchase A/c Dr. 2450

To Toys LTD. A/c 2450

(Goods purchased on Credit basis)

4 05/10/20 Bank A/c Dr. 1500

To Sales A/c 1500

(Goods sold by cheque)

5 12/10/20 Repair A/c Dr. 80

To Cash A/c 80

(Laptop Repair with cash)

6 18/10/20

Toys LTD. A/c

Dr. 100

To Purchase Return A/c 100

(Goods Return)

7 21/10/20 Bank A/c Dr. 500

To rent A/c 500

(Rent received)

8 23/10/20 Fred A/c Dr. 400

Cash A/c Dr. 1500

To Sales A/c 1900

(Goods sold)

9

To Bank A/c 1000

( Purchased laptop by cheque)

3 04/10/20 Purchase A/c Dr. 2450

To Toys LTD. A/c 2450

(Goods purchased on Credit basis)

4 05/10/20 Bank A/c Dr. 1500

To Sales A/c 1500

(Goods sold by cheque)

5 12/10/20 Repair A/c Dr. 80

To Cash A/c 80

(Laptop Repair with cash)

6 18/10/20

Toys LTD. A/c

Dr. 100

To Purchase Return A/c 100

(Goods Return)

7 21/10/20 Bank A/c Dr. 500

To rent A/c 500

(Rent received)

8 23/10/20 Fred A/c Dr. 400

Cash A/c Dr. 1500

To Sales A/c 1900

(Goods sold)

9

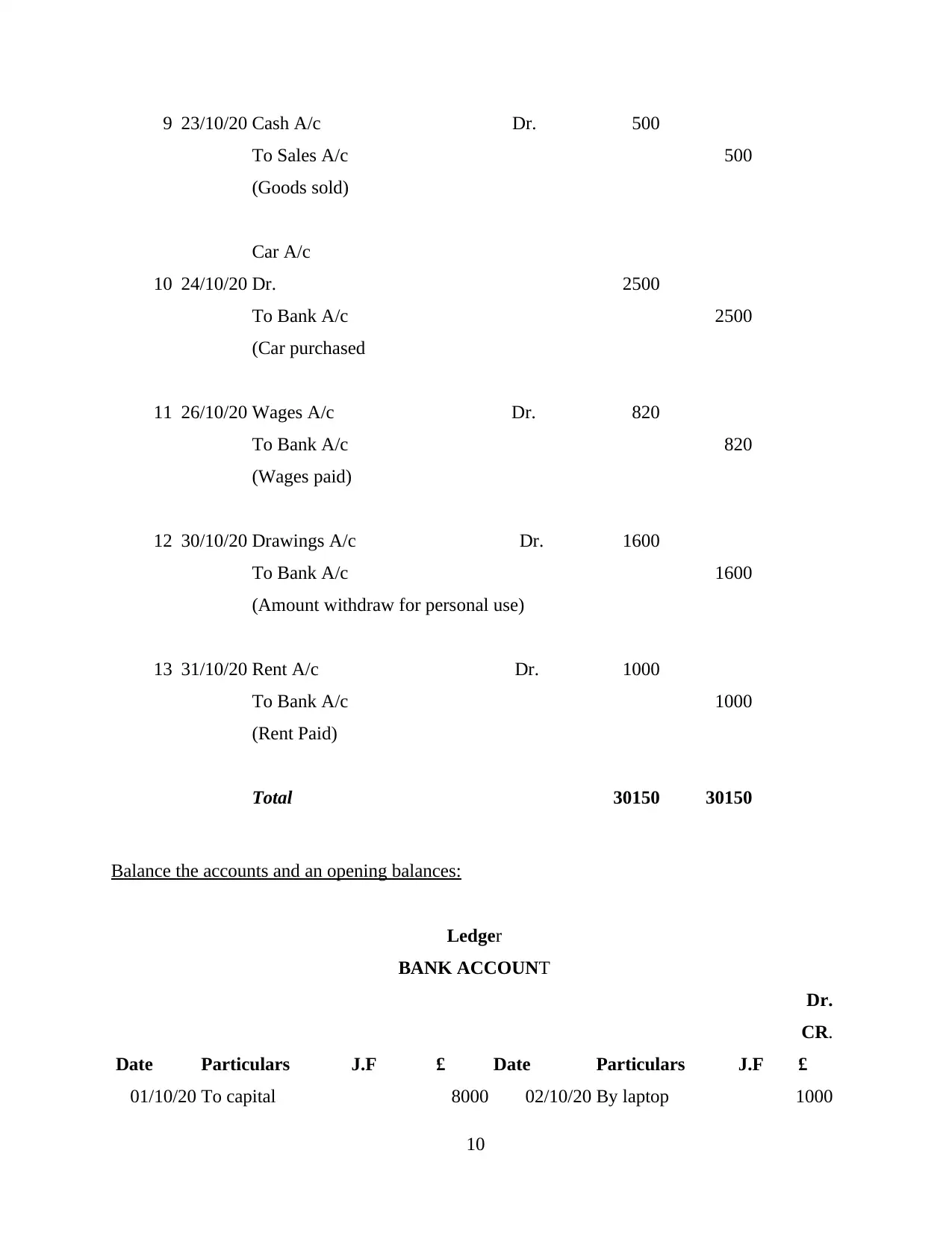

9 23/10/20 Cash A/c Dr. 500

To Sales A/c 500

(Goods sold)

10 24/10/20

Car A/c

Dr. 2500

To Bank A/c 2500

(Car purchased

11 26/10/20 Wages A/c Dr. 820

To Bank A/c 820

(Wages paid)

12 30/10/20 Drawings A/c Dr. 1600

To Bank A/c 1600

(Amount withdraw for personal use)

13 31/10/20 Rent A/c Dr. 1000

To Bank A/c 1000

(Rent Paid)

Total 30150 30150

Balance the accounts and an opening balances:

Ledger

BANK ACCOUNT

Dr.

CR.

Date Particulars J.F £ Date Particulars J.F £

01/10/20 To capital 8000 02/10/20 By laptop 1000

10

To Sales A/c 500

(Goods sold)

10 24/10/20

Car A/c

Dr. 2500

To Bank A/c 2500

(Car purchased

11 26/10/20 Wages A/c Dr. 820

To Bank A/c 820

(Wages paid)

12 30/10/20 Drawings A/c Dr. 1600

To Bank A/c 1600

(Amount withdraw for personal use)

13 31/10/20 Rent A/c Dr. 1000

To Bank A/c 1000

(Rent Paid)

Total 30150 30150

Balance the accounts and an opening balances:

Ledger

BANK ACCOUNT

Dr.

CR.

Date Particulars J.F £ Date Particulars J.F £

01/10/20 To capital 8000 02/10/20 By laptop 1000

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 23

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.