Recording Business Transactions: A Comprehensive Finance Analysis

VerifiedAdded on 2023/01/03

|13

|2642

|68

Homework Assignment

AI Summary

This assignment solution provides a comprehensive analysis of recording business transactions, covering various aspects of accounting and financial reporting. It begins with an introduction to accounting principles, followed by an exploration of decision-makers and their needs regarding accounting information, including the merits and demerits of accounting within a business unit. The solution then delves into practical applications, including journal entries, the preparation of general ledgers, and trial balances. Furthermore, the assignment includes the drafting of an income statement and a discussion of the COVID-19 pandemic's impact on financial statements, analyzing the effects on revenue, costs, and overall business performance. The solution incorporates examples and calculations to illustrate key concepts and provide a practical understanding of the subject matter.

Recording Business Transaction

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

PART 1............................................................................................................................................3

PART 2............................................................................................................................................5

PART 3............................................................................................................................................7

PART 4..........................................................................................................................................10

CONCLUSION..............................................................................................................................12

REFERENCE.................................................................................................................................13

INTRODUCTION...........................................................................................................................3

PART 1............................................................................................................................................3

PART 2............................................................................................................................................5

PART 3............................................................................................................................................7

PART 4..........................................................................................................................................10

CONCLUSION..............................................................................................................................12

REFERENCE.................................................................................................................................13

INTRODUCTION

Accounting alludes to a series or array of practices that involves tracking, assessment,

review and summarizing data of financial activity of an entity within business segment and that's

only carrying out with aid of accounting. Practically, accounting is indeed systematic language

of business and related activities. That allows the corporation to transform the current operations

into meaningful statements/reports that could be categorised according to their respective use and

relevance. Such statements and accounts shall be rendered in such a manner as to assist in the

measurement of financial results together with the status of the corporation (Coate and

Mitschow, 2018). The study covers different aspects related to accounts and recording

of financial transactions. The study consists of discussion about decision makers of corporation

and to what extent they require accounting information, pros and cons of accounting as well as

practical tasks to record business transactions and prepare financial statements.

PART 1

Recognise who are decision-makers and describe their requirement/needs with regard to

accounting-information.

The decision-makers are an individual, generally in the management, who takes tough

choices that have an effect on the way the organisation works. Employee personnel who are good

decision-makers understand how to quickly solve challenges and leverage critical reasoning

skills to better resolve issues. They will easily weigh the different choices and settle on the result

that ideally serves the corporation and its personnel (Zeff and Dyckman, 2020).

Financial management includes the compilation, review and summary of all financial

details in the way that could be utilized in reporting. Such kinds of reports, which provide

financial statistics, are helpful for drawing up an appropriate financial and budgetary plan and

policy. Through this organisation will be able to cope with their performance in near future. As

well as being able to deliver better customer offerings to end customers. All the tasks, beginning

from induction to shooting, include the assessment of the revenues target, the preparation of

advertising events along with their budgeting, as well as option of various strategies and

applications for conducting different tasks and operations. And both of these decisions are made

by top executives and corporate managers.

Decision makers are mainly top management personnel within company like in Tesco

which multinational UK based retailer has Board of directors which prime decision makers of

Accounting alludes to a series or array of practices that involves tracking, assessment,

review and summarizing data of financial activity of an entity within business segment and that's

only carrying out with aid of accounting. Practically, accounting is indeed systematic language

of business and related activities. That allows the corporation to transform the current operations

into meaningful statements/reports that could be categorised according to their respective use and

relevance. Such statements and accounts shall be rendered in such a manner as to assist in the

measurement of financial results together with the status of the corporation (Coate and

Mitschow, 2018). The study covers different aspects related to accounts and recording

of financial transactions. The study consists of discussion about decision makers of corporation

and to what extent they require accounting information, pros and cons of accounting as well as

practical tasks to record business transactions and prepare financial statements.

PART 1

Recognise who are decision-makers and describe their requirement/needs with regard to

accounting-information.

The decision-makers are an individual, generally in the management, who takes tough

choices that have an effect on the way the organisation works. Employee personnel who are good

decision-makers understand how to quickly solve challenges and leverage critical reasoning

skills to better resolve issues. They will easily weigh the different choices and settle on the result

that ideally serves the corporation and its personnel (Zeff and Dyckman, 2020).

Financial management includes the compilation, review and summary of all financial

details in the way that could be utilized in reporting. Such kinds of reports, which provide

financial statistics, are helpful for drawing up an appropriate financial and budgetary plan and

policy. Through this organisation will be able to cope with their performance in near future. As

well as being able to deliver better customer offerings to end customers. All the tasks, beginning

from induction to shooting, include the assessment of the revenues target, the preparation of

advertising events along with their budgeting, as well as option of various strategies and

applications for conducting different tasks and operations. And both of these decisions are made

by top executives and corporate managers.

Decision makers are mainly top management personnel within company like in Tesco

which multinational UK based retailer has Board of directors which prime decision makers of

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

company. Company have Board of Directors with varying perceptions, insights and opinions

supports the members of the Community by improved corporate results. Our Board consists

of Chairman, Senior Independent Director, Group's Chief Executive Officer, Chief Financial

Officer, and number of independent non-executive directors. Tesco’s Board consists of:

Jhon Allan Non-executive Chairman

Ken Murphy Group Chief Executive

Alan Stewart CFO

Stewart Gilliland Independent Non-executive Director.

Byron Grote Independent Non-executive Director.

Alison Platt Independent Non-executive Director.

Mikael Olsson Independent Non-executive Director.

Steve Golsby Independent Non-executive Director.

Simon Patterson Independent Non-executive Director.

They require accounting information about cost of revenue, performance and liquidity of

the corporation for strategy, monitoring and making decisions. Decision makers is involved in

evaluating the potential of the group to make money in the potential. It is accountable for

determining the liquidity of the organisation and fulfilling its financial commitments on

schedule. By the different proportions like Debts – Equity Proportion, Current Ratio etc. They

need accounting information to understand shorter-term or longer-term solvency of company.

Likewise, the imperative for shorter-term and longer-term funds could be identified with aid

of Cash Flows Statements.

Financial accounts/statements reflect all accounting transactions relating to the business

in a nutshell that allows it feasible and convenient for the executive team, alongside

corporate managers, to use this knowledge in the implementation of strategies. In which the

financial statements are drawn out on the grounds of common standards and procedures

that are same across the sector. This allows them to distinguish themselves from other rivals for

positioning around industry benchmarks. It establishes a framework for management/BOD to

take decisions on the capital budgeting, including whether such decisions are desirable and

commercially viable for the organisation to take. Furthermore, forecasts and predictions are both

based on financial information within the organisation and on change as per business conditions.

supports the members of the Community by improved corporate results. Our Board consists

of Chairman, Senior Independent Director, Group's Chief Executive Officer, Chief Financial

Officer, and number of independent non-executive directors. Tesco’s Board consists of:

Jhon Allan Non-executive Chairman

Ken Murphy Group Chief Executive

Alan Stewart CFO

Stewart Gilliland Independent Non-executive Director.

Byron Grote Independent Non-executive Director.

Alison Platt Independent Non-executive Director.

Mikael Olsson Independent Non-executive Director.

Steve Golsby Independent Non-executive Director.

Simon Patterson Independent Non-executive Director.

They require accounting information about cost of revenue, performance and liquidity of

the corporation for strategy, monitoring and making decisions. Decision makers is involved in

evaluating the potential of the group to make money in the potential. It is accountable for

determining the liquidity of the organisation and fulfilling its financial commitments on

schedule. By the different proportions like Debts – Equity Proportion, Current Ratio etc. They

need accounting information to understand shorter-term or longer-term solvency of company.

Likewise, the imperative for shorter-term and longer-term funds could be identified with aid

of Cash Flows Statements.

Financial accounts/statements reflect all accounting transactions relating to the business

in a nutshell that allows it feasible and convenient for the executive team, alongside

corporate managers, to use this knowledge in the implementation of strategies. In which the

financial statements are drawn out on the grounds of common standards and procedures

that are same across the sector. This allows them to distinguish themselves from other rivals for

positioning around industry benchmarks. It establishes a framework for management/BOD to

take decisions on the capital budgeting, including whether such decisions are desirable and

commercially viable for the organisation to take. Furthermore, forecasts and predictions are both

based on financial information within the organisation and on change as per business conditions.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

This is important not just in respect of comparative analysis, but also in respect of the framework

for collecting valuable knowledge through non-financial details.

Merits and demerits of accounting within a business unit:

Advantages:

Performance Comparison

It makes it possible to equate the financial reports of one period with others. Management should

also evaluate the structured reporting of all fiscal and accounting transactions in compliance with

the requirements of the company (Ionescu, 2017).

Decision-making

Decisions are made easier for managers because there is a thorough accounting of finance

transactions. Financial statements allow management to schedule its potential plans, schedule

and organise operations in separate organisations. Which offers facts on cash inflows and

outflows along with sales and expenditures that render it easier to foresee deficit or

surplus within the funds that ought to be handled in timely manner. This also helps to develop

clarity and oversight for the prevention and identification of fraud.

Disadvantage:

Describes information on the accounting in monetary terms

Non-fiscal transactions cannot have an impact on the statements of accounts. Only operations

of financial type may be assessed by accountant. Evidently, financial events are represented in

monetary terms. As a consequence, it provides an imperfect image during the implementation of

policy and the taking of crucial business decisions. In the sense of a tow corporation, the

company directors cannot on grounds of accounting books, take decisions pertaining to other

considerations such as economic, social and other considerations.

Accounting information could be subject to biasness

Accounting personnel have a personal impact over the corporation's accounting records. The

accounting officer may use various metrics of inventory assessment, depreciation techniques,

classification of revenues and capital spending, etc to assess the corporation's income (Hsieh, Ma

and Novoselov, 2018).

PART 2

A. Journal Entries of David for the month February 2020

for collecting valuable knowledge through non-financial details.

Merits and demerits of accounting within a business unit:

Advantages:

Performance Comparison

It makes it possible to equate the financial reports of one period with others. Management should

also evaluate the structured reporting of all fiscal and accounting transactions in compliance with

the requirements of the company (Ionescu, 2017).

Decision-making

Decisions are made easier for managers because there is a thorough accounting of finance

transactions. Financial statements allow management to schedule its potential plans, schedule

and organise operations in separate organisations. Which offers facts on cash inflows and

outflows along with sales and expenditures that render it easier to foresee deficit or

surplus within the funds that ought to be handled in timely manner. This also helps to develop

clarity and oversight for the prevention and identification of fraud.

Disadvantage:

Describes information on the accounting in monetary terms

Non-fiscal transactions cannot have an impact on the statements of accounts. Only operations

of financial type may be assessed by accountant. Evidently, financial events are represented in

monetary terms. As a consequence, it provides an imperfect image during the implementation of

policy and the taking of crucial business decisions. In the sense of a tow corporation, the

company directors cannot on grounds of accounting books, take decisions pertaining to other

considerations such as economic, social and other considerations.

Accounting information could be subject to biasness

Accounting personnel have a personal impact over the corporation's accounting records. The

accounting officer may use various metrics of inventory assessment, depreciation techniques,

classification of revenues and capital spending, etc to assess the corporation's income (Hsieh, Ma

and Novoselov, 2018).

PART 2

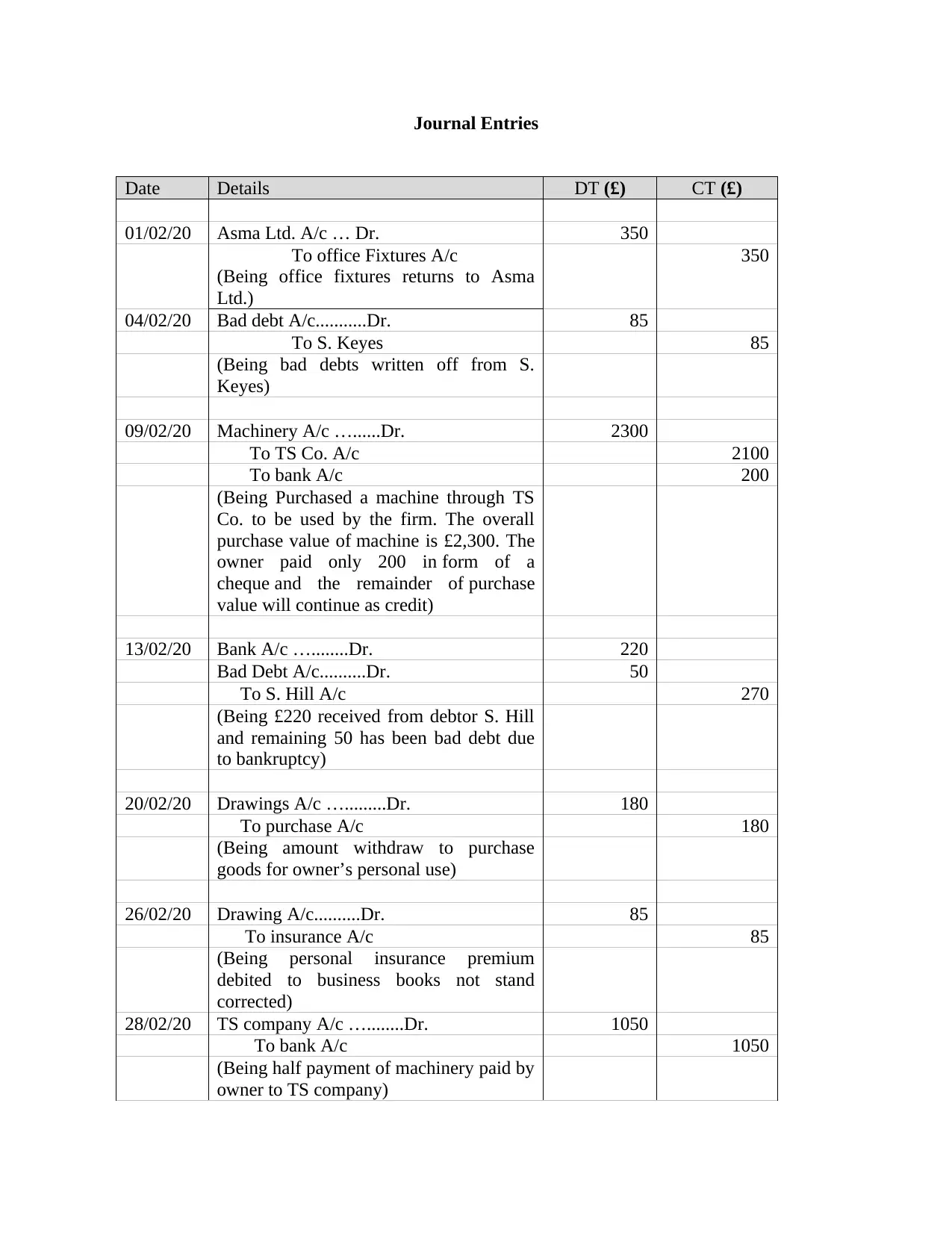

A. Journal Entries of David for the month February 2020

Journal Entries

Date Details DT (£) CT (£)

01/02/20 Asma Ltd. A/c … Dr. 350

To office Fixtures A/c

(Being office fixtures returns to Asma

Ltd.)

350

04/02/20 Bad debt A/c...........Dr. 85

To S. Keyes 85

(Being bad debts written off from S.

Keyes)

09/02/20 Machinery A/c …......Dr. 2300

To TS Co. A/c 2100

To bank A/c 200

(Being Purchased a machine through TS

Co. to be used by the firm. The overall

purchase value of machine is £2,300. The

owner paid only 200 in form of a

cheque and the remainder of purchase

value will continue as credit)

13/02/20 Bank A/c …........Dr. 220

Bad Debt A/c..........Dr. 50

To S. Hill A/c 270

(Being £220 received from debtor S. Hill

and remaining 50 has been bad debt due

to bankruptcy)

20/02/20 Drawings A/c ….........Dr. 180

To purchase A/c 180

(Being amount withdraw to purchase

goods for owner’s personal use)

26/02/20 Drawing A/c..........Dr. 85

To insurance A/c 85

(Being personal insurance premium

debited to business books not stand

corrected)

28/02/20 TS company A/c …........Dr. 1050

To bank A/c 1050

(Being half payment of machinery paid by

owner to TS company)

Date Details DT (£) CT (£)

01/02/20 Asma Ltd. A/c … Dr. 350

To office Fixtures A/c

(Being office fixtures returns to Asma

Ltd.)

350

04/02/20 Bad debt A/c...........Dr. 85

To S. Keyes 85

(Being bad debts written off from S.

Keyes)

09/02/20 Machinery A/c …......Dr. 2300

To TS Co. A/c 2100

To bank A/c 200

(Being Purchased a machine through TS

Co. to be used by the firm. The overall

purchase value of machine is £2,300. The

owner paid only 200 in form of a

cheque and the remainder of purchase

value will continue as credit)

13/02/20 Bank A/c …........Dr. 220

Bad Debt A/c..........Dr. 50

To S. Hill A/c 270

(Being £220 received from debtor S. Hill

and remaining 50 has been bad debt due

to bankruptcy)

20/02/20 Drawings A/c ….........Dr. 180

To purchase A/c 180

(Being amount withdraw to purchase

goods for owner’s personal use)

26/02/20 Drawing A/c..........Dr. 85

To insurance A/c 85

(Being personal insurance premium

debited to business books not stand

corrected)

28/02/20 TS company A/c …........Dr. 1050

To bank A/c 1050

(Being half payment of machinery paid by

owner to TS company)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

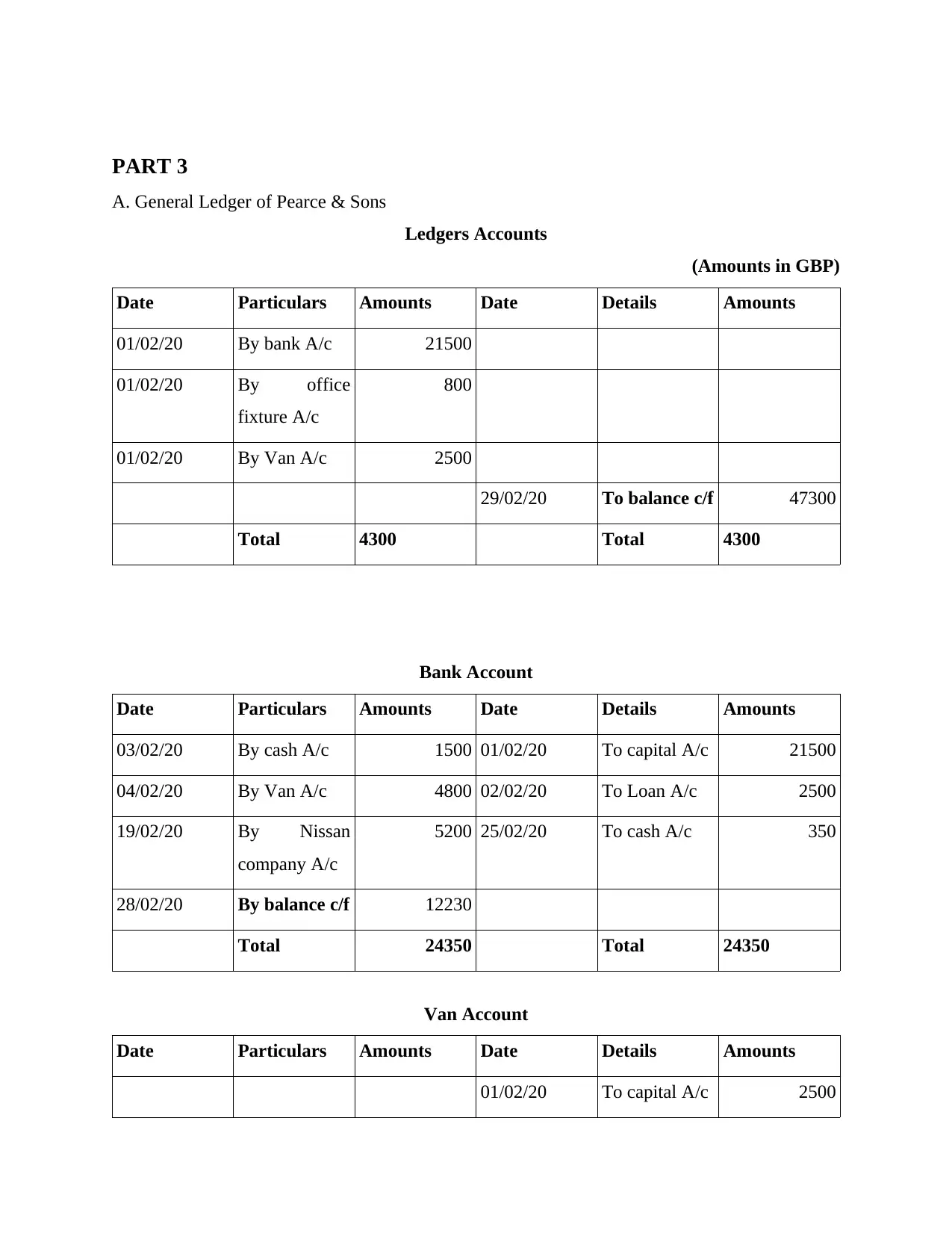

PART 3

A. General Ledger of Pearce & Sons

Ledgers Accounts

(Amounts in GBP)

Date Particulars Amounts Date Details Amounts

01/02/20 By bank A/c 21500

01/02/20 By office

fixture A/c

800

01/02/20 By Van A/c 2500

29/02/20 To balance c/f 47300

Total 4300 Total 4300

Bank Account

Date Particulars Amounts Date Details Amounts

03/02/20 By cash A/c 1500 01/02/20 To capital A/c 21500

04/02/20 By Van A/c 4800 02/02/20 To Loan A/c 2500

19/02/20 By Nissan

company A/c

5200 25/02/20 To cash A/c 350

28/02/20 By balance c/f 12230

Total 24350 Total 24350

Van Account

Date Particulars Amounts Date Details Amounts

01/02/20 To capital A/c 2500

A. General Ledger of Pearce & Sons

Ledgers Accounts

(Amounts in GBP)

Date Particulars Amounts Date Details Amounts

01/02/20 By bank A/c 21500

01/02/20 By office

fixture A/c

800

01/02/20 By Van A/c 2500

29/02/20 To balance c/f 47300

Total 4300 Total 4300

Bank Account

Date Particulars Amounts Date Details Amounts

03/02/20 By cash A/c 1500 01/02/20 To capital A/c 21500

04/02/20 By Van A/c 4800 02/02/20 To Loan A/c 2500

19/02/20 By Nissan

company A/c

5200 25/02/20 To cash A/c 350

28/02/20 By balance c/f 12230

Total 24350 Total 24350

Van Account

Date Particulars Amounts Date Details Amounts

01/02/20 To capital A/c 2500

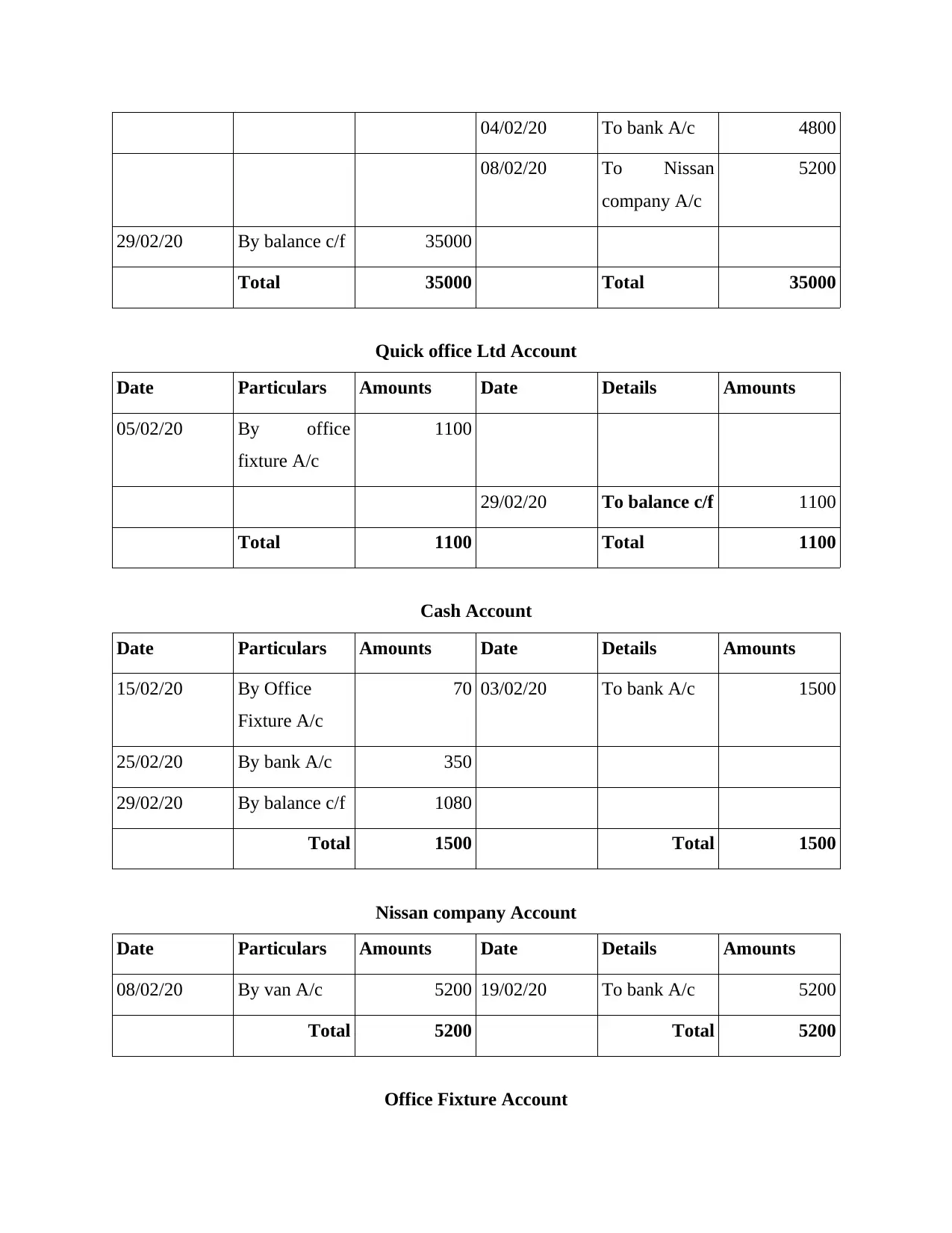

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

04/02/20 To bank A/c 4800

08/02/20 To Nissan

company A/c

5200

29/02/20 By balance c/f 35000

Total 35000 Total 35000

Quick office Ltd Account

Date Particulars Amounts Date Details Amounts

05/02/20 By office

fixture A/c

1100

29/02/20 To balance c/f 1100

Total 1100 Total 1100

Cash Account

Date Particulars Amounts Date Details Amounts

15/02/20 By Office

Fixture A/c

70 03/02/20 To bank A/c 1500

25/02/20 By bank A/c 350

29/02/20 By balance c/f 1080

Total 1500 Total 1500

Nissan company Account

Date Particulars Amounts Date Details Amounts

08/02/20 By van A/c 5200 19/02/20 To bank A/c 5200

Total 5200 Total 5200

Office Fixture Account

08/02/20 To Nissan

company A/c

5200

29/02/20 By balance c/f 35000

Total 35000 Total 35000

Quick office Ltd Account

Date Particulars Amounts Date Details Amounts

05/02/20 By office

fixture A/c

1100

29/02/20 To balance c/f 1100

Total 1100 Total 1100

Cash Account

Date Particulars Amounts Date Details Amounts

15/02/20 By Office

Fixture A/c

70 03/02/20 To bank A/c 1500

25/02/20 By bank A/c 350

29/02/20 By balance c/f 1080

Total 1500 Total 1500

Nissan company Account

Date Particulars Amounts Date Details Amounts

08/02/20 By van A/c 5200 19/02/20 To bank A/c 5200

Total 5200 Total 5200

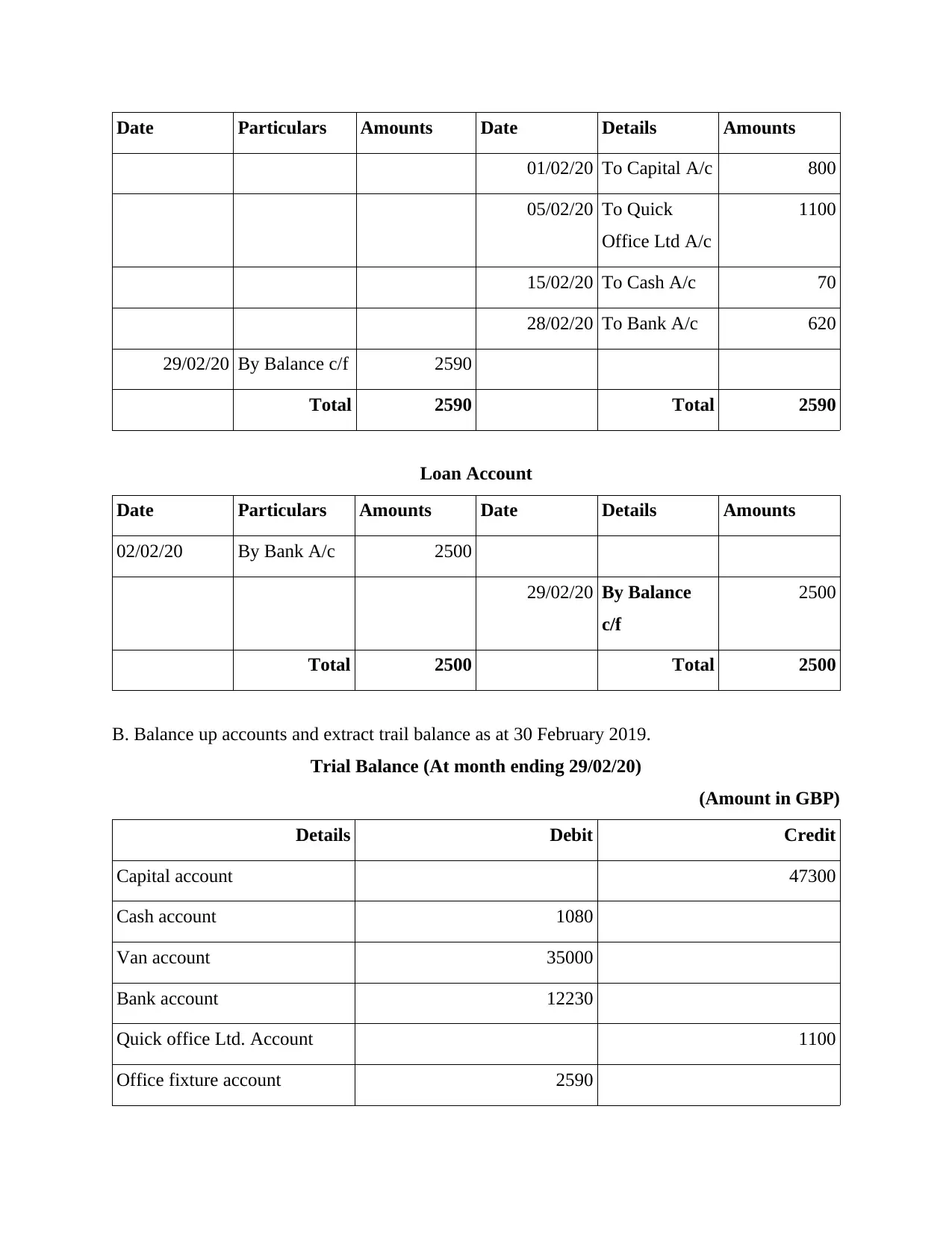

Office Fixture Account

Date Particulars Amounts Date Details Amounts

01/02/20 To Capital A/c 800

05/02/20 To Quick

Office Ltd A/c

1100

15/02/20 To Cash A/c 70

28/02/20 To Bank A/c 620

29/02/20 By Balance c/f 2590

Total 2590 Total 2590

Loan Account

Date Particulars Amounts Date Details Amounts

02/02/20 By Bank A/c 2500

29/02/20 By Balance

c/f

2500

Total 2500 Total 2500

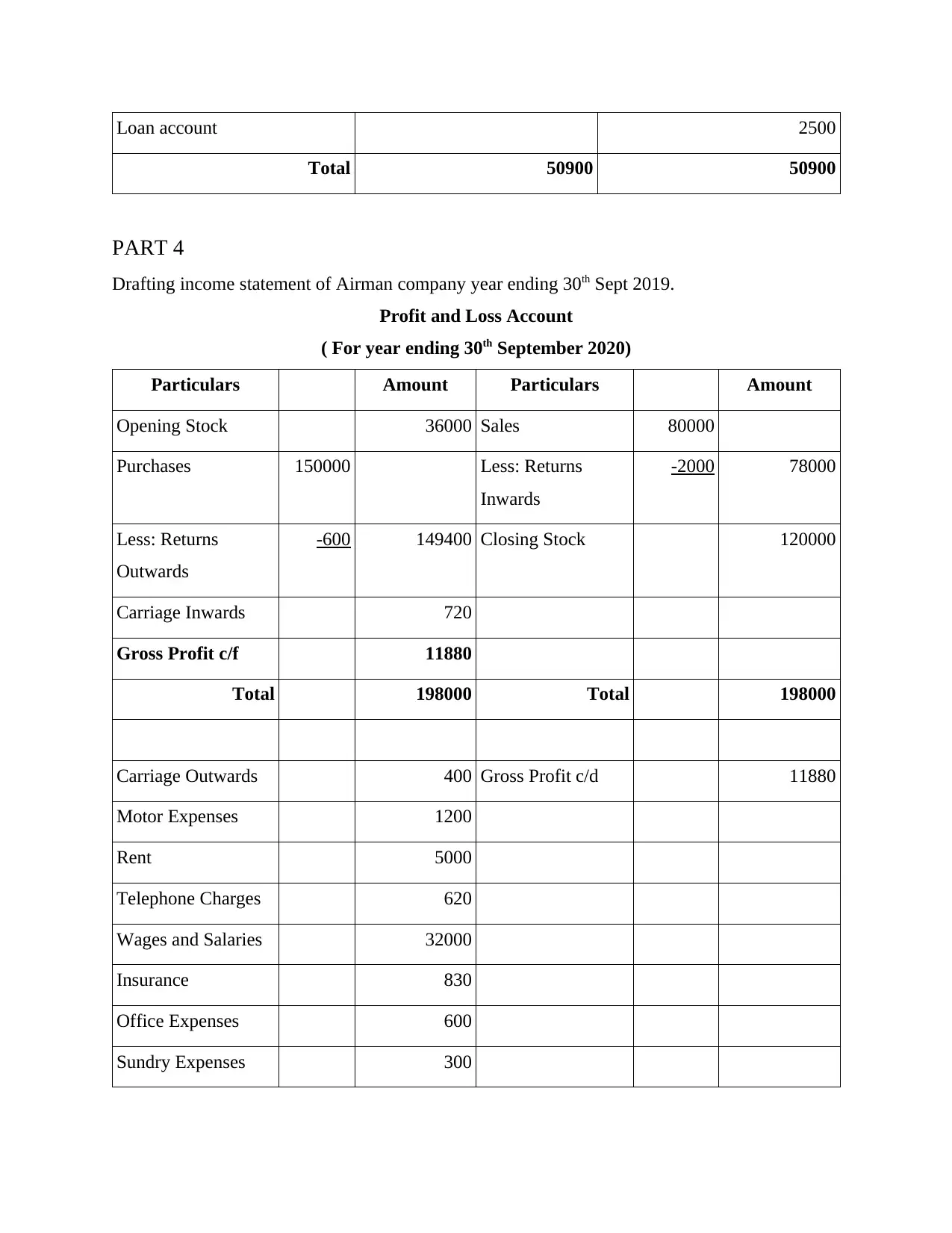

B. Balance up accounts and extract trail balance as at 30 February 2019.

Trial Balance (At month ending 29/02/20)

(Amount in GBP)

Details Debit Credit

Capital account 47300

Cash account 1080

Van account 35000

Bank account 12230

Quick office Ltd. Account 1100

Office fixture account 2590

01/02/20 To Capital A/c 800

05/02/20 To Quick

Office Ltd A/c

1100

15/02/20 To Cash A/c 70

28/02/20 To Bank A/c 620

29/02/20 By Balance c/f 2590

Total 2590 Total 2590

Loan Account

Date Particulars Amounts Date Details Amounts

02/02/20 By Bank A/c 2500

29/02/20 By Balance

c/f

2500

Total 2500 Total 2500

B. Balance up accounts and extract trail balance as at 30 February 2019.

Trial Balance (At month ending 29/02/20)

(Amount in GBP)

Details Debit Credit

Capital account 47300

Cash account 1080

Van account 35000

Bank account 12230

Quick office Ltd. Account 1100

Office fixture account 2590

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Loan account 2500

Total 50900 50900

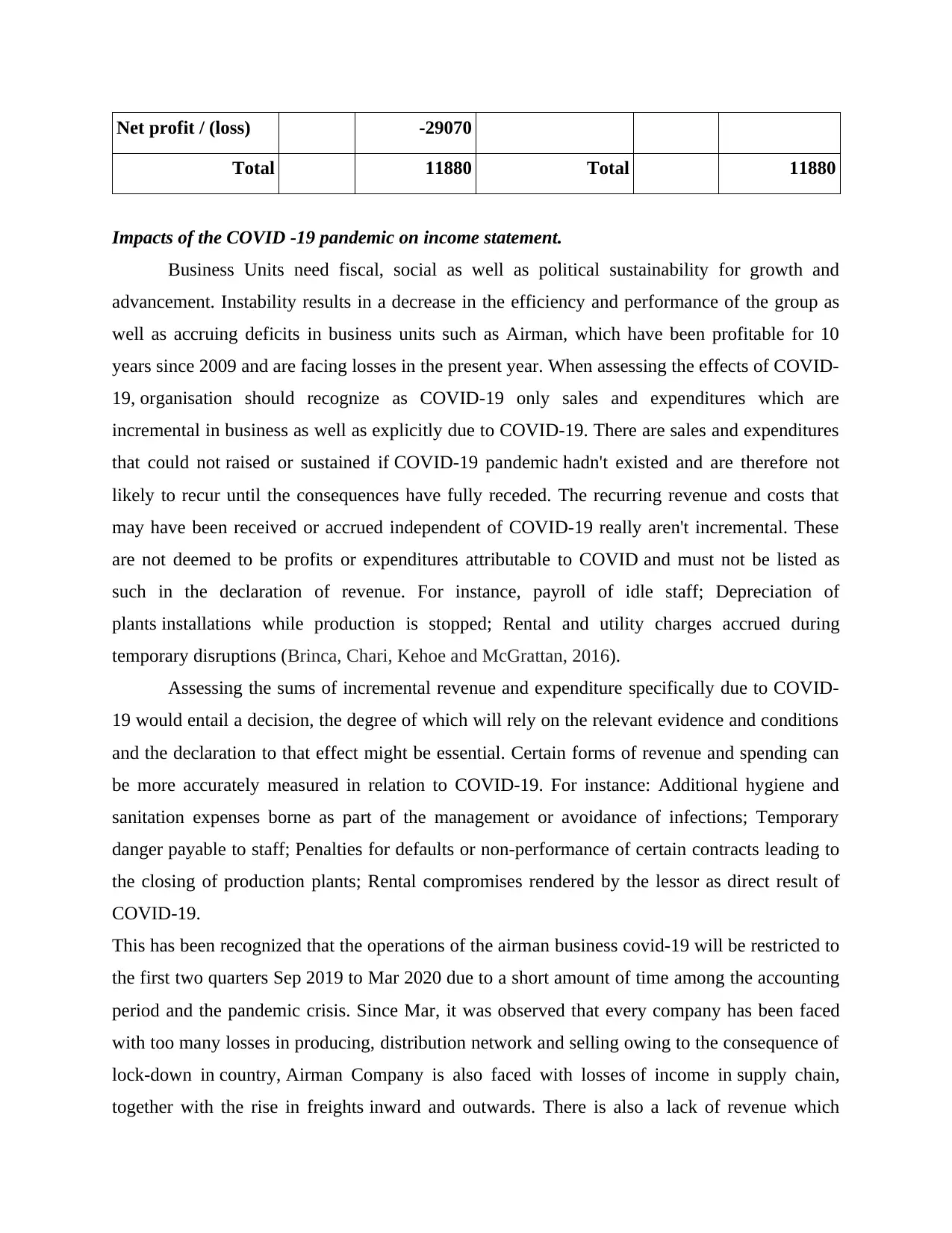

PART 4

Drafting income statement of Airman company year ending 30th Sept 2019.

Profit and Loss Account

( For year ending 30th September 2020)

Particulars Amount Particulars Amount

Opening Stock 36000 Sales 80000

Purchases 150000 Less: Returns

Inwards

-2000 78000

Less: Returns

Outwards

-600 149400 Closing Stock 120000

Carriage Inwards 720

Gross Profit c/f 11880

Total 198000 Total 198000

Carriage Outwards 400 Gross Profit c/d 11880

Motor Expenses 1200

Rent 5000

Telephone Charges 620

Wages and Salaries 32000

Insurance 830

Office Expenses 600

Sundry Expenses 300

Total 50900 50900

PART 4

Drafting income statement of Airman company year ending 30th Sept 2019.

Profit and Loss Account

( For year ending 30th September 2020)

Particulars Amount Particulars Amount

Opening Stock 36000 Sales 80000

Purchases 150000 Less: Returns

Inwards

-2000 78000

Less: Returns

Outwards

-600 149400 Closing Stock 120000

Carriage Inwards 720

Gross Profit c/f 11880

Total 198000 Total 198000

Carriage Outwards 400 Gross Profit c/d 11880

Motor Expenses 1200

Rent 5000

Telephone Charges 620

Wages and Salaries 32000

Insurance 830

Office Expenses 600

Sundry Expenses 300

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Net profit / (loss) -29070

Total 11880 Total 11880

Impacts of the COVID -19 pandemic on income statement.

Business Units need fiscal, social as well as political sustainability for growth and

advancement. Instability results in a decrease in the efficiency and performance of the group as

well as accruing deficits in business units such as Airman, which have been profitable for 10

years since 2009 and are facing losses in the present year. When assessing the effects of COVID-

19, organisation should recognize as COVID-19 only sales and expenditures which are

incremental in business as well as explicitly due to COVID-19. There are sales and expenditures

that could not raised or sustained if COVID-19 pandemic hadn't existed and are therefore not

likely to recur until the consequences have fully receded. The recurring revenue and costs that

may have been received or accrued independent of COVID-19 really aren't incremental. These

are not deemed to be profits or expenditures attributable to COVID and must not be listed as

such in the declaration of revenue. For instance, payroll of idle staff; Depreciation of

plants installations while production is stopped; Rental and utility charges accrued during

temporary disruptions (Brinca, Chari, Kehoe and McGrattan, 2016).

Assessing the sums of incremental revenue and expenditure specifically due to COVID-

19 would entail a decision, the degree of which will rely on the relevant evidence and conditions

and the declaration to that effect might be essential. Certain forms of revenue and spending can

be more accurately measured in relation to COVID-19. For instance: Additional hygiene and

sanitation expenses borne as part of the management or avoidance of infections; Temporary

danger payable to staff; Penalties for defaults or non-performance of certain contracts leading to

the closing of production plants; Rental compromises rendered by the lessor as direct result of

COVID-19.

This has been recognized that the operations of the airman business covid-19 will be restricted to

the first two quarters Sep 2019 to Mar 2020 due to a short amount of time among the accounting

period and the pandemic crisis. Since Mar, it was observed that every company has been faced

with too many losses in producing, distribution network and selling owing to the consequence of

lock-down in country, Airman Company is also faced with losses of income in supply chain,

together with the rise in freights inward and outwards. There is also a lack of revenue which

Total 11880 Total 11880

Impacts of the COVID -19 pandemic on income statement.

Business Units need fiscal, social as well as political sustainability for growth and

advancement. Instability results in a decrease in the efficiency and performance of the group as

well as accruing deficits in business units such as Airman, which have been profitable for 10

years since 2009 and are facing losses in the present year. When assessing the effects of COVID-

19, organisation should recognize as COVID-19 only sales and expenditures which are

incremental in business as well as explicitly due to COVID-19. There are sales and expenditures

that could not raised or sustained if COVID-19 pandemic hadn't existed and are therefore not

likely to recur until the consequences have fully receded. The recurring revenue and costs that

may have been received or accrued independent of COVID-19 really aren't incremental. These

are not deemed to be profits or expenditures attributable to COVID and must not be listed as

such in the declaration of revenue. For instance, payroll of idle staff; Depreciation of

plants installations while production is stopped; Rental and utility charges accrued during

temporary disruptions (Brinca, Chari, Kehoe and McGrattan, 2016).

Assessing the sums of incremental revenue and expenditure specifically due to COVID-

19 would entail a decision, the degree of which will rely on the relevant evidence and conditions

and the declaration to that effect might be essential. Certain forms of revenue and spending can

be more accurately measured in relation to COVID-19. For instance: Additional hygiene and

sanitation expenses borne as part of the management or avoidance of infections; Temporary

danger payable to staff; Penalties for defaults or non-performance of certain contracts leading to

the closing of production plants; Rental compromises rendered by the lessor as direct result of

COVID-19.

This has been recognized that the operations of the airman business covid-19 will be restricted to

the first two quarters Sep 2019 to Mar 2020 due to a short amount of time among the accounting

period and the pandemic crisis. Since Mar, it was observed that every company has been faced

with too many losses in producing, distribution network and selling owing to the consequence of

lock-down in country, Airman Company is also faced with losses of income in supply chain,

together with the rise in freights inward and outwards. There is also a lack of revenue which

decreases the demand for goods on the market and the business needs to pay fixed expenses

correspondingly. As a consequence, it's been analysed that this effect on the activity and work of

the business results. As long as Airman is concerned, they may face a failure in this financial

institution that they have reported in their documents. The condition developed by Covid-19 is

special and unusual. This complex to predict how longer this pandemic will have an effect on the

commercial activity of the organization and how much it will have an effect on the economic

state of the corporation. The distinction of patterns over the last 10 years versus present years is

also not warranted. In fact, the effect of this pandemic on potential output of financial era cannot

be predicted with certainty (Alstadsæter, Jacob, Kopczuk and Telle, 2016).

CONCLUSION

From above study this has been articulated that accounting is vital aspect in business

which enable organisation to handle financial information and take business decisions.

Accounting information are mainly used by decision makers to decisions and achieve targeted

objectives of business.

correspondingly. As a consequence, it's been analysed that this effect on the activity and work of

the business results. As long as Airman is concerned, they may face a failure in this financial

institution that they have reported in their documents. The condition developed by Covid-19 is

special and unusual. This complex to predict how longer this pandemic will have an effect on the

commercial activity of the organization and how much it will have an effect on the economic

state of the corporation. The distinction of patterns over the last 10 years versus present years is

also not warranted. In fact, the effect of this pandemic on potential output of financial era cannot

be predicted with certainty (Alstadsæter, Jacob, Kopczuk and Telle, 2016).

CONCLUSION

From above study this has been articulated that accounting is vital aspect in business

which enable organisation to handle financial information and take business decisions.

Accounting information are mainly used by decision makers to decisions and achieve targeted

objectives of business.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.