BA30592E Recording Business Transactions - University of West London

VerifiedAdded on 2023/04/06

|16

|2195

|182

Practical Assignment

AI Summary

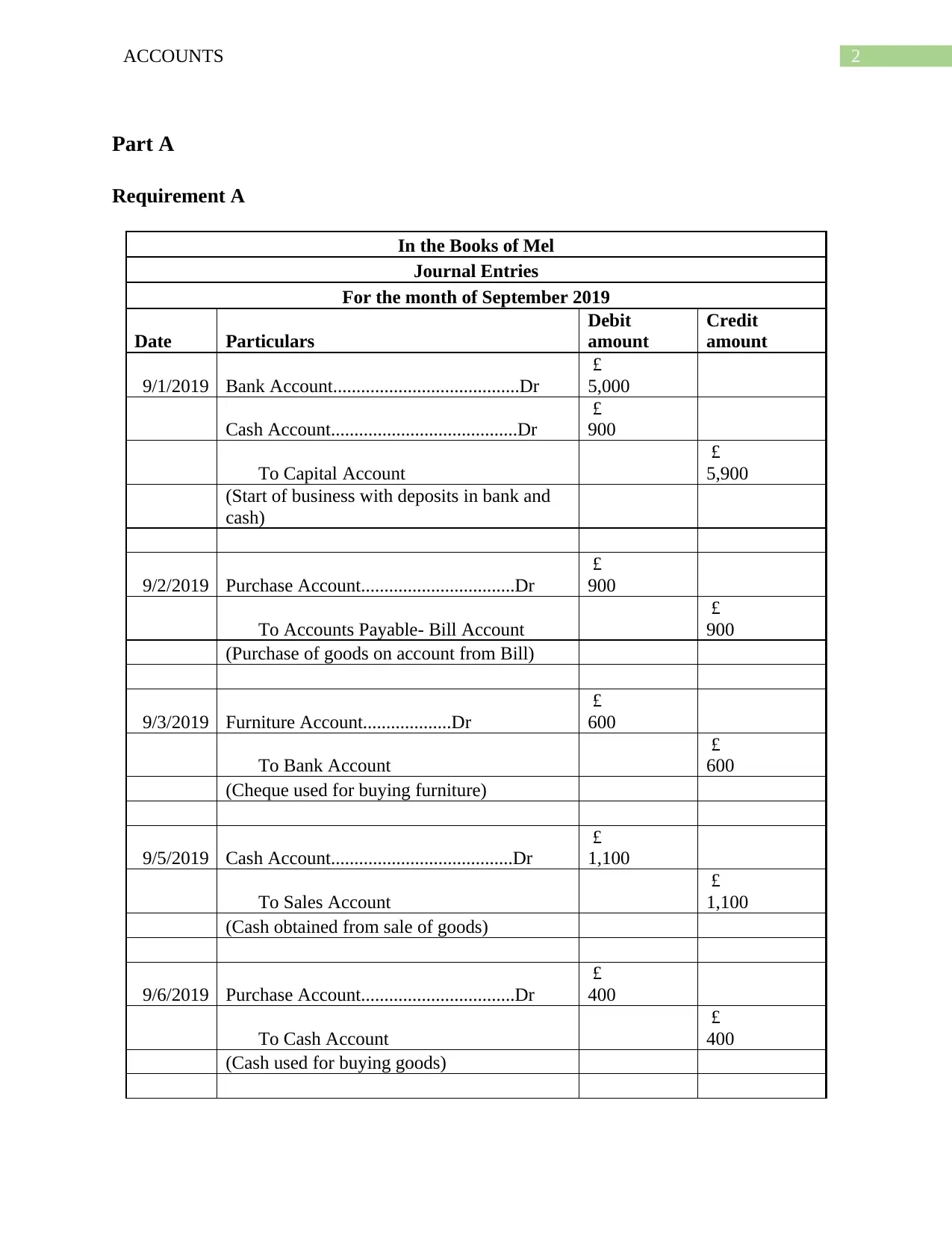

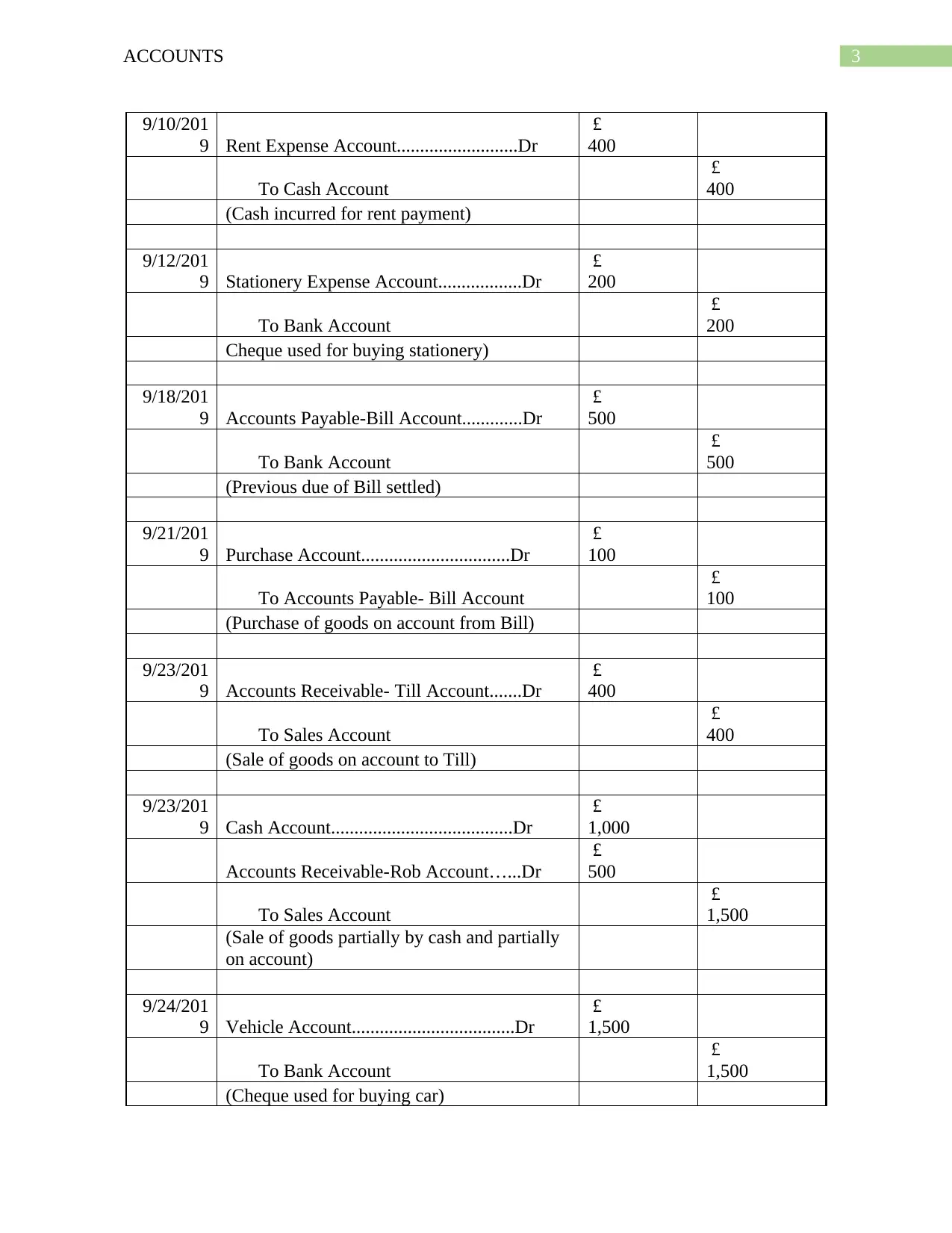

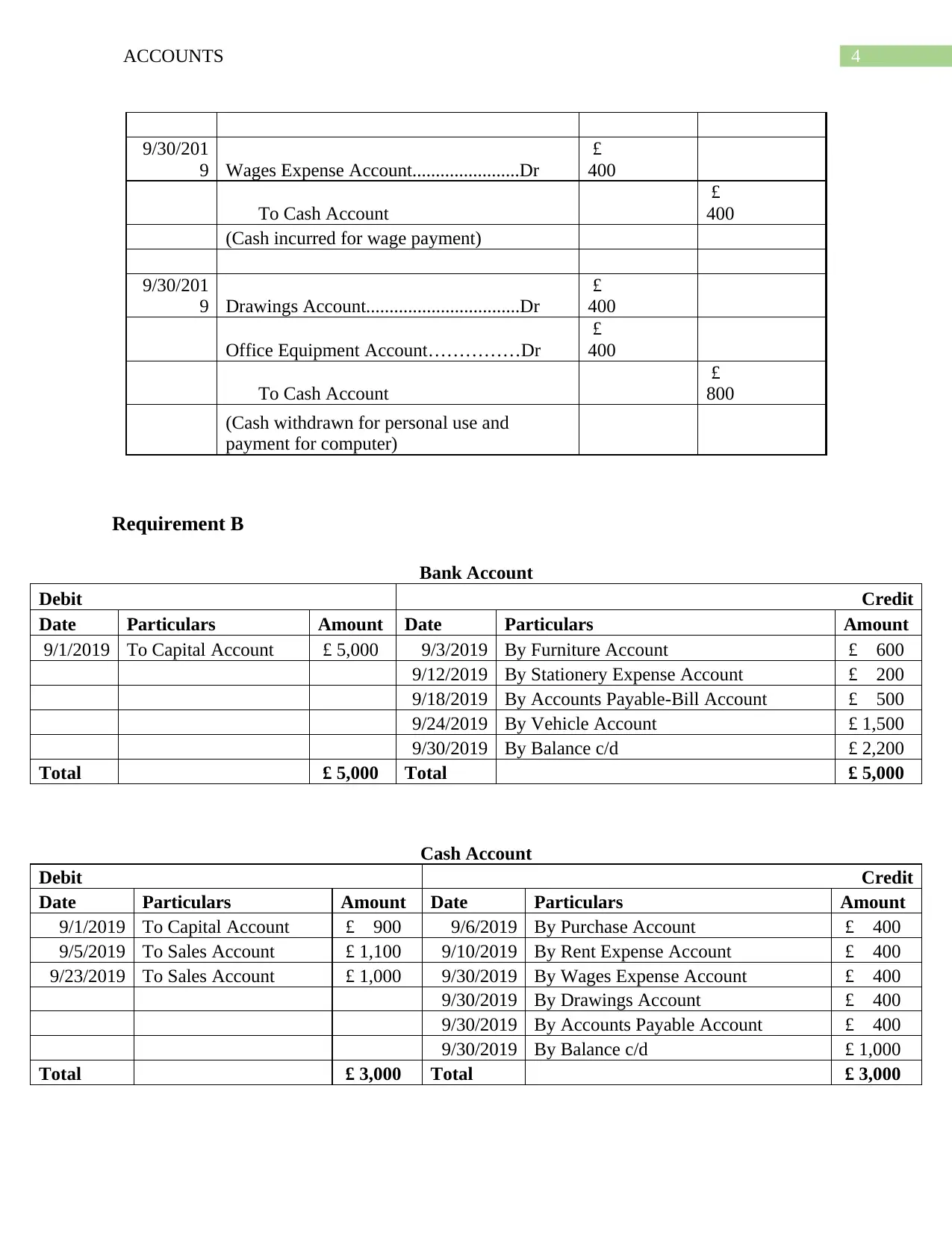

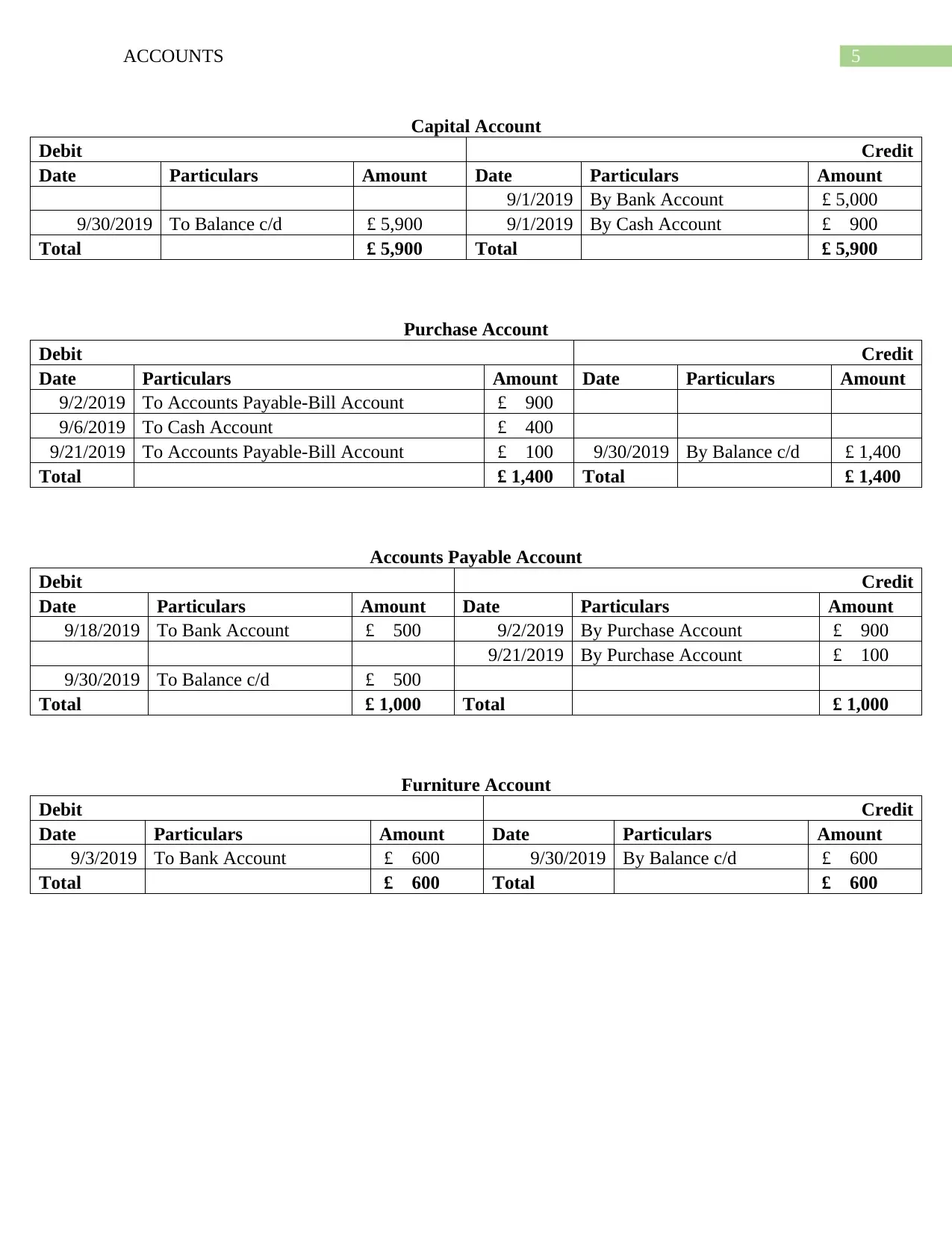

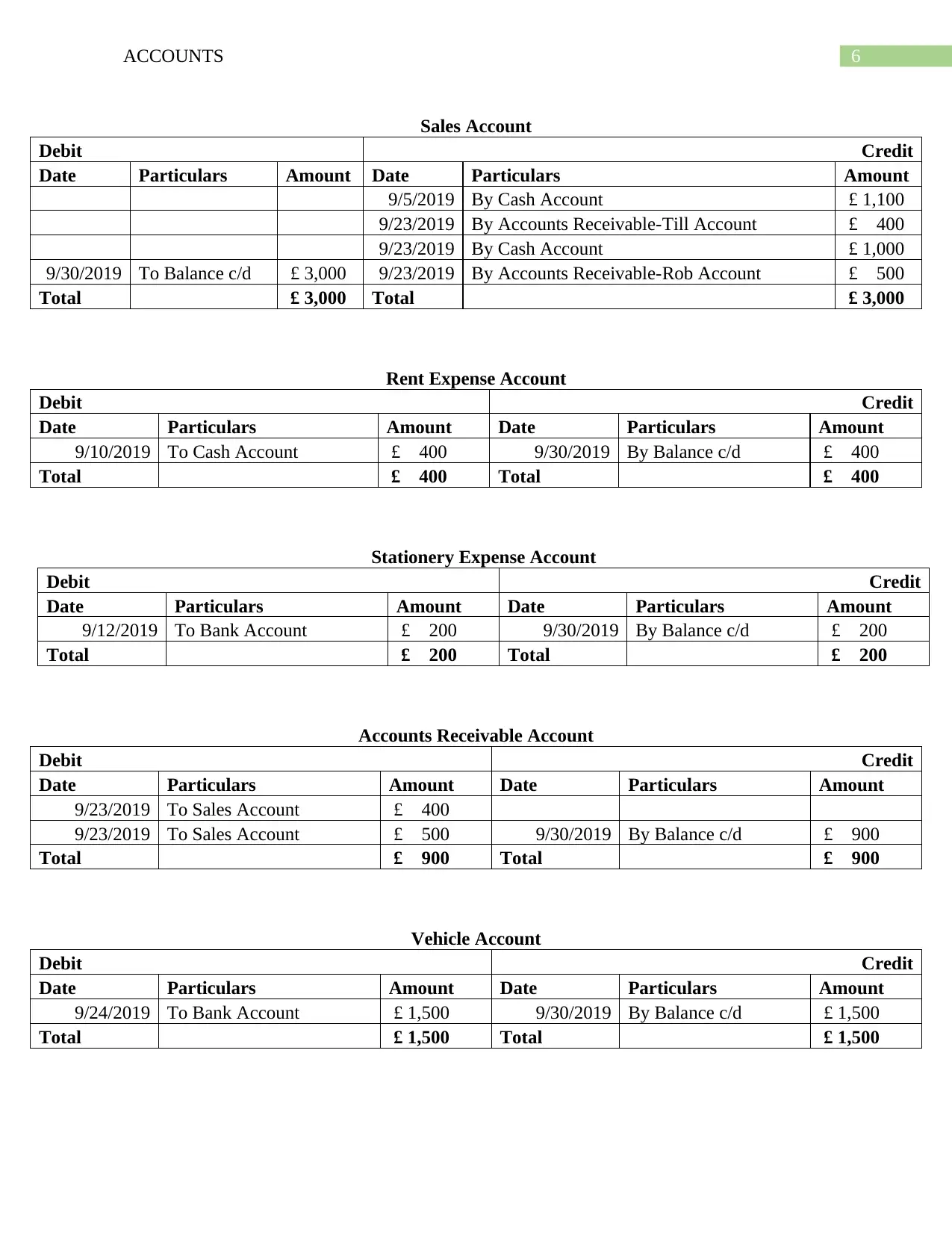

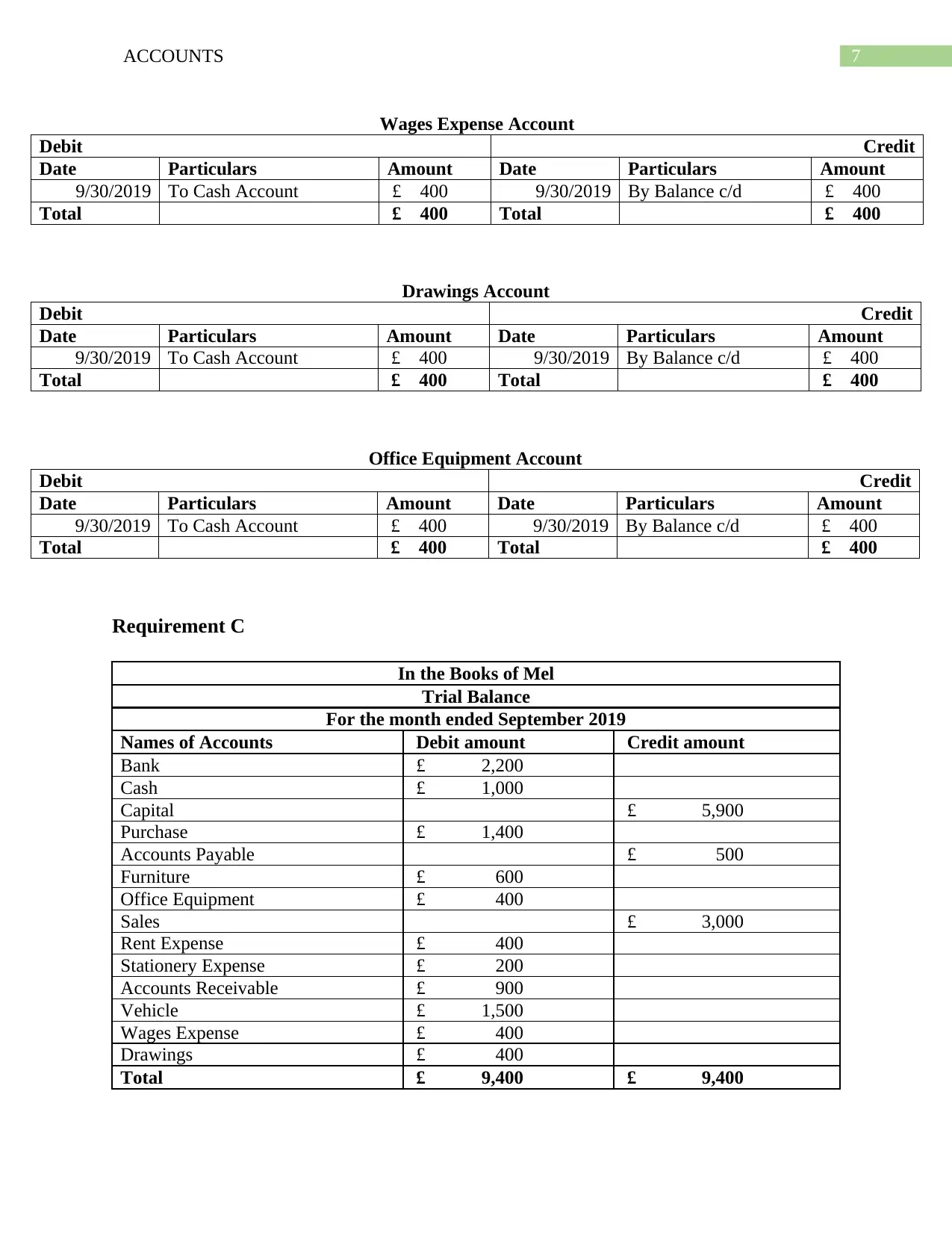

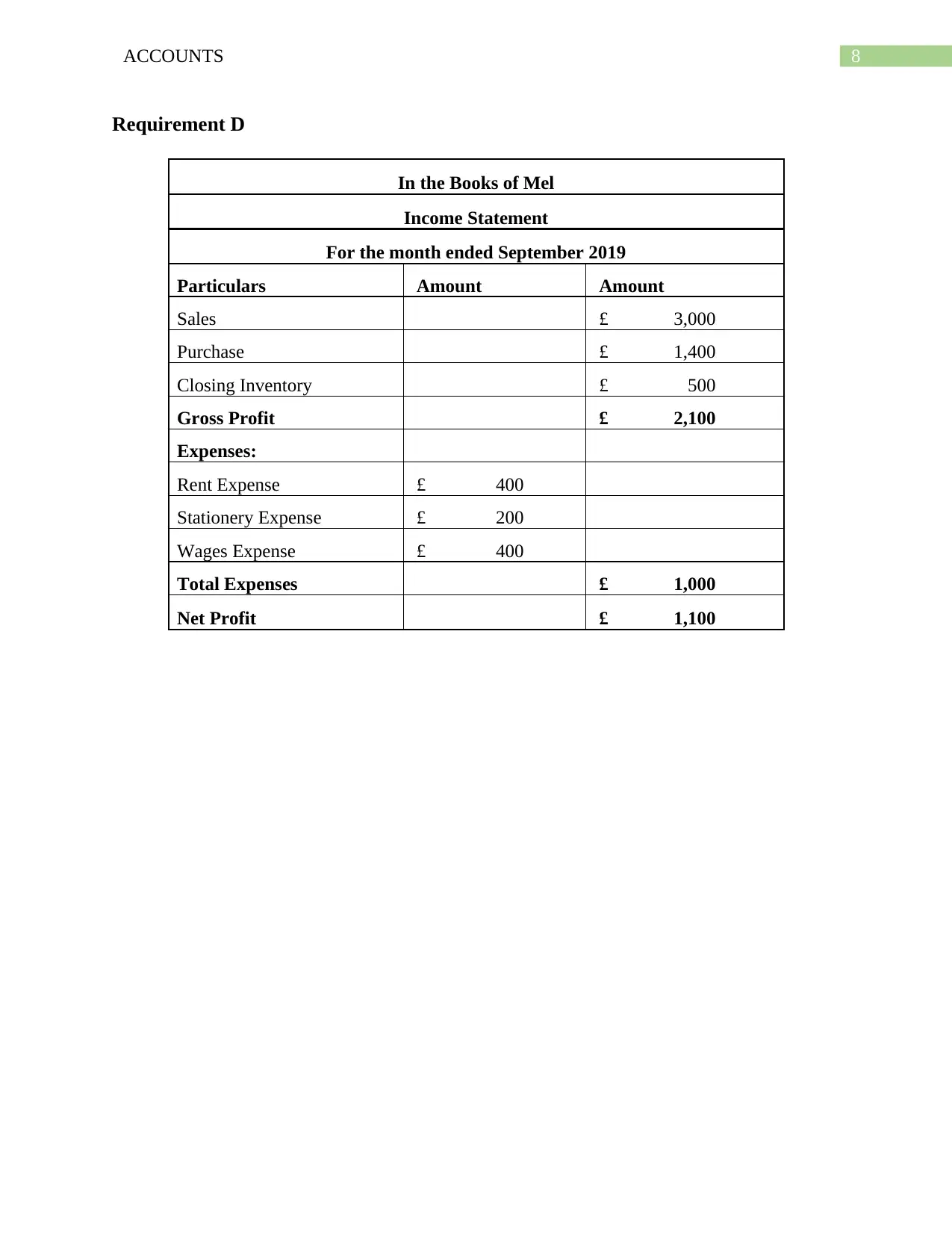

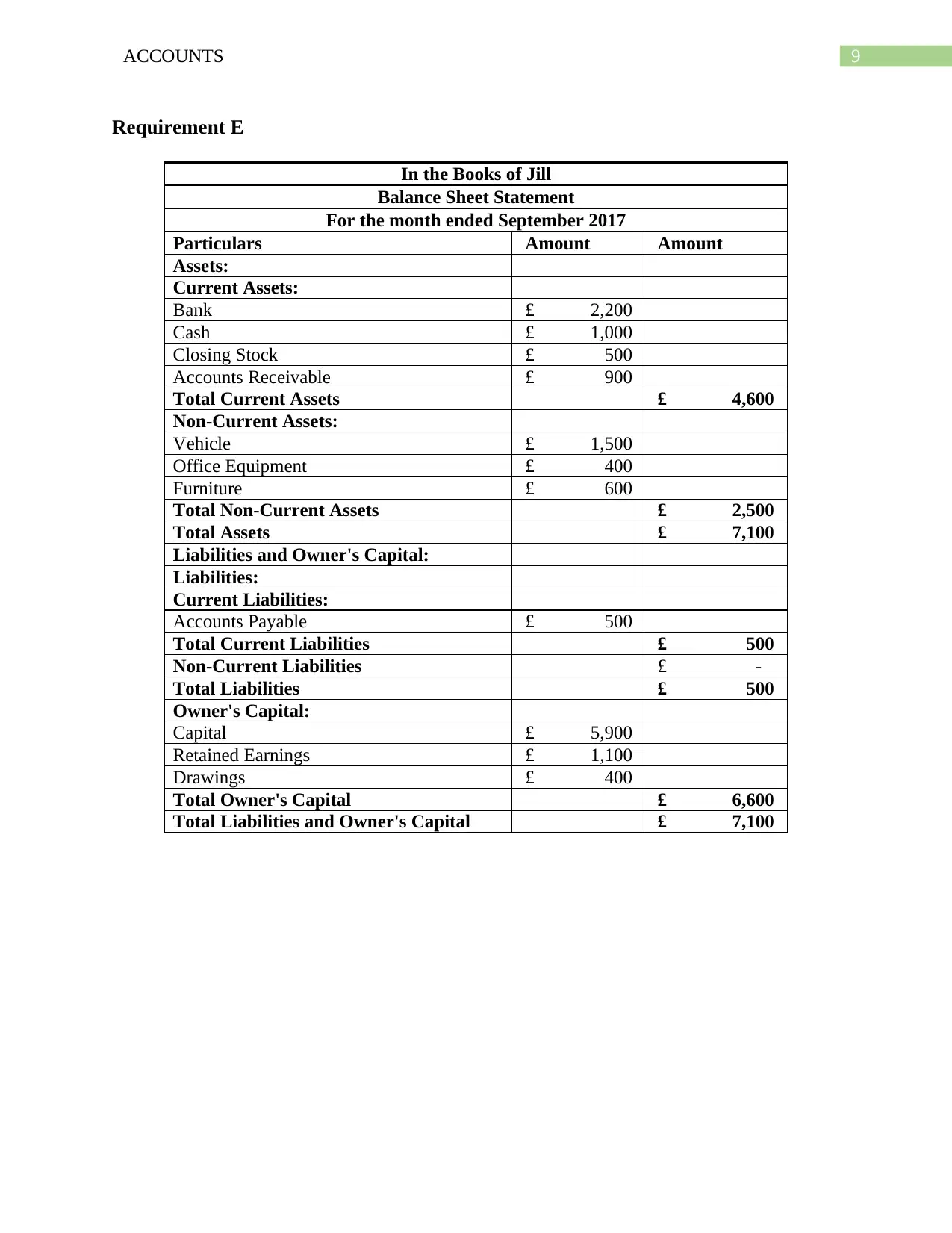

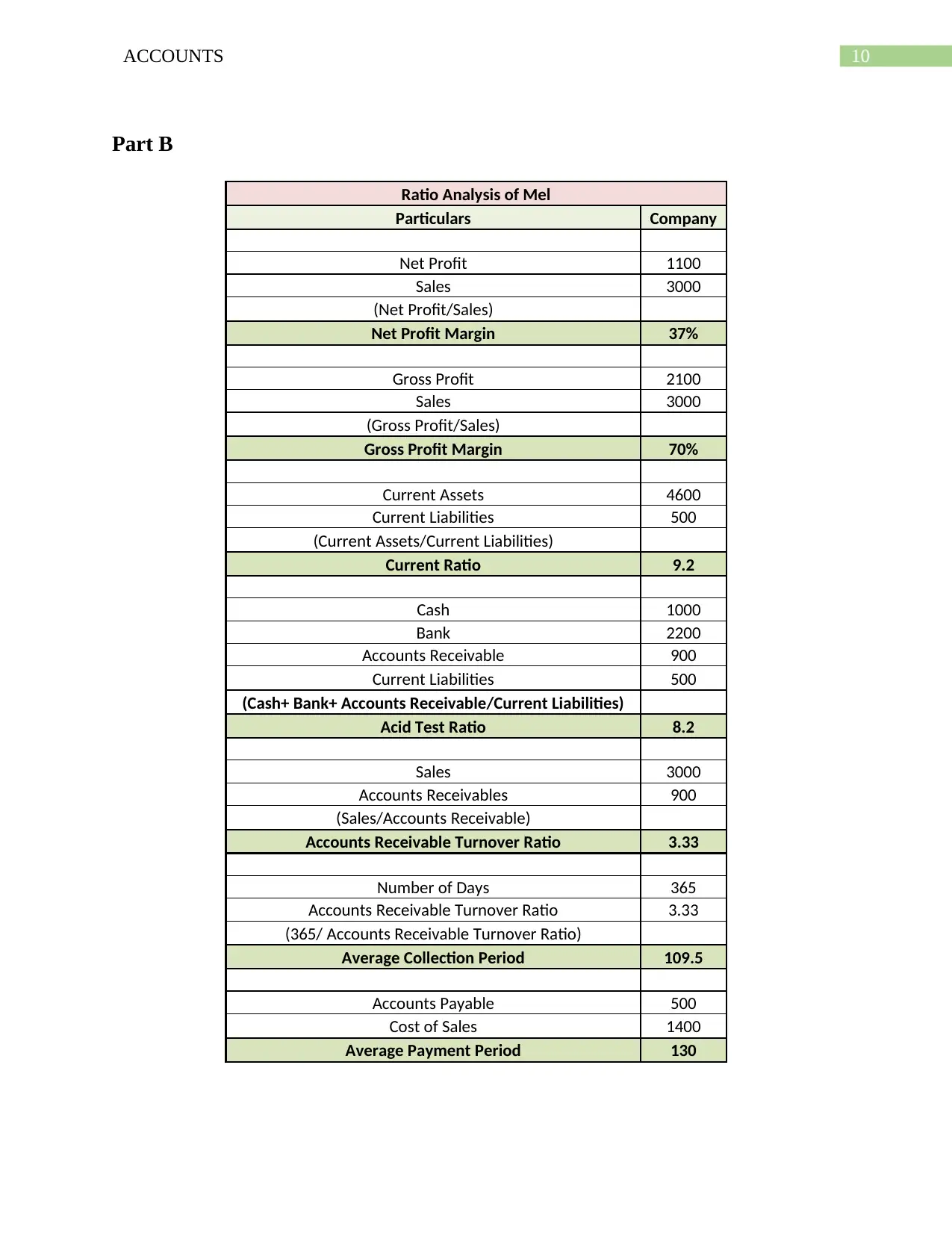

This assignment provides a detailed solution to a practical accounting problem involving the recording of business transactions for Mel, who commences trading on October 1, 2018. The solution includes journal entries for September 2019, T-accounts, a trial balance, an income statement, and a balance sheet. Additionally, the assignment includes a ratio analysis of Mel's financial performance, covering key metrics such as net profit margin, gross profit margin, current ratio, acid test ratio, accounts receivable turnover, and accounts payable payment period. Finally, a financial analysis of Jill’s company is conducted, comparing its performance against competitors, focusing on net profit margin, gross profit margin, current ratio, acid test ratio, accounts receivable collection period, and accounts payable payment period. This document is available on Desklib, a platform offering a range of study tools and solved assignments for students.

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.