Regis Resources Ltd. Audit and Ethics Report - ACCT20075, 2019

VerifiedAdded on 2023/01/18

|16

|3210

|99

Report

AI Summary

This report provides a critical analysis of the audit of Regis Resources Ltd., focusing on key aspects such as materiality, analytical review, and the review of the cash flow statement. The report begins with an introduction to Regis Resources, a public limited company involved in gold production and exploration, highlighting the importance of proper financial reporting and adherence to regulations. The report then delves into the level of materiality, discussing risks like impairment of intangibles, transactions between related parties, and the impact of inventory valuation. It further reviews the company's draft notes and disclosures, focusing on the valuation of low-grade ore stockpiles and Exploration and Evaluation (E&E) assets. The report also includes a preliminary analytical review, assessing the current and quick ratios, and debt-to-equity ratio to gauge the company's financial health. Finally, the report examines the cash flow statement, analyzing the net cash flow from operating, investing, and financing activities for the years 2017 and 2018. The overall aim is to provide a comprehensive assessment of the company's financial position and adherence to auditing principles.

AUDIT & ETHICS

1

[Year]

1

[Year]

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Regis Resources

Executive Summary

It is important for a company to adhere to the principles of disclosures and other relevant

regulations. It needs to be carefully assessed because any ignorance can lead to immense

problem for the auditor. The current report is based on Regis Resources Ltd, a company

engaged in resources. The main aim of the report is to provide a critical analysis of the skills

in tune to materiality by undertaking audit procedures and framing opinion.

2

Executive Summary

It is important for a company to adhere to the principles of disclosures and other relevant

regulations. It needs to be carefully assessed because any ignorance can lead to immense

problem for the auditor. The current report is based on Regis Resources Ltd, a company

engaged in resources. The main aim of the report is to provide a critical analysis of the skills

in tune to materiality by undertaking audit procedures and framing opinion.

2

Regis Resources

Contents

Introduction...........................................................................................................................................4

1. The level of materiality..................................................................................................................5

Review of the various draft notes and disclosures.........................................................................6

2. Preliminary analytical review........................................................................................................7

3. Review of cash flow statement......................................................................................................8

Conclusion...........................................................................................................................................11

References...........................................................................................................................................12

Appendix.............................................................................................................................................14

3

Contents

Introduction...........................................................................................................................................4

1. The level of materiality..................................................................................................................5

Review of the various draft notes and disclosures.........................................................................6

2. Preliminary analytical review........................................................................................................7

3. Review of cash flow statement......................................................................................................8

Conclusion...........................................................................................................................................11

References...........................................................................................................................................12

Appendix.............................................................................................................................................14

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Regis Resources

Introduction

Regis Resources is a public limited company that in engaged into production of gold and

exploration. It has a strong management team that has enabled it to develop mid size gold

operations within Australia. However, for a smooth functioning of the operations, it is

essential that the company should have proper resources and stakeholders. Therefore, it is

imperative must perform the duty with due care and diligence. The current report sheds light

on analytical review of the auditor and an assessment of the financial statement of the

company.

4

Introduction

Regis Resources is a public limited company that in engaged into production of gold and

exploration. It has a strong management team that has enabled it to develop mid size gold

operations within Australia. However, for a smooth functioning of the operations, it is

essential that the company should have proper resources and stakeholders. Therefore, it is

imperative must perform the duty with due care and diligence. The current report sheds light

on analytical review of the auditor and an assessment of the financial statement of the

company.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Regis Resources

1. The level of materiality

Impairment of intangibles is another material risk faced by Regis Resources Ltd. It is highly

material due to the fact that the organization did not account for impairment of its intangibles

in 2017. This means that the company did not account goodwill for impairment while the

non-financial assets were given due consideration in the year 2017. It is not just necessary but

also essential at the same time for an organization to examine and account impairment of its

intangibles every year. This allows an organization to account the changes in its intangibles

and duly allow the impairment of the same. The present values of assets and liabilities are

also affected by the risks that are aligned with the materiality level of investments such as

provisions, share-based payments, employee benefit liabilities, and deferred taxes.

The transactions between related parties also carry risks associated with material

misstatements. The real value of the transaction is often prone to risks and consequences

arising out of transactions between related parties. The transactions between related parties

also impact the financial wellbeing of an organization. There are multiple instances of

transactions between related parties at Regis Resources Ltd. The involvement of directors of

the company in multiple related party transactions is also seen. The financial status of the

company always gets impacted due to such related party transactions. Regis Resources Ltd

should now chuck out an audit plan in order to safeguard the financial wellbeing of the

company, keeping in mind the consequences of transactions between related parties.

Regis Resources Limited offered a loan to Duketon Resources that was non-interest bearing

and has no fixed date of repayment. The balance of the loan receivable was 24,157,000$ as in

the year 2017 while 25,971,000$ as on 30th June 2018. LFB Resources also received a loan

from Regis Resources Ltd on account of towards the subsidiary’s share of payments for

exploration and evaluation expenditure. The loan was non-interest-bearing and has no fixed

date of repayment as well. The balance of the loan receivable was 38,775,000$ as in the year

2017 while 63,945,000$ as on 30th June 2018.

5

1. The level of materiality

Impairment of intangibles is another material risk faced by Regis Resources Ltd. It is highly

material due to the fact that the organization did not account for impairment of its intangibles

in 2017. This means that the company did not account goodwill for impairment while the

non-financial assets were given due consideration in the year 2017. It is not just necessary but

also essential at the same time for an organization to examine and account impairment of its

intangibles every year. This allows an organization to account the changes in its intangibles

and duly allow the impairment of the same. The present values of assets and liabilities are

also affected by the risks that are aligned with the materiality level of investments such as

provisions, share-based payments, employee benefit liabilities, and deferred taxes.

The transactions between related parties also carry risks associated with material

misstatements. The real value of the transaction is often prone to risks and consequences

arising out of transactions between related parties. The transactions between related parties

also impact the financial wellbeing of an organization. There are multiple instances of

transactions between related parties at Regis Resources Ltd. The involvement of directors of

the company in multiple related party transactions is also seen. The financial status of the

company always gets impacted due to such related party transactions. Regis Resources Ltd

should now chuck out an audit plan in order to safeguard the financial wellbeing of the

company, keeping in mind the consequences of transactions between related parties.

Regis Resources Limited offered a loan to Duketon Resources that was non-interest bearing

and has no fixed date of repayment. The balance of the loan receivable was 24,157,000$ as in

the year 2017 while 25,971,000$ as on 30th June 2018. LFB Resources also received a loan

from Regis Resources Ltd on account of towards the subsidiary’s share of payments for

exploration and evaluation expenditure. The loan was non-interest-bearing and has no fixed

date of repayment as well. The balance of the loan receivable was 38,775,000$ as in the year

2017 while 63,945,000$ as on 30th June 2018.

5

Regis Resources

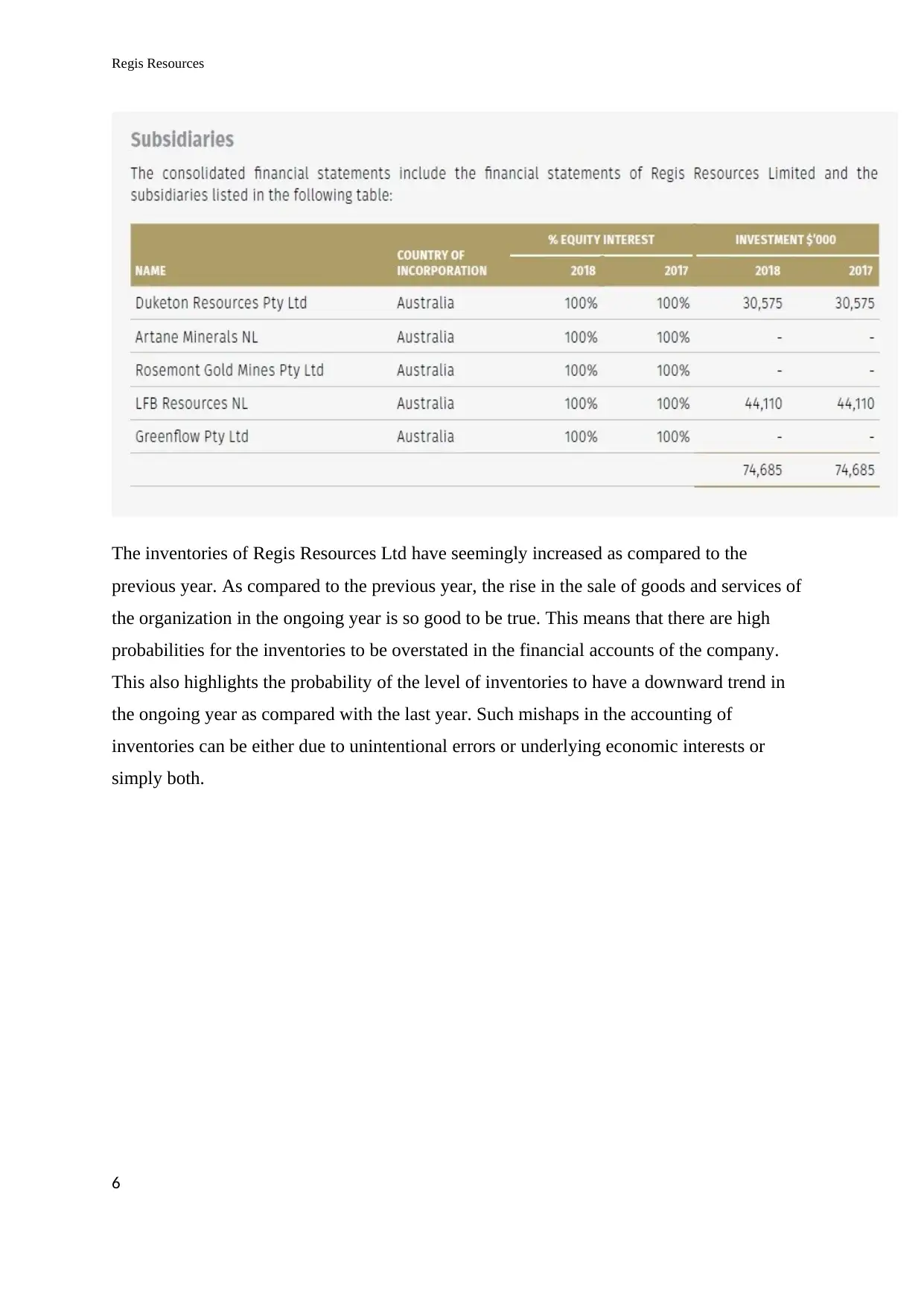

The inventories of Regis Resources Ltd have seemingly increased as compared to the

previous year. As compared to the previous year, the rise in the sale of goods and services of

the organization in the ongoing year is so good to be true. This means that there are high

probabilities for the inventories to be overstated in the financial accounts of the company.

This also highlights the probability of the level of inventories to have a downward trend in

the ongoing year as compared with the last year. Such mishaps in the accounting of

inventories can be either due to unintentional errors or underlying economic interests or

simply both.

6

The inventories of Regis Resources Ltd have seemingly increased as compared to the

previous year. As compared to the previous year, the rise in the sale of goods and services of

the organization in the ongoing year is so good to be true. This means that there are high

probabilities for the inventories to be overstated in the financial accounts of the company.

This also highlights the probability of the level of inventories to have a downward trend in

the ongoing year as compared with the last year. Such mishaps in the accounting of

inventories can be either due to unintentional errors or underlying economic interests or

simply both.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Regis Resources

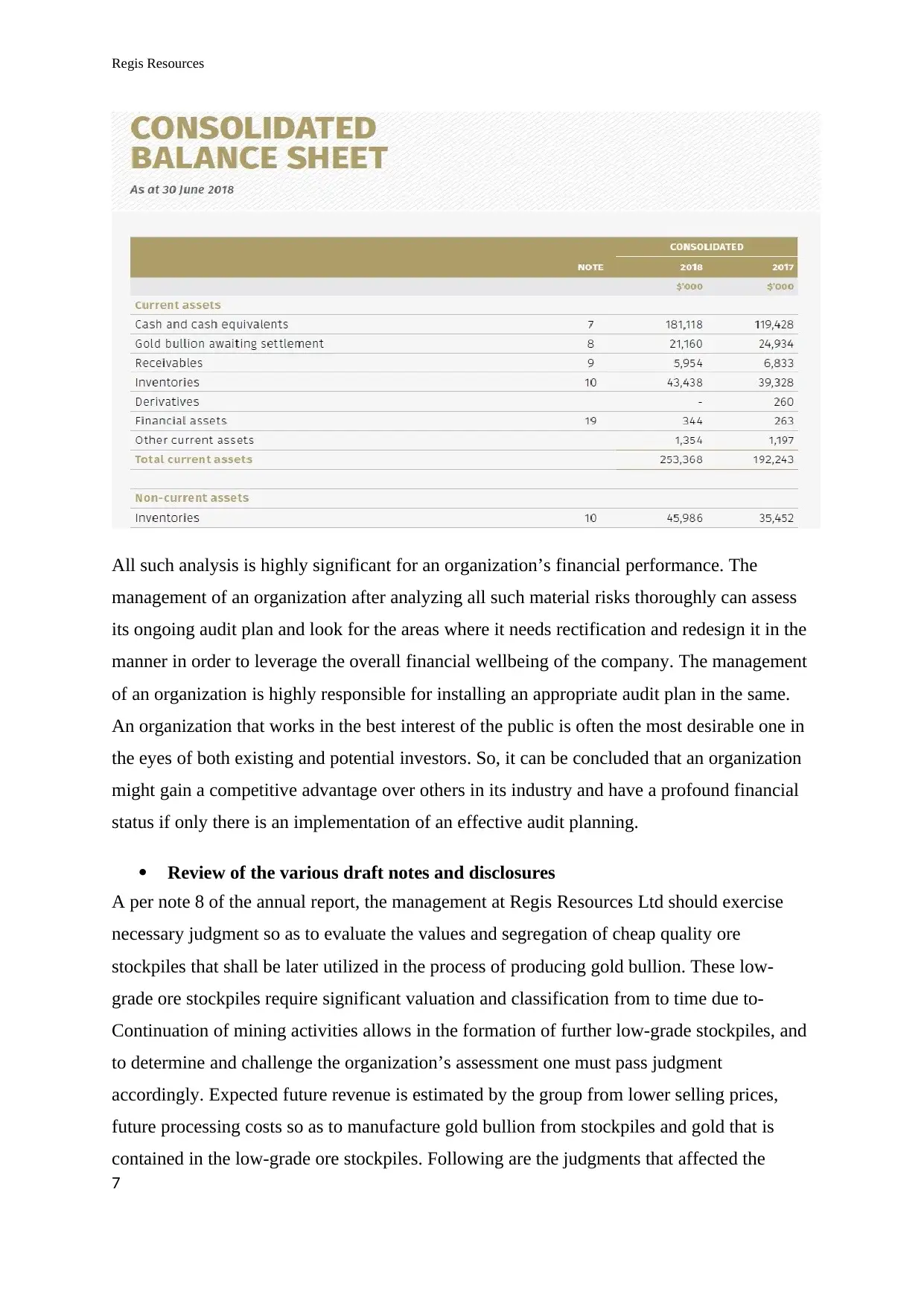

All such analysis is highly significant for an organization’s financial performance. The

management of an organization after analyzing all such material risks thoroughly can assess

its ongoing audit plan and look for the areas where it needs rectification and redesign it in the

manner in order to leverage the overall financial wellbeing of the company. The management

of an organization is highly responsible for installing an appropriate audit plan in the same.

An organization that works in the best interest of the public is often the most desirable one in

the eyes of both existing and potential investors. So, it can be concluded that an organization

might gain a competitive advantage over others in its industry and have a profound financial

status if only there is an implementation of an effective audit planning.

Review of the various draft notes and disclosures

A per note 8 of the annual report, the management at Regis Resources Ltd should exercise

necessary judgment so as to evaluate the values and segregation of cheap quality ore

stockpiles that shall be later utilized in the process of producing gold bullion. These low-

grade ore stockpiles require significant valuation and classification from to time due to-

Continuation of mining activities allows in the formation of further low-grade stockpiles, and

to determine and challenge the organization’s assessment one must pass judgment

accordingly. Expected future revenue is estimated by the group from lower selling prices,

future processing costs so as to manufacture gold bullion from stockpiles and gold that is

contained in the low-grade ore stockpiles. Following are the judgments that affected the

7

All such analysis is highly significant for an organization’s financial performance. The

management of an organization after analyzing all such material risks thoroughly can assess

its ongoing audit plan and look for the areas where it needs rectification and redesign it in the

manner in order to leverage the overall financial wellbeing of the company. The management

of an organization is highly responsible for installing an appropriate audit plan in the same.

An organization that works in the best interest of the public is often the most desirable one in

the eyes of both existing and potential investors. So, it can be concluded that an organization

might gain a competitive advantage over others in its industry and have a profound financial

status if only there is an implementation of an effective audit planning.

Review of the various draft notes and disclosures

A per note 8 of the annual report, the management at Regis Resources Ltd should exercise

necessary judgment so as to evaluate the values and segregation of cheap quality ore

stockpiles that shall be later utilized in the process of producing gold bullion. These low-

grade ore stockpiles require significant valuation and classification from to time due to-

Continuation of mining activities allows in the formation of further low-grade stockpiles, and

to determine and challenge the organization’s assessment one must pass judgment

accordingly. Expected future revenue is estimated by the group from lower selling prices,

future processing costs so as to manufacture gold bullion from stockpiles and gold that is

contained in the low-grade ore stockpiles. Following are the judgments that affected the

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Regis Resources

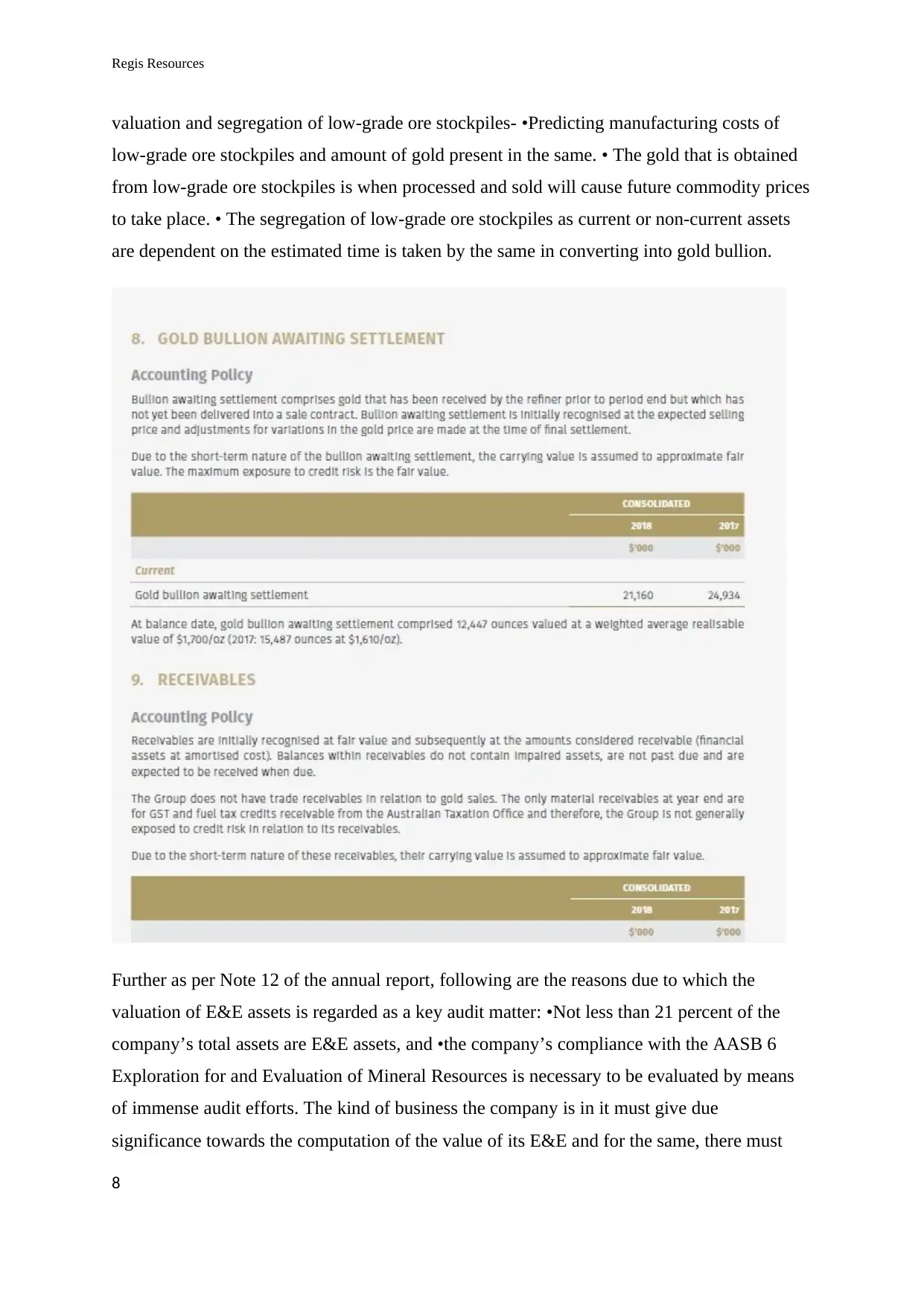

valuation and segregation of low-grade ore stockpiles- •Predicting manufacturing costs of

low-grade ore stockpiles and amount of gold present in the same. • The gold that is obtained

from low-grade ore stockpiles is when processed and sold will cause future commodity prices

to take place. • The segregation of low-grade ore stockpiles as current or non-current assets

are dependent on the estimated time is taken by the same in converting into gold bullion.

Further as per Note 12 of the annual report, following are the reasons due to which the

valuation of E&E assets is regarded as a key audit matter: •Not less than 21 percent of the

company’s total assets are E&E assets, and •the company’s compliance with the AASB 6

Exploration for and Evaluation of Mineral Resources is necessary to be evaluated by means

of immense audit efforts. The kind of business the company is in it must give due

significance towards the computation of the value of its E&E and for the same, there must

8

valuation and segregation of low-grade ore stockpiles- •Predicting manufacturing costs of

low-grade ore stockpiles and amount of gold present in the same. • The gold that is obtained

from low-grade ore stockpiles is when processed and sold will cause future commodity prices

to take place. • The segregation of low-grade ore stockpiles as current or non-current assets

are dependent on the estimated time is taken by the same in converting into gold bullion.

Further as per Note 12 of the annual report, following are the reasons due to which the

valuation of E&E assets is regarded as a key audit matter: •Not less than 21 percent of the

company’s total assets are E&E assets, and •the company’s compliance with the AASB 6

Exploration for and Evaluation of Mineral Resources is necessary to be evaluated by means

of immense audit efforts. The kind of business the company is in it must give due

significance towards the computation of the value of its E&E and for the same, there must

8

Regis Resources

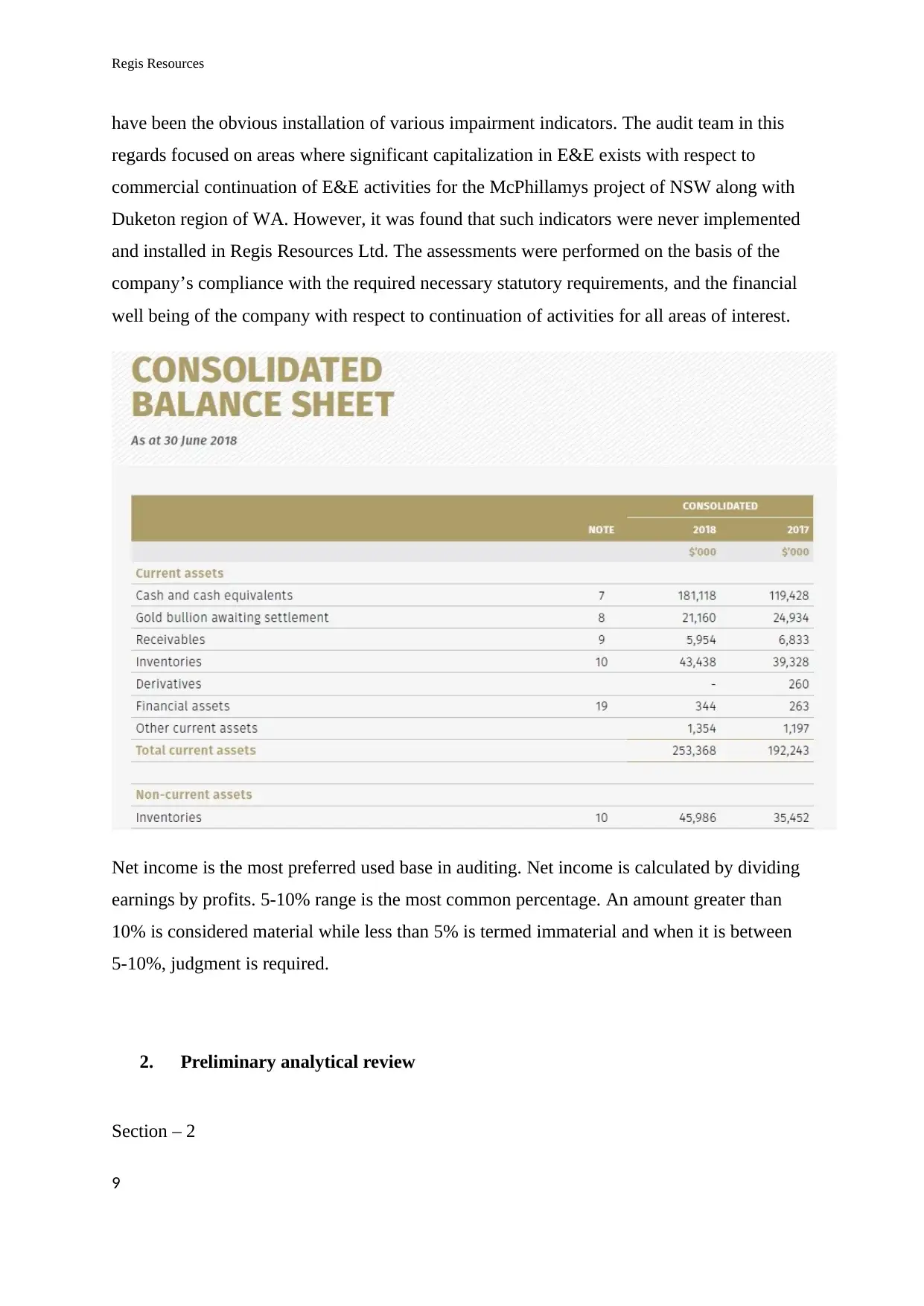

have been the obvious installation of various impairment indicators. The audit team in this

regards focused on areas where significant capitalization in E&E exists with respect to

commercial continuation of E&E activities for the McPhillamys project of NSW along with

Duketon region of WA. However, it was found that such indicators were never implemented

and installed in Regis Resources Ltd. The assessments were performed on the basis of the

company’s compliance with the required necessary statutory requirements, and the financial

well being of the company with respect to continuation of activities for all areas of interest.

Net income is the most preferred used base in auditing. Net income is calculated by dividing

earnings by profits. 5-10% range is the most common percentage. An amount greater than

10% is considered material while less than 5% is termed immaterial and when it is between

5-10%, judgment is required.

2. Preliminary analytical review

Section – 2

9

have been the obvious installation of various impairment indicators. The audit team in this

regards focused on areas where significant capitalization in E&E exists with respect to

commercial continuation of E&E activities for the McPhillamys project of NSW along with

Duketon region of WA. However, it was found that such indicators were never implemented

and installed in Regis Resources Ltd. The assessments were performed on the basis of the

company’s compliance with the required necessary statutory requirements, and the financial

well being of the company with respect to continuation of activities for all areas of interest.

Net income is the most preferred used base in auditing. Net income is calculated by dividing

earnings by profits. 5-10% range is the most common percentage. An amount greater than

10% is considered material while less than 5% is termed immaterial and when it is between

5-10%, judgment is required.

2. Preliminary analytical review

Section – 2

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Regis Resources

Current ratio is a very significant tool as it helps in ascertaining the short term liquidity

position of an organization. Current ratio is a comparison between an organization’s current

assets to its current liabilities. It is one such liquidity ratio that evaluates the ability of an

organization to tackle its short term obligations. In short, current ratio is used to analyse

whether the resources available with the company at present are sufficient enough so as to

overcome its short-term debts (Venanci, 2012).

Regis was unable to perform as per the industry standards in the previous year and therefore,

the company is looking to make amendments for the same in the current year. The company

highly aims at increasing its current ratio in the current year by means of increasing its sales

and reducing its levels of inventories and accounts receivables. The company must improve

its cash flow position along with its current assets and current liabilities so as to uplift its

performance in the ongoing year and meet its current goals. The company’s current ratio has

seemingly improved to 3.7 from 3.6 in the year 2018. The current ratio of the company

depicts a lower level of risk.

Quick ratio

Quick ratios are also known as liquidity ratios or acid test ratios. It is the comparison of a

company’s liquid assets to its liquid liabilities. Through quick ratios it becomes easier to

measure the ability of a business to tackle its short term debt obligations by means of its

liquid assets that is assets that can be easily converted into cash. The quick ratio of the

company is seemed to have improved in 2018. This means that the liquid assets of the

company have increased in comparison to the liquid liabilities of the same. It is the

responsibility of the auditor to ensure whether the improvement in the current ratio and quick

ratio of Regis is on the basis of rise in cash and cash equivalents and not because of the

growth in its debtors. Nevertheless, it should also be noted that the level of risk here is

relatively lower or may be a little moderate (Gay & Simnet, 2012).

Debt equity ratio

The debt to equity ratio is a leverage ratio. It is a comparison between an organization’s

overall liabilities to its total equity. The debt held for every 1 unit of equity in an organization

is ascertained by means of debt to equity ratio. The industry average for a standard debt to

equity ratio is 0.5 times while the same for Regis is 0.29 times. This means that there is a rise

10

Current ratio is a very significant tool as it helps in ascertaining the short term liquidity

position of an organization. Current ratio is a comparison between an organization’s current

assets to its current liabilities. It is one such liquidity ratio that evaluates the ability of an

organization to tackle its short term obligations. In short, current ratio is used to analyse

whether the resources available with the company at present are sufficient enough so as to

overcome its short-term debts (Venanci, 2012).

Regis was unable to perform as per the industry standards in the previous year and therefore,

the company is looking to make amendments for the same in the current year. The company

highly aims at increasing its current ratio in the current year by means of increasing its sales

and reducing its levels of inventories and accounts receivables. The company must improve

its cash flow position along with its current assets and current liabilities so as to uplift its

performance in the ongoing year and meet its current goals. The company’s current ratio has

seemingly improved to 3.7 from 3.6 in the year 2018. The current ratio of the company

depicts a lower level of risk.

Quick ratio

Quick ratios are also known as liquidity ratios or acid test ratios. It is the comparison of a

company’s liquid assets to its liquid liabilities. Through quick ratios it becomes easier to

measure the ability of a business to tackle its short term debt obligations by means of its

liquid assets that is assets that can be easily converted into cash. The quick ratio of the

company is seemed to have improved in 2018. This means that the liquid assets of the

company have increased in comparison to the liquid liabilities of the same. It is the

responsibility of the auditor to ensure whether the improvement in the current ratio and quick

ratio of Regis is on the basis of rise in cash and cash equivalents and not because of the

growth in its debtors. Nevertheless, it should also be noted that the level of risk here is

relatively lower or may be a little moderate (Gay & Simnet, 2012).

Debt equity ratio

The debt to equity ratio is a leverage ratio. It is a comparison between an organization’s

overall liabilities to its total equity. The debt held for every 1 unit of equity in an organization

is ascertained by means of debt to equity ratio. The industry average for a standard debt to

equity ratio is 0.5 times while the same for Regis is 0.29 times. This means that there is a rise

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Regis Resources

in overall debts and the same has exceeded the overall shareholders funds. The auditor must

focus on the company’s debt equity ratio and look for reasons behind the fall in the same and

suggest measures in order to make necessary rectifications. Underperforming debt to equity

ratio is a high risk area for the company (Niemi & Sundgren, 2012).

The assertions that can be followed are

Existence – this should be followed the auditor to know whether the asset or liability is

question is really present (Lapsley, 2012)

Right – whether the industry or any third party is involved in controlling rights of the asset or

liability

Occurrence – the disclosed events or transactions have link with the matter and pertain to the

entity.

3. Review of cash flow statement

2018 2017

Net cash from operating activities 2,59,727 2,06,082

Net cash used in investing activities -1,17,630 -1,04,782

Net cash used in financing activities -80,407 -81,407

As seen from the table that the net cash flow from operating activities provided the major

cash flow. The net cash inflow from operating activities increased in the year 2018 as

compared to 2017 owing to the fact that receipts from sale of goods was more. It needs to be

noted that the revenue brings in additional cash inflow for the company. For RRL, the

revenue was more followed by a marginal increment in the payment to the suppliers. The

receipt of interest was more and a marginal increment of income tax from ($36,230) in 2017

to ($36,868) in 2018 provided additional benefits to the company. Since the outflow was low

therefore the company was able to witness a major inflow of cash from this region.

On the other hand, the major cash outflows were witnessed from investing activities. As the

company purchased more plant, property and equipment there was a cash outflow in this area.

Further, there were payment in respect of the exploration, as well as acquisition of rent

refunds and payment, payment for acquisition pertaining to exploration of assets were the

11

in overall debts and the same has exceeded the overall shareholders funds. The auditor must

focus on the company’s debt equity ratio and look for reasons behind the fall in the same and

suggest measures in order to make necessary rectifications. Underperforming debt to equity

ratio is a high risk area for the company (Niemi & Sundgren, 2012).

The assertions that can be followed are

Existence – this should be followed the auditor to know whether the asset or liability is

question is really present (Lapsley, 2012)

Right – whether the industry or any third party is involved in controlling rights of the asset or

liability

Occurrence – the disclosed events or transactions have link with the matter and pertain to the

entity.

3. Review of cash flow statement

2018 2017

Net cash from operating activities 2,59,727 2,06,082

Net cash used in investing activities -1,17,630 -1,04,782

Net cash used in financing activities -80,407 -81,407

As seen from the table that the net cash flow from operating activities provided the major

cash flow. The net cash inflow from operating activities increased in the year 2018 as

compared to 2017 owing to the fact that receipts from sale of goods was more. It needs to be

noted that the revenue brings in additional cash inflow for the company. For RRL, the

revenue was more followed by a marginal increment in the payment to the suppliers. The

receipt of interest was more and a marginal increment of income tax from ($36,230) in 2017

to ($36,868) in 2018 provided additional benefits to the company. Since the outflow was low

therefore the company was able to witness a major inflow of cash from this region.

On the other hand, the major cash outflows were witnessed from investing activities. As the

company purchased more plant, property and equipment there was a cash outflow in this area.

Further, there were payment in respect of the exploration, as well as acquisition of rent

refunds and payment, payment for acquisition pertaining to exploration of assets were the

11

Regis Resources

main reason of outflow (Kaplan, 2011). Furthermore, payments were made for intangible

assets and the same lead to more cash outflows. Net cash was used in investing activities and

hence the figure increased from -1,04,782 in 2017 to -1,17,630 in 2018.

The primary cash receipts were mainly from the sale of gold, proceeds from the sale of

shares, receipt of interest income.

The primary cash outflow was seen in the area of payments to suppliers, payment of interest,

payment in investing activities, payment for mine activities, etc.

In the case of Regis Resources there was no presence of the non cash financial and investing

activities. Conversely, it states that the entity will not be allowed to stop the operations under

any scenario. As per the cash flow, a declaration can be made that the business does not have

the intention nor the requirement to liquidate the business (Fazal, 2013). Hence, from the

cash flow statement it is imperative that there is no foreseeable situation that will led to the

curtailment of the operations (Lapsley, 2012). The business is meeting the obligations as and

when it is due hence, the financial stability of the business is strong. The cash flow from

operating activities is strong and increased as compared to 2017. Moreover, the company’s

investing activities tend to be strong while financing activities projects that the finance has

been used. There is no risk or danger that will put the going concern of the company into

problem hence no adequate measure or step in this scenario is needed (Matthew, 2015).

An unqualified opinion was provided by the auditors since there as no problem pertaining to

the company. Performing an audit in accordance with AAS might not always trace material

misstatements even in the existence of the same. Misstatements can either be intentional or

unintentional or sometimes both (Merchant, 2012). Misstatements can be construed as

material if it impacts the investments related decisions of the investors based on the financials

of the company (Kaplan, 2011).

12

main reason of outflow (Kaplan, 2011). Furthermore, payments were made for intangible

assets and the same lead to more cash outflows. Net cash was used in investing activities and

hence the figure increased from -1,04,782 in 2017 to -1,17,630 in 2018.

The primary cash receipts were mainly from the sale of gold, proceeds from the sale of

shares, receipt of interest income.

The primary cash outflow was seen in the area of payments to suppliers, payment of interest,

payment in investing activities, payment for mine activities, etc.

In the case of Regis Resources there was no presence of the non cash financial and investing

activities. Conversely, it states that the entity will not be allowed to stop the operations under

any scenario. As per the cash flow, a declaration can be made that the business does not have

the intention nor the requirement to liquidate the business (Fazal, 2013). Hence, from the

cash flow statement it is imperative that there is no foreseeable situation that will led to the

curtailment of the operations (Lapsley, 2012). The business is meeting the obligations as and

when it is due hence, the financial stability of the business is strong. The cash flow from

operating activities is strong and increased as compared to 2017. Moreover, the company’s

investing activities tend to be strong while financing activities projects that the finance has

been used. There is no risk or danger that will put the going concern of the company into

problem hence no adequate measure or step in this scenario is needed (Matthew, 2015).

An unqualified opinion was provided by the auditors since there as no problem pertaining to

the company. Performing an audit in accordance with AAS might not always trace material

misstatements even in the existence of the same. Misstatements can either be intentional or

unintentional or sometimes both (Merchant, 2012). Misstatements can be construed as

material if it impacts the investments related decisions of the investors based on the financials

of the company (Kaplan, 2011).

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.