Financial Econometrics: Regression Modeling of Greece's Economy Data

VerifiedAdded on 2023/03/24

|20

|4230

|84

Report

AI Summary

This report delves into the application of financial econometrics to analyze the Greek economy, focusing on national income and inflation rates. It employs regression models and various tests, including Durbin-Watson (DW), Lagrange Multiplier (LM), and Ramsey RESET, to assess autocorrelation, specification errors, and heteroscedasticity. The report evaluates regression results using economic, statistical, and econometric criteria, suggesting improvements through data transformation and polynomial regression. It further discusses specific-to-general (S-G) and general-to-specific approaches in time series regression, addressing spurious regression. Finally, it explores the differences between conditional and unconditional variances and the application of ARCH and GARCH models, particularly in the context of bond returns. Desklib provides access to similar solved assignments and past papers for students.

FINANCIAL

ECONOMETRICS

ECONOMETRICS

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................4

QUESTION 1..................................................................................................................................4

1. Testing for autocorrelation by using Durbin-Watson (DW) and Lagrange Multiplier (LM)

tests..............................................................................................................................................5

2. Testing specification errors by using Ramsey Regression Equation Specification Error Test

(RESET)......................................................................................................................................7

3. Test for heteroscedasticity.......................................................................................................8

4. Evaluating regression results through using economic, statistical and econometric criteria...9

10

5. Explaining the manner in which regression results can be improved...................................10

QUESTION 2................................................................................................................................11

Presenting the attractiveness of specific-to-general (S-G) and general-to-specific approaches

related to time series regression models....................................................................................11

QUESTION 3................................................................................................................................11

i. Explaining the difference between the conditional variance and unconditional variance of r

...................................................................................................................................................11

ii. Outlining ARCH and GARCH models that helps in resolving problems.............................12

iii. Assessing the extent to which variance of 𝑒 affects the return on the bond and apply

GARCH model in this regard....................................................................................................12

iv. GARCH model and case.......................................................................................................12

QUESTION 4................................................................................................................................13

(a) Defining below mentioned aspects along with the suitable examples.................................13

i. Covariance Stationary.............................................................................................................13

ii. Trend Stationary....................................................................................................................13

INTRODUCTION...........................................................................................................................4

QUESTION 1..................................................................................................................................4

1. Testing for autocorrelation by using Durbin-Watson (DW) and Lagrange Multiplier (LM)

tests..............................................................................................................................................5

2. Testing specification errors by using Ramsey Regression Equation Specification Error Test

(RESET)......................................................................................................................................7

3. Test for heteroscedasticity.......................................................................................................8

4. Evaluating regression results through using economic, statistical and econometric criteria...9

10

5. Explaining the manner in which regression results can be improved...................................10

QUESTION 2................................................................................................................................11

Presenting the attractiveness of specific-to-general (S-G) and general-to-specific approaches

related to time series regression models....................................................................................11

QUESTION 3................................................................................................................................11

i. Explaining the difference between the conditional variance and unconditional variance of r

...................................................................................................................................................11

ii. Outlining ARCH and GARCH models that helps in resolving problems.............................12

iii. Assessing the extent to which variance of 𝑒 affects the return on the bond and apply

GARCH model in this regard....................................................................................................12

iv. GARCH model and case.......................................................................................................12

QUESTION 4................................................................................................................................13

(a) Defining below mentioned aspects along with the suitable examples.................................13

i. Covariance Stationary.............................................................................................................13

ii. Trend Stationary....................................................................................................................13

iii. Difference Stationary...........................................................................................................13

(b) Presenting decompositions relevant for trend stationary and stationary processes along

with its usefulness......................................................................................................................14

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................15

...................................................................................................................................................15

(b) Presenting decompositions relevant for trend stationary and stationary processes along

with its usefulness......................................................................................................................14

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................15

...................................................................................................................................................15

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Econometrics implies for the application of statistical and mathematical theories

pertaining to economics. Such tool as well as theoretical framework provides high level of

assistance in testing hypothesis and forecasting future trends. Field of econometrics lays high

level of emphasis on undertaking economic models and testing variables through the means of

statistical trial. Econometrics can be distinguished into two types such as theoretical and applied

which helps analyst in resolving specific issue. The present report will provide deeper insight

about the national income and inflationary trend of Greece. Further, on such data set Durbin-

Watson (DW), Lagrange Multiplier and Ramsey Regression Equation Specification Error Test

(RESET) will be applied to determine suitable outcome. Besides this, report will shed light on the

specific-to-general and general-to-specific approach which is associated with time series regression

model. It will describe the manner S-G and G-S approach helps in dealing with the issue of spurious

regression. Further, it also depicts the extent to which conditional as well as unconditional variances

differ from each other and thereby aid in decision making.

QUESTION 1

Years National income Rate of inflation

2004 237701914576.61 3.09

2005 248174203581.64 3.62

2006 268245507339.10 2.91

2007 310292161374.21 3.88

2008 343903324007.62 1.97

2009 322674845512.64 2.64

2010 293229174390.91 5.17

2011 279940194486.18 2.41

Econometrics implies for the application of statistical and mathematical theories

pertaining to economics. Such tool as well as theoretical framework provides high level of

assistance in testing hypothesis and forecasting future trends. Field of econometrics lays high

level of emphasis on undertaking economic models and testing variables through the means of

statistical trial. Econometrics can be distinguished into two types such as theoretical and applied

which helps analyst in resolving specific issue. The present report will provide deeper insight

about the national income and inflationary trend of Greece. Further, on such data set Durbin-

Watson (DW), Lagrange Multiplier and Ramsey Regression Equation Specification Error Test

(RESET) will be applied to determine suitable outcome. Besides this, report will shed light on the

specific-to-general and general-to-specific approach which is associated with time series regression

model. It will describe the manner S-G and G-S approach helps in dealing with the issue of spurious

regression. Further, it also depicts the extent to which conditional as well as unconditional variances

differ from each other and thereby aid in decision making.

QUESTION 1

Years National income Rate of inflation

2004 237701914576.61 3.09

2005 248174203581.64 3.62

2006 268245507339.10 2.91

2007 310292161374.21 3.88

2008 343903324007.62 1.97

2009 322674845512.64 2.64

2010 293229174390.91 5.17

2011 279940194486.18 2.41

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2012 247300884461.34 0.80

2013 239573179546.78 -1.71

2014 236599180334.16 -2.61

2015 195528679024.14 -0.17

2016 195338356749.17 (National income

of Greece, 2017)

0.02 (Inflationary trend of

Greece, 2017)

1. Testing for autocorrelation by using Durbin-Watson (DW) and Lagrange Multiplier (LM) tests

Variables Entered/Removeda

Model Variables Entered Variables

Removed

Method

1 Inflateb . Enter

a. Dependent Variable: NI

b. All requested variables entered.

Model Summaryb

Model R R Square Adjusted R Square Std. Error of the

Estimate

Durbin-Watson

1 .683a .467 .418 33991.84402 .794

a. Predictors: (Constant), Inflate

b. Dependent Variable: NI

ANOVAa

Model Sum of Squares df Mean Square F Sig.

1

Regression 11130993649.311 1 11130993649.311 9.634 .010b

Residual 12709900062.408 11 1155445460.219

Total 23840893711.720 12

a. Dependent Variable: NI

b. Predictors: (Constant), Inflate

2013 239573179546.78 -1.71

2014 236599180334.16 -2.61

2015 195528679024.14 -0.17

2016 195338356749.17 (National income

of Greece, 2017)

0.02 (Inflationary trend of

Greece, 2017)

1. Testing for autocorrelation by using Durbin-Watson (DW) and Lagrange Multiplier (LM) tests

Variables Entered/Removeda

Model Variables Entered Variables

Removed

Method

1 Inflateb . Enter

a. Dependent Variable: NI

b. All requested variables entered.

Model Summaryb

Model R R Square Adjusted R Square Std. Error of the

Estimate

Durbin-Watson

1 .683a .467 .418 33991.84402 .794

a. Predictors: (Constant), Inflate

b. Dependent Variable: NI

ANOVAa

Model Sum of Squares df Mean Square F Sig.

1

Regression 11130993649.311 1 11130993649.311 9.634 .010b

Residual 12709900062.408 11 1155445460.219

Total 23840893711.720 12

a. Dependent Variable: NI

b. Predictors: (Constant), Inflate

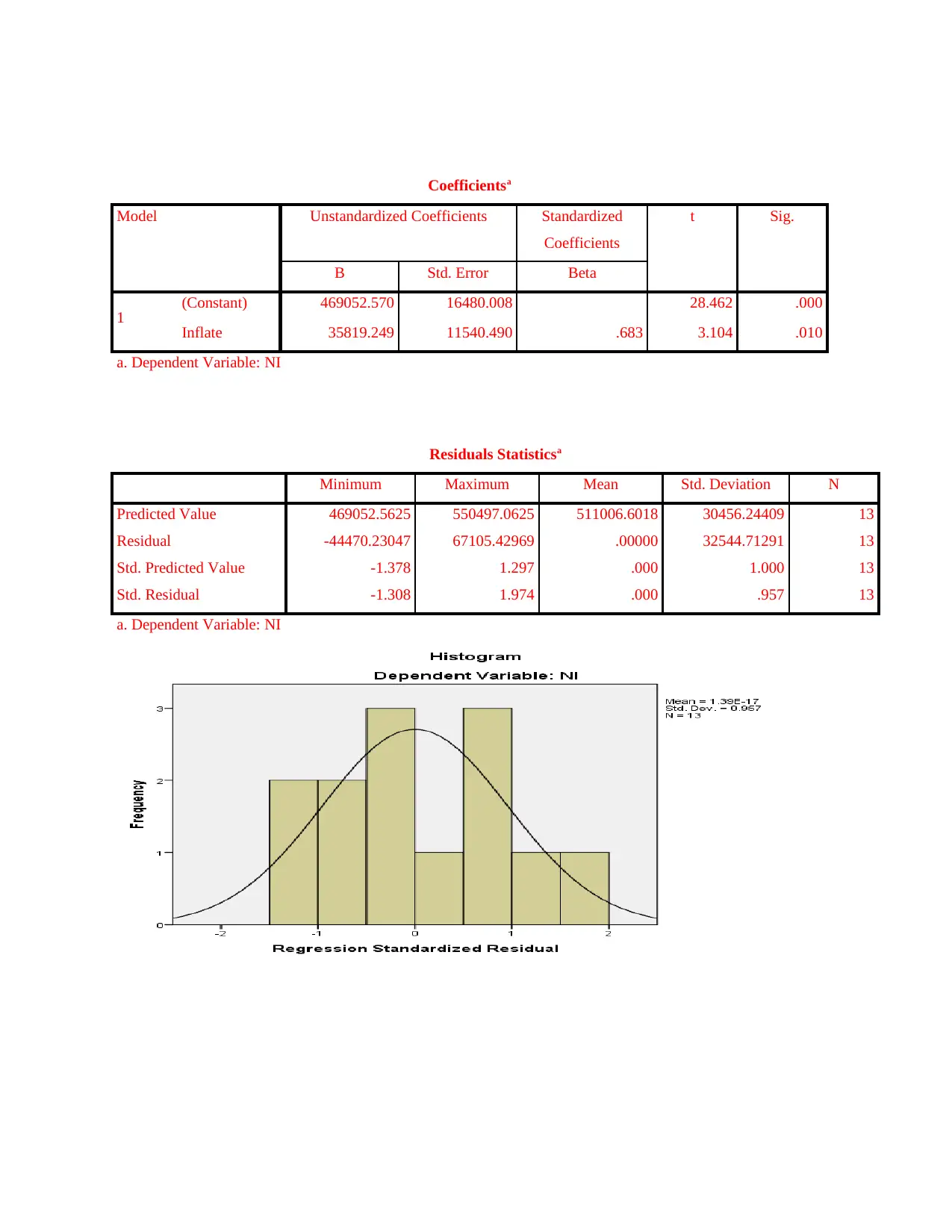

Coefficientsa

Model Unstandardized Coefficients Standardized

Coefficients

t Sig.

B Std. Error Beta

1 (Constant) 469052.570 16480.008 28.462 .000

Inflate 35819.249 11540.490 .683 3.104 .010

a. Dependent Variable: NI

Residuals Statisticsa

Minimum Maximum Mean Std. Deviation N

Predicted Value 469052.5625 550497.0625 511006.6018 30456.24409 13

Residual -44470.23047 67105.42969 .00000 32544.71291 13

Std. Predicted Value -1.378 1.297 .000 1.000 13

Std. Residual -1.308 1.974 .000 .957 13

a. Dependent Variable: NI

Model Unstandardized Coefficients Standardized

Coefficients

t Sig.

B Std. Error Beta

1 (Constant) 469052.570 16480.008 28.462 .000

Inflate 35819.249 11540.490 .683 3.104 .010

a. Dependent Variable: NI

Residuals Statisticsa

Minimum Maximum Mean Std. Deviation N

Predicted Value 469052.5625 550497.0625 511006.6018 30456.24409 13

Residual -44470.23047 67105.42969 .00000 32544.71291 13

Std. Predicted Value -1.378 1.297 .000 1.000 13

Std. Residual -1.308 1.974 .000 .957 13

a. Dependent Variable: NI

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

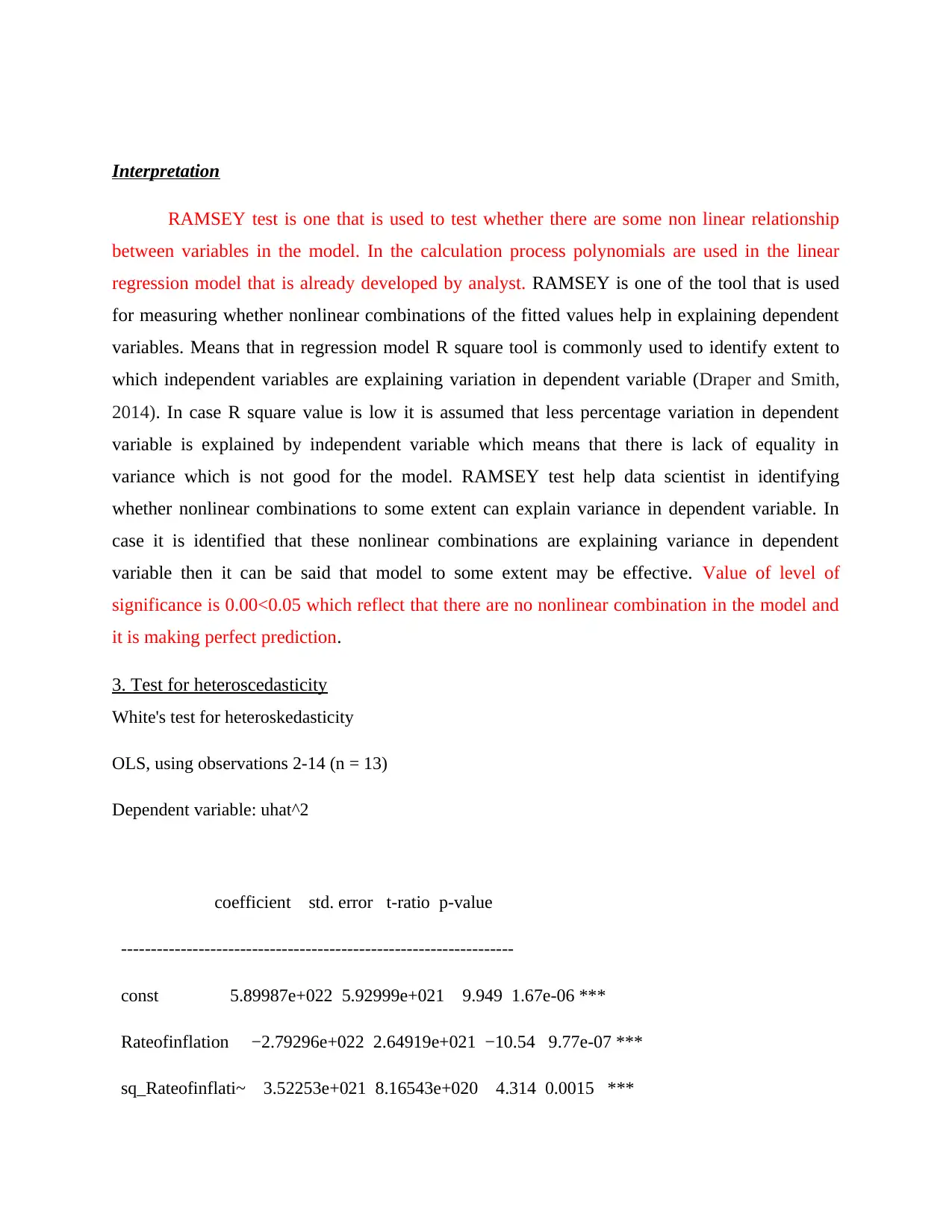

2. Testing specification errors by using Ramsey Regression Equation Specification Error Test

(RESET)

Auxiliary regression for RESET specification test

OLS, using observations 2-14 (n = 13)

Dependent variable: Nationalincome

coefficient std. error t-ratio p-value

-----------------------------------------------------------------

Rateofinflation 4.84836e+010 2.77494e+010 1.747 0.1112

yhat^2 9.74445e-012 2.35922e-012 4.130 0.0020 ***

yhat^3 0.00000 0.00000 −3.166 0.0101 **

Test statistic: F = 8.536954,

with p-value = P(F(2,10) > 8.53695) = 0.00687

(RESET)

Auxiliary regression for RESET specification test

OLS, using observations 2-14 (n = 13)

Dependent variable: Nationalincome

coefficient std. error t-ratio p-value

-----------------------------------------------------------------

Rateofinflation 4.84836e+010 2.77494e+010 1.747 0.1112

yhat^2 9.74445e-012 2.35922e-012 4.130 0.0020 ***

yhat^3 0.00000 0.00000 −3.166 0.0101 **

Test statistic: F = 8.536954,

with p-value = P(F(2,10) > 8.53695) = 0.00687

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Interpretation

RAMSEY test is one that is used to test whether there are some non linear relationship

between variables in the model. In the calculation process polynomials are used in the linear

regression model that is already developed by analyst. RAMSEY is one of the tool that is used

for measuring whether nonlinear combinations of the fitted values help in explaining dependent

variables. Means that in regression model R square tool is commonly used to identify extent to

which independent variables are explaining variation in dependent variable (Draper and Smith,

2014). In case R square value is low it is assumed that less percentage variation in dependent

variable is explained by independent variable which means that there is lack of equality in

variance which is not good for the model. RAMSEY test help data scientist in identifying

whether nonlinear combinations to some extent can explain variance in dependent variable. In

case it is identified that these nonlinear combinations are explaining variance in dependent

variable then it can be said that model to some extent may be effective. Value of level of

significance is 0.00<0.05 which reflect that there are no nonlinear combination in the model and

it is making perfect prediction.

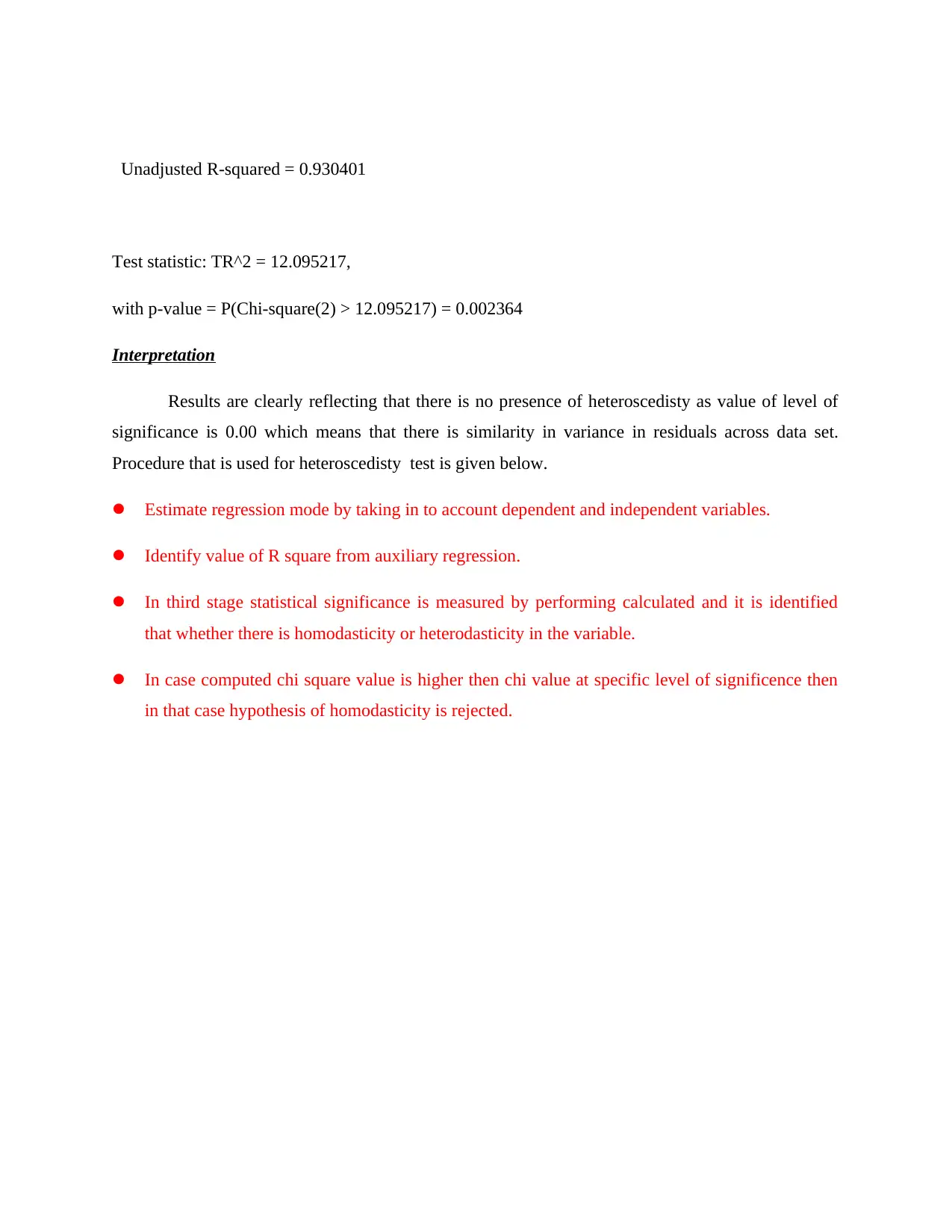

3. Test for heteroscedasticity

White's test for heteroskedasticity

OLS, using observations 2-14 (n = 13)

Dependent variable: uhat^2

coefficient std. error t-ratio p-value

------------------------------------------------------------------

const 5.89987e+022 5.92999e+021 9.949 1.67e-06 ***

Rateofinflation −2.79296e+022 2.64919e+021 −10.54 9.77e-07 ***

sq_Rateofinflati~ 3.52253e+021 8.16543e+020 4.314 0.0015 ***

RAMSEY test is one that is used to test whether there are some non linear relationship

between variables in the model. In the calculation process polynomials are used in the linear

regression model that is already developed by analyst. RAMSEY is one of the tool that is used

for measuring whether nonlinear combinations of the fitted values help in explaining dependent

variables. Means that in regression model R square tool is commonly used to identify extent to

which independent variables are explaining variation in dependent variable (Draper and Smith,

2014). In case R square value is low it is assumed that less percentage variation in dependent

variable is explained by independent variable which means that there is lack of equality in

variance which is not good for the model. RAMSEY test help data scientist in identifying

whether nonlinear combinations to some extent can explain variance in dependent variable. In

case it is identified that these nonlinear combinations are explaining variance in dependent

variable then it can be said that model to some extent may be effective. Value of level of

significance is 0.00<0.05 which reflect that there are no nonlinear combination in the model and

it is making perfect prediction.

3. Test for heteroscedasticity

White's test for heteroskedasticity

OLS, using observations 2-14 (n = 13)

Dependent variable: uhat^2

coefficient std. error t-ratio p-value

------------------------------------------------------------------

const 5.89987e+022 5.92999e+021 9.949 1.67e-06 ***

Rateofinflation −2.79296e+022 2.64919e+021 −10.54 9.77e-07 ***

sq_Rateofinflati~ 3.52253e+021 8.16543e+020 4.314 0.0015 ***

Unadjusted R-squared = 0.930401

Test statistic: TR^2 = 12.095217,

with p-value = P(Chi-square(2) > 12.095217) = 0.002364

Interpretation

Results are clearly reflecting that there is no presence of heteroscedisty as value of level of

significance is 0.00 which means that there is similarity in variance in residuals across data set.

Procedure that is used for heteroscedisty test is given below.

Estimate regression mode by taking in to account dependent and independent variables.

Identify value of R square from auxiliary regression.

In third stage statistical significance is measured by performing calculated and it is identified

that whether there is homodasticity or heterodasticity in the variable.

In case computed chi square value is higher then chi value at specific level of significence then

in that case hypothesis of homodasticity is rejected.

Test statistic: TR^2 = 12.095217,

with p-value = P(Chi-square(2) > 12.095217) = 0.002364

Interpretation

Results are clearly reflecting that there is no presence of heteroscedisty as value of level of

significance is 0.00 which means that there is similarity in variance in residuals across data set.

Procedure that is used for heteroscedisty test is given below.

Estimate regression mode by taking in to account dependent and independent variables.

Identify value of R square from auxiliary regression.

In third stage statistical significance is measured by performing calculated and it is identified

that whether there is homodasticity or heterodasticity in the variable.

In case computed chi square value is higher then chi value at specific level of significence then

in that case hypothesis of homodasticity is rejected.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

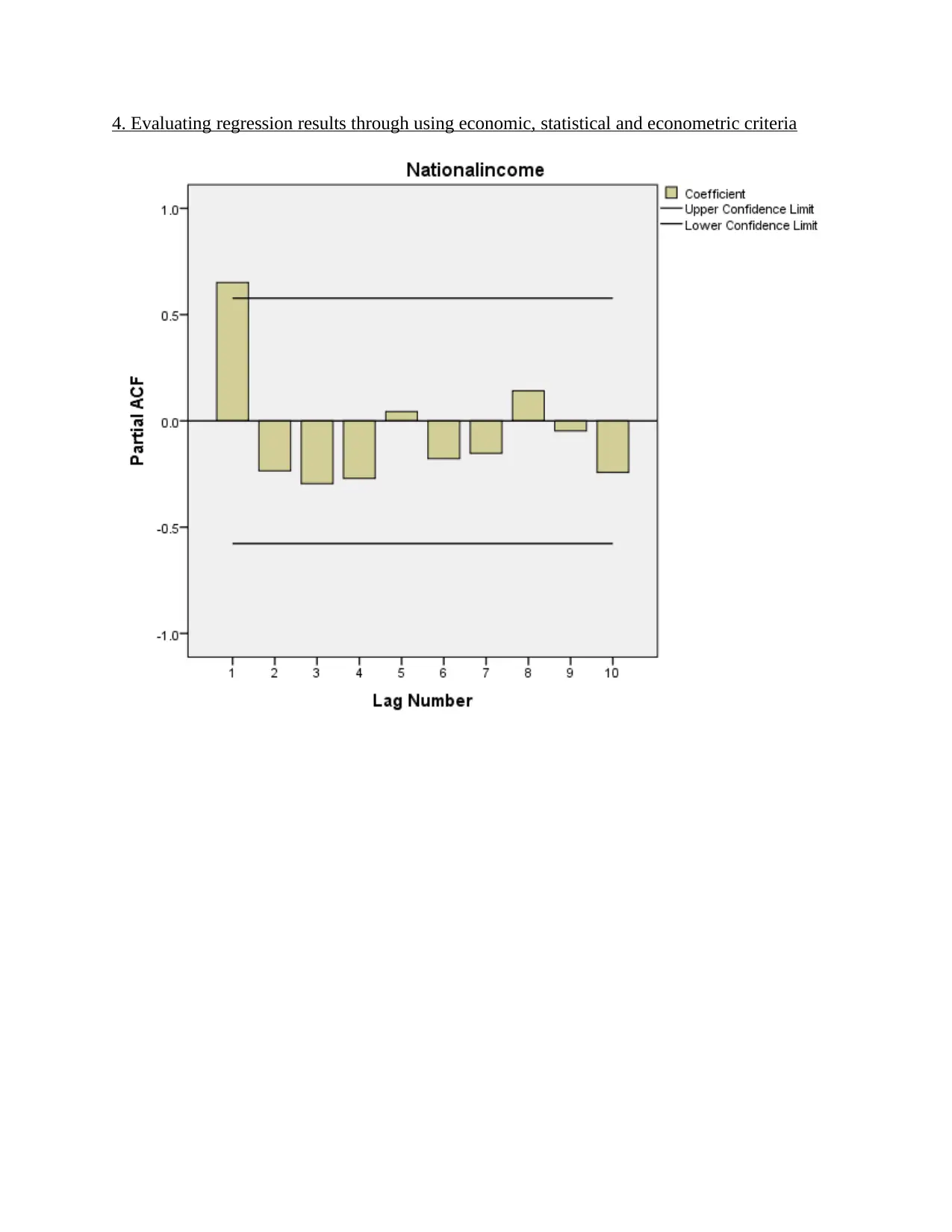

4. Evaluating regression results through using economic, statistical and econometric criteria

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

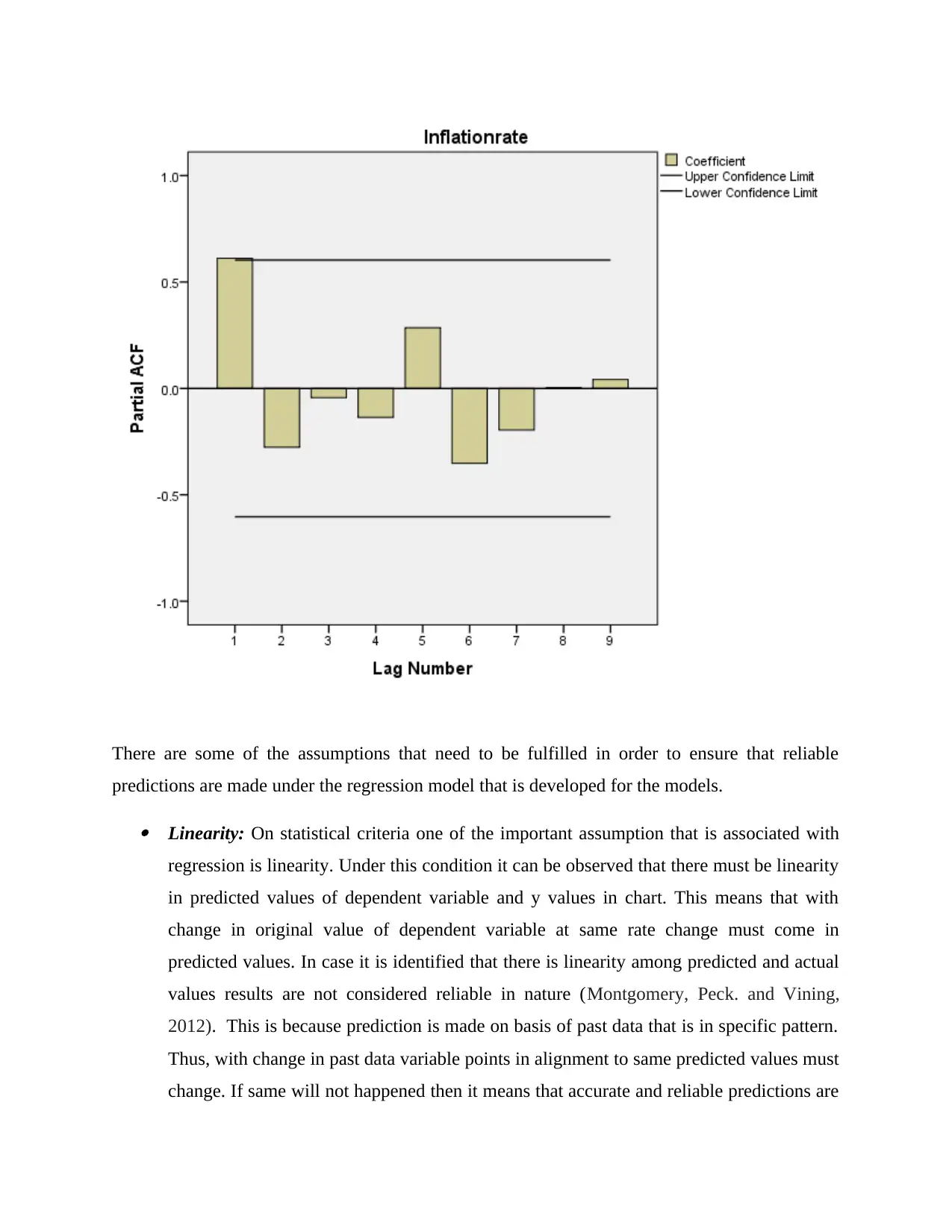

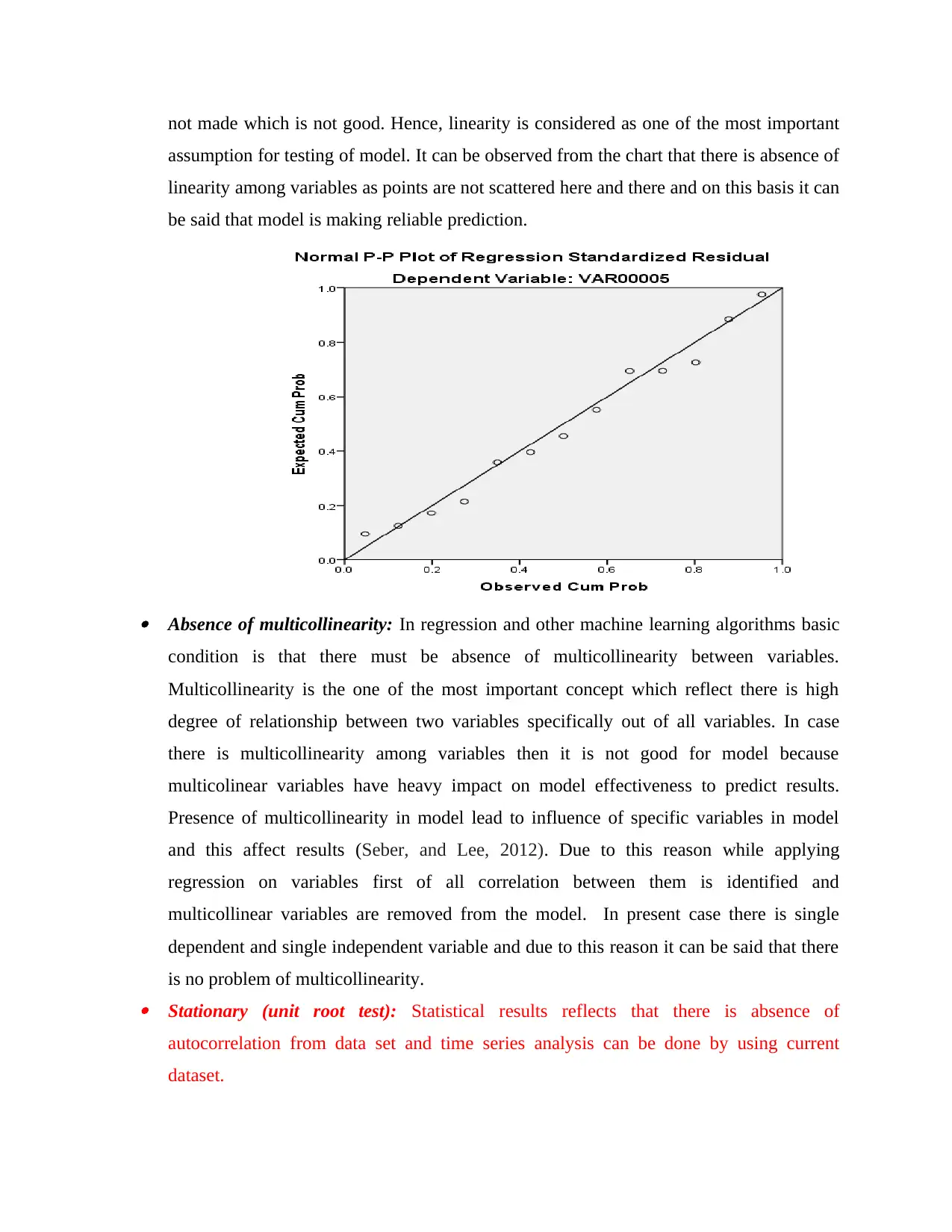

There are some of the assumptions that need to be fulfilled in order to ensure that reliable

predictions are made under the regression model that is developed for the models.

Linearity: On statistical criteria one of the important assumption that is associated with

regression is linearity. Under this condition it can be observed that there must be linearity

in predicted values of dependent variable and y values in chart. This means that with

change in original value of dependent variable at same rate change must come in

predicted values. In case it is identified that there is linearity among predicted and actual

values results are not considered reliable in nature (Montgomery, Peck. and Vining,

2012). This is because prediction is made on basis of past data that is in specific pattern.

Thus, with change in past data variable points in alignment to same predicted values must

change. If same will not happened then it means that accurate and reliable predictions are

predictions are made under the regression model that is developed for the models.

Linearity: On statistical criteria one of the important assumption that is associated with

regression is linearity. Under this condition it can be observed that there must be linearity

in predicted values of dependent variable and y values in chart. This means that with

change in original value of dependent variable at same rate change must come in

predicted values. In case it is identified that there is linearity among predicted and actual

values results are not considered reliable in nature (Montgomery, Peck. and Vining,

2012). This is because prediction is made on basis of past data that is in specific pattern.

Thus, with change in past data variable points in alignment to same predicted values must

change. If same will not happened then it means that accurate and reliable predictions are

not made which is not good. Hence, linearity is considered as one of the most important

assumption for testing of model. It can be observed from the chart that there is absence of

linearity among variables as points are not scattered here and there and on this basis it can

be said that model is making reliable prediction.

Absence of multicollinearity: In regression and other machine learning algorithms basic

condition is that there must be absence of multicollinearity between variables.

Multicollinearity is the one of the most important concept which reflect there is high

degree of relationship between two variables specifically out of all variables. In case

there is multicollinearity among variables then it is not good for model because

multicolinear variables have heavy impact on model effectiveness to predict results.

Presence of multicollinearity in model lead to influence of specific variables in model

and this affect results (Seber, and Lee, 2012). Due to this reason while applying

regression on variables first of all correlation between them is identified and

multicollinear variables are removed from the model. In present case there is single

dependent and single independent variable and due to this reason it can be said that there

is no problem of multicollinearity. Stationary (unit root test): Statistical results reflects that there is absence of

autocorrelation from data set and time series analysis can be done by using current

dataset.

assumption for testing of model. It can be observed from the chart that there is absence of

linearity among variables as points are not scattered here and there and on this basis it can

be said that model is making reliable prediction.

Absence of multicollinearity: In regression and other machine learning algorithms basic

condition is that there must be absence of multicollinearity between variables.

Multicollinearity is the one of the most important concept which reflect there is high

degree of relationship between two variables specifically out of all variables. In case

there is multicollinearity among variables then it is not good for model because

multicolinear variables have heavy impact on model effectiveness to predict results.

Presence of multicollinearity in model lead to influence of specific variables in model

and this affect results (Seber, and Lee, 2012). Due to this reason while applying

regression on variables first of all correlation between them is identified and

multicollinear variables are removed from the model. In present case there is single

dependent and single independent variable and due to this reason it can be said that there

is no problem of multicollinearity. Stationary (unit root test): Statistical results reflects that there is absence of

autocorrelation from data set and time series analysis can be done by using current

dataset.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.