Accounting: Recording and Reporting Business Transactions Analysis

VerifiedAdded on 2023/01/03

|13

|2100

|54

Report

AI Summary

This report provides a detailed analysis of recording and reporting business transactions. It begins by identifying decision-makers in organizations and their requirements for accounting information, discussing the advantages and disadvantages of accounting practices. The report then presents practical examples, including journal entries for David and a general ledger and trial balance for Pearce & Sons. Finally, it addresses the impact of the COVID-19 pandemic on income statements, considering factors such as reduced productivity and profitability, and the need for economic resilience. The report covers various aspects of accounting, from fundamental principles to practical applications, making it a comprehensive resource for understanding financial transactions and their implications.

Recording Business Transaction

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

PART 1............................................................................................................................................3

PART 2............................................................................................................................................5

PART 3............................................................................................................................................6

PART 4..........................................................................................................................................10

CONCLUSION..............................................................................................................................12

REFERENCE.................................................................................................................................13

INTRODUCTION...........................................................................................................................3

PART 1............................................................................................................................................3

PART 2............................................................................................................................................5

PART 3............................................................................................................................................6

PART 4..........................................................................................................................................10

CONCLUSION..............................................................................................................................12

REFERENCE.................................................................................................................................13

INTRODUCTION

Accounting term points out towards activities or practises for defining and assessing

quantitative financial transactions and presents such financial information to company's decision-

makers. Accounting is an integrated methodology. The framework in which an organisation 's

financial statements are documented over a fixed period of time to recognize the operational

performance and financial status of that company and evaluate and transmit same to concerned

users is termed as Accounting. The study-report covers numerous concepts relating to the

accounting and the documentation of finance transactions. The study-report consists of

discussions regarding corporate decision-makers as well as degree to which accounting

knowledge, positives and negatives of accounting, and also practical activities are needed to

report company transactions and produce financial reports.

PART 1

Recognising decision-makers and describe their requirements with regard to accounting-

information:

Decision-makers are key part of organization and includes people, usually in

top leadership, who take vital decisions which have impacts on way the corporation runs.

Organizational staff who are successful decision-makers consider how to efficiently overcome

problems and use strategic thinking capabilities to help fix concerns. They can quickly weigh the

various options and decide on the outcome that best suits the organisation and its staff.

Decision-makers discourage businesses from making premature decisions that impede

company growth. These are vital part of any company and they maximise connectivity, human

capital and operations management. Efficient decision-makers manage difficult problems and

select the best approach that presents their business with most longer-term benefits. In brief, an

effective decision could transform a corporation significantly. Wrong decision will have

significant ramifications for companies in any niche. Effective leadership decision-making lets

businesses secure revenue, create new prospects, develop their promotional processes and

enhance the awareness of their brands. It is also helpful for development plans. At the end of the

day the strongest decision-makers ensure market performance. Decision-makers are typically

senior management staff within the corporation, which is the case in Seveso, a global UK-based

supermarket-chain whose board of directors are the company’s key decision makers. Tesco’s

board-of-directors have:

Accounting term points out towards activities or practises for defining and assessing

quantitative financial transactions and presents such financial information to company's decision-

makers. Accounting is an integrated methodology. The framework in which an organisation 's

financial statements are documented over a fixed period of time to recognize the operational

performance and financial status of that company and evaluate and transmit same to concerned

users is termed as Accounting. The study-report covers numerous concepts relating to the

accounting and the documentation of finance transactions. The study-report consists of

discussions regarding corporate decision-makers as well as degree to which accounting

knowledge, positives and negatives of accounting, and also practical activities are needed to

report company transactions and produce financial reports.

PART 1

Recognising decision-makers and describe their requirements with regard to accounting-

information:

Decision-makers are key part of organization and includes people, usually in

top leadership, who take vital decisions which have impacts on way the corporation runs.

Organizational staff who are successful decision-makers consider how to efficiently overcome

problems and use strategic thinking capabilities to help fix concerns. They can quickly weigh the

various options and decide on the outcome that best suits the organisation and its staff.

Decision-makers discourage businesses from making premature decisions that impede

company growth. These are vital part of any company and they maximise connectivity, human

capital and operations management. Efficient decision-makers manage difficult problems and

select the best approach that presents their business with most longer-term benefits. In brief, an

effective decision could transform a corporation significantly. Wrong decision will have

significant ramifications for companies in any niche. Effective leadership decision-making lets

businesses secure revenue, create new prospects, develop their promotional processes and

enhance the awareness of their brands. It is also helpful for development plans. At the end of the

day the strongest decision-makers ensure market performance. Decision-makers are typically

senior management staff within the corporation, which is the case in Seveso, a global UK-based

supermarket-chain whose board of directors are the company’s key decision makers. Tesco’s

board-of-directors have:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1. Non-executive Chairman: Jhon Allan

2. Group Chief Executive: Ken Murphy

3. CFO: Alan Stewart

4. Non-executive Directors: Stewart Gilliland Independent.

5. Independent Non-executive Director: Byron Grote, Alison Platt, Mikael Olsson, Steve

Golsby and Simon Patterson

Decision makers utilizes accounting reports and information to assess and examine the

operating performance and status of the company, to take critical steps and to undertake effective

measures to enhance economic performance in consideration of revenue, company's financial.

Another main functions of decision maker is to lay down guidelines and procedures for the

accomplishment of corporate objectives. To this end, decision makers utilizes information

created by organization's financial and management accounting systems. They need accounting

reports on the company's sales, results and liquidity costs for strategy, reporting and decision-

making. The decision-makers are interested in deciding the ability of the community to raise

profits. It is responsible for assessing liquidity of the company and for meeting its financial

obligations on time. Various ratios/proportions, such as debt–equity ratio, present ratio, etc. They

want accounting information in order to consider shorter-term or longer-term profitability of a

business. Similarly, the need for shorter and longer-term finances could be established with the

help of Cash-Flows Statements.

Financial accounts/statements reflect all accounting transactions relating to the business

in a nutshell that allows it feasible and convenient for the executive team, alongside

corporate managers, to use this knowledge in the implementation of strategies. In which the

financial statements are drawn out on the grounds of common standards and procedures

that are same across the sector. This allows them to distinguish themselves from other rivals for

positioning around industry benchmarks. It establishes a framework for management/BOD to

take decisions on the capital budgeting, including whether such decisions are desirable and

commercially viable for the organisation to take. Furthermore, forecasts and predictions are both

based on financial information within the organisation and on change as per business conditions.

This is important not just in respect of comparative analysis, but also in respect of the framework

for collecting valuable knowledge through non-financial details.

2. Group Chief Executive: Ken Murphy

3. CFO: Alan Stewart

4. Non-executive Directors: Stewart Gilliland Independent.

5. Independent Non-executive Director: Byron Grote, Alison Platt, Mikael Olsson, Steve

Golsby and Simon Patterson

Decision makers utilizes accounting reports and information to assess and examine the

operating performance and status of the company, to take critical steps and to undertake effective

measures to enhance economic performance in consideration of revenue, company's financial.

Another main functions of decision maker is to lay down guidelines and procedures for the

accomplishment of corporate objectives. To this end, decision makers utilizes information

created by organization's financial and management accounting systems. They need accounting

reports on the company's sales, results and liquidity costs for strategy, reporting and decision-

making. The decision-makers are interested in deciding the ability of the community to raise

profits. It is responsible for assessing liquidity of the company and for meeting its financial

obligations on time. Various ratios/proportions, such as debt–equity ratio, present ratio, etc. They

want accounting information in order to consider shorter-term or longer-term profitability of a

business. Similarly, the need for shorter and longer-term finances could be established with the

help of Cash-Flows Statements.

Financial accounts/statements reflect all accounting transactions relating to the business

in a nutshell that allows it feasible and convenient for the executive team, alongside

corporate managers, to use this knowledge in the implementation of strategies. In which the

financial statements are drawn out on the grounds of common standards and procedures

that are same across the sector. This allows them to distinguish themselves from other rivals for

positioning around industry benchmarks. It establishes a framework for management/BOD to

take decisions on the capital budgeting, including whether such decisions are desirable and

commercially viable for the organisation to take. Furthermore, forecasts and predictions are both

based on financial information within the organisation and on change as per business conditions.

This is important not just in respect of comparative analysis, but also in respect of the framework

for collecting valuable knowledge through non-financial details.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Advantages and disadvantages of accounting:

Advantages:

Comparative Performance/results analysis:

Accounting enables it easier to compare financial reports of timeframe with past years. Decision

makers should also analyse the formal reporting of both financial as well as accounting

operations in line with the norms of corporation.

Decision makings

Decision making will be simpler/easier for administrators when there is comprehensive

accounting of financial transactions. Balance sheet and Profit or loss make it easier for managers

to organize, arrange and coordinate activities in different entities. That includes statistics on

funds inflows and outflows alongside revenues and expenses that make it convenient to estimate

the shortfall or savings within funds that should be dealt within timely manner. Which further

leads to the production of transparency and monitoring in the detection and recognition of

misconduct.

Disadvantage:

Depicts accounting data in money-terms only

Non-fiscal activities can affect on accounts. Only finance form transactions can be evaluated by

the accounting personnel. Obviously, financial activities are described in money terms. It offers

an incomplete portrait during the execution of legislation and the introduction of important

business decisions. In case of two business, directors of the corporation cannot on the basis of

accounting records, take choices relating to other variables, like political, cultural, social and

many other factors.

Accounting information may be subjected to bias

Accounting professionals have personal effect on accounting reports of the company. The

accounting personnel can use separate calculations of stock valuation, depreciation methods,

categorisation of earnings and capital expense, etc to determine income of company.

PART 2

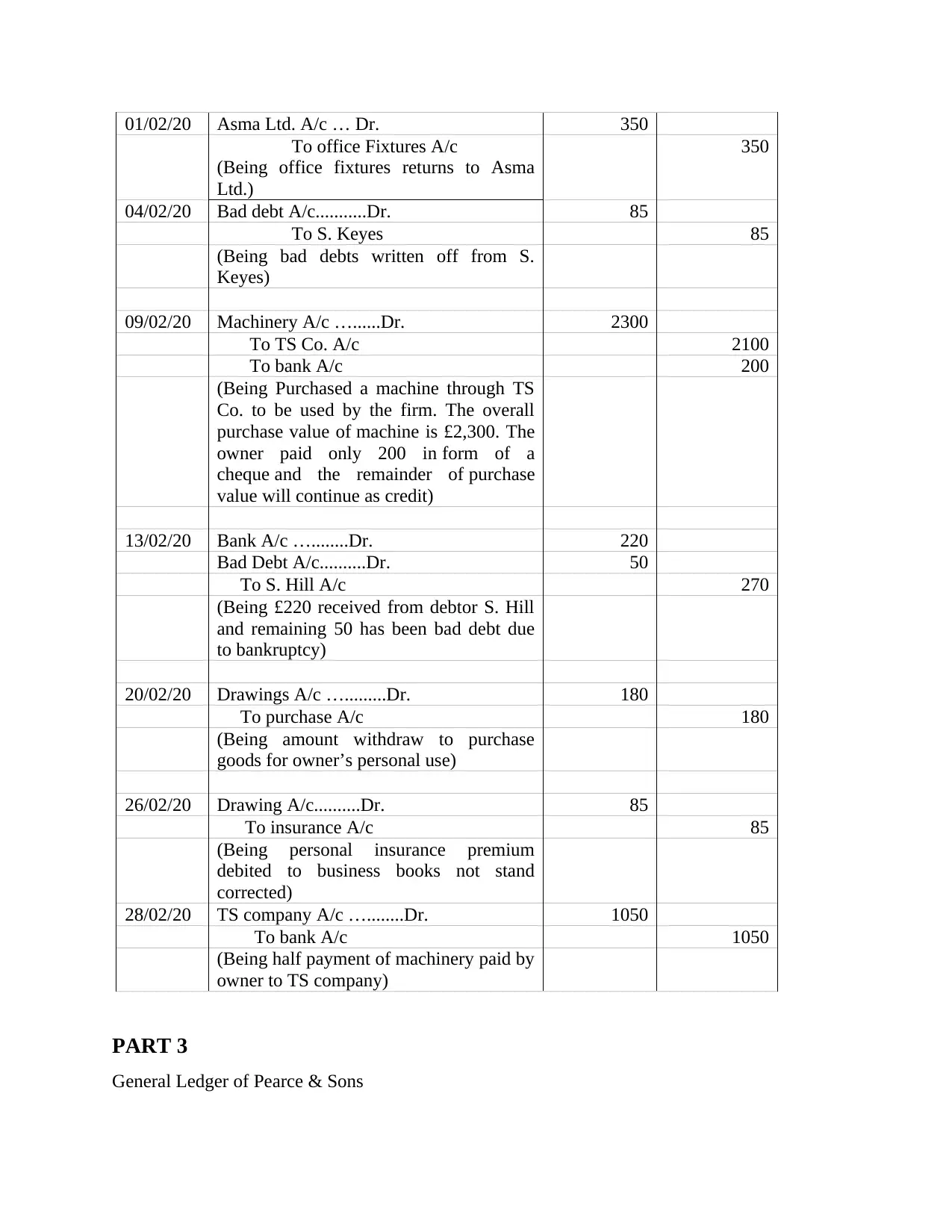

A. Journal Entries of David for the month February 2020

Journal Entries

Date Particulars Dr. (£) Cr. (£)

Advantages:

Comparative Performance/results analysis:

Accounting enables it easier to compare financial reports of timeframe with past years. Decision

makers should also analyse the formal reporting of both financial as well as accounting

operations in line with the norms of corporation.

Decision makings

Decision making will be simpler/easier for administrators when there is comprehensive

accounting of financial transactions. Balance sheet and Profit or loss make it easier for managers

to organize, arrange and coordinate activities in different entities. That includes statistics on

funds inflows and outflows alongside revenues and expenses that make it convenient to estimate

the shortfall or savings within funds that should be dealt within timely manner. Which further

leads to the production of transparency and monitoring in the detection and recognition of

misconduct.

Disadvantage:

Depicts accounting data in money-terms only

Non-fiscal activities can affect on accounts. Only finance form transactions can be evaluated by

the accounting personnel. Obviously, financial activities are described in money terms. It offers

an incomplete portrait during the execution of legislation and the introduction of important

business decisions. In case of two business, directors of the corporation cannot on the basis of

accounting records, take choices relating to other variables, like political, cultural, social and

many other factors.

Accounting information may be subjected to bias

Accounting professionals have personal effect on accounting reports of the company. The

accounting personnel can use separate calculations of stock valuation, depreciation methods,

categorisation of earnings and capital expense, etc to determine income of company.

PART 2

A. Journal Entries of David for the month February 2020

Journal Entries

Date Particulars Dr. (£) Cr. (£)

01/02/20 Asma Ltd. A/c … Dr. 350

To office Fixtures A/c

(Being office fixtures returns to Asma

Ltd.)

350

04/02/20 Bad debt A/c...........Dr. 85

To S. Keyes 85

(Being bad debts written off from S.

Keyes)

09/02/20 Machinery A/c …......Dr. 2300

To TS Co. A/c 2100

To bank A/c 200

(Being Purchased a machine through TS

Co. to be used by the firm. The overall

purchase value of machine is £2,300. The

owner paid only 200 in form of a

cheque and the remainder of purchase

value will continue as credit)

13/02/20 Bank A/c …........Dr. 220

Bad Debt A/c..........Dr. 50

To S. Hill A/c 270

(Being £220 received from debtor S. Hill

and remaining 50 has been bad debt due

to bankruptcy)

20/02/20 Drawings A/c ….........Dr. 180

To purchase A/c 180

(Being amount withdraw to purchase

goods for owner’s personal use)

26/02/20 Drawing A/c..........Dr. 85

To insurance A/c 85

(Being personal insurance premium

debited to business books not stand

corrected)

28/02/20 TS company A/c …........Dr. 1050

To bank A/c 1050

(Being half payment of machinery paid by

owner to TS company)

PART 3

General Ledger of Pearce & Sons

To office Fixtures A/c

(Being office fixtures returns to Asma

Ltd.)

350

04/02/20 Bad debt A/c...........Dr. 85

To S. Keyes 85

(Being bad debts written off from S.

Keyes)

09/02/20 Machinery A/c …......Dr. 2300

To TS Co. A/c 2100

To bank A/c 200

(Being Purchased a machine through TS

Co. to be used by the firm. The overall

purchase value of machine is £2,300. The

owner paid only 200 in form of a

cheque and the remainder of purchase

value will continue as credit)

13/02/20 Bank A/c …........Dr. 220

Bad Debt A/c..........Dr. 50

To S. Hill A/c 270

(Being £220 received from debtor S. Hill

and remaining 50 has been bad debt due

to bankruptcy)

20/02/20 Drawings A/c ….........Dr. 180

To purchase A/c 180

(Being amount withdraw to purchase

goods for owner’s personal use)

26/02/20 Drawing A/c..........Dr. 85

To insurance A/c 85

(Being personal insurance premium

debited to business books not stand

corrected)

28/02/20 TS company A/c …........Dr. 1050

To bank A/c 1050

(Being half payment of machinery paid by

owner to TS company)

PART 3

General Ledger of Pearce & Sons

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

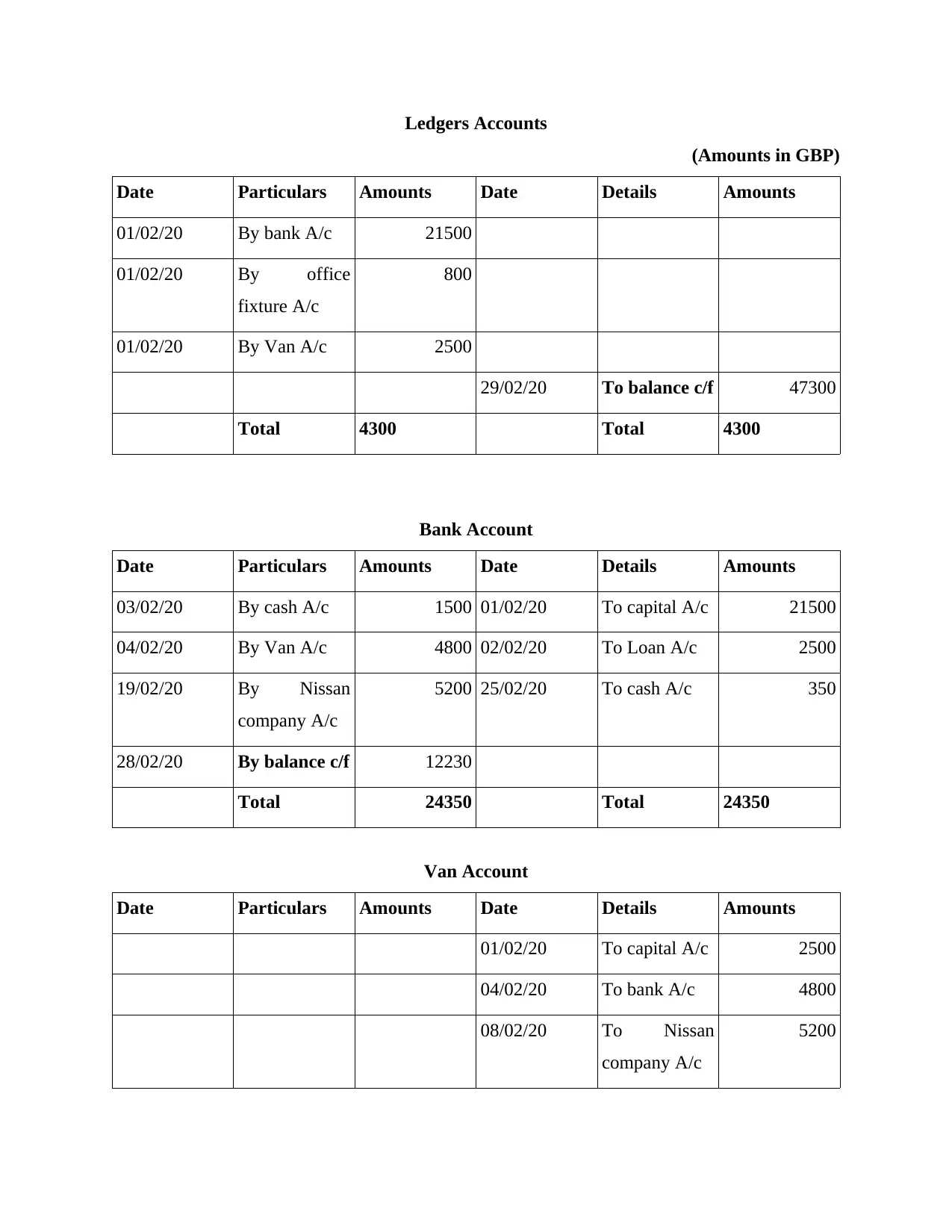

Ledgers Accounts

(Amounts in GBP)

Date Particulars Amounts Date Details Amounts

01/02/20 By bank A/c 21500

01/02/20 By office

fixture A/c

800

01/02/20 By Van A/c 2500

29/02/20 To balance c/f 47300

Total 4300 Total 4300

Bank Account

Date Particulars Amounts Date Details Amounts

03/02/20 By cash A/c 1500 01/02/20 To capital A/c 21500

04/02/20 By Van A/c 4800 02/02/20 To Loan A/c 2500

19/02/20 By Nissan

company A/c

5200 25/02/20 To cash A/c 350

28/02/20 By balance c/f 12230

Total 24350 Total 24350

Van Account

Date Particulars Amounts Date Details Amounts

01/02/20 To capital A/c 2500

04/02/20 To bank A/c 4800

08/02/20 To Nissan

company A/c

5200

(Amounts in GBP)

Date Particulars Amounts Date Details Amounts

01/02/20 By bank A/c 21500

01/02/20 By office

fixture A/c

800

01/02/20 By Van A/c 2500

29/02/20 To balance c/f 47300

Total 4300 Total 4300

Bank Account

Date Particulars Amounts Date Details Amounts

03/02/20 By cash A/c 1500 01/02/20 To capital A/c 21500

04/02/20 By Van A/c 4800 02/02/20 To Loan A/c 2500

19/02/20 By Nissan

company A/c

5200 25/02/20 To cash A/c 350

28/02/20 By balance c/f 12230

Total 24350 Total 24350

Van Account

Date Particulars Amounts Date Details Amounts

01/02/20 To capital A/c 2500

04/02/20 To bank A/c 4800

08/02/20 To Nissan

company A/c

5200

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

29/02/20 By balance c/f 35000

Total 35000 Total 35000

Quick office Ltd Account

Date Particulars Amounts Date Details Amounts

05/02/20 By office

fixture A/c

1100

29/02/20 To balance c/f 1100

Total 1100 Total 1100

Cash Account

Date Particulars Amounts Date Details Amounts

15/02/20 By Office

Fixture A/c

70 03/02/20 To bank A/c 1500

25/02/20 By bank A/c 350

29/02/20 By balance c/f 1080

Total 1500 Total 1500

Nissan company Account

Date Particulars Amounts Date Details Amounts

08/02/20 By van A/c 5200 19/02/20 To bank A/c 5200

Total 5200 Total 5200

Office Fixture Account

Date Particulars Amounts Date Details Amounts

01/02/20 To Capital A/c 800

Total 35000 Total 35000

Quick office Ltd Account

Date Particulars Amounts Date Details Amounts

05/02/20 By office

fixture A/c

1100

29/02/20 To balance c/f 1100

Total 1100 Total 1100

Cash Account

Date Particulars Amounts Date Details Amounts

15/02/20 By Office

Fixture A/c

70 03/02/20 To bank A/c 1500

25/02/20 By bank A/c 350

29/02/20 By balance c/f 1080

Total 1500 Total 1500

Nissan company Account

Date Particulars Amounts Date Details Amounts

08/02/20 By van A/c 5200 19/02/20 To bank A/c 5200

Total 5200 Total 5200

Office Fixture Account

Date Particulars Amounts Date Details Amounts

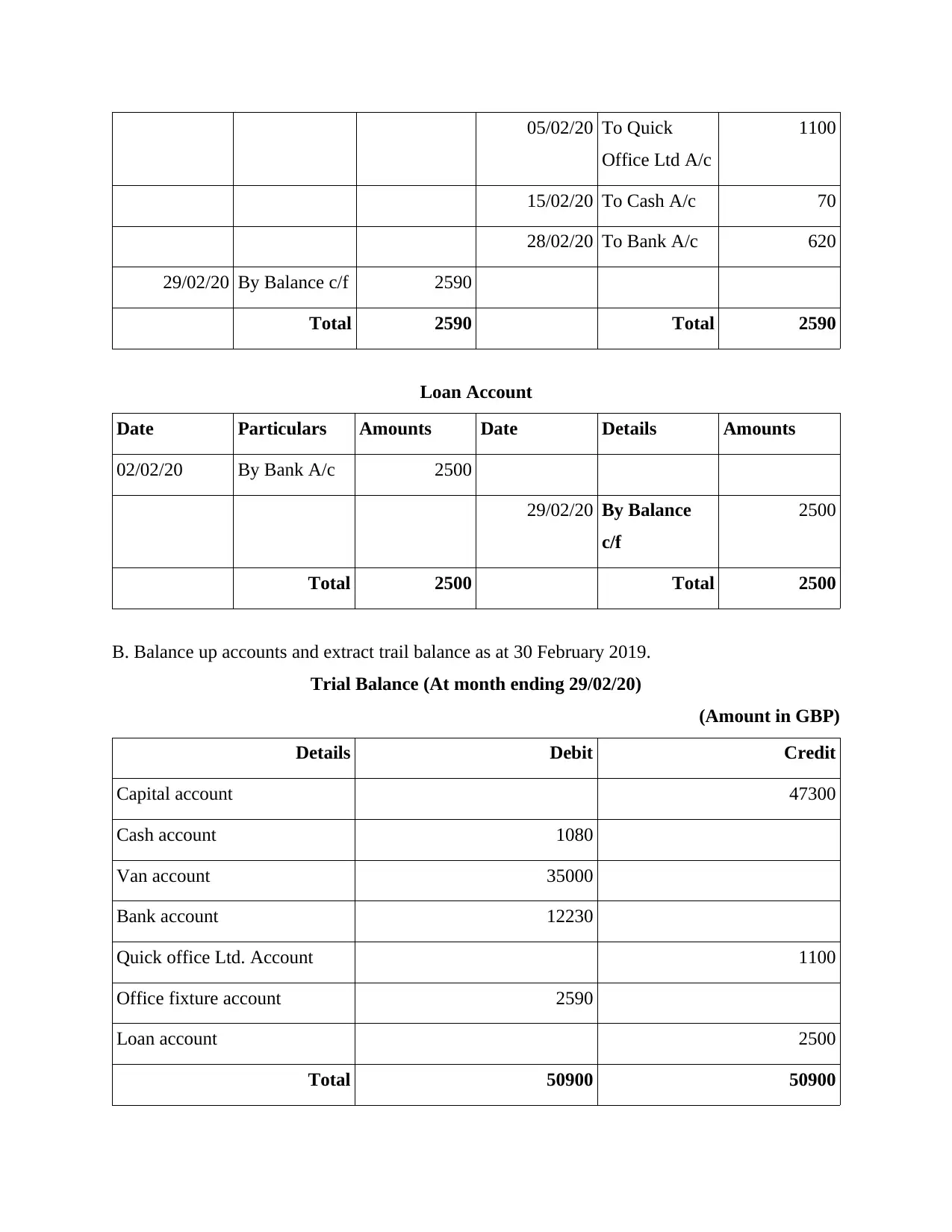

01/02/20 To Capital A/c 800

05/02/20 To Quick

Office Ltd A/c

1100

15/02/20 To Cash A/c 70

28/02/20 To Bank A/c 620

29/02/20 By Balance c/f 2590

Total 2590 Total 2590

Loan Account

Date Particulars Amounts Date Details Amounts

02/02/20 By Bank A/c 2500

29/02/20 By Balance

c/f

2500

Total 2500 Total 2500

B. Balance up accounts and extract trail balance as at 30 February 2019.

Trial Balance (At month ending 29/02/20)

(Amount in GBP)

Details Debit Credit

Capital account 47300

Cash account 1080

Van account 35000

Bank account 12230

Quick office Ltd. Account 1100

Office fixture account 2590

Loan account 2500

Total 50900 50900

Office Ltd A/c

1100

15/02/20 To Cash A/c 70

28/02/20 To Bank A/c 620

29/02/20 By Balance c/f 2590

Total 2590 Total 2590

Loan Account

Date Particulars Amounts Date Details Amounts

02/02/20 By Bank A/c 2500

29/02/20 By Balance

c/f

2500

Total 2500 Total 2500

B. Balance up accounts and extract trail balance as at 30 February 2019.

Trial Balance (At month ending 29/02/20)

(Amount in GBP)

Details Debit Credit

Capital account 47300

Cash account 1080

Van account 35000

Bank account 12230

Quick office Ltd. Account 1100

Office fixture account 2590

Loan account 2500

Total 50900 50900

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

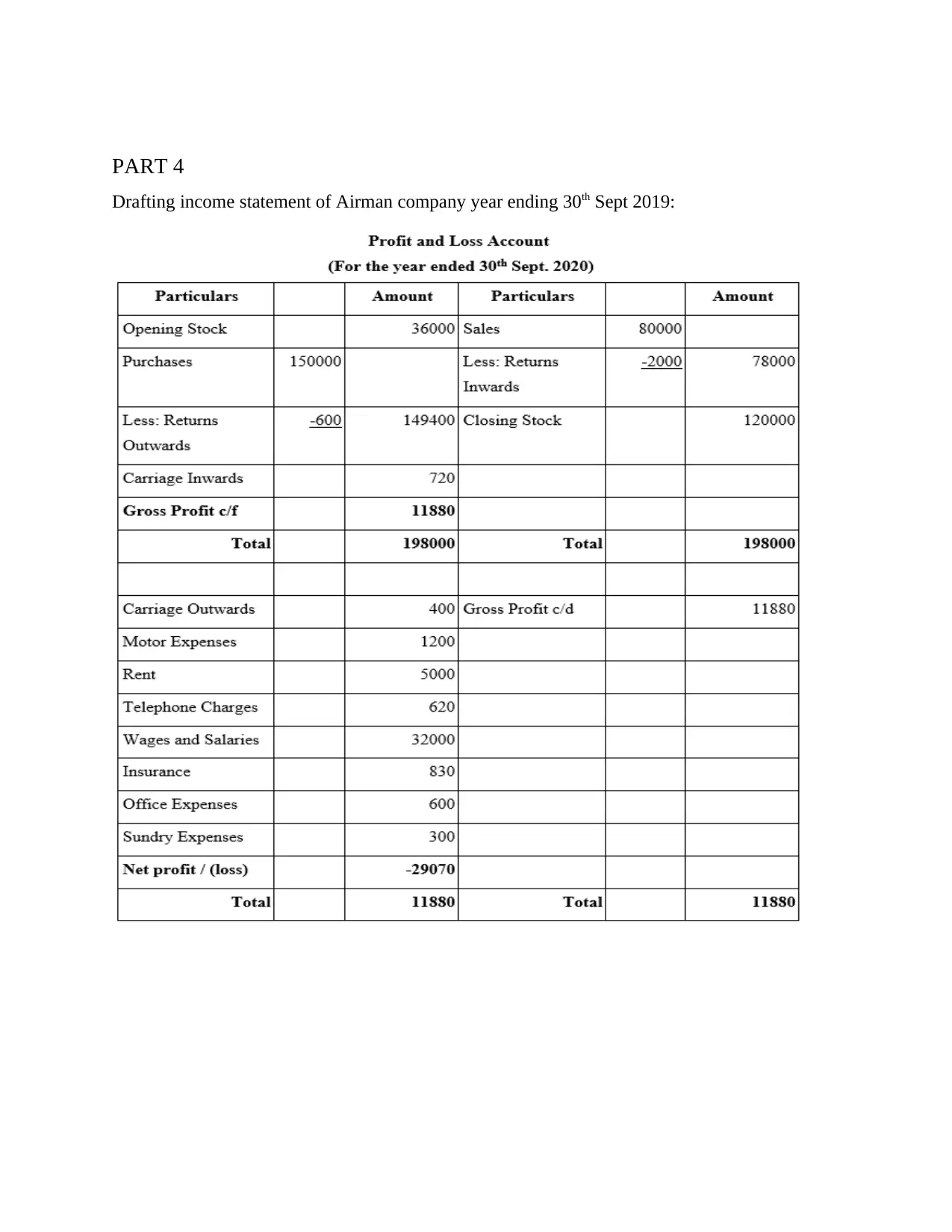

PART 4

Drafting income statement of Airman company year ending 30th Sept 2019:

Drafting income statement of Airman company year ending 30th Sept 2019:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Impacts of the COVID -19 pandemic on income statement.

Company require economic, social and also political resilience for development and

progression. Instability resulted in a reduction in Group's productivity and profitability, as well

as a rise in deficits/losses in company such as Airman, who have been financial and profitable

for Ten years since year-2009 and are experiencing losses in current year. In analysing the

consequences of COVID-19, the corporation should consider as the COVID-19 only earnings

and losses that are marginal in industry and also directly attributable to COVID-19. Selling and

losses could not be improved or maintained if COVID-19 outbreak did not occur and are thus

unlikely to recur until effects had completely receded. The recurrent profits and expenses which

might have been earned or incurred independently of COVID are not in effect, gradual. These

shall not be considered to be income or expenses attributed to COVID and shall not be included

as such in account of sales.

Evaluating the levels of additional revenues and expenditures directly owing to COVID-19

would require a judgement, the extent to which this would be necessary to depend on the

applicable facts and circumstances and declaration to that impact. Certain sources of income and

investment can be calculated more specifically in regard to COVID-19, for example extra

hygiene sanitation costs incurred as part of treatment or prevention of infectious diseases;

temporary liability incurred to staff; fines for non-performance of such contracts contributing to

the closure of manufacturing plants; lease agreements made by lessor as direct consequence of

COVID-19.

It has been noted that the actions of airman corporation Covid-19 will be reduced to first 2-

quarters of Sept,19 to Mar,20 related to a small span of duration between accounting cycle and

the disease outbreak crisis. Afterwards Mar-20, it's been noted that every industry has suffered so

many losses in production, delivery and sales as a result of lock-downs in the region, Airman

Business is also confronted with revenue declines in the production chain, along with an increase

in direct expenses. There is reduction in production which reduces demands for products

across market and the company requires to reimburse fixed costs accordingly. As an outcome,

this impact on the operating condition and function of the company performance has been

analysed.

Company require economic, social and also political resilience for development and

progression. Instability resulted in a reduction in Group's productivity and profitability, as well

as a rise in deficits/losses in company such as Airman, who have been financial and profitable

for Ten years since year-2009 and are experiencing losses in current year. In analysing the

consequences of COVID-19, the corporation should consider as the COVID-19 only earnings

and losses that are marginal in industry and also directly attributable to COVID-19. Selling and

losses could not be improved or maintained if COVID-19 outbreak did not occur and are thus

unlikely to recur until effects had completely receded. The recurrent profits and expenses which

might have been earned or incurred independently of COVID are not in effect, gradual. These

shall not be considered to be income or expenses attributed to COVID and shall not be included

as such in account of sales.

Evaluating the levels of additional revenues and expenditures directly owing to COVID-19

would require a judgement, the extent to which this would be necessary to depend on the

applicable facts and circumstances and declaration to that impact. Certain sources of income and

investment can be calculated more specifically in regard to COVID-19, for example extra

hygiene sanitation costs incurred as part of treatment or prevention of infectious diseases;

temporary liability incurred to staff; fines for non-performance of such contracts contributing to

the closure of manufacturing plants; lease agreements made by lessor as direct consequence of

COVID-19.

It has been noted that the actions of airman corporation Covid-19 will be reduced to first 2-

quarters of Sept,19 to Mar,20 related to a small span of duration between accounting cycle and

the disease outbreak crisis. Afterwards Mar-20, it's been noted that every industry has suffered so

many losses in production, delivery and sales as a result of lock-downs in the region, Airman

Business is also confronted with revenue declines in the production chain, along with an increase

in direct expenses. There is reduction in production which reduces demands for products

across market and the company requires to reimburse fixed costs accordingly. As an outcome,

this impact on the operating condition and function of the company performance has been

analysed.

CONCLUSION

According to the aforementioned study, accounting is critical part of business that allows

the company to manage financial reports and to undertake business decision-making. Accounting

information are primarily utilized by decision-makers to take decisions as well as to accomplish

defined corporate goals.

According to the aforementioned study, accounting is critical part of business that allows

the company to manage financial reports and to undertake business decision-making. Accounting

information are primarily utilized by decision-makers to take decisions as well as to accomplish

defined corporate goals.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.