Recording Business Transactions Portfolio - Financial Accounting

VerifiedAdded on 2023/01/05

|13

|1789

|56

Project

AI Summary

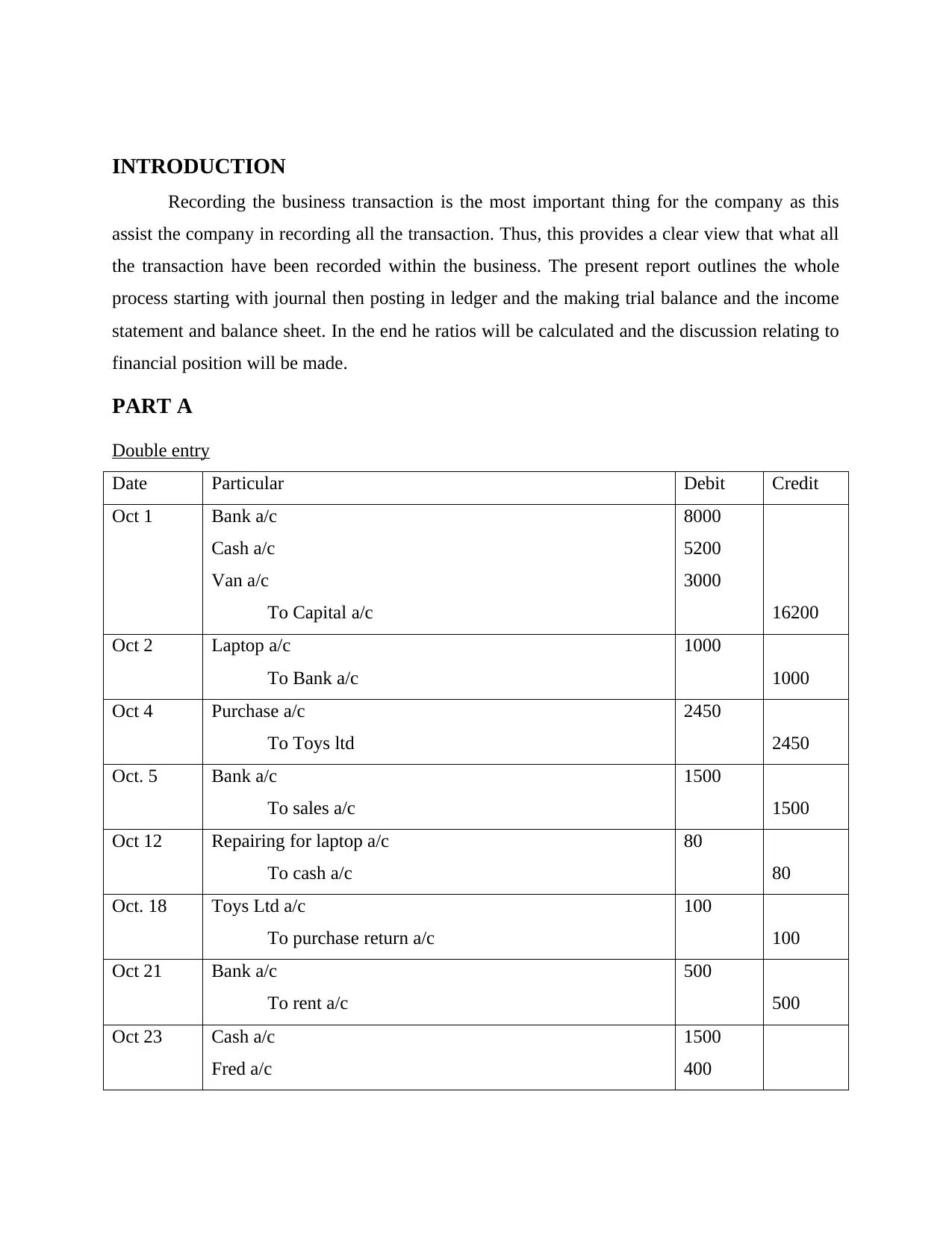

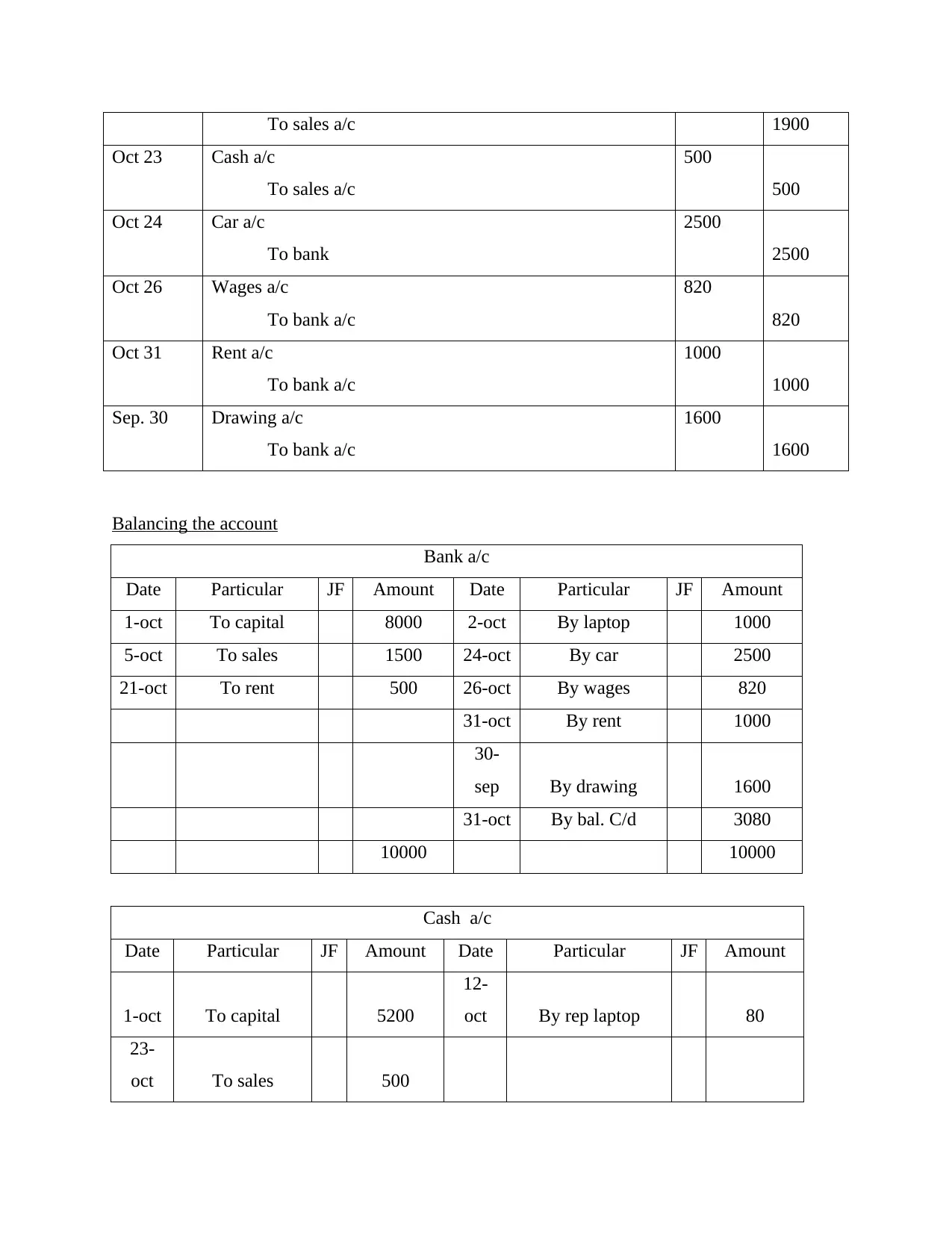

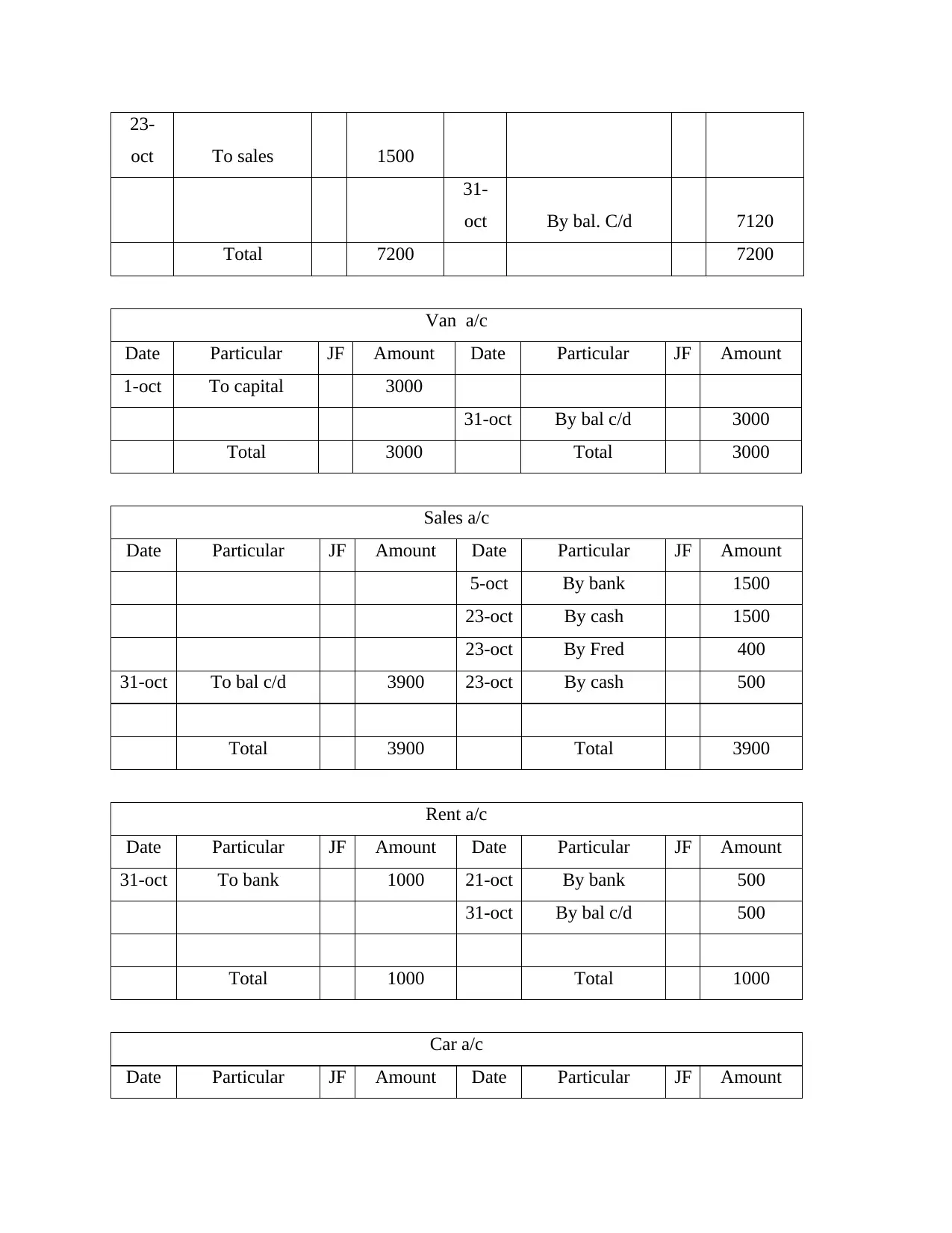

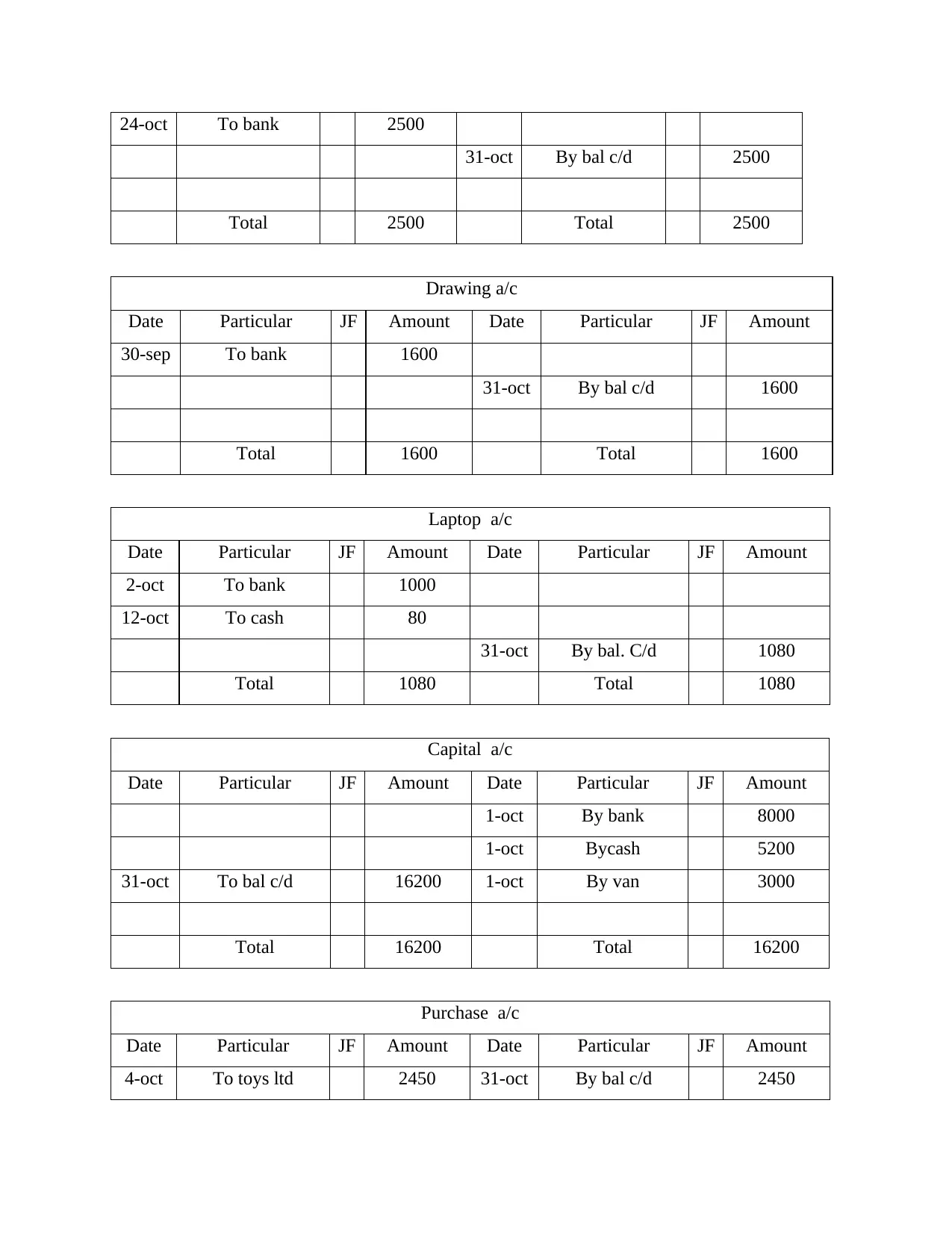

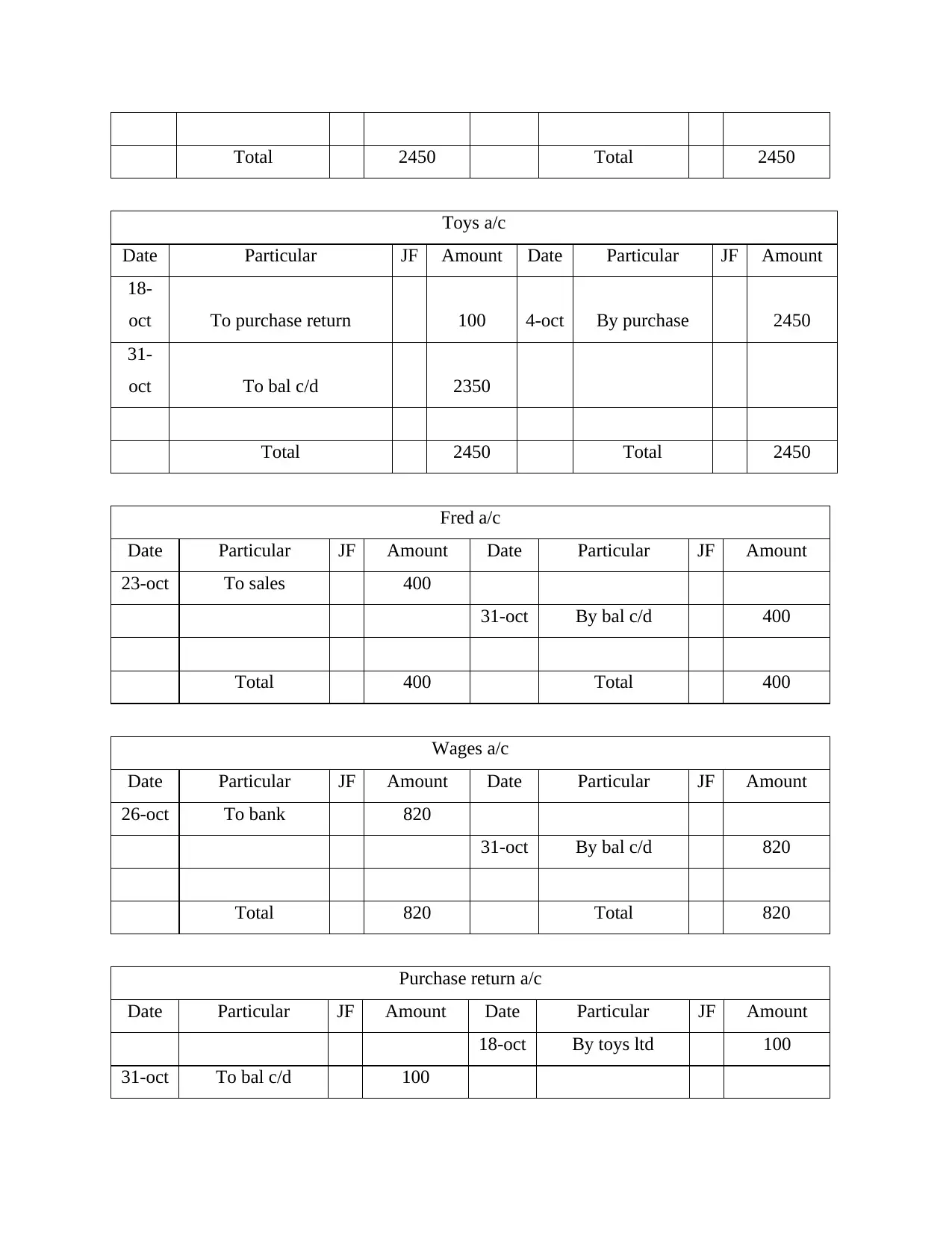

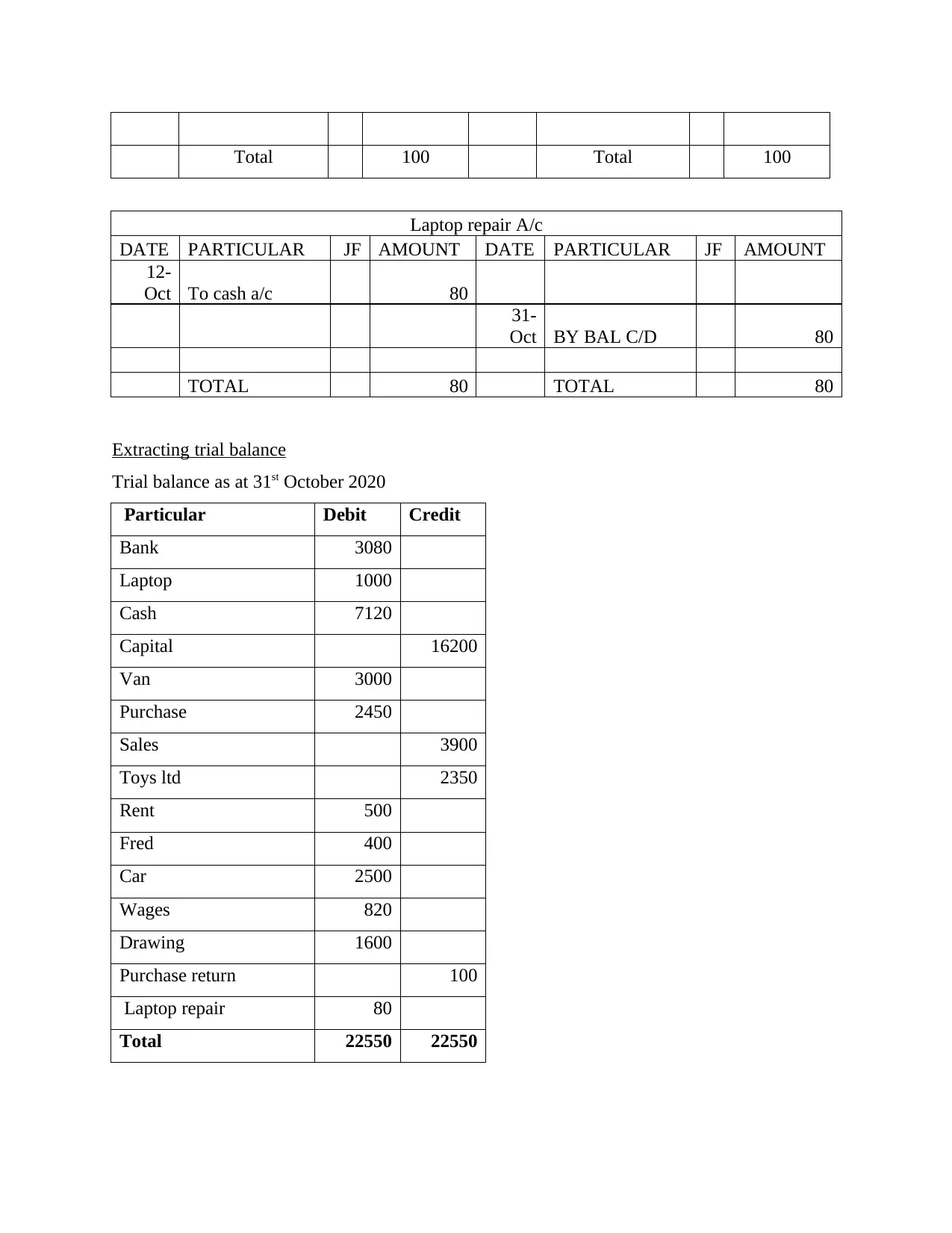

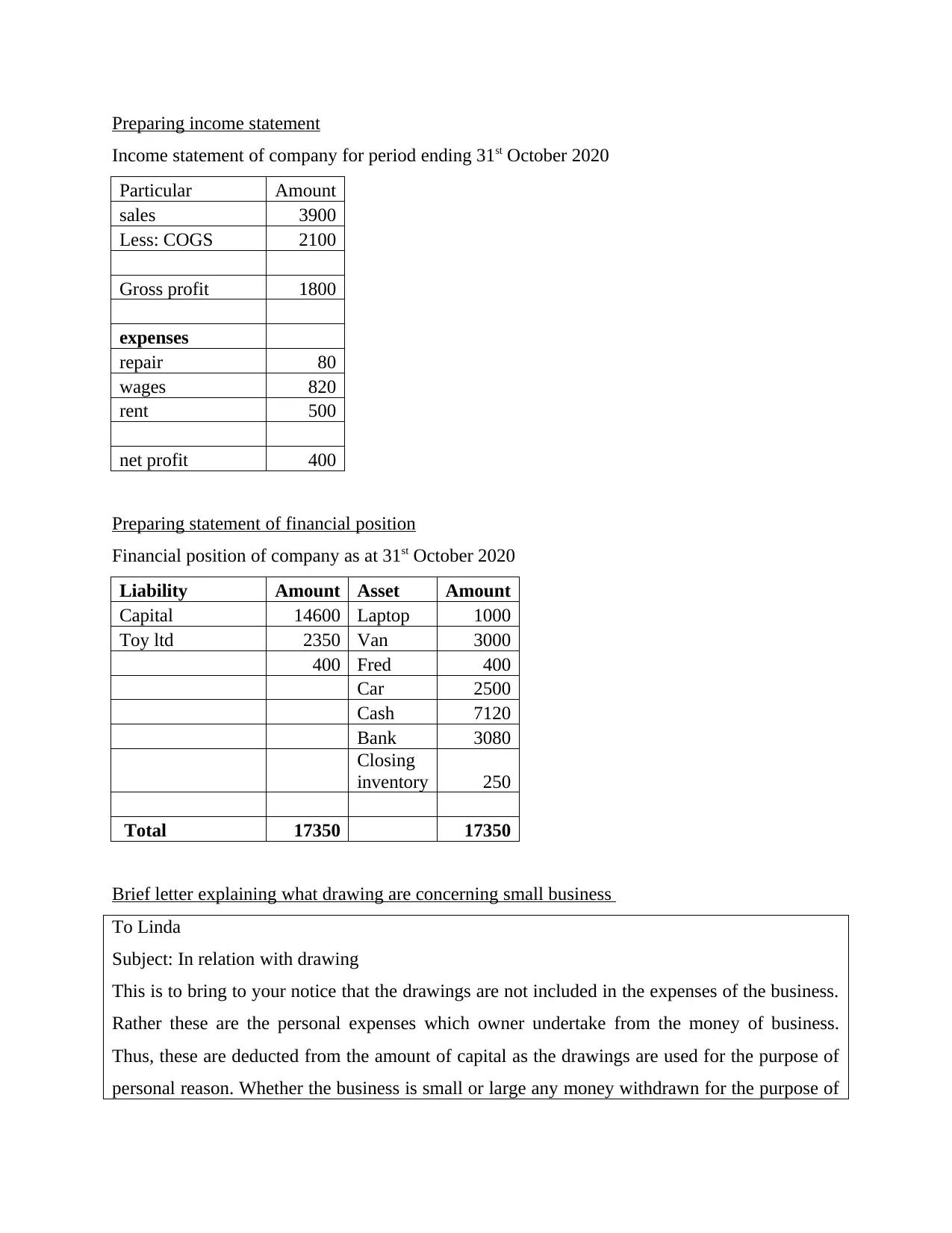

This project is a finance portfolio that meticulously documents the process of recording business transactions, starting with journal entries and progressing through ledger postings, trial balance preparation, and the creation of income statements and balance sheets. The portfolio includes a detailed double-entry bookkeeping example, followed by balancing accounts and extracting a trial balance. It then moves on to preparing an income statement and a statement of financial position. Further, the project provides a brief explanation of drawings in the context of a small business. Part B of the project focuses on calculating key financial ratios, such as gross profit ratio, net profit ratio, current ratio, and quick ratio. The portfolio concludes with an analysis of the company's performance based on these ratios, comparing them to industry benchmarks and competitors. This project serves as a comprehensive guide to financial accounting principles.

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.