Corporate Accounting: Recoverable Amount Calculation and Analysis

VerifiedAdded on 2023/06/11

|7

|1386

|212

Report

AI Summary

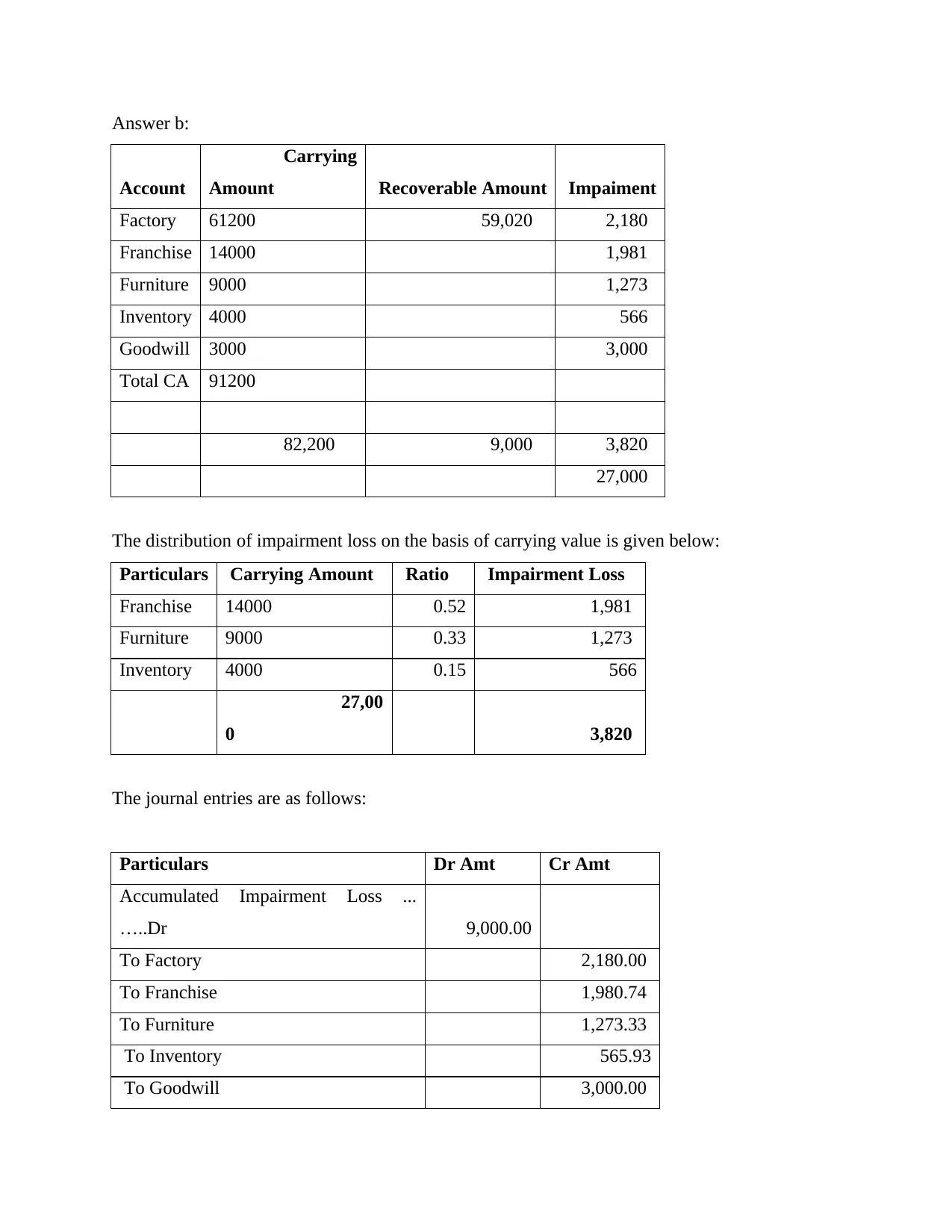

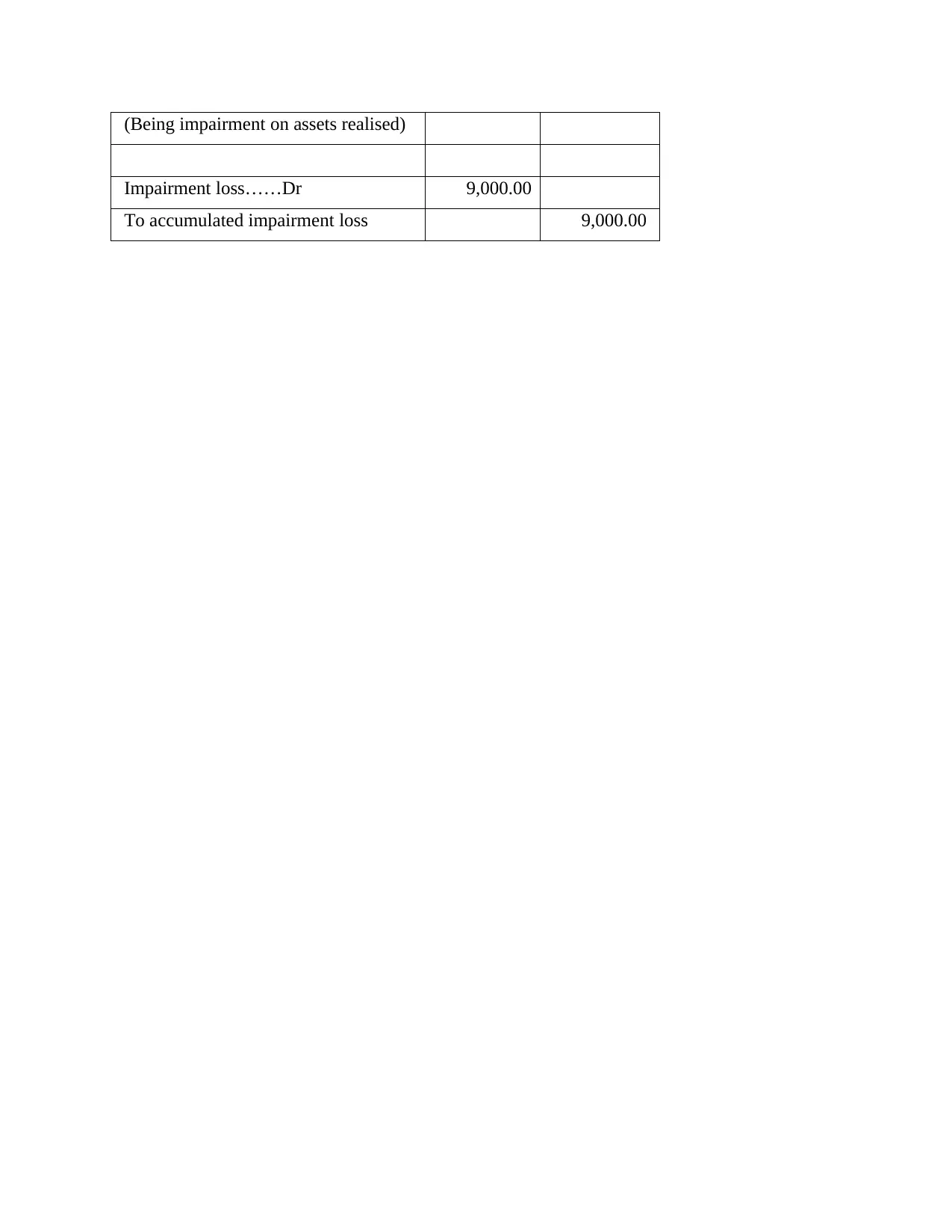

This report provides a detailed analysis of recoverable amounts and impairment loss in corporate accounting. It begins by defining the recoverable amount as the higher of value in use and fair value less cost of selling, crucial for impairment testing against the carrying amount of a cash-generating unit. The value in use is calculated by discounting future cash flows, considering factors like liquidity and risk. The report highlights key points for forecasting cash flows, including valid assumptions, excluding reconstruction charges, and comparing actual vs. forecasted performance. It discusses traditional and expected cash flow approaches, emphasizing consistency in interest rates. The fair value less cost of disposal is determined through sales agreements, market prices, or discounted cash flow analysis. The report also includes a practical example of impairment loss distribution across assets like franchise, furniture, and inventory, with corresponding journal entries. Finally, the report covers the distribution of impairment loss based on carrying value and provides relevant journal entries, offering a comprehensive overview of impairment accounting.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.