Financial Accounting: Recording Transactions and Statement Analysis

VerifiedAdded on 2023/06/14

|26

|4259

|381

Report

AI Summary

This report provides a detailed analysis of recording business transactions, starting with setting up a business and understanding the role of financial accounting in decision-making. It includes journal entries for F Polk, general ledgers and trial balances for Maurice and Brothers, and an income statement analysis for B Moore. The report also covers accounting ratios for Anne's business and discusses factors affecting profit increases and decreases, offering insights into financial management. Desklib provides similar solved assignments and past papers for students.

Recording Business

Transactions

Transactions

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Introduction......................................................................................................................................3

Assessment 1....................................................................................................................................3

Give consultation on setting up the business..........................................................................3

How the financial accounting helps in decision - making and who are the decision makers?5

1. Depict the journal entries of F Polk as on 1 September.....................................................5

2. Record the General Ledger and Trial Balance of the Maurice and brothers......................7

3. Prepare income Statement and analyse why the profit has increased and decreased over the

years......................................................................................................................................10

b) Why the profit has decreased and increased over the years and what will be the estimate of

profit in 2022........................................................................................................................11

Assessment 2..................................................................................................................................11

Part A.............................................................................................................................................11

a)Journal entry of Anne's business...................................................................................11

b).LEDGER OF FOR October,2021.................................................................................14

c).Trial balance as at 31 October, 2021............................................................................18

d).Income Statement of B Moore. for the year................................................................19

e). Balance Sheet.................................................................................................................19

f).This is a brief letter to Linda explaining her query concerning her holiday.....................21

PART B..........................................................................................................................................21

a) Accounting Ratios............................................................................................................21

Analysis for Anne.................................................................................................................22

Conclusion.....................................................................................................................................22

References:.....................................................................................................................................24

Introduction......................................................................................................................................3

Assessment 1....................................................................................................................................3

Give consultation on setting up the business..........................................................................3

How the financial accounting helps in decision - making and who are the decision makers?5

1. Depict the journal entries of F Polk as on 1 September.....................................................5

2. Record the General Ledger and Trial Balance of the Maurice and brothers......................7

3. Prepare income Statement and analyse why the profit has increased and decreased over the

years......................................................................................................................................10

b) Why the profit has decreased and increased over the years and what will be the estimate of

profit in 2022........................................................................................................................11

Assessment 2..................................................................................................................................11

Part A.............................................................................................................................................11

a)Journal entry of Anne's business...................................................................................11

b).LEDGER OF FOR October,2021.................................................................................14

c).Trial balance as at 31 October, 2021............................................................................18

d).Income Statement of B Moore. for the year................................................................19

e). Balance Sheet.................................................................................................................19

f).This is a brief letter to Linda explaining her query concerning her holiday.....................21

PART B..........................................................................................................................................21

a) Accounting Ratios............................................................................................................21

Analysis for Anne.................................................................................................................22

Conclusion.....................................................................................................................................22

References:.....................................................................................................................................24

Introduction

This report focuses on recording, classifying and summarising the monetary transactions of

the business concern. In this Anne York started the business of furniture in Brighton and will be

hiring financial manager to record and maintain monetary transactions in the following steps.

Firstly, these transactions will be recorded in Journal book then posted into ledger and at the last

it is summarised in financial statements. So, these financial statements will ensure that business

is performing well and consistently improving all the weak areas (DENARO, 2017). Moreover,

in this financial tools are used such as ratios which helps to compare relation between two

components as well as it helps to analyse previous profit trends. Not only this, it helps in

comparing companies of same industry and will assist them to take required actions to improve

its performance.

Assessment 1

Give consultation on setting up the business.

David Greene is the sole proprietor and is willing to start its own business as the decorator.

He knows that he is a sole proprietor and will be individually responsible for every liability and

debt of its company. He shall also be accountable and responsible for the bookkeeping duties of

it. He is not being familiar with various stages of starting up a business so there are some of the

steps which are being outlined below

Building the business model- In order to prosper as the decorator, it is the first step which

involves setting up the business framework. For instance, if David wants to run the sole

proprietorship, he must be aware of all its drawbacks and benefits.

Creating the business strategy- After the business model is being created it is essential to

create the plan as it will act as a guidance to its activity which are involved in everyday

business activities, budget and a person which will be liable to manage it willingly.

Setting up the portfolio of business- In general the portfolio of the business is more than a

brochure as it contains the broad information about the competencies and goals of the

company. It includes how a project must be carried forward in a successful manner and

also includes the profile of essential people of the business together with highlighting the

real skills, professional experience and qualifications of them (Kane, 2020).

This report focuses on recording, classifying and summarising the monetary transactions of

the business concern. In this Anne York started the business of furniture in Brighton and will be

hiring financial manager to record and maintain monetary transactions in the following steps.

Firstly, these transactions will be recorded in Journal book then posted into ledger and at the last

it is summarised in financial statements. So, these financial statements will ensure that business

is performing well and consistently improving all the weak areas (DENARO, 2017). Moreover,

in this financial tools are used such as ratios which helps to compare relation between two

components as well as it helps to analyse previous profit trends. Not only this, it helps in

comparing companies of same industry and will assist them to take required actions to improve

its performance.

Assessment 1

Give consultation on setting up the business.

David Greene is the sole proprietor and is willing to start its own business as the decorator.

He knows that he is a sole proprietor and will be individually responsible for every liability and

debt of its company. He shall also be accountable and responsible for the bookkeeping duties of

it. He is not being familiar with various stages of starting up a business so there are some of the

steps which are being outlined below

Building the business model- In order to prosper as the decorator, it is the first step which

involves setting up the business framework. For instance, if David wants to run the sole

proprietorship, he must be aware of all its drawbacks and benefits.

Creating the business strategy- After the business model is being created it is essential to

create the plan as it will act as a guidance to its activity which are involved in everyday

business activities, budget and a person which will be liable to manage it willingly.

Setting up the portfolio of business- In general the portfolio of the business is more than a

brochure as it contains the broad information about the competencies and goals of the

company. It includes how a project must be carried forward in a successful manner and

also includes the profile of essential people of the business together with highlighting the

real skills, professional experience and qualifications of them (Kane, 2020).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Obtaining necessary equipment- David Green must be aware of all the necessary as well

as essential equipment which are required for the decoration after it has established the

business strategy. Prior to purchasing essential tools, David must measure the space that

is available to him so that everything can be fitted into it.

Creation of technological road map- It is a strategic tool which comprises of combination

of long as well as short term goals of the institution with some technical options. This

will help in having an understanding of modern possibilities of technology and the goals

so that innovative process can be introduced.

Setting up social media account- As the customers nowadays prefer the searching of the

business on online product platform so David must ensure that it creates its business

social profile as well as website so that the online visibility of the business is enhanced.

Some of the social media sites like Instagram and Facebook may help the company to

stand out from its competitor as it will help in offering the samples of work in the form of

images and videos. The customer can get involved on the platform of social media by

way of sharing some good information and also asking some of the questions (Kulikova,

Aminova and Lyzhova, 2020).

Building the community network- David Greene must have the ability to strive in order to

connect with the community in a physical manner by way of engaging in some of the

charitable activity which promotes the sustainable environment. This is considered as a

win-win situation where the commitment shall be beneficial to a business and customers

will be able to appreciate the offering made by an organization. This also helps as a

contacting point between business as well as its customers and will make the goodwill of

the company.

Hence by the above mentioned steps David can set up it’s business as a decorator and can

grow its firm.

Advantages to David:

If the business is well managed, then it will get huge success in the business.

The business of decoration is at the hype in the market, it is a pro for David.

Disadvantages to David: If the venture is not managed and the cost allocation is not done

appropriately then it may suffer loss.

as essential equipment which are required for the decoration after it has established the

business strategy. Prior to purchasing essential tools, David must measure the space that

is available to him so that everything can be fitted into it.

Creation of technological road map- It is a strategic tool which comprises of combination

of long as well as short term goals of the institution with some technical options. This

will help in having an understanding of modern possibilities of technology and the goals

so that innovative process can be introduced.

Setting up social media account- As the customers nowadays prefer the searching of the

business on online product platform so David must ensure that it creates its business

social profile as well as website so that the online visibility of the business is enhanced.

Some of the social media sites like Instagram and Facebook may help the company to

stand out from its competitor as it will help in offering the samples of work in the form of

images and videos. The customer can get involved on the platform of social media by

way of sharing some good information and also asking some of the questions (Kulikova,

Aminova and Lyzhova, 2020).

Building the community network- David Greene must have the ability to strive in order to

connect with the community in a physical manner by way of engaging in some of the

charitable activity which promotes the sustainable environment. This is considered as a

win-win situation where the commitment shall be beneficial to a business and customers

will be able to appreciate the offering made by an organization. This also helps as a

contacting point between business as well as its customers and will make the goodwill of

the company.

Hence by the above mentioned steps David can set up it’s business as a decorator and can

grow its firm.

Advantages to David:

If the business is well managed, then it will get huge success in the business.

The business of decoration is at the hype in the market, it is a pro for David.

Disadvantages to David: If the venture is not managed and the cost allocation is not done

appropriately then it may suffer loss.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

How the financial accounting helps in decision - making and who are the decision makers?

Accounting includes the identification, tracking, communicating, analysing as well as

interpreting the information of accounts to the users. The main goal of the accounting system

is mainly to provide the physical information about business. The data which relates to the

physical status as well as performance of the company and is also designed in order to be

used in the process of decision making by the external and internal users. The managers at

every level of business are the decision makers as they are likely to make decisions which are

mainly based on the accounting facts and data. Tesco is a large organization which is listed

on London Stock Exchange and has different decision makers who are being responsible for

maintaining the position of the company at marketplace. Accusations as well as incentives

must be considered in order to develop the product and services and the correct information

is very important so that the business can be profitable for a long time (Rathi and Given,

2017)(Rosengren, 2018). The users of the accounting information are as follows-

Owners- They mainly review return on the investment of the business by making use

of financial information and also compare the result of it with many other

competitors.

Management- In the big companies like Tesco, there is a separation among the

shareholders and the management but these two are likely to make a choice which is

for the benefit of the company by considering the decisions of investment as well as

initiatives.

Creditors- They make the use of the accounting data so that the trustworthiness as

well as the ability of the Tesco company can be assessed so that their repayment can

be safeguarded.

Investors- Before making any investment, the capitalists are required to analyse as

well as review the financial condition of Tesco by making use of the data of

bookkeeping.

Government- It is required of the bookkeeping data so that they can collect many

types of taxes like direct or indirect (Seliverstova, 2017).

PART B

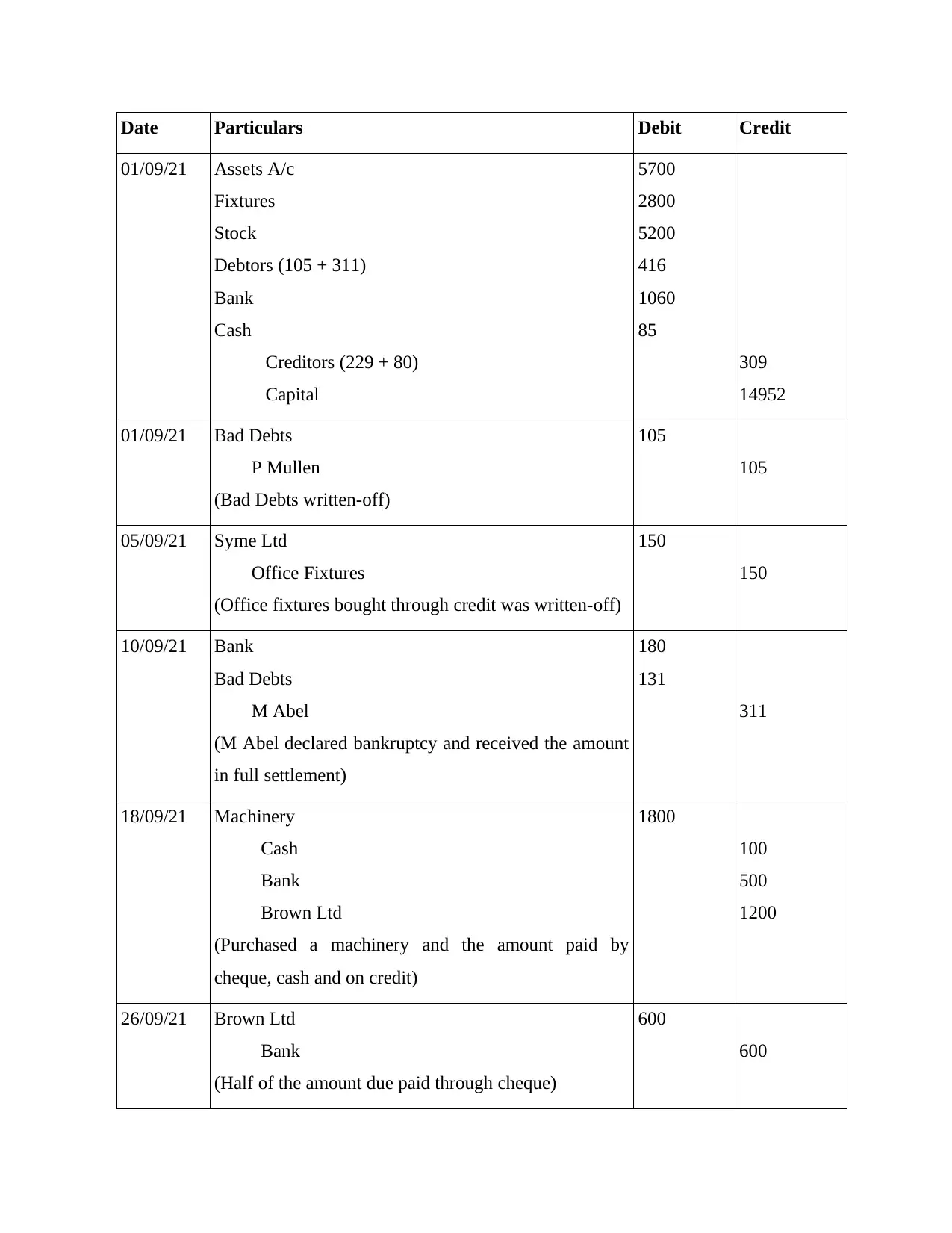

1. Depict the journal entries of F Polk as on 1 September.

JOURNAL ENTRIES – F POLK

Accounting includes the identification, tracking, communicating, analysing as well as

interpreting the information of accounts to the users. The main goal of the accounting system

is mainly to provide the physical information about business. The data which relates to the

physical status as well as performance of the company and is also designed in order to be

used in the process of decision making by the external and internal users. The managers at

every level of business are the decision makers as they are likely to make decisions which are

mainly based on the accounting facts and data. Tesco is a large organization which is listed

on London Stock Exchange and has different decision makers who are being responsible for

maintaining the position of the company at marketplace. Accusations as well as incentives

must be considered in order to develop the product and services and the correct information

is very important so that the business can be profitable for a long time (Rathi and Given,

2017)(Rosengren, 2018). The users of the accounting information are as follows-

Owners- They mainly review return on the investment of the business by making use

of financial information and also compare the result of it with many other

competitors.

Management- In the big companies like Tesco, there is a separation among the

shareholders and the management but these two are likely to make a choice which is

for the benefit of the company by considering the decisions of investment as well as

initiatives.

Creditors- They make the use of the accounting data so that the trustworthiness as

well as the ability of the Tesco company can be assessed so that their repayment can

be safeguarded.

Investors- Before making any investment, the capitalists are required to analyse as

well as review the financial condition of Tesco by making use of the data of

bookkeeping.

Government- It is required of the bookkeeping data so that they can collect many

types of taxes like direct or indirect (Seliverstova, 2017).

PART B

1. Depict the journal entries of F Polk as on 1 September.

JOURNAL ENTRIES – F POLK

Date Particulars Debit Credit

01/09/21 Assets A/c

Fixtures

Stock

Debtors (105 + 311)

Bank

Cash

Creditors (229 + 80)

Capital

5700

2800

5200

416

1060

85

309

14952

01/09/21 Bad Debts

P Mullen

(Bad Debts written-off)

105

105

05/09/21 Syme Ltd

Office Fixtures

(Office fixtures bought through credit was written-off)

150

150

10/09/21 Bank

Bad Debts

M Abel

(M Abel declared bankruptcy and received the amount

in full settlement)

180

131

311

18/09/21 Machinery

Cash

Bank

Brown Ltd

(Purchased a machinery and the amount paid by

cheque, cash and on credit)

1800

100

500

1200

26/09/21 Brown Ltd

Bank

(Half of the amount due paid through cheque)

600

600

01/09/21 Assets A/c

Fixtures

Stock

Debtors (105 + 311)

Bank

Cash

Creditors (229 + 80)

Capital

5700

2800

5200

416

1060

85

309

14952

01/09/21 Bad Debts

P Mullen

(Bad Debts written-off)

105

105

05/09/21 Syme Ltd

Office Fixtures

(Office fixtures bought through credit was written-off)

150

150

10/09/21 Bank

Bad Debts

M Abel

(M Abel declared bankruptcy and received the amount

in full settlement)

180

131

311

18/09/21 Machinery

Cash

Bank

Brown Ltd

(Purchased a machinery and the amount paid by

cheque, cash and on credit)

1800

100

500

1200

26/09/21 Brown Ltd

Bank

(Half of the amount due paid through cheque)

600

600

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

28/09/21 Insurance Expenses

Drawings

Bank

(Insurance expenses paid by bank but later realised that

£70 is of personal house)

60

70

130

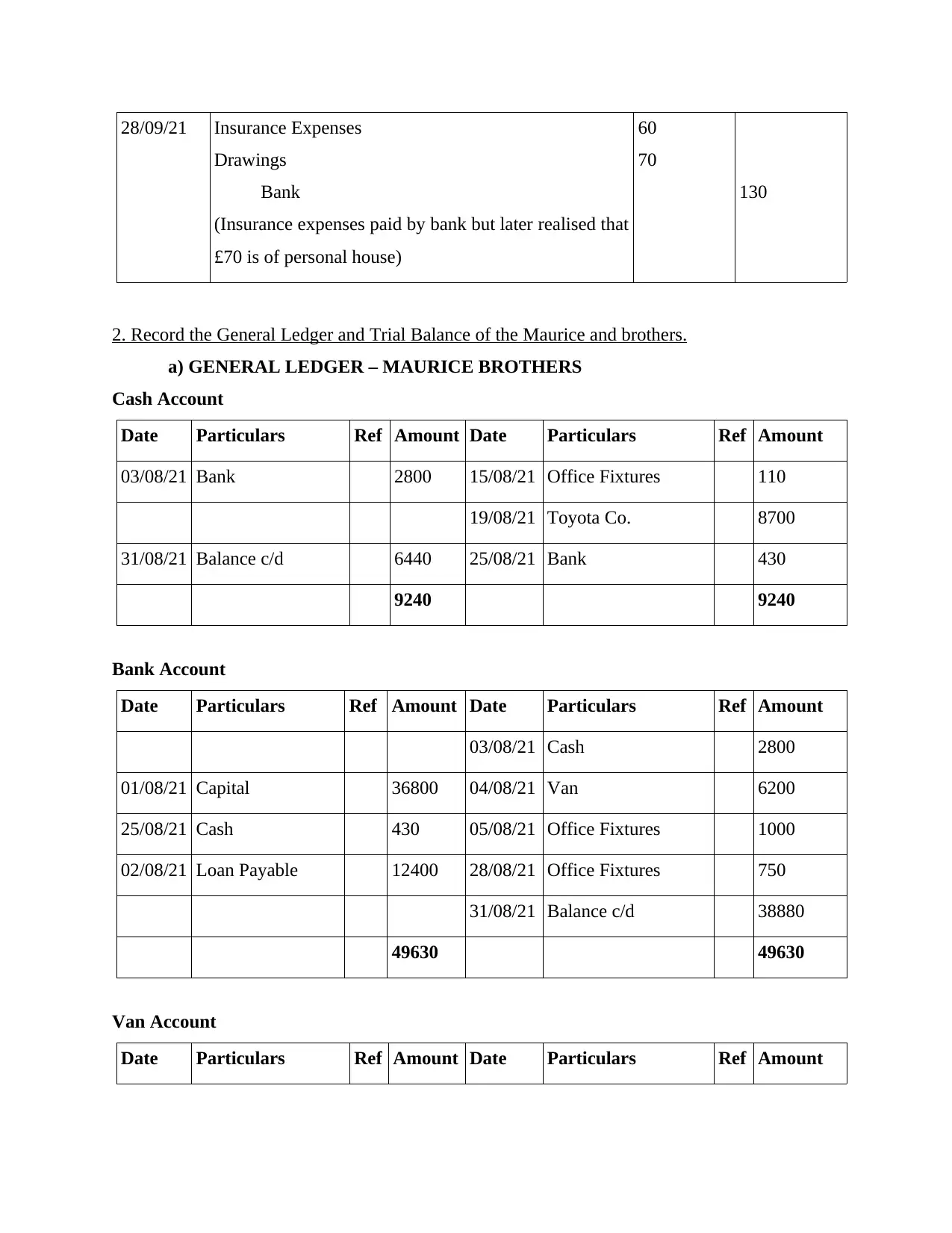

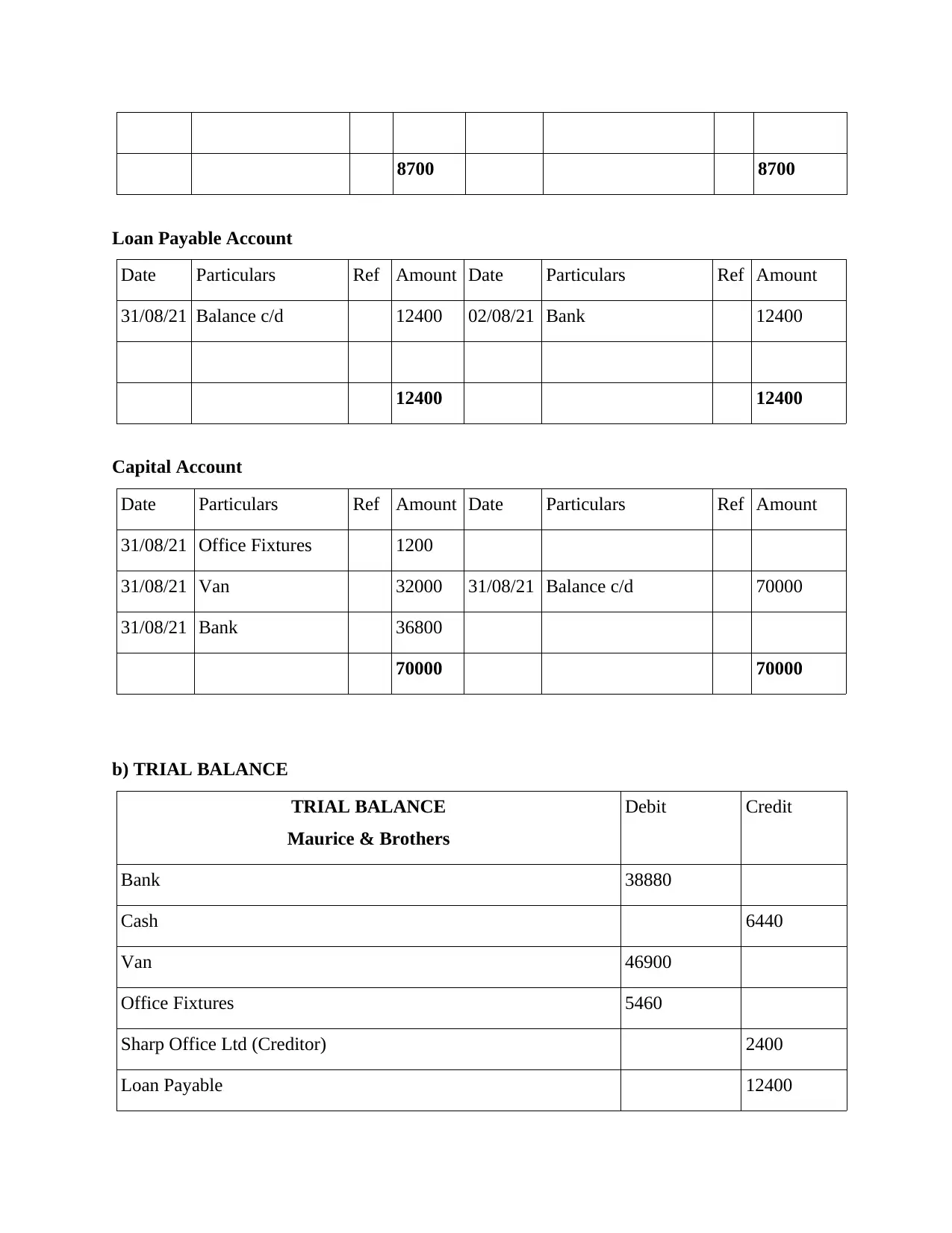

2. Record the General Ledger and Trial Balance of the Maurice and brothers.

a) GENERAL LEDGER – MAURICE BROTHERS

Cash Account

Date Particulars Ref Amount Date Particulars Ref Amount

03/08/21 Bank 2800 15/08/21 Office Fixtures 110

19/08/21 Toyota Co. 8700

31/08/21 Balance c/d 6440 25/08/21 Bank 430

9240 9240

Bank Account

Date Particulars Ref Amount Date Particulars Ref Amount

03/08/21 Cash 2800

01/08/21 Capital 36800 04/08/21 Van 6200

25/08/21 Cash 430 05/08/21 Office Fixtures 1000

02/08/21 Loan Payable 12400 28/08/21 Office Fixtures 750

31/08/21 Balance c/d 38880

49630 49630

Van Account

Date Particulars Ref Amount Date Particulars Ref Amount

Drawings

Bank

(Insurance expenses paid by bank but later realised that

£70 is of personal house)

60

70

130

2. Record the General Ledger and Trial Balance of the Maurice and brothers.

a) GENERAL LEDGER – MAURICE BROTHERS

Cash Account

Date Particulars Ref Amount Date Particulars Ref Amount

03/08/21 Bank 2800 15/08/21 Office Fixtures 110

19/08/21 Toyota Co. 8700

31/08/21 Balance c/d 6440 25/08/21 Bank 430

9240 9240

Bank Account

Date Particulars Ref Amount Date Particulars Ref Amount

03/08/21 Cash 2800

01/08/21 Capital 36800 04/08/21 Van 6200

25/08/21 Cash 430 05/08/21 Office Fixtures 1000

02/08/21 Loan Payable 12400 28/08/21 Office Fixtures 750

31/08/21 Balance c/d 38880

49630 49630

Van Account

Date Particulars Ref Amount Date Particulars Ref Amount

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

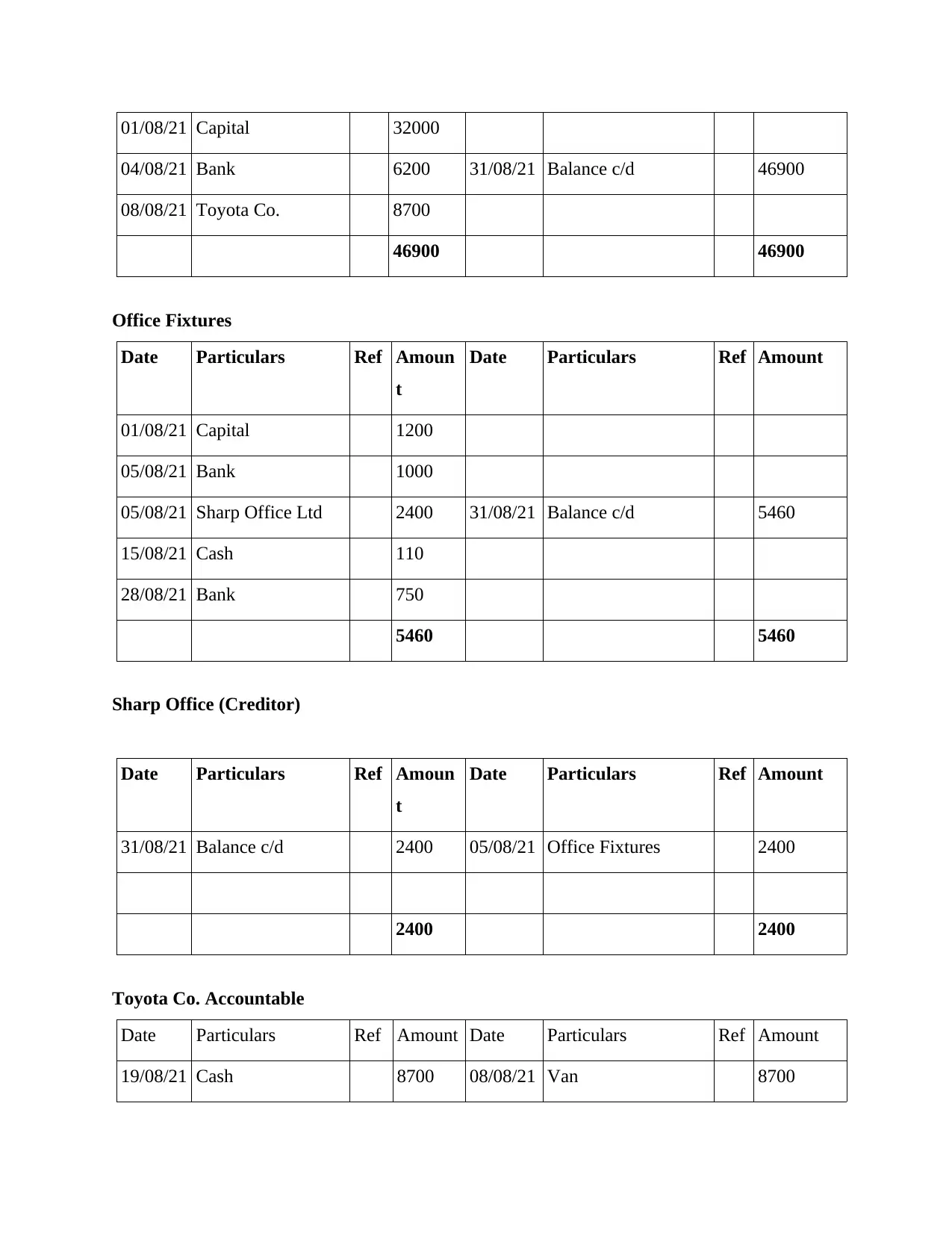

01/08/21 Capital 32000

04/08/21 Bank 6200 31/08/21 Balance c/d 46900

08/08/21 Toyota Co. 8700

46900 46900

Office Fixtures

Date Particulars Ref Amoun

t

Date Particulars Ref Amount

01/08/21 Capital 1200

05/08/21 Bank 1000

05/08/21 Sharp Office Ltd 2400 31/08/21 Balance c/d 5460

15/08/21 Cash 110

28/08/21 Bank 750

5460 5460

Sharp Office (Creditor)

Date Particulars Ref Amoun

t

Date Particulars Ref Amount

31/08/21 Balance c/d 2400 05/08/21 Office Fixtures 2400

2400 2400

Toyota Co. Accountable

Date Particulars Ref Amount Date Particulars Ref Amount

19/08/21 Cash 8700 08/08/21 Van 8700

04/08/21 Bank 6200 31/08/21 Balance c/d 46900

08/08/21 Toyota Co. 8700

46900 46900

Office Fixtures

Date Particulars Ref Amoun

t

Date Particulars Ref Amount

01/08/21 Capital 1200

05/08/21 Bank 1000

05/08/21 Sharp Office Ltd 2400 31/08/21 Balance c/d 5460

15/08/21 Cash 110

28/08/21 Bank 750

5460 5460

Sharp Office (Creditor)

Date Particulars Ref Amoun

t

Date Particulars Ref Amount

31/08/21 Balance c/d 2400 05/08/21 Office Fixtures 2400

2400 2400

Toyota Co. Accountable

Date Particulars Ref Amount Date Particulars Ref Amount

19/08/21 Cash 8700 08/08/21 Van 8700

8700 8700

Loan Payable Account

Date Particulars Ref Amount Date Particulars Ref Amount

31/08/21 Balance c/d 12400 02/08/21 Bank 12400

12400 12400

Capital Account

Date Particulars Ref Amount Date Particulars Ref Amount

31/08/21 Office Fixtures 1200

31/08/21 Van 32000 31/08/21 Balance c/d 70000

31/08/21 Bank 36800

70000 70000

b) TRIAL BALANCE

TRIAL BALANCE

Maurice & Brothers

Debit Credit

Bank 38880

Cash 6440

Van 46900

Office Fixtures 5460

Sharp Office Ltd (Creditor) 2400

Loan Payable 12400

Loan Payable Account

Date Particulars Ref Amount Date Particulars Ref Amount

31/08/21 Balance c/d 12400 02/08/21 Bank 12400

12400 12400

Capital Account

Date Particulars Ref Amount Date Particulars Ref Amount

31/08/21 Office Fixtures 1200

31/08/21 Van 32000 31/08/21 Balance c/d 70000

31/08/21 Bank 36800

70000 70000

b) TRIAL BALANCE

TRIAL BALANCE

Maurice & Brothers

Debit Credit

Bank 38880

Cash 6440

Van 46900

Office Fixtures 5460

Sharp Office Ltd (Creditor) 2400

Loan Payable 12400

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Capital 70000

TOTAL 91240 91240

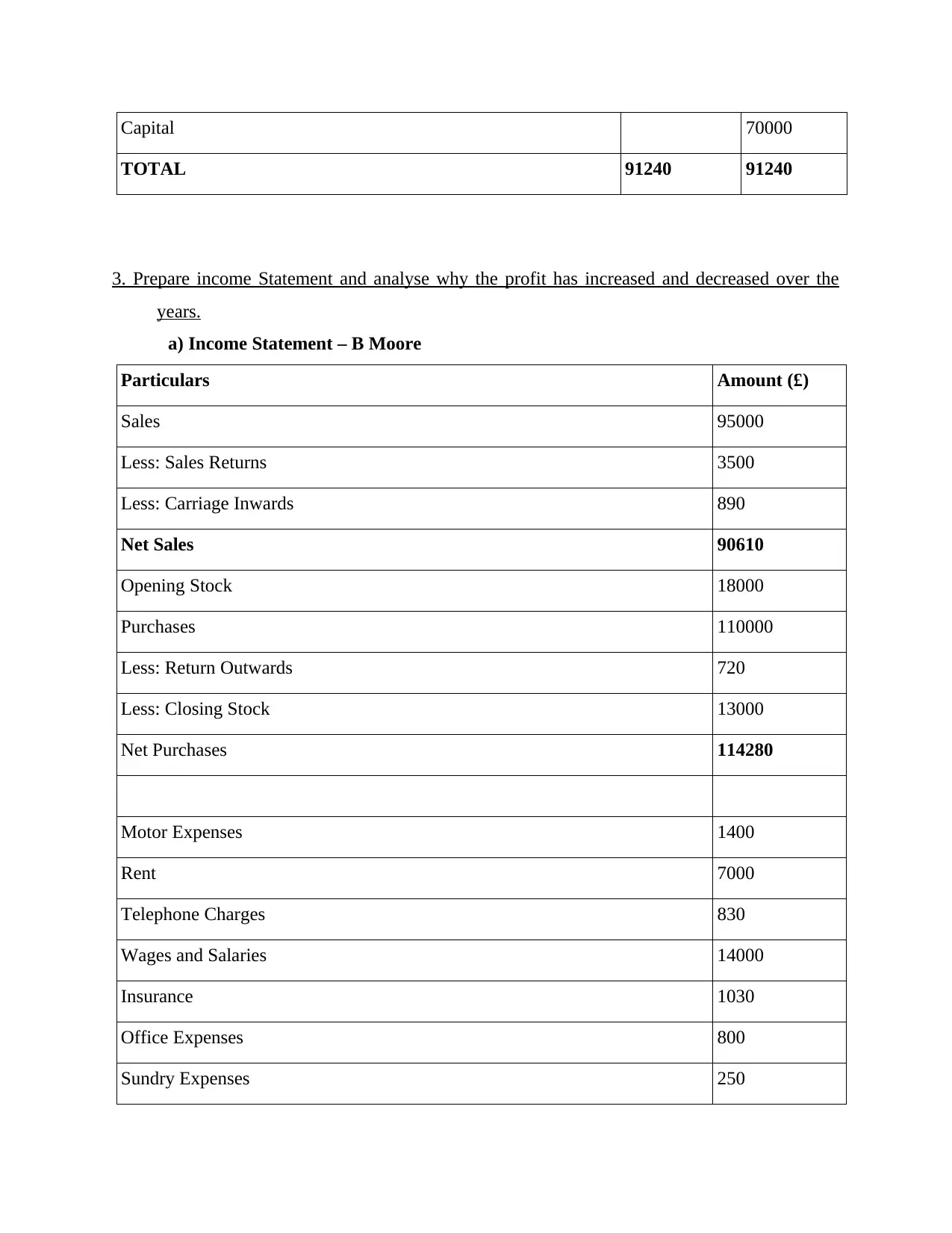

3. Prepare income Statement and analyse why the profit has increased and decreased over the

years.

a) Income Statement – B Moore

Particulars Amount (£)

Sales 95000

Less: Sales Returns 3500

Less: Carriage Inwards 890

Net Sales 90610

Opening Stock 18000

Purchases 110000

Less: Return Outwards 720

Less: Closing Stock 13000

Net Purchases 114280

Motor Expenses 1400

Rent 7000

Telephone Charges 830

Wages and Salaries 14000

Insurance 1030

Office Expenses 800

Sundry Expenses 250

TOTAL 91240 91240

3. Prepare income Statement and analyse why the profit has increased and decreased over the

years.

a) Income Statement – B Moore

Particulars Amount (£)

Sales 95000

Less: Sales Returns 3500

Less: Carriage Inwards 890

Net Sales 90610

Opening Stock 18000

Purchases 110000

Less: Return Outwards 720

Less: Closing Stock 13000

Net Purchases 114280

Motor Expenses 1400

Rent 7000

Telephone Charges 830

Wages and Salaries 14000

Insurance 1030

Office Expenses 800

Sundry Expenses 250

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Operating Expenses 25310

TOTALS -48980

b) Why the profit has decreased and increased over the years and what will be the estimate of

profit in 2022.

For various organization, the first quarter of the year 2020 is one of the very difficult

scenario in many recent years. There are many companies which made the steady progress in its

early 2020 but the pandemic of COVID-19 has halted the progress. In different regions of the

world from March mid, there were many interruptions in the regular operations in the business

and somewhere complete shutdown of many departments in stores. In accordance with the

income statement, it can be analyzed that many businesses have suffered huge losses which

indicates that the expenses of the company has exceeded the income of it. The sales of the

company is being making very less money which cannot even cover the expenses of it as the

demand for the products has been decreased. There are different consequences which ranges

from the small effect like the closure of business to many large impact like the changes in the

strategy of the company. So it is very essential for the business owners to have the understanding

of the financial implications as well as the impact of company (Szudoczky and Karolyi, 2020).

Assessment 2

Part A

Journal books :

It is an act of recording and managing business transaction of either economic or non

economic nature. It depicts companies debit or credit balances which further helps to make

future strategies of business concern. There are five type of entries recorded in the books of

accounts such as opening entries, transfer entries, closing entries, adjusting entries and various

others. These transactions are recorded as per accounting principles and conventions in books of

accounts (Van Greuning and Bratanovic, 2020).

TOTALS -48980

b) Why the profit has decreased and increased over the years and what will be the estimate of

profit in 2022.

For various organization, the first quarter of the year 2020 is one of the very difficult

scenario in many recent years. There are many companies which made the steady progress in its

early 2020 but the pandemic of COVID-19 has halted the progress. In different regions of the

world from March mid, there were many interruptions in the regular operations in the business

and somewhere complete shutdown of many departments in stores. In accordance with the

income statement, it can be analyzed that many businesses have suffered huge losses which

indicates that the expenses of the company has exceeded the income of it. The sales of the

company is being making very less money which cannot even cover the expenses of it as the

demand for the products has been decreased. There are different consequences which ranges

from the small effect like the closure of business to many large impact like the changes in the

strategy of the company. So it is very essential for the business owners to have the understanding

of the financial implications as well as the impact of company (Szudoczky and Karolyi, 2020).

Assessment 2

Part A

Journal books :

It is an act of recording and managing business transaction of either economic or non

economic nature. It depicts companies debit or credit balances which further helps to make

future strategies of business concern. There are five type of entries recorded in the books of

accounts such as opening entries, transfer entries, closing entries, adjusting entries and various

others. These transactions are recorded as per accounting principles and conventions in books of

accounts (Van Greuning and Bratanovic, 2020).

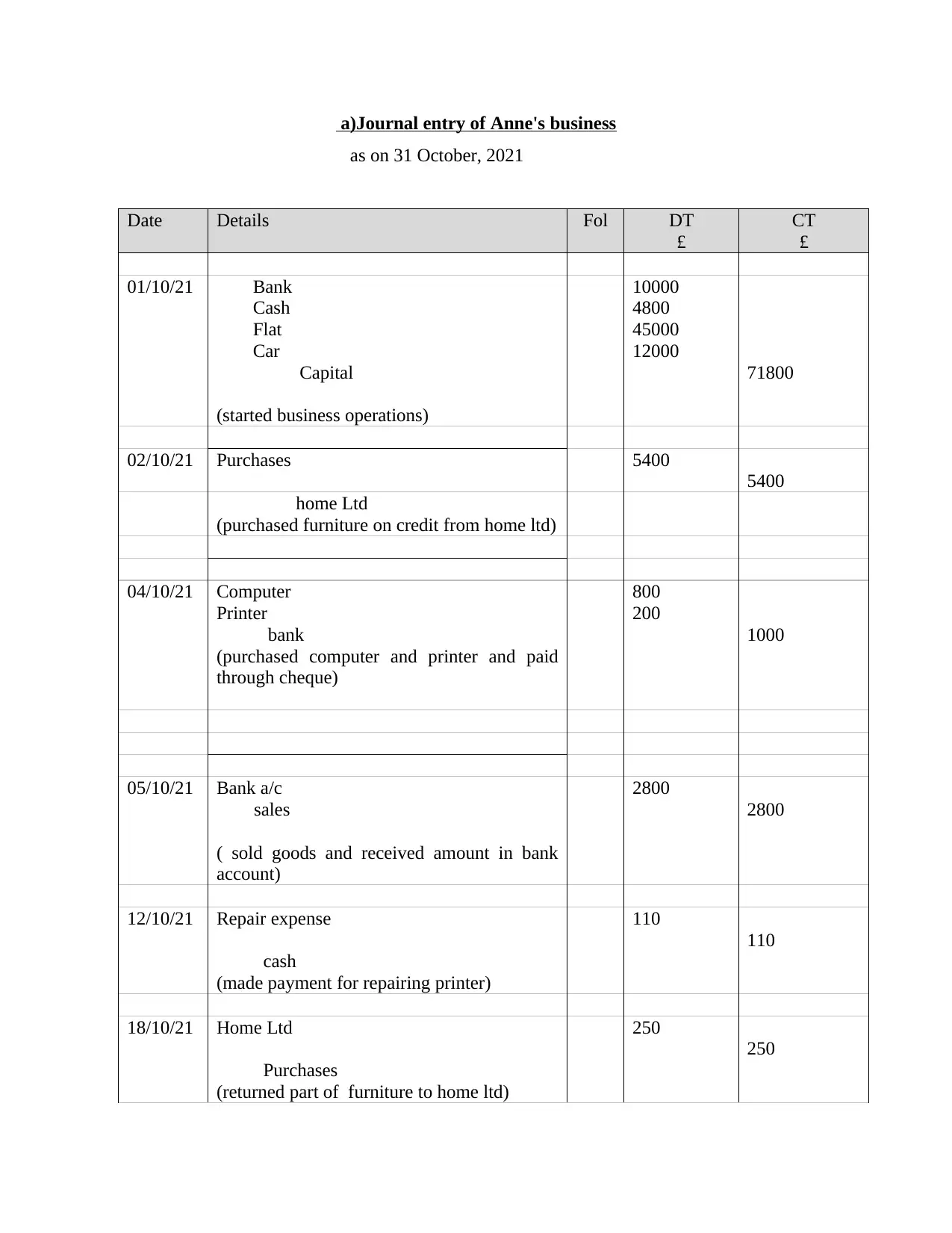

a)Journal entry of Anne's business

as on 31 October, 2021

Date Details Fol DT

£

CT

£

01/10/21 Bank

Cash

Flat

Car

Capital

(started business operations)

10000

4800

45000

12000

71800

02/10/21 Purchases 5400

5400

home Ltd

(purchased furniture on credit from home ltd)

04/10/21 Computer

Printer

bank

(purchased computer and printer and paid

through cheque)

800

200

1000

05/10/21 Bank a/c

sales

( sold goods and received amount in bank

account)

2800

2800

12/10/21 Repair expense

cash

(made payment for repairing printer)

110

110

18/10/21 Home Ltd

Purchases

(returned part of furniture to home ltd)

250

250

as on 31 October, 2021

Date Details Fol DT

£

CT

£

01/10/21 Bank

Cash

Flat

Car

Capital

(started business operations)

10000

4800

45000

12000

71800

02/10/21 Purchases 5400

5400

home Ltd

(purchased furniture on credit from home ltd)

04/10/21 Computer

Printer

bank

(purchased computer and printer and paid

through cheque)

800

200

1000

05/10/21 Bank a/c

sales

( sold goods and received amount in bank

account)

2800

2800

12/10/21 Repair expense

cash

(made payment for repairing printer)

110

110

18/10/21 Home Ltd

Purchases

(returned part of furniture to home ltd)

250

250

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 26

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.