Analysis of Recording Business Transactions and Financial Statements

VerifiedAdded on 2022/12/28

|13

|2154

|37

Report

AI Summary

This report provides a comprehensive analysis of recording business transactions and preparing financial statements. It begins with an introduction to business transactions and the importance of accounting information for decision-makers, including advantages and disadvantages of recording accounting information. The report then presents journal entries with narrations for specific transactions, followed by the creation of ledgers and a trial balance. Furthermore, it includes the preparation of income statements and examines the impact of COVID-19 on various income statement items. The report also covers the creation of T-accounts, balance sheets, and ratio calculations. Finally, it offers a conclusion summarizing the key findings and references the sources used throughout the analysis. The report covers a wide range of financial accounting topics, providing a thorough understanding of the subject matter.

RECORDING

BUSINESS

TRANSACTIONS

BUSINESS

TRANSACTIONS

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

ASSESSMENT 1.............................................................................................................................3

PART 1............................................................................................................................................3

Decision makers and their need for accounting information..................................................3

Advantage and Disadvantage of recording accounting information......................................4

PART 2............................................................................................................................................4

Journal entries with narration for the David wises.................................................................4

PART 3............................................................................................................................................5

Ledger and trail balance of Pearce & sons:...........................................................................5

PART 4 ...........................................................................................................................................7

Income statement for Airman co............................................................................................7

Impact of COVID 19 on company income statement items...................................................7

ASSESSMENT 2.............................................................................................................................8

PART A...........................................................................................................................................8

Journal transaction of T- accounts..........................................................................................8

Balance the accounts and an opening balances......................................................................9

Trial balance.........................................................................................................................12

Income statement for the period 31 Oct. 2020.....................................................................13

Preparation of financial position 31 Oct. 2020.....................................................................13

PART B..........................................................................................................................................13

Ratio calculation for Linda's business..................................................................................13

Analysis of ratio analysis in comparison to it's competitors ...............................................14

CONCLUSION..............................................................................................................................15

REFERENCES .............................................................................................................................16

INTRODUCTION...........................................................................................................................3

ASSESSMENT 1.............................................................................................................................3

PART 1............................................................................................................................................3

Decision makers and their need for accounting information..................................................3

Advantage and Disadvantage of recording accounting information......................................4

PART 2............................................................................................................................................4

Journal entries with narration for the David wises.................................................................4

PART 3............................................................................................................................................5

Ledger and trail balance of Pearce & sons:...........................................................................5

PART 4 ...........................................................................................................................................7

Income statement for Airman co............................................................................................7

Impact of COVID 19 on company income statement items...................................................7

ASSESSMENT 2.............................................................................................................................8

PART A...........................................................................................................................................8

Journal transaction of T- accounts..........................................................................................8

Balance the accounts and an opening balances......................................................................9

Trial balance.........................................................................................................................12

Income statement for the period 31 Oct. 2020.....................................................................13

Preparation of financial position 31 Oct. 2020.....................................................................13

PART B..........................................................................................................................................13

Ratio calculation for Linda's business..................................................................................13

Analysis of ratio analysis in comparison to it's competitors ...............................................14

CONCLUSION..............................................................................................................................15

REFERENCES .............................................................................................................................16

INTRODUCTION

A business transaction is referred to as day to day activities done in a business firm which

includes transfer of money, goods as well as services between two or more then two parties.

These transactions are measured in money and are been recorded for maintaining transparency of

the business firm. Management of sound business firm records and displays its report of financial

activities of the organisation (Prodanova and et. al., 2019).

ASSESSMENT 1

PART 1

Decision makers and their need for accounting information

Accounting plays an important role in enhancing effectiveness of a business firm. It

allows its managers and leaders to take respective decisions in various operational activities of

the business firm. Financial accounting is an element of accounting which forms basics of

operational activities of the business enterprise (Drake, Quinn and Thornock, 2017). Under

standard guidelines of accounting systems, transactions of business firms are been recorded,

summarized and then are presented in financial statements such as P&L account, balance sheet

of the company and many more. There are so many ways to prepare financial statements of

respective companies. However to provide comparative and competitive differences some

universal set of financial statements are been prepared (Dabbicco, 2018). It proves to be an

important tool for management of companies to make respective decisions by providing with

statical data in planning structure of firm. As competition plays crucial role in deciding up of

success or failures of firm's strategies and policies, financial statements provides reliable

information about facts and figures to perform better than their competitors and helps in boosting

up of net profits of an organisation.

Financial accounts displays all monetary information related to operational activities of

the workforce. Respective decision making of various firm's depends on information been

extracted from financial statements of company (Maroun, 2017). By distinctive preparation of

financial statements of a business firm, this enables firm's leaders and managers to make

effective strategies to give a string fight to company’s competitors.

A business transaction is referred to as day to day activities done in a business firm which

includes transfer of money, goods as well as services between two or more then two parties.

These transactions are measured in money and are been recorded for maintaining transparency of

the business firm. Management of sound business firm records and displays its report of financial

activities of the organisation (Prodanova and et. al., 2019).

ASSESSMENT 1

PART 1

Decision makers and their need for accounting information

Accounting plays an important role in enhancing effectiveness of a business firm. It

allows its managers and leaders to take respective decisions in various operational activities of

the business firm. Financial accounting is an element of accounting which forms basics of

operational activities of the business enterprise (Drake, Quinn and Thornock, 2017). Under

standard guidelines of accounting systems, transactions of business firms are been recorded,

summarized and then are presented in financial statements such as P&L account, balance sheet

of the company and many more. There are so many ways to prepare financial statements of

respective companies. However to provide comparative and competitive differences some

universal set of financial statements are been prepared (Dabbicco, 2018). It proves to be an

important tool for management of companies to make respective decisions by providing with

statical data in planning structure of firm. As competition plays crucial role in deciding up of

success or failures of firm's strategies and policies, financial statements provides reliable

information about facts and figures to perform better than their competitors and helps in boosting

up of net profits of an organisation.

Financial accounts displays all monetary information related to operational activities of

the workforce. Respective decision making of various firm's depends on information been

extracted from financial statements of company (Maroun, 2017). By distinctive preparation of

financial statements of a business firm, this enables firm's leaders and managers to make

effective strategies to give a string fight to company’s competitors.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Advantage and Disadvantage of recording accounting information

Accounting information refers to the data about various financial activities conducted by a

business organisation. Accounting information is used by individuals which are associated with

the organisation such as shareholders, managers and employees (Kwilinski, 2019). This data is

also accessed by individuals which are not associated with the company such as government

authorities, regulation agencies and news reporters.

Advantage of recording accounting information

1) Formulation of financial report:

Keeping detailed record of various accounting information allows corporations to formulate

precise and accurate financial reports. Such financial reports give the organisation insight about

their net earnings and overall expenditures of the company.

2) Comparing previous data: Recording financial information in a detailed and precise manner

allows corporations to compare current financial position of the company with financial situation

of past year. This helps the company evaluate their growth and effect of policy changes on

financial situation of the organization.

3) Improves decision making: Another advantage of recording accounting information is that it

helps organizations improve their decision making process by giving them detailed insight about

their current and past financial conditions.

Disadvantages of recording financial information:

1) Inability to express non-financial transactions: Recording accounting information is limited to

expressing each business transaction as the monetary value it denotes. This excludes important

information which cannot be defined by monetary terms.

2) Misuse of data: Accounting information can be easily manipulated and controlled to showcase

incorrect financial position of the company (International Labour Organisation, 2020). By

controlling such information cheaters and criminals can easily defraud the corporation.

3) Involvement Personal Bias: Records of accounting information are not protected from

personal bias, prejudiced opinions and errors of employees. This increases inaccuracy of such

records and effectiveness of decisions formed on the basis of such records.

Accounting information refers to the data about various financial activities conducted by a

business organisation. Accounting information is used by individuals which are associated with

the organisation such as shareholders, managers and employees (Kwilinski, 2019). This data is

also accessed by individuals which are not associated with the company such as government

authorities, regulation agencies and news reporters.

Advantage of recording accounting information

1) Formulation of financial report:

Keeping detailed record of various accounting information allows corporations to formulate

precise and accurate financial reports. Such financial reports give the organisation insight about

their net earnings and overall expenditures of the company.

2) Comparing previous data: Recording financial information in a detailed and precise manner

allows corporations to compare current financial position of the company with financial situation

of past year. This helps the company evaluate their growth and effect of policy changes on

financial situation of the organization.

3) Improves decision making: Another advantage of recording accounting information is that it

helps organizations improve their decision making process by giving them detailed insight about

their current and past financial conditions.

Disadvantages of recording financial information:

1) Inability to express non-financial transactions: Recording accounting information is limited to

expressing each business transaction as the monetary value it denotes. This excludes important

information which cannot be defined by monetary terms.

2) Misuse of data: Accounting information can be easily manipulated and controlled to showcase

incorrect financial position of the company (International Labour Organisation, 2020). By

controlling such information cheaters and criminals can easily defraud the corporation.

3) Involvement Personal Bias: Records of accounting information are not protected from

personal bias, prejudiced opinions and errors of employees. This increases inaccuracy of such

records and effectiveness of decisions formed on the basis of such records.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

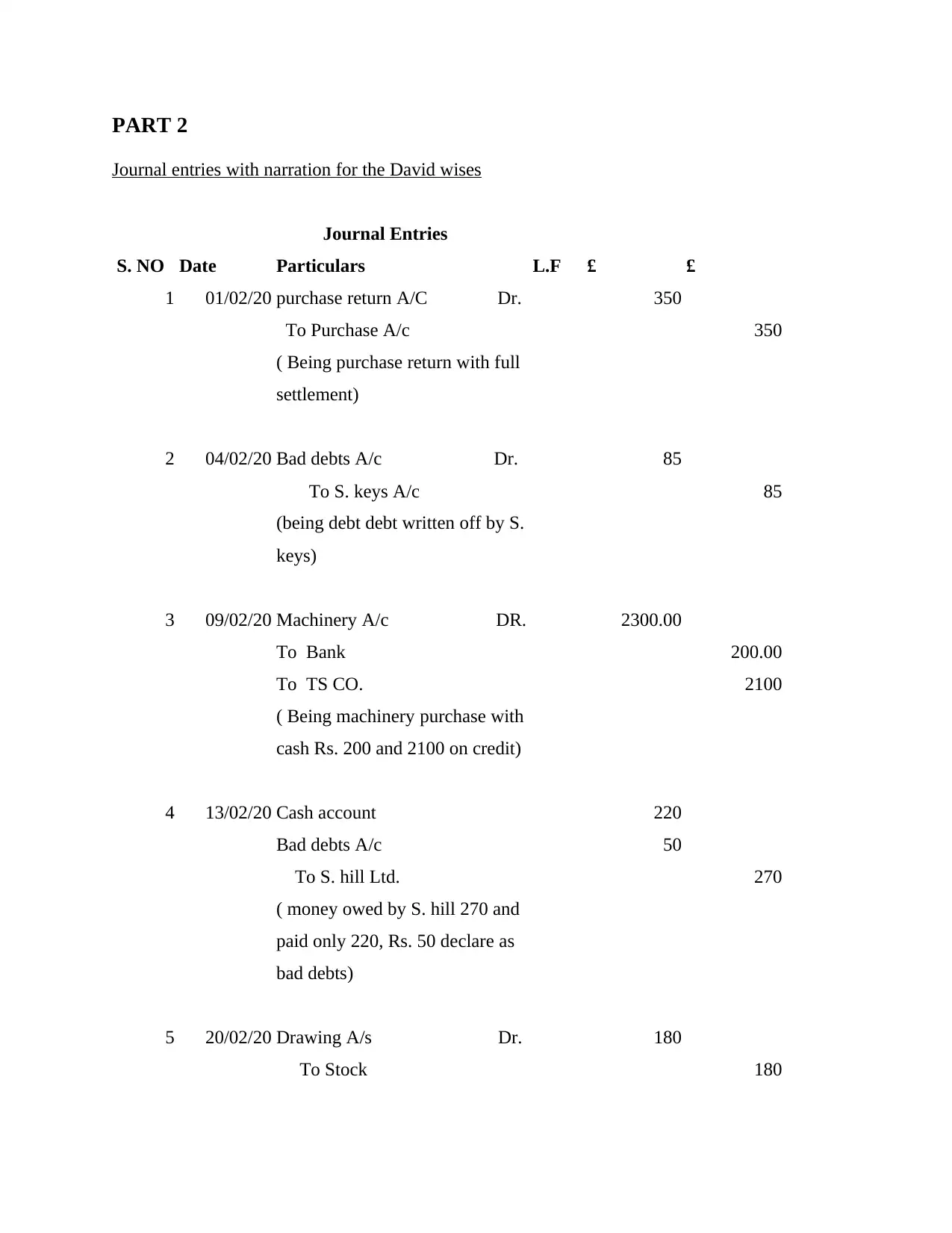

PART 2

Journal entries with narration for the David wises

Journal Entries

S. NO Date Particulars L.F £ £

1 01/02/20 purchase return A/C Dr. 350

To Purchase A/c 350

( Being purchase return with full

settlement)

2 04/02/20 Bad debts A/c Dr. 85

To S. keys A/c 85

(being debt debt written off by S.

keys)

3 09/02/20 Machinery A/c DR. 2300.00

To Bank 200.00

To TS CO. 2100

( Being machinery purchase with

cash Rs. 200 and 2100 on credit)

4 13/02/20 Cash account 220

Bad debts A/c 50

To S. hill Ltd. 270

( money owed by S. hill 270 and

paid only 220, Rs. 50 declare as

bad debts)

5 20/02/20 Drawing A/s Dr. 180

To Stock 180

Journal entries with narration for the David wises

Journal Entries

S. NO Date Particulars L.F £ £

1 01/02/20 purchase return A/C Dr. 350

To Purchase A/c 350

( Being purchase return with full

settlement)

2 04/02/20 Bad debts A/c Dr. 85

To S. keys A/c 85

(being debt debt written off by S.

keys)

3 09/02/20 Machinery A/c DR. 2300.00

To Bank 200.00

To TS CO. 2100

( Being machinery purchase with

cash Rs. 200 and 2100 on credit)

4 13/02/20 Cash account 220

Bad debts A/c 50

To S. hill Ltd. 270

( money owed by S. hill 270 and

paid only 220, Rs. 50 declare as

bad debts)

5 20/02/20 Drawing A/s Dr. 180

To Stock 180

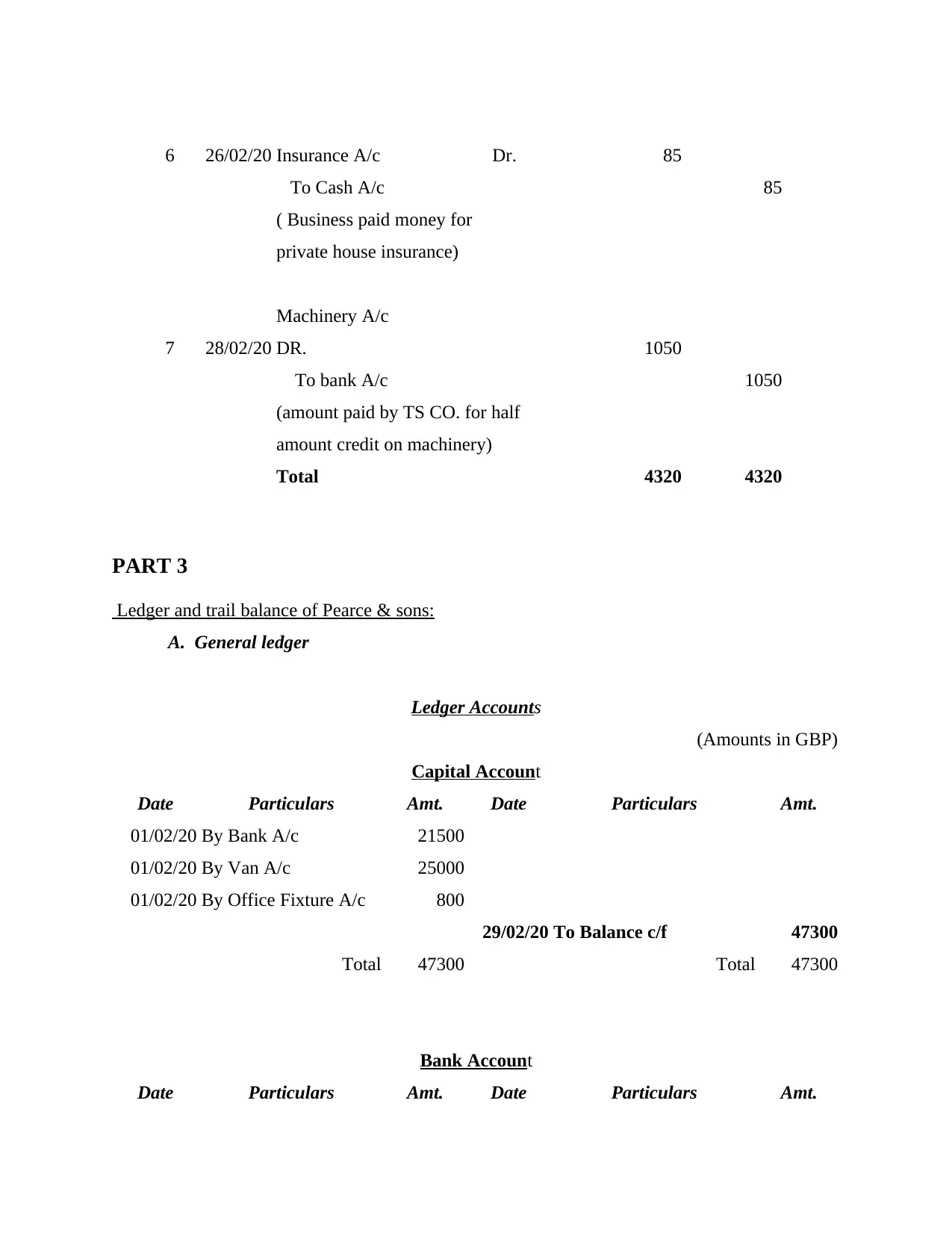

6 26/02/20 Insurance A/c Dr. 85

To Cash A/c 85

( Business paid money for

private house insurance)

7 28/02/20

Machinery A/c

DR. 1050

To bank A/c 1050

(amount paid by TS CO. for half

amount credit on machinery)

Total 4320 4320

PART 3

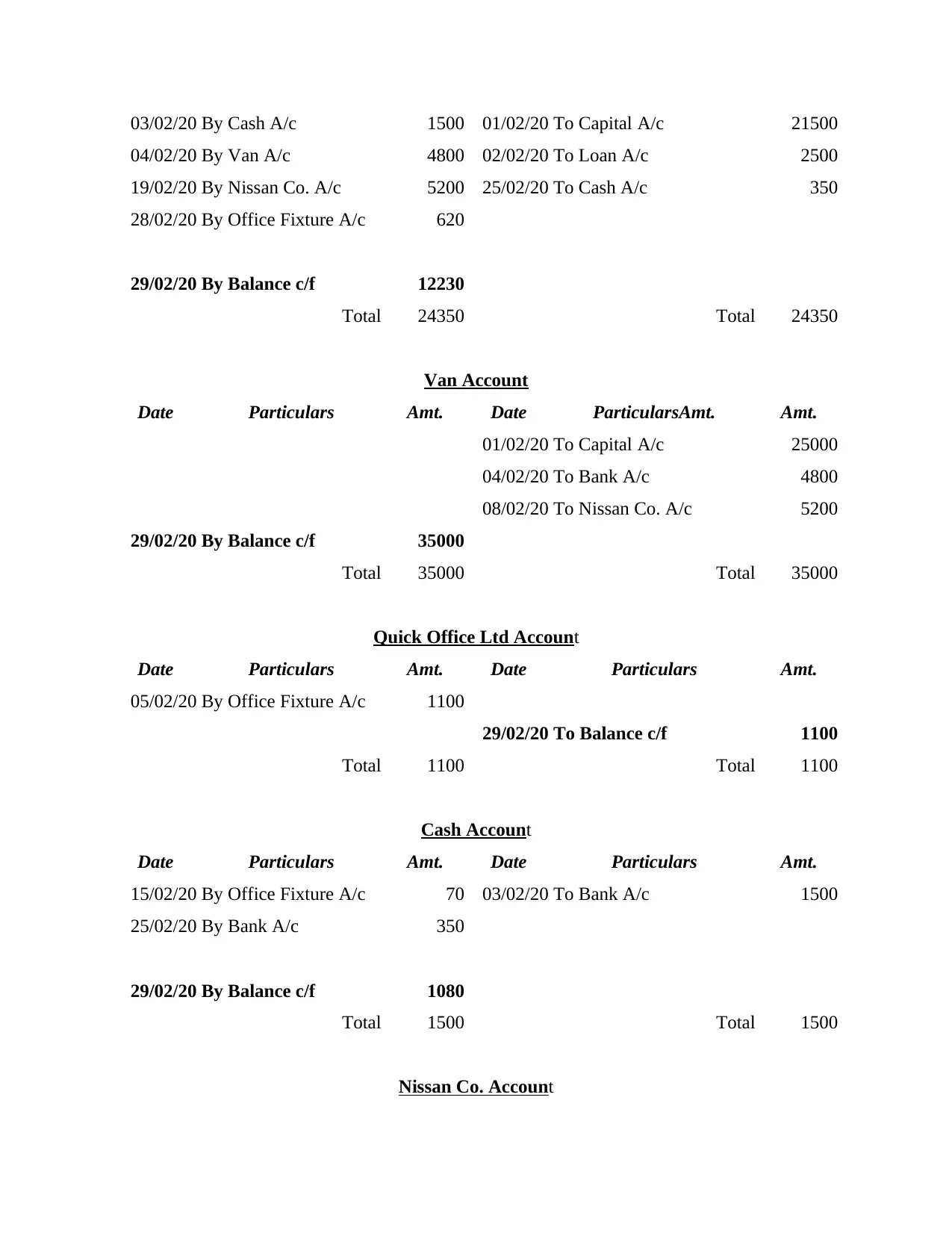

Ledger and trail balance of Pearce & sons:

A. General ledger

Ledger Accounts

(Amounts in GBP)

Capital Account

Date Particulars Amt. Date Particulars Amt.

01/02/20 By Bank A/c 21500

01/02/20 By Van A/c 25000

01/02/20 By Office Fixture A/c 800

29/02/20 To Balance c/f 47300

Total 47300 Total 47300

Bank Account

Date Particulars Amt. Date Particulars Amt.

To Cash A/c 85

( Business paid money for

private house insurance)

7 28/02/20

Machinery A/c

DR. 1050

To bank A/c 1050

(amount paid by TS CO. for half

amount credit on machinery)

Total 4320 4320

PART 3

Ledger and trail balance of Pearce & sons:

A. General ledger

Ledger Accounts

(Amounts in GBP)

Capital Account

Date Particulars Amt. Date Particulars Amt.

01/02/20 By Bank A/c 21500

01/02/20 By Van A/c 25000

01/02/20 By Office Fixture A/c 800

29/02/20 To Balance c/f 47300

Total 47300 Total 47300

Bank Account

Date Particulars Amt. Date Particulars Amt.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

03/02/20 By Cash A/c 1500 01/02/20 To Capital A/c 21500

04/02/20 By Van A/c 4800 02/02/20 To Loan A/c 2500

19/02/20 By Nissan Co. A/c 5200 25/02/20 To Cash A/c 350

28/02/20 By Office Fixture A/c 620

29/02/20 By Balance c/f 12230

Total 24350 Total 24350

Van Account

Date Particulars Amt. Date ParticularsAmt. Amt.

01/02/20 To Capital A/c 25000

04/02/20 To Bank A/c 4800

08/02/20 To Nissan Co. A/c 5200

29/02/20 By Balance c/f 35000

Total 35000 Total 35000

Quick Office Ltd Account

Date Particulars Amt. Date Particulars Amt.

05/02/20 By Office Fixture A/c 1100

29/02/20 To Balance c/f 1100

Total 1100 Total 1100

Cash Account

Date Particulars Amt. Date Particulars Amt.

15/02/20 By Office Fixture A/c 70 03/02/20 To Bank A/c 1500

25/02/20 By Bank A/c 350

29/02/20 By Balance c/f 1080

Total 1500 Total 1500

Nissan Co. Account

04/02/20 By Van A/c 4800 02/02/20 To Loan A/c 2500

19/02/20 By Nissan Co. A/c 5200 25/02/20 To Cash A/c 350

28/02/20 By Office Fixture A/c 620

29/02/20 By Balance c/f 12230

Total 24350 Total 24350

Van Account

Date Particulars Amt. Date ParticularsAmt. Amt.

01/02/20 To Capital A/c 25000

04/02/20 To Bank A/c 4800

08/02/20 To Nissan Co. A/c 5200

29/02/20 By Balance c/f 35000

Total 35000 Total 35000

Quick Office Ltd Account

Date Particulars Amt. Date Particulars Amt.

05/02/20 By Office Fixture A/c 1100

29/02/20 To Balance c/f 1100

Total 1100 Total 1100

Cash Account

Date Particulars Amt. Date Particulars Amt.

15/02/20 By Office Fixture A/c 70 03/02/20 To Bank A/c 1500

25/02/20 By Bank A/c 350

29/02/20 By Balance c/f 1080

Total 1500 Total 1500

Nissan Co. Account

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

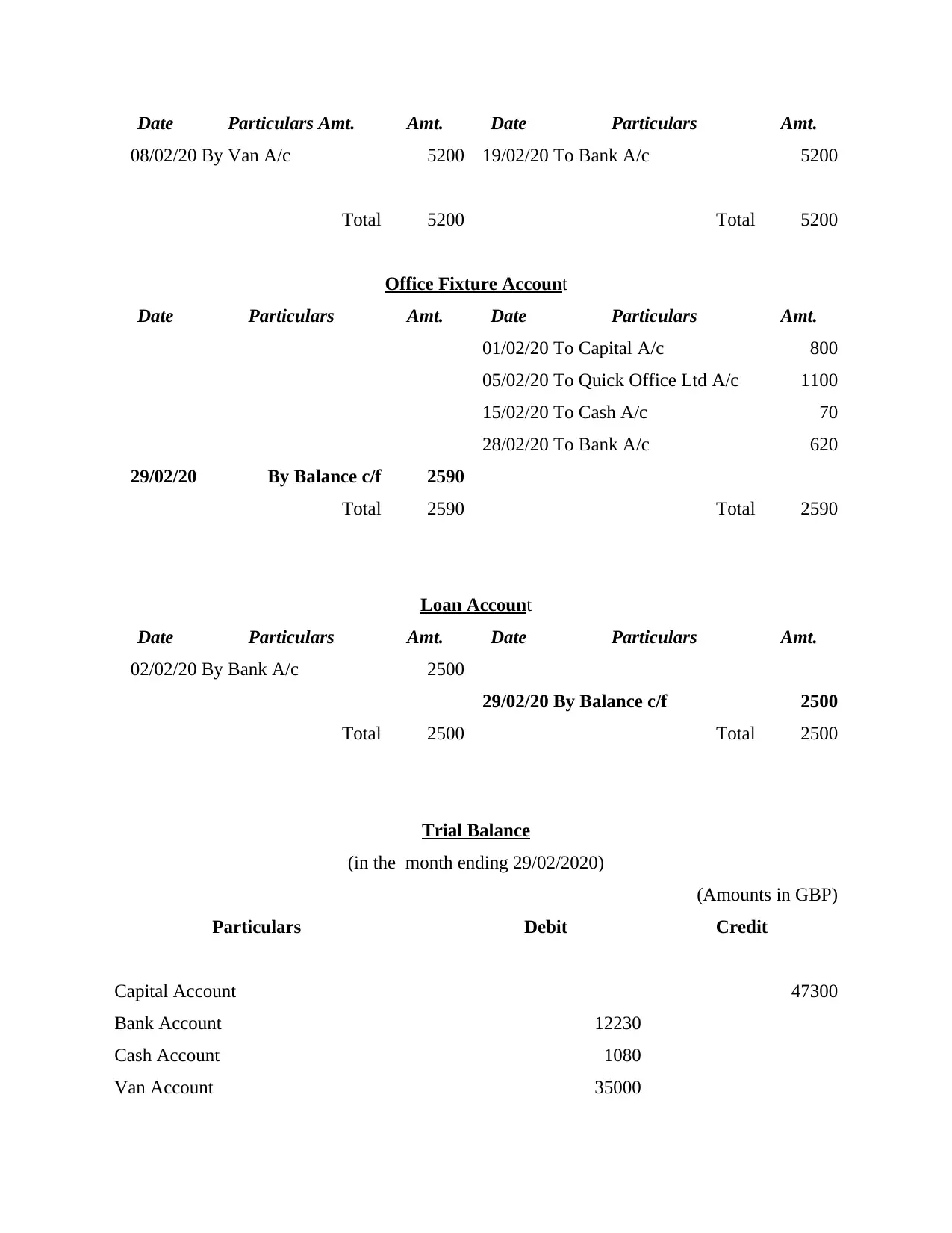

Date Particulars Amt. Amt. Date Particulars Amt.

08/02/20 By Van A/c 5200 19/02/20 To Bank A/c 5200

Total 5200 Total 5200

Office Fixture Account

Date Particulars Amt. Date Particulars Amt.

01/02/20 To Capital A/c 800

05/02/20 To Quick Office Ltd A/c 1100

15/02/20 To Cash A/c 70

28/02/20 To Bank A/c 620

29/02/20 By Balance c/f 2590

Total 2590 Total 2590

Loan Account

Date Particulars Amt. Date Particulars Amt.

02/02/20 By Bank A/c 2500

29/02/20 By Balance c/f 2500

Total 2500 Total 2500

Trial Balance

(in the month ending 29/02/2020)

(Amounts in GBP)

Particulars Debit Credit

Capital Account 47300

Bank Account 12230

Cash Account 1080

Van Account 35000

08/02/20 By Van A/c 5200 19/02/20 To Bank A/c 5200

Total 5200 Total 5200

Office Fixture Account

Date Particulars Amt. Date Particulars Amt.

01/02/20 To Capital A/c 800

05/02/20 To Quick Office Ltd A/c 1100

15/02/20 To Cash A/c 70

28/02/20 To Bank A/c 620

29/02/20 By Balance c/f 2590

Total 2590 Total 2590

Loan Account

Date Particulars Amt. Date Particulars Amt.

02/02/20 By Bank A/c 2500

29/02/20 By Balance c/f 2500

Total 2500 Total 2500

Trial Balance

(in the month ending 29/02/2020)

(Amounts in GBP)

Particulars Debit Credit

Capital Account 47300

Bank Account 12230

Cash Account 1080

Van Account 35000

Quick Office Ltd. Account 1100

Office Fixture Account 2590

Loan Account 2500

Total 50900 50900

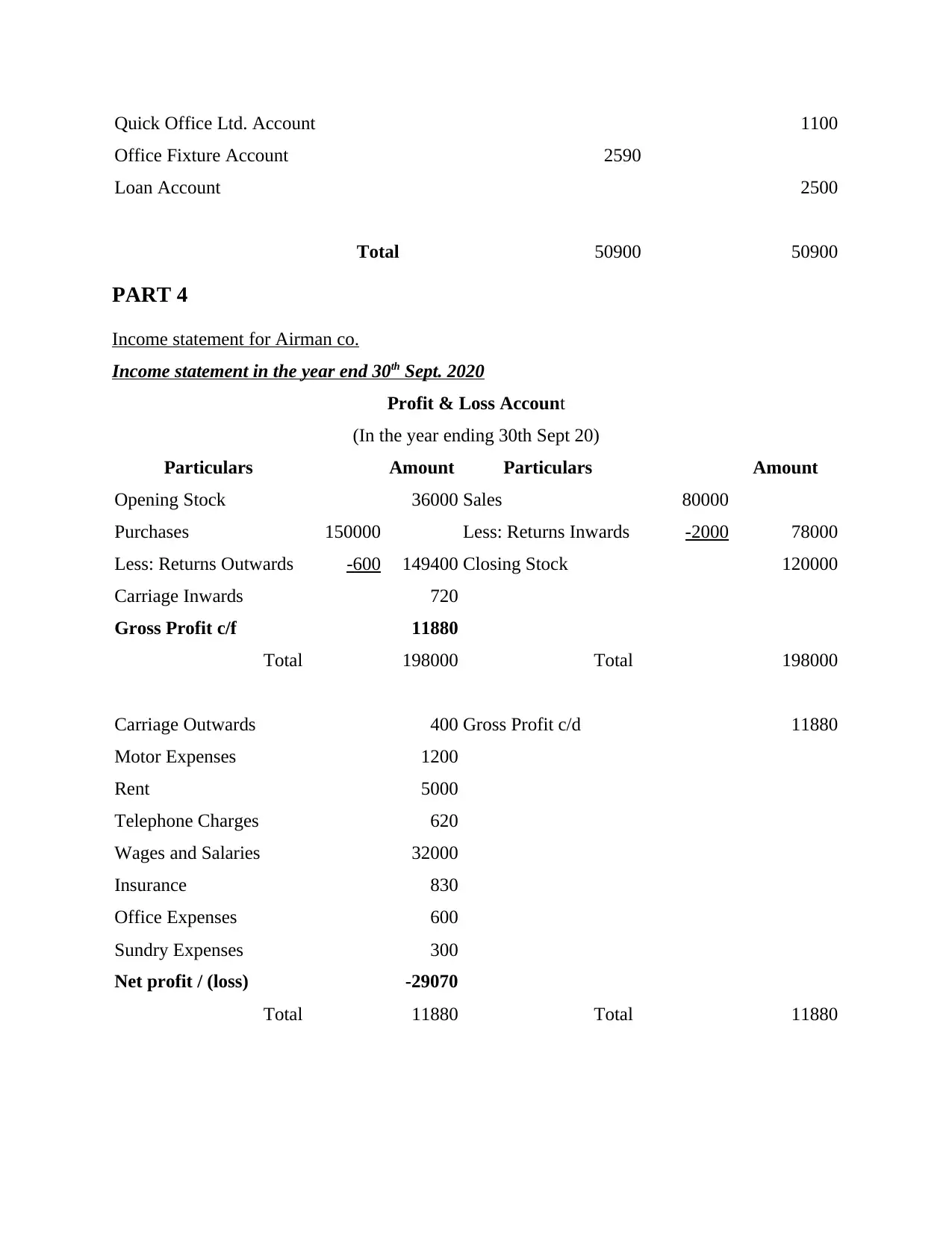

PART 4

Income statement for Airman co.

Income statement in the year end 30th Sept. 2020

Profit & Loss Account

(In the year ending 30th Sept 20)

Particulars Amount Particulars Amount

Opening Stock 36000 Sales 80000

Purchases 150000 Less: Returns Inwards -2000 78000

Less: Returns Outwards -600 149400 Closing Stock 120000

Carriage Inwards 720

Gross Profit c/f 11880

Total 198000 Total 198000

Carriage Outwards 400 Gross Profit c/d 11880

Motor Expenses 1200

Rent 5000

Telephone Charges 620

Wages and Salaries 32000

Insurance 830

Office Expenses 600

Sundry Expenses 300

Net profit / (loss) -29070

Total 11880 Total 11880

Office Fixture Account 2590

Loan Account 2500

Total 50900 50900

PART 4

Income statement for Airman co.

Income statement in the year end 30th Sept. 2020

Profit & Loss Account

(In the year ending 30th Sept 20)

Particulars Amount Particulars Amount

Opening Stock 36000 Sales 80000

Purchases 150000 Less: Returns Inwards -2000 78000

Less: Returns Outwards -600 149400 Closing Stock 120000

Carriage Inwards 720

Gross Profit c/f 11880

Total 198000 Total 198000

Carriage Outwards 400 Gross Profit c/d 11880

Motor Expenses 1200

Rent 5000

Telephone Charges 620

Wages and Salaries 32000

Insurance 830

Office Expenses 600

Sundry Expenses 300

Net profit / (loss) -29070

Total 11880 Total 11880

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Impact of COVID 19 on company income statement items

Income statement is part of the financial statements of the organisation and depicts total revenue

collected and expenses incurred by the company in particular time period. The main objective of

this statement is to calculate total losses suffered or profit obtained by the company in a given

time period. Income statement of the company has faced various changes as businesses from all

over the globe are facing threat from COVID-19 pandemic.

The pandemic stopped business activities all over the globe which obstructed various

organisations from co ducting their daily operations. This resulted in various organisations

suffering huge losses. This impacted the process of revenue recognition for various enterprises.

Many organisations provided detailed description about effect of COVID-19 on their quarterly

financial statements. This pandemic has influenced credit losses and future prediction of cash

flow. As such information is used in impairment testing, this area of income statement is

influenced by the economic collapse caused by COVID-19.

Various organisations are using fair value measurement for conducting impairment

measurements (Flower and Ebbers, 2018). This process involves identification of price at which

usual transaction would take place between various business organisations under market

situation during the time of measurement.

The pandemic resulted in termination of various business activities between different

organisations. Sudden cloning of such business dealings increased costs of the company in the

form of fines paid for such termination (Weygandt and et. al., 2018). Such onetime costs need to

be recognized by various organisations and considered during formation of financial statements

in order to gain accurate insight about the current financial conditions of the company.

Taking each factor produced by pandemic into consideration during creation of income statement

will help the company take effective decisions about their strategies for the future.

Income statement is part of the financial statements of the organisation and depicts total revenue

collected and expenses incurred by the company in particular time period. The main objective of

this statement is to calculate total losses suffered or profit obtained by the company in a given

time period. Income statement of the company has faced various changes as businesses from all

over the globe are facing threat from COVID-19 pandemic.

The pandemic stopped business activities all over the globe which obstructed various

organisations from co ducting their daily operations. This resulted in various organisations

suffering huge losses. This impacted the process of revenue recognition for various enterprises.

Many organisations provided detailed description about effect of COVID-19 on their quarterly

financial statements. This pandemic has influenced credit losses and future prediction of cash

flow. As such information is used in impairment testing, this area of income statement is

influenced by the economic collapse caused by COVID-19.

Various organisations are using fair value measurement for conducting impairment

measurements (Flower and Ebbers, 2018). This process involves identification of price at which

usual transaction would take place between various business organisations under market

situation during the time of measurement.

The pandemic resulted in termination of various business activities between different

organisations. Sudden cloning of such business dealings increased costs of the company in the

form of fines paid for such termination (Weygandt and et. al., 2018). Such onetime costs need to

be recognized by various organisations and considered during formation of financial statements

in order to gain accurate insight about the current financial conditions of the company.

Taking each factor produced by pandemic into consideration during creation of income statement

will help the company take effective decisions about their strategies for the future.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CONCLUSION

From the above report it can be concluded that recording of business transaction of

business firm plays an important role in firm's decision making. It helps management of business

organisation to grab important opportunities which helps its management to overcome fear of

competition. My maintaining proper financial statements a management of a firm is able to make

effective decisions towards company’s success in respective business operations.

From the above report it can be concluded that recording of business transaction of

business firm plays an important role in firm's decision making. It helps management of business

organisation to grab important opportunities which helps its management to overcome fear of

competition. My maintaining proper financial statements a management of a firm is able to make

effective decisions towards company’s success in respective business operations.

REFERENCES

Books and Journals

Prodanova, N.A. and et. al., 2019. Methodology for assessing control in the formation of

financial statements of a consolidated business. International Journal of Recent

Technology and Engineering, 8(1), pp.2696-2702.

Drake, M. S., Quinn, P. J. and Thornock, J. R., 2017. Who uses financial statements. A

demographic analysis of financial statement downloads from EDGAR. Accounting

Horizons, 31(3), pp.55-68.

Dabbicco, G., 2018. A comparison of debt measures in fiscal statistics and public sector financial

statements. Public Money & Management, 38(7), pp.511-518.

Maroun, W., 2017. Assuring the integrated report: Insights and recommendations from auditors

and preparers. The British Accounting Review, 49(3), pp.329-346.

Flower, J. and Ebbers, G., 2018. Global financial reporting. Macmillan International Higher

Education.

Weygandt, J.J. and et. al., 2018. Managerial Accounting: Tools for Business Decision-making.

John Wiley & Sons.

Kwilinski, A., 2019. Implementation of blockchain technology in accounting sphere. Academy

of Accounting and Financial Studies Journal, 23, pp.1-6.

Jasmine, C. A., 2019. Impacts of Covid-19 on Company and Efforts to Support Organization

Adaptable. Dr. David F. Rico, PMP, ACP, CSM, pp.67-70.

International Labour Organisation, 2020. COVID‐19 and the World of Work: Country Policy

Responses.

Books and Journals

Prodanova, N.A. and et. al., 2019. Methodology for assessing control in the formation of

financial statements of a consolidated business. International Journal of Recent

Technology and Engineering, 8(1), pp.2696-2702.

Drake, M. S., Quinn, P. J. and Thornock, J. R., 2017. Who uses financial statements. A

demographic analysis of financial statement downloads from EDGAR. Accounting

Horizons, 31(3), pp.55-68.

Dabbicco, G., 2018. A comparison of debt measures in fiscal statistics and public sector financial

statements. Public Money & Management, 38(7), pp.511-518.

Maroun, W., 2017. Assuring the integrated report: Insights and recommendations from auditors

and preparers. The British Accounting Review, 49(3), pp.329-346.

Flower, J. and Ebbers, G., 2018. Global financial reporting. Macmillan International Higher

Education.

Weygandt, J.J. and et. al., 2018. Managerial Accounting: Tools for Business Decision-making.

John Wiley & Sons.

Kwilinski, A., 2019. Implementation of blockchain technology in accounting sphere. Academy

of Accounting and Financial Studies Journal, 23, pp.1-6.

Jasmine, C. A., 2019. Impacts of Covid-19 on Company and Efforts to Support Organization

Adaptable. Dr. David F. Rico, PMP, ACP, CSM, pp.67-70.

International Labour Organisation, 2020. COVID‐19 and the World of Work: Country Policy

Responses.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.