Financial Report: Relevant Cost Analysis, Budgeting, and Variances

VerifiedAdded on 2020/05/11

|5

|1556

|43

Report

AI Summary

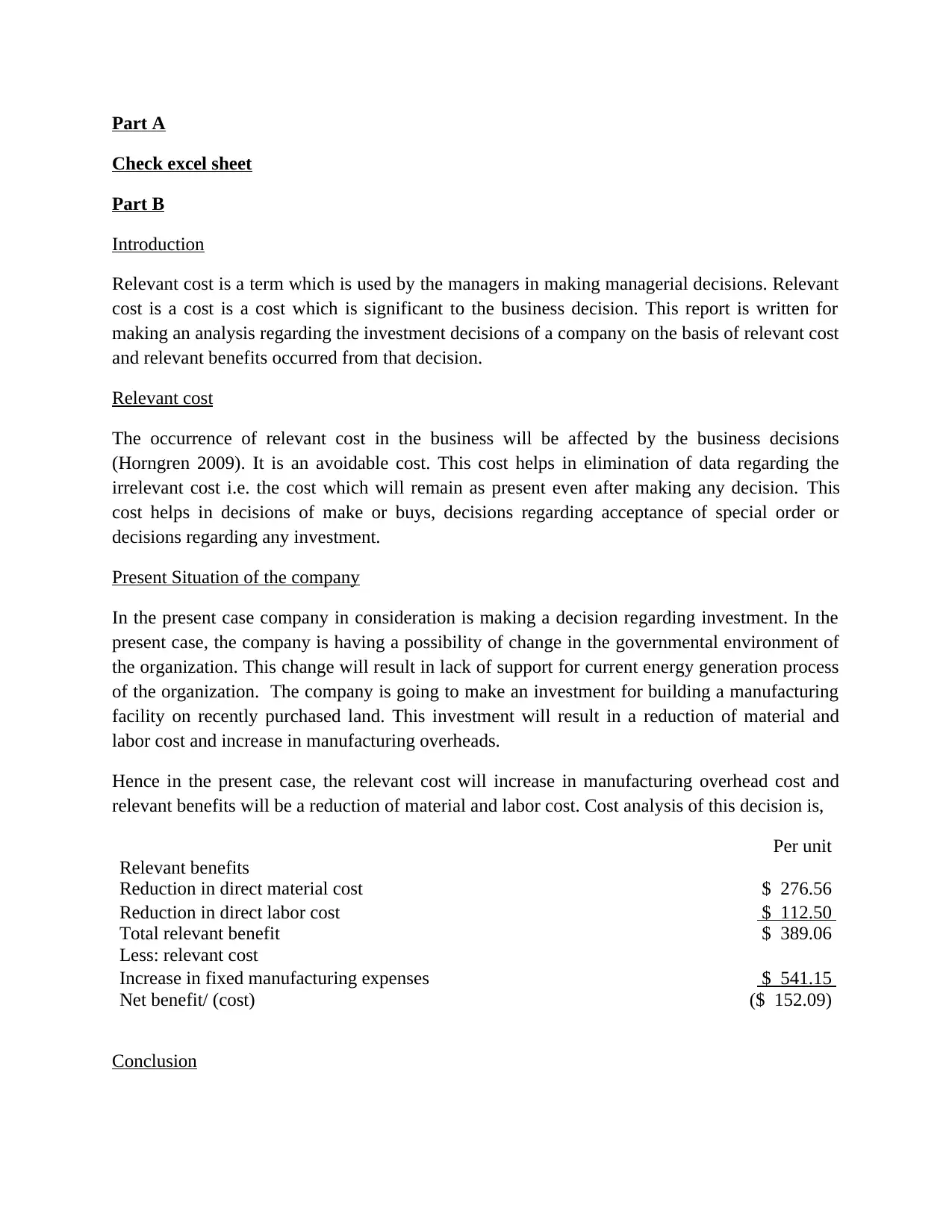

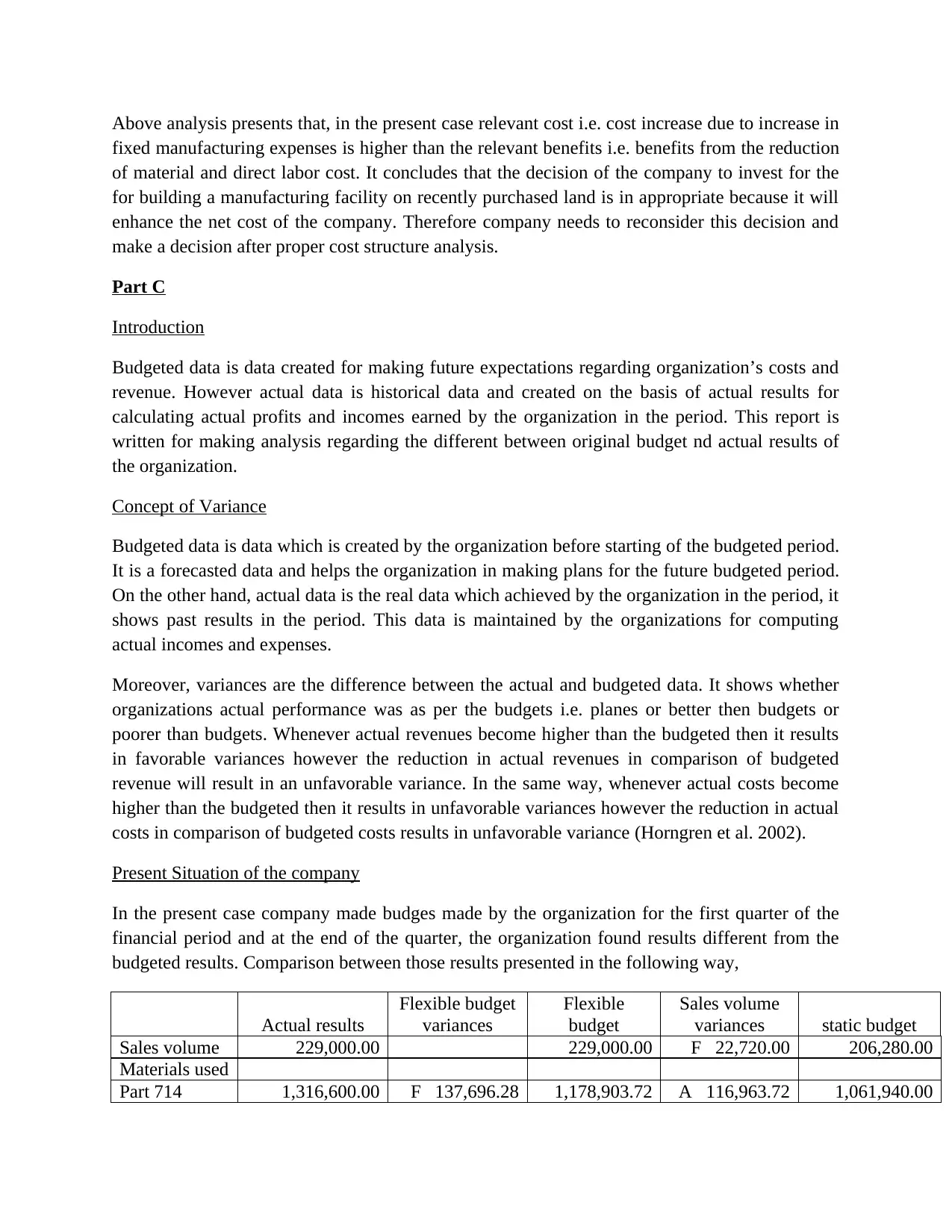

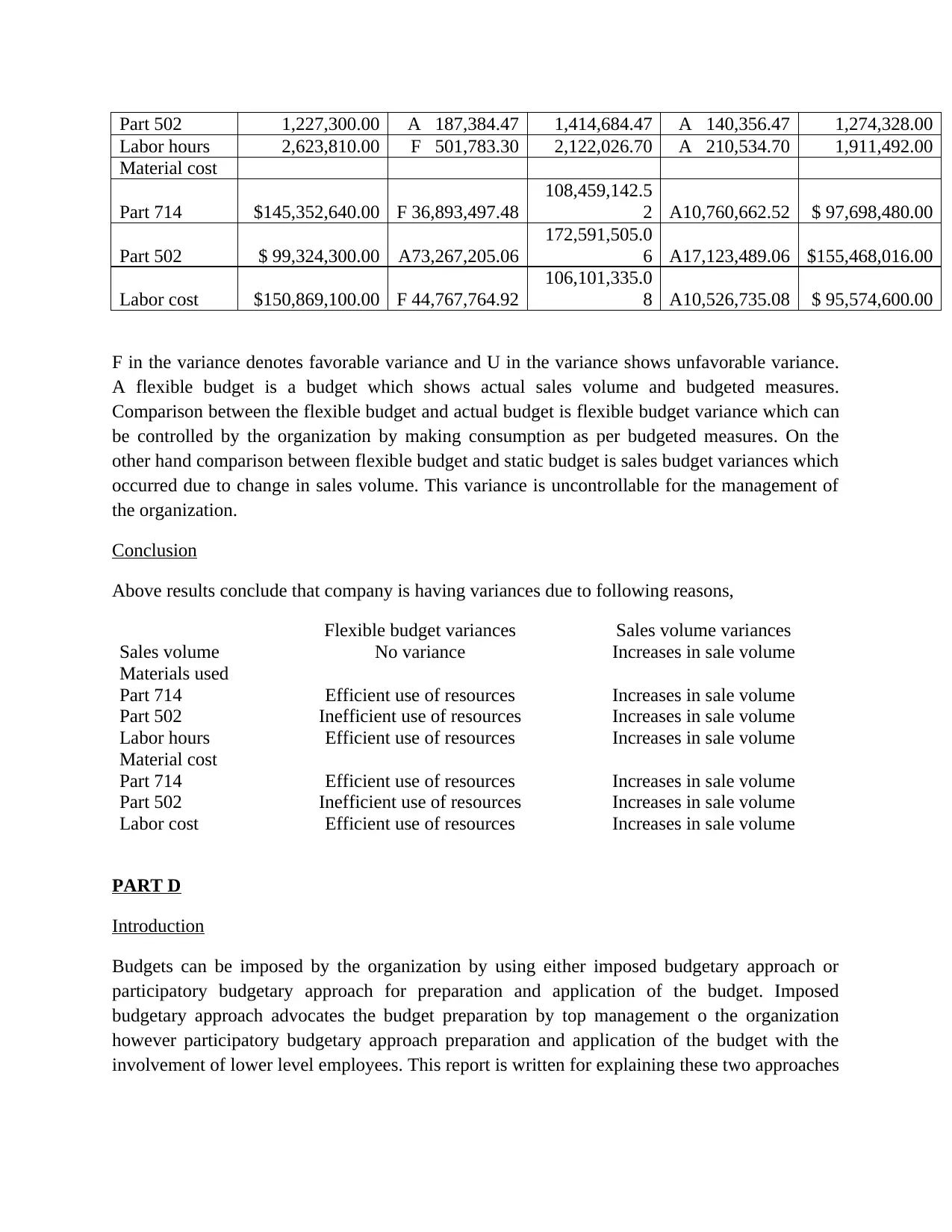

This report provides a comprehensive analysis of relevant cost, budgeting, and variance analysis within a financial context. Part A is an excel sheet, while Part B delves into relevant cost analysis, emphasizing its significance in managerial decision-making, particularly concerning investment choices. It examines a company's investment decision in light of changing governmental regulations, evaluating the relevant costs and benefits associated with building a new manufacturing facility. Part C focuses on budgeting, comparing budgeted data with actual results and analyzing variances. It explains the concepts of favorable and unfavorable variances, presenting a detailed comparison between flexible and static budgets. Part D explores the impact of imposed versus participatory budgeting approaches, illustrating how different budgetary methods influence employee behavior and organizational outcomes, specifically considering how Paulo Farmer would respond to each approach. The report concludes with a bibliography of supporting resources.

1 out of 5

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.