Financial Accounting: Recording Business Transactions and Analysis

VerifiedAdded on 2023/01/03

|11

|2196

|29

Report

AI Summary

This report delves into the crucial process of recording business transactions, beginning with an introduction to double-entry bookkeeping. The assessment covers various aspects of financial accounting, including the need for accounting information for decision-makers, exploring the advantages and disadvantages of different business structures for recording financial data. The report provides detailed journal entries for setting up a new business, along with ledger accounts and trial balance preparation. Furthermore, it presents an income statement analysis for a specific company, Airman Co., and examines the impact of the COVID-19 pandemic on the company's financial statements. The report concludes by summarizing the key takeaways and providing references to relevant sources. It showcases the practical application of accounting principles in real-world business scenarios, emphasizing the importance of accurate financial reporting and analysis for informed decision-making.

Recording Business

Transactions

Transactions

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

ASSESSMENT 1.............................................................................................................................1

PART 1............................................................................................................................................1

Need of the accounting information for the decision makers......................................................1

Advantages and disadvantages of the business structure for recording the accounting

information...................................................................................................................................2

PART 2............................................................................................................................................3

Journal entries for the David wise for setting up new business ..................................................3

PART 3............................................................................................................................................4

Prepare of the ledger accounts and trial balance for the Pearce & sons......................................4

PART 4............................................................................................................................................6

Income statement for Airman co.:...............................................................................................6

Impact of Covid-19 on the company financial statements...........................................................7

CONCLUSION................................................................................................................................7

REFERENCES ...............................................................................................................................8

INTRODUCTION...........................................................................................................................1

ASSESSMENT 1.............................................................................................................................1

PART 1............................................................................................................................................1

Need of the accounting information for the decision makers......................................................1

Advantages and disadvantages of the business structure for recording the accounting

information...................................................................................................................................2

PART 2............................................................................................................................................3

Journal entries for the David wise for setting up new business ..................................................3

PART 3............................................................................................................................................4

Prepare of the ledger accounts and trial balance for the Pearce & sons......................................4

PART 4............................................................................................................................................6

Income statement for Airman co.:...............................................................................................6

Impact of Covid-19 on the company financial statements...........................................................7

CONCLUSION................................................................................................................................7

REFERENCES ...............................................................................................................................8

INTRODUCTION

Recording business transaction is the double entry process in which all the steps are

included from recording to evaluation. It helps the business in in recording the transaction in the

debit and credit side which is done in the journal. In the financial statements there is the

summary of all the transactions which is recorded in the profit and loss. It means the economic

event that is recorded in the accounting system of the organization. All these transaction

measurable in the money (Aragon, 2017) . In this assessment, business transaction is recorded in

the form of journal,ledger and balance sheet which is based on the companies business records to

know about its financial growth and position. In this there is the need of the accounting

information for the decision makers and also the advantage and disadvantage of the business

structure.

ASSESSMENT 1

PART 1

Need of the accounting information for the decision makers

Accounting information play a important role in for the continuous running of the

business because it helps in tracking the income and expenditure, provide important information

to the investor and also financial information to the government. Financial accounting helps in to

keep track of all business transactions in the book of accounts. It involves recording,

summarizing, reporting of all economic activity from the business functioning over a specific

period of time (Kim, Rhee and Lee, 2016). There are many standards and policies are made for

the company in the UK which is follow by the generally accepted accounting principle. Financial

accounting helps the decision maker in making decisions in following ways.

Through this information investor can easily do the analysis of the company financial

statement and also comparison between the financial health of the trade securities.

It also help creditors in finding out the liquidity, solvency and and efficiency of the

business ate the particular time period.

It also helps to the manager in effective use of the resources for taking the business

decisions effectively.

1

Recording business transaction is the double entry process in which all the steps are

included from recording to evaluation. It helps the business in in recording the transaction in the

debit and credit side which is done in the journal. In the financial statements there is the

summary of all the transactions which is recorded in the profit and loss. It means the economic

event that is recorded in the accounting system of the organization. All these transaction

measurable in the money (Aragon, 2017) . In this assessment, business transaction is recorded in

the form of journal,ledger and balance sheet which is based on the companies business records to

know about its financial growth and position. In this there is the need of the accounting

information for the decision makers and also the advantage and disadvantage of the business

structure.

ASSESSMENT 1

PART 1

Need of the accounting information for the decision makers

Accounting information play a important role in for the continuous running of the

business because it helps in tracking the income and expenditure, provide important information

to the investor and also financial information to the government. Financial accounting helps in to

keep track of all business transactions in the book of accounts. It involves recording,

summarizing, reporting of all economic activity from the business functioning over a specific

period of time (Kim, Rhee and Lee, 2016). There are many standards and policies are made for

the company in the UK which is follow by the generally accepted accounting principle. Financial

accounting helps the decision maker in making decisions in following ways.

Through this information investor can easily do the analysis of the company financial

statement and also comparison between the financial health of the trade securities.

It also help creditors in finding out the liquidity, solvency and and efficiency of the

business ate the particular time period.

It also helps to the manager in effective use of the resources for taking the business

decisions effectively.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

It also help the management in recording the financial transaction for the good position of

the company such as Profit and loss, balance sheet and ratio analysis.

It helps the decision maker in making the planning in regards to the sales, development

and also help in determining the inventory in the stock.

Accounting information also help in making budget because it is very necessary for

making the estimation of revenue and expenses at the workplace.

It also help the internal user in making investment credit and other decisions for the

employees, investors and creditors.

It also help the finance manager in take decisions for controlling the operating activities

and financing activities (Klenk, Onyenokwe and Perez, 2020).

Advantages and disadvantages of the business structure for recording the accounting information

Accounting: It is a process of recording or financing the transaction for the pertinent of

the business. It includes summarize, and reporting the transaction for the accurate decision. Some

examples of the accounting are planning of income tax, financial planning, auditing.

Advantages

Maintenance of business records: It helps in recording all the transaction related to the

finance in a systematic manner in books. Every transaction related to the finance is not

easy to remember due to the size and complexities of the organisation.

Preparation of financial accounts: In financial statement all the accounts Balance

Sheet, P&L are prepared in a proper manner. The transaction related to the finance are

also recorded correctly so that the results are accurate enough.

Comparison of results: It helps in comparing the results of two years so that the accurate

data can be analysed. It helps in recording the transaction according to the policies.

Decision making: proper recording of the data make it easier for the management to take

the decisions in a proper manner and helps the management to plan its future activities of

the various department and prepare budgets.

Disadvantages:

Express accounting information in terms of money : transaction that are non-financial

are not recorded and do not have any effect in the books of accounts. Transactions related

to the finance are measurable in a proper manner because they are recorded in monetary

value.

2

the company such as Profit and loss, balance sheet and ratio analysis.

It helps the decision maker in making the planning in regards to the sales, development

and also help in determining the inventory in the stock.

Accounting information also help in making budget because it is very necessary for

making the estimation of revenue and expenses at the workplace.

It also help the internal user in making investment credit and other decisions for the

employees, investors and creditors.

It also help the finance manager in take decisions for controlling the operating activities

and financing activities (Klenk, Onyenokwe and Perez, 2020).

Advantages and disadvantages of the business structure for recording the accounting information

Accounting: It is a process of recording or financing the transaction for the pertinent of

the business. It includes summarize, and reporting the transaction for the accurate decision. Some

examples of the accounting are planning of income tax, financial planning, auditing.

Advantages

Maintenance of business records: It helps in recording all the transaction related to the

finance in a systematic manner in books. Every transaction related to the finance is not

easy to remember due to the size and complexities of the organisation.

Preparation of financial accounts: In financial statement all the accounts Balance

Sheet, P&L are prepared in a proper manner. The transaction related to the finance are

also recorded correctly so that the results are accurate enough.

Comparison of results: It helps in comparing the results of two years so that the accurate

data can be analysed. It helps in recording the transaction according to the policies.

Decision making: proper recording of the data make it easier for the management to take

the decisions in a proper manner and helps the management to plan its future activities of

the various department and prepare budgets.

Disadvantages:

Express accounting information in terms of money : transaction that are non-financial

are not recorded and do not have any effect in the books of accounts. Transactions related

to the finance are measurable in a proper manner because they are recorded in monetary

value.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Information based on estimates: The data maintained in books of accounts are

recorded on the basis of the estimates but sometimes the data recorded are also inaccurate

that makes the wrong decision (Peters, D 2016).

Biased information: It helps in influencing the entity of accounting information. For

measure of entity different accounting methods are adopted like inventory valuation,

depreciation, treatment of capital and the revenue expenses.

Recording of the fixed assets at the original cost: In accounting there is a difference

between the fixed cost and the current cost of the fixed asset due to change in time and

technology.

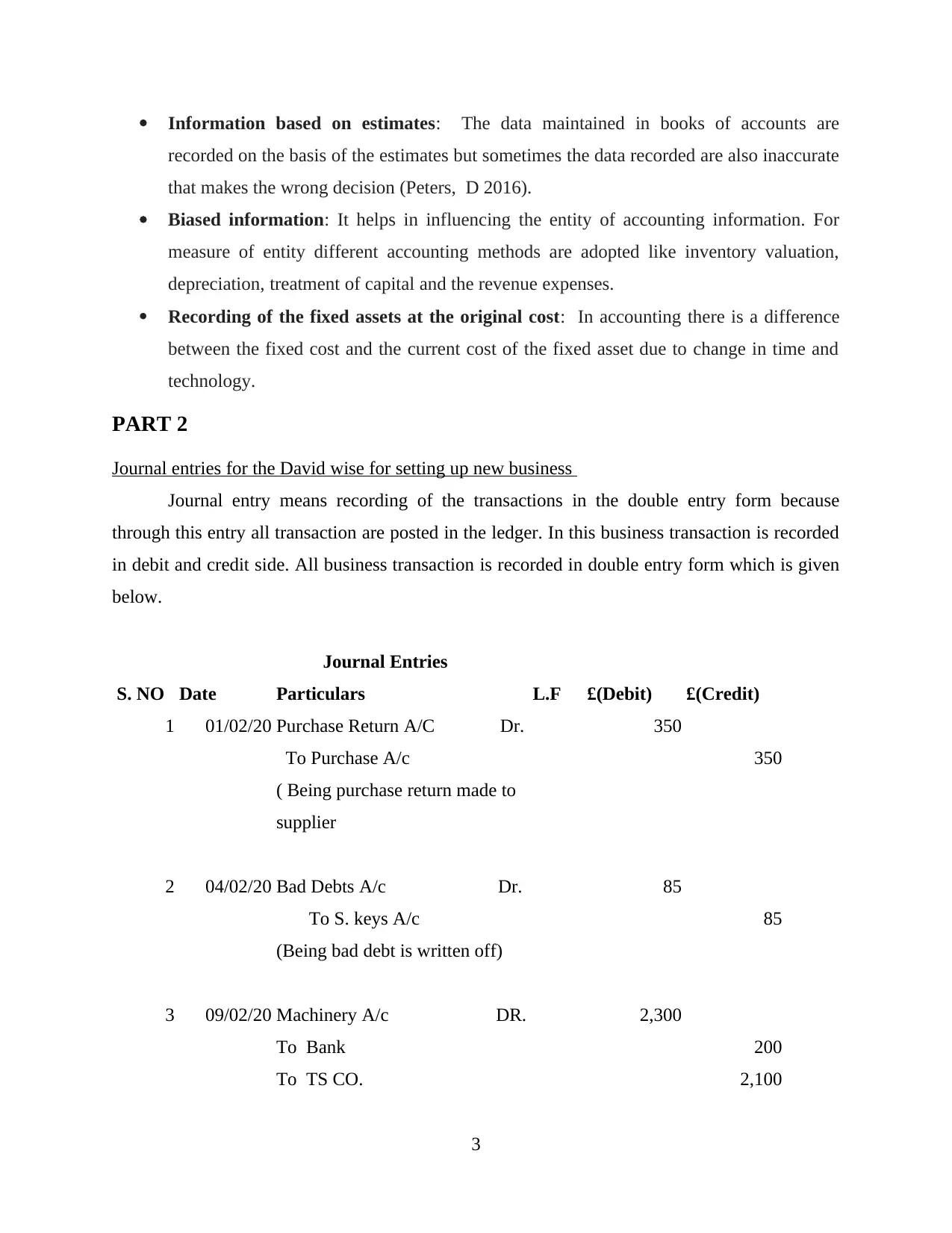

PART 2

Journal entries for the David wise for setting up new business

Journal entry means recording of the transactions in the double entry form because

through this entry all transaction are posted in the ledger. In this business transaction is recorded

in debit and credit side. All business transaction is recorded in double entry form which is given

below.

Journal Entries

S. NO Date Particulars L.F £(Debit) £(Credit)

1 01/02/20 Purchase Return A/C Dr. 350

To Purchase A/c 350

( Being purchase return made to

supplier

2 04/02/20 Bad Debts A/c Dr. 85

To S. keys A/c 85

(Being bad debt is written off)

3 09/02/20 Machinery A/c DR. 2,300

To Bank 200

To TS CO. 2,100

3

recorded on the basis of the estimates but sometimes the data recorded are also inaccurate

that makes the wrong decision (Peters, D 2016).

Biased information: It helps in influencing the entity of accounting information. For

measure of entity different accounting methods are adopted like inventory valuation,

depreciation, treatment of capital and the revenue expenses.

Recording of the fixed assets at the original cost: In accounting there is a difference

between the fixed cost and the current cost of the fixed asset due to change in time and

technology.

PART 2

Journal entries for the David wise for setting up new business

Journal entry means recording of the transactions in the double entry form because

through this entry all transaction are posted in the ledger. In this business transaction is recorded

in debit and credit side. All business transaction is recorded in double entry form which is given

below.

Journal Entries

S. NO Date Particulars L.F £(Debit) £(Credit)

1 01/02/20 Purchase Return A/C Dr. 350

To Purchase A/c 350

( Being purchase return made to

supplier

2 04/02/20 Bad Debts A/c Dr. 85

To S. keys A/c 85

(Being bad debt is written off)

3 09/02/20 Machinery A/c DR. 2,300

To Bank 200

To TS CO. 2,100

3

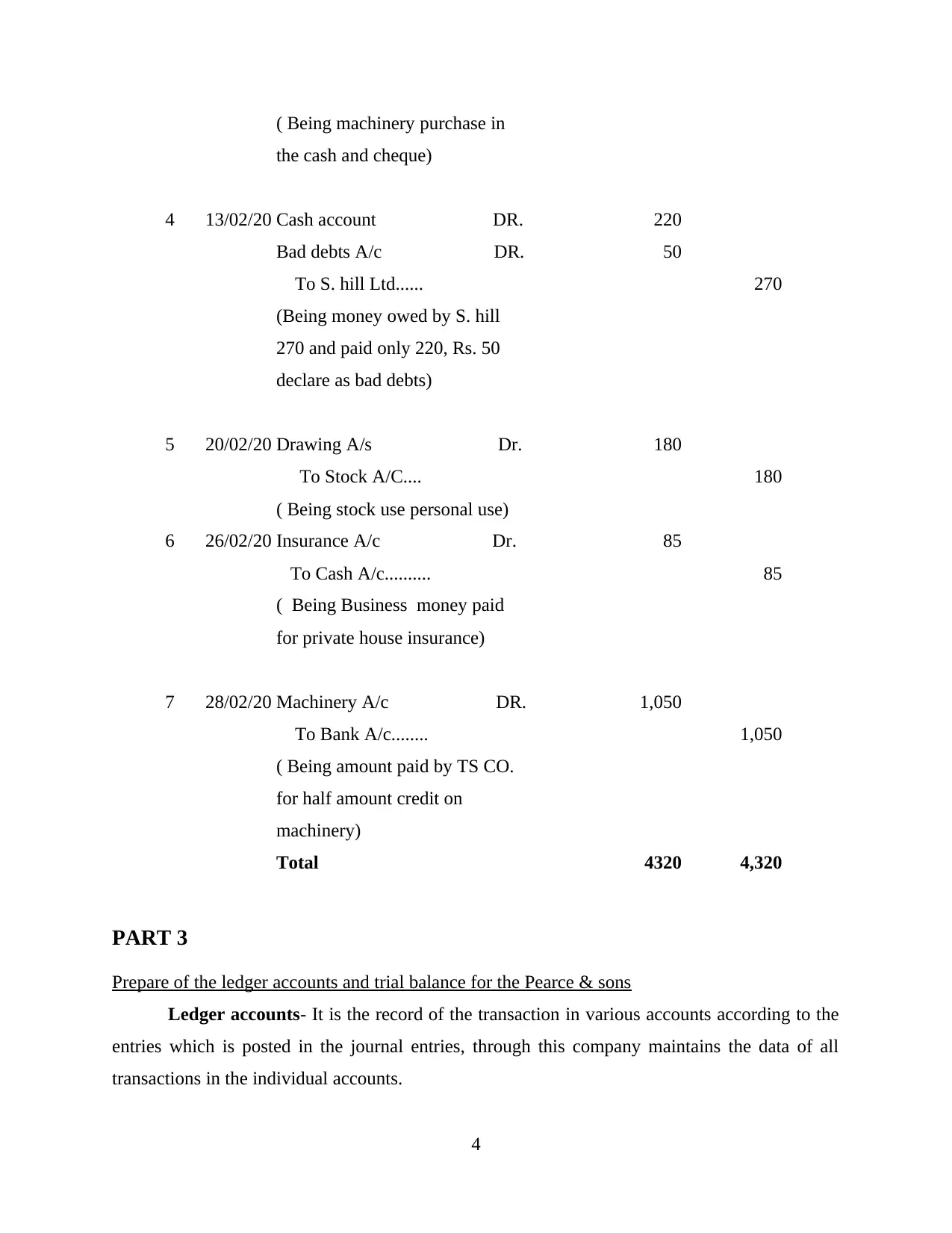

( Being machinery purchase in

the cash and cheque)

4 13/02/20 Cash account DR. 220

Bad debts A/c DR. 50

To S. hill Ltd...... 270

(Being money owed by S. hill

270 and paid only 220, Rs. 50

declare as bad debts)

5 20/02/20 Drawing A/s Dr. 180

To Stock A/C.... 180

( Being stock use personal use)

6 26/02/20 Insurance A/c Dr. 85

To Cash A/c.......... 85

( Being Business money paid

for private house insurance)

7 28/02/20 Machinery A/c DR. 1,050

To Bank A/c........ 1,050

( Being amount paid by TS CO.

for half amount credit on

machinery)

Total 4320 4,320

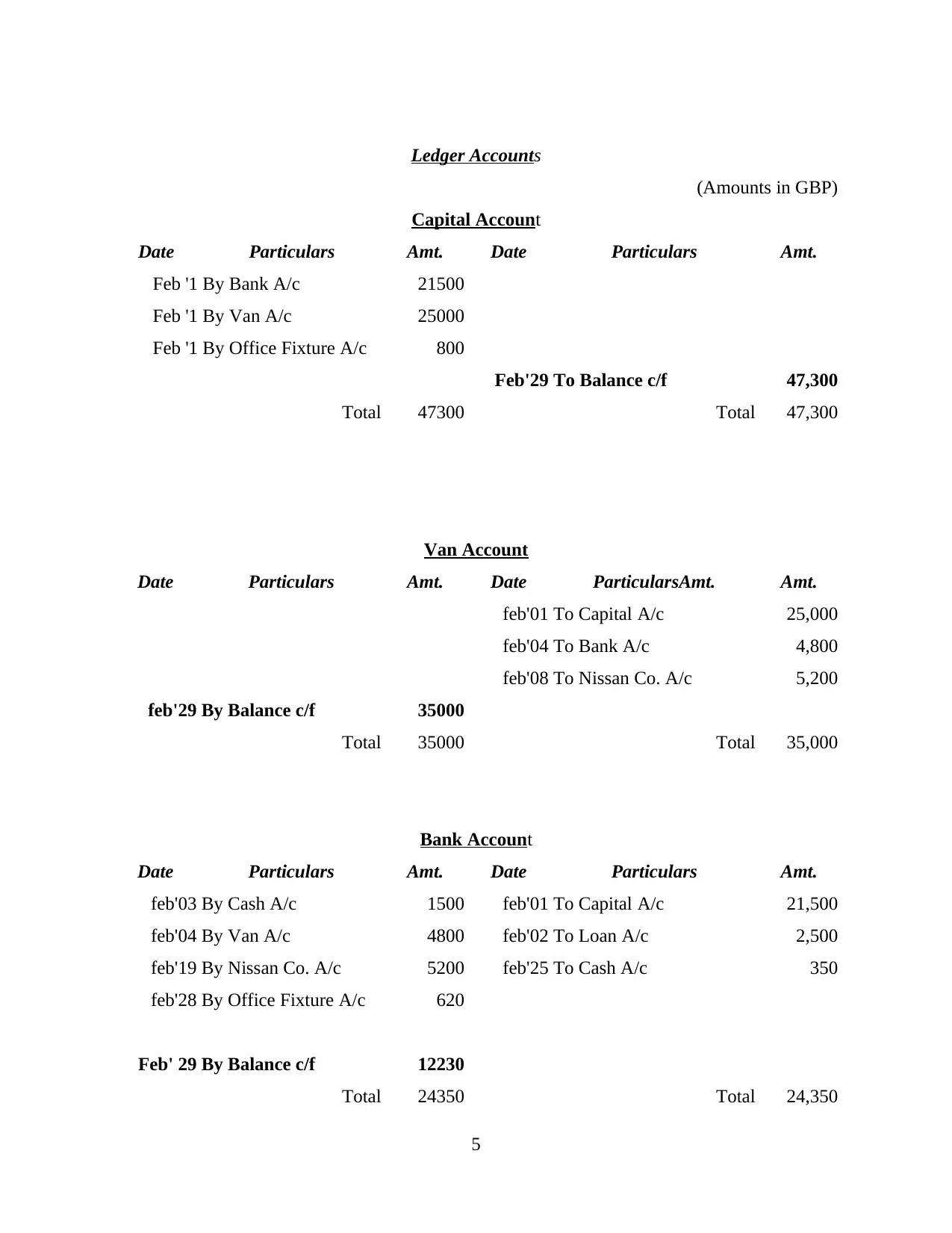

PART 3

Prepare of the ledger accounts and trial balance for the Pearce & sons

Ledger accounts- It is the record of the transaction in various accounts according to the

entries which is posted in the journal entries, through this company maintains the data of all

transactions in the individual accounts.

4

the cash and cheque)

4 13/02/20 Cash account DR. 220

Bad debts A/c DR. 50

To S. hill Ltd...... 270

(Being money owed by S. hill

270 and paid only 220, Rs. 50

declare as bad debts)

5 20/02/20 Drawing A/s Dr. 180

To Stock A/C.... 180

( Being stock use personal use)

6 26/02/20 Insurance A/c Dr. 85

To Cash A/c.......... 85

( Being Business money paid

for private house insurance)

7 28/02/20 Machinery A/c DR. 1,050

To Bank A/c........ 1,050

( Being amount paid by TS CO.

for half amount credit on

machinery)

Total 4320 4,320

PART 3

Prepare of the ledger accounts and trial balance for the Pearce & sons

Ledger accounts- It is the record of the transaction in various accounts according to the

entries which is posted in the journal entries, through this company maintains the data of all

transactions in the individual accounts.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Ledger Accounts

(Amounts in GBP)

Capital Account

Date Particulars Amt. Date Particulars Amt.

Feb '1 By Bank A/c 21500

Feb '1 By Van A/c 25000

Feb '1 By Office Fixture A/c 800

Feb'29 To Balance c/f 47,300

Total 47300 Total 47,300

Van Account

Date Particulars Amt. Date ParticularsAmt. Amt.

feb'01 To Capital A/c 25,000

feb'04 To Bank A/c 4,800

feb'08 To Nissan Co. A/c 5,200

feb'29 By Balance c/f 35000

Total 35000 Total 35,000

Bank Account

Date Particulars Amt. Date Particulars Amt.

feb'03 By Cash A/c 1500 feb'01 To Capital A/c 21,500

feb'04 By Van A/c 4800 feb'02 To Loan A/c 2,500

feb'19 By Nissan Co. A/c 5200 feb'25 To Cash A/c 350

feb'28 By Office Fixture A/c 620

Feb' 29 By Balance c/f 12230

Total 24350 Total 24,350

5

(Amounts in GBP)

Capital Account

Date Particulars Amt. Date Particulars Amt.

Feb '1 By Bank A/c 21500

Feb '1 By Van A/c 25000

Feb '1 By Office Fixture A/c 800

Feb'29 To Balance c/f 47,300

Total 47300 Total 47,300

Van Account

Date Particulars Amt. Date ParticularsAmt. Amt.

feb'01 To Capital A/c 25,000

feb'04 To Bank A/c 4,800

feb'08 To Nissan Co. A/c 5,200

feb'29 By Balance c/f 35000

Total 35000 Total 35,000

Bank Account

Date Particulars Amt. Date Particulars Amt.

feb'03 By Cash A/c 1500 feb'01 To Capital A/c 21,500

feb'04 By Van A/c 4800 feb'02 To Loan A/c 2,500

feb'19 By Nissan Co. A/c 5200 feb'25 To Cash A/c 350

feb'28 By Office Fixture A/c 620

Feb' 29 By Balance c/f 12230

Total 24350 Total 24,350

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

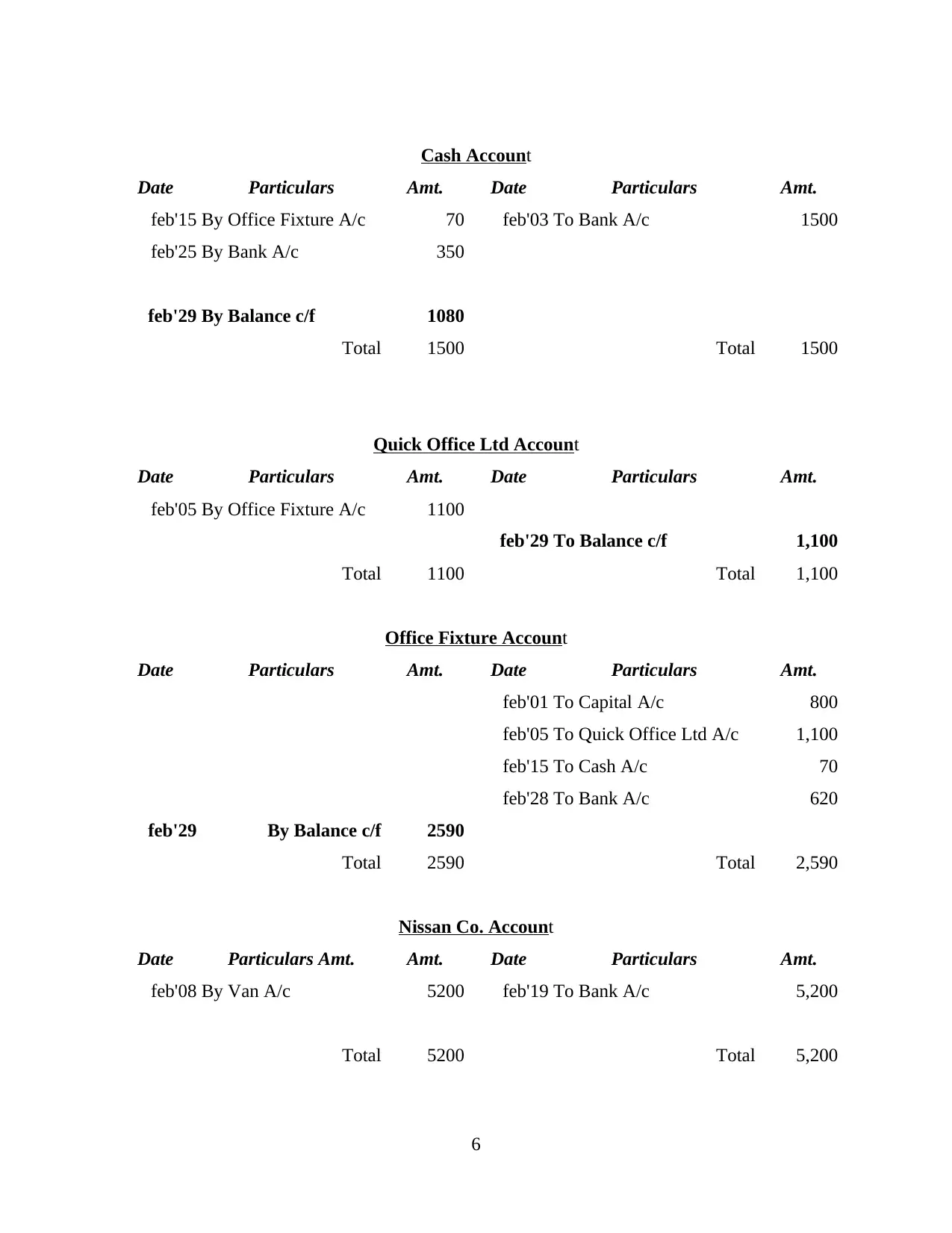

Cash Account

Date Particulars Amt. Date Particulars Amt.

feb'15 By Office Fixture A/c 70 feb'03 To Bank A/c 1500

feb'25 By Bank A/c 350

feb'29 By Balance c/f 1080

Total 1500 Total 1500

Quick Office Ltd Account

Date Particulars Amt. Date Particulars Amt.

feb'05 By Office Fixture A/c 1100

feb'29 To Balance c/f 1,100

Total 1100 Total 1,100

Office Fixture Account

Date Particulars Amt. Date Particulars Amt.

feb'01 To Capital A/c 800

feb'05 To Quick Office Ltd A/c 1,100

feb'15 To Cash A/c 70

feb'28 To Bank A/c 620

feb'29 By Balance c/f 2590

Total 2590 Total 2,590

Nissan Co. Account

Date Particulars Amt. Amt. Date Particulars Amt.

feb'08 By Van A/c 5200 feb'19 To Bank A/c 5,200

Total 5200 Total 5,200

6

Date Particulars Amt. Date Particulars Amt.

feb'15 By Office Fixture A/c 70 feb'03 To Bank A/c 1500

feb'25 By Bank A/c 350

feb'29 By Balance c/f 1080

Total 1500 Total 1500

Quick Office Ltd Account

Date Particulars Amt. Date Particulars Amt.

feb'05 By Office Fixture A/c 1100

feb'29 To Balance c/f 1,100

Total 1100 Total 1,100

Office Fixture Account

Date Particulars Amt. Date Particulars Amt.

feb'01 To Capital A/c 800

feb'05 To Quick Office Ltd A/c 1,100

feb'15 To Cash A/c 70

feb'28 To Bank A/c 620

feb'29 By Balance c/f 2590

Total 2590 Total 2,590

Nissan Co. Account

Date Particulars Amt. Amt. Date Particulars Amt.

feb'08 By Van A/c 5200 feb'19 To Bank A/c 5,200

Total 5200 Total 5,200

6

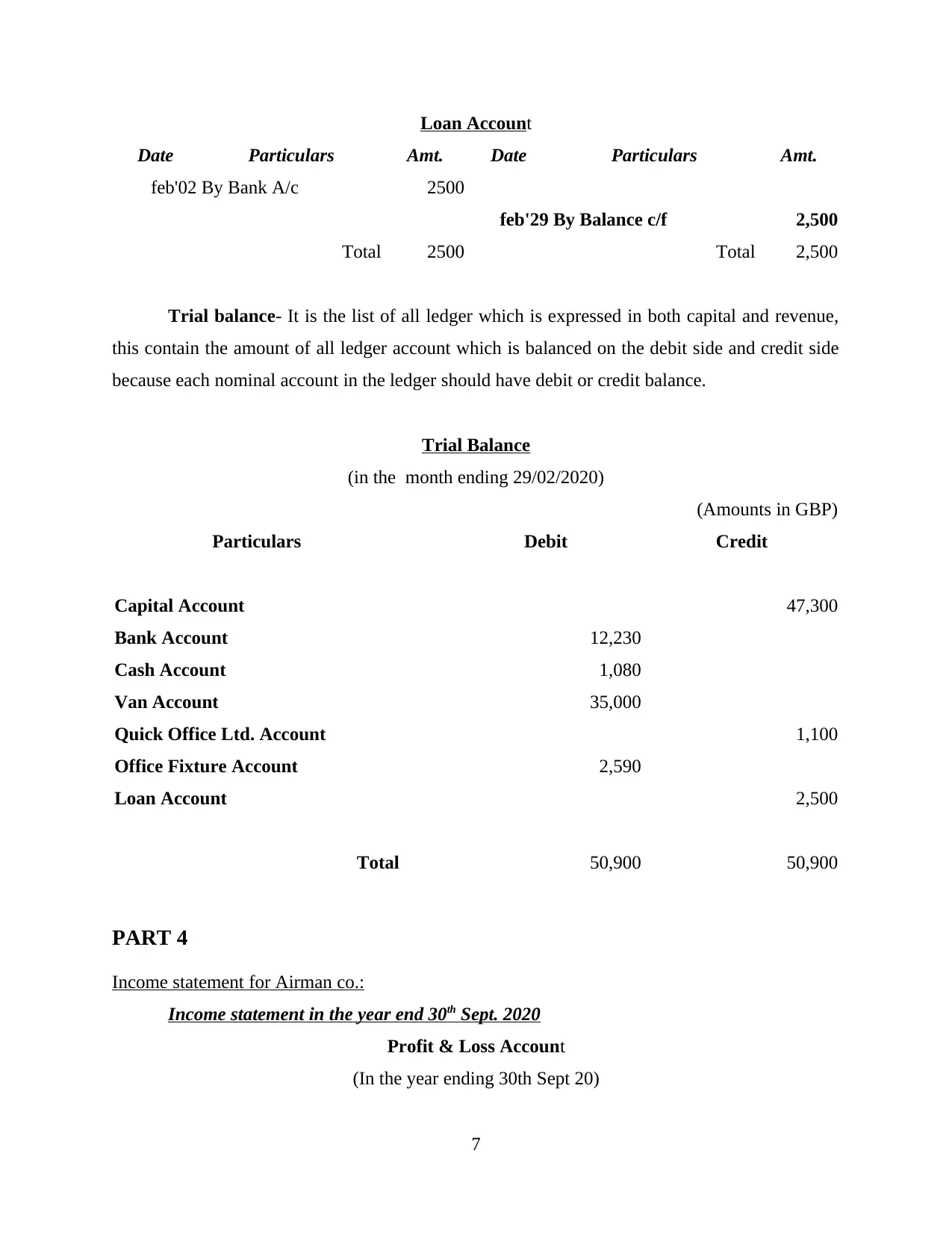

Loan Account

Date Particulars Amt. Date Particulars Amt.

feb'02 By Bank A/c 2500

feb'29 By Balance c/f 2,500

Total 2500 Total 2,500

Trial balance- It is the list of all ledger which is expressed in both capital and revenue,

this contain the amount of all ledger account which is balanced on the debit side and credit side

because each nominal account in the ledger should have debit or credit balance.

Trial Balance

(in the month ending 29/02/2020)

(Amounts in GBP)

Particulars Debit Credit

Capital Account 47,300

Bank Account 12,230

Cash Account 1,080

Van Account 35,000

Quick Office Ltd. Account 1,100

Office Fixture Account 2,590

Loan Account 2,500

Total 50,900 50,900

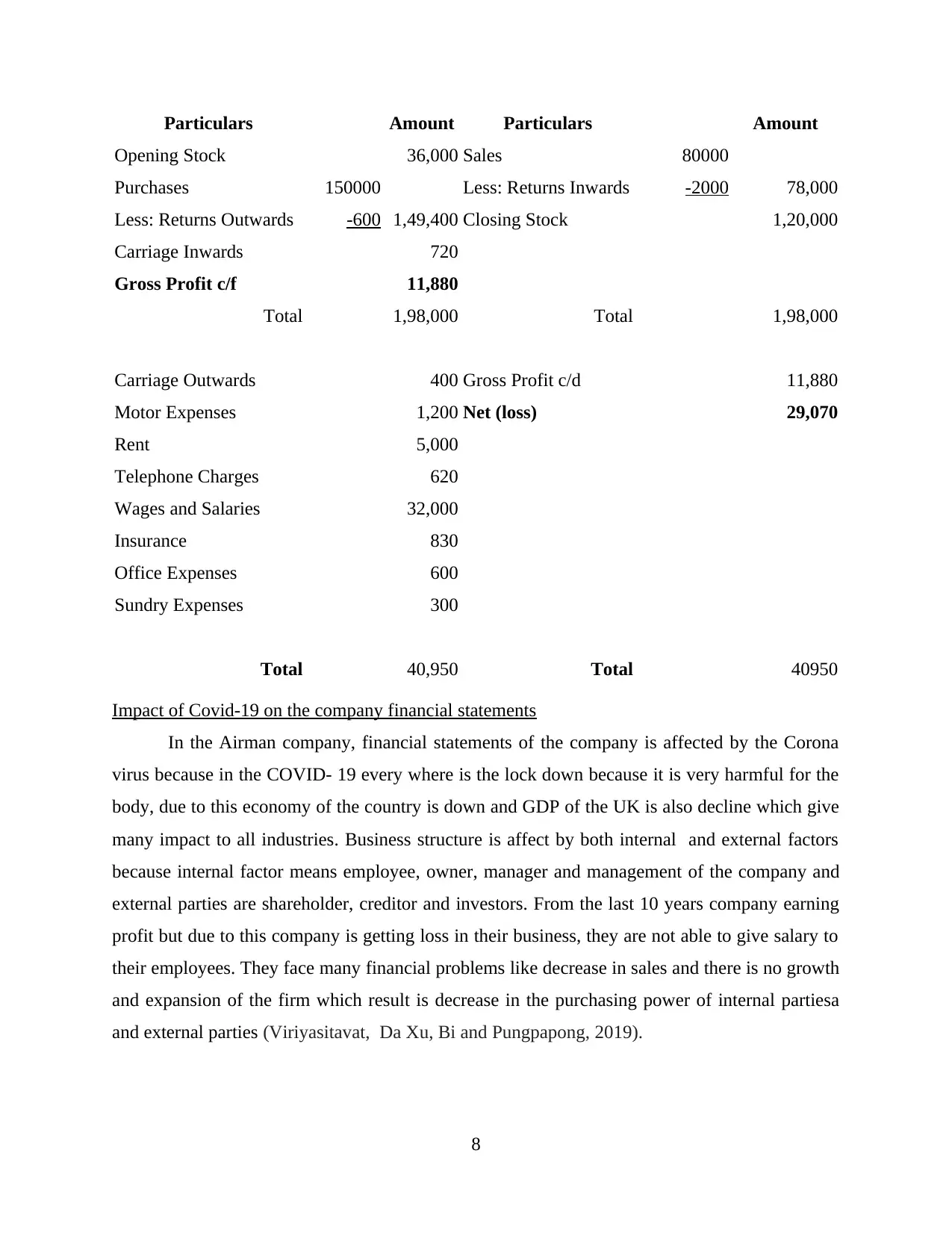

PART 4

Income statement for Airman co.:

Income statement in the year end 30th Sept. 2020

Profit & Loss Account

(In the year ending 30th Sept 20)

7

Date Particulars Amt. Date Particulars Amt.

feb'02 By Bank A/c 2500

feb'29 By Balance c/f 2,500

Total 2500 Total 2,500

Trial balance- It is the list of all ledger which is expressed in both capital and revenue,

this contain the amount of all ledger account which is balanced on the debit side and credit side

because each nominal account in the ledger should have debit or credit balance.

Trial Balance

(in the month ending 29/02/2020)

(Amounts in GBP)

Particulars Debit Credit

Capital Account 47,300

Bank Account 12,230

Cash Account 1,080

Van Account 35,000

Quick Office Ltd. Account 1,100

Office Fixture Account 2,590

Loan Account 2,500

Total 50,900 50,900

PART 4

Income statement for Airman co.:

Income statement in the year end 30th Sept. 2020

Profit & Loss Account

(In the year ending 30th Sept 20)

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Particulars Amount Particulars Amount

Opening Stock 36,000 Sales 80000

Purchases 150000 Less: Returns Inwards -2000 78,000

Less: Returns Outwards -600 1,49,400 Closing Stock 1,20,000

Carriage Inwards 720

Gross Profit c/f 11,880

Total 1,98,000 Total 1,98,000

Carriage Outwards 400 Gross Profit c/d 11,880

Motor Expenses 1,200 Net (loss) 29,070

Rent 5,000

Telephone Charges 620

Wages and Salaries 32,000

Insurance 830

Office Expenses 600

Sundry Expenses 300

Total 40,950 Total 40950

Impact of Covid-19 on the company financial statements

In the Airman company, financial statements of the company is affected by the Corona

virus because in the COVID- 19 every where is the lock down because it is very harmful for the

body, due to this economy of the country is down and GDP of the UK is also decline which give

many impact to all industries. Business structure is affect by both internal and external factors

because internal factor means employee, owner, manager and management of the company and

external parties are shareholder, creditor and investors. From the last 10 years company earning

profit but due to this company is getting loss in their business, they are not able to give salary to

their employees. They face many financial problems like decrease in sales and there is no growth

and expansion of the firm which result is decrease in the purchasing power of internal partiesa

and external parties (Viriyasitavat, Da Xu, Bi and Pungpapong, 2019).

8

Opening Stock 36,000 Sales 80000

Purchases 150000 Less: Returns Inwards -2000 78,000

Less: Returns Outwards -600 1,49,400 Closing Stock 1,20,000

Carriage Inwards 720

Gross Profit c/f 11,880

Total 1,98,000 Total 1,98,000

Carriage Outwards 400 Gross Profit c/d 11,880

Motor Expenses 1,200 Net (loss) 29,070

Rent 5,000

Telephone Charges 620

Wages and Salaries 32,000

Insurance 830

Office Expenses 600

Sundry Expenses 300

Total 40,950 Total 40950

Impact of Covid-19 on the company financial statements

In the Airman company, financial statements of the company is affected by the Corona

virus because in the COVID- 19 every where is the lock down because it is very harmful for the

body, due to this economy of the country is down and GDP of the UK is also decline which give

many impact to all industries. Business structure is affect by both internal and external factors

because internal factor means employee, owner, manager and management of the company and

external parties are shareholder, creditor and investors. From the last 10 years company earning

profit but due to this company is getting loss in their business, they are not able to give salary to

their employees. They face many financial problems like decrease in sales and there is no growth

and expansion of the firm which result is decrease in the purchasing power of internal partiesa

and external parties (Viriyasitavat, Da Xu, Bi and Pungpapong, 2019).

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CONCLUSION

From the above report it has been concluded that recording business transaction is very

useful in maintaining the dual entry book keeping by making the profit and loss account,

balance sheet. It also help in making the business structure of the company and analysis of all

elements of income statements

REFERENCES

Books and Journals

Aragon, N., 2017. Calculating Artists' Royalties: An Analysis of the Courts' Dualistic

Interpretations of Recording Contracts Negotiated in a Pre-Digital Age.Cardozo L. Rev.

De-Novo, p.180.

Kim, H., Rhee, C. E. and Lee, H .J., 2016. A low-power video recording system with multiple

operation modes for H. 264 and light-weight compression.IEEE Transactions on

Multimedia. 18(4). pp.603-613.

Klenk, A .D., Onyenokwe, C. M. and Perez, E. A., 2020. Recording Human Stories in a Time of

Crisis.

Peters, J. D., 2016. Recording beyond the grave: Joseph Smith’s celestial bookkeeping.Critical

Inquiry.42(4). pp.842-864.

Viriyasitavat, W., Da Xu, L., Bi, Z. and Pungpapong, V., 2019. Blockchain and internet of things

for modern business process in digital economy—the state of the artIEEE Transactions

on Computational Social Systems.6(6). pp.1420-1432.

9

From the above report it has been concluded that recording business transaction is very

useful in maintaining the dual entry book keeping by making the profit and loss account,

balance sheet. It also help in making the business structure of the company and analysis of all

elements of income statements

REFERENCES

Books and Journals

Aragon, N., 2017. Calculating Artists' Royalties: An Analysis of the Courts' Dualistic

Interpretations of Recording Contracts Negotiated in a Pre-Digital Age.Cardozo L. Rev.

De-Novo, p.180.

Kim, H., Rhee, C. E. and Lee, H .J., 2016. A low-power video recording system with multiple

operation modes for H. 264 and light-weight compression.IEEE Transactions on

Multimedia. 18(4). pp.603-613.

Klenk, A .D., Onyenokwe, C. M. and Perez, E. A., 2020. Recording Human Stories in a Time of

Crisis.

Peters, J. D., 2016. Recording beyond the grave: Joseph Smith’s celestial bookkeeping.Critical

Inquiry.42(4). pp.842-864.

Viriyasitavat, W., Da Xu, L., Bi, Z. and Pungpapong, V., 2019. Blockchain and internet of things

for modern business process in digital economy—the state of the artIEEE Transactions

on Computational Social Systems.6(6). pp.1420-1432.

9

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.