L&J Audit Plan: Reliable Printers Ltd (RPL) Accounts Payable - 2019

VerifiedAdded on 2023/01/05

|12

|2088

|53

Report

AI Summary

This report presents an audit plan for Reliable Printers Ltd (RPL), a printing company, for the year ended June 30, 2019. The plan, developed by a student, focuses specifically on the accounts payable section. It includes an overview of the audit team, consisting of a main auditor, junior auditors, and a tax specialist. The audit plan outlines the objectives, procedures, and assertions related to accounts payable, such as verifying completeness, accuracy, and relevance of financial information. The report details the audit scope, nature, and timing, including the duration allocated for specific tests of control. The report references the case study notes from the textbook and provides insights into the audit process. The plan ensures compliance with auditing standards and helps minimize audit costs. This report aims to help students understand the auditing process.

Running head: AUDITING

AUDITING

Name of the Student

Name of the University

Author Note

AUDITING

Name of the Student

Name of the University

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

AUDITING

Executive Summary

The report shows the auditing aspects upon company financial statement. Auditor has to

analysis the risk that is associated in organization business. The report is based upon

organization RPL which is a printing-based company, its show the audit plan which the

auditor has made in regards of financial report. It also states the scope and nature of audit

upon the company financial report.

AUDITING

Executive Summary

The report shows the auditing aspects upon company financial statement. Auditor has to

analysis the risk that is associated in organization business. The report is based upon

organization RPL which is a printing-based company, its show the audit plan which the

auditor has made in regards of financial report. It also states the scope and nature of audit

upon the company financial report.

2

AUDITING

Table of Contents

Introduction................................................................................................................................3

Audit Planning...........................................................................................................................3

Auditing Team...........................................................................................................................6

Audit Scope, Nature and Timing...............................................................................................7

Conclusion..................................................................................................................................9

Reference..................................................................................................................................10

AUDITING

Table of Contents

Introduction................................................................................................................................3

Audit Planning...........................................................................................................................3

Auditing Team...........................................................................................................................6

Audit Scope, Nature and Timing...............................................................................................7

Conclusion..................................................................................................................................9

Reference..................................................................................................................................10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

AUDITING

Introduction

Auditing is the inspection and examination of organization financial report to know

how the company is preparing its financial statement. Auditing process helps the users to

know in regards financial health of the organization (De Simone, Ege and Stomberg 2014).

Auditor has to carry many audit procedures in the company financial report to ascertain the

materiality in company accounts. Internal control should also be checked by the auditor that

shows how company is managing to reduce the business risk in the financial statement. The

reports show about the RPL as how the auditor has carried its audit process in the

organization financial report. It shows the audit plan which is made by the auditor related to

accounting payable of company financial statement. Auditing staff which is required by the

auditor to carry the audit process has also mentioned in the report.

Audit Planning

Audit Planning is the planning of the audit process which the auditor will carry upon

the company financial statement. These plans are made to ensure that all the essential points

have covered in the audit process. Auditor develops a proper strategy by preparing the audit

plan in the company business which helps it to carry all the process easily upon the company

financial reports. The scope, nature and time of audit is also mentioned in the audit plan.

Audit plan helps the auditor to follow all the required guidelines which are listed as per

auditing standard. It helps the auditor to get sufficient audit evidence from organization

financial report and also minimise the overall cost of audit.

The report shows the audit plan and procedure, which is created by an auditor in

regards to account payable of the company.

Audit

Objective

Audit Procedure Assertions Justification Impact on

Financial

AUDITING

Introduction

Auditing is the inspection and examination of organization financial report to know

how the company is preparing its financial statement. Auditing process helps the users to

know in regards financial health of the organization (De Simone, Ege and Stomberg 2014).

Auditor has to carry many audit procedures in the company financial report to ascertain the

materiality in company accounts. Internal control should also be checked by the auditor that

shows how company is managing to reduce the business risk in the financial statement. The

reports show about the RPL as how the auditor has carried its audit process in the

organization financial report. It shows the audit plan which is made by the auditor related to

accounting payable of company financial statement. Auditing staff which is required by the

auditor to carry the audit process has also mentioned in the report.

Audit Planning

Audit Planning is the planning of the audit process which the auditor will carry upon

the company financial statement. These plans are made to ensure that all the essential points

have covered in the audit process. Auditor develops a proper strategy by preparing the audit

plan in the company business which helps it to carry all the process easily upon the company

financial reports. The scope, nature and time of audit is also mentioned in the audit plan.

Audit plan helps the auditor to follow all the required guidelines which are listed as per

auditing standard. It helps the auditor to get sufficient audit evidence from organization

financial report and also minimise the overall cost of audit.

The report shows the audit plan and procedure, which is created by an auditor in

regards to account payable of the company.

Audit

Objective

Audit Procedure Assertions Justification Impact on

Financial

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

AUDITING

Statement

To verify

whether the

company has

given proper

disclosure or

not in their

financial

report

Auditor has to

analysis the

company

financial

information to

know how the

company can

provide

disclosure in the

financial

statement

(DeFond, and

Lennox 2017). It

can carry random

sampling which

will help the

auditor to

assertion the

materiality factor

in company

business and help

to know the risk

management

process carried by

Completeness –

Company should

record all the

information

correctly in their

financial report

(DeFond and

Zhang 2014). It

should verify all

the document to

know the

efficiency of

company in

carrying the

accounting

information in

their financial

statement.

The auditor will

able to ensure

that company

financial

statement is

showing true

and fair and no

materiality and

misstatement

are there in

company

business.

As if the

company has

materiality in

their financial

statement, then

it will provide

the wrong

information to

the company

financial user,

and as a result

they may take a

wrong idea

about the

company

financial health.

AUDITING

Statement

To verify

whether the

company has

given proper

disclosure or

not in their

financial

report

Auditor has to

analysis the

company

financial

information to

know how the

company can

provide

disclosure in the

financial

statement

(DeFond, and

Lennox 2017). It

can carry random

sampling which

will help the

auditor to

assertion the

materiality factor

in company

business and help

to know the risk

management

process carried by

Completeness –

Company should

record all the

information

correctly in their

financial report

(DeFond and

Zhang 2014). It

should verify all

the document to

know the

efficiency of

company in

carrying the

accounting

information in

their financial

statement.

The auditor will

able to ensure

that company

financial

statement is

showing true

and fair and no

materiality and

misstatement

are there in

company

business.

As if the

company has

materiality in

their financial

statement, then

it will provide

the wrong

information to

the company

financial user,

and as a result

they may take a

wrong idea

about the

company

financial health.

5

AUDITING

the company.

To check the

efficiency of

company in

regards to

the

preparation

of ledger

account of

accounts

payables.

Auditor has to

carry audit trail in

regards to

company

financial

statement

(Furnham and

Gunter 2015). As

it has to choose

and trace general

ledger entries and

able to know how

the company can

carry its business

operation. An

audit trail will

help the auditor to

understand any

control weakness

in company

accounting

system and the

proper area where

company can

Accuracy –

Company should

prepare each

ledger account

accurately, which

will help the

company to

provide useful

information in its

financial

statement.

This audit trail

will help the

auditor to

ascertain the

efficiency of

company

accounting

system and also

helps to know

the process in

which a

company can

improve its

management.

Ledger

accounts are the

base of

company

financial

information, so

if the company

accounting

system is

having any

weakness than

the overall

financial

statement will

not show an

accurate picture

of company

financial health.

AUDITING

the company.

To check the

efficiency of

company in

regards to

the

preparation

of ledger

account of

accounts

payables.

Auditor has to

carry audit trail in

regards to

company

financial

statement

(Furnham and

Gunter 2015). As

it has to choose

and trace general

ledger entries and

able to know how

the company can

carry its business

operation. An

audit trail will

help the auditor to

understand any

control weakness

in company

accounting

system and the

proper area where

company can

Accuracy –

Company should

prepare each

ledger account

accurately, which

will help the

company to

provide useful

information in its

financial

statement.

This audit trail

will help the

auditor to

ascertain the

efficiency of

company

accounting

system and also

helps to know

the process in

which a

company can

improve its

management.

Ledger

accounts are the

base of

company

financial

information, so

if the company

accounting

system is

having any

weakness than

the overall

financial

statement will

not show an

accurate picture

of company

financial health.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

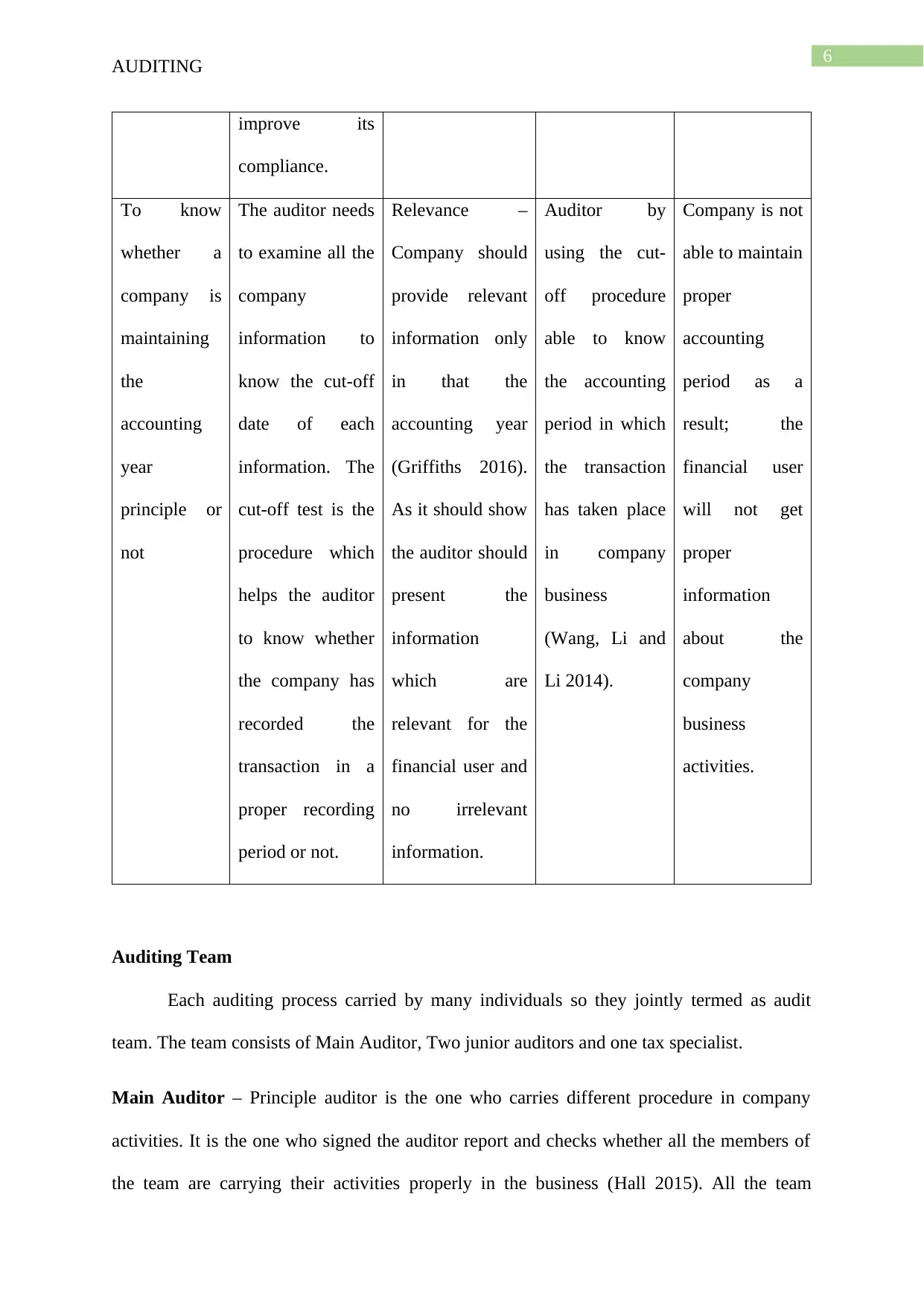

6

AUDITING

improve its

compliance.

To know

whether a

company is

maintaining

the

accounting

year

principle or

not

The auditor needs

to examine all the

company

information to

know the cut-off

date of each

information. The

cut-off test is the

procedure which

helps the auditor

to know whether

the company has

recorded the

transaction in a

proper recording

period or not.

Relevance –

Company should

provide relevant

information only

in that the

accounting year

(Griffiths 2016).

As it should show

the auditor should

present the

information

which are

relevant for the

financial user and

no irrelevant

information.

Auditor by

using the cut-

off procedure

able to know

the accounting

period in which

the transaction

has taken place

in company

business

(Wang, Li and

Li 2014).

Company is not

able to maintain

proper

accounting

period as a

result; the

financial user

will not get

proper

information

about the

company

business

activities.

Auditing Team

Each auditing process carried by many individuals so they jointly termed as audit

team. The team consists of Main Auditor, Two junior auditors and one tax specialist.

Main Auditor – Principle auditor is the one who carries different procedure in company

activities. It is the one who signed the auditor report and checks whether all the members of

the team are carrying their activities properly in the business (Hall 2015). All the team

AUDITING

improve its

compliance.

To know

whether a

company is

maintaining

the

accounting

year

principle or

not

The auditor needs

to examine all the

company

information to

know the cut-off

date of each

information. The

cut-off test is the

procedure which

helps the auditor

to know whether

the company has

recorded the

transaction in a

proper recording

period or not.

Relevance –

Company should

provide relevant

information only

in that the

accounting year

(Griffiths 2016).

As it should show

the auditor should

present the

information

which are

relevant for the

financial user and

no irrelevant

information.

Auditor by

using the cut-

off procedure

able to know

the accounting

period in which

the transaction

has taken place

in company

business

(Wang, Li and

Li 2014).

Company is not

able to maintain

proper

accounting

period as a

result; the

financial user

will not get

proper

information

about the

company

business

activities.

Auditing Team

Each auditing process carried by many individuals so they jointly termed as audit

team. The team consists of Main Auditor, Two junior auditors and one tax specialist.

Main Auditor – Principle auditor is the one who carries different procedure in company

activities. It is the one who signed the auditor report and checks whether all the members of

the team are carrying their activities properly in the business (Hall 2015). All the team

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

AUDITING

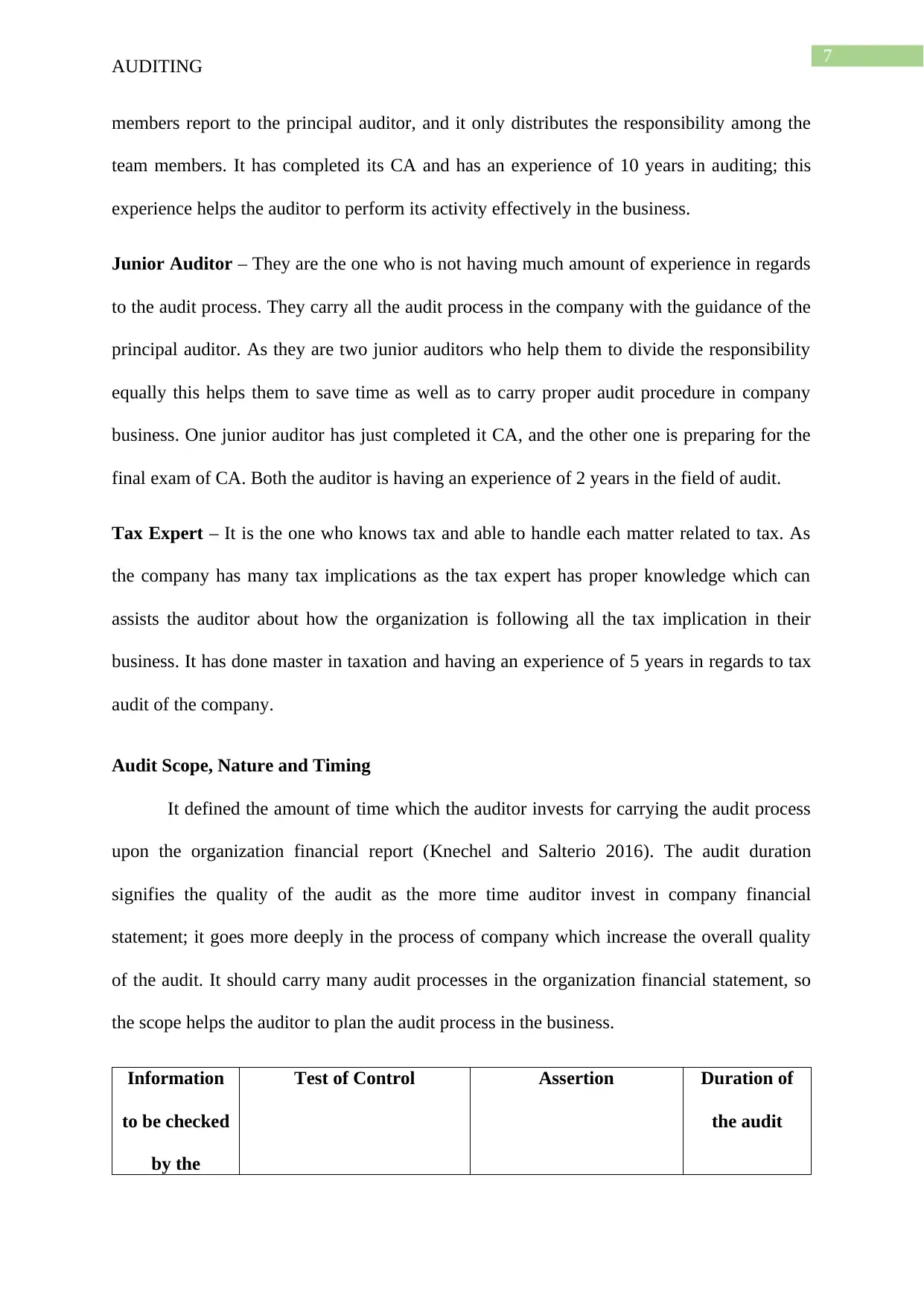

members report to the principal auditor, and it only distributes the responsibility among the

team members. It has completed its CA and has an experience of 10 years in auditing; this

experience helps the auditor to perform its activity effectively in the business.

Junior Auditor – They are the one who is not having much amount of experience in regards

to the audit process. They carry all the audit process in the company with the guidance of the

principal auditor. As they are two junior auditors who help them to divide the responsibility

equally this helps them to save time as well as to carry proper audit procedure in company

business. One junior auditor has just completed it CA, and the other one is preparing for the

final exam of CA. Both the auditor is having an experience of 2 years in the field of audit.

Tax Expert – It is the one who knows tax and able to handle each matter related to tax. As

the company has many tax implications as the tax expert has proper knowledge which can

assists the auditor about how the organization is following all the tax implication in their

business. It has done master in taxation and having an experience of 5 years in regards to tax

audit of the company.

Audit Scope, Nature and Timing

It defined the amount of time which the auditor invests for carrying the audit process

upon the organization financial report (Knechel and Salterio 2016). The audit duration

signifies the quality of the audit as the more time auditor invest in company financial

statement; it goes more deeply in the process of company which increase the overall quality

of the audit. It should carry many audit processes in the organization financial statement, so

the scope helps the auditor to plan the audit process in the business.

Information

to be checked

by the

Test of Control Assertion Duration of

the audit

AUDITING

members report to the principal auditor, and it only distributes the responsibility among the

team members. It has completed its CA and has an experience of 10 years in auditing; this

experience helps the auditor to perform its activity effectively in the business.

Junior Auditor – They are the one who is not having much amount of experience in regards

to the audit process. They carry all the audit process in the company with the guidance of the

principal auditor. As they are two junior auditors who help them to divide the responsibility

equally this helps them to save time as well as to carry proper audit procedure in company

business. One junior auditor has just completed it CA, and the other one is preparing for the

final exam of CA. Both the auditor is having an experience of 2 years in the field of audit.

Tax Expert – It is the one who knows tax and able to handle each matter related to tax. As

the company has many tax implications as the tax expert has proper knowledge which can

assists the auditor about how the organization is following all the tax implication in their

business. It has done master in taxation and having an experience of 5 years in regards to tax

audit of the company.

Audit Scope, Nature and Timing

It defined the amount of time which the auditor invests for carrying the audit process

upon the organization financial report (Knechel and Salterio 2016). The audit duration

signifies the quality of the audit as the more time auditor invest in company financial

statement; it goes more deeply in the process of company which increase the overall quality

of the audit. It should carry many audit processes in the organization financial statement, so

the scope helps the auditor to plan the audit process in the business.

Information

to be checked

by the

Test of Control Assertion Duration of

the audit

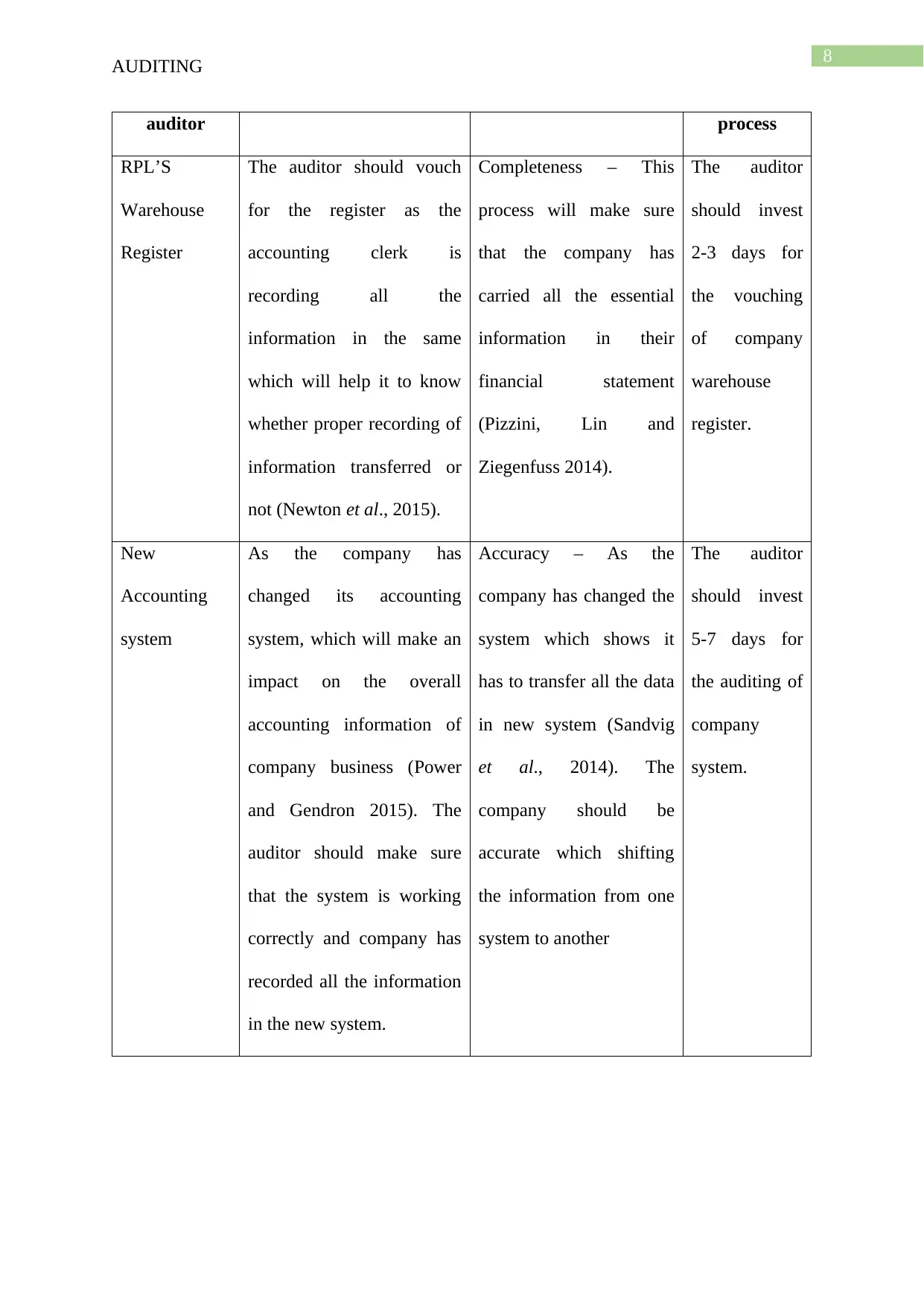

8

AUDITING

auditor process

RPL’S

Warehouse

Register

The auditor should vouch

for the register as the

accounting clerk is

recording all the

information in the same

which will help it to know

whether proper recording of

information transferred or

not (Newton et al., 2015).

Completeness – This

process will make sure

that the company has

carried all the essential

information in their

financial statement

(Pizzini, Lin and

Ziegenfuss 2014).

The auditor

should invest

2-3 days for

the vouching

of company

warehouse

register.

New

Accounting

system

As the company has

changed its accounting

system, which will make an

impact on the overall

accounting information of

company business (Power

and Gendron 2015). The

auditor should make sure

that the system is working

correctly and company has

recorded all the information

in the new system.

Accuracy – As the

company has changed the

system which shows it

has to transfer all the data

in new system (Sandvig

et al., 2014). The

company should be

accurate which shifting

the information from one

system to another

The auditor

should invest

5-7 days for

the auditing of

company

system.

AUDITING

auditor process

RPL’S

Warehouse

Register

The auditor should vouch

for the register as the

accounting clerk is

recording all the

information in the same

which will help it to know

whether proper recording of

information transferred or

not (Newton et al., 2015).

Completeness – This

process will make sure

that the company has

carried all the essential

information in their

financial statement

(Pizzini, Lin and

Ziegenfuss 2014).

The auditor

should invest

2-3 days for

the vouching

of company

warehouse

register.

New

Accounting

system

As the company has

changed its accounting

system, which will make an

impact on the overall

accounting information of

company business (Power

and Gendron 2015). The

auditor should make sure

that the system is working

correctly and company has

recorded all the information

in the new system.

Accuracy – As the

company has changed the

system which shows it

has to transfer all the data

in new system (Sandvig

et al., 2014). The

company should be

accurate which shifting

the information from one

system to another

The auditor

should invest

5-7 days for

the auditing of

company

system.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

AUDITING

Conclusion

On a final decision, the reports conclude as how the auditor carries the audit process

in company financial report. Auditor has to ascertain the materiality impact upon the

company financial reports. It has to verify all the document to know the amount of risk

associated in organization financial report. The report describes the company RPL which is a

printing company. It shows about the auditing plan as how the auditor plans its audit

procedure upon the organization financial report. The table shows different aspects of audit

plan and how the auditor carries its audit process in the company business. Lastly, the report

shows the scope of audit which is made by the auditor in regards to the organization.

AUDITING

Conclusion

On a final decision, the reports conclude as how the auditor carries the audit process

in company financial report. Auditor has to ascertain the materiality impact upon the

company financial reports. It has to verify all the document to know the amount of risk

associated in organization financial report. The report describes the company RPL which is a

printing company. It shows about the auditing plan as how the auditor plans its audit

procedure upon the organization financial report. The table shows different aspects of audit

plan and how the auditor carries its audit process in the company business. Lastly, the report

shows the scope of audit which is made by the auditor in regards to the organization.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

AUDITING

Reference

De Simone, L., Ege, M.S. and Stomberg, B., 2014. Internal control quality: The role of

auditor-provided tax services. The Accounting Review, 90(4), pp.1469-1496.

DeFond, M. and Zhang, J., 2014. A review of archival auditing research. Journal of

Accounting and Economics, 58(2-3), pp.275-326.

DeFond, M.L. and Lennox, C.S., 2017. Do PCAOB inspections improve the quality of

internal control audits?. Journal of Accounting Research, 55(3), pp.591-627.

Furnham, A. and Gunter, B., 2015. Corporate Assessment (Routledge Revivals): Auditing a

Company's Personality. Routledge.

Griffiths, P., 2016. Risk-based auditing. Routledge.

Hall, J.A., 2015. Information technology auditing. Cengage Learning.

Knechel, W.R. and Salterio, S.E., 2016. Auditing: Assurance and risk. Routledge.

Newton, N.J., Persellin, J.S., Wang, D. and Wilkins, M.S., 2015. Internal control opinion

shopping and audit market competition. The Accounting Review, 91(2), pp.603-623.

Pizzini, M., Lin, S. and Ziegenfuss, D.E., 2014. The impact of internal audit function quality

and contribution on audit delay. Auditing: A Journal of Practice & Theory, 34(1), pp.25-58.

Power, M.K. and Gendron, Y., 2015. Qualitative research in auditing: A methodological

roadmap. Auditing: A Journal of Practice & Theory, 34(2), pp.147-165.

Sandvig, C., Hamilton, K., Karahalios, K. and Langbort, C., 2014. Auditing algorithms:

Research methods for detecting discrimination on internet platforms. Data and

discrimination: converting critical concerns into productive inquiry, 22.

AUDITING

Reference

De Simone, L., Ege, M.S. and Stomberg, B., 2014. Internal control quality: The role of

auditor-provided tax services. The Accounting Review, 90(4), pp.1469-1496.

DeFond, M. and Zhang, J., 2014. A review of archival auditing research. Journal of

Accounting and Economics, 58(2-3), pp.275-326.

DeFond, M.L. and Lennox, C.S., 2017. Do PCAOB inspections improve the quality of

internal control audits?. Journal of Accounting Research, 55(3), pp.591-627.

Furnham, A. and Gunter, B., 2015. Corporate Assessment (Routledge Revivals): Auditing a

Company's Personality. Routledge.

Griffiths, P., 2016. Risk-based auditing. Routledge.

Hall, J.A., 2015. Information technology auditing. Cengage Learning.

Knechel, W.R. and Salterio, S.E., 2016. Auditing: Assurance and risk. Routledge.

Newton, N.J., Persellin, J.S., Wang, D. and Wilkins, M.S., 2015. Internal control opinion

shopping and audit market competition. The Accounting Review, 91(2), pp.603-623.

Pizzini, M., Lin, S. and Ziegenfuss, D.E., 2014. The impact of internal audit function quality

and contribution on audit delay. Auditing: A Journal of Practice & Theory, 34(1), pp.25-58.

Power, M.K. and Gendron, Y., 2015. Qualitative research in auditing: A methodological

roadmap. Auditing: A Journal of Practice & Theory, 34(2), pp.147-165.

Sandvig, C., Hamilton, K., Karahalios, K. and Langbort, C., 2014. Auditing algorithms:

Research methods for detecting discrimination on internet platforms. Data and

discrimination: converting critical concerns into productive inquiry, 22.

11

AUDITING

Wang, B., Li, B. and Li, H., 2014. Oruta: Privacy-preserving public auditing for shared data

in the cloud. IEEE transactions on cloud computing, 2(1), pp.43-56.

AUDITING

Wang, B., Li, B. and Li, H., 2014. Oruta: Privacy-preserving public auditing for shared data

in the cloud. IEEE transactions on cloud computing, 2(1), pp.43-56.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.