Recording Business Transactions: Assessment 1, BA3LC92O, LSST

VerifiedAdded on 2023/01/05

|8

|1624

|99

Homework Assignment

AI Summary

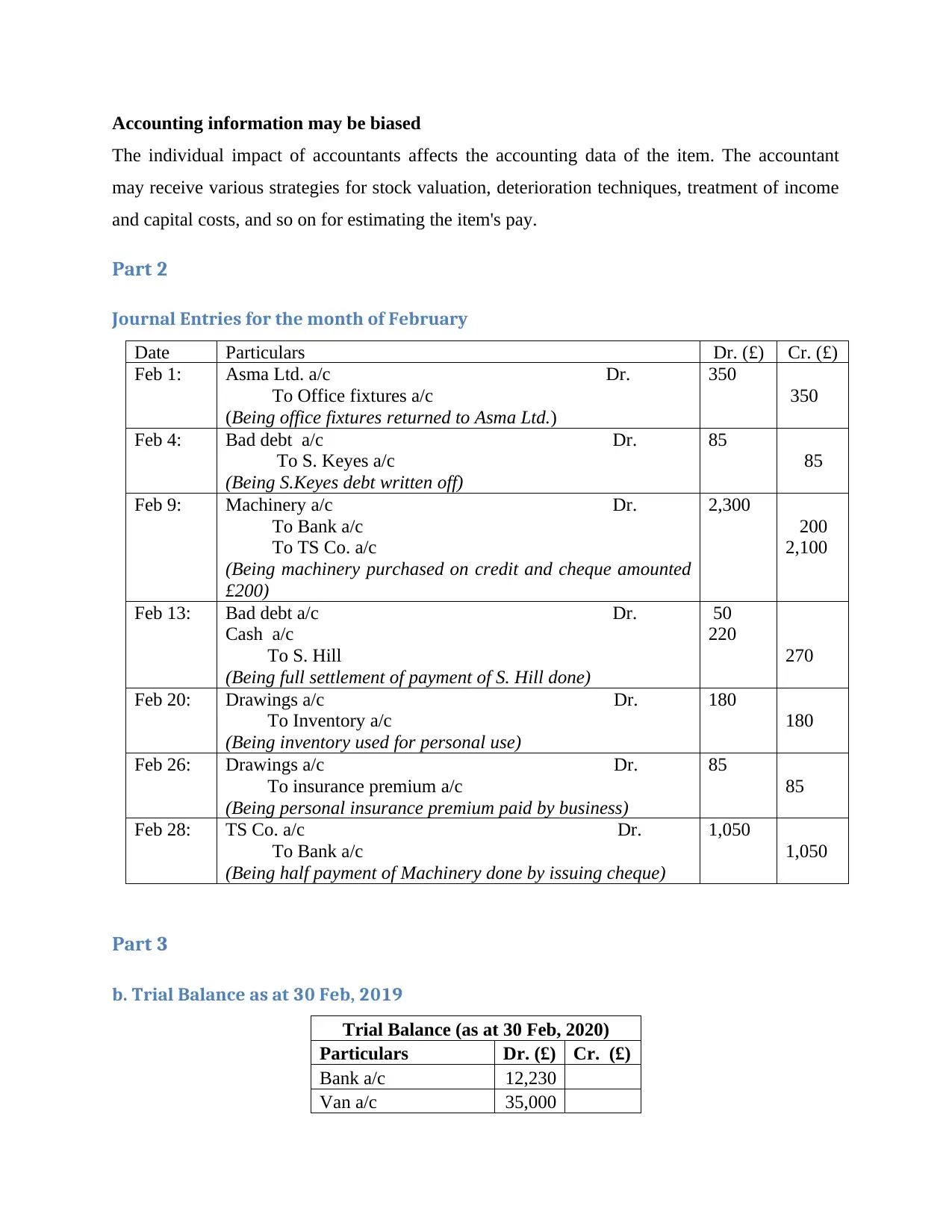

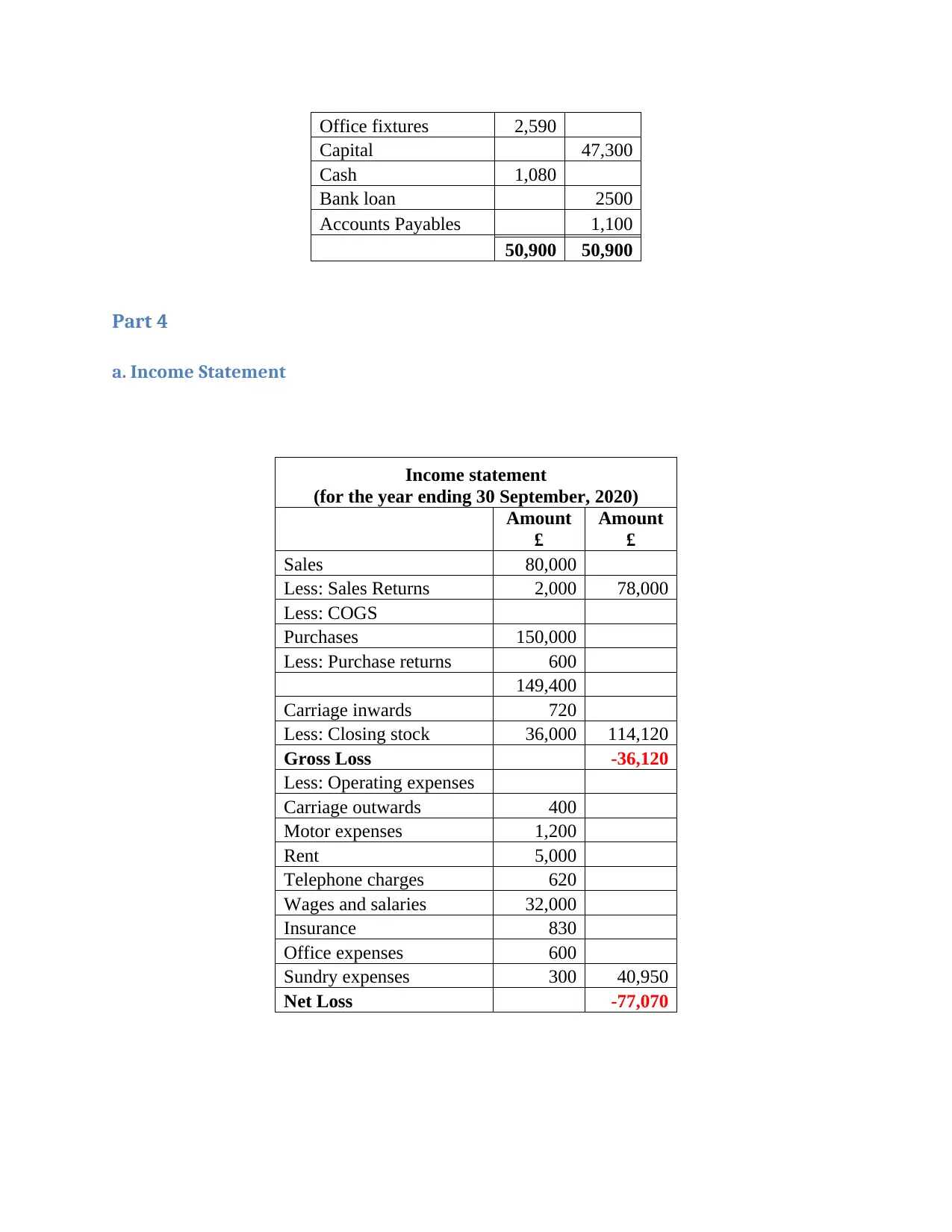

This document presents a solution to an assignment on recording business transactions, focusing on key aspects of financial accounting. The assignment begins with the identification of decision-makers within a business context and explores the advantages and disadvantages of various profit business structures. Part 2 provides detailed journal entries for the month of February, illustrating the recording of various transactions. Part 3 includes a trial balance as of February 30, 2019, which summarizes the debit and credit balances of different accounts. Part 4 focuses on the preparation of an income statement for the year ending September 30, 2020, and analyzes the potential impact of the COVID-19 pandemic on the company's financial statement items, considering factors such as income, expenses, and the challenges in accurately determining the pandemic's effects on financial reporting. This assignment provides a comprehensive overview of accounting principles and their application in practical scenarios.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.