REITS Analysis Report

VerifiedAdded on 2020/03/16

|24

|4284

|284

Report

AI Summary

This report provides a comprehensive analysis of two major Australian real estate investment trusts (REITS), Goodman Group and Mirvac Group. It evaluates their business summaries, property portfolios, historical share performances, financial performances, and profitability metrics. The report also includes market commentary and a comparison of key statistics, highlighting the strengths and weaknesses of each group. Recommendations for investors are provided based on the findings.

REITS

Name of the Student:

Name of the University:

Authors note:

Name of the Student:

Name of the University:

Authors note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Introduction:...............................................................................................................................2

Goodman Group:........................................................................................................................3

Business Summary:................................................................................................................3

Property Portfolio:..................................................................................................................4

Historic Share Performance:..................................................................................................4

Financial Performance:..........................................................................................................6

Profitability:...........................................................................................................................8

MIRVAC Group.........................................................................................................................9

Business summary:...............................................................................................................10

Property Portfolio:................................................................................................................11

Share Performance:..............................................................................................................16

Financial Performance:........................................................................................................17

Profitability:.........................................................................................................................19

Market Commentary................................................................................................................20

General Market Commentary:..............................................................................................20

Retail and Office Market:.....................................................................................................20

Industrial Market:.................................................................................................................20

Comparison:.........................................................................................................................21

Risks:....................................................................................................................................21

Reference..................................................................................................................................23

Introduction:...............................................................................................................................2

Goodman Group:........................................................................................................................3

Business Summary:................................................................................................................3

Property Portfolio:..................................................................................................................4

Historic Share Performance:..................................................................................................4

Financial Performance:..........................................................................................................6

Profitability:...........................................................................................................................8

MIRVAC Group.........................................................................................................................9

Business summary:...............................................................................................................10

Property Portfolio:................................................................................................................11

Share Performance:..............................................................................................................16

Financial Performance:........................................................................................................17

Profitability:.........................................................................................................................19

Market Commentary................................................................................................................20

General Market Commentary:..............................................................................................20

Retail and Office Market:.....................................................................................................20

Industrial Market:.................................................................................................................20

Comparison:.........................................................................................................................21

Risks:....................................................................................................................................21

Reference..................................................................................................................................23

Introduction:

In this report, an effort has been made to compare and evaluate the activities and

performance of two Australia based real estate companies that are Mirvac Group and

Goodman Group. In this report discussion as well as evaluation regarding several aspects of

both the companies has been made which includes Business Summary, portfolio of the

company’s properties, historical performance of shares, financial information, profitability

and holding period return of both the companies (Afolayan 2017). On successful evaluation

of each of the following points as well as funds, a report has been prepared to facilitate

comparison between the two companies and to provide appropriate recommendations to the

investors and other important clients and peoples.

Goodman Group:

Business Summary:

Goodman Group is an Australia based real estate company that owns, manages and

develops business areas and industrial spaces of high and premium quality. According to the

current records, Goodman Group has over 161 established properties around Australia

location in different major cities like Adelaide, Brisbane, Melbourne, Perth and Sydney

(Brounen and de Koning 2013). The primary objective of this group is establishment of

secure and long-term relation with its client by providing services of premium quality backed

by incomparable standard. The blue-chip client database of Goodman Group includes a wide

In this report, an effort has been made to compare and evaluate the activities and

performance of two Australia based real estate companies that are Mirvac Group and

Goodman Group. In this report discussion as well as evaluation regarding several aspects of

both the companies has been made which includes Business Summary, portfolio of the

company’s properties, historical performance of shares, financial information, profitability

and holding period return of both the companies (Afolayan 2017). On successful evaluation

of each of the following points as well as funds, a report has been prepared to facilitate

comparison between the two companies and to provide appropriate recommendations to the

investors and other important clients and peoples.

Goodman Group:

Business Summary:

Goodman Group is an Australia based real estate company that owns, manages and

develops business areas and industrial spaces of high and premium quality. According to the

current records, Goodman Group has over 161 established properties around Australia

location in different major cities like Adelaide, Brisbane, Melbourne, Perth and Sydney

(Brounen and de Koning 2013). The primary objective of this group is establishment of

secure and long-term relation with its client by providing services of premium quality backed

by incomparable standard. The blue-chip client database of Goodman Group includes a wide

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

range of well-established and branded industries like Linfox, DHL, Coca-Cola, TNT,

Brambles and Toll.

An essential and important subsidiary of Goodman Group is Goodman Australia. In

the four unlisted property funds, i.e. Goodman Australia Industrial Partnership (GAIP),

Goodman Australia Partnership (GAP), Goodman Australia Development Partnership

(GADP) and KWASA-Goodman Industrial Partnership (KGIP), Goodman Group is a

cornerstone investor within Australia. The Goodman Australia team comprises of about 300

staffs who have a wide range of professional knowledge regarding Marketing and Finance,

Property, Development, Legal matters, etc. The contribution of all these members and staffs

is the secret behind the success of the entire Goodman Group.

Property Portfolio:

The significant properties of Goodman Australia are scattered all over Eastern and

South Australia’s major cities like Adelaide, Brisbane, Melbourne and Sydney. The group

has divided its entire property into four major categories which are In Adelaide the company

has a property that is under-construction named Corner Edinburgh Road and West Avenue

covering an area of 5000 to 80000 square metre (Hasan. and Sulaiman 2016).

Brambles and Toll.

An essential and important subsidiary of Goodman Group is Goodman Australia. In

the four unlisted property funds, i.e. Goodman Australia Industrial Partnership (GAIP),

Goodman Australia Partnership (GAP), Goodman Australia Development Partnership

(GADP) and KWASA-Goodman Industrial Partnership (KGIP), Goodman Group is a

cornerstone investor within Australia. The Goodman Australia team comprises of about 300

staffs who have a wide range of professional knowledge regarding Marketing and Finance,

Property, Development, Legal matters, etc. The contribution of all these members and staffs

is the secret behind the success of the entire Goodman Group.

Property Portfolio:

The significant properties of Goodman Australia are scattered all over Eastern and

South Australia’s major cities like Adelaide, Brisbane, Melbourne and Sydney. The group

has divided its entire property into four major categories which are In Adelaide the company

has a property that is under-construction named Corner Edinburgh Road and West Avenue

covering an area of 5000 to 80000 square metre (Hasan. and Sulaiman 2016).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

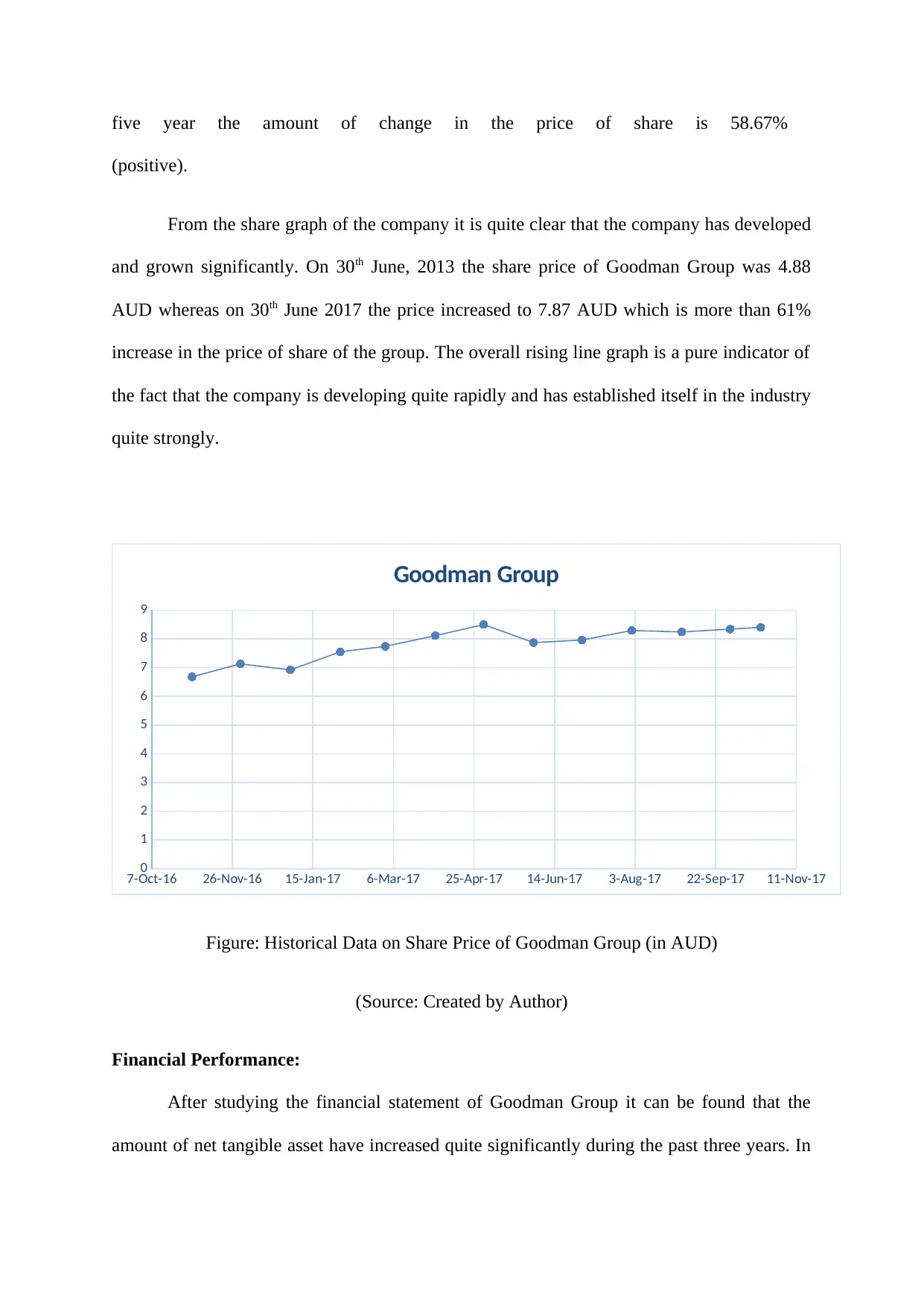

Historic Share Performance:

In this segment, a brief summary about the performance of Goodman Group in the

security market is being discussed. As far as the security market of the group is concerned,

quite decent ups and downs have been found in the share graph of Goodman group in the past

5 years. However, there was an overall increase in the price of the share of the company (Lee

et al. 2014). In 2013, the overall percentage change in the performance was 9.23% which has

increased to 16.40% in the year 2017 which is approximately 99.04% change in terms of 5

years.

Figure 1: Performance Report of Goodman Group.

(Source: Annual Report 2017)

At present the market capitalization of Goodman Group is 14,920.26 Million and the

total number of shares currently available in the market is 1,789.00 Million. During the last

In this segment, a brief summary about the performance of Goodman Group in the

security market is being discussed. As far as the security market of the group is concerned,

quite decent ups and downs have been found in the share graph of Goodman group in the past

5 years. However, there was an overall increase in the price of the share of the company (Lee

et al. 2014). In 2013, the overall percentage change in the performance was 9.23% which has

increased to 16.40% in the year 2017 which is approximately 99.04% change in terms of 5

years.

Figure 1: Performance Report of Goodman Group.

(Source: Annual Report 2017)

At present the market capitalization of Goodman Group is 14,920.26 Million and the

total number of shares currently available in the market is 1,789.00 Million. During the last

five year the amount of change in the price of share is 58.67%

(positive).

From the share graph of the company it is quite clear that the company has developed

and grown significantly. On 30th June, 2013 the share price of Goodman Group was 4.88

AUD whereas on 30th June 2017 the price increased to 7.87 AUD which is more than 61%

increase in the price of share of the group. The overall rising line graph is a pure indicator of

the fact that the company is developing quite rapidly and has established itself in the industry

quite strongly.

7-Oct-16 26-Nov-16 15-Jan-17 6-Mar-17 25-Apr-17 14-Jun-17 3-Aug-17 22-Sep-17 11-Nov-17

0

1

2

3

4

5

6

7

8

9

Goodman Group

Figure: Historical Data on Share Price of Goodman Group (in AUD)

(Source: Created by Author)

Financial Performance:

After studying the financial statement of Goodman Group it can be found that the

amount of net tangible asset have increased quite significantly during the past three years. In

(positive).

From the share graph of the company it is quite clear that the company has developed

and grown significantly. On 30th June, 2013 the share price of Goodman Group was 4.88

AUD whereas on 30th June 2017 the price increased to 7.87 AUD which is more than 61%

increase in the price of share of the group. The overall rising line graph is a pure indicator of

the fact that the company is developing quite rapidly and has established itself in the industry

quite strongly.

7-Oct-16 26-Nov-16 15-Jan-17 6-Mar-17 25-Apr-17 14-Jun-17 3-Aug-17 22-Sep-17 11-Nov-17

0

1

2

3

4

5

6

7

8

9

Goodman Group

Figure: Historical Data on Share Price of Goodman Group (in AUD)

(Source: Created by Author)

Financial Performance:

After studying the financial statement of Goodman Group it can be found that the

amount of net tangible asset have increased quite significantly during the past three years. In

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

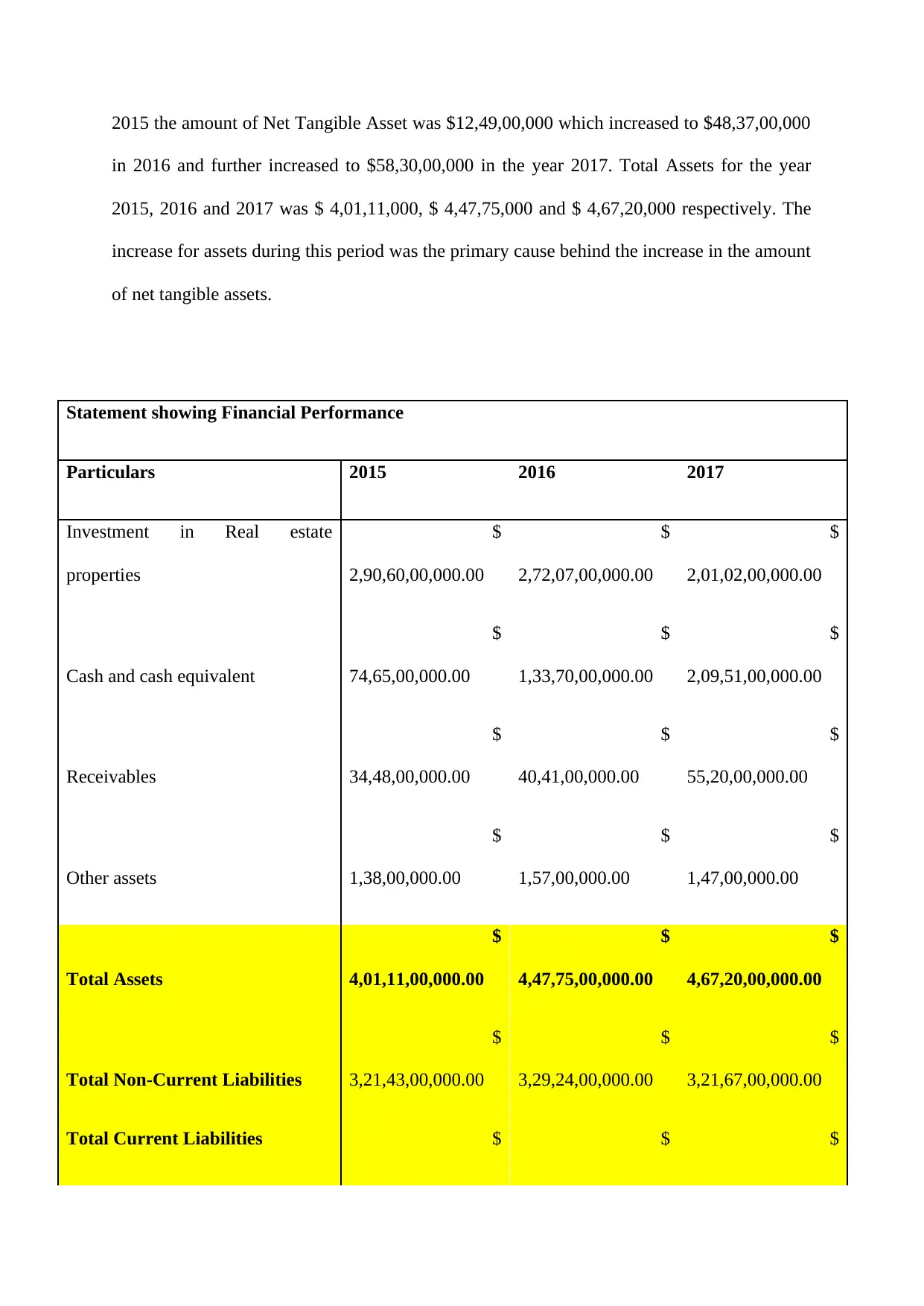

2015 the amount of Net Tangible Asset was $12,49,00,000 which increased to $48,37,00,000

in 2016 and further increased to $58,30,00,000 in the year 2017. Total Assets for the year

2015, 2016 and 2017 was $ 4,01,11,000, $ 4,47,75,000 and $ 4,67,20,000 respectively. The

increase for assets during this period was the primary cause behind the increase in the amount

of net tangible assets.

Statement showing Financial Performance

Particulars 2015 2016 2017

Investment in Real estate

properties

$

2,90,60,00,000.00

$

2,72,07,00,000.00

$

2,01,02,00,000.00

Cash and cash equivalent

$

74,65,00,000.00

$

1,33,70,00,000.00

$

2,09,51,00,000.00

Receivables

$

34,48,00,000.00

$

40,41,00,000.00

$

55,20,00,000.00

Other assets

$

1,38,00,000.00

$

1,57,00,000.00

$

1,47,00,000.00

Total Assets

$

4,01,11,00,000.00

$

4,47,75,00,000.00

$

4,67,20,00,000.00

Total Non-Current Liabilities

$

3,21,43,00,000.00

$

3,29,24,00,000.00

$

3,21,67,00,000.00

Total Current Liabilities $ $ $

in 2016 and further increased to $58,30,00,000 in the year 2017. Total Assets for the year

2015, 2016 and 2017 was $ 4,01,11,000, $ 4,47,75,000 and $ 4,67,20,000 respectively. The

increase for assets during this period was the primary cause behind the increase in the amount

of net tangible assets.

Statement showing Financial Performance

Particulars 2015 2016 2017

Investment in Real estate

properties

$

2,90,60,00,000.00

$

2,72,07,00,000.00

$

2,01,02,00,000.00

Cash and cash equivalent

$

74,65,00,000.00

$

1,33,70,00,000.00

$

2,09,51,00,000.00

Receivables

$

34,48,00,000.00

$

40,41,00,000.00

$

55,20,00,000.00

Other assets

$

1,38,00,000.00

$

1,57,00,000.00

$

1,47,00,000.00

Total Assets

$

4,01,11,00,000.00

$

4,47,75,00,000.00

$

4,67,20,00,000.00

Total Non-Current Liabilities

$

3,21,43,00,000.00

$

3,29,24,00,000.00

$

3,21,67,00,000.00

Total Current Liabilities $ $ $

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

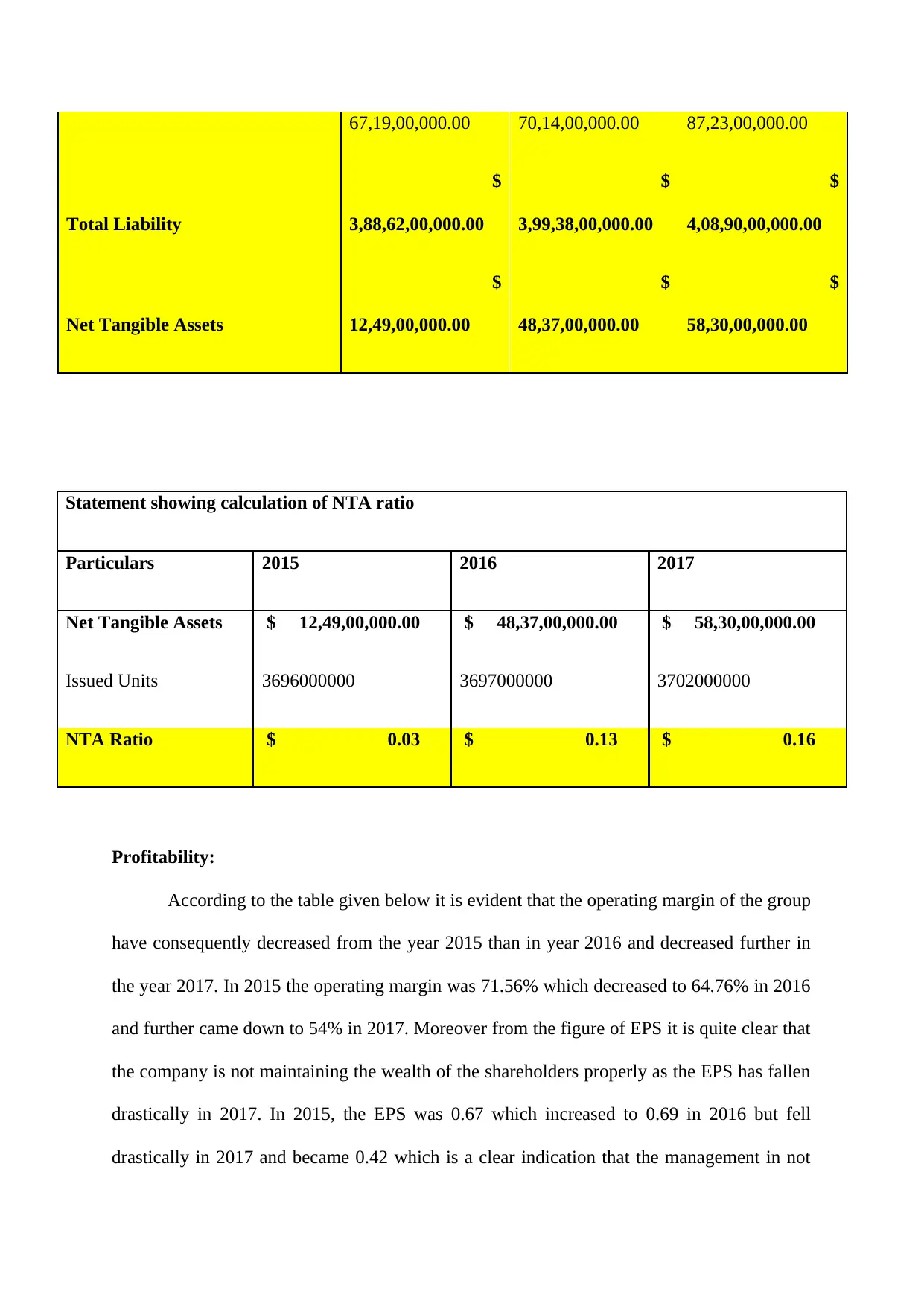

67,19,00,000.00 70,14,00,000.00 87,23,00,000.00

Total Liability

$

3,88,62,00,000.00

$

3,99,38,00,000.00

$

4,08,90,00,000.00

Net Tangible Assets

$

12,49,00,000.00

$

48,37,00,000.00

$

58,30,00,000.00

Statement showing calculation of NTA ratio

Particulars 2015 2016 2017

Net Tangible Assets $ 12,49,00,000.00 $ 48,37,00,000.00 $ 58,30,00,000.00

Issued Units 3696000000 3697000000 3702000000

NTA Ratio $ 0.03 $ 0.13 $ 0.16

Profitability:

According to the table given below it is evident that the operating margin of the group

have consequently decreased from the year 2015 than in year 2016 and decreased further in

the year 2017. In 2015 the operating margin was 71.56% which decreased to 64.76% in 2016

and further came down to 54% in 2017. Moreover from the figure of EPS it is quite clear that

the company is not maintaining the wealth of the shareholders properly as the EPS has fallen

drastically in 2017. In 2015, the EPS was 0.67 which increased to 0.69 in 2016 but fell

drastically in 2017 and became 0.42 which is a clear indication that the management in not

Total Liability

$

3,88,62,00,000.00

$

3,99,38,00,000.00

$

4,08,90,00,000.00

Net Tangible Assets

$

12,49,00,000.00

$

48,37,00,000.00

$

58,30,00,000.00

Statement showing calculation of NTA ratio

Particulars 2015 2016 2017

Net Tangible Assets $ 12,49,00,000.00 $ 48,37,00,000.00 $ 58,30,00,000.00

Issued Units 3696000000 3697000000 3702000000

NTA Ratio $ 0.03 $ 0.13 $ 0.16

Profitability:

According to the table given below it is evident that the operating margin of the group

have consequently decreased from the year 2015 than in year 2016 and decreased further in

the year 2017. In 2015 the operating margin was 71.56% which decreased to 64.76% in 2016

and further came down to 54% in 2017. Moreover from the figure of EPS it is quite clear that

the company is not maintaining the wealth of the shareholders properly as the EPS has fallen

drastically in 2017. In 2015, the EPS was 0.67 which increased to 0.69 in 2016 but fell

drastically in 2017 and became 0.42 which is a clear indication that the management in not

efficiently utilising shareholders wealth (O'Connell and Young 2017). Even there was a

decrease in return on equity from that of the previous year. The figures of return on capital

investment also shows negative results. Thus, it is very essential for the management of the

company to take immediate and correct action so that the company can make more profit in

the future years.

Statement showing Profitability Ratio

Particulars 2015 2016 2017

Gross Margin % 47.01 44.64 46.42

Operating Margin % 71.56 64.76 54

Earnings Per Share AUD 0.67 0.69 0.42

Book Value Per Share * AUD 3.37 3.96 4.51

Asset Turnover (Average) 0.12 0.15 0.14

Return on Equity % 18.65 16.86 9.51

Return on Invested Capital % 15.56 13.4 9.61

decrease in return on equity from that of the previous year. The figures of return on capital

investment also shows negative results. Thus, it is very essential for the management of the

company to take immediate and correct action so that the company can make more profit in

the future years.

Statement showing Profitability Ratio

Particulars 2015 2016 2017

Gross Margin % 47.01 44.64 46.42

Operating Margin % 71.56 64.76 54

Earnings Per Share AUD 0.67 0.69 0.42

Book Value Per Share * AUD 3.37 3.96 4.51

Asset Turnover (Average) 0.12 0.15 0.14

Return on Equity % 18.65 16.86 9.51

Return on Invested Capital % 15.56 13.4 9.61

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

MIRVAC Group

Business summary:

MIRVAC Group is a real estate investment trust (REIT) that as per the recent analysis

done by several organizations has stated that this is a sophisticated real estate investment,

improvement and investment administration group. This is one of the best and diversified

group that is engaged in the business if property of Australia. This group has its own

integrated asset administration capacity and expansion. This is traded in the name of ASX:

MGR as this is public form company. This is listed in Australian Stock Exchange (ASX) with

works in the sector of property development and investment field, as well as in the services

found in retail form (Dimovski 2016). This has its headquarters in Sydney in Australia as this

was established on 1972. This is one of the top groups in real estate business that has an

experience is more than forty years in this sector of business. MIRVAC group has a stapled

security system that composed of MIRVAC Limited and MIRVAC Property Trust (MPT).

The MIRVAC Limited composed of vital two sectors like development (MGR) and

investment (MPT) that involves both commercial and residential enhancements. MIRVAC

group functions in almost all over the region of Australia with the few overseas investments.

The improvement of the field of MIRVAC group (MGR) is composed of housing

Business summary:

MIRVAC Group is a real estate investment trust (REIT) that as per the recent analysis

done by several organizations has stated that this is a sophisticated real estate investment,

improvement and investment administration group. This is one of the best and diversified

group that is engaged in the business if property of Australia. This group has its own

integrated asset administration capacity and expansion. This is traded in the name of ASX:

MGR as this is public form company. This is listed in Australian Stock Exchange (ASX) with

works in the sector of property development and investment field, as well as in the services

found in retail form (Dimovski 2016). This has its headquarters in Sydney in Australia as this

was established on 1972. This is one of the top groups in real estate business that has an

experience is more than forty years in this sector of business. MIRVAC group has a stapled

security system that composed of MIRVAC Limited and MIRVAC Property Trust (MPT).

The MIRVAC Limited composed of vital two sectors like development (MGR) and

investment (MPT) that involves both commercial and residential enhancements. MIRVAC

group functions in almost all over the region of Australia with the few overseas investments.

The improvement of the field of MIRVAC group (MGR) is composed of housing

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

merchandises. The main businesses that this group operate are on retail property, property

and investments.

As critically observed that the enhancement of MIRVAC group’s division that

involves commercial merchandises and residential merchandises. As the MIRVAC is lead by

the enthusiastic John Mulcahy is the Chairman and Susan Lloyd-Hurwitz is the Managing

Director of MGR. This group is mainly centred in around the four cities of Australia is

Brisbane, Melbourne, Perth and Sydney (Zhou 2016). This group has owned and

administering all over the markets of industrial, retail and office fields that amounts to over a

$ 15 Billion of the assets under the title of the group. MIRVAC group’s tactics in urban has

given fruitful in Operating income has raised by 11% and distributions has risen by 5% as per

the earlier year. The Operating income in 2017 in case of retail was $ 156 Million, residential

was $ 302 Million and Industrial & Office was $ 319Million. In aggregate, the MGR had an

operating income before tax & interest was $ 750 Million. This huge profit is due to greater

understandings of the customers and our cities. The profit is $ 1.16 Billion that is due to

utilization of the property in sustainable manner in MIRVAC group (MGR).

Property Portfolio:

MIRVAC group (MGR) invests in industrial, hotel properties, commercial, retail

businesses all over Australia, and centred on high revenue assets and the tenant who are good

and investments.

As critically observed that the enhancement of MIRVAC group’s division that

involves commercial merchandises and residential merchandises. As the MIRVAC is lead by

the enthusiastic John Mulcahy is the Chairman and Susan Lloyd-Hurwitz is the Managing

Director of MGR. This group is mainly centred in around the four cities of Australia is

Brisbane, Melbourne, Perth and Sydney (Zhou 2016). This group has owned and

administering all over the markets of industrial, retail and office fields that amounts to over a

$ 15 Billion of the assets under the title of the group. MIRVAC group’s tactics in urban has

given fruitful in Operating income has raised by 11% and distributions has risen by 5% as per

the earlier year. The Operating income in 2017 in case of retail was $ 156 Million, residential

was $ 302 Million and Industrial & Office was $ 319Million. In aggregate, the MGR had an

operating income before tax & interest was $ 750 Million. This huge profit is due to greater

understandings of the customers and our cities. The profit is $ 1.16 Billion that is due to

utilization of the property in sustainable manner in MIRVAC group (MGR).

Property Portfolio:

MIRVAC group (MGR) invests in industrial, hotel properties, commercial, retail

businesses all over Australia, and centred on high revenue assets and the tenant who are good

makes it easier for agencies of the government and big firms. MGR keeps the assortment of

the present premium level assets as properly given below.

ASSET

TYPE

ASSET VALUE WALE

(years)

CAP

RATE

MAJOR TENANT

Retail

BIRKENHEAD

POINT OUTLET

CENTRE

DRUMMOYNE,

NSW

$ 374.9

Million

2.9 5.50% 100% MPT

Residential

WATERFRONT,

PIER PRECINCT,

NEWSTEAD

TERRACE

NEWSTEAD, QLD

(in progress)

$ 320.9

Million

(in

progress)

(in

progress)

(in

progress)

100% MWRDP

(in progress)

the present premium level assets as properly given below.

ASSET

TYPE

ASSET VALUE WALE

(years)

CAP

RATE

MAJOR TENANT

Retail

BIRKENHEAD

POINT OUTLET

CENTRE

DRUMMOYNE,

NSW

$ 374.9

Million

2.9 5.50% 100% MPT

Residential

WATERFRONT,

PIER PRECINCT,

NEWSTEAD

TERRACE

NEWSTEAD, QLD

(in progress)

$ 320.9

Million

(in

progress)

(in

progress)

(in

progress)

100% MWRDP

(in progress)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 24

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.