Accounting Report on Recording and Analyzing Business Transactions

VerifiedAdded on 2022/12/29

|13

|2592

|39

Report

AI Summary

This report provides a comprehensive analysis of recording business transactions. It begins with an introduction defining business transactions and their importance, followed by an assessment that includes identifying decision-makers at Unilever and their need for accounting information, along with the advantages and disadvantages of accounting practices. The report then delves into practical application by computing journal entries for business transactions in January 2020, creating a general ledger for Pearce and Sons, and extracting a trial balance. Furthermore, it constructs an income statement for Airman Co. and explains the impact of COVID-19 on the company's financial performance. The report concludes by summarizing the key findings and emphasizing the significance of accounting in financial decision-making, systematic recording of financial transactions, and preparation of financial statements to assess business performance and financial position.

Recording

Business

transactions

Business

transactions

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

ASSESSMENT 1.............................................................................................................................1

Part 1............................................................................................................................................1

Part 2............................................................................................................................................3

Part 3............................................................................................................................................4

Part 4............................................................................................................................................7

CONCLUSION ...............................................................................................................................8

REFERENCES..............................................................................................................................10

INTRODUCTION...........................................................................................................................1

ASSESSMENT 1.............................................................................................................................1

Part 1............................................................................................................................................1

Part 2............................................................................................................................................3

Part 3............................................................................................................................................4

Part 4............................................................................................................................................7

CONCLUSION ...............................................................................................................................8

REFERENCES..............................................................................................................................10

INTRODUCTION

Business transactions can be described as an event which is measurable in monetary

terms and possess essential impacts on financial position of an enterprise. Recording of business

transactions refers to an activity of recording financial transactions of an organization. It is a

multiple step procedure in which first step involves recording of transaction incorporated in

business in relation ton funds for the purpose of examining and deciding its effect on business

(Chaplin, 2017). This report is based on assessment of business transactions of a company. It

consists description of accounting information along with its advantages and disadvantages.

Further, journal entries are prepared for recording business items. Apart from it, general ledger

and trial balance of an organization is computed. And lastly, income statement and balance sheet

of company is prepared.

ASSESSMENT 1

Part 1

A. Identification of decision makers of Unilever and explanation of its requirement for

accounting information:

Accounting information refers to a data of business transactions of an entity. It can be

described as a data which enables identification and analysis of financial information of an

organization for the purpose of generating useful report for users or decision makers.

Decision makers, here, can be explained as a persons which are authorised to take

essential decisions for effective performance of company by implementing efficient planning and

formulating adequate strategies (Hirschmeier and Yui, 2018). It leads to enhancement of

sustainability as well as probability of an enterprise in long run. In context to large companies,

such as, Unilever, there are mainly two types of decision makers, that are, internal and external.

Internal decision makers consists of people that are working in an organization and utilises

financial information of business to improvise its productivity and efficiency. Internal decision

makers consists of managers, board of directors or owners of a Unilever. Assessment of

accounting information by managers of an enterprise helps is adequate management of financial

resources of a company. It enables management team of business in evaluation of performance

of business which ensures identification and elimination of any hindrances or loopholes for

better performance in future. Along with it, analysis of financial reports enables owners of an

1

Business transactions can be described as an event which is measurable in monetary

terms and possess essential impacts on financial position of an enterprise. Recording of business

transactions refers to an activity of recording financial transactions of an organization. It is a

multiple step procedure in which first step involves recording of transaction incorporated in

business in relation ton funds for the purpose of examining and deciding its effect on business

(Chaplin, 2017). This report is based on assessment of business transactions of a company. It

consists description of accounting information along with its advantages and disadvantages.

Further, journal entries are prepared for recording business items. Apart from it, general ledger

and trial balance of an organization is computed. And lastly, income statement and balance sheet

of company is prepared.

ASSESSMENT 1

Part 1

A. Identification of decision makers of Unilever and explanation of its requirement for

accounting information:

Accounting information refers to a data of business transactions of an entity. It can be

described as a data which enables identification and analysis of financial information of an

organization for the purpose of generating useful report for users or decision makers.

Decision makers, here, can be explained as a persons which are authorised to take

essential decisions for effective performance of company by implementing efficient planning and

formulating adequate strategies (Hirschmeier and Yui, 2018). It leads to enhancement of

sustainability as well as probability of an enterprise in long run. In context to large companies,

such as, Unilever, there are mainly two types of decision makers, that are, internal and external.

Internal decision makers consists of people that are working in an organization and utilises

financial information of business to improvise its productivity and efficiency. Internal decision

makers consists of managers, board of directors or owners of a Unilever. Assessment of

accounting information by managers of an enterprise helps is adequate management of financial

resources of a company. It enables management team of business in evaluation of performance

of business which ensures identification and elimination of any hindrances or loopholes for

better performance in future. Along with it, analysis of financial reports enables owners of an

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

organization in effective shaping of decisions regarding borrowing or investing of fund

resources of Unilever with ensures improvement in profitability of business. Apart from it,

accounting information also helps in making decisions regarding expansion or downsizing. Apart

from it, employees of an organization forms a part of its operations, although they don't

participate in process of decision making but workforce are interested in getting informed about

financial performance of company which pertains huge impact on their job security. Hence,

decisions related to stability of employees in an organization in highly based on its financial

performance.

Further, external users or decision makers of Unilever are lenders or creditors, customers,

governmental units, suppliers as well as general public. Prior to extension of credit, paying

capacity of firm is evaluated by its financial position which is showcased through information of

accounting. Creditors utilise accounting information for the purpose of evaluating ability of an

organization in context to repayment of loan (Kanodia and Sapra, 2016). Hence, information of

accounting is analysed for identifying the credit worthiness of a company. Further, government

or tax authorities use information related to accounting for the purpose of determining taxes of

Unilever. As, different types of taxes are paid by an entity in reference to various tax base or

rules. Apart from it, customers are interested in identifying capabilities of a firm. Other external

user of accounting information are investors of an enterprise. Investors of business are interested

in its prior performance as well as its potential earnings. As, financial statement of Unilever

summarizes its information in relation to financial performance of firm, business activities and

its performance.

B. Advantages as well as disadvantages of accounting:

Accounting is a procedure of recording transactions related to finance that is pertaining to

an organization (Maas Schaltegger and Crutzen, 2016). Process of accounting involves activities

of summarizing, analysing as well as reporting such financial transactions of business. It pertains

various advantages and disadvantages which are elaborated below:

Advantages:

Indicates financial position: Accounting enables interpretation of financial position of an

organization which helps in comparison of financial performance of business along with

other similar entities. It helps in determining efficiency of an organization.

2

resources of Unilever with ensures improvement in profitability of business. Apart from it,

accounting information also helps in making decisions regarding expansion or downsizing. Apart

from it, employees of an organization forms a part of its operations, although they don't

participate in process of decision making but workforce are interested in getting informed about

financial performance of company which pertains huge impact on their job security. Hence,

decisions related to stability of employees in an organization in highly based on its financial

performance.

Further, external users or decision makers of Unilever are lenders or creditors, customers,

governmental units, suppliers as well as general public. Prior to extension of credit, paying

capacity of firm is evaluated by its financial position which is showcased through information of

accounting. Creditors utilise accounting information for the purpose of evaluating ability of an

organization in context to repayment of loan (Kanodia and Sapra, 2016). Hence, information of

accounting is analysed for identifying the credit worthiness of a company. Further, government

or tax authorities use information related to accounting for the purpose of determining taxes of

Unilever. As, different types of taxes are paid by an entity in reference to various tax base or

rules. Apart from it, customers are interested in identifying capabilities of a firm. Other external

user of accounting information are investors of an enterprise. Investors of business are interested

in its prior performance as well as its potential earnings. As, financial statement of Unilever

summarizes its information in relation to financial performance of firm, business activities and

its performance.

B. Advantages as well as disadvantages of accounting:

Accounting is a procedure of recording transactions related to finance that is pertaining to

an organization (Maas Schaltegger and Crutzen, 2016). Process of accounting involves activities

of summarizing, analysing as well as reporting such financial transactions of business. It pertains

various advantages and disadvantages which are elaborated below:

Advantages:

Indicates financial position: Accounting enables interpretation of financial position of an

organization which helps in comparison of financial performance of business along with

other similar entities. It helps in determining efficiency of an organization.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

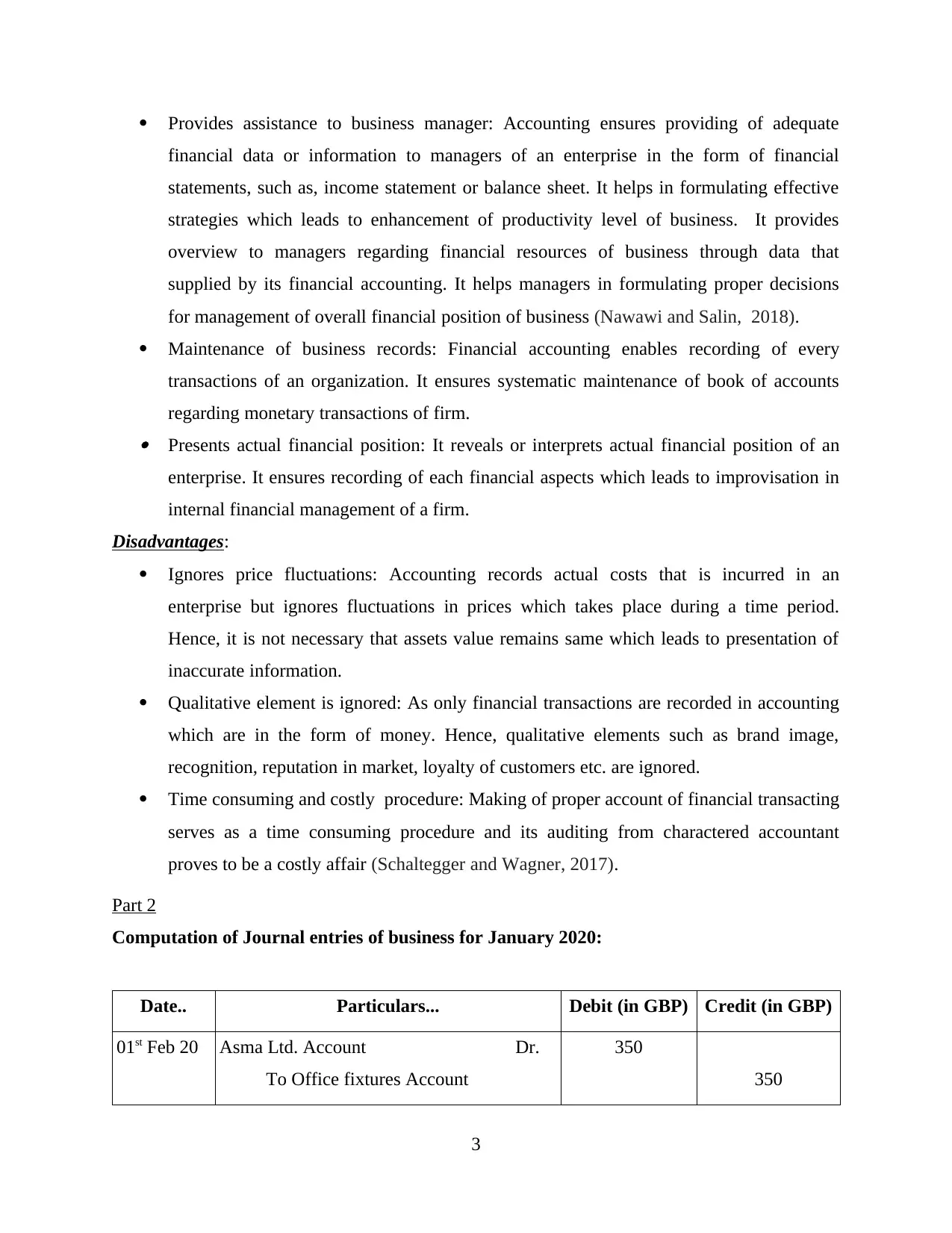

Provides assistance to business manager: Accounting ensures providing of adequate

financial data or information to managers of an enterprise in the form of financial

statements, such as, income statement or balance sheet. It helps in formulating effective

strategies which leads to enhancement of productivity level of business. It provides

overview to managers regarding financial resources of business through data that

supplied by its financial accounting. It helps managers in formulating proper decisions

for management of overall financial position of business (Nawawi and Salin, 2018).

Maintenance of business records: Financial accounting enables recording of every

transactions of an organization. It ensures systematic maintenance of book of accounts

regarding monetary transactions of firm. Presents actual financial position: It reveals or interprets actual financial position of an

enterprise. It ensures recording of each financial aspects which leads to improvisation in

internal financial management of a firm.

Disadvantages:

Ignores price fluctuations: Accounting records actual costs that is incurred in an

enterprise but ignores fluctuations in prices which takes place during a time period.

Hence, it is not necessary that assets value remains same which leads to presentation of

inaccurate information.

Qualitative element is ignored: As only financial transactions are recorded in accounting

which are in the form of money. Hence, qualitative elements such as brand image,

recognition, reputation in market, loyalty of customers etc. are ignored.

Time consuming and costly procedure: Making of proper account of financial transacting

serves as a time consuming procedure and its auditing from charactered accountant

proves to be a costly affair (Schaltegger and Wagner, 2017).

Part 2

Computation of Journal entries of business for January 2020:

Date.. Particulars... Debit (in GBP) Credit (in GBP)

01st Feb 20 Asma Ltd. Account________________Dr.

To Office fixtures Account.

350

350

3

financial data or information to managers of an enterprise in the form of financial

statements, such as, income statement or balance sheet. It helps in formulating effective

strategies which leads to enhancement of productivity level of business. It provides

overview to managers regarding financial resources of business through data that

supplied by its financial accounting. It helps managers in formulating proper decisions

for management of overall financial position of business (Nawawi and Salin, 2018).

Maintenance of business records: Financial accounting enables recording of every

transactions of an organization. It ensures systematic maintenance of book of accounts

regarding monetary transactions of firm. Presents actual financial position: It reveals or interprets actual financial position of an

enterprise. It ensures recording of each financial aspects which leads to improvisation in

internal financial management of a firm.

Disadvantages:

Ignores price fluctuations: Accounting records actual costs that is incurred in an

enterprise but ignores fluctuations in prices which takes place during a time period.

Hence, it is not necessary that assets value remains same which leads to presentation of

inaccurate information.

Qualitative element is ignored: As only financial transactions are recorded in accounting

which are in the form of money. Hence, qualitative elements such as brand image,

recognition, reputation in market, loyalty of customers etc. are ignored.

Time consuming and costly procedure: Making of proper account of financial transacting

serves as a time consuming procedure and its auditing from charactered accountant

proves to be a costly affair (Schaltegger and Wagner, 2017).

Part 2

Computation of Journal entries of business for January 2020:

Date.. Particulars... Debit (in GBP) Credit (in GBP)

01st Feb 20 Asma Ltd. Account________________Dr.

To Office fixtures Account.

350

350

3

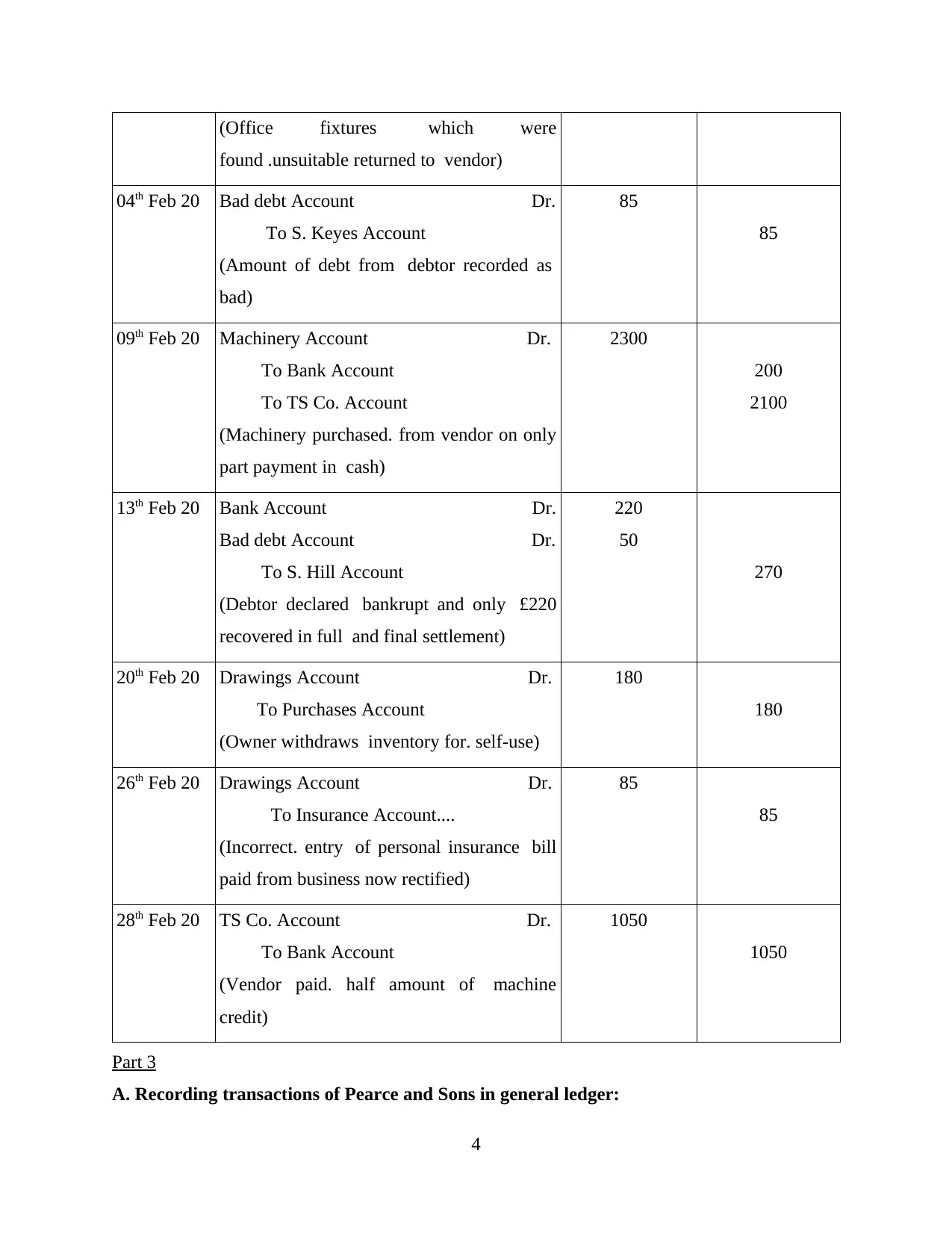

(Office fixtures. which were

found .unsuitable returned to .vendor)

04th Feb 20 Bad debt Account___________________Dr.

To S. Keyes Account.....

(Amount of debt from. debtor recorded as.

bad)

85

85

09th Feb 20 Machinery Account_________________Dr.

To Bank Account..

To TS Co. Account..

(Machinery purchased. from vendor on only

part payment in. cash)

2300

200

2100

13th Feb 20 Bank Account______________________Dr.

Bad debt Account___________________Dr.

To S. Hill Account...

(Debtor declared. bankrupt and only. £220

recovered in full .and final settlement)

220

50

270

20th Feb 20 Drawings Account__________________Dr.

To Purchases Account...

(Owner withdraws. inventory for. self-use)

180

180

26th Feb 20 Drawings Account__________________Dr.

To Insurance Account....

(Incorrect. entry .of personal insurance. bill

paid from business now rectified)

85

85

28th Feb 20 TS Co. Account____________________Dr.

To Bank Account....

(Vendor paid. half amount of. machine

credit)

1050

1050

Part 3

A. Recording transactions of Pearce and Sons in general ledger:

4

found .unsuitable returned to .vendor)

04th Feb 20 Bad debt Account___________________Dr.

To S. Keyes Account.....

(Amount of debt from. debtor recorded as.

bad)

85

85

09th Feb 20 Machinery Account_________________Dr.

To Bank Account..

To TS Co. Account..

(Machinery purchased. from vendor on only

part payment in. cash)

2300

200

2100

13th Feb 20 Bank Account______________________Dr.

Bad debt Account___________________Dr.

To S. Hill Account...

(Debtor declared. bankrupt and only. £220

recovered in full .and final settlement)

220

50

270

20th Feb 20 Drawings Account__________________Dr.

To Purchases Account...

(Owner withdraws. inventory for. self-use)

180

180

26th Feb 20 Drawings Account__________________Dr.

To Insurance Account....

(Incorrect. entry .of personal insurance. bill

paid from business now rectified)

85

85

28th Feb 20 TS Co. Account____________________Dr.

To Bank Account....

(Vendor paid. half amount of. machine

credit)

1050

1050

Part 3

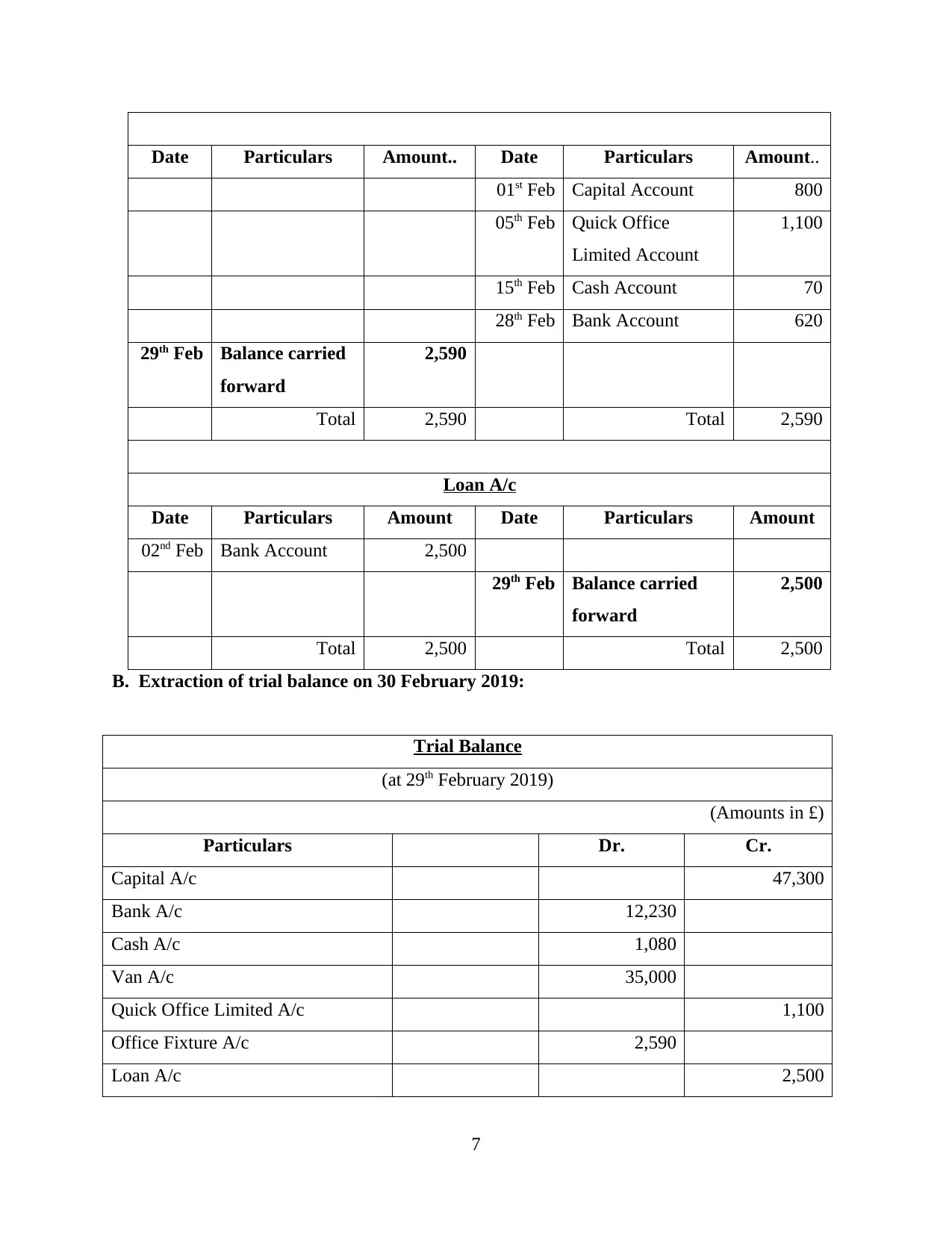

A. Recording transactions of Pearce and Sons in general ledger:

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

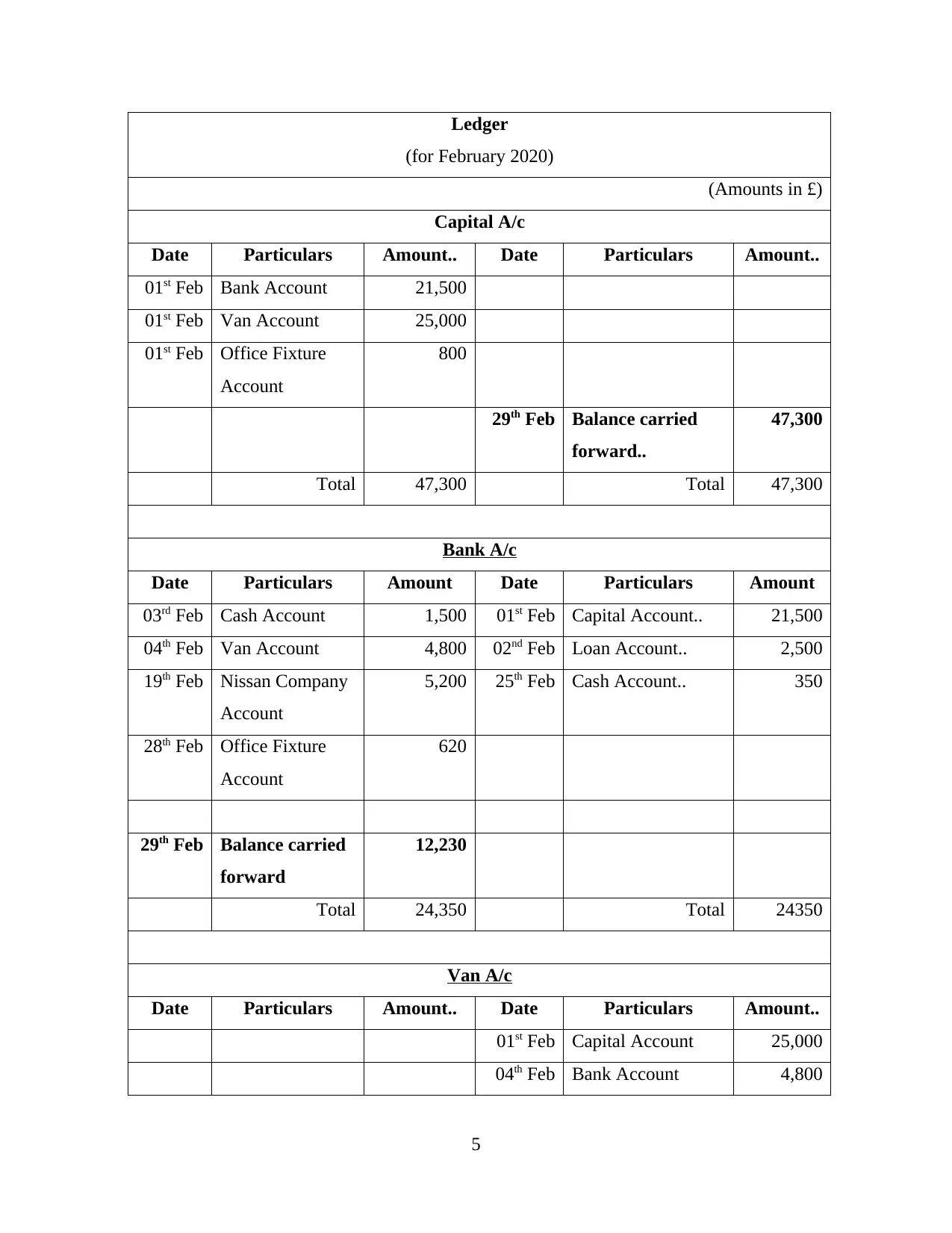

Ledger

(for February 2020)

(Amounts in £)

Capital A/c

Date Particulars Amount.. Date Particulars Amount..

01st Feb Bank Account.. 21,500

01st Feb Van Account.. 25,000

01st Feb Office Fixture..

Account..

800

29th Feb Balance carried

forward..

47,300

Total 47,300 Total 47,300

Bank A/c

Date Particulars Amount Date Particulars Amount

03rd Feb Cash Account.. 1,500 01st Feb Capital Account.. 21,500

04th Feb Van Account.. 4,800 02nd Feb Loan Account.. 2,500

19th Feb Nissan Company

Account..

5,200 25th Feb Cash Account.. 350

28th Feb Office Fixture

Account..

620

29th Feb Balance carried

forward..

12,230

Total 24,350 Total 24350

Van A/c

Date Particulars Amount.. Date Particulars Amount..

01st Feb Capital Account.. 25,000

04th Feb Bank Account.. 4,800

5

(for February 2020)

(Amounts in £)

Capital A/c

Date Particulars Amount.. Date Particulars Amount..

01st Feb Bank Account.. 21,500

01st Feb Van Account.. 25,000

01st Feb Office Fixture..

Account..

800

29th Feb Balance carried

forward..

47,300

Total 47,300 Total 47,300

Bank A/c

Date Particulars Amount Date Particulars Amount

03rd Feb Cash Account.. 1,500 01st Feb Capital Account.. 21,500

04th Feb Van Account.. 4,800 02nd Feb Loan Account.. 2,500

19th Feb Nissan Company

Account..

5,200 25th Feb Cash Account.. 350

28th Feb Office Fixture

Account..

620

29th Feb Balance carried

forward..

12,230

Total 24,350 Total 24350

Van A/c

Date Particulars Amount.. Date Particulars Amount..

01st Feb Capital Account.. 25,000

04th Feb Bank Account.. 4,800

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

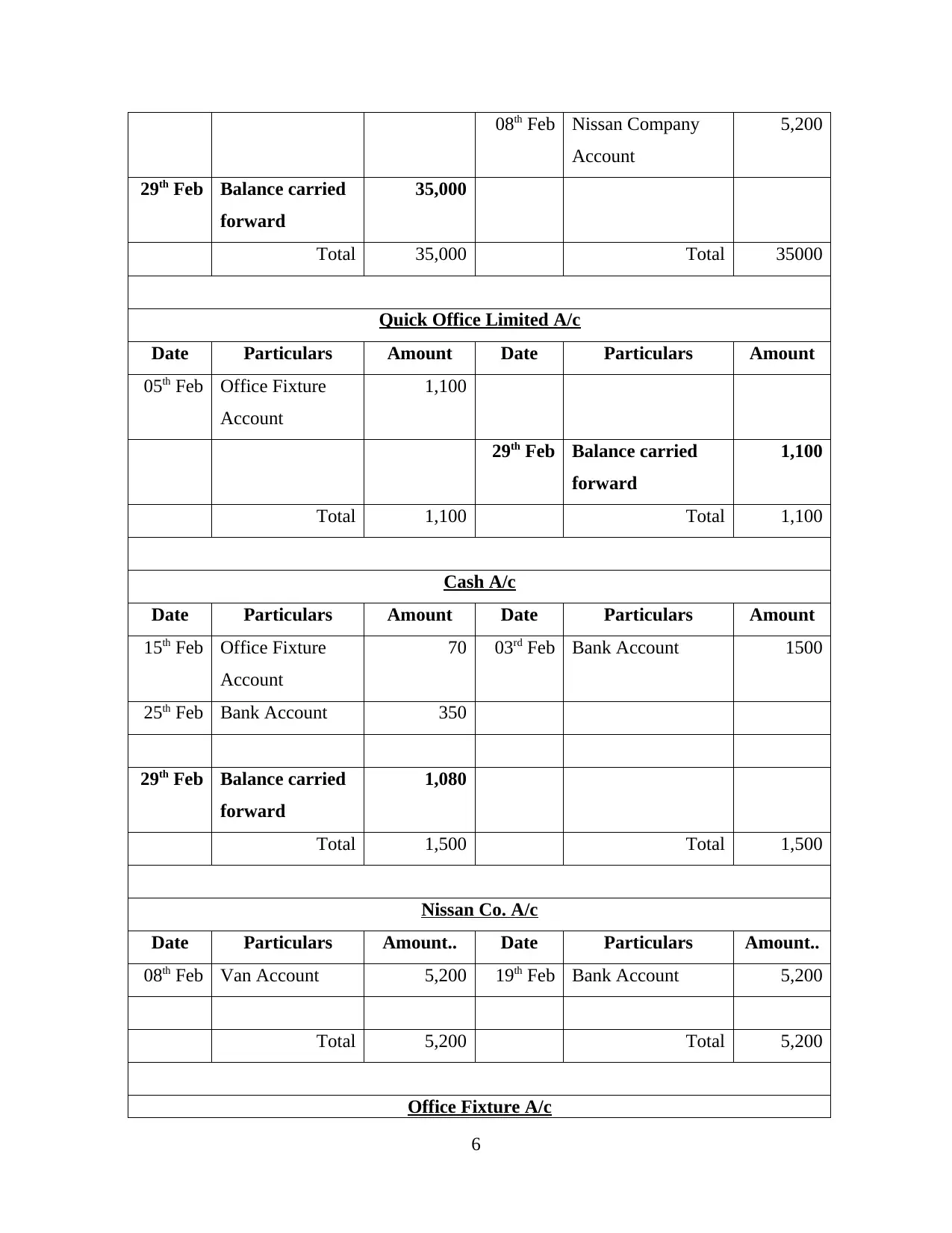

08th Feb Nissan Company

Account..

5,200

29th Feb Balance carried

forward..

35,000

Total 35,000 Total 35000

Quick Office Limited A/c

Date Particulars Amount Date Particulars Amount

05th Feb Office Fixture

Account..

1,100

29th Feb Balance carried

forward..

1,100

Total 1,100 Total 1,100

Cash A/c

Date Particulars Amount Date Particulars Amount

15th Feb Office Fixture

Account..

70 03rd Feb Bank Account.. 1500

25th Feb Bank Account.. 350

29th Feb Balance carried

forward..

1,080

Total 1,500 Total 1,500

Nissan Co. A/c

Date Particulars Amount.. Date Particulars Amount..

08th Feb Van Account.. 5,200 19th Feb Bank Account.. 5,200

Total 5,200 Total 5,200

Office Fixture A/c

6

Account..

5,200

29th Feb Balance carried

forward..

35,000

Total 35,000 Total 35000

Quick Office Limited A/c

Date Particulars Amount Date Particulars Amount

05th Feb Office Fixture

Account..

1,100

29th Feb Balance carried

forward..

1,100

Total 1,100 Total 1,100

Cash A/c

Date Particulars Amount Date Particulars Amount

15th Feb Office Fixture

Account..

70 03rd Feb Bank Account.. 1500

25th Feb Bank Account.. 350

29th Feb Balance carried

forward..

1,080

Total 1,500 Total 1,500

Nissan Co. A/c

Date Particulars Amount.. Date Particulars Amount..

08th Feb Van Account.. 5,200 19th Feb Bank Account.. 5,200

Total 5,200 Total 5,200

Office Fixture A/c

6

Date Particulars Amount.. Date Particulars Amount..

01st Feb Capital Account.. 800

05th Feb Quick Office

Limited Account..

1,100

15th Feb Cash Account.. 70

28th Feb Bank Account.. 620

29th Feb Balance carried

forward..

2,590

Total 2,590 Total 2,590

Loan A/c

Date Particulars Amount Date Particulars Amount

02nd Feb Bank Account.. 2,500

29th Feb Balance carried

forward..

2,500

Total 2,500 Total 2,500

B. Extraction of trial balance on 30 February 2019:

Trial Balance

(at 29th February 2019)

(Amounts in £)

Particulars Dr. Cr.

Capital A/c…. 47,300

Bank A/c…. 12,230

Cash A/c…. 1,080

Van A/c…. 35,000

Quick Office Limited A/c…. 1,100

Office Fixture A/c…. 2,590

Loan A/c…. 2,500

7

01st Feb Capital Account.. 800

05th Feb Quick Office

Limited Account..

1,100

15th Feb Cash Account.. 70

28th Feb Bank Account.. 620

29th Feb Balance carried

forward..

2,590

Total 2,590 Total 2,590

Loan A/c

Date Particulars Amount Date Particulars Amount

02nd Feb Bank Account.. 2,500

29th Feb Balance carried

forward..

2,500

Total 2,500 Total 2,500

B. Extraction of trial balance on 30 February 2019:

Trial Balance

(at 29th February 2019)

(Amounts in £)

Particulars Dr. Cr.

Capital A/c…. 47,300

Bank A/c…. 12,230

Cash A/c…. 1,080

Van A/c…. 35,000

Quick Office Limited A/c…. 1,100

Office Fixture A/c…. 2,590

Loan A/c…. 2,500

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Total.... 50,900 50,900

Part 4

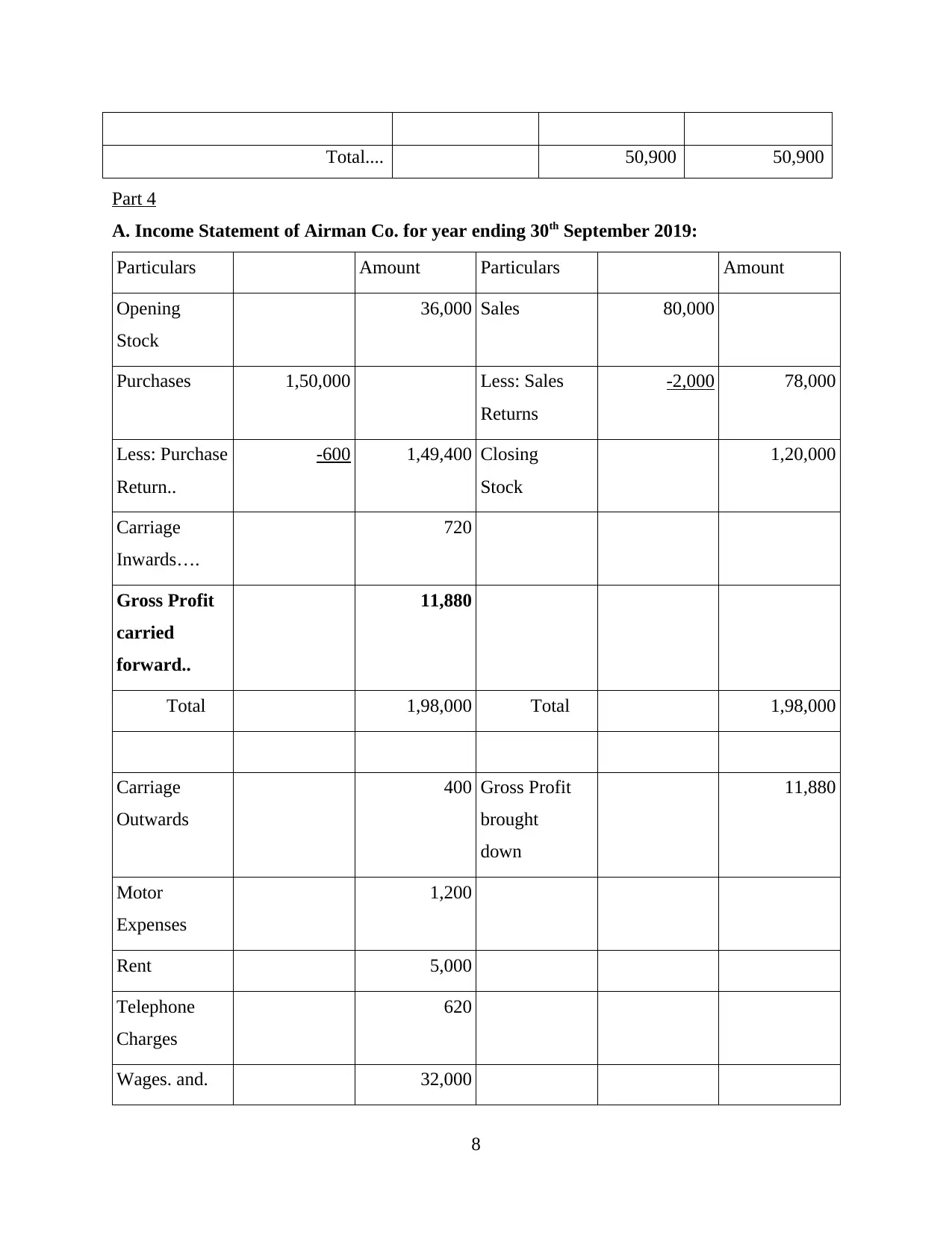

A. Income Statement of Airman Co. for year ending 30th September 2019:

Particulars Amount Particulars Amount

Opening

Stock….

36,000 Sales…. 80,000

Purchases…. 1,50,000 Less: Sales

Returns..

-2,000 78,000

Less: Purchase

Return..

-600 1,49,400 Closing

Stock….

1,20,000

Carriage

Inwards….

720

Gross Profit

carried

forward..

11,880

Total…. 1,98,000 Total…. 1,98,000

Carriage

Outwards….

400 Gross Profit

brought

down..

11,880

Motor

Expenses….

1,200

Rent…. 5,000

Telephone

Charges….

620

Wages. and. 32,000

8

Part 4

A. Income Statement of Airman Co. for year ending 30th September 2019:

Particulars Amount Particulars Amount

Opening

Stock….

36,000 Sales…. 80,000

Purchases…. 1,50,000 Less: Sales

Returns..

-2,000 78,000

Less: Purchase

Return..

-600 1,49,400 Closing

Stock….

1,20,000

Carriage

Inwards….

720

Gross Profit

carried

forward..

11,880

Total…. 1,98,000 Total…. 1,98,000

Carriage

Outwards….

400 Gross Profit

brought

down..

11,880

Motor

Expenses….

1,200

Rent…. 5,000

Telephone

Charges….

620

Wages. and. 32,000

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

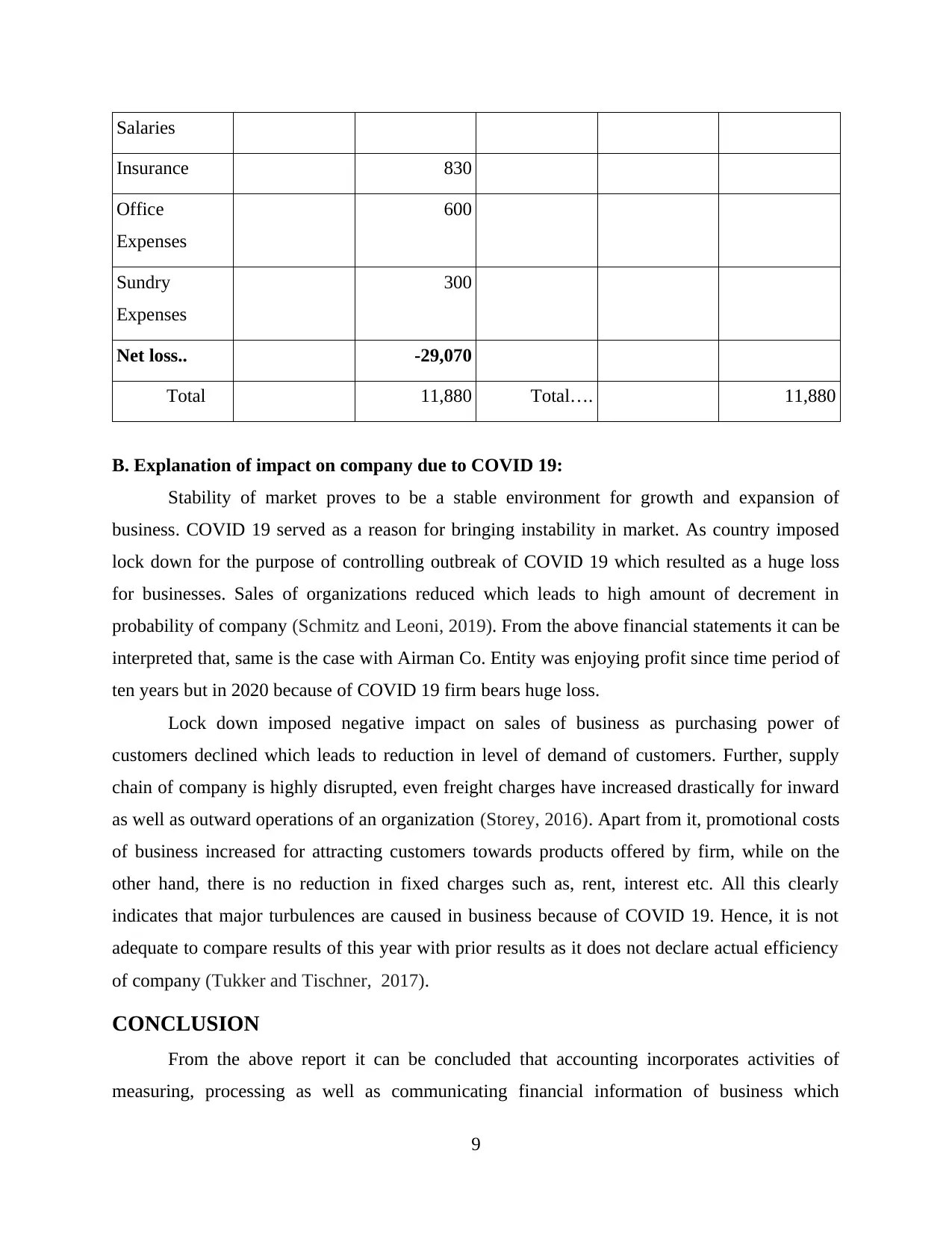

Salaries….

Insurance… 830

Office

Expenses….

600

Sundry

Expenses….

300

Net loss.. -29,070

Total…. 11,880 Total…. 11,880

B. Explanation of impact on company due to COVID 19:

Stability of market proves to be a stable environment for growth and expansion of

business. COVID 19 served as a reason for bringing instability in market. As country imposed

lock down for the purpose of controlling outbreak of COVID 19 which resulted as a huge loss

for businesses. Sales of organizations reduced which leads to high amount of decrement in

probability of company (Schmitz and Leoni, 2019). From the above financial statements it can be

interpreted that, same is the case with Airman Co. Entity was enjoying profit since time period of

ten years but in 2020 because of COVID 19 firm bears huge loss.

Lock down imposed negative impact on sales of business as purchasing power of

customers declined which leads to reduction in level of demand of customers. Further, supply

chain of company is highly disrupted, even freight charges have increased drastically for inward

as well as outward operations of an organization (Storey, 2016). Apart from it, promotional costs

of business increased for attracting customers towards products offered by firm, while on the

other hand, there is no reduction in fixed charges such as, rent, interest etc. All this clearly

indicates that major turbulences are caused in business because of COVID 19. Hence, it is not

adequate to compare results of this year with prior results as it does not declare actual efficiency

of company (Tukker and Tischner, 2017).

CONCLUSION

From the above report it can be concluded that accounting incorporates activities of

measuring, processing as well as communicating financial information of business which

9

Insurance… 830

Office

Expenses….

600

Sundry

Expenses….

300

Net loss.. -29,070

Total…. 11,880 Total…. 11,880

B. Explanation of impact on company due to COVID 19:

Stability of market proves to be a stable environment for growth and expansion of

business. COVID 19 served as a reason for bringing instability in market. As country imposed

lock down for the purpose of controlling outbreak of COVID 19 which resulted as a huge loss

for businesses. Sales of organizations reduced which leads to high amount of decrement in

probability of company (Schmitz and Leoni, 2019). From the above financial statements it can be

interpreted that, same is the case with Airman Co. Entity was enjoying profit since time period of

ten years but in 2020 because of COVID 19 firm bears huge loss.

Lock down imposed negative impact on sales of business as purchasing power of

customers declined which leads to reduction in level of demand of customers. Further, supply

chain of company is highly disrupted, even freight charges have increased drastically for inward

as well as outward operations of an organization (Storey, 2016). Apart from it, promotional costs

of business increased for attracting customers towards products offered by firm, while on the

other hand, there is no reduction in fixed charges such as, rent, interest etc. All this clearly

indicates that major turbulences are caused in business because of COVID 19. Hence, it is not

adequate to compare results of this year with prior results as it does not declare actual efficiency

of company (Tukker and Tischner, 2017).

CONCLUSION

From the above report it can be concluded that accounting incorporates activities of

measuring, processing as well as communicating financial information of business which

9

improvises decision making process of an organization. Process of accounting involves

preparation of journal entries, ledger, trial balance and financial reports. Accounting information

is utilized by decision makers which enables improvement of efficiency of firm. Such decision

makers are managers and owners of company. Apart from it, customers, government, employees

and investors also evaluate information related to financial accounting of an entity. Hence, it can

be stated that accounting is a procedure of systematic recording of transactions related to

business transactions related to finance. Financial statements that are utilised in recording

concise summary of business transactions over a time period which serves as a indicator for

performance of company and its financial position. Financial statements incorporate income

statement, balance sheet and cash flow statement of business.

10

preparation of journal entries, ledger, trial balance and financial reports. Accounting information

is utilized by decision makers which enables improvement of efficiency of firm. Such decision

makers are managers and owners of company. Apart from it, customers, government, employees

and investors also evaluate information related to financial accounting of an entity. Hence, it can

be stated that accounting is a procedure of systematic recording of transactions related to

business transactions related to finance. Financial statements that are utilised in recording

concise summary of business transactions over a time period which serves as a indicator for

performance of company and its financial position. Financial statements incorporate income

statement, balance sheet and cash flow statement of business.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.