BA30592E Recording Business Transactions Homework Assignment - UWL

VerifiedAdded on 2023/01/04

|14

|1906

|58

Homework Assignment

AI Summary

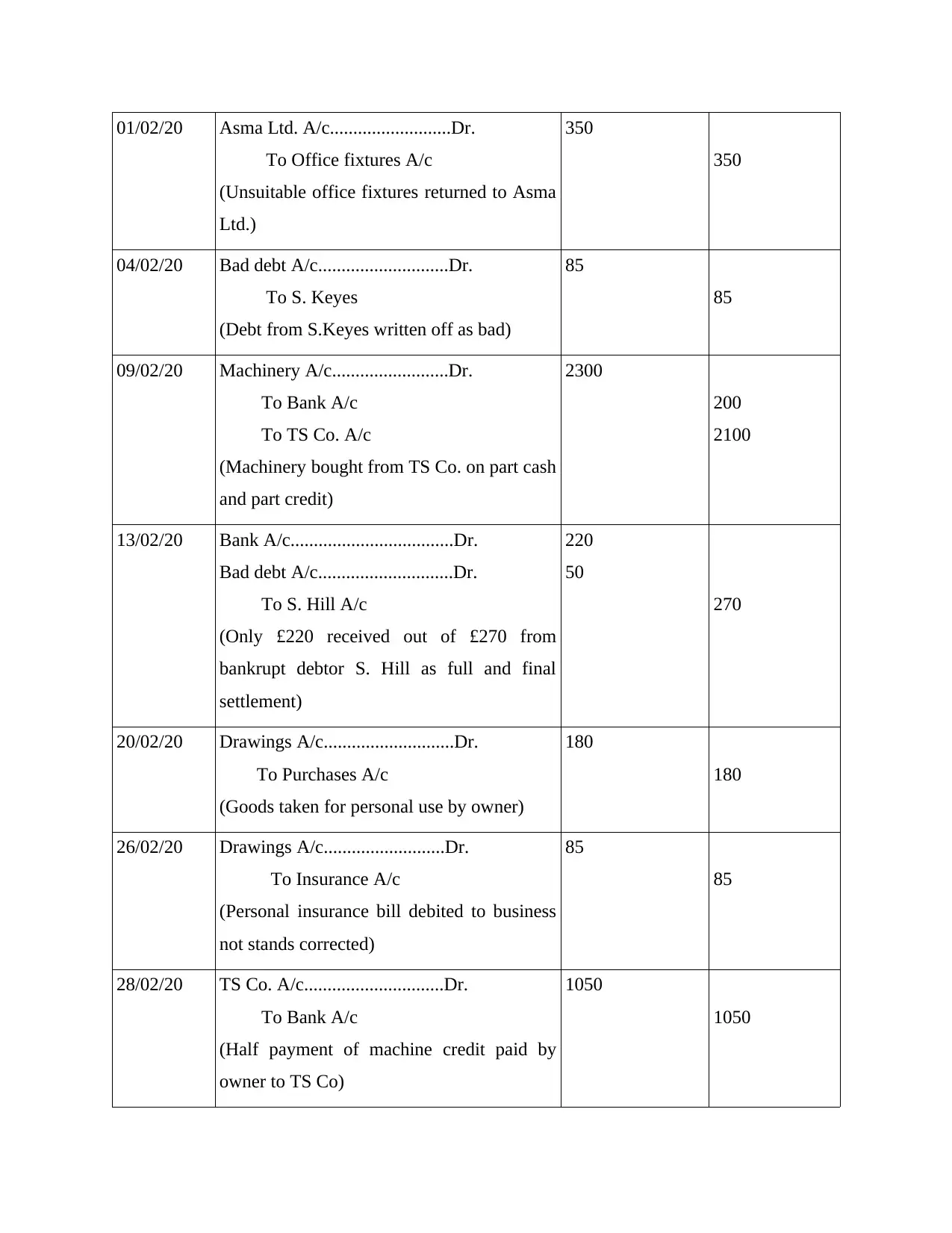

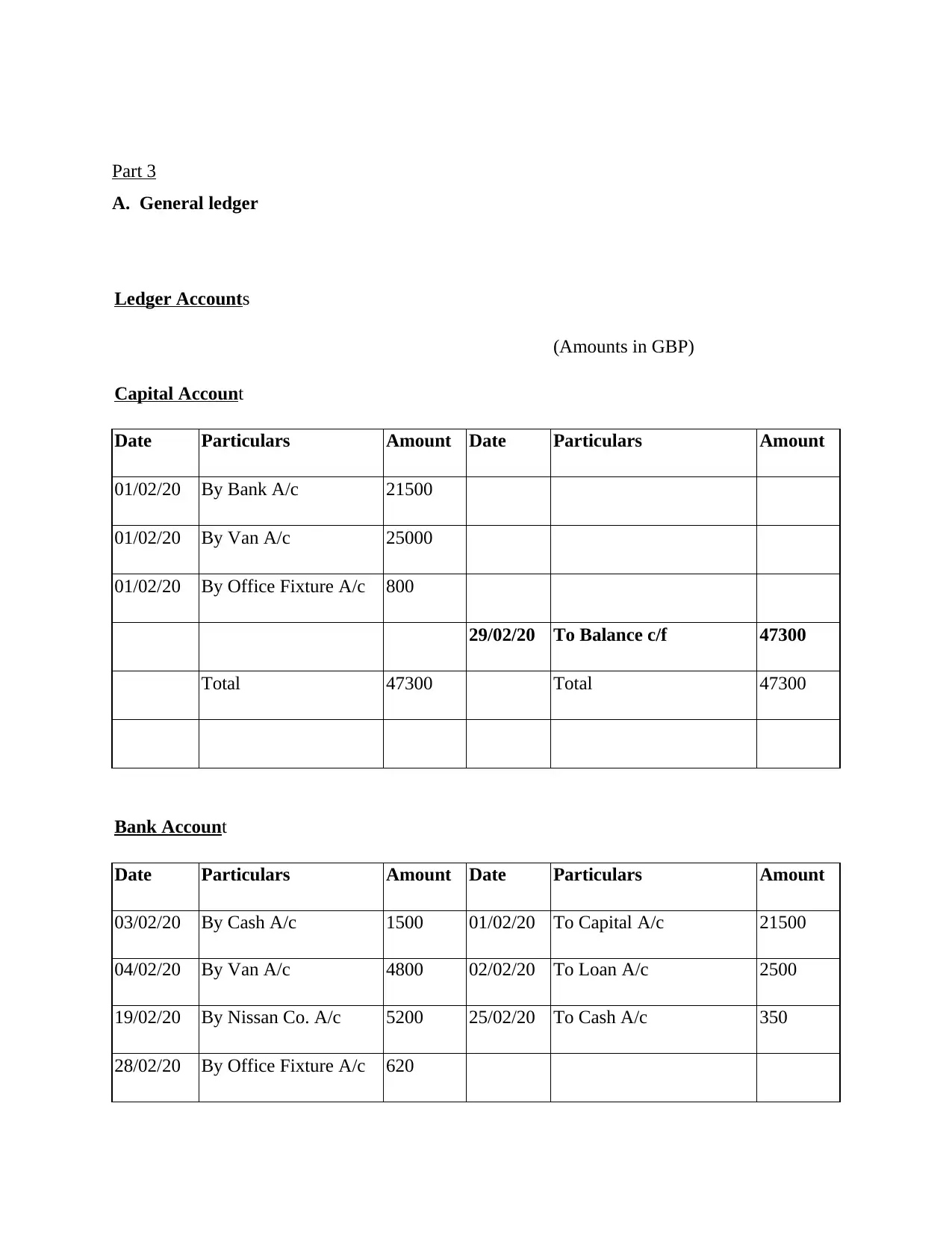

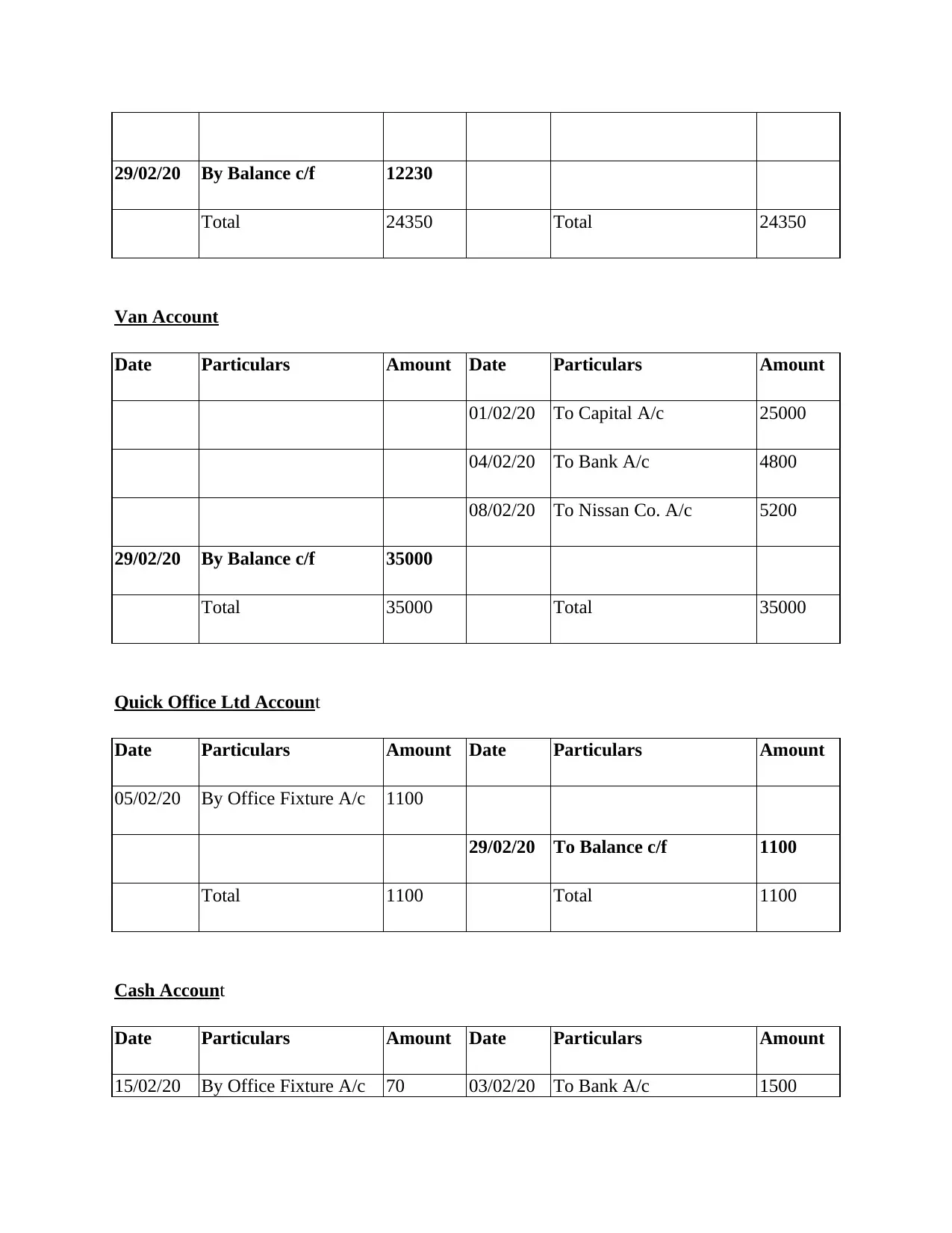

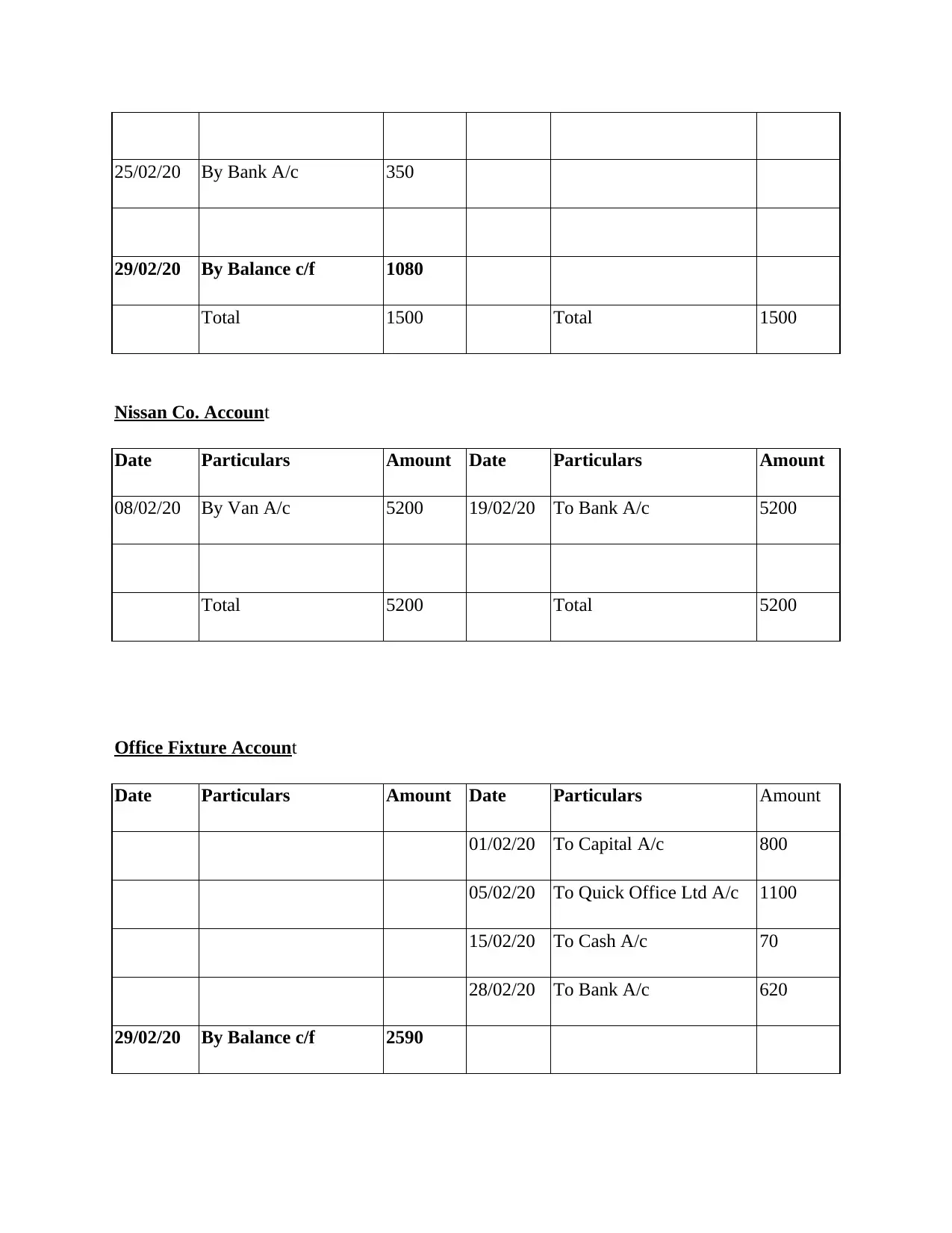

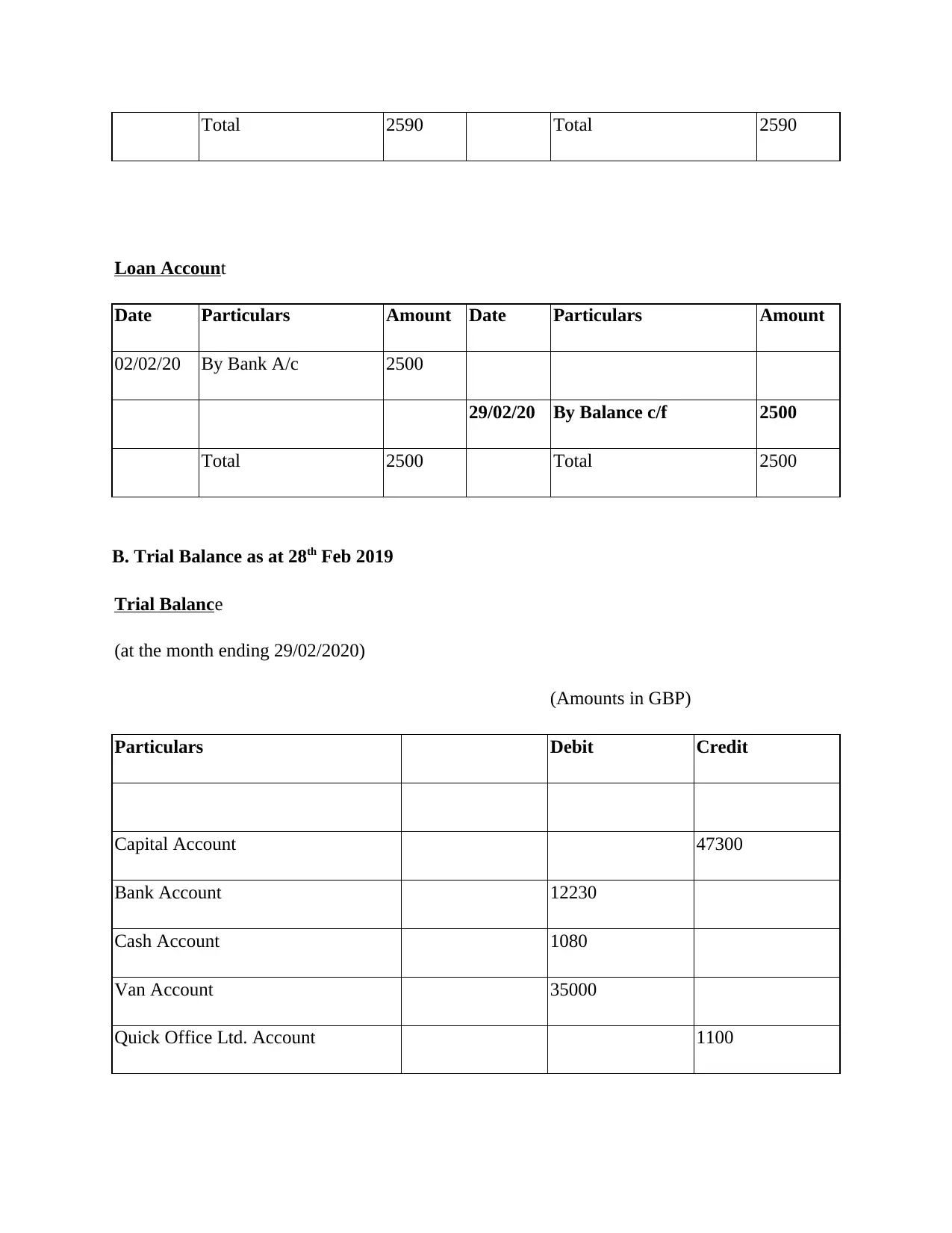

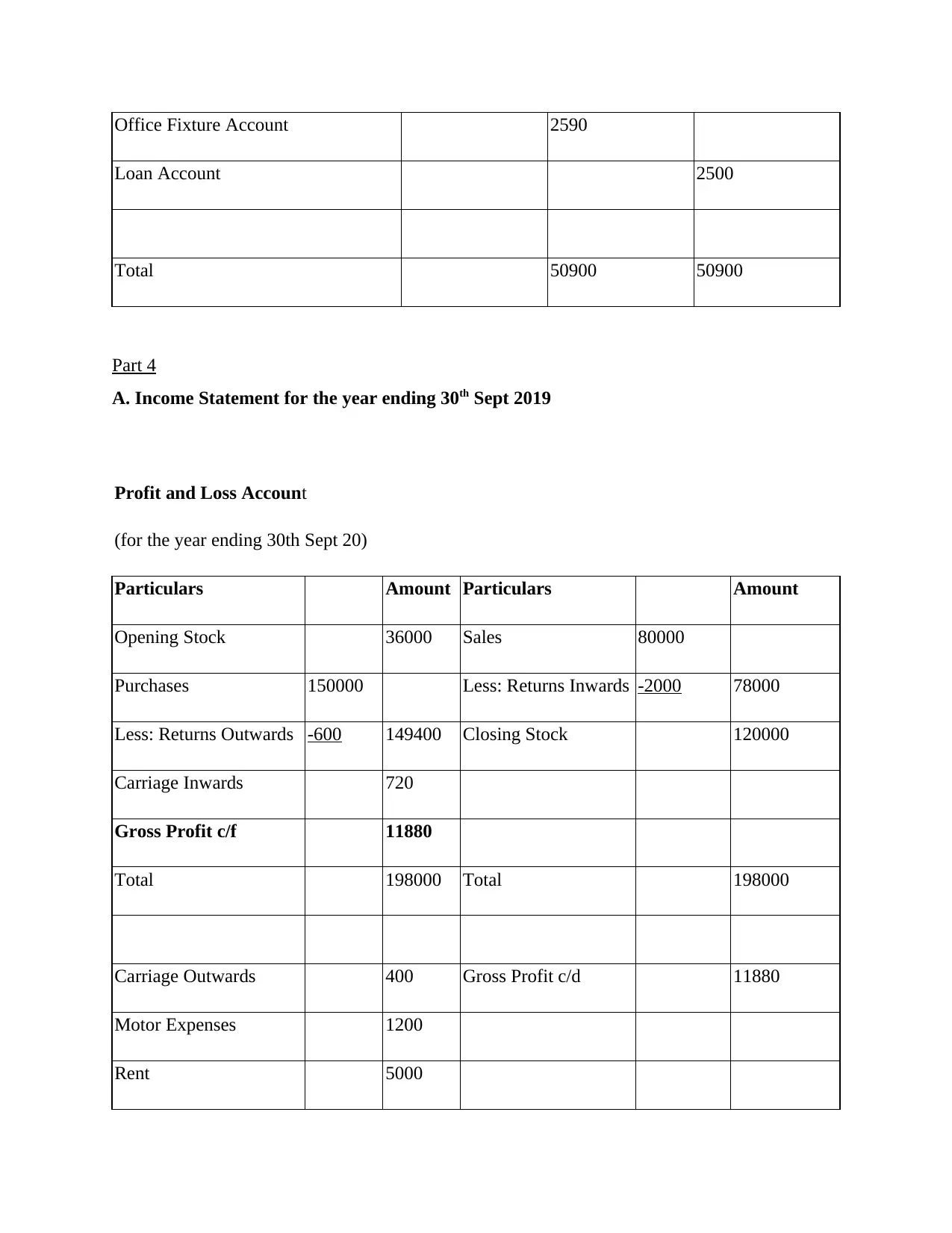

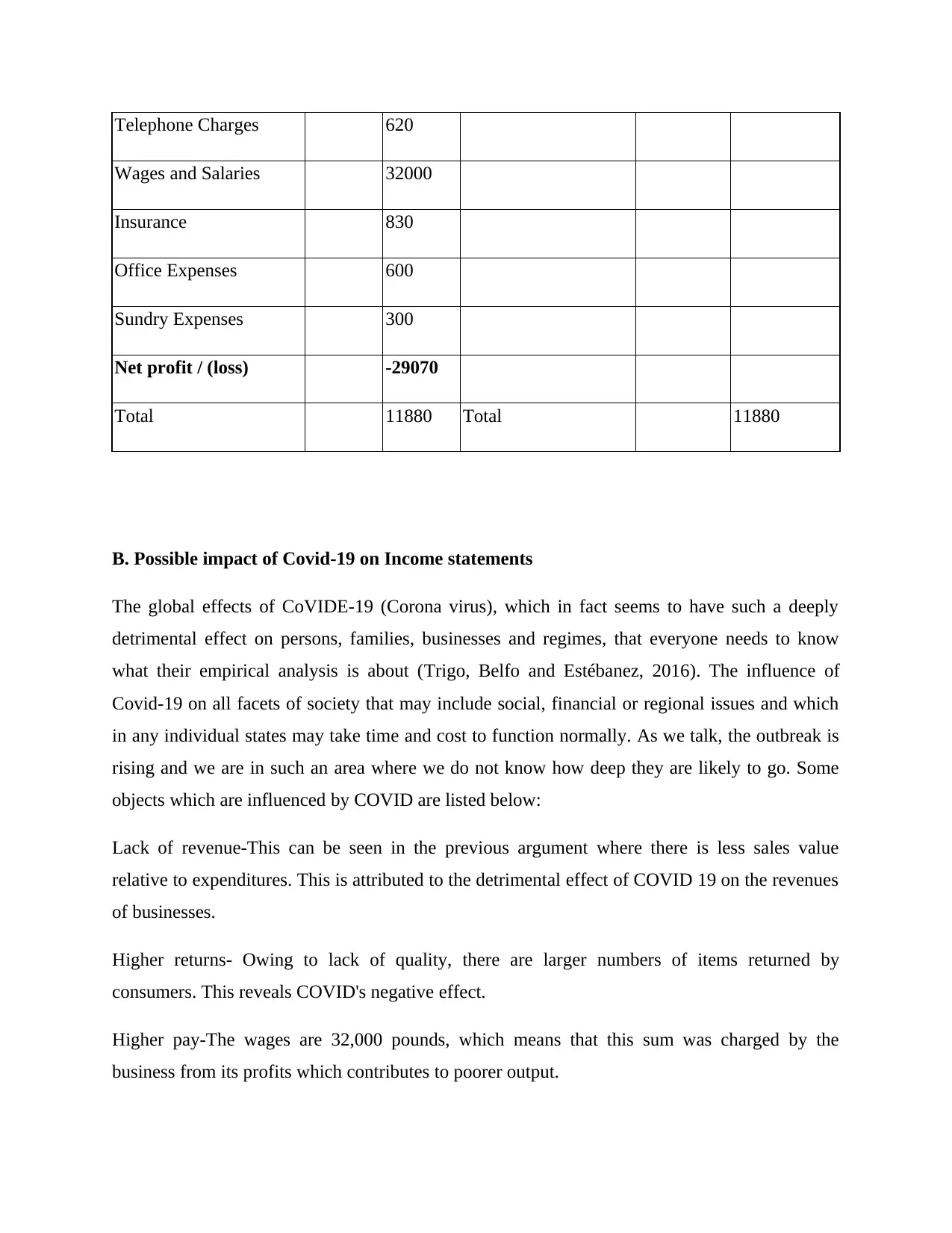

This document presents a comprehensive solution to a recording business transactions assignment, likely for a university-level accounting course. It begins with an introduction to accounting principles, emphasizing the role of financial information in decision-making. The main body of the assignment is divided into multiple parts. Part 1 addresses the roles of decision-makers and the importance of accounting information, along with the advantages and disadvantages of different business structures. Part 2 provides journal entries for various transactions in February 2020. Part 3 includes general ledger accounts and a trial balance. Finally, Part 4 presents an income statement and discusses the potential impacts of COVID-19 on income statements. The solution includes references to academic sources, demonstrating a strong understanding of accounting concepts and their practical application.

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.